municipal financial management

TRANSCRIPT

Municipal Financial ManagementPresented by Brenda Wedge, CPA CGA

February 25, 2021

WELCOME

MUNICIPAL CAO EDUCATION & TRAINING

CAO and Council – Roles and Responsibilities

Effective Meetings, Public Engagement and Communication

Municipal Law

Municipal Financial Management

Land Use Planning and Development

& INTRODUCTIONS

1

R

M

L

F

P

Agenda

1. Financial Management Role

2. The Financial Plan

3. Municipal Borrowing Limits

4. Procurement

5. Financial Reporting

2

Financial Management Role

3

The CAO is the administrative head of the municipality and Council’s principal advisor.

The CAO provides information and advices council on: policies, finance, legislative requirements, plans and more.

- PEI MUNICIPAL AFFAIRS

4

✓ Hires, directs, manages and supervises employees and contractors ✓ May (subject to bylaw or contract) suspend, discipline or dismiss employees✓ May delegate duties to employees (except power to dismiss employee)

✓ Ensures statements and reports are provided to the Minister

✓ Ensuresresolutions and policies are complied with

✓ Ensures funds are disbursed appropriately

✓ Ensures all municipal assets are maintained safely

✓ Appointed/supervised by and reports to council

✓ Notifies council if actions are contrary to bylaws, resolutions or Acts

✓ Ensures council and council committee meeting minutes are recorded

✓ Informs council on the operations and affairs of municipality

✓ Maintains indexed register with certified copies of bylaws and resolutions

✓ Ensures an accurate record of assets and liabilities are maintained

✓ Takes charge of all books, documents and records

5

Financial Management Roles

• Council has overall accountability for the financial position of the municipality

• BUT they rely on you, the CAO to provide them with the information they need to ensure

• Resources are protected and

• Finances are responsibly managed

6

Financial Management Roles

• Council achieves fiscal management by:• Ensuring effective financial controls are in place;

• Developing a financial plan;

• Monitoring the financial position of the municipality throughout the year; and

• Reporting on the municipality’s financial position at the end of the year.

7

Legislation

• Municipal Government Act (MGA) Part 6 deals with Financial Matters• Division 1 – Financial Operations

• Division 2 – Raising of Revenue

• Division 3 – Debt Restrictions

• Division 4 – Financial Statements and Auditor

• Financial Plan Regulations provide detail on what is to be included in the Financial Plan

8

The Financial Plan1. Preparing the Financial Plan2. Adopting the Financial Plan

3. Monitoring the Financial Plan

9

Financial Plan

• Operating budget• A template is available for municipalities

• https://www.princeedwardisland.ca/en/information/fisheries-and-communities/financial-plan-budget-and-financial-reporting

• Capital budget

• 5 year capital expenditure program, with an asset management plan• A Municipal Expenditure Tool has been created by Infrastructure Secretariat

• https://www.princeedwardisland.ca/en/publication/municipal-expenditure-tool

10

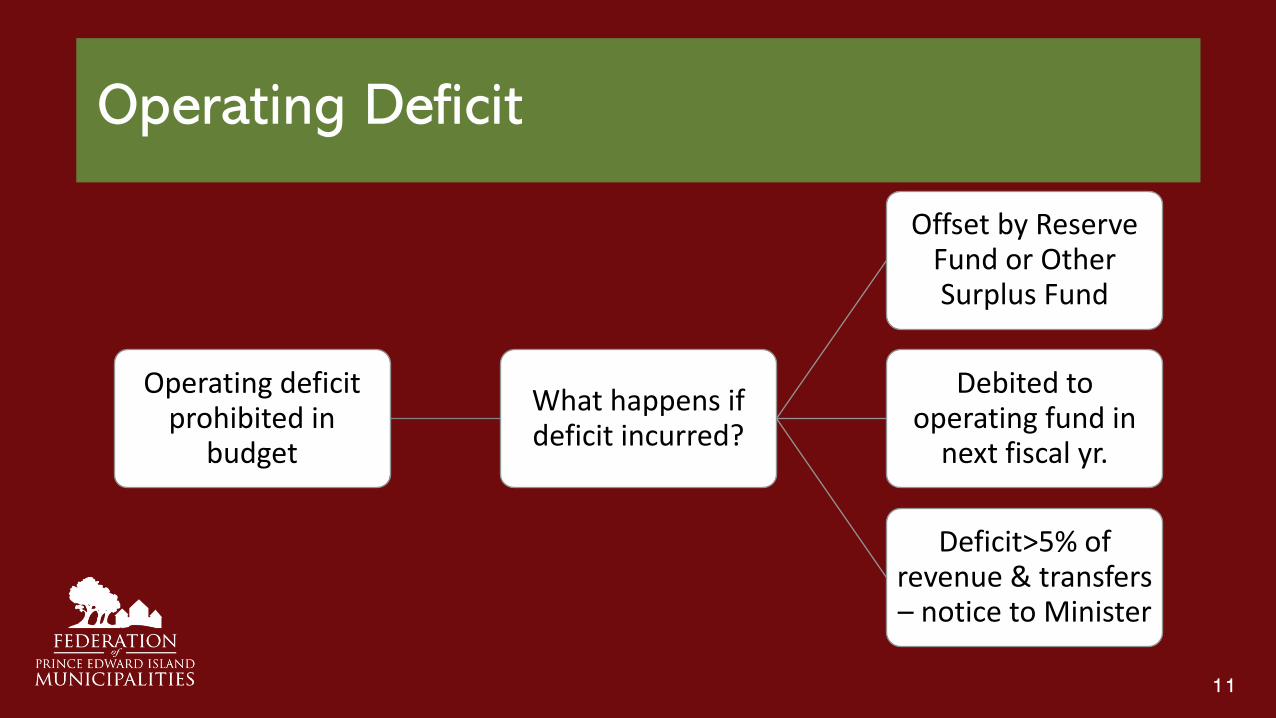

Operating Deficit

Operating deficit prohibited in

budget

What happens if deficit incurred?

Offset by Reserve Fund or Other Surplus Fund

Debited to operating fund in

next fiscal yr.

Deficit>5% of revenue & transfers – notice to Minister

11

Financial Plan – Operating Budget

OPERATING BUDGET

Estimated revenues

Less:

Estimated expenditures

Projected Surplus or Breakeven

12

Financial Plan – Capital Budget

• Estimates for the fiscal year of:• Capital projects for the fiscal year

• Costs to acquire, construct, remove or improve

• Amount of money required to pay for these costs• anticipated sources for these funds

• Any amounts to be transferred from the operating budget or a reserve fund

13

Financial Plan – 5 YR Capital Expenditure and Asset Management Programs

• 5 YR Capital Expenditure Program• Each proposed capital project for the next five years;

• Estimated amount and source to cover the capital projects;

• Asset Management Program• Inventory of municipally-owned infrastructure;

• Costs required to maintain the existing infrastructure; and

• Costs required to maintain the infrastructure planned for in the 5 YR capital expenditure program

14

Asset Management Plan

• Requirement to be eligible for federal funding

• Helps municipalities get the most out of their infrastructure• Helps to project life cycle costs which helps with decision making on

improvements vs. replacement

• Prioritizes spending

• Considerations for development• What do we own, and where is it?

• What is its current condition?

• What is its value?

• What is its useful life?

• What do we need to do to it?

• When do we need to do it?

15

A Municipal Expenditure Tool was developed by Infrastructure Secretariat to assist municipalities with their asset management program.

https://www.princeedwardisland.ca/en/publication/municipal-expenditure-tool

Asset Management Plan

16

Break Out Session #1

Appoint a notetaker and spokesperson.

Take 7 minutes and discuss in your group the things you would consider

in preparing a Financial Plan for your municipality.

Highlight a couple of things you would do to assist you in

developing the financial plan.

17

Financial Plan - Process

• Review of historical actual expenditures and revenues

• Consultation with department heads and committee chairs

• Consultation with Provincial government departments re: municipal-provincial funding agreement

• Realistic estimates for repairs and maintenance

• “Wish lists” for capital expenditures and annual planning/prioritization

18

Financial Plan - Process

• CAO needs to prepare or have prepared a draft financial plan and provide information• For Council’s review

• To facilitate Council’s budgetary discussions, and

• To provide information to the public with respect to the financial plan

19

The Financial Plan1. Preparing the Financial Plan

2. Adopting the Financial Plan3. Monitoring the Financial Plan

20

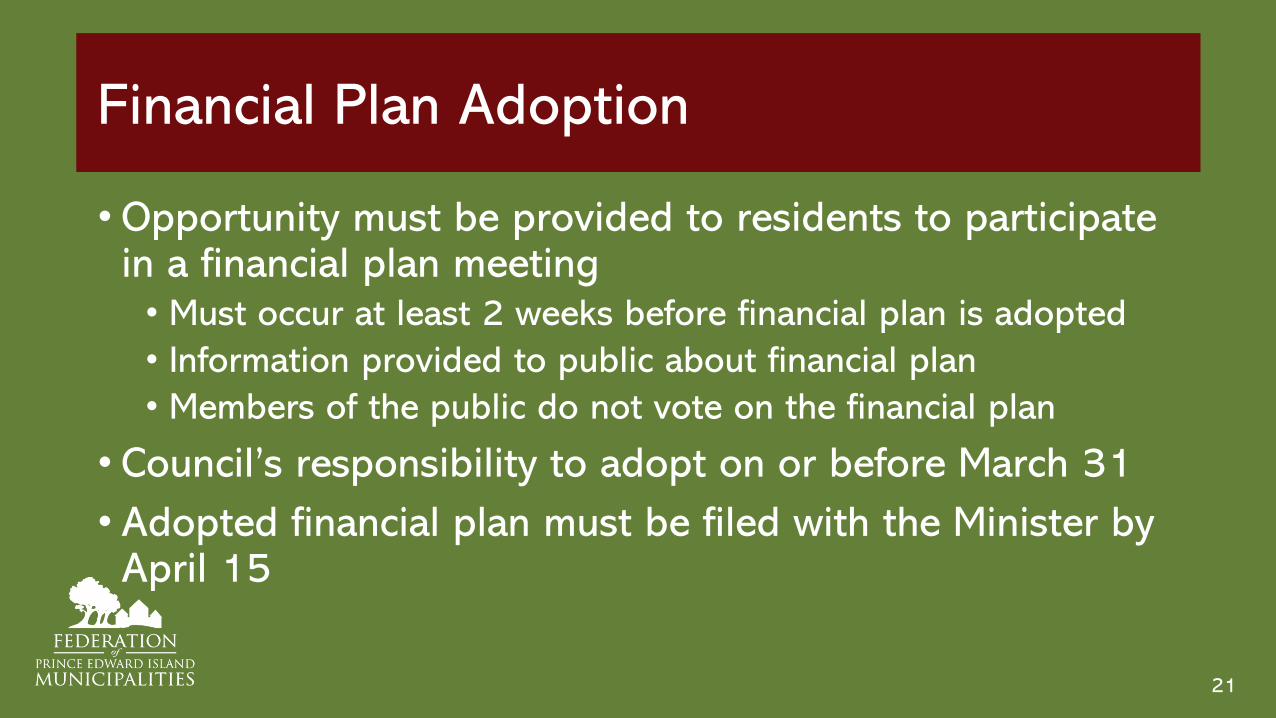

Financial Plan Adoption

• Opportunity must be provided to residents to participate in a financial plan meeting• Must occur at least 2 weeks before financial plan is adopted

• Information provided to public about financial plan

• Members of the public do not vote on the financial plan

• Council’s responsibility to adopt on or before March 31

• Adopted financial plan must be filed with the Minister by April 15

21

Reporting Dates to Keep in Mind

Date Deliverable

January/February Financial Plan being developed, Public Meetings & Council approval

March 10 - 12 Latest date for public meeting

March 31 Council adopts Financial Plan

March 31 Submit any tax rate form to Taxation – retroactive to January 1st

April 15 Submit approved financial plan to Municipal Affairs

22

The Financial Plan1. Preparing the Financial Plan

2. Adopting the Financial Plan

3. Monitoring the Financial Plan

23

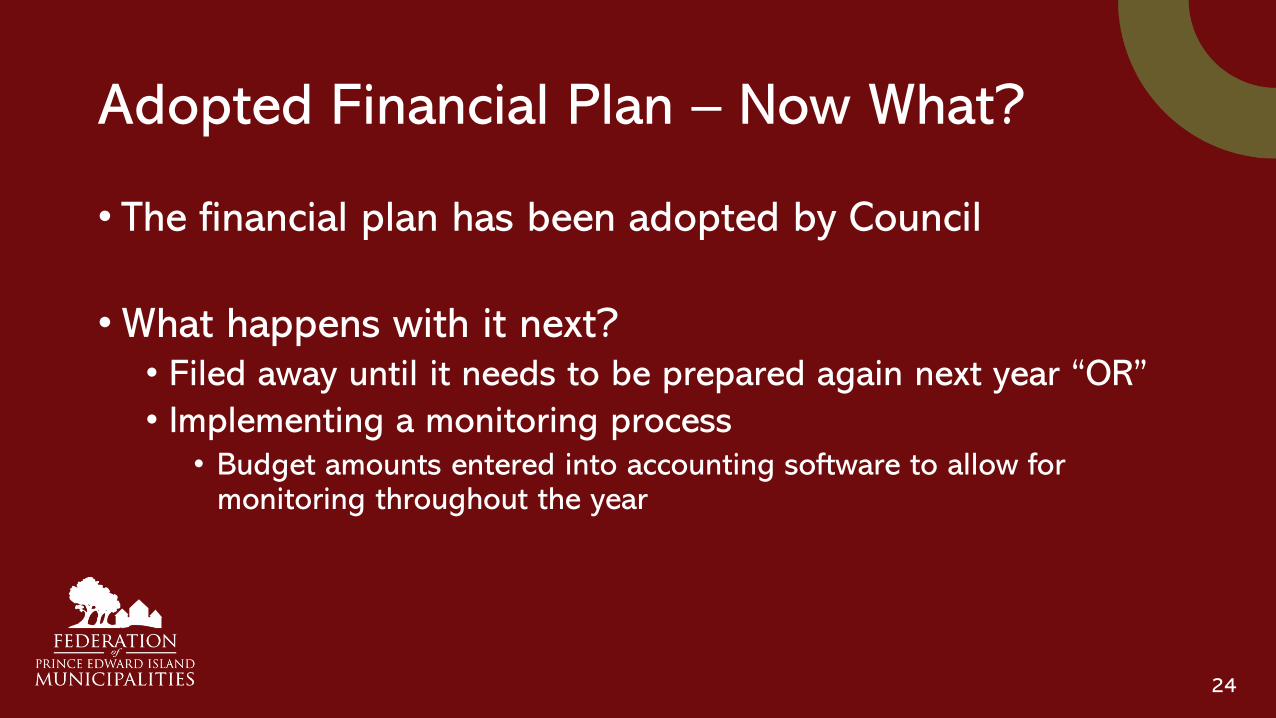

Adopted Financial Plan – Now What?

• The financial plan has been adopted by Council

•What happens with it next?• Filed away until it needs to be prepared again next year “OR”

• Implementing a monitoring process• Budget amounts entered into accounting software to allow for

monitoring throughout the year

24

Monitoring the Financial Plan

• Shows the maximum amount that is approved for expenditure

• Budget is both a financial plan and policy document• Municipality should be monitoring spending based on the

annual budget (financial plan)

• If spending in a way that is not consistent with the approved annual budget this is a red flag that will require further review and explanations

25

What Financial Information should be Provided to Council?

Expenditure Actual YTD Budget Variance (Over/(Under)

Office 5,000 4,000 1,000

Utilities 7,000 6,500 500

Repairs & maintenance

8,000 10,000 (2,000)

Festival & events 2,500 3,000 (500)

Salaries & benefits 55,000 50,000 5,000

26

Signing Authority

• Internal control

•Signed by both the CAO and Mayor

•Payments matched to documentation

•Blank cheques being signed are not good practice

•Contracts/agreements under $25,000 – By Council resolution CAO can be authorized to sign

27

Q&A

28

Municipal Borrowing Limits1. Borrowing for Capital Expenditures

2. Short Term Borrowing

29

Borrowing – Capital Expenditures

•Must be authorized by bylaw

•A resolution of council is required to authorize

•Municipality’s capital debt (including controlled corporations) can not exceed 10% of the current assessed value of all real property in the municipality;

30

Borrowing – Short Term

•Can borrow short-term to finance operations

•Must be authorized by bylaw

•A resolution of council is required to authorize

BUT

•Cannot exceed 50% of the total estimated revenues of the municipality for that year

31

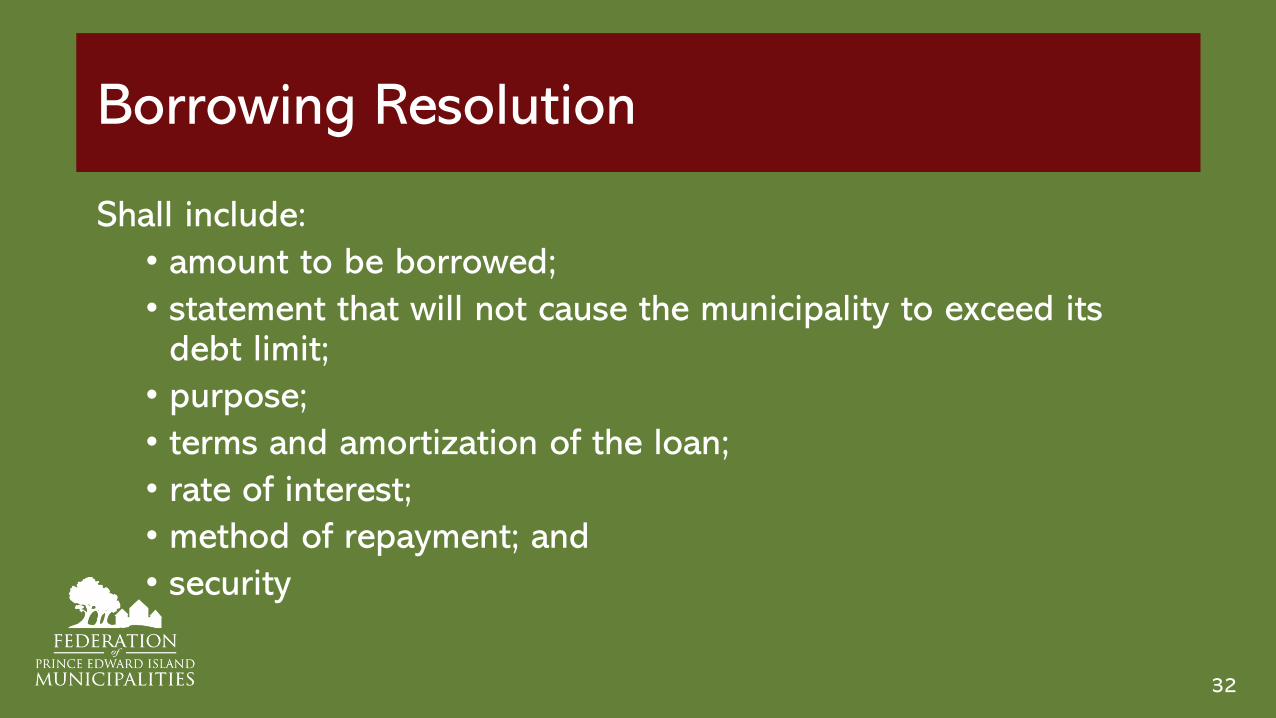

Borrowing Resolution

Shall include:

• amount to be borrowed;

• statement that will not cause the municipality to exceed its debt limit;

• purpose;

• terms and amortization of the loan;

• rate of interest;

• method of repayment; and

• security

32

Q&A

33

Procurement1. Principles

2. Trade Agreements

3. Methods

4. Advertising

5. Evaluation Criteria

6. Evaluation Process

7. Bylaw

34

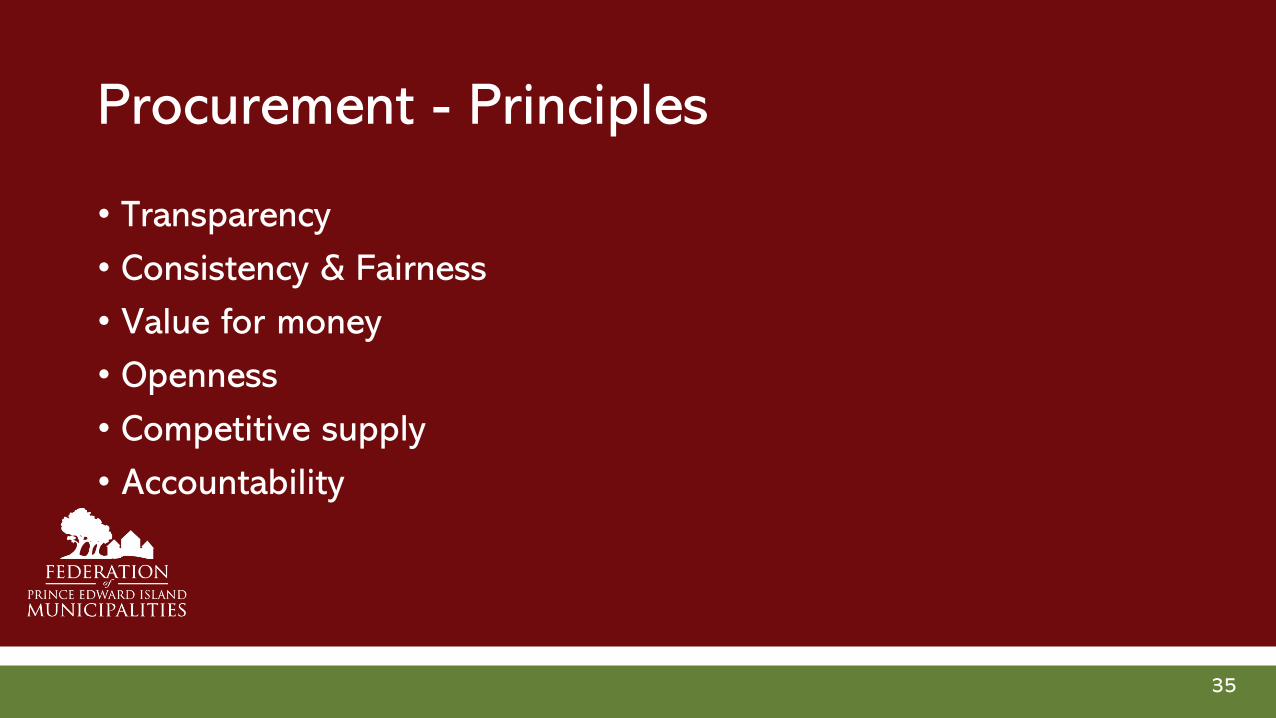

Procurement - Principles

• Transparency

• Consistency & Fairness

• Value for money

• Openness

• Competitive supply

• Accountability

35

Procurement – Trade Agreements

• Equal access, opportunity, and information to all respondents

• Competitive selection process unless a specific exception applies

• Fair and transparent steps leading to a possible contract

• No splitting of work to be done to avoid agreement requirements

• No unnecessary difficulties for eligible respondents

• Override municipal procurement policies or bylaws if inconsistent

36

Procurement – Trade Agreements

• Estimated value of work is at or above thresholds:• Publish tender notice on government’s procurement

website• New information available to all • Ensure adequate preparation and response time given• Tenders need to be in writing• Respondents must be informed of decision • Unsuccessful respondent must be provided with reasons

37

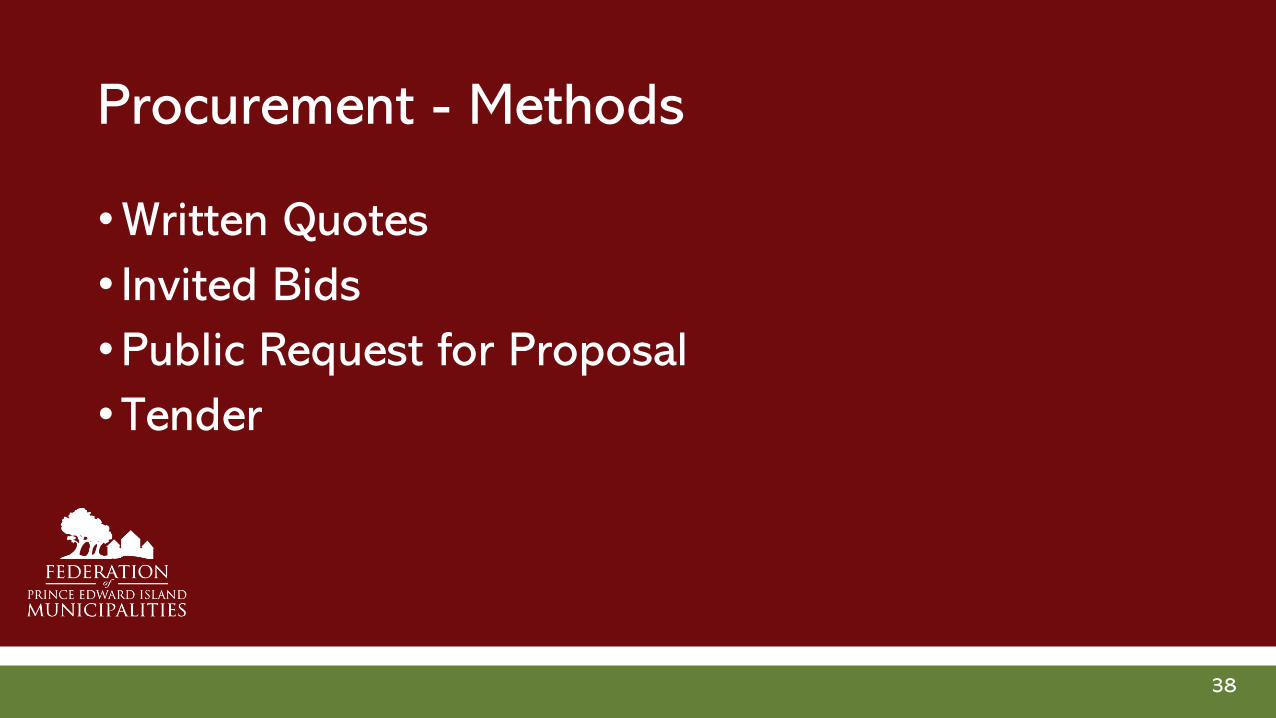

Procurement - Methods

•Written Quotes

• Invited Bids

•Public Request for Proposal

•Tender

38

Procurement MethodsGoods

$0 - $4,999 Procure directly or public or invited competitive process

$5,000 - $9,999 3 written quotes or public or invited competitive process

$10,000 to lowest applicable Trade Agreement Threshold

Public or invited competitive process

Lowest applicable Trade Agreement Threshold and over

Public tender

Services

< $50,000 3 written quotes

> $50,000 Formal RFP required

Construction

> $100,000 Formal RFP advertised to comply with CFTA

39

Procurement – Trade Agreements

Atlantic Procurement Agreement (APA)

Canadian Free Trade Agreement (CFTA)

Canada-European Comprehensive Economic and Trade Agreement (CETA)

Goods $25,000 $101,100 $365,700

Services $50,000 $101,100 $365,700

Construction $100,000 $252,700 $9,100,000

Note: Other requirements may apply to municipal utilities and police services

40

Procurement - Advertising

•Municipal Website

•Government of PEI Tenders –princeedwardisland.ca/en/tenders

•Newspaper ad

• Invited vendors

41

Procurement Methods

Atlantic Procurement Agreement –Public Notice Threshold

Goods $10,000

Services $50,000

Construction $100,000

Canadian Free Trade Agreement –Public Notice Threshold

Goods $25,000

Services $101,100

Construction $252,700

42

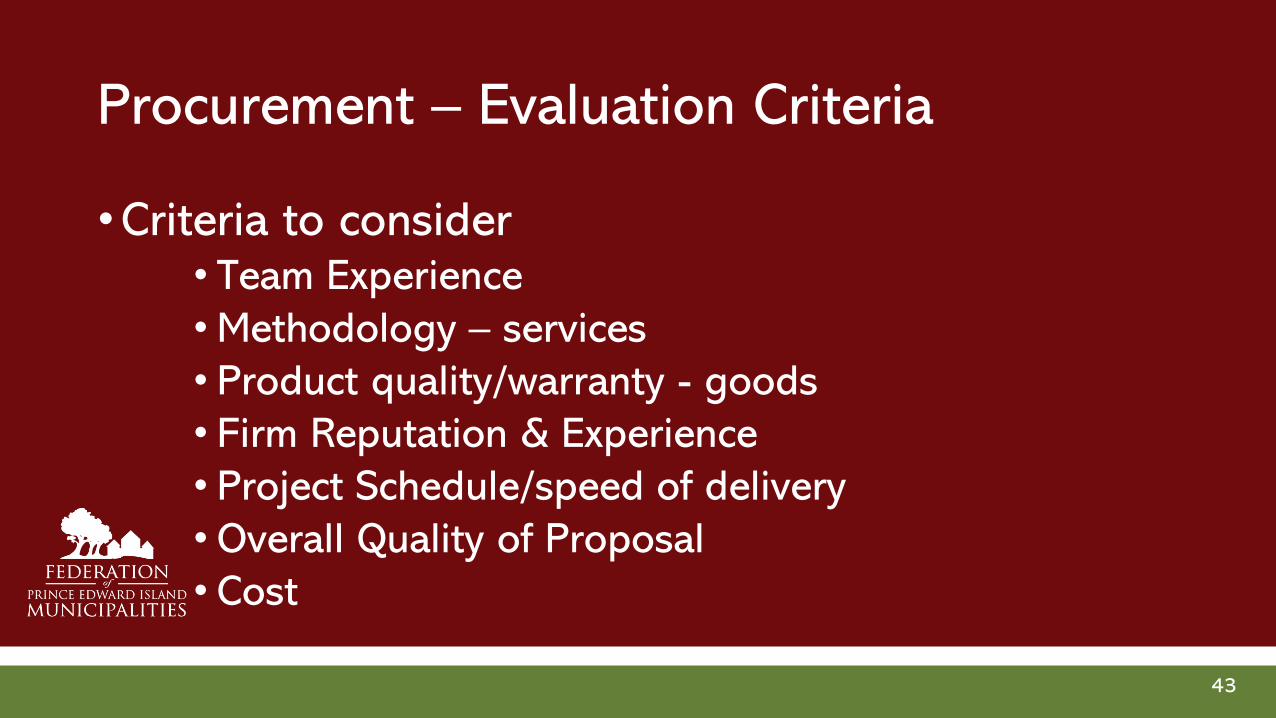

Procurement – Evaluation Criteria

•Criteria to consider• Team Experience

•Methodology – services

• Product quality/warranty - goods

• Firm Reputation & Experience

• Project Schedule/speed of delivery

• Overall Quality of Proposal

• Cost

43

Procurement –Evaluation Criteria (Weighting)

• Example Weighting• Team Experience – 20%

• Methodology (services) or Product quality/warranty – goods –20%

• Firm Reputation & Experience – 25%

• Project Schedule/speed of delivery – 20%

• Overall Quality of Proposal – 5%

• Cost – 10%

44

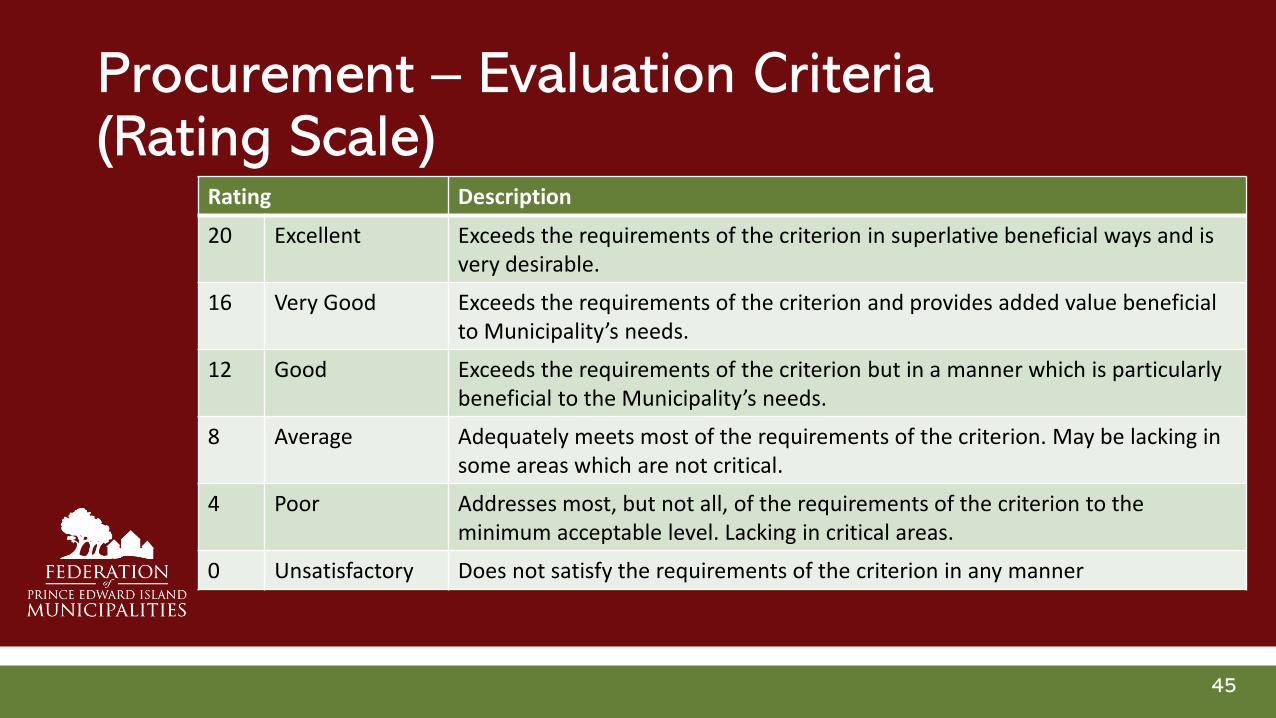

Procurement – Evaluation Criteria (Rating Scale)

Rating Description

20 Excellent Exceeds the requirements of the criterion in superlative beneficial ways and is very desirable.

16 Very Good Exceeds the requirements of the criterion and provides added value beneficial to Municipality’s needs.

12 Good Exceeds the requirements of the criterion but in a manner which is particularly beneficial to the Municipality’s needs.

8 Average Adequately meets most of the requirements of the criterion. May be lacking in some areas which are not critical.

4 Poor Addresses most, but not all, of the requirements of the criterion to the minimum acceptable level. Lacking in critical areas.

0 Unsatisfactory Does not satisfy the requirements of the criterion in any manner

45

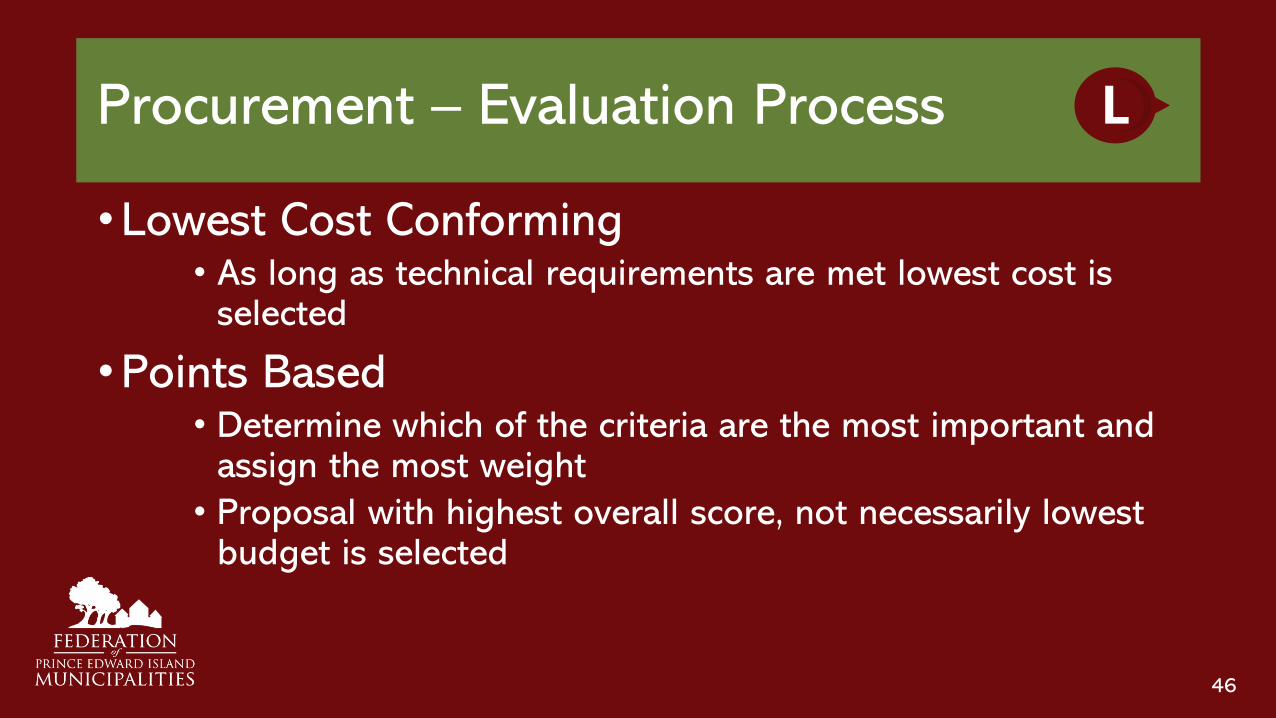

Procurement – Evaluation Process

•Lowest Cost Conforming• As long as technical requirements are met lowest cost is

selected

•Points Based• Determine which of the criteria are the most important and

assign the most weight

• Proposal with highest overall score, not necessarily lowest budget is selected

46

L

Procurement – Evaluation Process

•Who will evaluate the proposal?•Set up evaluation committee

•Can include CAO and Council Members

47

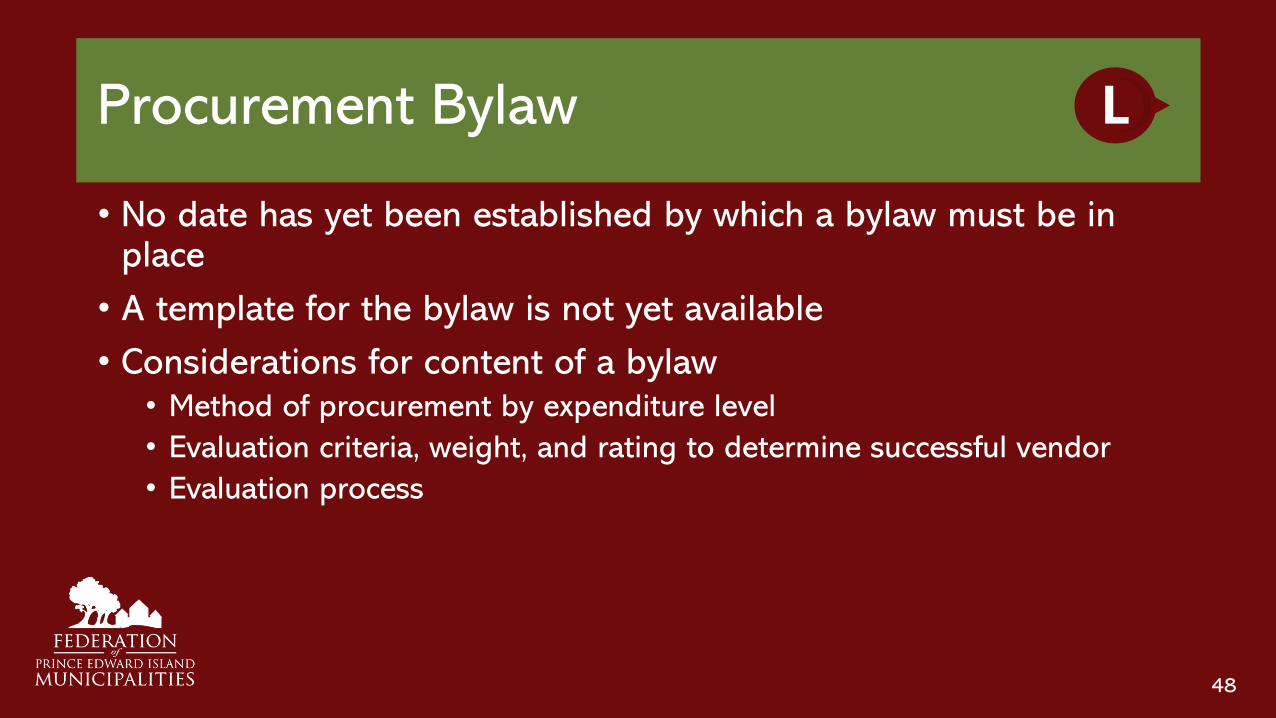

Procurement Bylaw

• No date has yet been established by which a bylaw must be in place

• A template for the bylaw is not yet available

• Considerations for content of a bylaw• Method of procurement by expenditure level

• Evaluation criteria, weight, and rating to determine successful vendor

• Evaluation process

48

L

FPEIM’s Trade Program

• Leverage group buying to secure preferential pricing and service

• FPEIM administers procurement process

• Some of the goods that can be procured through FPEIM’s program

• Tires

• Office supplies

• Fleet management

• Traffic signage

• Capital purchasing through premium brands

49

Break Out Session #2

Appoint a notetaker and spokesperson.

Take 7 minutes and discuss in your group how your municipality currently

deals with procurement.

Share with the group a couple of approaches that are being

used.

50

Q&A

51

Financial Reporting

1. Requirements and Timelines

2. Understanding the Financial Statements

3. Audit Requirements

52

Year-end Financial Statements

• Most important tool for reporting on the financial position of the municipality

• Ensure accountability and transparency to residents

53

Municipal Financial Information Return (MFIR)

• Requirement of all municipalities

• Used by Municipal Affairs • to generate municipal statistical reports; and

• Meet reporting requirements of Statistics Canada for National Reporting

• Two versions• Municipality with no utilities

• Municipality with utilities

• Downloadable at https://www.princeedwardisland.ca/en/information/fisheries-and-communities/financial-plan-budget-and-financial-reporting

54

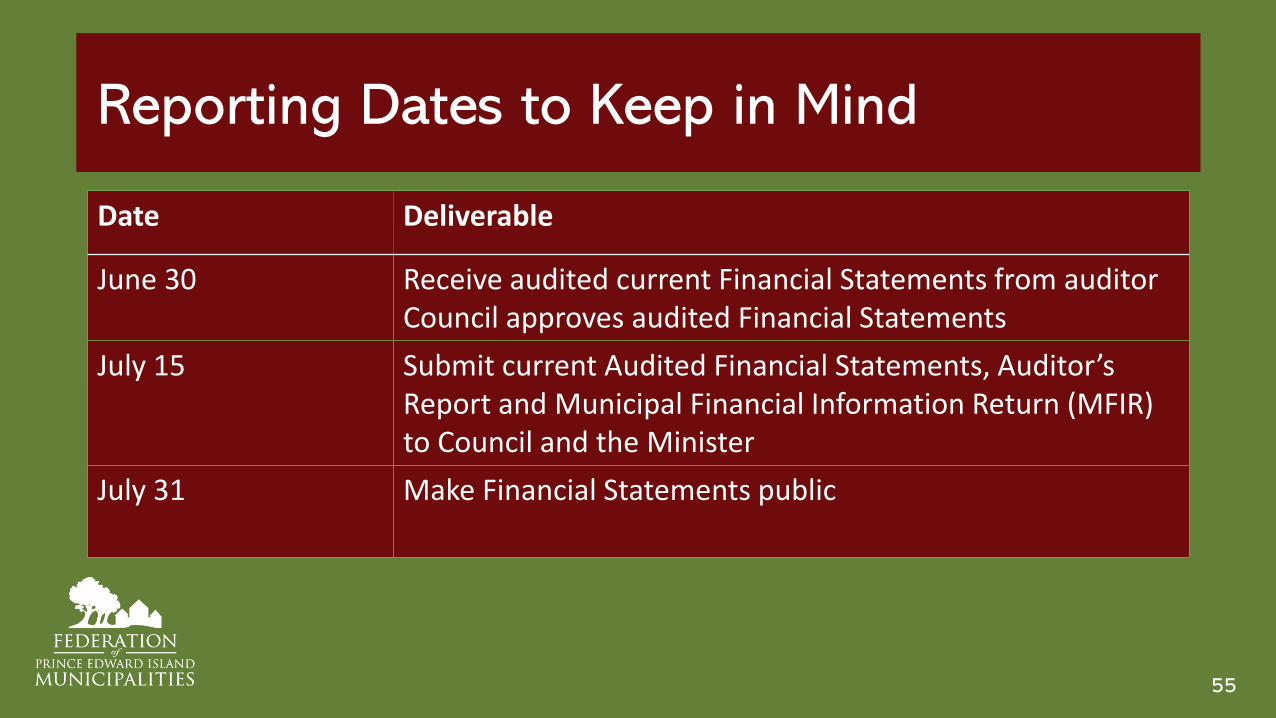

Reporting Dates to Keep in Mind

Date Deliverable

June 30 Receive audited current Financial Statements from auditorCouncil approves audited Financial Statements

July 15 Submit current Audited Financial Statements, Auditor’s Report and Municipal Financial Information Return (MFIR) to Council and the Minister

July 31 Make Financial Statements public

55

Financial Reporting1. Requirements and Timelines

2. Understanding the Financial Statements

3. Audit Requirements

56

Financial Statements

• Statement of Financial Position

• Statement of Operations

• Statement of Changes in Net Financial Assets

• Statement of Cash Flows

• Notes and Schedules

57

Financial Statement Review Questions

• Are there long-range planning or budgetary issues the municipality needs to address?

• Are there some “red flags” in the financial statements?

• Have there been any extraordinary or unusual financial transactions that may have future implications for the municipality?

• How did the current year’s financial decisions and operations impact the overall financial position of the municipality?

58

Financial Statement Review Questions

• Does the municipality have sufficient working capital?

• What is the remaining useful life of the municipality’s tangible capital assets?

• What is the content of the auditor’s management letter?

• Have the municipality’s financial statements been sufficiently communicated to the residents and businesses in the municipality?

59

Financial Reporting1. Requirements and Timelines

2. Understanding the Financial Statements

3. Audit Requirements

60

Requirement for an Audit

•Auditor must be appointed

•Auditor must provide report to CAO by June 30th

•Access to records, documents, and other items from financial reporting system must be provided to the Auditor

•Council, CAO and employees must provide information and explanations to the Auditor

61

Information Required for the Auditor

•Financial Overview

•Trial Balance

•Cash related information

•Accounts Receivable

•Accounts Payable and Accruals

•Prepaid Expenses

62

Information Required for the Auditor

•Capital Assets

•Deferred Revenue

•Long-term Debt

•Contractual Obligations, Contingencies and Subsequent Events

•Revenue and Expenses

63

Information Required for the Auditor

•Additional Requirements• Bylaws, corporate documentation.• Copy of annual operating budget.• Copy of personnel policy.• Copies of all Lease Agreements.

64

Q&A

65

66

THANK YOU!Next Session: Land Use Planning and Development

March 25, 2021 1:00 to 3:00 PM

This presentation is provided as information only and is a summary of the issues discussed. It is not meant as professional advice or a professional opinion and you are cautioned to seek specific professional advice for your unique circumstances. This presentation may

not be reproduced or distributed without the prior written consent of the Federation of PEI Municipalities.