2012 natural gas market outlook

TRANSCRIPT

© 2005 San Diego Gas and Electric and Southern California Gas Company. All copyright and trademark rights reserved

This information is provided solely for informational purposes. Although Southern California Gas Co. (SoCalGas) has used reasonable

efforts to assure its accuracy, no representation is made that the contents are free from error or suitable for use for any particular purpose.

SoCalGas assumes no responsibility for use of, or reliance on, this information by any party, and specifically advise such parties to discuss

any decisions or actions related hereto with their own advisors and experts.

2012 NATURAL GAS MARKET OUTLOOK

Marjorie Schmidt-Pines, Principal Regulatory Economic Advisor

Southern California Gas Company and SDG&E

Regulatory Affairs

January, 2012

2

Natural Gas Outlook

•U.S. shale gas resources drive increases U.S. production, lower prices, economic growth and lower imports of natural gas

•Industrial and electric power use drives future demand growth

•Non-hydro renewables and natural gas are the fastest growing electricity generation sources

•Natural gas prices expected to continue to be low in 2012 due to mild winter and an expanded shale gas resource base

2001 to 2011 – A decade makes a difference

3 Source: LDC Forum, Exxon Mobil,, October, 2011

Factors impacting Natural Gas Growth

4 Source: LDC Forum, Exxon Mobil, October, 2011

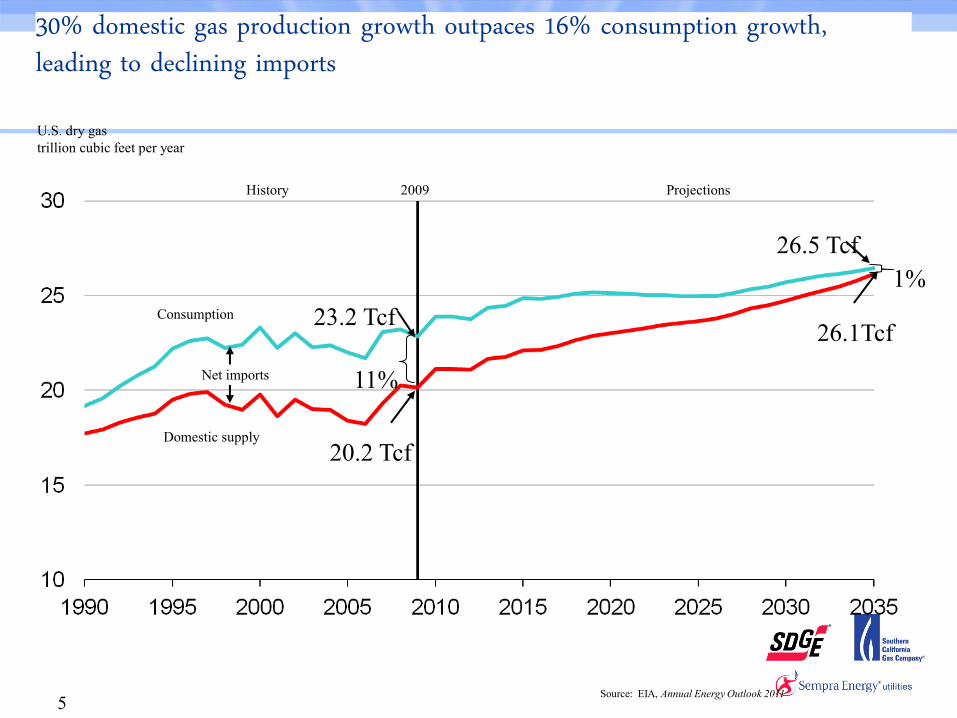

5

30% domestic gas production growth outpaces 16% consumption growth, leading to declining imports

Consumption

Domestic supply

Net imports

Projections History

1%

11%

Source: EIA, Annual Energy Outlook 2011

2009

U.S. dry gas

trillion cubic feet per year

23.2 Tcf 26.1Tcf

26.5 Tcf

20.2 Tcf

Horizontal drilling and hydraulic fracturing

6 Source: ProPublica,

http://www.propublica.org/special/hydraulic-fracturing-national

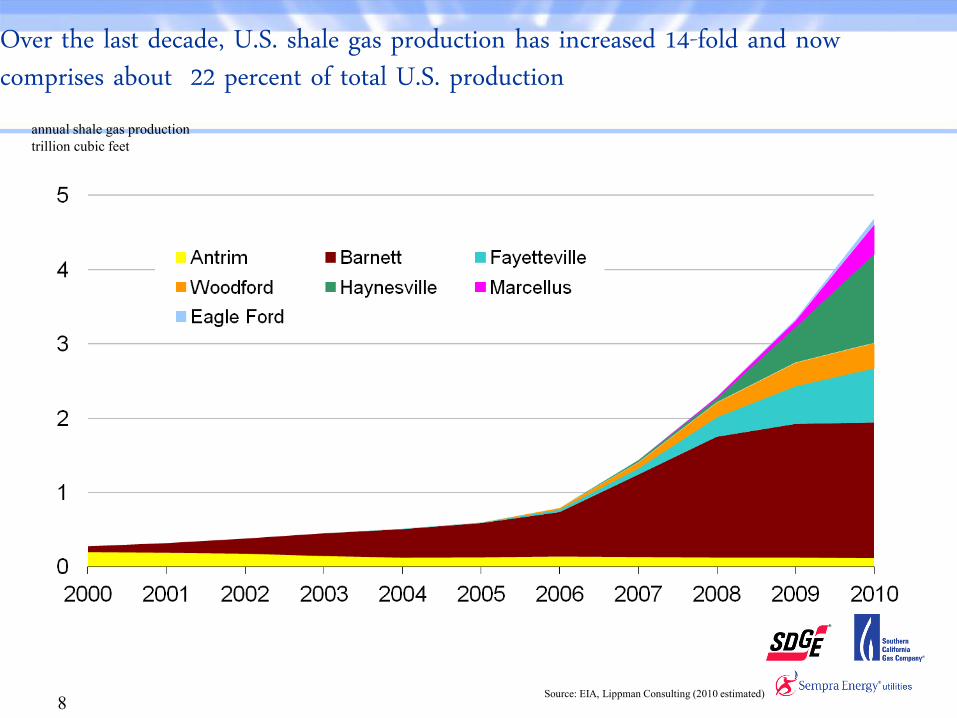

Success in the Barnett prompted companies to look at other shale formations in the United States

7

Over the last decade, U.S. shale gas production has increased 14-fold and now comprises about 22 percent of total U.S. production

Source: EIA, Lippman Consulting (2010 estimated)

annual shale gas production

trillion cubic feet

8

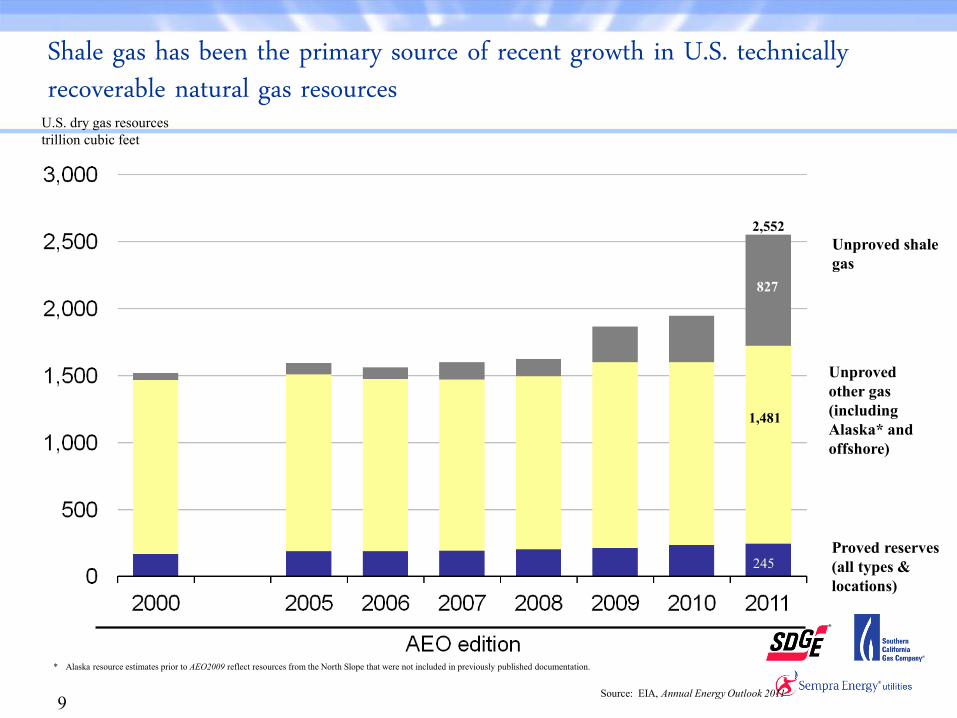

9

Shale gas has been the primary source of recent growth in U.S. technically recoverable natural gas resources

U.S. dry gas resources

trillion cubic feet

Unproved shale

gas

Unproved

other gas

(including

Alaska* and

offshore)

Proved reserves

(all types &

locations)

* Alaska resource estimates prior to AEO2009 reflect resources from the North Slope that were not included in previously published documentation.

Source: EIA, Annual Energy Outlook 2011

827

1,481

2,552

245

10

Four-fold increase in shale gas production offsets declines

in other U.S. supply, meeting consumption growth and

lowering import needs

11

Spurring Economic Growth

Source: LDC Forum, Exxon Mobil,, October, 2011, http://www.marcellus-

shale.us/

12

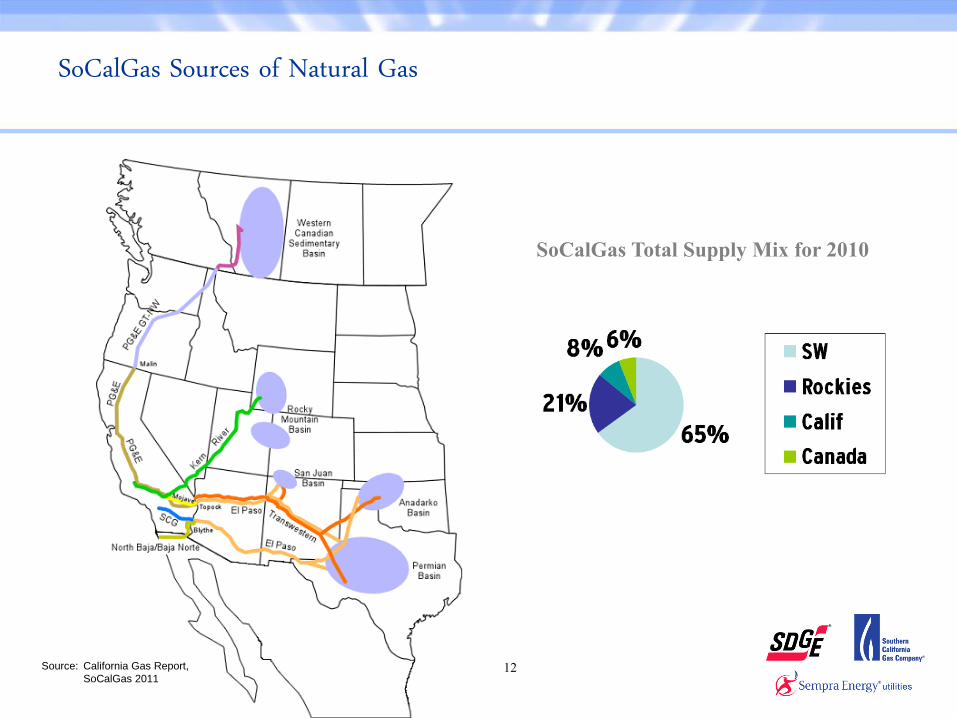

SoCalGas Sources of Natural Gas

Deliveries

(BCF)

2002 1012

2003 958

2004 995

2005 903

2006 959

SoCalGas Total Supply Mix for 2010

Source: California Gas Report,

SoCalGas 2011

13

U.S. dry gas consumption

trillion cubic feet per year

Commercial

Transportation** Residential

Central electric power

Industrial*

* Includes combined heat-and-power and lease and plant fuel. ** Includes pipeline fuel.

Source: EIA, Annual Energy Outlook 2011

2009

3%

14%

35%

18%

29%

3%

14%

32%

21%

30%

Projections History

Richard Newell, December 16, 2010

Natural gas consumption is quite dispersed; industrial and electric power use drives future demand growth

13

14

electricity net generation

trillion kilowatthours per year

Natural gas

Renewable

Projections History

Nuclear

Oil and other

Coal

20%

23%

25%

1% 1%

45%

43%

14% 10%

17%

The projected electricity mix gradually shifts to lower-carbon options, with generation from natural gas rising 37% and renewables rising 73%

Source: EIA, Annual Energy Outlook 2011

2009

Richard Newell, December 16, 2010 14

15

Southern California Gas Demand

0

200

400

600

800

1000

1200

2009 2010 2015 2020 2025 2030

Bc

f/Y

ea

r

Wholesale

EG

Noncore Non EG

Core Non Residential

Residential

Source: CGR 2010

16

U.S. Storage Expected to Remain High This Winter

Forecast

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

Jan 2007 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

U.S. Working Natural Gas in Storage

Deviation from 2006 - 2010 average

Storage level

Note: Colored band around storage levels represents the range between the minimum and maximum from Jan. 2006 - Dec. 2010.

billion cubic feet

Source: Short-Term Energy Outlook, December 2011

17

Weather has the most impact on spot natural gas prices.

Winter 2011/12

Source: NOAA

18

Natural Gas Price History

1

2

3

4

5

6

7

8

01

/01

06

/01

11

/01

04

/02

09

/02

02

/03

07

/03

12

/03

05

/04

10

/04

03

/05

08

/05

01

/06

06

/06

11

/06

04

/07

09

/07

02

/08

07

/08

12

/08

05

/09

10

/09

03

/10

08

/10

01

/11

06

/11

11

/11

$/m

mb

tu

CA AZ Border and SoCal Citygate - NGI Monthly Index Data Souce: NGI Bidweek Survey January 3, 2012

Southern Border, SoCalNGI Bidweek ($/Dth)

SoCal CitygateNGI Bidweek ($/Dth)

19

Oil vs Natural Gas Prices

0

5

10

15

20

25

Jan-0

4

Apr-

04

Jul-0

4

Oct-

04

Jan-0

5

Apr-

05

Jul-0

5

Oct-

05

Jan-0

6

Apr-

06

Jul-0

6

Oct-

06

Jan-0

7

Apr-

07

Jul-0

7

Oct-

07

Jan-0

8

Apr-

08

Jul-0

8

Oct-

08

Jan-0

9

Apr-

09

Jul-0

9

Oct-

09

Jan-1

0

Apr-

10

Jul-1

0

Oct-

10

Jan-1

1

Apr-

11

Jul-1

1

Oct-

11

Historical Oil Prices vs. Gas Prices Equivalent Unit Cost ($/MMBtu)

1 Barrel = 6.2 MMBtu Last Updated: 1/3/2012 Source: Source: Oil prices - EIA, CA/AZ Border Gas Price - ProphetX T:\oil vs gas.xls

CA/AZ Border NG Cash ($/MMBtu)

WTI Crude Equiv ($/MMBtu)

20

While Gas Prices Have Fluctuated: SoCalGas’ Transportation Costs Have Been Flat

$0.00 $1.00 $2.00 $3.00 $4.00 $5.00 $6.00 $7.00 $8.00 $9.00

$/m

mb

tu

Core Transport Noncore Transport

Core Gas Cost CA Border Index

`

Transport costs are the Volumetric & Customer Charge.

Core GN10 @ 100,000th/year and Noncore GTF/I3-D @ 1.5MMth/year.

Core Gas Cost is SCG’s core procurement rate and CA Border Index is Natural Gas Intelligence Index

21

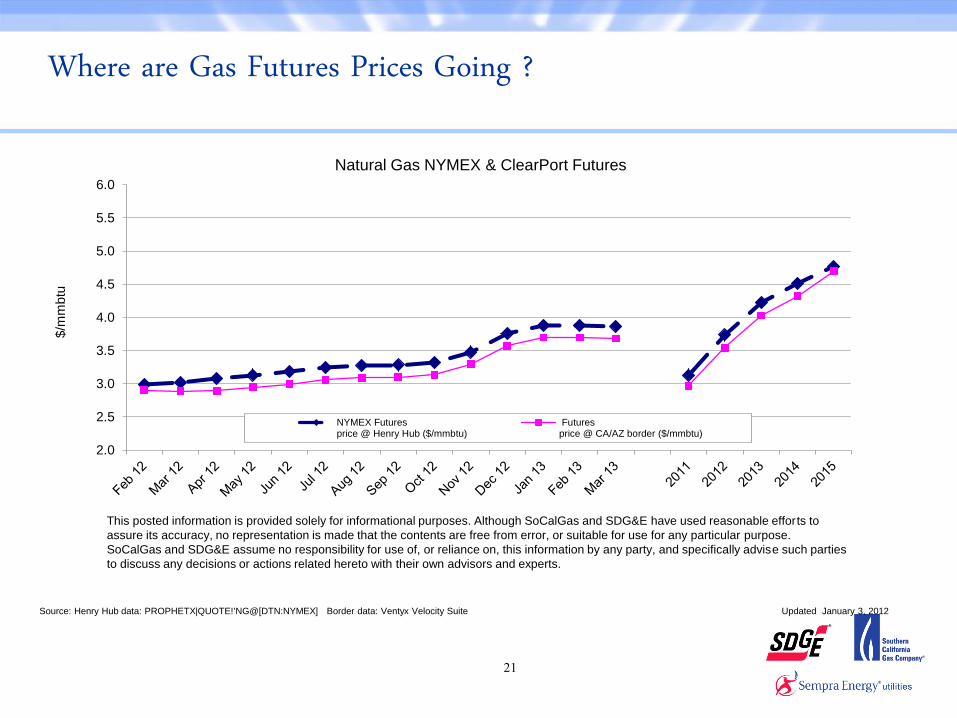

Where are Gas Futures Prices Going ?

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

$/m

mbtu

NYMEX Futuresprice @ Henry Hub ($/mmbtu)

Futuresprice @ CA/AZ border ($/mmbtu)

Natural Gas NYMEX & ClearPort Futures

Source: Henry Hub data: PROPHETX|QUOTE!'NG@[DTN:NYMEX] Border data: Ventyx Velocity Suite Updated January 3, 2012

This posted information is provided solely for informational purposes. Although SoCalGas and SDG&E have used reasonable efforts to

assure its accuracy, no representation is made that the contents are free from error, or suitable for use for any particular purpose.

SoCalGas and SDG&E assume no responsibility for use of, or reliance on, this information by any party, and specifically advise such parties

to discuss any decisions or actions related hereto with their own advisors and experts.

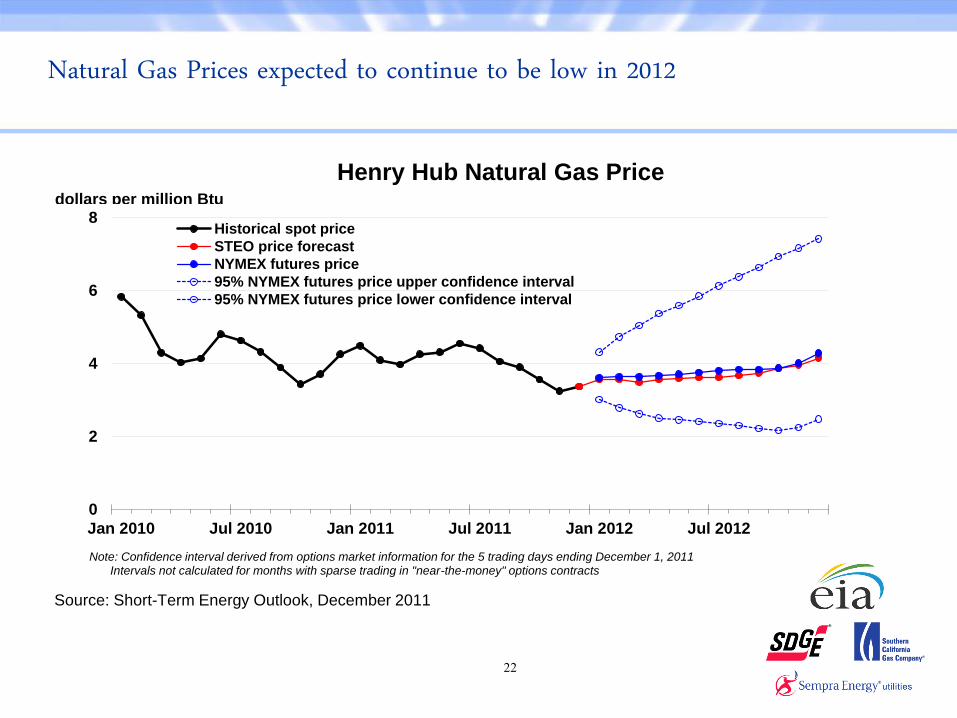

Natural Gas Prices expected to continue to be low in 2012

22

0

2

4

6

8

Jan 2010 Jul 2010 Jan 2011 Jul 2011 Jan 2012 Jul 2012

Henry Hub Natural Gas Price

Historical spot price

STEO price forecast

NYMEX futures price

95% NYMEX futures price upper confidence interval

95% NYMEX futures price lower confidence interval

Note: Confidence interval derived from options market information for the 5 trading days ending December 1, 2011 Intervals not calculated for months with sparse trading in "near-the-money" options contracts

dollars per million Btu

Source: Short-Term Energy Outlook, December 2011

23

• Shale gas drives growth in natural gas production, economy and reduces reliance on imported gas.

• Higher demand expected for U.S. gas fired electric generation and industrial demand.

• Natural gas prices much lower than oil prices.

• Natural Gas basis differences at various hubs diminished, driven by shale production increase in the east and new pipelines added.

• Natural gas price projections for 2012 are lower than past years due to warmer winter and an expanded shale gas resource base.

North American Natural Gas Market

24

What Can You Do to Manage Energy Costs?

• Take advantage of energy efficiency programs. Call your Account Executive for technical support.

• Go to socalgas.com/business for support tools.

• If you transport your own gas, talk to your gas supplier to discuss supply and pricing strategies.

• Look for ways to conserve and be more energy efficient.

25

Thank you