ndix departmental accounting e app - · pdf filedepartmental accounting ... on some equitable...

TRANSCRIPT

After you have completed this appendix, you will be able to do the following:

E-1

Departmental Accounting

Learning Objectives

1 Compile a departmental income statement. 2 Understand departmental margin.

AppE

nd

ix E

Apportionment of expenses (p. E-2)

departmental margin (p. E-4)

direct expenses (p. E-4)

indirect expenses (p. E-4)

Accounting Language

A company that is involved in several different business activities should be divided into a number of subdivisions or departments. This enables the company’s management to delegate authority to departmental managers, who are responsible for their respective departments, and to measure the profitability of each department. It is the element of profitability that we discuss in this appendix.

GROSS pROFiT BY dEpARTMEnTSA department’s gross profit depends on its sales volume and its markup on the goods sold:

Net Sales 2 Cost of Goods Sold 5 Gross Profit

To determine the gross profit of a given department, you need a separate set of figures for the department for each element entering into the gross profit. Use one of two ways to obtain these figures:

1. Keep separate general ledger accounts for each item affecting gross profit, such as a Sales account for each department and a Sales Returns and Allowances account for each department. Then, record the balances of these accounts on the income statement.

2. Keep only one general ledger account for each item affecting gross profit and apportion the balance to the various departments. For example, maintain one Sales account and one Sales Returns and Allowances account for the company and keep a breakdown of sales and sales returns for each department. Then, record the figures for each department on the income statement.

Keeping Separate Accounts by DepartmentKeeping separate accounts by department yields the most accurate accounting data. You need separate accounts for each department for Sales, Sales Returns and Allowances, Sales Discounts, Purchases, Purchases Returns and Allowances, Purchases Discounts, Freight In, and Merchandise Inventory. For example, Boag Hardware has five departments and uses five Sales accounts, five Sales Returns and Allowances accounts, five Sales Discounts accounts, five Merchandise Inventory accounts, and so on. The accountant posts each total to a separate account as indicated by the ledger account numbers.

Maintaining One General Ledger AccountWhen a company keeps only one general ledger account for each item involved in gross profit, the accountant must distribute the total amount among the various departments

Computerized systems are well suited to departmental accounting.

FYI

CHE-NOBLES-11-0409-Appendix E.indd 1 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental AccountingE-2

at the end of the accounting period. To do so, the accountant accumulates departmental information on supplementary records. Sales, sales returns, purchases, purchases returns and allowances, purchases discounts, and so on, are recorded in a journal and are recorded on a departmental analysis sheet. At the end of the accounting period, these analysis sheets give departmental breakdowns for each item.

Preparing a Departmental Income StatementJoyce Company has two departments, A and B, and keeps separate accounts for each. The company keeps separate accounts for each item that enters into gross profit and apportions the operating expenses between Gross Profit and Income from Operations to Department A or Department B on a logical basis.

An outline of this process is as follows:

From Sales Through Income from OperationsDepartmentalized

Revenue from SalesLess Cost of Goods Sold

Gross ProfitLess Selling ExpensesLess General Expenses

Income from OperationsNondepartmentalizedAdd Other IncomeLess Other Expenses

Net Income

Joyce Company income statement for the fiscal year ended December 31 appears in Figure 1 on pages E-4–E-5.

Gross ProfitBecause each department keeps separate accounts for gross profit items, such as sales and cost of goods sold, these items are reported separately on the income statements.

Apportionment of Operating ExpensesJoyce Company combines operating expenses such as Advertising Expense and Utilities Expense. Therefore, each department must assume its share of overhead expenses. Apportionment of expenses is a crucial element of departmental accounting. It consists of allocating operating expenses among operating departments. You can readily identify some operating expenses as belonging to a given department. For example, if a salesperson makes sales in only one department, the accountant assigns that salesperson’s salary or commission directly to that department. However, other operating expenses, such as Utilities Expense, cannot be restricted to one department and must be divided on some equitable basis. Let’s look at the operating expenses of Joyce Company and see how they are apportioned.

Separate departmental accounts or supplementary analysis sheets

Account balances are apportioned

Learning O

bjective

1 Compile a departmental income statement.

CHE-NOBLES-11-0409-Appendix E.indd 2 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental Accounting E-3

SALeS SALArY expenSeJoyce Company allocates the salespersons’ salaries to Department A or Department B according to the payroll register, which lists each employee by department. Department A’s share is $88,625; Department B’s share is $52,200.

AdvertISIng expenSeJoyce Company advertises only on the radio and allocates the cost of radio advertising to the two departments according to the amount of air time each department uses. In a year, Joyce Company buys 1,250 minutes of radio time, divided according to departments as shown here:

Advertising for Dept. A: 675 minutes or 6755 54%

1,250

Advertising for Dept. B: 575 minutes or 5755 46%

1,250

Dept. A’s share of cost of radio advertising: 54% of $17,600 5 $9,504

Dept. B’s share of cost of radio advertising: 46% of $17,600 5 $8,096

deprecIAtIOn expenSe, StOre equIpmentJoyce Company keeps a property and equipment ledger that notes the department in which each piece of equipment is located. The total year’s depreciation of the equipment used in Department A is $1,840; the total year’s depreciation of the equipment used in Department B is $1,460.

rent expenSe And utILItIeS expenSeJoyce Company rents 40,000 square feet of floor space and allocates the expenses of rent and utilities on the basis of floor space occupied by each department as follows. (Yearly expense for rent is $16,400; yearly expense for utilities is $4,840.)

Dept. A occupies 25,000 square feet or 25,0005 62.5%

40,000

Dept. B occupies 15,000 square feet or 15,0005 37.5%

40,000

Dept. A’s share of rent: 62.5% of $16,400 = $10,250

Dept. B’s share of rent: 37.5% of $16,400 = $6,150

Dept. A’s share of utilities: 62.5% of $4,840 = $3,025

Dept. B’s share of utilities: 37.5% of $4,840 = $1,815

Nonapportioned ExpensesOther Income and Expense Items, such as Interest Income and Interest Expense, are not apportioned among the departments. Instead, these items are only included in total on the income statement.

To apportion or to allocate means to divide up.

remember

CHE-NOBLES-11-0409-Appendix E.indd 3 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental AccountingE-4

dEpARTMEnTAL MARGindepartmental margin is a measurement of the contribution that a given department makes to the income of the firm—gross profit of a department minus the department’s direct expenses. When a company breaks down its expense figures on a departmental-margin basis, its income statement indicates the contribution that each department makes toward the overhead expenses incurred on behalf of the business as a whole. You can divide operating expenses into two classes: (1) direct expenses, which are incurred for the sole benefit of a given department and are under the control of the department head but not necessarily under the department being considered, and (2) indirect expenses,

Figure 1Income statement for Joyce Company

Joyce Company Income Statement

For Year Ended December 31, 20—

Department A Department B Total

Revenue from Sales:

Sales $560,000 $240,000 $800,000

Less: Sales Returns and Allowances 14,200 $545,800 5,800 $234,200 20,000 $780,000

Net Sales

Cost of Goods Sold:

Merchandise Inventory, Jan. 1, 20— $ 96,400 $ 82,740 $179,140

Purchases $ 312,115 $161,175 $473,290

Less: Purchases Returns and Allowances 9,580 4,756 14,336

Purchases Discounts 5,740 3,274 9,014

Net Purchases $296,795 $153,145 $449,940

Add Freight In 13,005 6,715 19,720

Delivered Cost of Purchases 309,800 159,860 469,660

Cost of Goods Available for Sale $406,200 $242,600 $648,800

Less Merchandise Inventory, Dec. 31, 20–– 110,000 90,000 200,000

Cost of Goods Sold 296,200 152,600 448,800

Gross Profit $249,600 $ 81,600 $331,200

Operating Expenses:

Selling Expenses:

Sales Salary Expense $ 88,625 $ 52,200 $140,825

Advertising Expense 9,504 8,096 17,600

Depreciation Expense, Store Equipment 1,840 1,460 3,300

Total Selling Expenses $ 99,969 $ 61,756 $161,725

General Expenses:

Rent Expense $ 10,250 $ 6,150 $ 16,400

Utilities Expense 3,025 1,815 4,840

Total General Expenses 13,275 7,965 21,240

Total Operating Expenses 113,244 69,721 182,965

Income from Operations $136,356 $ 11,879 $148,235

Other Income:

Interest Income $ 3,624

Other Expenses:

Interest Expense 2,400 1,224

Net Income $149,459

Learning O

bjective

2 Understand departmental margin.

CHE-NOBLES-11-0409-Appendix E.indd 4 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental Accounting E-5

which are incurred as overhead expenses of the entire business and thus are not under the control of one department head. For example, Sales Salary Expense is a direct expense because it is incurred purely for the benefit of one department. Officers’ Salary Expense, on the other hand, is an overhead expense incurred for the business as a whole; it is not directly chargeable to one department.

Some operating expenses may be partially direct and partially indirect. For example, suppose Rivera Company has five departments. Rivera Company’s Advertising Expense consisted partially of billboard advertising, which stresses the name and location of the company, and partially of newspaper and radio advertising, which directly benefits separate departments of the company. So the part of the advertising budget that went to billboard advertising is an indirect expense, and the part that went to newspaper and

Joyce Company Income Statement

For Year Ended December 31, 20—

Department A Department B Total

Revenue from Sales:

Sales $560,000 $240,000 $800,000

Less: Sales Returns and Allowances 14,200 $545,800 5,800 $234,200 20,000 $780,000

Net Sales

Cost of Goods Sold:

Merchandise Inventory, Jan. 1, 20— $ 96,400 $ 82,740 $179,140

Purchases $ 312,115 $161,175 $473,290

Less: Purchases Returns and Allowances 9,580 4,756 14,336

Purchases Discounts 5,740 3,274 9,014

Net Purchases $296,795 $153,145 $449,940

Add Freight In 13,005 6,715 19,720

Delivered Cost of Purchases 309,800 159,860 469,660

Cost of Goods Available for Sale $406,200 $242,600 $648,800

Less Merchandise Inventory, Dec. 31, 20–– 110,000 90,000 200,000

Cost of Goods Sold 296,200 152,600 448,800

Gross Profit $249,600 $ 81,600 $331,200

Operating Expenses:

Selling Expenses:

Sales Salary Expense $ 88,625 $ 52,200 $140,825

Advertising Expense 9,504 8,096 17,600

Depreciation Expense, Store Equipment 1,840 1,460 3,300

Total Selling Expenses $ 99,969 $ 61,756 $161,725

General Expenses:

Rent Expense $ 10,250 $ 6,150 $ 16,400

Utilities Expense 3,025 1,815 4,840

Total General Expenses 13,275 7,965 21,240

Total Operating Expenses 113,244 69,721 182,965

Income from Operations $136,356 $ 11,879 $148,235

Other Income:

Interest Income $ 3,624

Other Expenses:

Interest Expense 2,400 1,224

Net Income $149,459

CHE-NOBLES-11-0409-Appendix E.indd 5 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental AccountingE-6

radio advertising is a direct expense. When you classify an expense as direct or indirect, use this rule of thumb to identify direct expenses: The expense would not have been incurred if the department were not in existence. The expense must be directly related to the department.

Here is an outline of an income statement that emphasizes departmental margin.

From Sales Through Departmental Margin

Revenue from Sales Less Cost of Goods Sold

Based on separate departmental accounts or supplementary analysis sheets

Expenses that are directly related to the department

Gross Profit Less Direct Departmental Expenses

Departmental Margin Less Indirect Expenses

Income from Operations Add Other Income Less Other Expenses

Net Income

The Meaning of Departmental MarginDepartmental margin is the most realistic portrayal of the profitability of a department. If the company closes the department, the company’s income before income taxes will decrease or increase by the amount of the departmental margin. For example, assume that Rivera Company’s income from operations for last year was $120,000, which is about the same as it has been for the past four years. Rivera’s partial income statement, in which all operating expenses are apportioned to the various departments, shows that Department E has a loss from operations of $9,000. In an abbreviated departmental-margin format, the results of the fiscal year are shown in the following table:

ItemDepartment E

(only)

Departments A to D

(only)

Total, Departments A

to E

Total, Departments

A to D (with E eliminated)

SalesCost of Goods SoldGross ProfitDirect Departmental ExpensesDepartmental MarginIndirect ExpensesIncome (Loss) from Operations

$ 120,000 72,000 $ 48,000 32,000 $ 16,000 25,000 $ (9,000)

$ 1,480,000 880,000 $ 600,000 336,000 $ 264,000 135,000 $ 129,000

$ 1,600,000 952,000 $ 648,000 368,000 $ 280,000 160,000 $ 120,000

$ 1,480,000 880,000 $ 600,000 336,000 $ 264,000 160,000 $ 104,000

Now suppose Rivera Company eliminates Department E. Because Department E’s departmental margin amounts to $16,000, the Income from Operations of the entire firm will decrease by $16,000 ($120,000 2 $104,000). Another factor Rivera Company has to consider is possible “spillover sales” of Department E; that is, customers of Department E may buy things in other departments. Also, any change in income will cause a change in the amount of income taxes paid by Rivera Company. However, to simplify our analysis, we have omitted income taxes from our discussion.

CHE-NOBLES-11-0409-Appendix E.indd 6 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental Accounting E-7

The Usefulness of Departmental MarginIncome statements that show departmental margin are extremely useful when it comes to controlling a company’s direct expenses because the company can hold the head of a given department accountable for expenses directly chargeable to that department. If a department head reduces direct expenses, this action will have a favorable effect on the departmental margin.

A company that manufactures a number of different products can also use the concept of departmental margin to determine the profitability of a particular product. This is clearly one of the most important uses of departmental margin.

Management can use an income statement showing departmental margin as a tool for making future plans and for analyzing future operations. Sometimes such an income statement may even lead to the elimination of a department.

GlossaryApportionment of expenses Allocating operating

expenses among operating departments. (p. E-2)

departmental margin The contribution that a given department makes to the income of the firm—gross profit of a department minus the department’s direct expenses. (p. E-4)

direct expenses Expenses that benefit only one department and are controlled by the head of the department. (p. E-4)

Indirect expenses Overhead expenses that benefit several departments or the business as a whole and are not under the control of any one department head. (p. E-4)

Problems

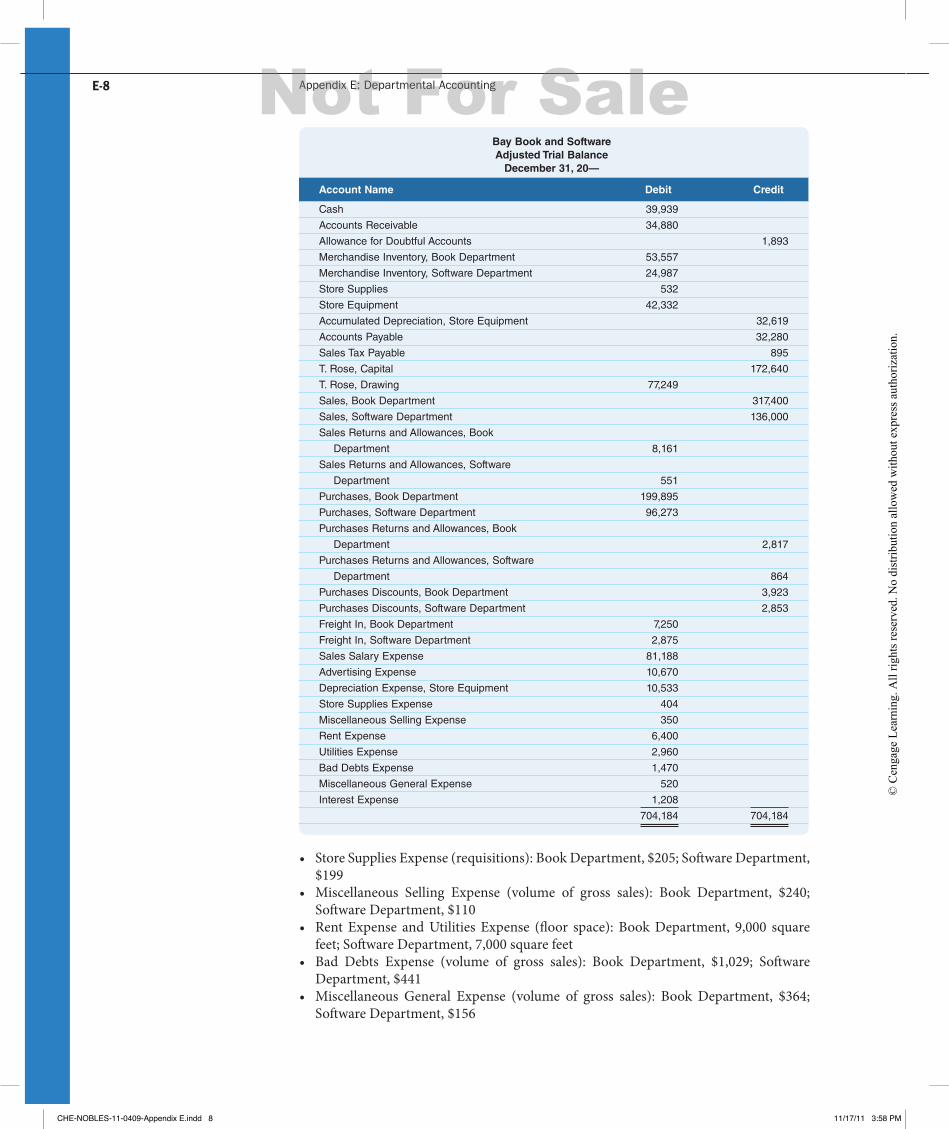

prOBLem e-1 Bay Book and Software has two sales departments: Book and Software. After recording and posting all adjustments, including the adjustments for merchandise inventory, the accountant prepared the adjusted trial balance (shown on the next page) at the end of the fiscal year.

Merchandise inventories at the beginning of the year were as follows: Book Department, $53,410; Software Department, $23,839. The bases (and sources of figures) for apportioning expenses to the two departments are as follows (rounded to the nearest dollar):

• Sales Salary Expense (payroll register): Book Department, $45,559; Software Department, $35,629

• Advertising Expense (newspaper column inches): Book Department, 550 inches; Software Department, 450 inches

• Depreciation Expense, Store Equipment (property and equipment ledger): Book Department, $7,851; Software Department, $2,682

1LO

Direct expenses are expenses incurred for the sole benefit of a department. If the department did not exist, the expense would not have been incurred.

remember

CHE-NOBLES-11-0409-Appendix E.indd 7 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental AccountingE-8

• Store Supplies Expense (requisitions): Book Department, $205; Software Department, $199

• Miscellaneous Selling Expense (volume of gross sales): Book Department, $240; Software Department, $110

• Rent Expense and Utilities Expense (floor space): Book Department, 9,000 square feet; Software Department, 7,000 square feet

• Bad Debts Expense (volume of gross sales): Book Department, $1,029; Software Department, $441

• Miscellaneous General Expense (volume of gross sales): Book Department, $364; Software Department, $156

Bay Book and Software Adjusted Trial Balance

December 31, 20—

Account Name Debit Credit

Cash 39,939

Accounts Receivable 34,880

Allowance for Doubtful Accounts 1,893

Merchandise Inventory, Book Department 53,557

Merchandise Inventory, Software Department 24,987

Store Supplies 532

Store Equipment 42,332

Accumulated Depreciation, Store Equipment 32,619

Accounts Payable 32,280

Sales Tax Payable 895

T. Rose, Capital 172,640

T. Rose, Drawing 77,249

Sales, Book Department 317,400

Sales, Software Department 136,000

Sales Returns and Allowances, Book

Department 8,161

Sales Returns and Allowances, Software

Department 551

Purchases, Book Department 199,895

Purchases, Software Department 96,273

Purchases Returns and Allowances, Book

Department 2,817

Purchases Returns and Allowances, Software

Department 864

Purchases Discounts, Book Department 3,923

Purchases Discounts, Software Department 2,853

Freight In, Book Department 7,250

Freight In, Software Department 2,875

Sales Salary Expense 81,188

Advertising Expense 10,670

Depreciation Expense, Store Equipment 10,533

Store Supplies Expense 404

Miscellaneous Selling Expense 350

Rent Expense 6,400

Utilities Expense 2,960

Bad Debts Expense 1,470

Miscellaneous General Expense 520

Interest Expense 1,208

704,184 704,184

CHE-NOBLES-11-0409-Appendix E.indd 8 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental Accounting E-9

requiredPrepare an income statement by department to show income from operations, as well as a nondepartmentalized income statement (using the Total columns) to show net income for the entire company.

prOBLem e-2 La Hacienda Company has two departments: Furniture and Lighting. La Hacienda’s accountant prepares an adjusted trial balance (shown below) at the end of the fiscal year.

check FigureNet Income, $34,444

1LO

La Hacienda Company Adjusted Trial Balance

January 31, 20—

Account Name Debit Credit

Cash 28,274

Accounts Receivable 68,890

Allowance for Doubtful Accounts 2,620

Merchandise Inventory, Furniture Department 84,142

Merchandise Inventory, Lighting Department 41,138

Store Supplies 762

Store Equipment 50,682

Accumulated Depreciation, Store Equipment 41,810

Accounts Payable 38,680

Sales Tax Payable 1,284

M. Chapman, Capital 238,332

M. Chapman, Drawing 126,480

Sales, Furniture Department 409,800

Sales, Lighting Department 273,200

Sales Returns and Allowances, Furniture

Department 11,685

Sales Returns and Allowances, Lighting

Department 1,716

Purchases, Furniture Department 251,847

Purchases, Lighting Department 165,242

Purchases Returns and Allowances, Furniture

Department 4,618

Purchases Returns and Allowances, Lighting

Department 1,792

Purchases Discounts, Furniture Department 5,496

Purchases Discounts, Lighting Department 2,964

Freight In, Furniture Department 13,255

Freight In, Lighting Department 6,885

Sales Salary Expense 123,220

Advertising Expense 14,000

Depreciation Expense, Store Equipment 13,436

Store Supplies Expense 742

Miscellaneous Selling Expense 680

Rent Expense 8,000

Utilities Expense 4,100

Bad Debts Expense 1,800

Miscellaneous General Expense 820

Interest Expense 2,800

1,020,596 1,020,596

CHE-NOBLES-11-0409-Appendix E.indd 9 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Appendix E: Departmental AccountingE-10

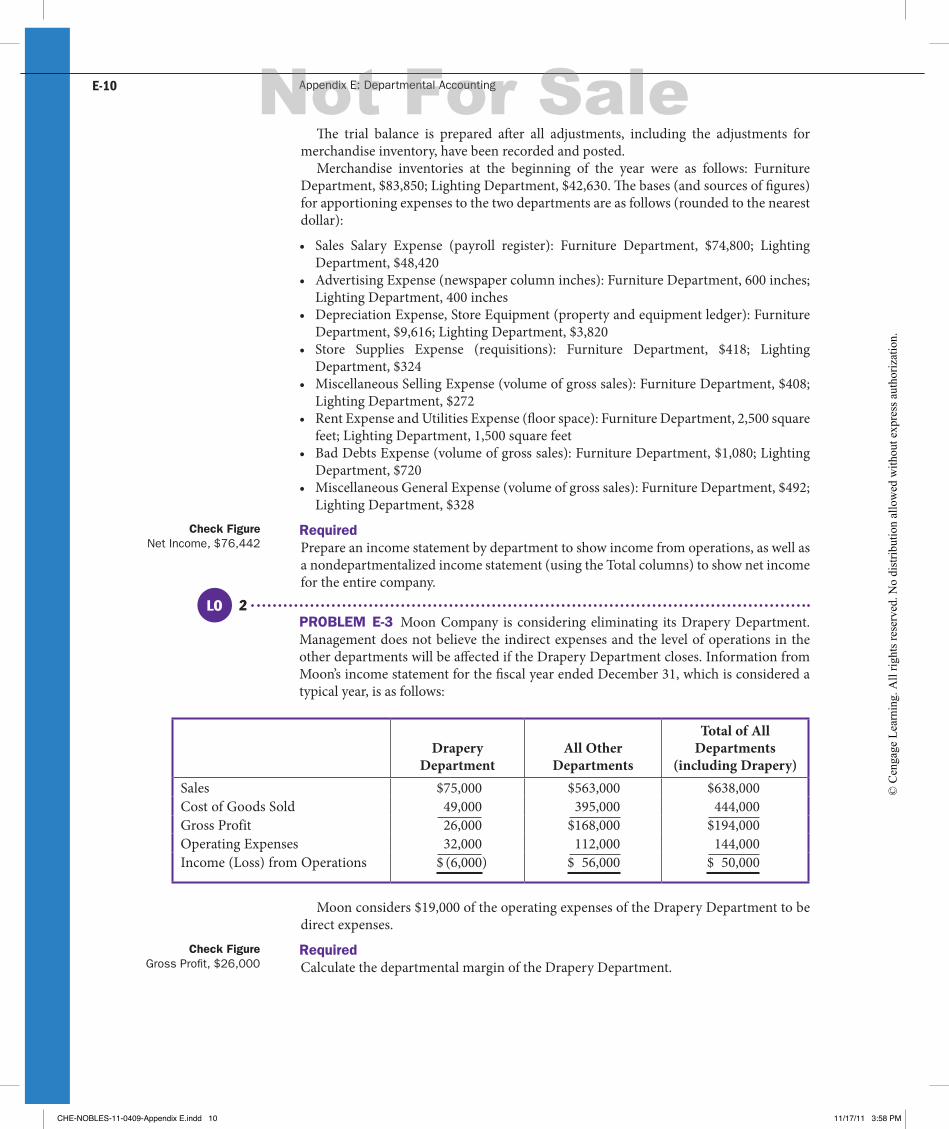

The trial balance is prepared after all adjustments, including the adjustments for merchandise inventory, have been recorded and posted.

Merchandise inventories at the beginning of the year were as follows: Furniture Department, $83,850; Lighting Department, $42,630. The bases (and sources of figures) for apportioning expenses to the two departments are as follows (rounded to the nearest dollar):

• Sales Salary Expense (payroll register): Furniture Department, $74,800; Lighting Department, $48,420

• Advertising Expense (newspaper column inches): Furniture Department, 600 inches; Lighting Department, 400 inches

• Depreciation Expense, Store Equipment (property and equipment ledger): Furniture Department, $9,616; Lighting Department, $3,820

• Store Supplies Expense (requisitions): Furniture Department, $418; Lighting Department, $324

• Miscellaneous Selling Expense (volume of gross sales): Furniture Department, $408; Lighting Department, $272

• Rent Expense and Utilities Expense (floor space): Furniture Department, 2,500 square feet; Lighting Department, 1,500 square feet

• Bad Debts Expense (volume of gross sales): Furniture Department, $1,080; Lighting Department, $720

• Miscellaneous General Expense (volume of gross sales): Furniture Department, $492; Lighting Department, $328

requiredPrepare an income statement by department to show income from operations, as well as a nondepartmentalized income statement (using the Total columns) to show net income for the entire company.

prOBLem e-3 Moon Company is considering eliminating its Drapery Department. Management does not believe the indirect expenses and the level of operations in the other departments will be affected if the Drapery Department closes. Information from Moon’s income statement for the fiscal year ended December 31, which is considered a typical year, is as follows:

Drapery Department

All Other Departments

Total of All Departments

(including Drapery)Sales $75,000 $563,000 $638,000Cost of Goods Sold 49,000 395,000 444,000Gross Profit 26,000 $168,000 $194,000Operating Expenses 32,000 112,000 144,000Income (Loss) from Operations $ (6,000) $ 56,000 $ 50,000

Moon considers $19,000 of the operating expenses of the Drapery Department to be direct expenses.

requiredCalculate the departmental margin of the Drapery Department.

check FigureNet Income, $76,442

2LO

check FigureGross Profit, $26,000

CHE-NOBLES-11-0409-Appendix E.indd 10 11/17/11 3:58 PM

Not For Sale

© C

enga

ge L

earn

ing.

All

right

s res

erve

d. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.