na1onal+conference+on+financial+capabili1es+ … files/optimum... · nonfinancial: health,’ ......

TRANSCRIPT

Roundtable Discussion 3 Re1rement and long term saving strategy

There is NO Single Op1mum Replacement

Rate

Na1onal Conference on Financial Capabili1es

Beirut, Lebanon 21st October 2015

© Copyright, 2015. All Rights Reserved.

Ibrahim Muhanna FCAA, MSAA, FLAA MD & Actuary i.e. Muhanna & co. (Actuaries and Consultants)

1

"Actuaries are multi-skilled strategic thinkers, trained in the theory and application of mathematics, statistics, economics, probability and finance. They have been called financial architects and social mathematicians, because their unique combination of analytical and business skills are used to address a growing variety of financial and social challenges worldwide."

“What is an Actuary”

2

“Education for Retirement”

“A baby born today will retire in 2080 (if not later).

We, to a certain extent, agree &/or accept on how to educate our children for a future that we have no clue of.

On a shorter horizon, a person who is 25 years old today is

expected to retire in 2065 (if not later) . Yet, we do not financially educate our workforce on what is in store

for them after retirement.

The longer we postponed this education the more expensive the lesson becomes.

The obligation is to look long term and adjust &/or adapt as we go

along!!!”

i.e. muhanna

Understanding Protection Systems

4

PILLAR 0 1 2 3 4 Description

Basic, social pension, or social assistance

Public pension plan (Publicly managed)

Occupational or personal pension plans

Private schemes (Individual savings)

Informal support, other formal social programs (e.g. health) & other individual assets

Who is

covere

d

Life-‐time poor, Informal and formal sector

Formal sector Formal sector Middle & higher income persons

Life-‐time poor, informal and formal sector

What is

covered

Basic protection for the elderly & the disadvantaged

Basic beneCit replacing a portion of pre-‐retirement income (40%)

Additional beneCit replacing an extra portion of pre-‐retirement income (+30%)

Savings & investments

Non Financial: Health, Homeownership, lands

Participation

& Funding

Universal / General budget

Mandated / Contributions linked to earnings

Mandated / DeCined Contributions

Voluntary / Contributions, Ind. savings or employer sponsored

Voluntary / Government and Individual assets

n World Bank Five-‐pillar Social Protec1on Framework

5

Why support a mul:-‐pillar system? § Prevent old-‐age poverty § Reduce the obliga:on of children to support their families and ul:mately spend more :me in educa:on

§ Diversify the source of re:rement income § Development of the financial services industry

Pillars of Re1rement Income

© Copyright, 2015. All Rights Reserved.

Pillars of Re1rement Income

6

Replacement Ra1o

Pillar 3: Personal Savings; etc.

Pillar 2: Occupa1onal Pension Plans (DB or DC)

Pillar 1: Social Insurance Pension Plan

Pillar 0: Old-‐Age Security (Universal Program)

40%

15%

100% Coverage

© Copyright, 2015. All Rights Reserved.

MYOPIA of the general public…. – Individuals can have difficulties planning for the future

and under-save when young. – Orientation towards short-term consumption needs – Cultural stigma associated with sickness, accidents

and death – Religious barriers – Traditional protection systems still in place in

developing societies (family, community….) – Women are still not educated enough to take the

matter into hand for the sake of their family – Coverage is believed to be the sole responsibility of

the government

MYOPIA of the level of Replacement Rate • Adequacy: an absolute measure of

living standards. – individual pension entitlement as a

proportion of economy-wide average earnings.

– pension level.

• Insurance: a relative measure of living standards. – individual pension entitlement

relative to individual earnings when working.

SEVERITY

• Permanent Total Disability

• Death

• Long Term Disability

• Retirement

• Unemployment

• Temporary Total Disability

• Permanent partial Disability

• Healthcare

• Schooling

INDIVIDUAL RISKS

1. Age & Sex

2. Souse & Children – ages & sex

3. Assets (savings, home, …)

4. Liabilities (loans, mortgages, …)

5. Income (individual – spouse) – (home or expatriate)

6. Expenses (before & after risk) & Taxes

7. Schooling, University, Dowry, Start up capital.

8. Employee Benefits & other insurances

9. Social Security

10. Economic & Social Conditions (returns, inflation, …)

INDIVIDUAL PARAMETERS

INDIVIDUAL PARAMETERS Principal Assumption

Age 25 years

Annual Income $ 15,000

Income Increase (before age 35) 5.5%

Income Increase (Long-term) 4.0%

Annual Individual Expenses $ 12,000

Price Inflation 3.0%

Age at Marriage 30 years

Retirement Age 65 years

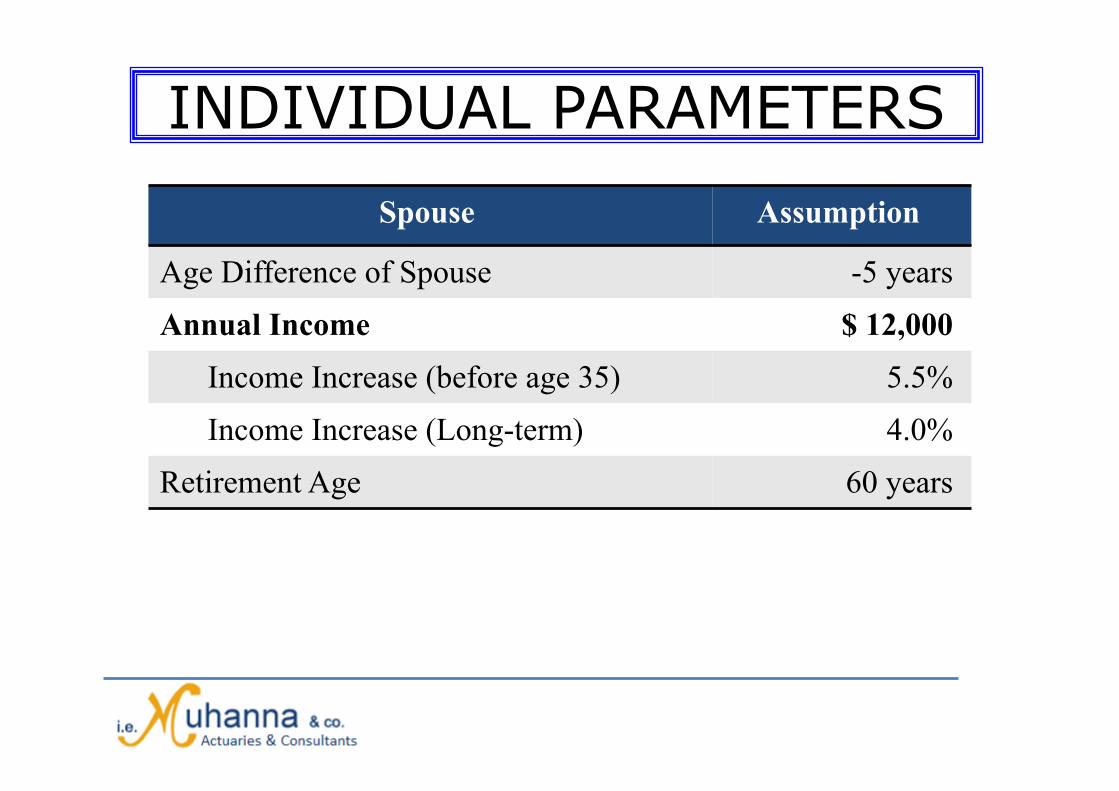

INDIVIDUAL PARAMETERS Spouse Assumption

Age Difference of Spouse -5 years

Annual Income $ 12,000 Income Increase (before age 35) 5.5%

Income Increase (Long-term) 4.0%

Retirement Age 60 years

INDIVIDUAL PARAMETERS Children Assumption

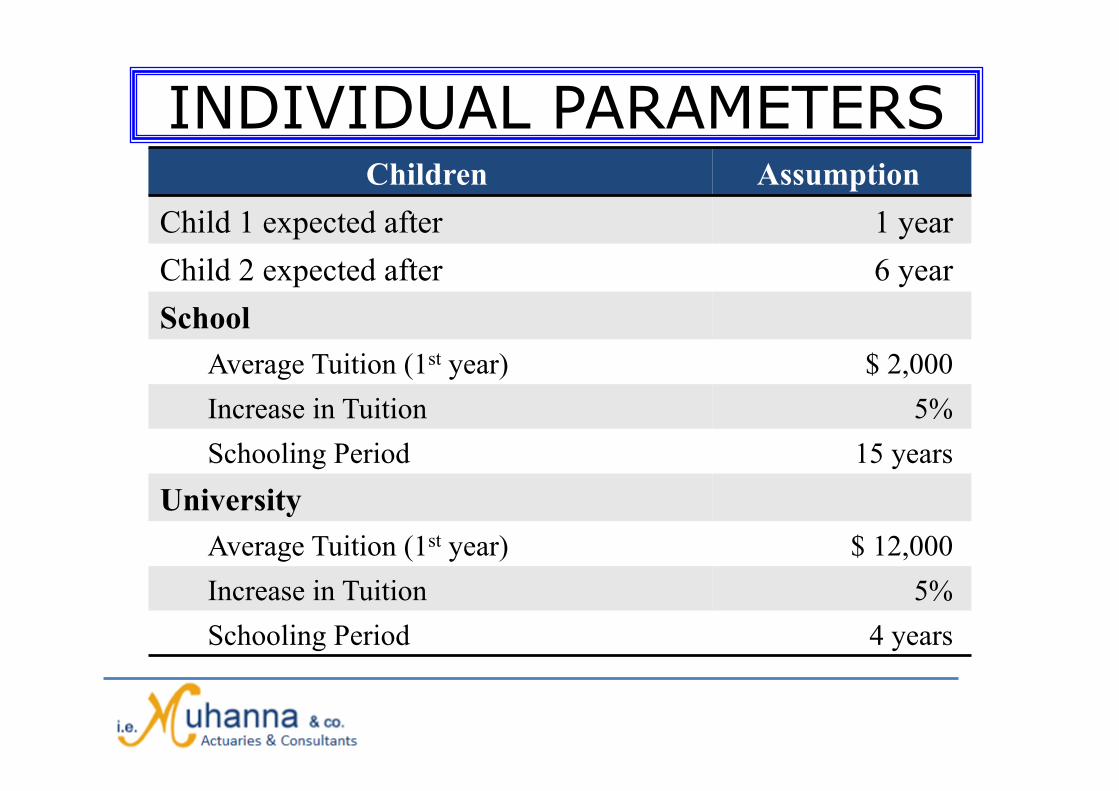

Child 1 expected after 1 year Child 2 expected after 6 year School

Average Tuition (1st year) $ 2,000 Increase in Tuition 5% Schooling Period 15 years

University Average Tuition (1st year) $ 12,000 Increase in Tuition 5% Schooling Period 4 years

INDIVIDUAL PARAMETERS Family Assumption

Annual Expenses $ 20,000 Price Inflation 3%

Return on the Investments 5% Mortgage Loan $ 180,000

Period 30 years Interest 5%

Pension Funding (% of Income) % Pension Level (% of last family exp.) % Annual Increase in Pension 2% Widow’s Pension Level 80%

Projecting Income

0.00

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

140,000.00

160,000.00

25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82

Total Annual Income (USD)

Projecting Income & Desired Pension

0.00

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

140,000.00

160,000.00

25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82

Total Annual Income (USD)

70% RR At Re1rement

Projecting Income & Desired Pension Family expenses

Projecting Desired Pension Funding for Retirement

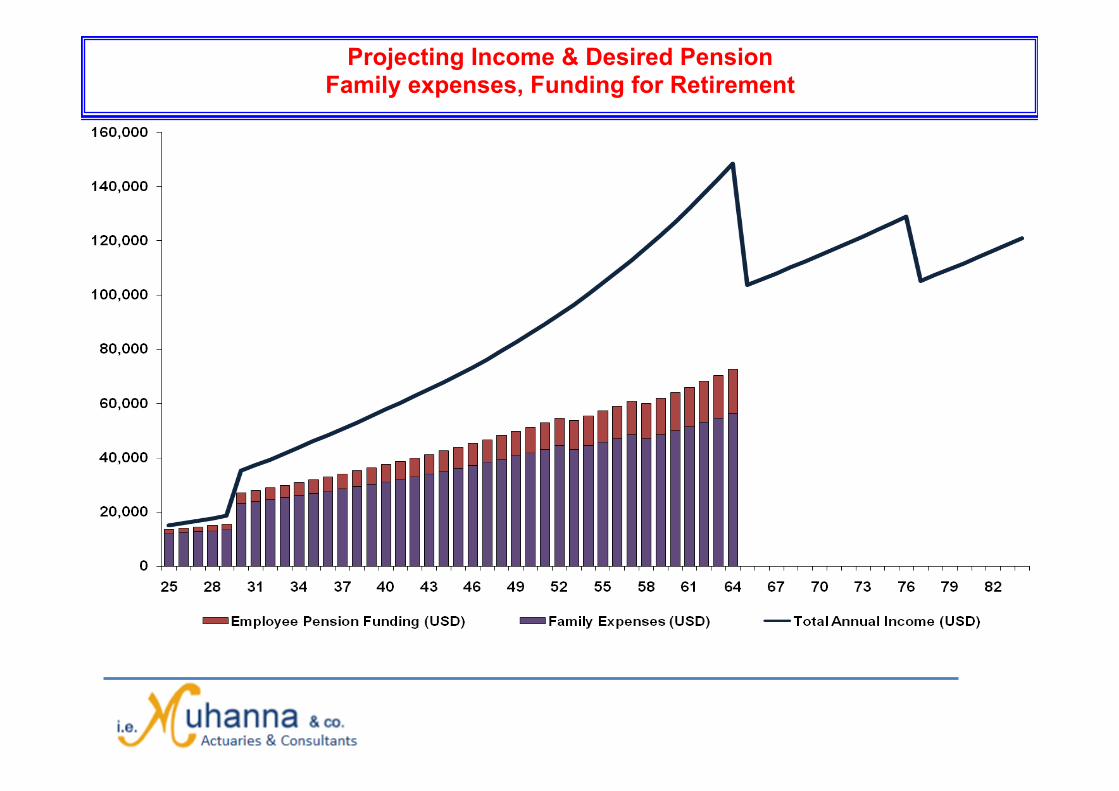

Projecting Income & Desired Pension Family expenses, Funding for Retirement

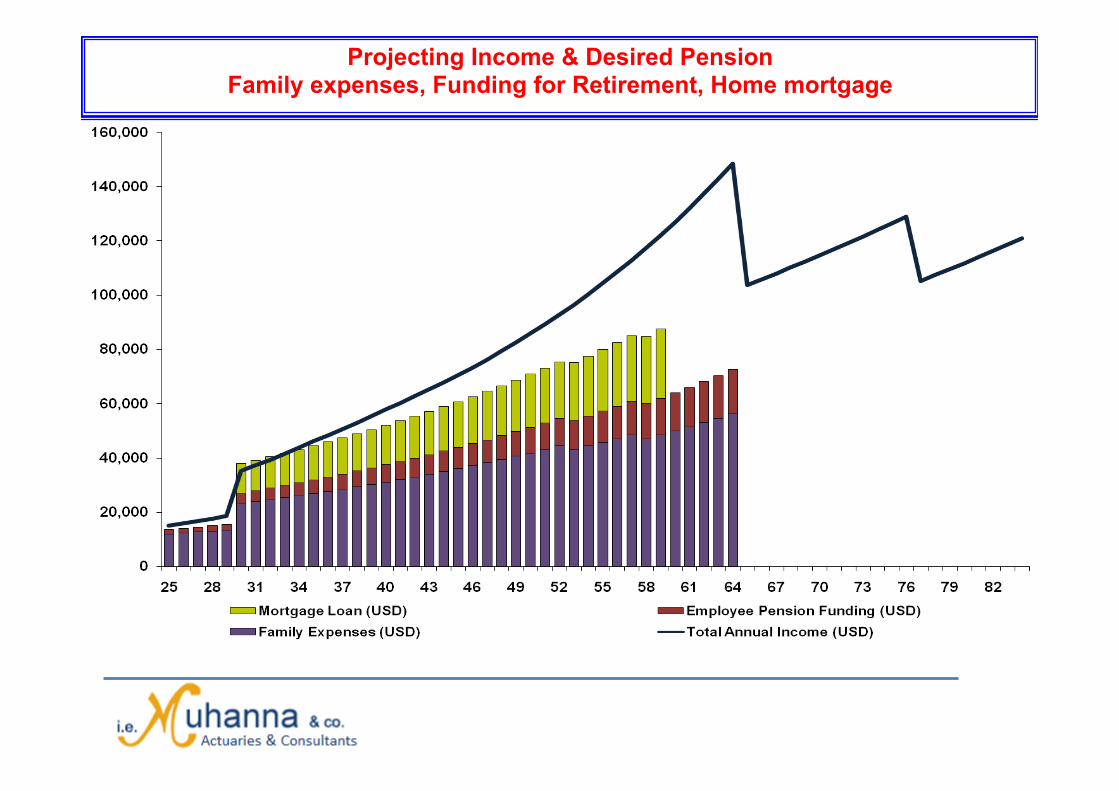

Projecting Income & Desired Pension Family expenses, Funding for Retirement, Home mortgage

Projecting Income & Desired Pension Family expenses, Funding for Retirement, Home mortgage, Education

Projecting Income & Desired Pension Family expenses, Funding for Retirement, Home mortgage, Education

• Needs change after retirement

• Children education fees no longer exist

• The house mortgage loan is already paid

• Some more needs emerge

• Like health care expenses if not covered under a different plan...

• There is no need to over-fund and burden the employee’s expense budget during active life..

Are all pre-retirement expenses to be funded for after retirement??

Projecting NEEDED Pension Funding for Retirement

Projecting Income & NEEDED Pension Family expenses, Funding for Retirement, Home mortgage, Education

• Only family expenses persist after retirement

• Funding for future pension should take only those expenses into account

• It is more easily sustained by the active employee

• Mandated schemes should focus more on this basic need, making the whole funding operation easier to implement for all parties involved...

• Quality of the advice is so critical

Funding for what is really needed...

1. MEDICAL DOCTOR 1. Visited

2. Diagnosed

3. Prescribed (the MD signs)

4. Followed Up (need)

2. FINANCIAL DOCTOR 1. Solicited (sold not bought concept)

2. Analysed (inshallah)

3. Sold (the clients signs)

4. After sales service (hopefully)

MD vs FD

28

For feedback: [email protected] Tel +9611 752 999 For more Informa:on: www.muhanna.org www.muhanna.com

Thanks for the a\en1on!

Q&A

© Copyright, 2015. All Rights Reserved.