national property market update september quarter

TRANSCRIPT

Dr. Andrew J. Wilson

Australian housing markets report

Dr Andrew Wilson – Chief Economist Domain GroupOctober 2017

Copyright 2017 Dr Andrew Wilson – all rights reserved

Dr Andrew J. Wilson

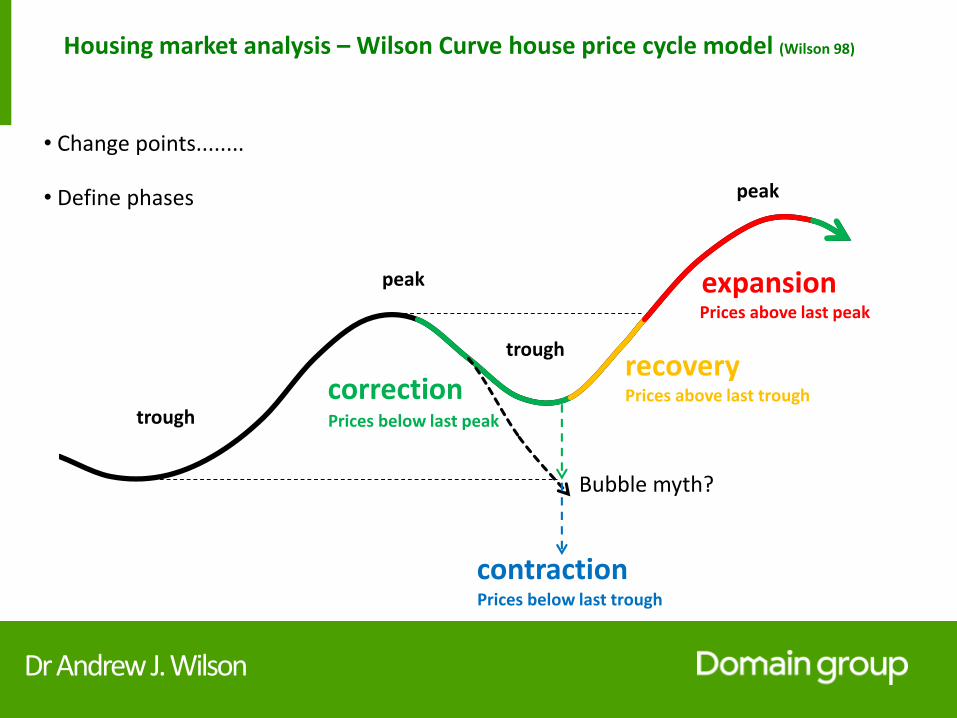

Australian capital city housing markets -synchronised, orderly growth and correction phases

Dr Andrew J. Wilson

expansion

trough

peak

trough

peak

correctionrecovery

contraction

• Change points........

• Define phases

Housing market analysis – Wilson Curve house price cycle model (Wilson 98)

Prices below last peak

Prices below last trough

Prices above last trough

Prices above last peak

Bubble myth?

Dr Andrew J. Wilson

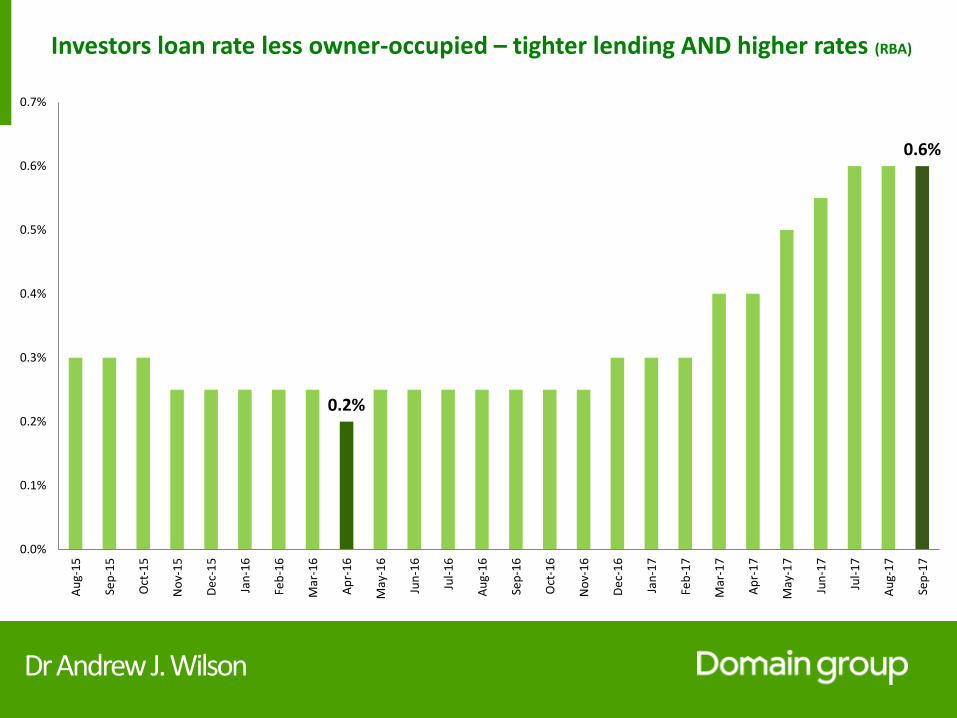

Investors loan rate less owner-occupied – tighter lending AND higher rates (RBA)

0.2%

0.6%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

De

c-1

5

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

De

c-1

6

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Dr Andrew J. Wilson

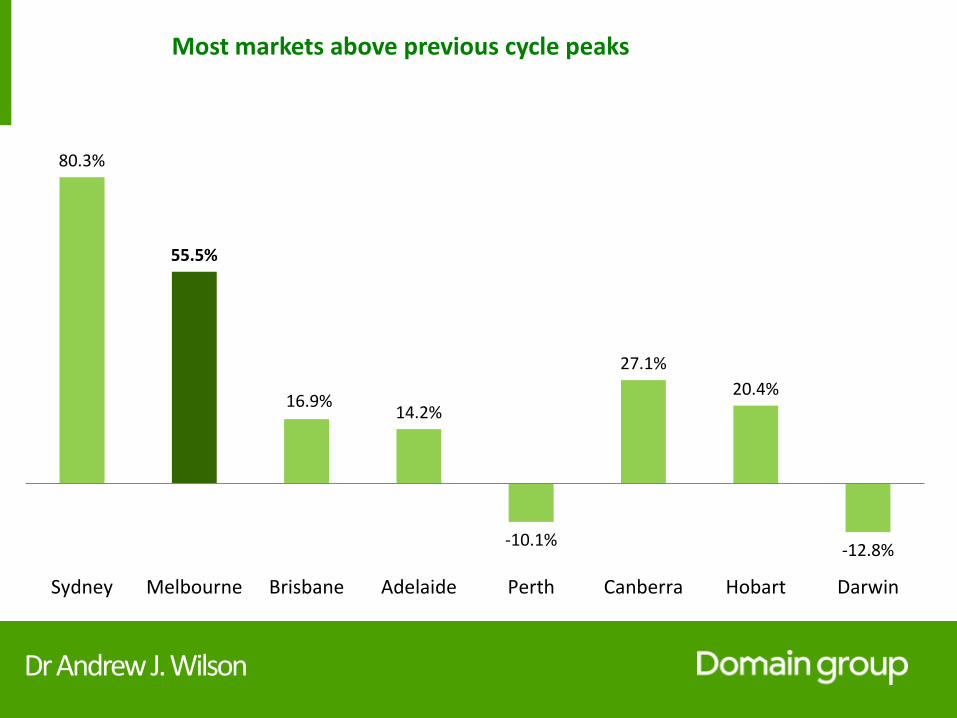

Most markets above previous cycle peaks

80.3%

55.5%

16.9%14.2%

-10.1%

27.1%

20.4%

-12.8%

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

Dr Andrew J. Wilson

Capital city house price cycle – Wilson Curve

correctionrecovery

expansion

contraction

Sydney PerthMelbourne

Canberra

Brisbane

Darwin

Adelaide

Hobart

Dr Andrew J. Wilson

Current quarter capital city prices

Dr Andrew J. Wilson

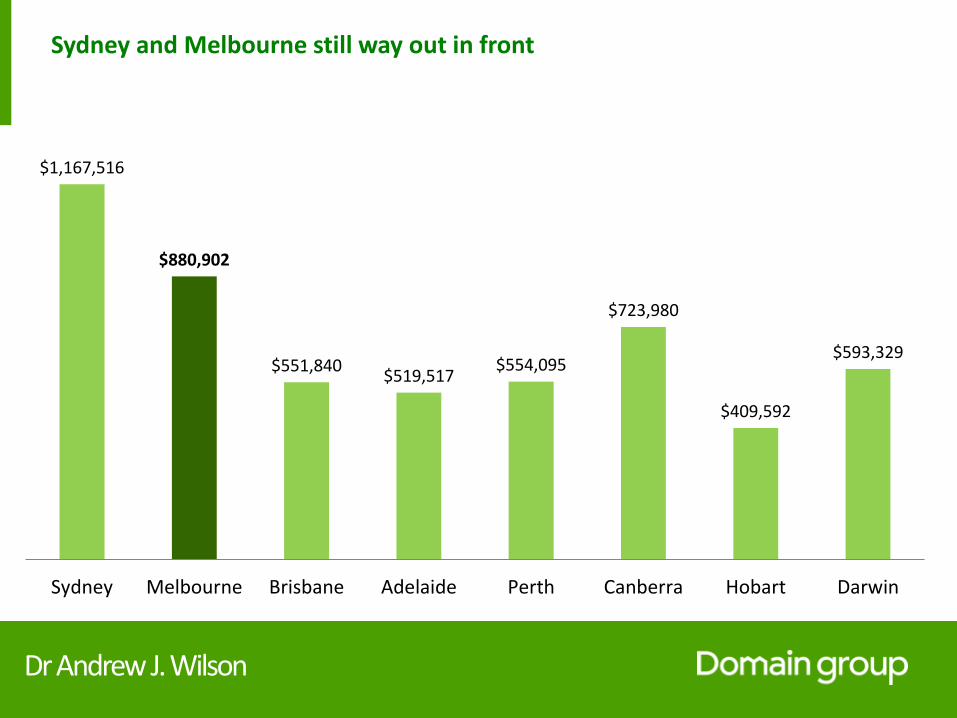

Sydney and Melbourne still way out in front

$1,167,516

$880,902

$551,840$519,517

$554,095

$723,980

$409,592

$593,329

Sydney Melbourne Brisbane Adelaide Perth Canberra Hobart Darwin

Dr Andrew J. Wilson

Rental Markets

Dr Andrew J. Wilson

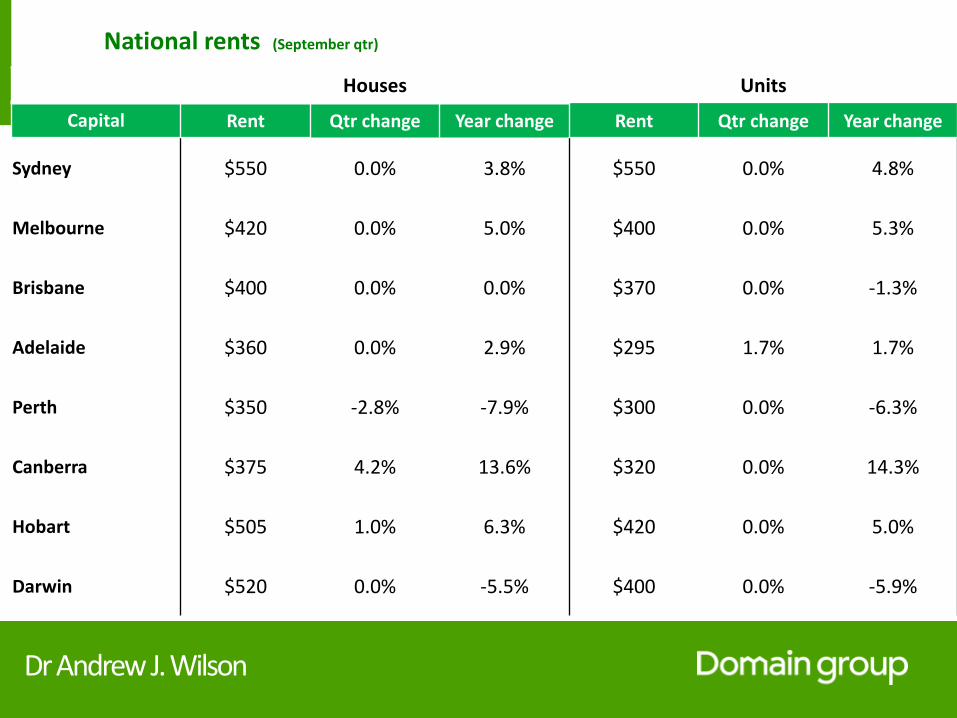

National rents (September qtr)

Houses Units

Capital Rent Qtr change Year change Rent Qtr change Year change

Sydney $550 0.0% 3.8% $550 0.0% 4.8%

Melbourne $420 0.0% 5.0% $400 0.0% 5.3%

Brisbane $400 0.0% 0.0% $370 0.0% -1.3%

Adelaide $360 0.0% 2.9% $295 1.7% 1.7%

Perth $350 -2.8% -7.9% $300 0.0% -6.3%

Canberra $375 4.2% 13.6% $320 0.0% 14.3%

Hobart $505 1.0% 6.3% $420 0.0% 5.0%

Darwin $520 0.0% -5.5% $400 0.0% -5.9%

Dr Andrew J. Wilson

National yields (September qtr)

Houses Units

Capital Gross yield Qtr change Year change Gross yield Qtr change Year change

Sydney 3.12% -1.1% -6.3% 3.86% 0.4% -2.6%

Melbourne 3.34% -1.2% -5.7% 4.47% -1.1% 1.6%

Brisbane 4.67% -0.5% -2.9% 4.93% -3.5% -1.2%

Adelaide 4.51% -1.5% -1.8% 5.18% -1.4% 0.6%

Perth 4.08% -1.1% -2.4% 4.37% -2.3% -5.7%

Canberra 5.29% -1.3% -4.1% 5.53% 0.7% -3.6%

Hobart 4.33% 0.4% -2.4% 5.77% 1.1% 3.7%

Darwin 4.88% -1.7% 3.9% 5.65% -0.8% 2.1%

Dr Andrew J. Wilson

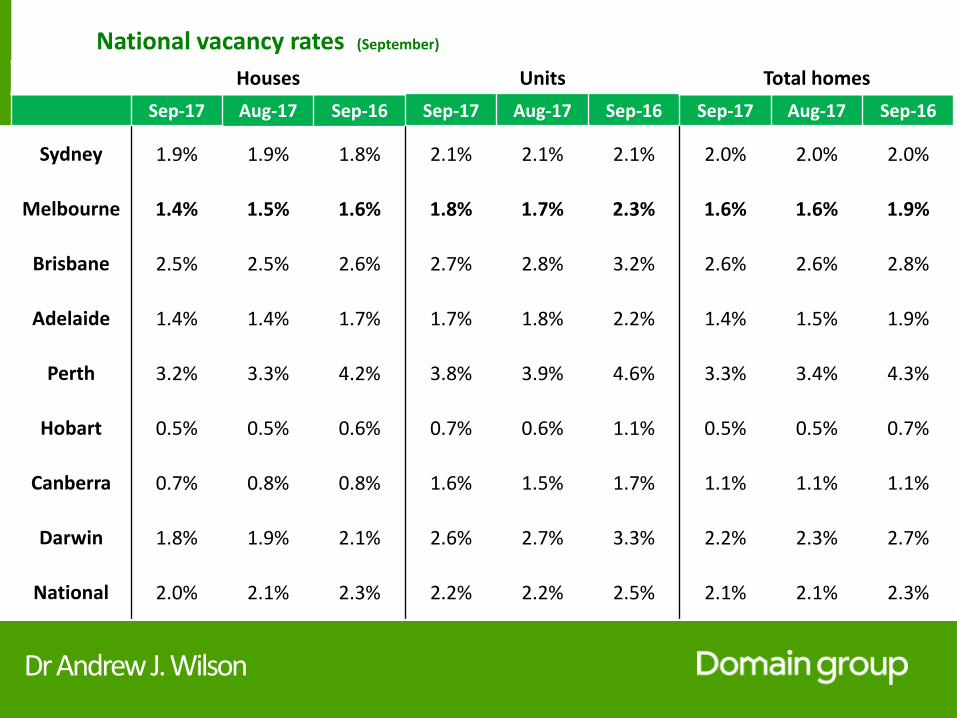

Houses Units Total homes

Sep-17 Aug-17 Sep-16 Sep-17 Aug-17 Sep-16 Sep-17 Aug-17 Sep-16

Sydney 1.9% 1.9% 1.8% 2.1% 2.1% 2.1% 2.0% 2.0% 2.0%

Melbourne 1.4% 1.5% 1.6% 1.8% 1.7% 2.3% 1.6% 1.6% 1.9%

Brisbane 2.5% 2.5% 2.6% 2.7% 2.8% 3.2% 2.6% 2.6% 2.8%

Adelaide 1.4% 1.4% 1.7% 1.7% 1.8% 2.2% 1.4% 1.5% 1.9%

Perth 3.2% 3.3% 4.2% 3.8% 3.9% 4.6% 3.3% 3.4% 4.3%

Hobart 0.5% 0.5% 0.6% 0.7% 0.6% 1.1% 0.5% 0.5% 0.7%

Canberra 0.7% 0.8% 0.8% 1.6% 1.5% 1.7% 1.1% 1.1% 1.1%

Darwin 1.8% 1.9% 2.1% 2.6% 2.7% 3.3% 2.2% 2.3% 2.7%

National 2.0% 2.1% 2.3% 2.2% 2.2% 2.5% 2.1% 2.1% 2.3%

National vacancy rates (September)

Dr Andrew J. Wilson

Key price drivers

Dr Andrew J. Wilson

The future for house price growth?

....as usual depends on the economy

Key Drivers

Unemployment and jobs

Wages, incomes and profits

Interest rates

Tax policies

Stockmarket

Population growth

New home supply

Confidence

Dr Andrew J. Wilson

Interest rates and housing markets

Dr Andrew J. Wilson

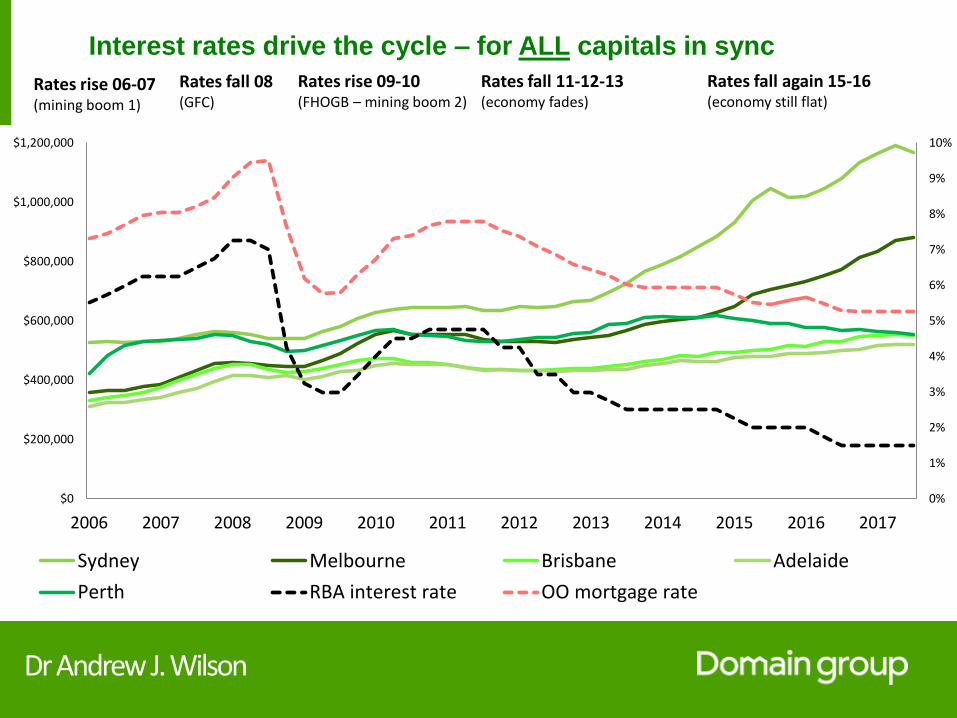

Interest rates drive the cycle – for ALL capitals in sync

Rates rise 09-10(FHOGB – mining boom 2)

Rates fall 11-12-13(economy fades)

Rates fall 08(GFC)

Rates rise 06-07(mining boom 1)

Rates fall again 15-16(economy still flat)

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sydney Melbourne Brisbane Adelaide

Perth RBA interest rate OO mortgage rate

Dr Andrew J. Wilson

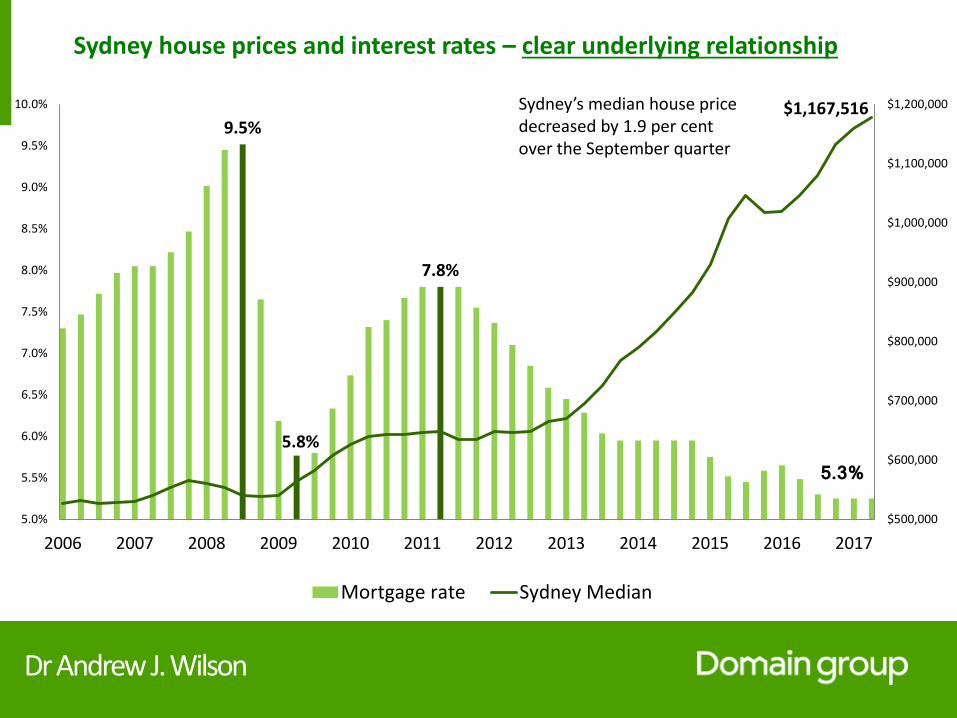

Sydney house prices and interest rates – clear underlying relationship

9.5%

5.8%

7.8%

5.3%

$1,167,516

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

$1,100,000

$1,200,000

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Mortgage rate Sydney Median

Sydney’s median house price decreased by 1.9 per cent over the September quarter

Dr Andrew J. Wilson

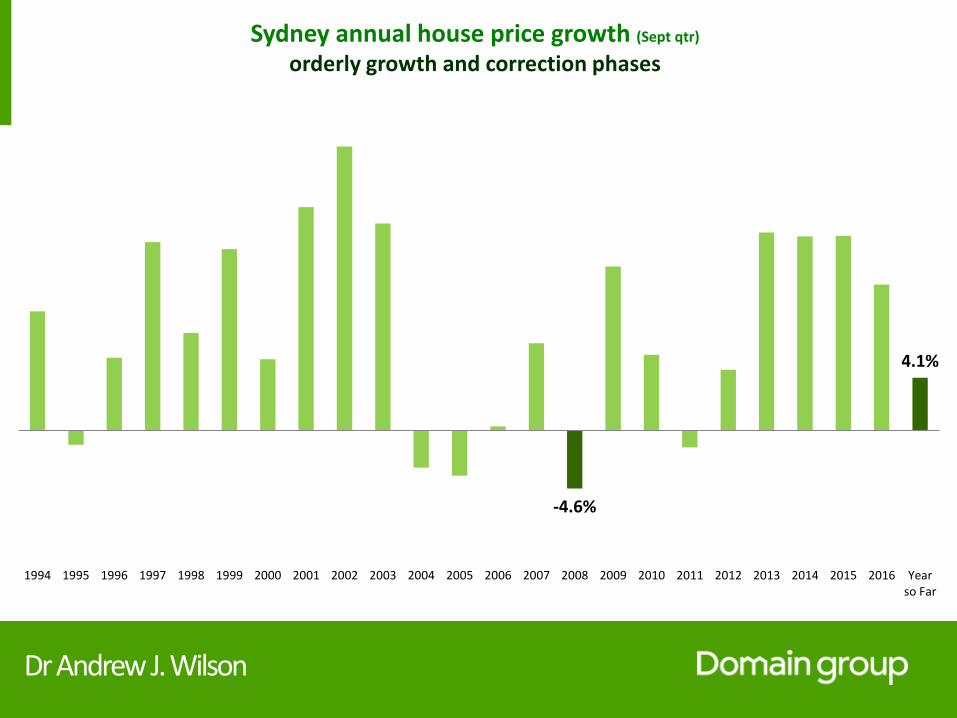

Sydney annual house price growth (Sept qtr)

orderly growth and correction phases

-4.6%

4.1%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Yearso Far

Dr Andrew J. Wilson

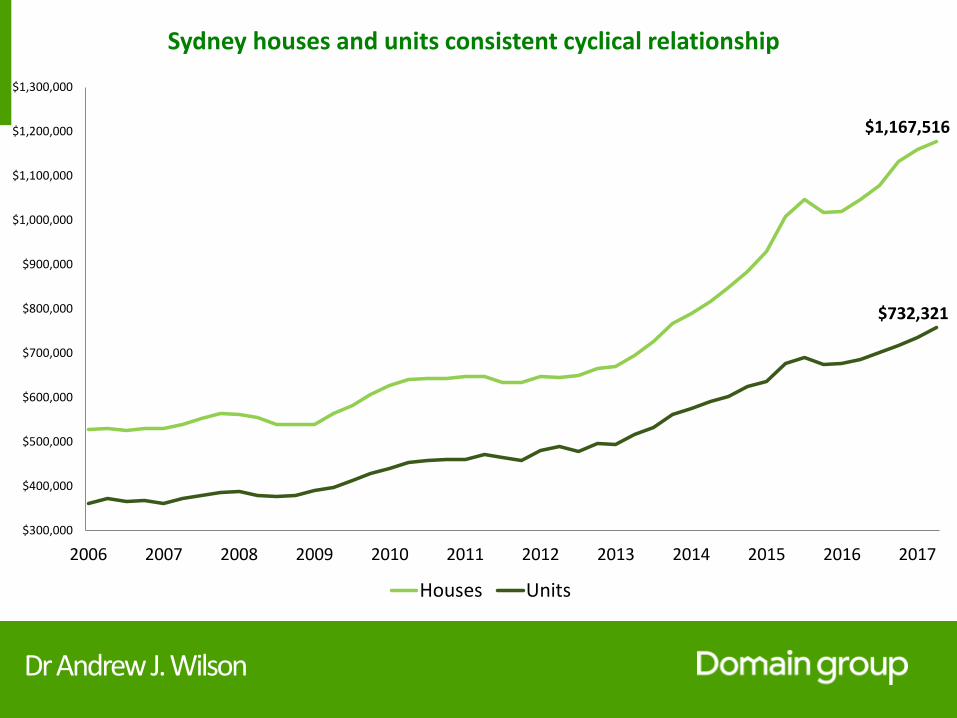

Sydney houses and units consistent cyclical relationship

$1,167,516

$732,321

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

$1,100,000

$1,200,000

$1,300,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Houses Units

Dr Andrew J. Wilson

Sydney gross house yields vs bank deposit rates - better returns (bank term deposit 1yr 10k)

2.3%

3.2%

2%

3%

4%

5%

6%

7%

8%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Term deposit House yield

Dr Andrew J. Wilson

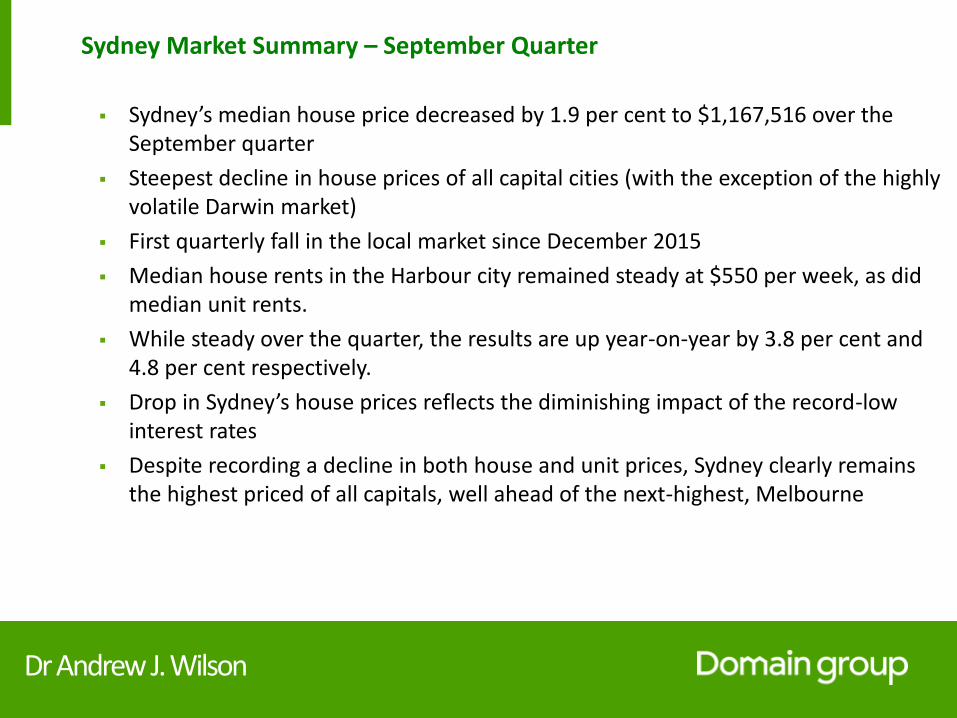

Sydney Market Summary – September Quarter

Sydney’s median house price decreased by 1.9 per cent to $1,167,516 over the September quarter

Steepest decline in house prices of all capital cities (with the exception of the highly volatile Darwin market)

First quarterly fall in the local market since December 2015

Median house rents in the Harbour city remained steady at $550 per week, as did median unit rents.

While steady over the quarter, the results are up year-on-year by 3.8 per cent and 4.8 per cent respectively.

Drop in Sydney’s house prices reflects the diminishing impact of the record-low interest rates

Despite recording a decline in both house and unit prices, Sydney clearly remains the highest priced of all capitals, well ahead of the next-highest, Melbourne

Dr Andrew J. Wilson

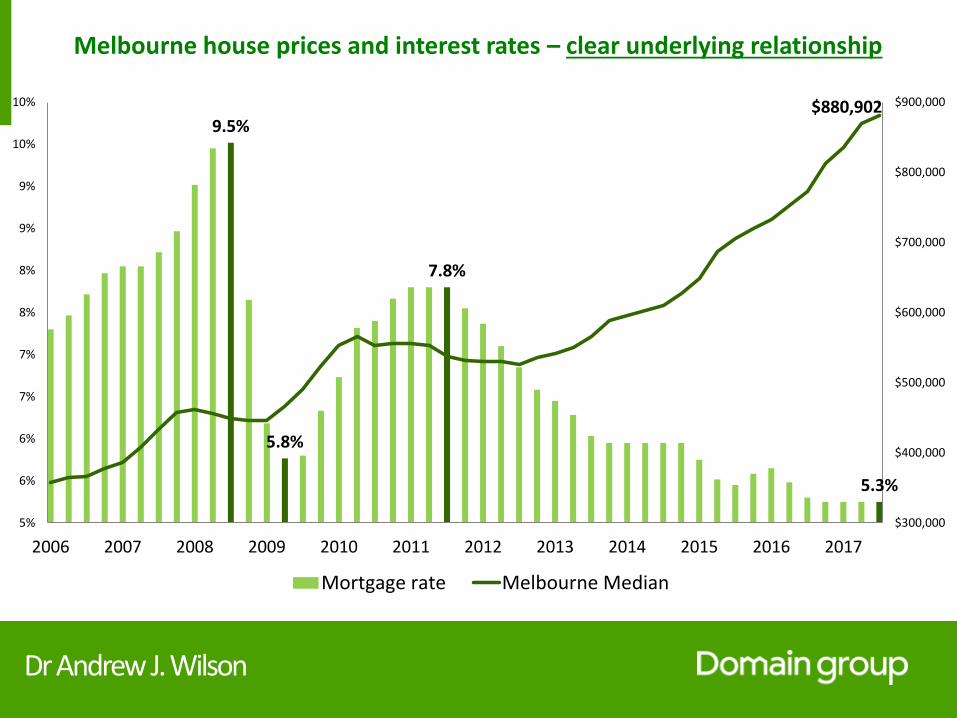

Melbourne house prices and interest rates – clear underlying relationship

9.5%

5.8%

7.8%

5.3%

$880,902

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

5%

6%

6%

7%

7%

8%

8%

9%

9%

10%

10%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Mortgage rate Melbourne Median

Dr Andrew J. Wilson

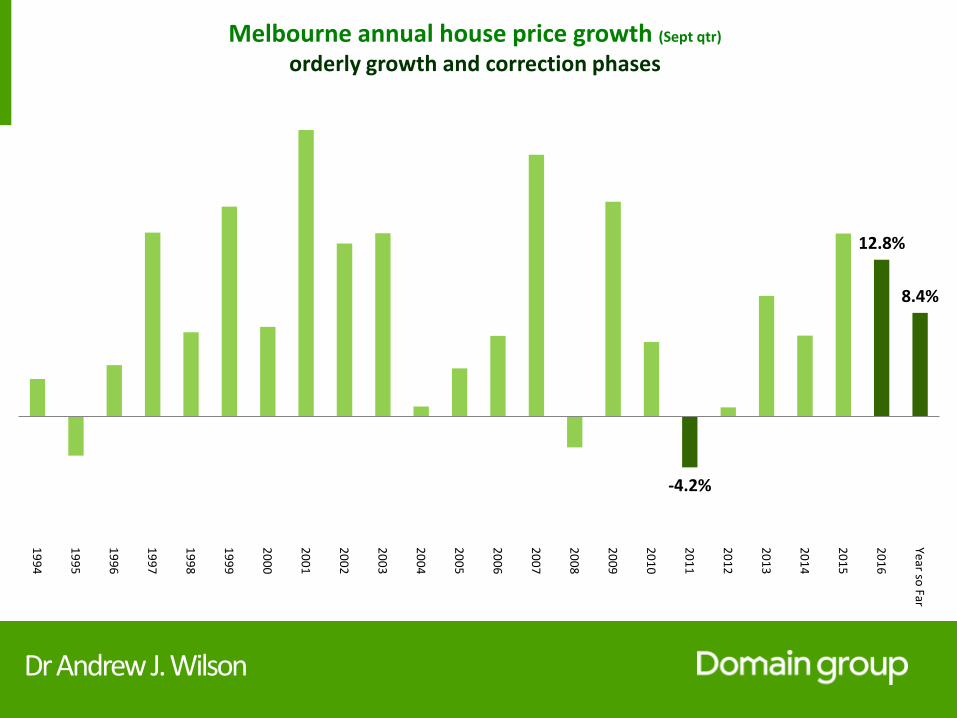

Melbourne annual house price growth (Sept qtr)

orderly growth and correction phases

-4.2%

12.8%

8.4%

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Year so Far

Dr Andrew J. Wilson

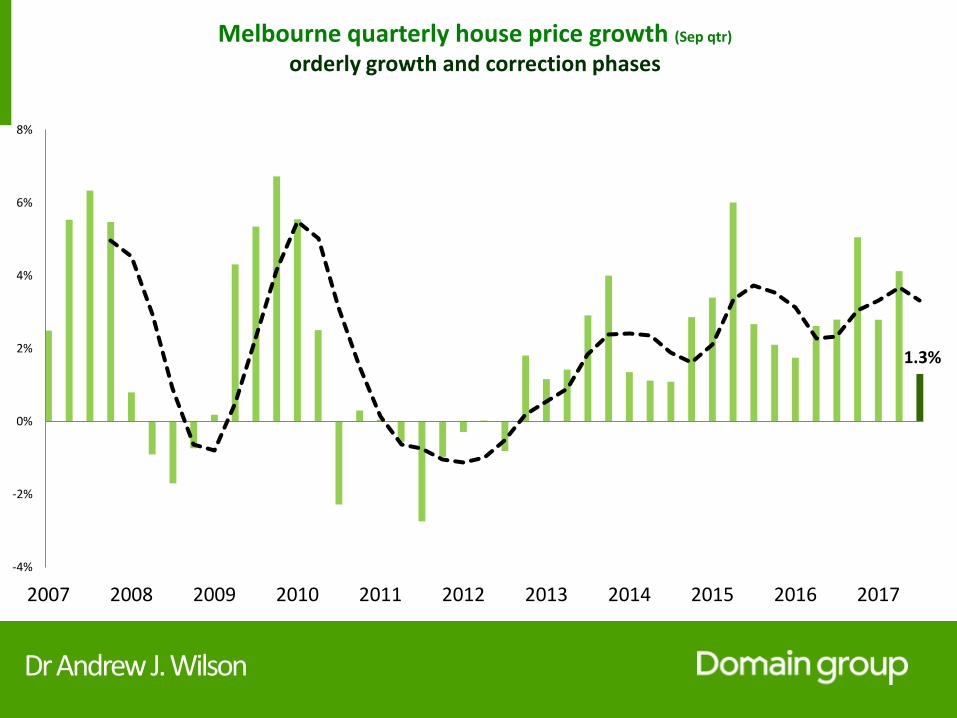

Melbourne quarterly house price growth (Sep qtr)

orderly growth and correction phases

1.3%

-4%

-2%

0%

2%

4%

6%

8%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Dr Andrew J. Wilson

Houses and units

Dr Andrew J. Wilson

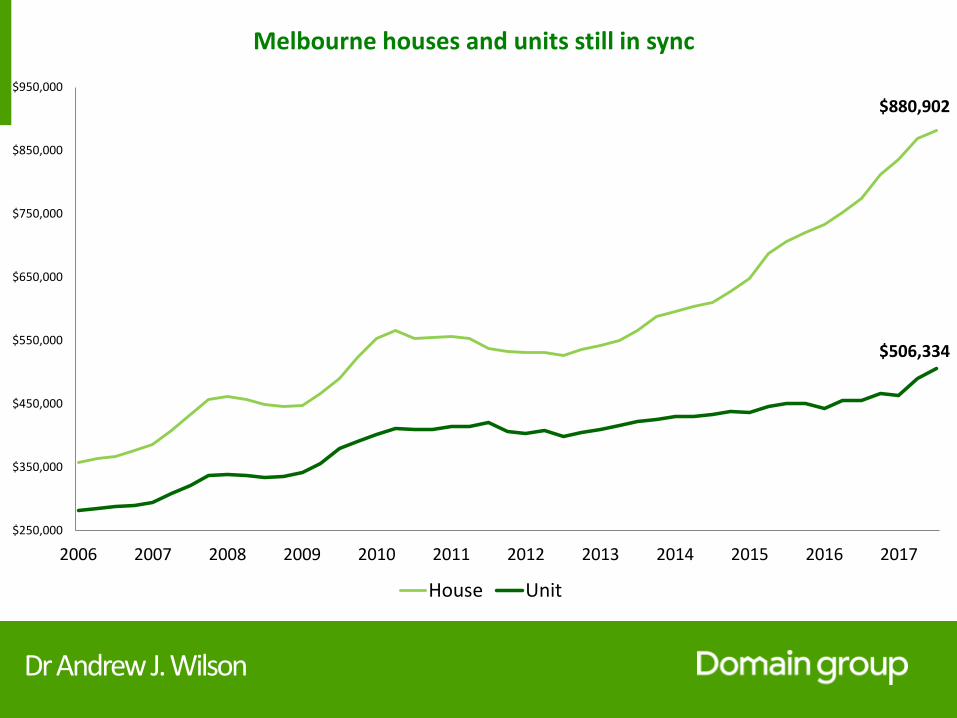

Melbourne houses and units still in sync

$880,902

$506,334

$250,000

$350,000

$450,000

$550,000

$650,000

$750,000

$850,000

$950,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

House Unit

Dr Andrew J. Wilson

Buyer types

Dr Andrew J. Wilson

Investor loan growth still up this year – FHB now rising (ABS this year to August vs last year VIC)

3.8%

12.3%

6.3%

11.8%

First home buyers Investors Changeover buyers Total

Dr Andrew J. Wilson

Housing supply

Dr Andrew J. Wilson

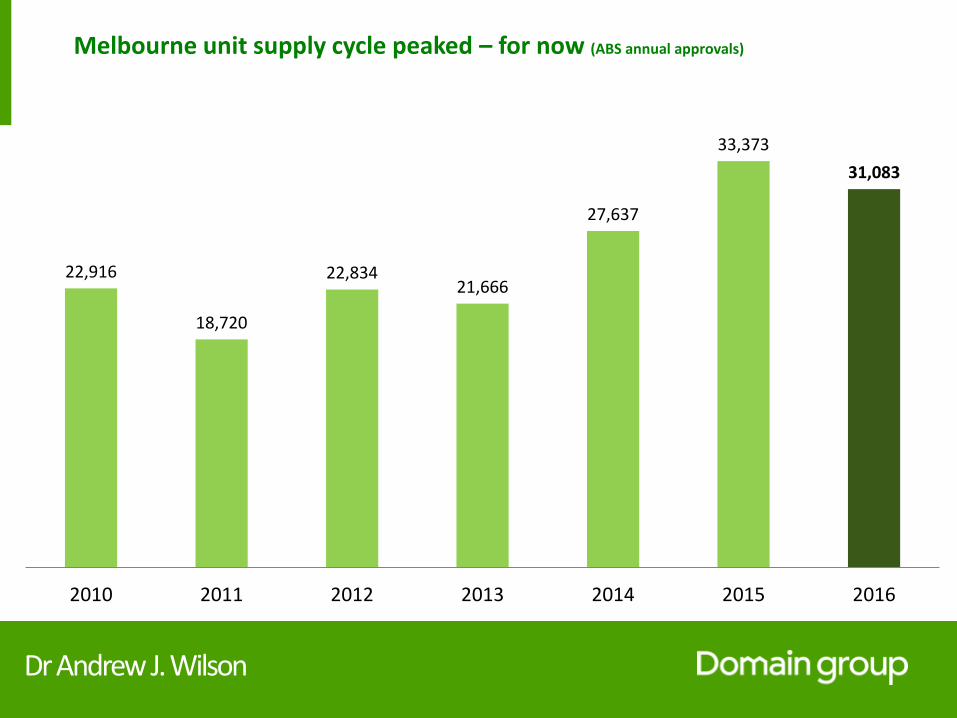

Melbourne unit supply cycle peaked – for now (ABS annual approvals)

22,916

18,720

22,83421,666

27,637

33,373

31,083

2010 2011 2012 2013 2014 2015 2016

Dr Andrew J. Wilson

Melbourne house supply cycle rising (ABS approvals)

2569 2613

0

500

1000

1500

2000

2500

3000

Jan-1

5

Feb

-15

Mar-1

5

Ap

r-15

May-1

5

Jun

-15

Jul-1

5

Au

g-15

Sep

-15

Oct-1

5

No

v-15

De

c-15

Jan-1

6

Feb

-16

Mar-1

6

Ap

r-16

May-1

6

Jun

-16

Jul-1

6

Au

g-16

Sep

-16

Oct-1

6

No

v-16

De

c-16

Jan-1

7

Feb

-17

Mar-1

7

Ap

r-17

May-1

7

Jun

-17

Jul-1

7

Au

g-17

Dr Andrew J. Wilson

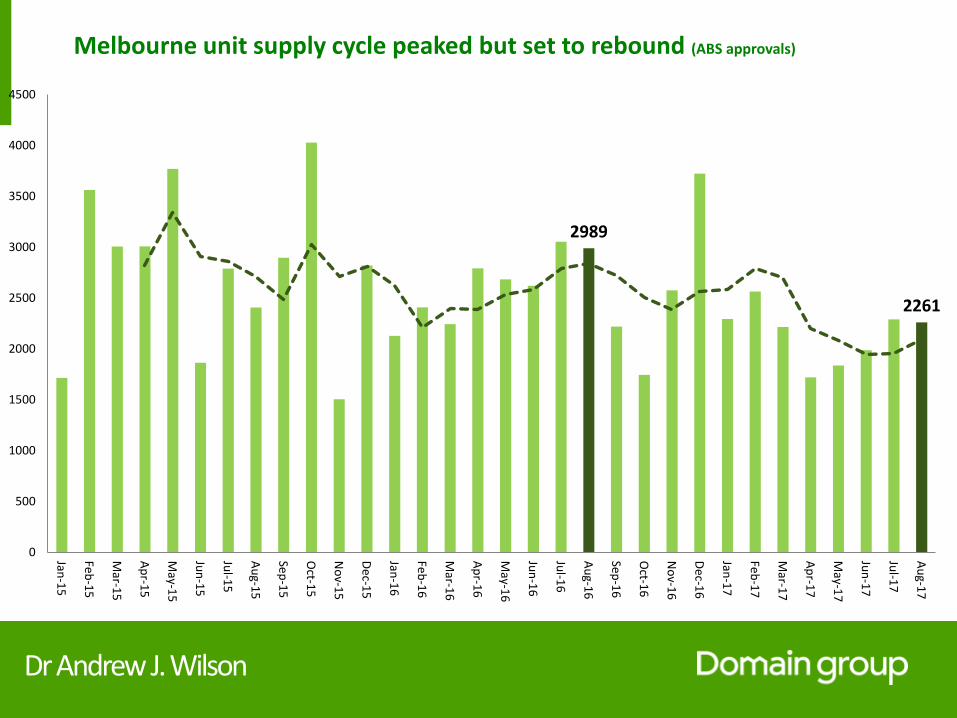

Melbourne unit supply cycle peaked but set to rebound (ABS approvals)

2989

2261

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Jan-1

5

Feb

-15

Mar-1

5

Ap

r-15

May-1

5

Jun

-15

Jul-1

5

Au

g-15

Sep

-15

Oct-1

5

No

v-15

De

c-15

Jan-1

6

Feb

-16

Mar-1

6

Ap

r-16

May-1

6

Jun

-16

Jul-1

6

Au

g-16

Sep

-16

Oct-1

6

No

v-16

De

c-16

Jan-1

7

Feb

-17

Mar-1

7

Ap

r-17

May-1

7

Jun

-17

Jul-1

7

Au

g-17

Dr Andrew J. Wilson

Housing demand

Dr Andrew J. Wilson

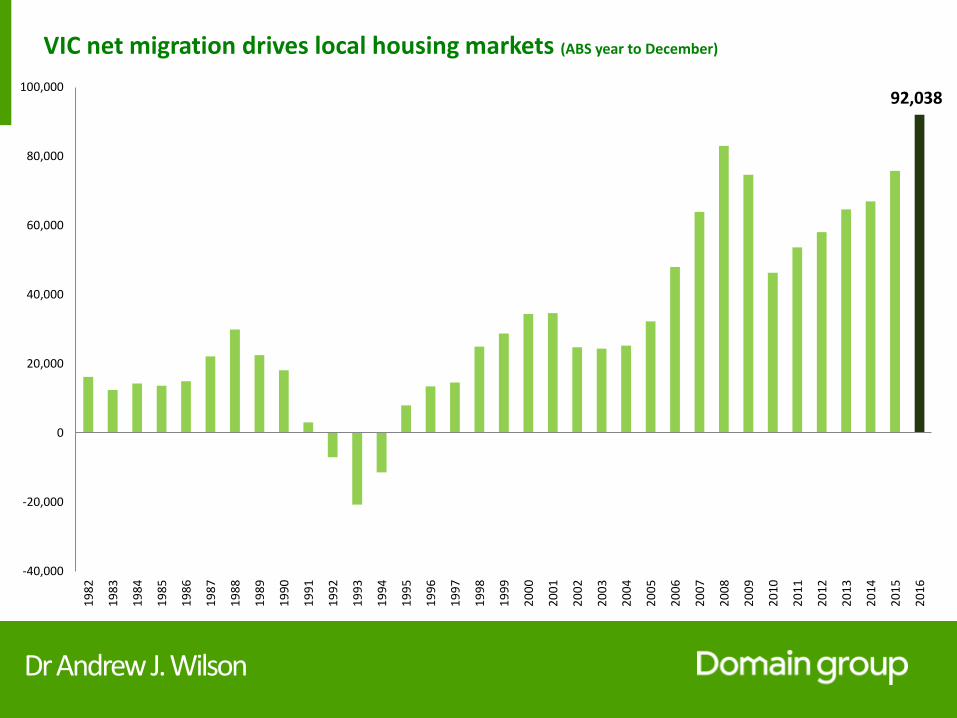

VIC net migration drives local housing markets (ABS year to December)

92,038

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,0001

98

2

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Dr Andrew J. Wilson

Melbourne unit market

Dr Andrew J. Wilson

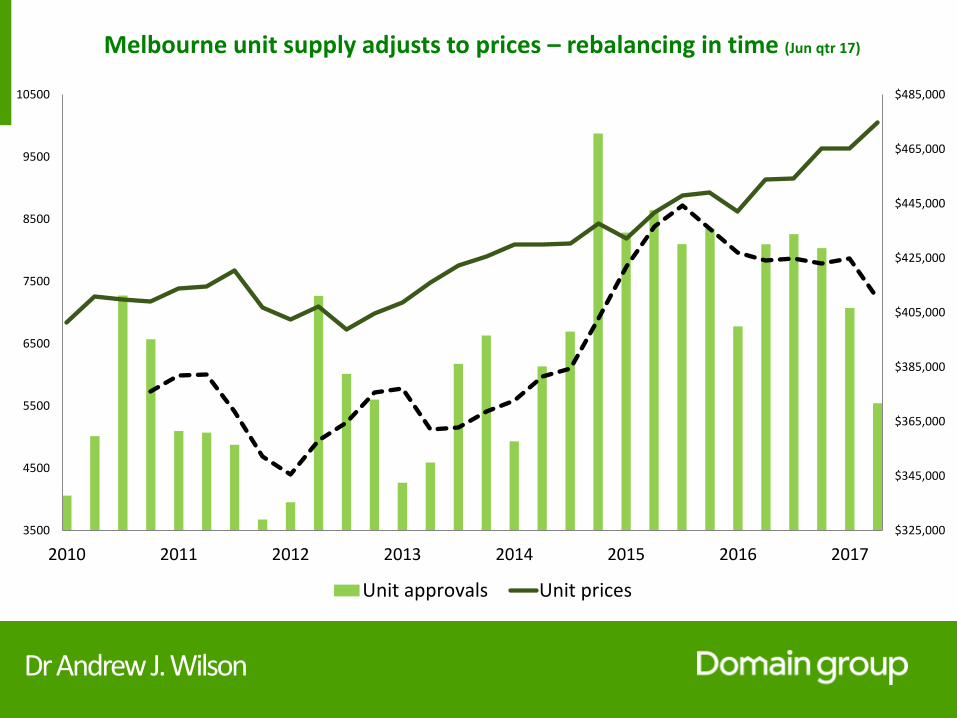

Melbourne unit supply adjusts to prices – rebalancing in time (Jun qtr 17)

$325,000

$345,000

$365,000

$385,000

$405,000

$425,000

$445,000

$465,000

$485,000

3500

4500

5500

6500

7500

8500

9500

10500

2010 2011 2012 2013 2014 2015 2016 2017

Unit approvals Unit prices

Dr Andrew J. Wilson

Melbourne market outlook 2017

Dr Andrew J. Wilson

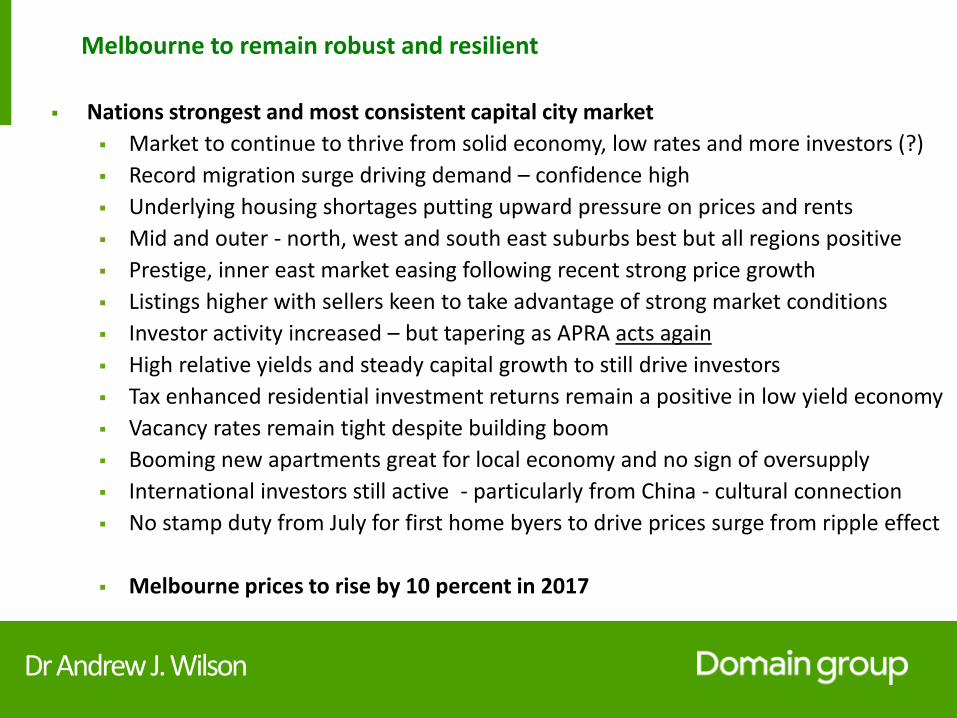

Melbourne to remain robust and resilient

Nations strongest and most consistent capital city market

Market to continue to thrive from solid economy, low rates and more investors (?)

Record migration surge driving demand – confidence high

Underlying housing shortages putting upward pressure on prices and rents

Mid and outer - north, west and south east suburbs best but all regions positive

Prestige, inner east market easing following recent strong price growth

Listings higher with sellers keen to take advantage of strong market conditions

Investor activity increased – but tapering as APRA acts again

High relative yields and steady capital growth to still drive investors

Tax enhanced residential investment returns remain a positive in low yield economy

Vacancy rates remain tight despite building boom

Booming new apartments great for local economy and no sign of oversupply

International investors still active - particularly from China - cultural connection

No stamp duty from July for first home byers to drive prices surge from ripple effect

Melbourne prices to rise by 10 percent in 2017

Dr Andrew J. Wilson

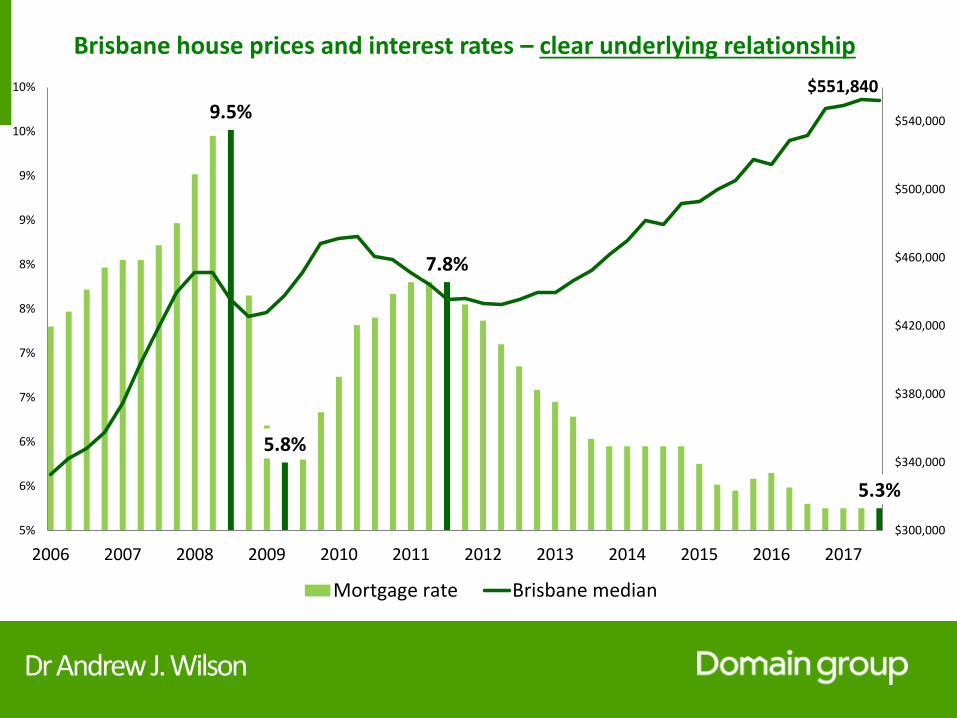

Brisbane house prices and interest rates – clear underlying relationship

9.5%

5.8%

7.8%

5.3%

$551,840

$300,000

$340,000

$380,000

$420,000

$460,000

$500,000

$540,000

5%

6%

6%

7%

7%

8%

8%

9%

9%

10%

10%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Mortgage rate Brisbane median

Dr Andrew J. Wilson

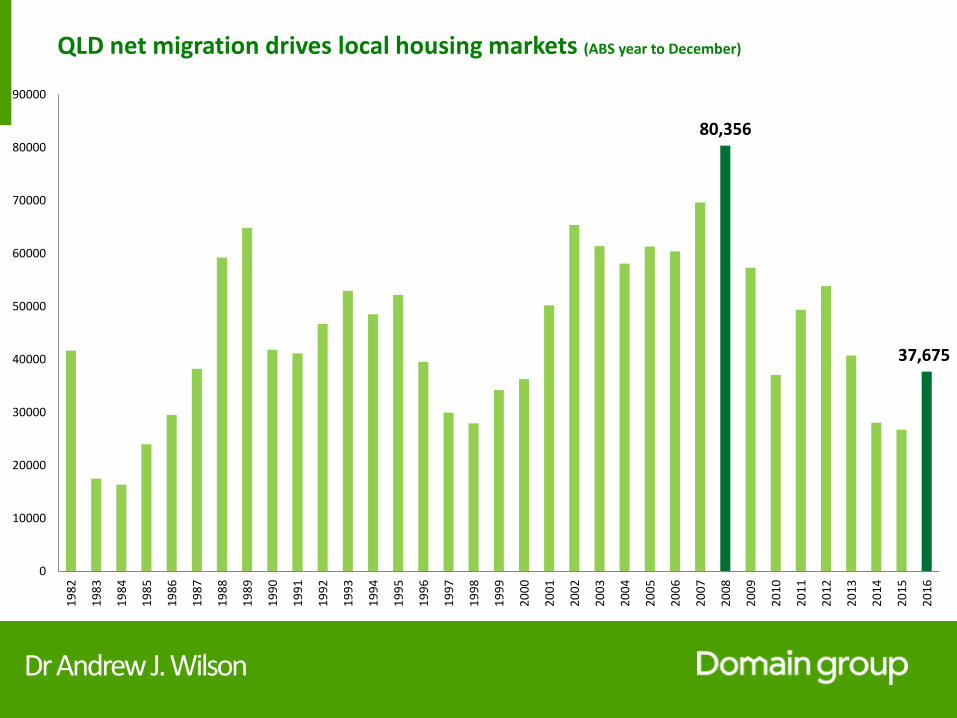

QLD net migration drives local housing markets (ABS year to December)

80,356

37,675

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Dr Andrew J. Wilson

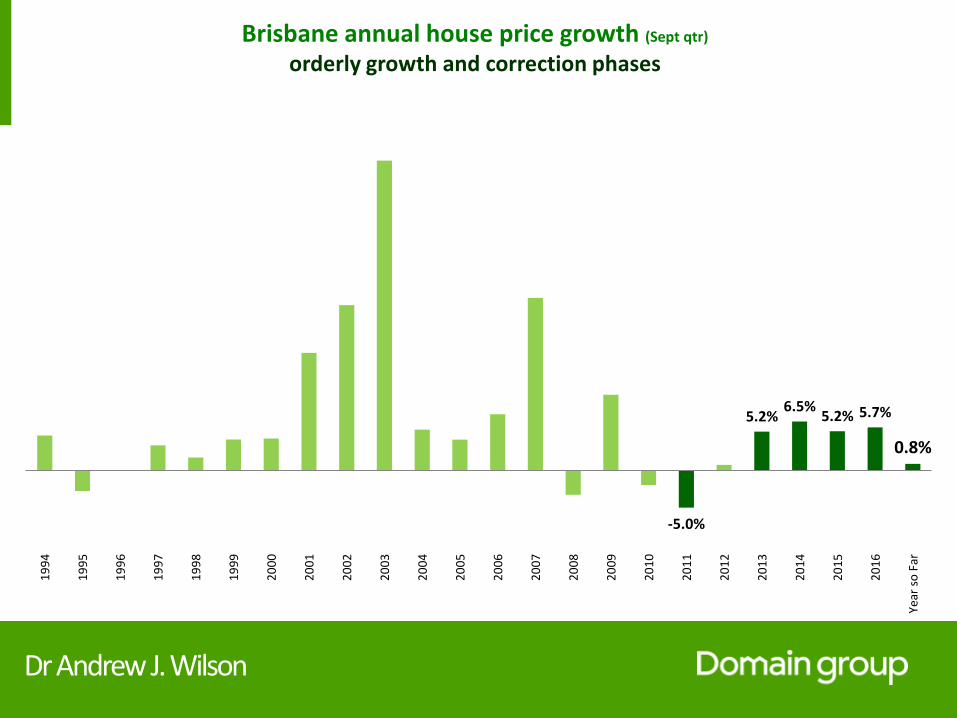

Brisbane annual house price growth (Sept qtr)

orderly growth and correction phases

-5.0%

5.2%6.5%

5.2% 5.7%

0.8%

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Year

so

Far

Dr Andrew J. Wilson

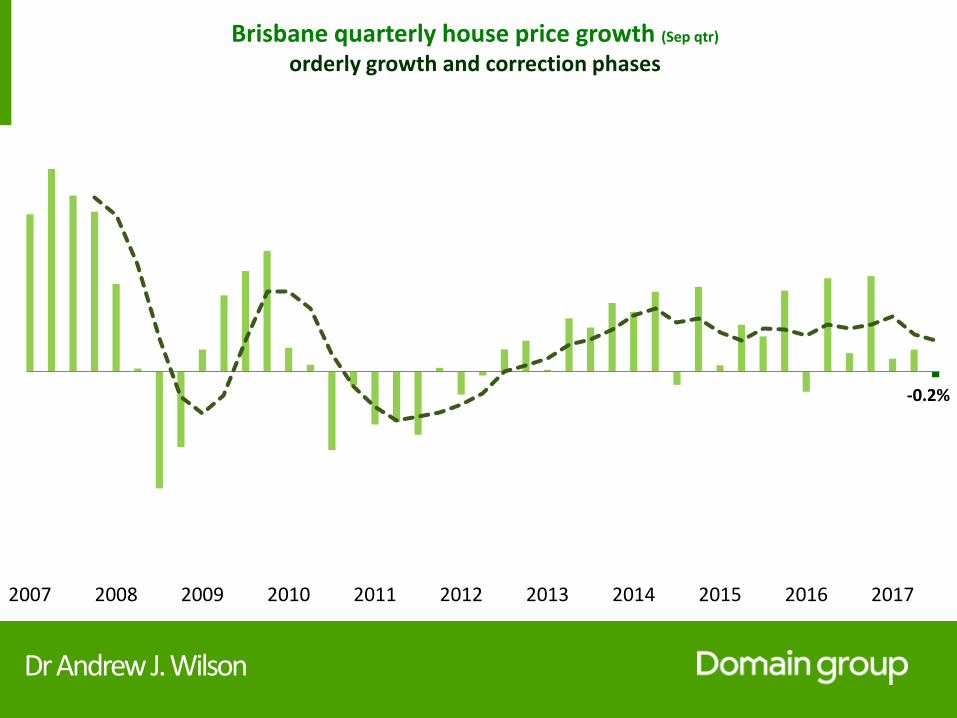

Brisbane quarterly house price growth (Sep qtr)

orderly growth and correction phases

-0.2%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Dr Andrew J. Wilson

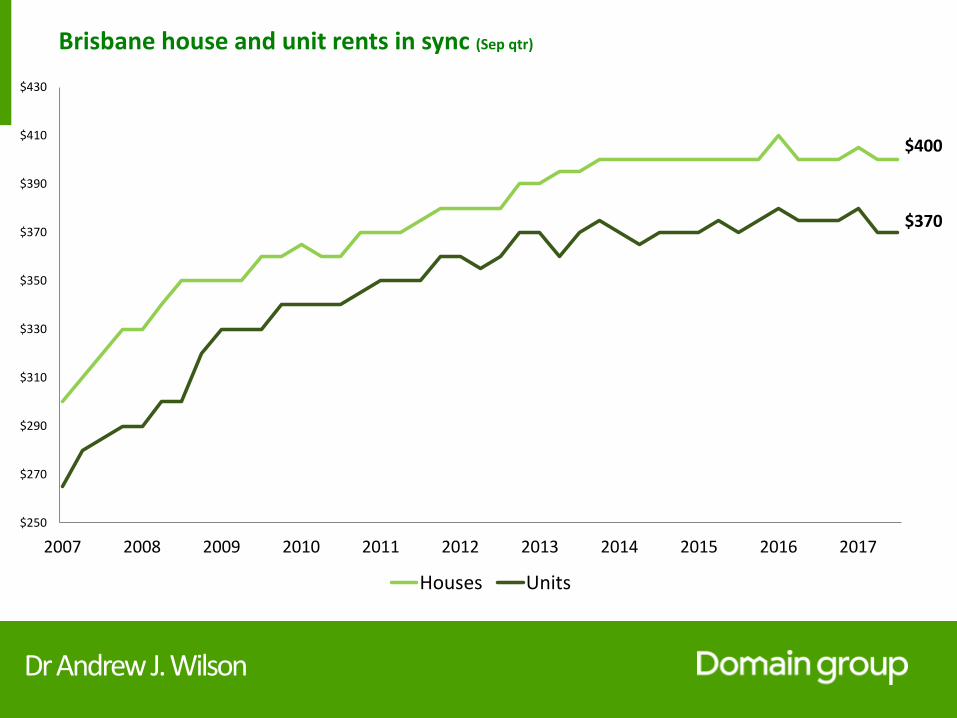

Brisbane house and unit rents in sync (Sep qtr)

$400

$370

$250

$270

$290

$310

$330

$350

$370

$390

$410

$430

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Houses Units

Dr Andrew J. Wilson

Brisbane house and unit yields in sync and rising (Sep qtr)

4.67%

4.93%

4.0%

4.2%

4.4%

4.6%

4.8%

5.0%

5.2%

5.4%

5.6%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Houses Units

Dr Andrew J. Wilson

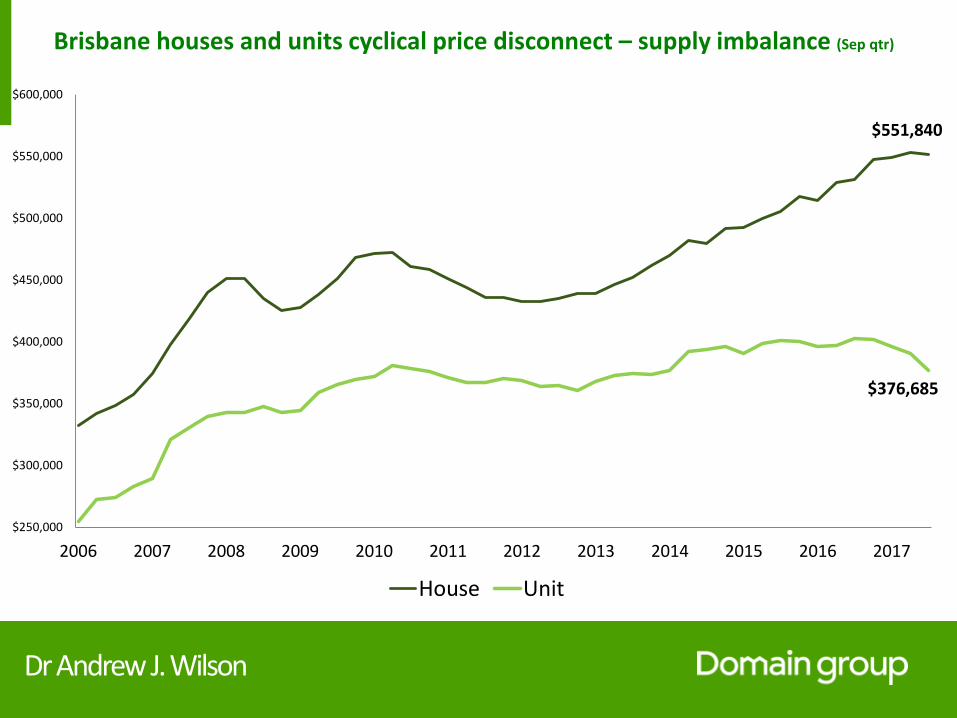

Brisbane houses and units cyclical price disconnect – supply imbalance (Sep qtr)

$551,840

$376,685

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

$550,000

$600,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

House Unit

Dr Andrew J. Wilson

National market outlook 2017

Dr Andrew J. Wilson

Housing Market Barometer

12%

2%

1%

0%

0%

Perth 0%

RISING

FALLING

2017 forecasts

4%8%

6%

4%

2%

2%

3%

4%

5%

Boom

Strong

Robust

Solid

Moderate

Moderate

Solid

Robust

Strong

Bust

Flat

Sydney, Adelaide, Darwin 5%

Hobart, Canberra 7%

Melbourne 10%

Brisbane 3%

Dr. Andrew J. Wilson

Thank you