natural gas roundtable - gti presentation

DESCRIPTION

Ted Barnes, Gas Technology Institute, presented information on Developments in the Surrounding States for our Natural Gas for Transportation Roundtable in Janesville, WI.TRANSCRIPT

Wisconsin Natural Gas Roundtable: Developments in Surrounding States

Ted Barnes

Gas Technology Institute

October 2014

2 2

Objectives

1. GTI Background

2. What’s Already Here - Locating Current Stations

3. What’s Coming and When?

4. Grants/Upcoming Developments

5. Contact your local Clean Cities Coordinator

3 3

ESTABLISHED 1941

GTI: Company Overview

> Staff of 250

> 350 active projects

> 1,200 patents; 500 products

Energy & Environmental Technology Center

Office & Labs Pilot-Scale Gasification Campus

Training

Natural Gas Research and

Development Focus

4

GTI – Barrier Reduction Grant

Webinar Series

I. Inspection Guidelines for CNG/LPG Vehicle Conversions

II. Considerations for Garage & Maintenance Shops When Using CNG/LPG

III. Station Installation Guidelines for CNG

IV. Station Installation Guidelines for LPG

V. Best Practices for End Users for CNG, LPG & Electric Vehicles

The webinars and slides are available online at www.wicleancities.org/webinars.php

Barriers Survey

Survey to gather barriers for adoption of alternative fuels

Please complete the survey at:

www.wicleancities.org

5 5

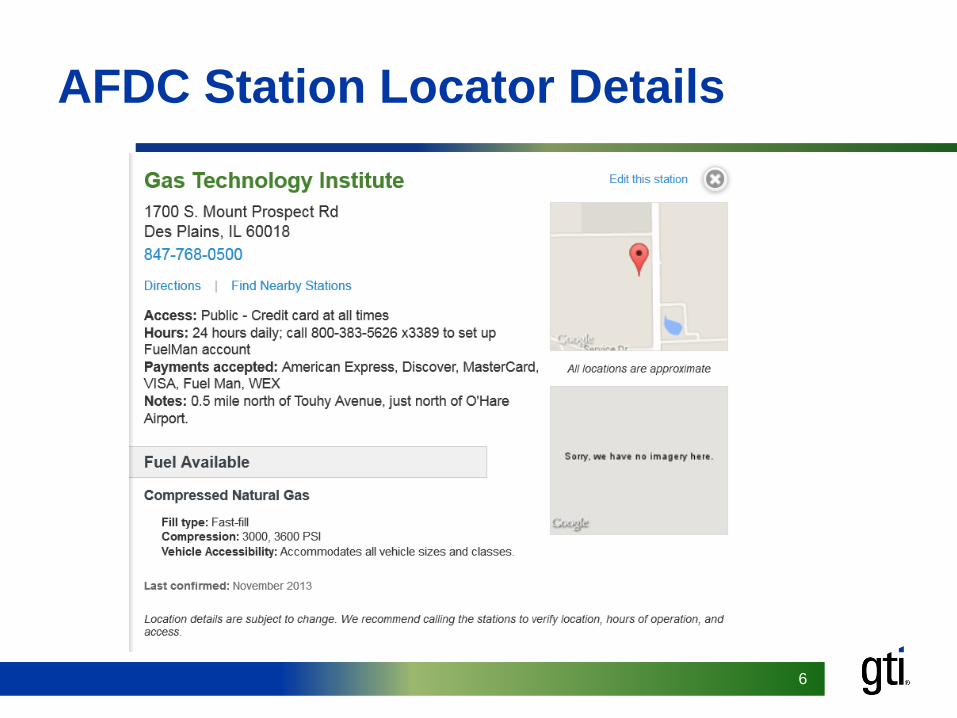

What’s Available Now?

Locating Current CNG Fueling Stations

• Use AFDC Station Locator

(http://www.afdc.energy.gov/locator/stations/)

• Access through all local Clean Cities websites

• Shows stations that are planned to be available soon

• Shows public and private stations

• Gives details on each facility

• Other websites include: CNGnow.com; station provider

websites; fuel management card websites; utility websites

• Often incomplete because of regional or proprietary nature

6 6

AFDC Station Locator Details

7 7

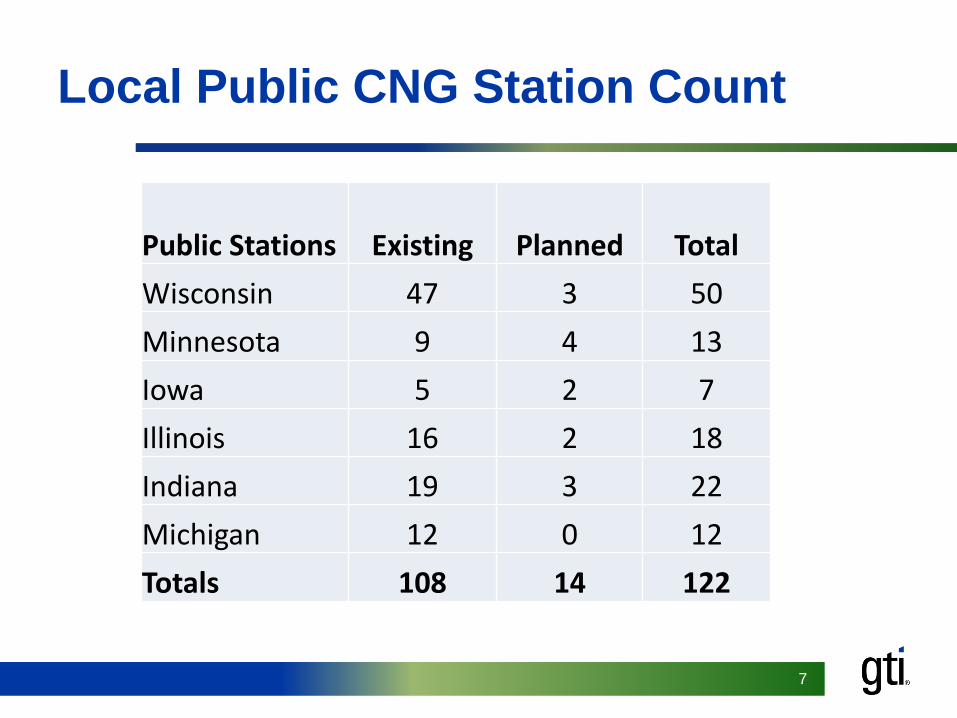

Local Public CNG Station Count

Public Stations Existing Planned Total

Wisconsin 47 3 50

Minnesota 9 4 13

Iowa 5 2 7

Illinois 16 2 18

Indiana 19 3 22

Michigan 12 0 12

Totals 108 14 122

8 8

9 9

10 10

11 11

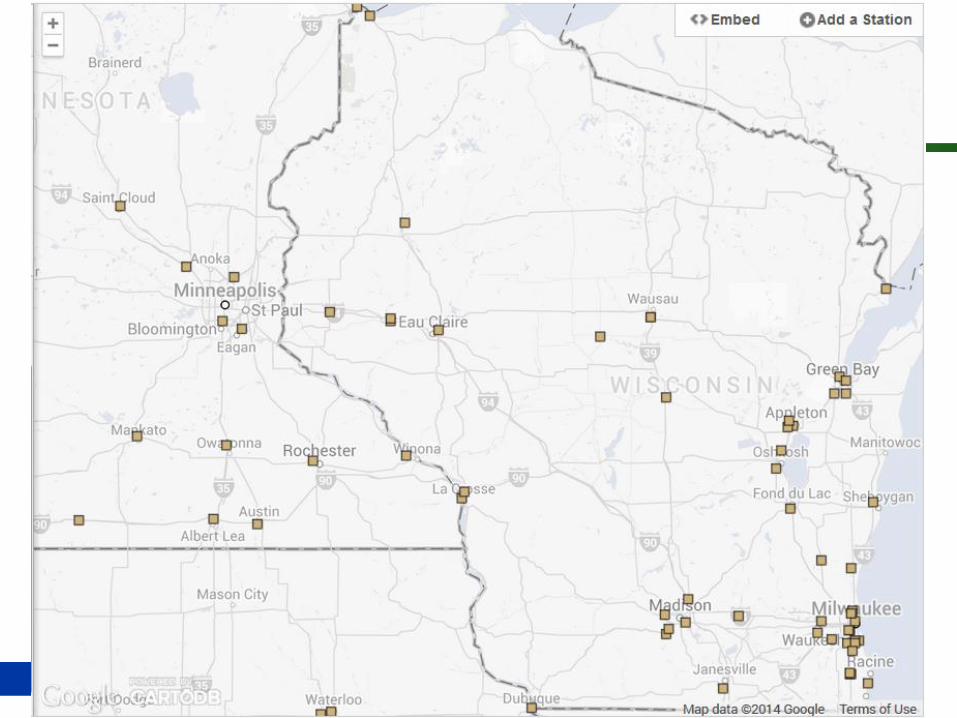

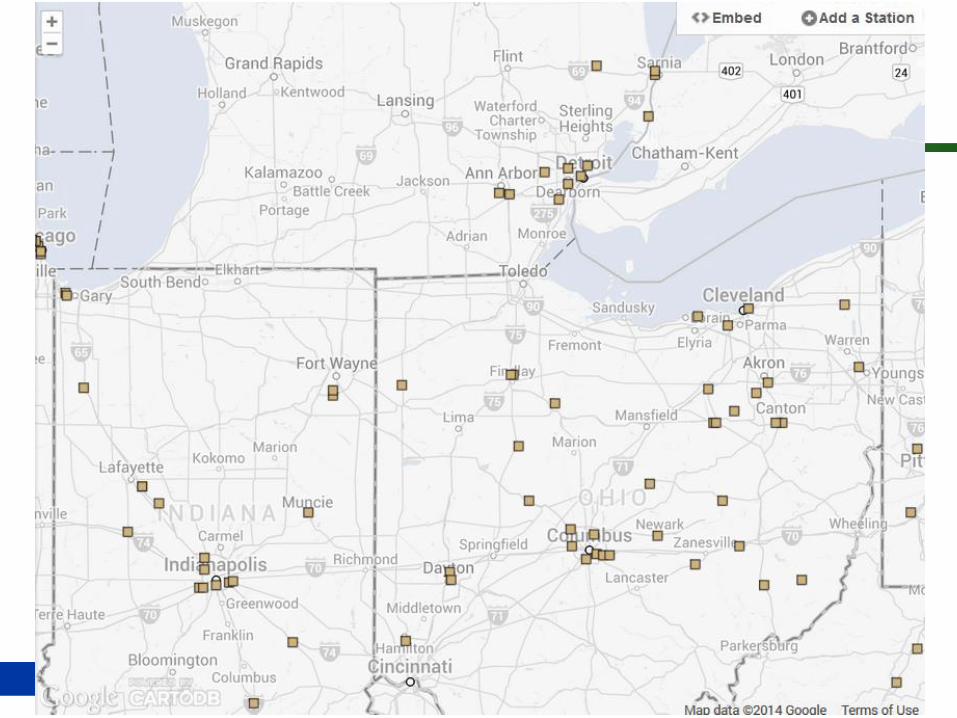

What’s Coming and When?

• List from AFDC – incomplete but still promising

Provider City State Date

Barnes Inc - US Oil Madison WI 4/15/2015

GAIN Clean Fuel Middleton WI 10/24/2014

Kwik Trip Windsor WI 12/1/2014

Clean Energy Chicago IL 12/1/2014

WM Rockdale IL 12/1/2014

CNG Source Indianapolis IN 7/15/2014

GAIN Clean Fuel Indianapolis IN 11/15/2014

CNG Fuel Inc Fort Wayne IN 4/1/2015

South Bend South Bend IN Mid 2015

Great River Energy West Burlington IA 4/15/2014

GAIN Clean Fuel Des Moines IA 1/1/2015

CHS Inc Fairmont MN 9/15/2014

Kwik Trip Austin MN 11/20/2014

Kwik Trip Albert Lea MN 10/30/2014

Saint Cloud Metro Bus Saint Cloud MN 12/31/2014

DTE Energy Grand Rapids MI TBD

12 12

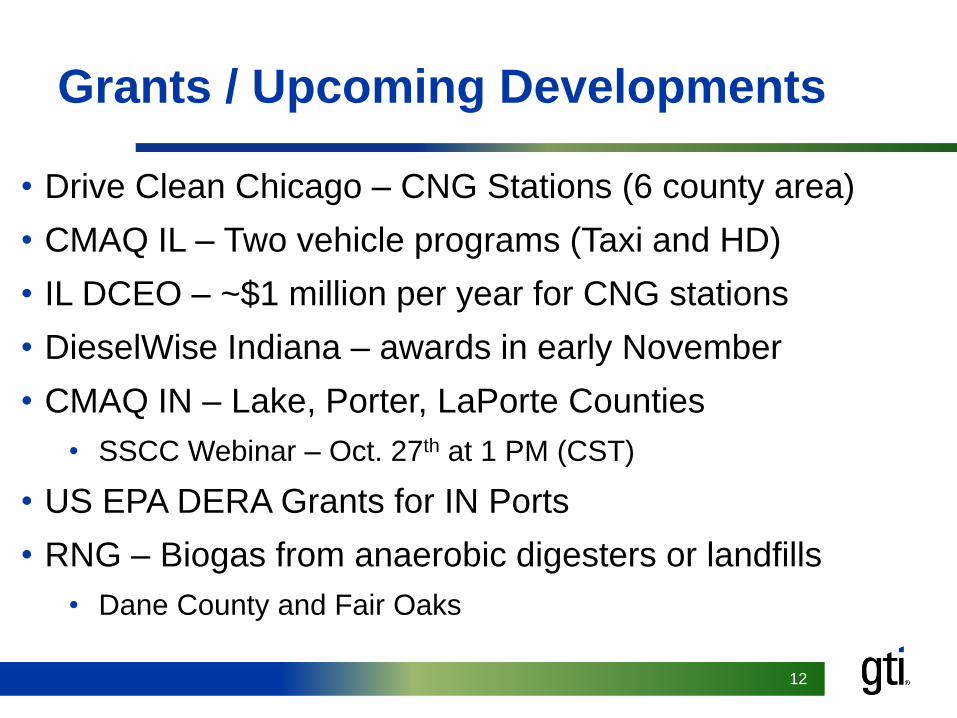

Grants / Upcoming Developments

• Drive Clean Chicago – CNG Stations (6 county area)

• CMAQ IL – Two vehicle programs (Taxi and HD)

• IL DCEO – ~$1 million per year for CNG stations

• DieselWise Indiana – awards in early November

• CMAQ IN – Lake, Porter, LaPorte Counties

• SSCC Webinar – Oct. 27th at 1 PM (CST)

• US EPA DERA Grants for IN Ports

• RNG – Biogas from anaerobic digesters or landfills

• Dane County and Fair Oaks

13 13

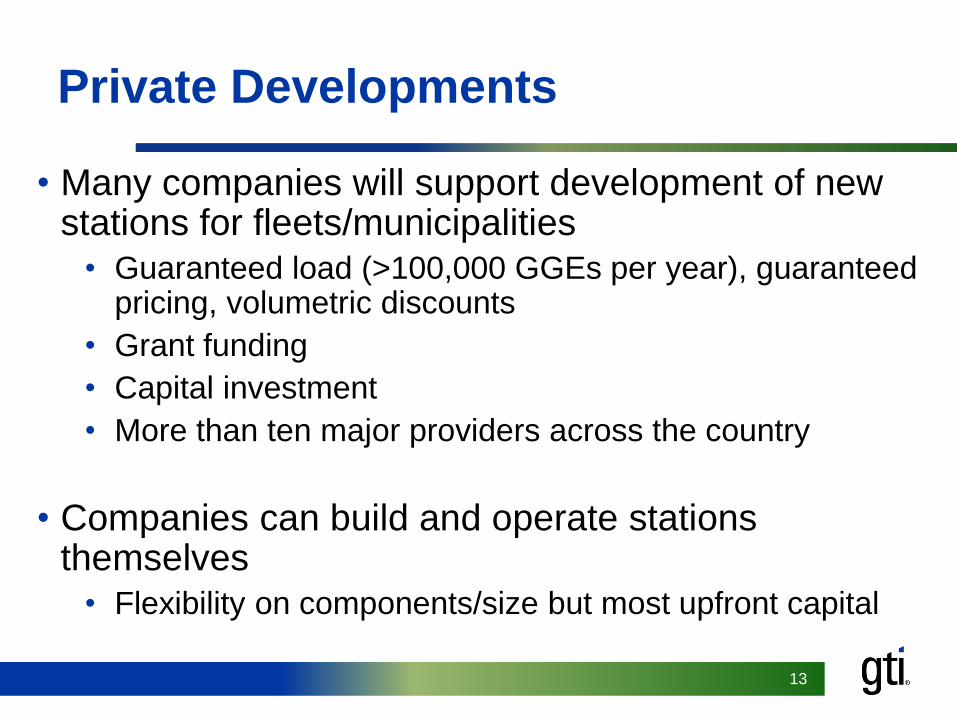

Private Developments

• Many companies will support development of new stations for fleets/municipalities

• Guaranteed load (>100,000 GGEs per year), guaranteed pricing, volumetric discounts

• Grant funding

• Capital investment

• More than ten major providers across the country

• Companies can build and operate stations themselves

• Flexibility on components/size but most upfront capital

14 14

Resources

15 15

Acknowledgement of Support

16 16

Backup Slides

17 17

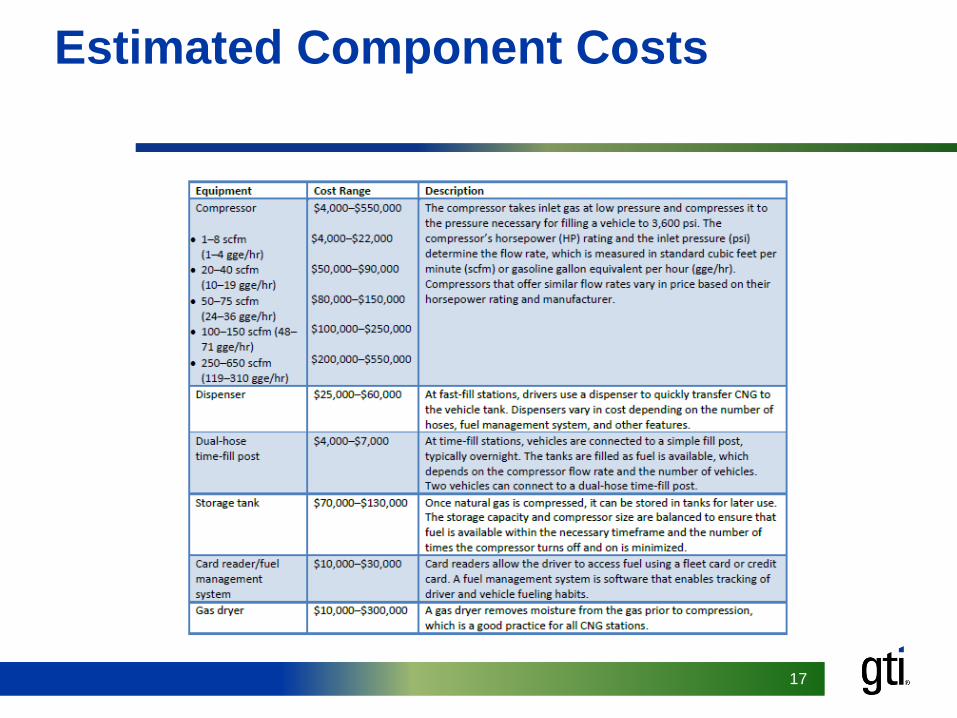

Estimated Component Costs

18 18

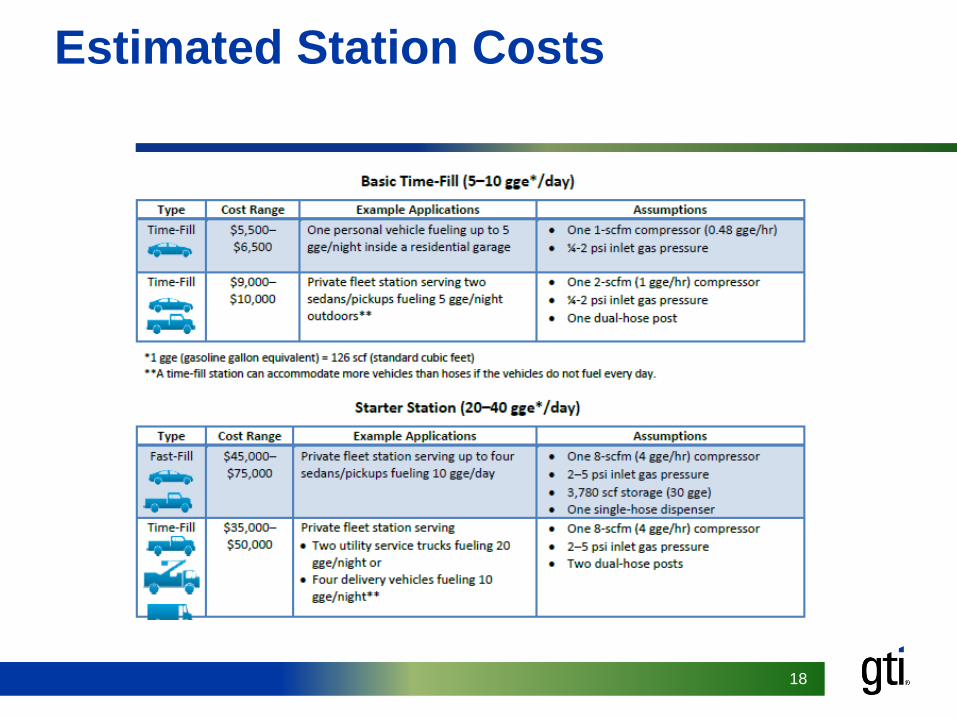

Estimated Station Costs

19 19

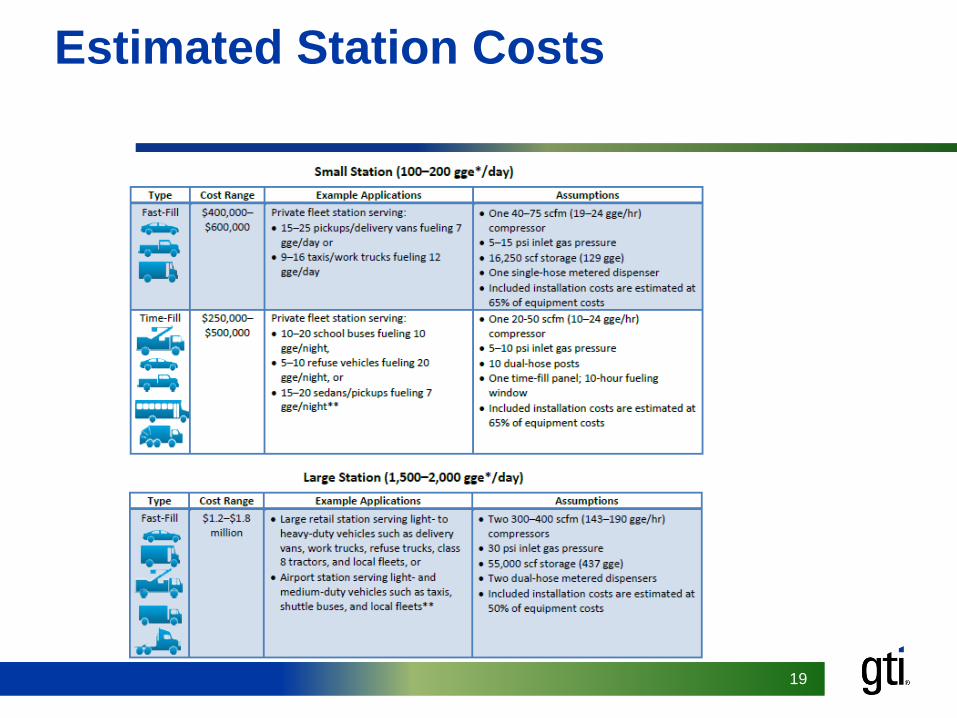

Estimated Station Costs

20

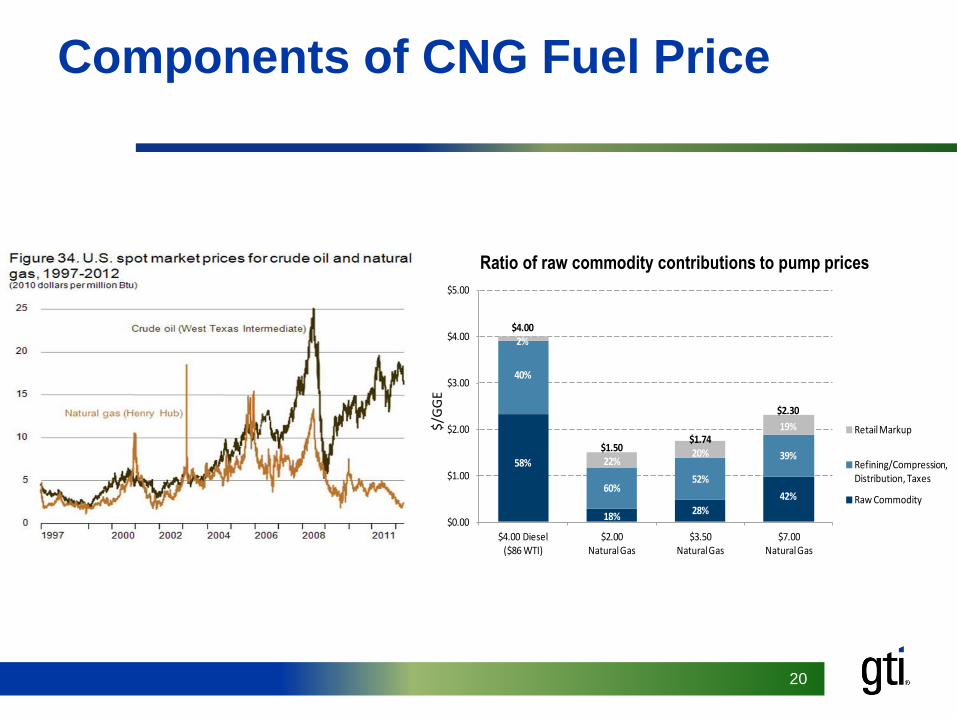

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$4.00 Diesel($86 WTI)

$2.00Natural Gas

$3.50Natural Gas

$7.00Natural Gas

Retail Markup

Refining/Compression,Distribution, Taxes

Raw Commodity

$4.002%

40%

58%

$1.5022%

60%

18%

$1.7420%

52%

28%

$2.30

19%

39%

42%

Ratio of raw commodity contributions to pump prices

Components of CNG Fuel Price

$/G

GE

21 21

Components of CNG

Fuel Price

> Gas Commodity (.55/GGE @ “weighted average” cost of $4.40/MCF)

> Pipeline transportation/services to utility “city gate” and then delivered under regulated tariff by your local utility to your meter uncompressed ($.10 - .25)

> Compression - Rule of thumb: One fully-loaded kWh/GGE ($.10-15/GGE)

> Station Maintenance - Normal PM, repair/replace parts, rebuild ($.15-.30/GGE)

> Equipment amortization ($.35 - .65/GGE)

─ Cost of equipment or cost of capital factored into each

GGE over life of station equipment (typically10 years)

> Station operator profit (if a retail provider)

> Add federal motor fuels excise tax & State/Local tax

─ FEET = $.183/gallon; State of IL $0.19/gallon = $0.373/GGE

> Bottom line: approximately $1.52 to $2.02 (without profit margin or any incentives)

22 22

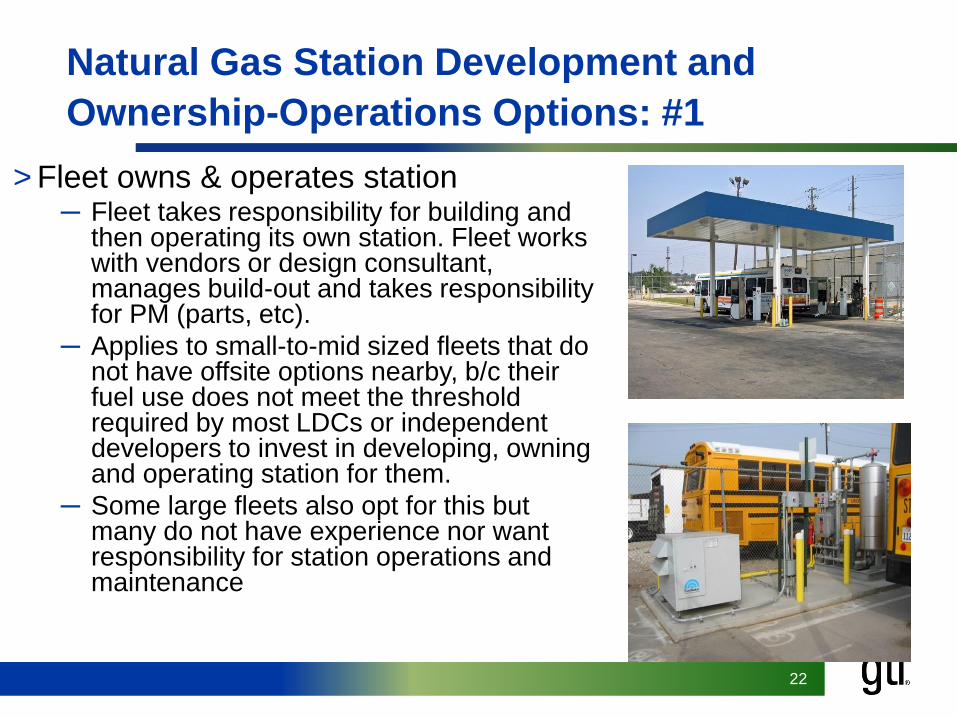

Natural Gas Station Development and

Ownership-Operations Options: #1

> Fleet owns & operates station ─ Fleet takes responsibility for building and

then operating its own station. Fleet works with vendors or design consultant, manages build-out and takes responsibility for PM (parts, etc).

─ Applies to small-to-mid sized fleets that do not have offsite options nearby, b/c their fuel use does not meet the threshold required by most LDCs or independent developers to invest in developing, owning and operating station for them.

─ Some large fleets also opt for this but many do not have experience nor want responsibility for station operations and maintenance

23 23

Natural Gas Station Development and

Ownership-Operations Options: #2

> Outsource station development, ownership, O&M to independent fuel provider

─ Fleet serves as anchor for independent operator’s station, contracts long term fuel agreement with set price(s) and expected throughput for duration.

─ One stop shop. All capital investment and O&M risks are borne by independent fuel provider while fleet focuses on core competencies.

─ Fleet usually provides low-cost lease for property – important to making deal work - land is costly!

─ Often allows fuel provider option to create public access as well – sometimes a “royalty” paid back to fleet for retail sales from premises

24 24

Natural Gas Station Development and

Ownership-Operations Options: #3

> Fleet owns/leases station but contracts out operations for a fee (e.g., monthly fee or GGE basis)

─ Option used by many large fleets that need/desire ownership of their own station equipment but want to reduce risk, assure best O&M practices, etc

─ Contract is often (but not always) awarded to the firm that builds station; usually a 5-7yr contract.

─ Some fleets that initially Own & Operate their own stations decide that they want to delegate to others – put out RFP for O&M contract

─ Decision weighs pros/cons of “leaving $ on table” versus potential downtime risks, maintaining parts inventories, updated training of techs, etc

25 25

References

> References for previous slides