natural gas…at a crossroads?. 2 commodities (before peak)

TRANSCRIPT

Natural Gas…At A Crossroads?

2

Commodities (before peak)

CRUDE OIL NATURAL GAS COAL

WHEAT US DOLLAR GOLD

$20

$40

$60

$80

$100

$120

$140

$160

Jan-

06

Apr

-06

Jul-06

Oct

-06

Jan-

07

Apr

-07

Jul-07

Oct

-07

Jan-

08

Apr

-08

Jul-08

$2

$4

$6

$8

$10

$12

$14

$16

Jan-

06

Apr

-06

Jul-06

Oct

-06

Jan-

07

Apr

-07

Jul-07

Oct

-07

Jan-

08

Apr

-08

Jul-08

$20

$40

$60

$80

$100

$120

$140

$160

Jan-

06

Apr

-06

Jul-06

Oct

-06

Jan-

07

Apr

-07

Jul-07

Oct

-07

Jan-

08

Apr

-08

Jul-08

$200

$400

$600

$800

$1,000

$1,200

$1,400

Jan-

06

Apr

-06

Jul-06

Oct

-06

Jan-

07

Apr

-07

Jul-07

Oct

-07

Jan-

08

Apr

-08

Jul-08

$70

$75

$80

$85

$90

$95

Jan-

06

Apr

-06

Jul-06

Oct

-06

Jan-

07

Apr

-07

Jul-07

Oct

-07

Jan-

08

Apr

-08

Jul-08

$500

$600

$700

$800

$900

$1,000

$1,100

Jan-

06

Apr

-06

Jul-06

Oct

-06

Jan-

07

Apr

-07

Jul-07

Oct

-07

Jan-

08

Apr

-08

Jul-08

3

Commodities (to current)

CRUDE OIL NATURAL GAS COAL

WHEAT US DOLLAR GOLD

$20

$40

$60

$80

$100

$120

$140

$160

Jan-

06

Jun-

06

Nov

-06

Apr

-07

Sep-

07

Feb-

08

Jul-08

Dec

-08

May

-09

Oct

-09

Mar

-10

$2

$4

$6

$8

$10

$12

$14

$16

Jan-

06

Jun-

06

Nov

-06

Apr

-07

Sep-

07

Feb-

08

Jul-08

Dec

-08

May

-09

Oct

-09

Mar

-10

$20

$40

$60

$80

$100

$120

$140

$160

Jan-

06

Jun-

06

Nov

-06

Apr

-07

Sep-

07

Feb-

08

Jul-08

Dec

-08

May

-09

Oct

-09

Mar

-10

$200

$400

$600

$800

$1,000

$1,200

$1,400

Jan-

06

Jun-

06

Nov

-06

Apr

-07

Sep-

07

Feb-

08

Jul-08

Dec

-08

May

-09

Oct

-09

Mar

-10

$70

$75

$80

$85

$90

$95

Jan-

06

Jun-

06

Nov

-06

Apr

-07

Sep-

07

Feb-

08

Jul-08

Dec

-08

May

-09

Oct

-09

Mar

-10

$500

$600

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

Jan-

06

Jun-

06

Nov

-06

Apr

-07

Sep-

07

Feb-

08

Jul-08

Dec

-08

May

-09

Oct

-09

Mar

-10

4

Futures – Are They Accurate?

"That's mathematics, son. You can argue with me, but

you can't argue with figures.“ Foghorn

Leghorn

-60%

-30%

0%

30%

60%

90%

120%

Jan-99

Jan-01

Jan-03

Jan-05

Jan-07

Jan-09

NYM

EX S

trip

, Pr

edic

ted -Act

ual, %

Strip Too High

(Strip Too Low)

Commodity Price Forecasts

Qualitatively Quantitatively

Oil Gas Oil Gas

$90/bbl $6.50/mcf

Cardinal Rule Of Price ForecastingNever Provide Both Price And Year

At The Same Time!

5

6

Natural Gas

Ample gas supply in almost any demand scenario – long term

□ Shale gas

1 bcf/day net demand growth assumed

Shale, Shale and more Shale

Fewer rigs required (~1,500)

Lower equilibrium natural gas price

□ $6.20/mcf in 2010

□ $6.50/mcf in 2011+

Implications for all energy subsectors/stocks

7

16

18

20

22

24

26

28

30

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Ann

ual Nat

ural

Gas

Dem

and (Tc

f/Ye

ar)

Natural Gas Demand

HUGEHUGEGAPGAP

NPC Study…Way Off Target

8

Shalemania – Shale is a Game Changer

Long Term – ample gas supply

□ Need fewer rigs in fewer places

□ Shales will grow

□ Everywhere else declines

Near Term – “damn the torpedoes”

□ Lot’s of drilling to hold acreage

□ Uh Oh! Cliff ahead.

Crude oil

□ The Rod Tidwell of energy “You’re loving me now!”

□ Lots of desire to “get oily”…but harder to accomplish

9

Why Shale? Meet GOM Shelf Production

0

2

4

6

8

10

12

14

16

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Gas

Pro

ducti

on, b

cf/d

ay

GOM Total

GOM Shelf

Deepwater

“I can hardly remember how I built my bankroll, but I can't stop thinking about the way I lost it." Mike….Rounders

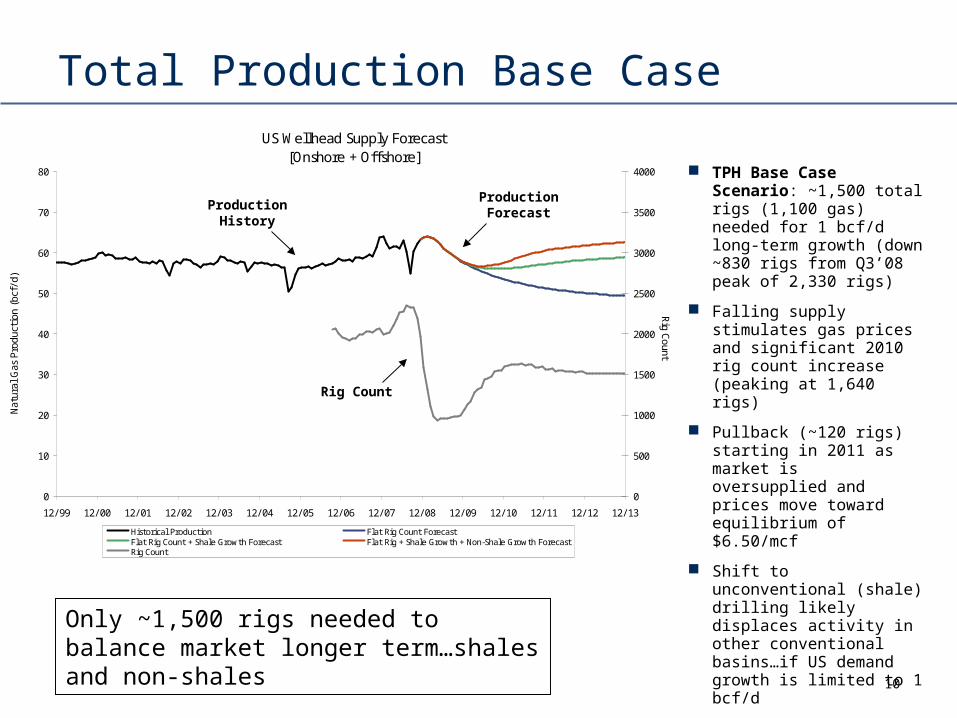

US Wellhead Supply Forecast[Onshore + Offshore]

0

10

20

30

40

50

60

70

80

12/ 99 12/ 00 12/ 01 12/ 02 12/ 03 12/ 04 12/ 05 12/ 06 12/ 07 12/ 08 12/ 09 12/ 10 12/ 11 12/ 12 12/ 13

Nat

ural

Gas

Pro

duct

ion

(bcf

/d)

0

500

1000

1500

2000

2500

3000

3500

4000

Rig Count

Historical Production Flat Rig Count ForecastFlat Rig Count + Shale Growth Forecast Flat Rig + Shale Growth + Non-Shale Growth ForecastRig Count

Total Production Base Case

Rig Count

Production Forecast

Production History

10

Only ~1,500 rigs needed to balance market longer term…shales and non-shales

TPH Base Case Scenario: ~1,500 total rigs (1,100 gas) needed for 1 bcf/d long-term growth (down ~830 rigs from Q3’08 peak of 2,330 rigs)

Falling supply stimulates gas prices and significant 2010 rig count increase (peaking at 1,640 rigs)

Pullback (~120 rigs) starting in 2011 as market is oversupplied and prices move toward equilibrium of $6.50/mcf

Shift to unconventional (shale) drilling likely displaces activity in other conventional basins…if US demand growth is limited to 1 bcf/d

US Wellhead Supply Forecast[Shale Production]

0

5

10

15

20

25

12/ 99 12/ 00 12/ 01 12/ 02 12/ 03 12/ 04 12/ 05 12/ 06 12/ 07 12/ 08 12/ 09 12/ 10 12/ 11 12/ 12 12/ 13

Nat

ural

Gas

Pro

duct

ion

(bcf

/d)

0

500

1,000

1,500

2,000

2,500

Rig Count

Historical Production Forecasted Production Rig Count

Production History

Shales –The Growth Engine

Rig Count

Production Forecast

11

Shale gas 12/08

□ Production = 8 bcf/d (12% of US)

□ Rig Count = 357 rigs (18% of US)

Shale gas 12/13

□ Production = 22 bcf/d (35% of US)

□ Rig Count = 614 rigs (41% of US)

Demonstrates dependence on shale gas to maintain/grow US supply as conventional production declines

Betting on the turn…early in producing life of most shales. Long-term production profile is a big unknown

Source: Rig Count = Rig Data Onshore/Baker Hughes Offshore, Production History = HPDI and EIA,

Forecast = TPH Estimates

Note: Wellhead production is wet gas. Rig count is total rig count gas/oil and onshore/offshore.

Annual Average RatesRate Δ Rate Δ Rate Rig Δ Rig Δ Rigbcf/d bcf/d %/yr Count Count # Count %

2007A 4.5 2862008A 6.5 2.0 45% 344 58 20%2009E 8.7 2.2 34% 277 -67 -19%2010E 10.5 1.8 21% 422 144 52%2011E 14.4 3.9 37% 582 160 38%2012E 18.0 3.6 25% 625 43 7%2013E 20.6 2.5 14% 614 -11 -2%

Shale Basin 12/08a 7/09e 12/13e

Haynesville 0.2 1.0 6.3

Barnett 5.0 4.7 5.5

Marcellus 0.0 0.2 4.4

Fayetteville 1.3 1.5 2.8

Woodford 0.9 0.9 1.5

Eagle Ford 0.0 0.0 0.7

Antrim 0.4 0.4 0.3

Total 7.8 8.7 21.5

Daily Gas Volumes, bcf/d

US Wellhead Supply Forecast[Non-Shale Production]

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

12/ 99 12/ 00 12/ 01 12/ 02 12/ 03 12/ 04 12/ 05 12/ 06 12/ 07 12/ 08 12/ 09 12/ 10 12/ 11 12/ 12 12/ 13

Nat

ural

Gas

Pro

duct

ion

(bcf

/d)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Rig Count

Historical Production Forecasted Production Rig Count

Production History

Non-Shale Production

Rig Count

Production Forecast

12

Non-Shale gas 12/08

□ 56 bcf/d (88% of US)

□ 1,600 rigs (82% of US)

Non-Shale gas 12/13

□ 41bcf/d (66% of US)

□ 900 rigs (59% of US)

Highly Technical – Revenge of the Nerds

Horizontal Drilling – Orientation / optimum Length

Completion – Hydraulic Fracture…can’t boilerplate

□ Number of stages

□ Slickwater vs. Gelled Fracs

□ Proppant type

Geology – Faulting, heterogeneity, seismic

Don’t forget the reservoir engineer!

□ Decline curve and recovery

□ Well spacing/drainage area (ultimate recovery)

□ Reservoir modeling is difficult Natural fracture spacing orientation Isotherm, gas-in-place, free gas porosity

13

14

44

46

48

50

52

54

56

58

60

Tota

l Ons

hore

Gas

(bcf

/d)

Total Onshore Gas (TPH vs. EIA 914 Data)

914 Data Model

Production Declining…but Less Than Expected

Damn the Torpedoes…Full Steam Ahead

15

1,543

414

1,957

643

179

822 914

450

1,364

0

500

1,000

1,500

2,000

2,500

Gas-Directed Oil-Directed Total

# ri

gs w

orki

ng

Peak Trough Current

Not Just Public Co’s Ignoring the Torpedoes

16

1,345

1,029

2,374

548 353

901 901

610

1,511

0

500

1,000

1,500

2,000

2,500

Public E&P Private E&P Total

# ri

gs w

orki

ng

Peak Trough Current

Natural Gas Demand

Forecasting 1 bcf/d annual demand growth long-term from depressed 2009 levels

Driver of growth is electricity sector with 0.7 bcf/d of annual demand increase.

□ 2% annual GDP growth

□ A 10% renewable standard is achieved by 2020

Industrial demand grows 0.3 bcf/d (~1.5%) annually from depressed 2009 levels

□ Reversing long-term trend of declining industrial demand

17

GDP and % Renewables – Key Variables

18

Annual Gas Demand Growth, bcf/day% Renewable by 2020

0.7 2% 5% 10% 15%0% 0.0 -0.1 -0.3 -0.61% 0.5 0.4 0.1 -0.12% 1.1 0.9 0.7 0.43% 1.7 1.5 1.2 1.04% 2.4 2.2 1.9 1.6G

DP

Gro

wth

%

Electricity is Gas Demand Driver

19

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Ann

ual G

ener

ation

-th

ousa

nd m

egaw

att-h

rsCoal Petroleum Natural Gas

Nuclear Hydro Electric Alternative (Wind)

Natural Gas and Alternative(Wind) fuel power generation growth in the next decade.

Industrial Demand Growth

(1,000)

1,000

3,000

5,000

7,000

9,000

11,000

13,000

15,000

2001

2003

2005

2007

2009

e

2011

f

2013

f

2015

f

2017

f

2019

f

US

GD

P

0

5

10

15

20

25

Ind

ust

rial

Dem

and

, b

cf/d

ay

US GDP Industrial Demand

Industrial natural gas demand not correlated with GDP (2001-2008). High gas prices caused reduced demand even in a growing

We assume industrial gas will be correlated with GDP in next decade as a more plentiful supply of natural gas allows for industrial demand expansion.

Ample gas supply and lower long-term gas prices, combined with GDP growth spurs industrial demand recovery

0.3 bcf/d (~1.5%) annual growth is from depressed 2009 levels

If overall US natural gas demand is flat at current levels, we would expect equilibrium gas prices to average $5.50/mcf (vs. our base case of $6.50/mcf)

20

Existing Gas Flows…Go East Young Man?

Rockies

Supply

Gulf Coast Supply

Haynesville

Eagle Ford

Marcellus

Appalachia Supply

Source: Tudor, Pickering, Holt & Co.

21

According to the map we've only gone 4 inches. Harry Dumb and Dumber

Cumulative Percent Gas Rig Count By Economic Threshold [2013]

0%

25%

50%

75%

100%

$4.50 $5.00 $5.50 $6.00 $6.50 $7.00 $7.50 $8.00 $8.50 $9.00 $9.50 $10.00

Threshold Natural Gas Price ($/mcf)

Cum

ulat

ive

Perc

ent

Rig

Cou

nt

10% IRR 20% IRR

10% IRR

Marginal Cost - 2013 Cumulative Rig Count

20% IRR

22

Long-Term 2011+ Price Forecast

Marginal cost curve shifts to the left as a higher percentage of the overall US drilling portfolio includes shale wells

Our long-term gas price is $6.50/mcf

"Ah! It's a profit deal! Navin Johnson The Jerk

(Most Economic Basins) (Least Economic Basins)

23

Gas Supply Wild CardsShale Performance

Officer and a Gentleman

□ “I got nowhere else to go”

Gas Macro Variables

□ LNG

□ Renewables

□ Canada Shales/Imports

□ Demand

High-Grading/Well efficiency

Frac Regulations

Infrastructure Build-Out

Midstream/MLP Sector Implications

24

Near term: Likely greater gathering and intrastate pipeline declines. Biggest impacts in 2H’09 and 1H’10

Opportunities for investment in shale play takeaway capacity and processing

Narrowing of basis differentials across the board

Lower gas prices and higher oil prices positive for domestic NGL business and processing utilization

Longer term: some long-haul pipelines may be re-contracted at discounts or capacity utilization drops

Power Sector Implications

25

Stabilizing impact on power markets

Enhances natural gas as obvious choice for next generation of supply

Reduces attractiveness of renewable generation

Provides a practical solution to reduced carbon

Final Thoughts

Natural Gas – a $6.5/mcf commodity

E&P’s acting like prices are already there...ugh

Shales are a game changer

□ But non-shales will set the marginal price of gas

26

27

Conclusion

Formula for success:

“Rise early, work hard, strike oil.”

J. Paul Getty

Note: Getty said “Oil”…not more shale gas!