ne process industry productivity benchmark 2009 10 th march 2010

TRANSCRIPT

NE Process Industry Productivity Benchmark 2009

10th March 2010

Companies Involved

Benchmark Process

• Word Models

• Performance “Change” Since 2006

• Personal Interviews

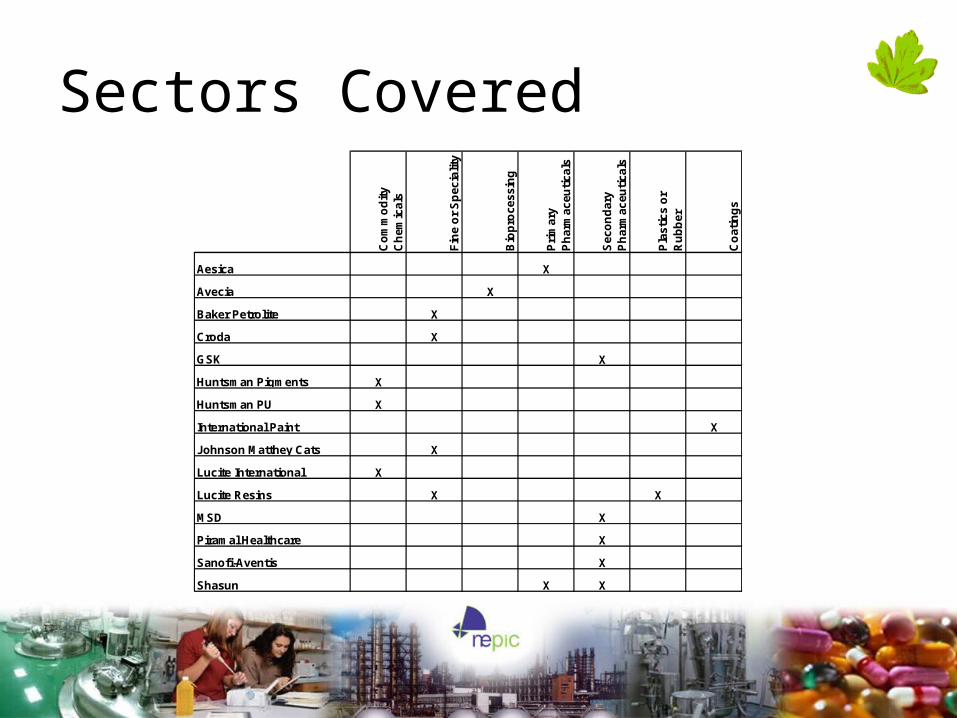

Sectors Covered

Co

mm

od

ity

Ch

emic

als

Fin

e o

r S

pec

ialit

y

Bio

pro

cess

ing

Pri

mar

y P

har

mac

euti

cals

Sec

on

dar

y P

har

mac

euti

cals

Pla

stic

s o

r R

ub

ber

Co

atin

gs

Aesica X

Avecia X

Baker Petrolite X

Croda X

GSK X

Huntsman Pigments X

Huntsman PU X

International Paint X

Johnson Matthey Cats X

Lucite International X

Lucite Resins X X

MSD X

Piramal Healthcare X

Sanofi-Aventis X

Shasun X X

Areas Investigated

• Unit Cost• Energy Cost• OEE• Quality Performance• Engineering

Productivity

• Safety Performance• OTIF• Stock Turns• Supplier OTIF

Orientation !

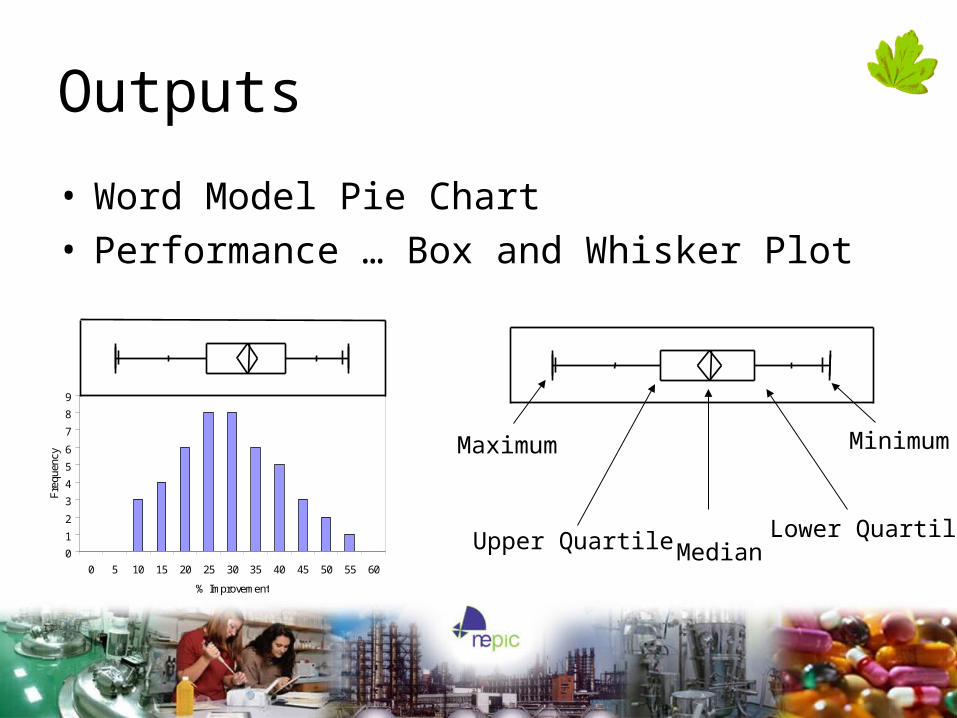

Outputs

• Word Model Pie Chart• Performance … Box and Whisker Plot

MedianUpper Quartile Lower Quartile

MinimumMaximum

0

1

2

3

4

5

6

7

8

9

0 5 10 15 20 25 30 35 40 45 50 55 60

% Improvement

Fre

quen

cy

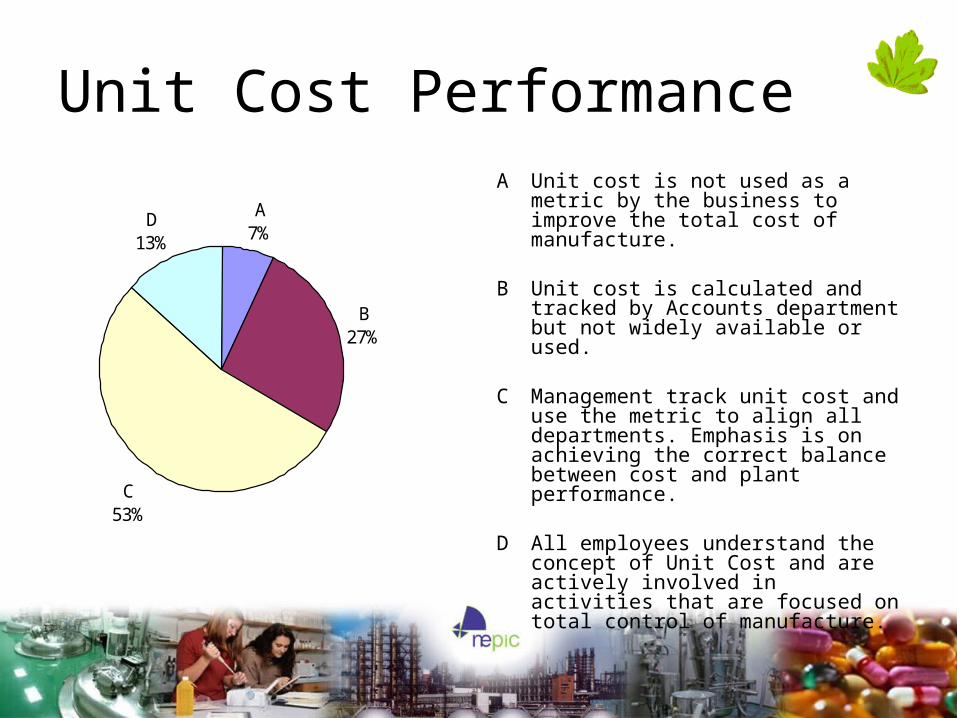

Unit Cost PerformanceA Unit cost is not used as a metric by the

business to improve the total cost of manufacture.

B Unit cost is calculated and tracked by Accounts department but not widely available or used.

C Management track unit cost and use the metric to align all departments. Emphasis is on achieving the correct balance between cost and plant performance.

D All employees understand the concept of Unit Cost and are actively involved in activities that are focused on total control of manufacture.

A7%

B27%

C53%

D13%

Unit Cost Performance

100.0% maximum 42.000

75.0% quartile 16.000

50.0% median 0.000

25.0% quartile 0.000

0.0% minimum 0.000

0123456789

10

0 5 10 15 20 25 30 35 40 45 50

% Improvement

Fre

qu

en

cy

Energy Cost PerformanceA The company has informal systems to

monitor energy usage. Ad hoc monitoring occurs usually in response to high / low values often flagged up by Accounts Group.

B The company actively manages its energy usages and takes steps to minimise losses at all levels of manufacture.

C The company can demonstrate an ‘Energy Balance’ approach to the use of energy with usages fully identified and measured.

D The company works both with Suppliers and Customers to reduce the overall environmental impact of the Supply Chain by optimising energy usage and recycling materials. Evidence of shop floor led teams leading energy reduction activities.

A7%

B46%

C40%

D7%

Energy Performance100.0% maximum 30.000

75.0% quartile 13.700

50.0% median 9.100

25.0% quartile 2.000

0.0% minimum 0.000

0

1

2

3

4

5

0 5 10 15 20 25 30 35

% Improvement

Fre

quen

cy

0

1

2

3

4

5

0 5 10 15 20 25 30 35

% Improvement

Fre

quen

cy

OEE PerformanceA There is limited formal monitoring of the key

plant performance against “Best Achieved”

B There is formal monitoring of the key plant performance metrics but the information is not widely circulated or briefed within the plant.

C The formal data is monitored and circulated within the plant and is used by management to identify opportunities to take the business forward in line with the business strategy.

D The data is generated and owned by the shop floor teams, displayed at their workstations and used by them to improve plant performance and eliminate defects in line with the business strategy.

A7%

B20%

C40%

D33%

OEE Performance

100.0% maximum 60.000

75.0% quartile 20.000

50.0% median 10.000

25.0% quartile 0.000

0.0% minimum 0.000

0

1

2

3

4

5

0 5 10 15 20 25 30 35 40 45 50 55 60

% Improvement

Fre

quen

cy

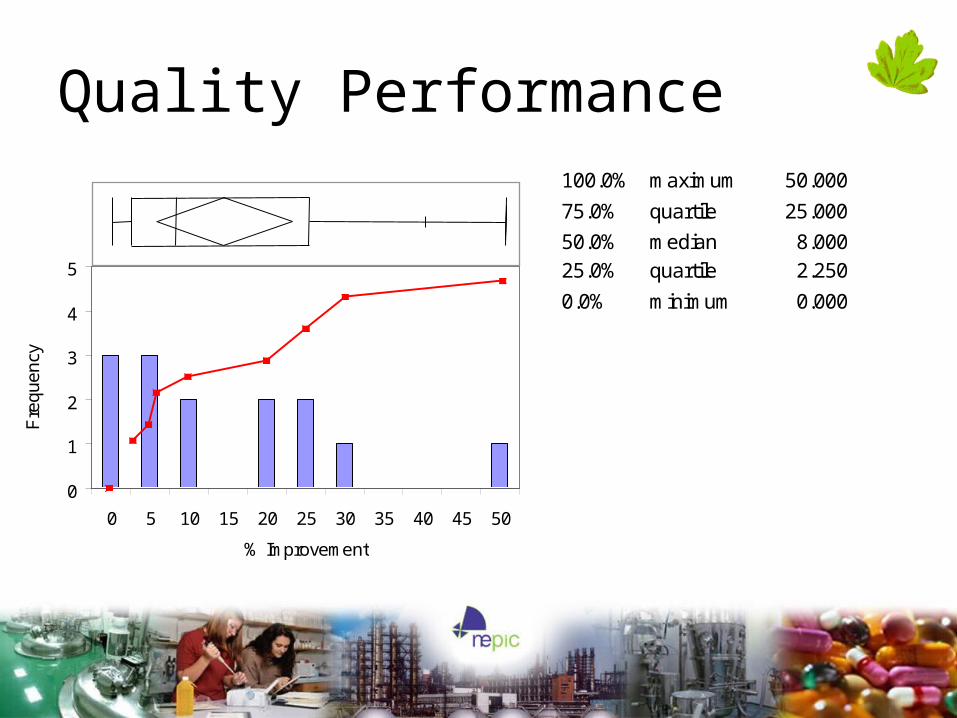

Quality PerformanceA No formal systems are used to monitor

supplied quality rate. Ad-hoc monitoring occurs usually in response to customer issues.

B There is a formal quality procedure is used for monitoring quality.

C A quality system with regular external auditing is used for capturing issues and uses internal management review and action plans.

D The business uses an appropriate quality system with regular external auditing as part of its business strategy. The operation uses appropriate tools with work groups capturing and using data and information to improve performance.

A0%

B7%

C33%

D60%

Quality Performance100.0% maximum 50.000

75.0% quartile 25.000

50.0% median 8.000

25.0% quartile 2.250

0.0% minimum 0.000

0

1

2

3

4

5

0 5 10 15 20 25 30 35 40 45 50

% Improvement

Fre

quen

cy

Safety Performance 2009/2008

0

1

2

3

4

5

6

0 1 2 3 4 5 6 7

Reportable Injuries 2008 + 2009

Fre

qu

en

cy

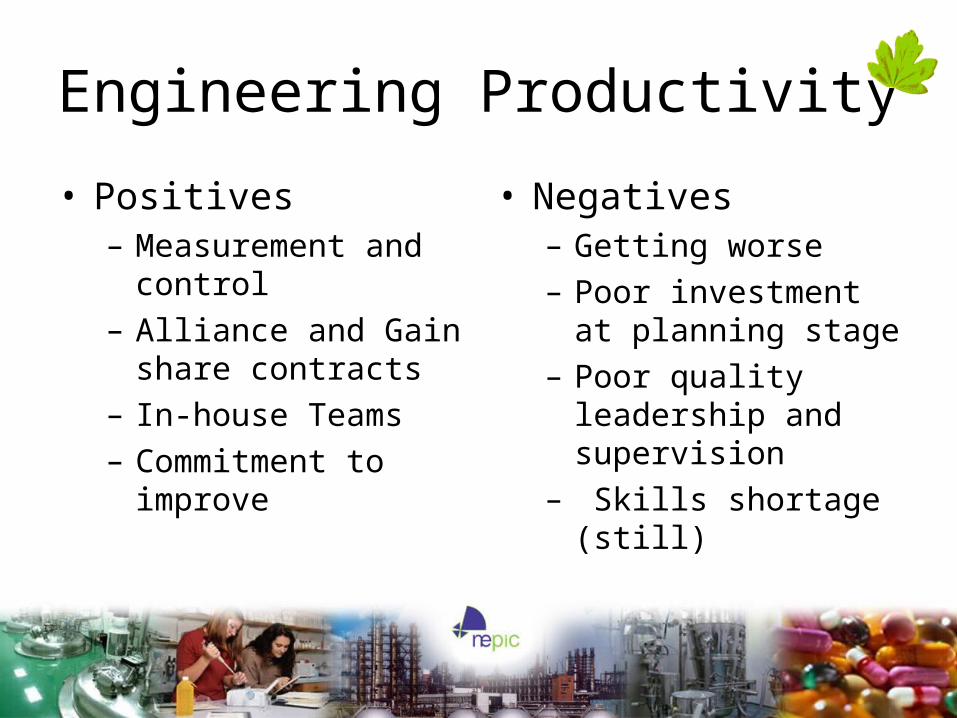

Engineering Productivity

• Positives– Measurement and

control– Alliance and Gain

share contracts– In-house Teams– Commitment to

improve

• Negatives– Getting worse– Poor investment at

planning stage– Poor quality leadership

and supervision– Skills shortage (still)

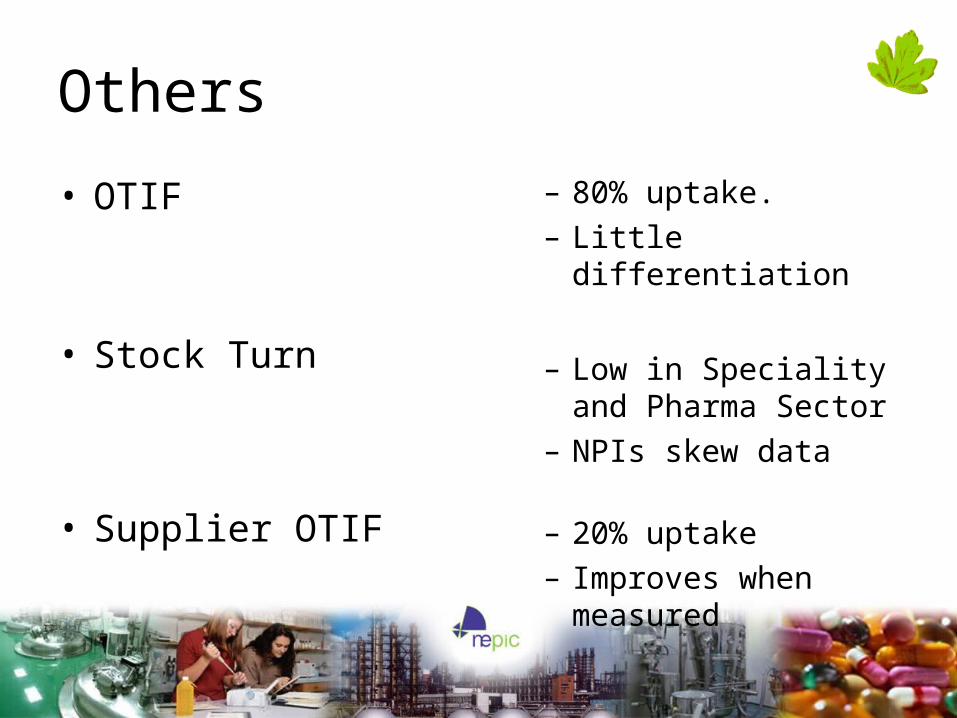

Others

• OTIF

• Stock Turn

• Supplier OTIF

– 80% uptake. – Little differentiation

– Low in Speciality and Pharma Sector

– NPIs skew data

– 20% uptake– Improves when

measured

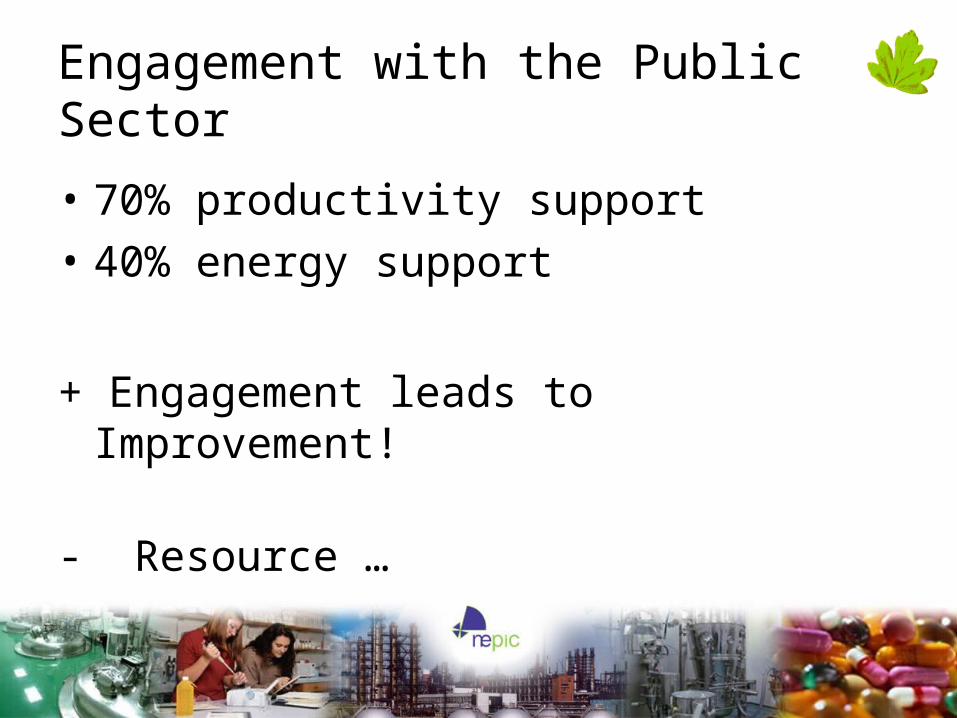

Engagement with the Public Sector

• 70% productivity support

• 40% energy support

+ Engagement leads to Improvement!

- Resource …

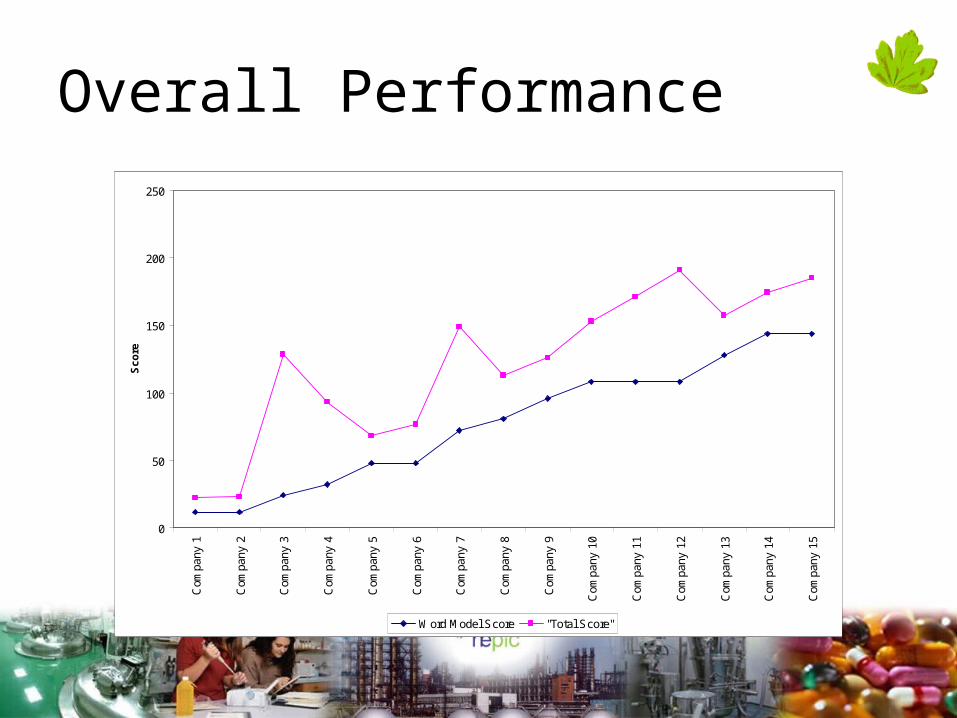

Overall Performance

0

50

100

150

200

250C

ompa

ny 1

Com

pany

2

Com

pany

3

Com

pany

4

Com

pany

5

Com

pany

6

Com

pany

7

Com

pany

8

Com

pany

9

Com

pany

10

Com

pany

11

Com

pany

12

Com

pany

13

Com

pany

14

Com

pany

15

Sc

ore

Word Model Score

Overall Performance

0

50

100

150

200

250C

ompa

ny 1

Com

pany

2

Com

pany

3

Com

pany

4

Com

pany

5

Com

pany

6

Com

pany

7

Com

pany

8

Com

pany

9

Com

pany

10

Com

pany

11

Com

pany

12

Com

pany

13

Com

pany

14

Com

pany

15

Sc

ore

Word Model Score "Total Score"

Conclusions - Strengths• Technical competence

• Tough cost control

• Improvement orientation

• Resource Management

• Uptake of NEPA and ERE support

• Technical competence

• Tough cost control

• Improvement orientation

• Resource Management

• Uptake of NEPA and ERE support

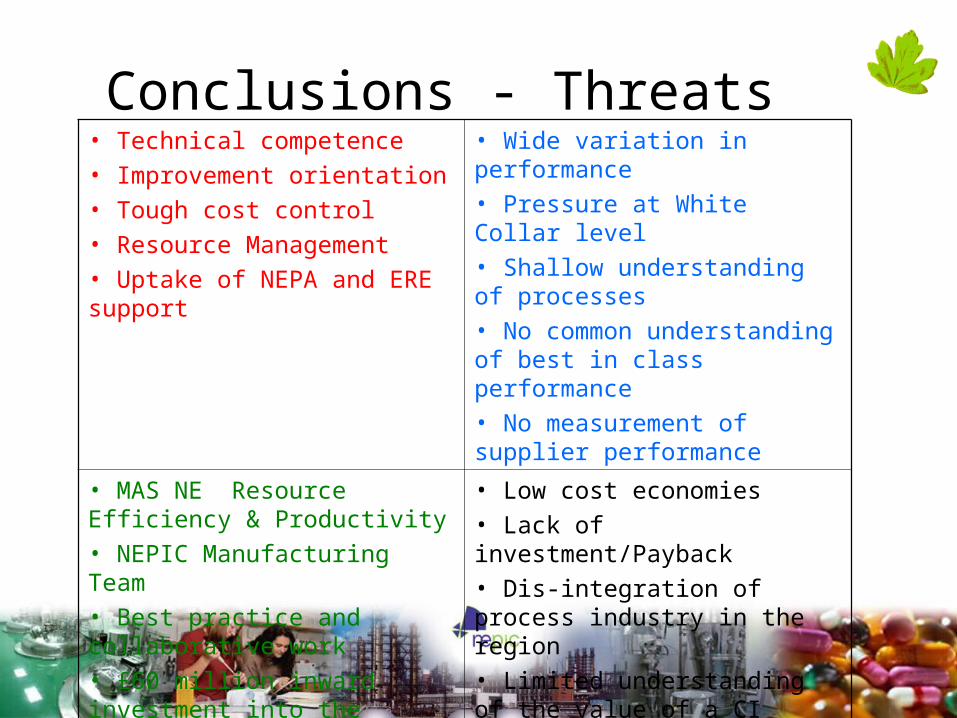

• Wide variation in performance

• Pressure at White Collar level

• Shallow understanding of processes

• No common understanding of best in class performance

• No measurement of supplier performance

Conclusions - Weakness

• Technical competence

• Tough cost control

• Improvement orientation

• Resource Management

• Uptake of NEPA and ERE support

• Wide variation in performance

• Pressure at White Collar level

• Shallow understanding of processes

•No common understanding of best in class performance

• No measurement of supplier performance

• MAS NE Resource Efficiency & Productivity

• NEPIC Manufacturing Team

• Best practice and collaborative work

• £60 million inward investment into the region

Conclusions - Opportunities

• Technical competence

• Improvement orientation

• Tough cost control

• Resource Management

• Uptake of NEPA and ERE support

• Wide variation in performance

• Pressure at White Collar level

• Shallow understanding of processes

• No common understanding of best in class performance

• No measurement of supplier performance

• MAS NE Resource Efficiency & Productivity

• NEPIC Manufacturing Team

• Best practice and collaborative work

• £60 million inward investment into the region

• Low cost economies

• Lack of investment/Payback

• Dis-integration of process industry in the region

• Limited understanding of the value of a CI culture

Conclusions - Threats

Next Steps

• Workshops …