natural gas basis market outlook

TRANSCRIPT

NATURAL GAS BASIS MARKET OUTLOOK

FEBRUARY 18, 2015

A GUEST SPEAKER CALL WITH Keith Barnett Head of Fundamental Analysis at Asset Risk Management (ARM) There will be a Q&A session at the end of the call; email questions for Keith to [email protected].

HEDGEYE 2

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

HEDGEYE DISCLAIMER

DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice for individuals. This research does not constitute an offer to sell, or a solicitation of an offer to buy any security. This research is presented without regard to individual investment preferences or risk parameters; it is general information and does not constitute specific investment advice. This presentation is based on information from sources believed to be reliable. Hedgeye Risk Management is not responsible for errors, inaccuracies or omissions of information. This presentation is the work of Keith Barnett of Asset Risk Management (ARM) and is protected intellectual property. Views and opinions expressed herein do not necessarily reflect the opinions of Hedgeye Risk Management. This presentation is for information purposes and is not intended as an investment recommendation.

TERMS OF USE This report is intended solely for the use of its recipient. Re-distribution or republication of this report and its contents are prohibited. For more details please refer to the appropriate sections of the Hedgeye Services Agreement and the Terms of Use at www.hedgeye.com

3

Natural Gas Basis Market Outlook

February 2015

Fundamental Analysis Keith Barnett

Houston (281) 655-3200 Pittsburgh (412) 886-1800 Chicago (847) 920-5199 Denver (303) 409-7677 Calgary (403) 538-3770

Hedgeye Market View

4

Asset Risk Management (ARM) Overview

ARM has been assisting Oil & Gas Producers with their hedge portfolios since 2004. We use a dynamic approach to risk management by implementing initial strategies that provide commodity price protection for balance sheets and capital programs while retaining the ability to adjust/enhance as the market provides opportunity.

• ARM provided strategies can: • Reduce exposure to energy market risk while optimizing and actively

managing hedge assets • Improve financial management of hedging portfolio and increase overall

returns • ARM develops, implements, manages, and maintains hedge positions for clients • ARM is not a trading counterpart, broker, aggregator, or supplier • In response to our client’s needs ARM has expanded its services to include:

• Physical marketing of crude, natural gas and NGL’s • Development and ownership of gathering and midstream assets (JV or 100%)

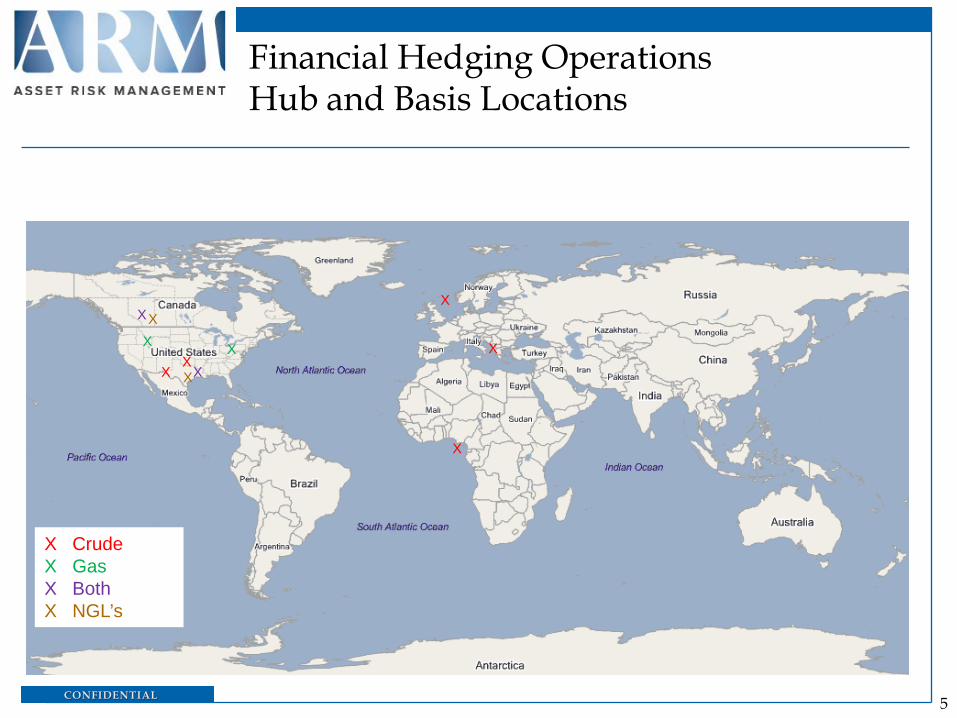

Financial Hedging Operations Hub and Basis Locations

5

X

X

X

X

X X X

X

X Crude X Gas X Both X NGL’s

X

X

X

6

North American Basis Markets

AECO

HSC

OPAL

Chicago CG

DOM South

NYC

X Henry Hub

Southern Cal Border

7

• Crude, liquids, and nat gas prices have altered production and demand outlooks while infrastructure growth continues, although additional projects will slow down

• L-48 production growth will slow dramatically and could even decline in 2016 • 2018 exit rate is lower than prior ARM outlook

• 3 of 4 “Pillars of Demand” are threatened by lower oil price • Exports to Mexico are threatened by negative impacts to

economy rippling through power and industrial projects • Industrial demand impacted by drop in competitive

position for petrochemicals vs. global naphtha crackers, lower oilfield activity and stronger US dollar

• LNG exports are sensitive to global crude prices so lower Brent price reduces potential to Asia and Europe

• Gas for power generation is least affected with projected retirements of coal plants actually increasing over prior estimates

• Adjacent cumulative production growth chart for production and demand only address the 4-pillars of demand and do not estimate coal to gas switching levels needed in 2015 to balance the market as expected storage levels approach 4 Tcf or higher • Cumulative shortfall of 2017 & 2018 combined should

encourage price response leading to production increase

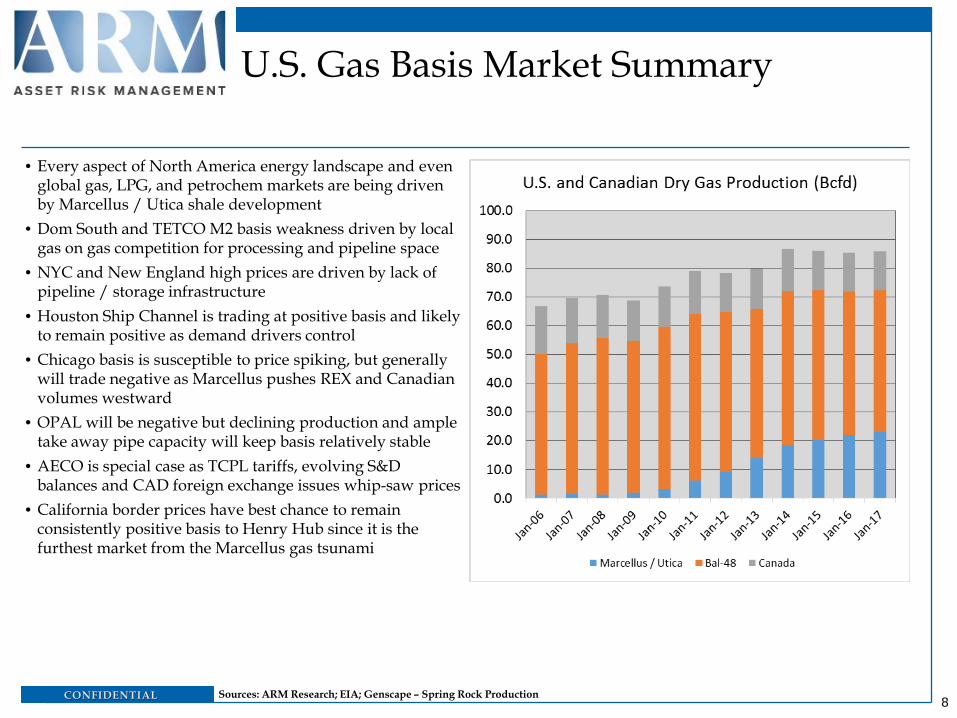

U.S. Gas Market Summary

Sources: ARM Research; EIA; Genscape – Spring Rock Production

8

• Every aspect of North America energy landscape and even global gas, LPG, and petrochem markets are being driven by Marcellus / Utica shale development

• Dom South and TETCO M2 basis weakness driven by local gas on gas competition for processing and pipeline space

• NYC and New England high prices are driven by lack of pipeline / storage infrastructure

• Houston Ship Channel is trading at positive basis and likely to remain positive as demand drivers control

• Chicago basis is susceptible to price spiking, but generally will trade negative as Marcellus pushes REX and Canadian volumes westward

• OPAL will be negative but declining production and ample take away pipe capacity will keep basis relatively stable

• AECO is special case as TCPL tariffs, evolving S&D balances and CAD foreign exchange issues whip-saw prices

• California border prices have best chance to remain consistently positive basis to Henry Hub since it is the furthest market from the Marcellus gas tsunami

U.S. Gas Basis Market Summary

Sources: ARM Research; EIA; Genscape – Spring Rock Production

9

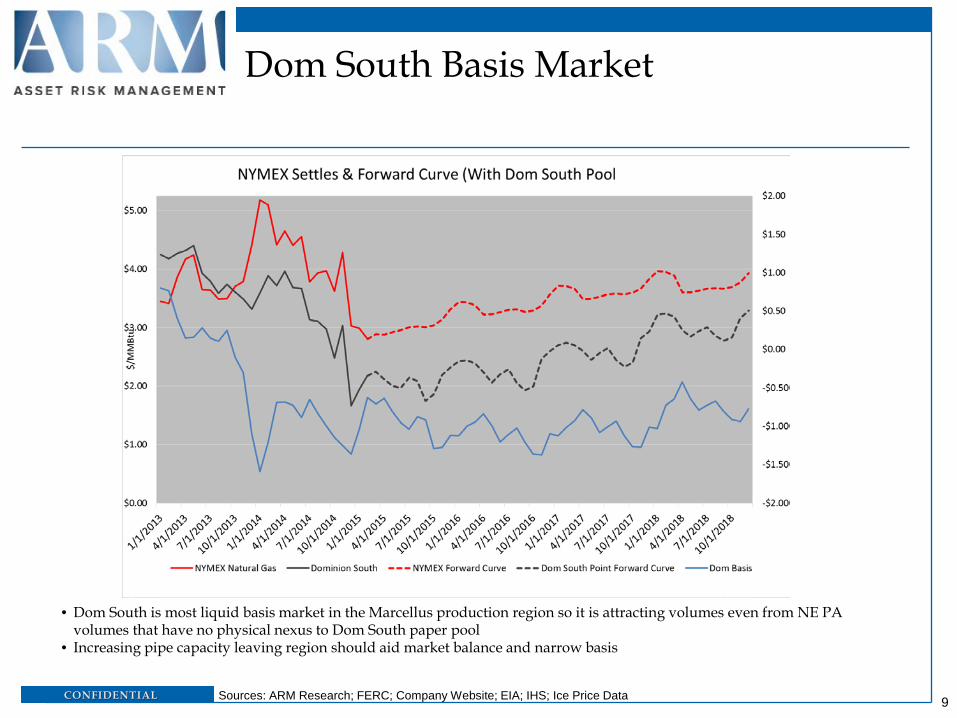

• Dom South is most liquid basis market in the Marcellus production region so it is attracting volumes even from NE PA volumes that have no physical nexus to Dom South paper pool

• Increasing pipe capacity leaving region should aid market balance and narrow basis

Dom South Basis Market

Sources: ARM Research; FERC; Company Website; EIA; IHS; Ice Price Data

10

Northeast Balances and Projects

• New projects in 2014 added an estimated 2.6 Bcfd of pipeline capacity out of the Northeast Texas Eastern’s TEAM 2014 project brings 600

MMcfd from Southwestern PA to the East Coast and Gulf Coast markets

Columbia’s Westside Expansion brings 440 MMcfd from Waynesburg to Leach

• Additional ~4.2 Bcfd of infrastructure expected to come online in 2015 led by REX’s 1.2 Bcfd East to West project REX’s East to West project will bring 1.2 Bcfd of

Northeast gas to Midwest interconnects and we believe full capability by as early as March

Transco’s Leidy Southeast will take 525 MMcfd of Marcellus gas to New York by November

TGP has a trio of pipelines expected to come online in Nov with a capacity of 1.1 Bcfd

We expect ~9.4 Bcfd additional capacity in 2016 led by: Energy Transfer’s 3.25 Bcfd Rover project REX’s 2.4 Bcfd Clarington West pipeline Columbia’s 1.5 Bcfd Leach/Rayne Xpress

Recently announced projects include: Jointly-owned 300 MMcfd Coast to Coast project

11

Northeast Infrastructure Update PA Gas Pushing to Midwest and Gulf

12

• Largest concentrated market in the U.S. on annual basis with average demand of 6+ Bcfd for coastal region from Beaumont to Corpus Christi

• HSC basis price has averaged very close to Henry Hub NYMEX pricing and is forecasted to become small premium year-round as demand strengthens and Marcellus Utica Projects push gas to Louisiana and Southeast

Houston Ship Channel (HSC)

Sources: ARM Research; FERC; EIA; IHS; Ice Price Data

Houston Ship Channel Pricing Region

13

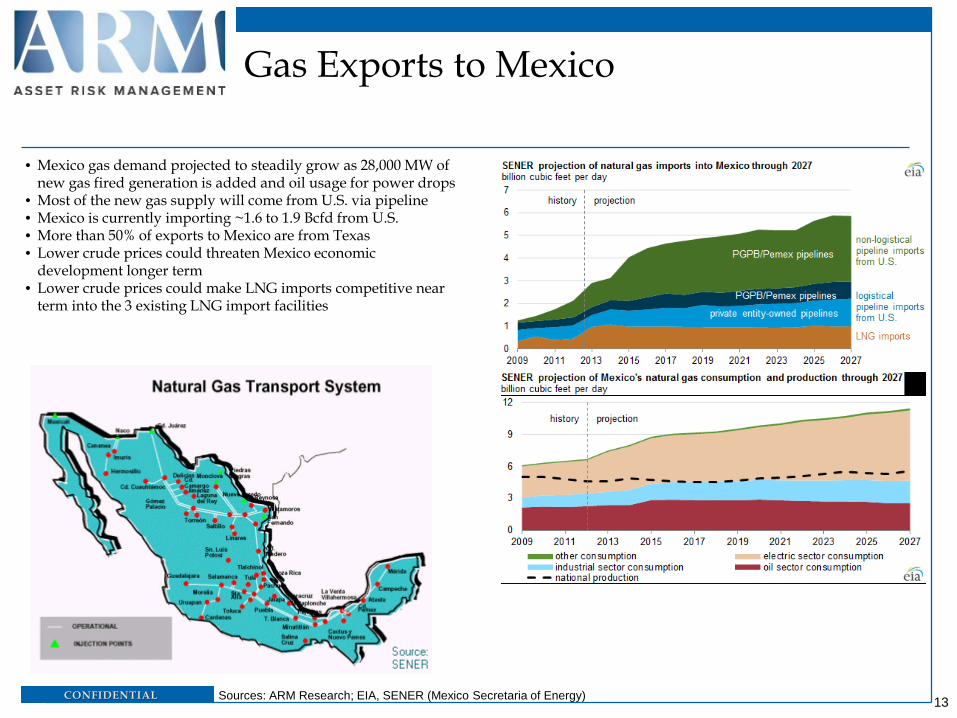

• Mexico gas demand projected to steadily grow as 28,000 MW of new gas fired generation is added and oil usage for power drops

• Most of the new gas supply will come from U.S. via pipeline • Mexico is currently importing ~1.6 to 1.9 Bcfd from U.S. • More than 50% of exports to Mexico are from Texas • Lower crude prices could threaten Mexico economic

development longer term • Lower crude prices could make LNG imports competitive near

term into the 3 existing LNG import facilities

Gas Exports to Mexico

Sources: ARM Research; EIA, SENER (Mexico Secretaria of Energy)

14

• ARM is tracking 100+ gas intensive industrial projects; the vast majority are petrochemical based

• American Chemistry Council update to their shale gas competitive study shows 197 U.S. projects and $125 billion investment as of 9/30/2014

• U.S. investments driven by competitive pricing of NGL’s and natural gas versus Naphtha based ethylene cracking

• Other industrial projects for steel, tubular goods, and not petchem are also primarily coming to the U.S. Gulf Coast, especially Texas region [HSC gas pricing]

• Wide range of potential gas demand from these projects, but cumulatively above 3 Bcfd by 2020 along Gulf Coast

Industrial Projects along Gulf Coast and Power Burn in Texas

Sources: ARM Research; American Chemistry Council; FERC

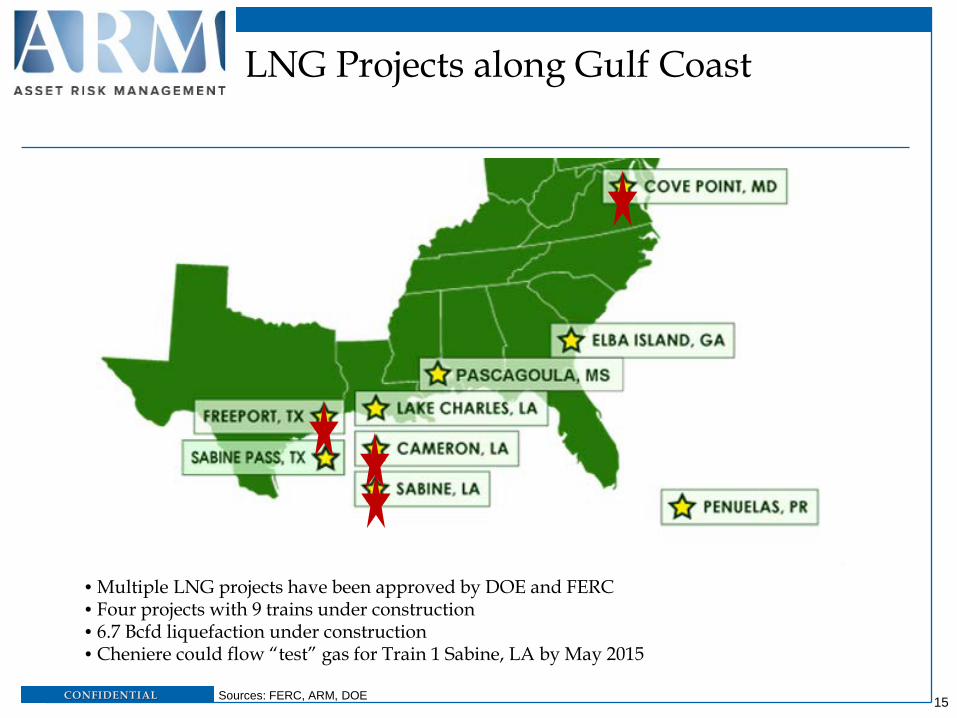

15

• Multiple LNG projects have been approved by DOE and FERC • Four projects with 9 trains under construction • 6.7 Bcfd liquefaction under construction • Cheniere could flow “test” gas for Train 1 Sabine, LA by May 2015

LNG Projects along Gulf Coast

Sources: FERC, ARM, DOE

16

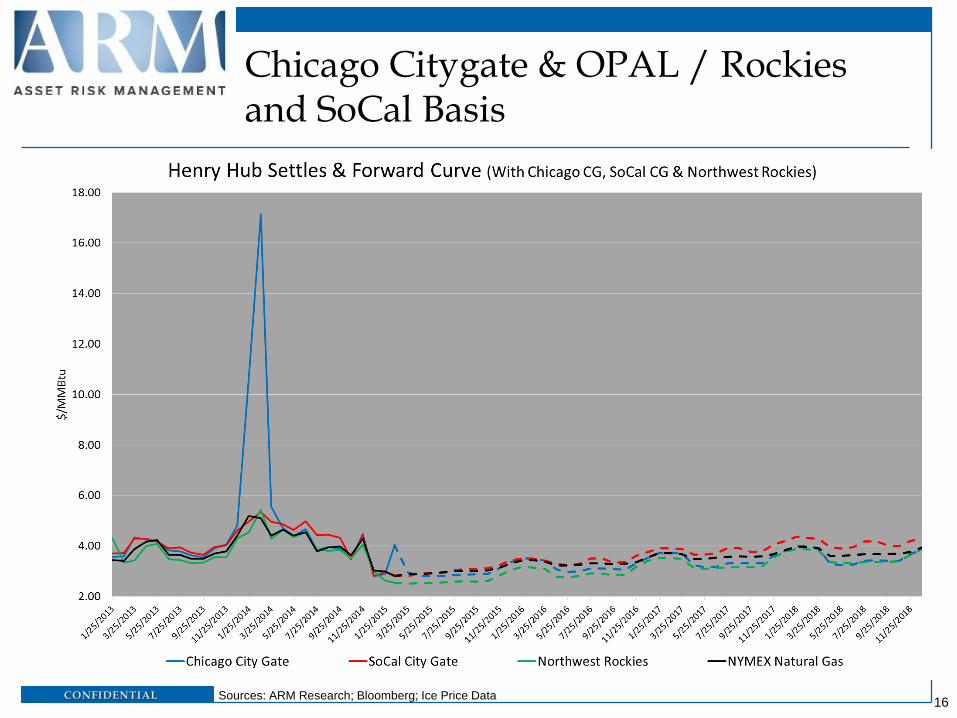

Chicago Citygate & OPAL / Rockies and SoCal Basis

Sources: ARM Research; Bloomberg; Ice Price Data

17

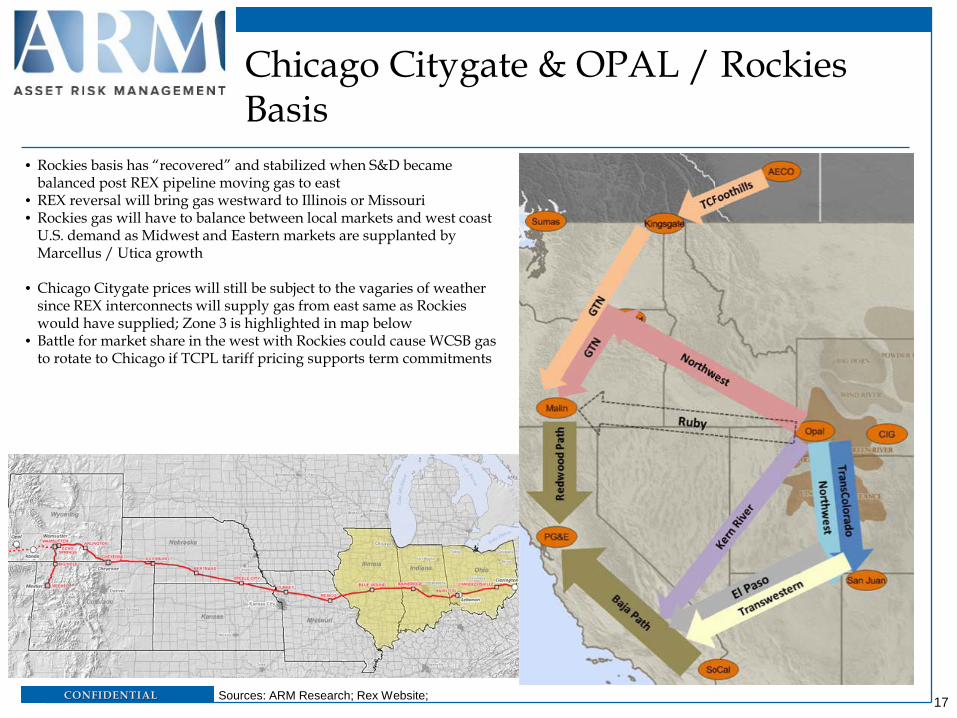

• Rockies basis has “recovered” and stabilized when S&D became balanced post REX pipeline moving gas to east

• REX reversal will bring gas westward to Illinois or Missouri • Rockies gas will have to balance between local markets and west coast

U.S. demand as Midwest and Eastern markets are supplanted by Marcellus / Utica growth

• Chicago Citygate prices will still be subject to the vagaries of weather since REX interconnects will supply gas from east same as Rockies would have supplied; Zone 3 is highlighted in map below

• Battle for market share in the west with Rockies could cause WCSB gas to rotate to Chicago if TCPL tariff pricing supports term commitments

Chicago Citygate & OPAL / Rockies Basis

Sources: ARM Research; Rex Website;

18

• ARM’s gas production outlook relies upon Genscape’s Spring Rock Production Forecast as its underlying driver • Production forecast is price responsive and uses highest quality modeling techniques with frequent, and proven, back

testing calibrations • Genscape has other natural gas related products; Analyst, Basis Reports, infrastructure portal, real-time flow data, and

gas storage estimates • Sub-products tie out public companies production versus their published guidance estimates

Contact: www.Genscape.com [email protected] 281-566-6640 (Sugar Land / Houston Office Main Number)

Spring Rock Production – Genscape Natural Gas Products