franklin regional council of governments essentials series municipal financial management review...

TRANSCRIPT

Franklin RegionalCouncil of Governments

Essentials Series

Municipal Financial Management Review

September 16, 2015

Contact Information

Joe MarkarianFRCOG Special Projects

781-588-2050

Introduction

What happens at what time of Year

Who should be involved

What policies should your town have

Insights into best practices

Pitfalls to avoid

What Happens When

Legally required Accountant, Treasurer, Collector, Assessors DLS Municipal Calendar

www.mass.gov/dls-->dls publications

Discretionary actions Select Board, Finance Committee Town Administrator / Coordinator Department Heads

Source of Authority

Mass General Laws DLS Legal Index for Municipal Officials Subject matter index MGL Chapter-Section search

Chapter 39 & Chapter 40 – Towns Chapter 41 – Individual Officers Bylaws / Charters Municipal Finance Reference

www.frcog.org Publications Regionalization & Special Projects

Responsibilities Select Board

Ethics Guide

Finance Committee MGL Chapter 39 §16

who shall consider any or all municipal questions for the purpose of making reports or recommendations to the town

Ethics Guide

Town Administrator / Coordinator Capital Improvement Committee / bylaws Accountant, Treasurer, Collector, Assessor…

Association manuals

Finance-Related Events

Note: activity in early 1st half of FY

Closing the books / balance sheet

Statement of Indebtedness

Schedule A

Tax bills

Tax Recap Sheet

Operating budget

Capital budget

Closing the Books

Accountant responsibility(With reliance on other departments)

DOR: complete by July 15(More typical: end of August)

Means of identifying problems

First step toward Free Cash certification

July: Look Back

Select board / FinCom / TA-TC

Budget report (aka Expenditure Report)

ID revenue / appropriation deficits

Take corrective actionSB/FinCom transfer by July 15 w/ limits

Town meeting action before Tax Recap filed

ID issuestimely completion of tasks / info exchange

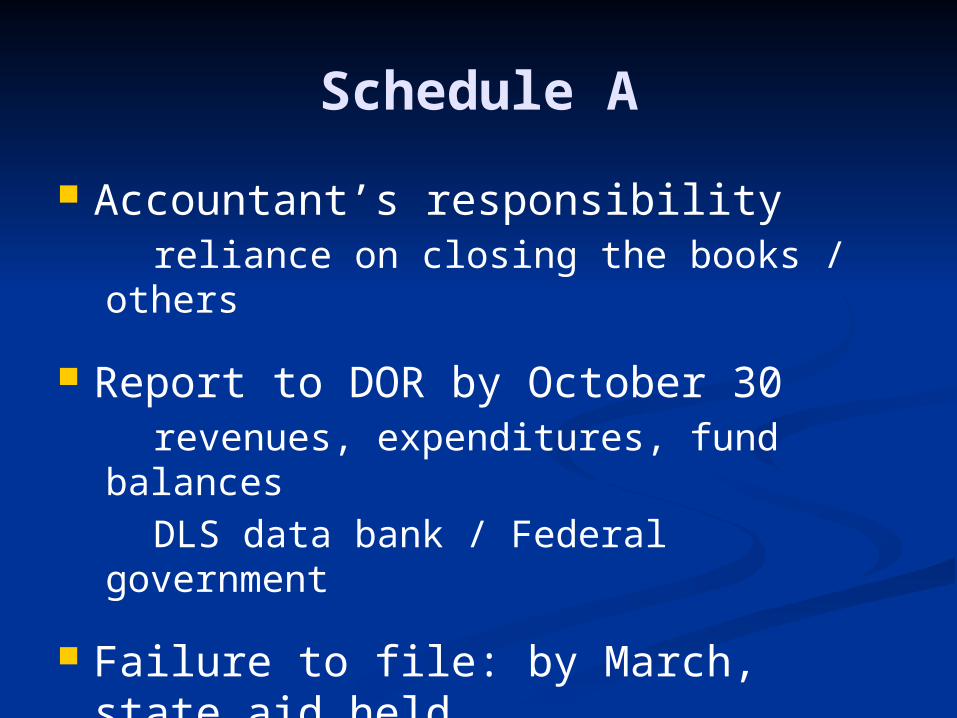

Schedule A

Accountant’s responsibilityreliance on closing the books / others

Report to DOR by October 30revenues, expenditures, fund balances

DLS data bank / Federal government

Failure to file: by March, state aid held A reference / should monitor progress

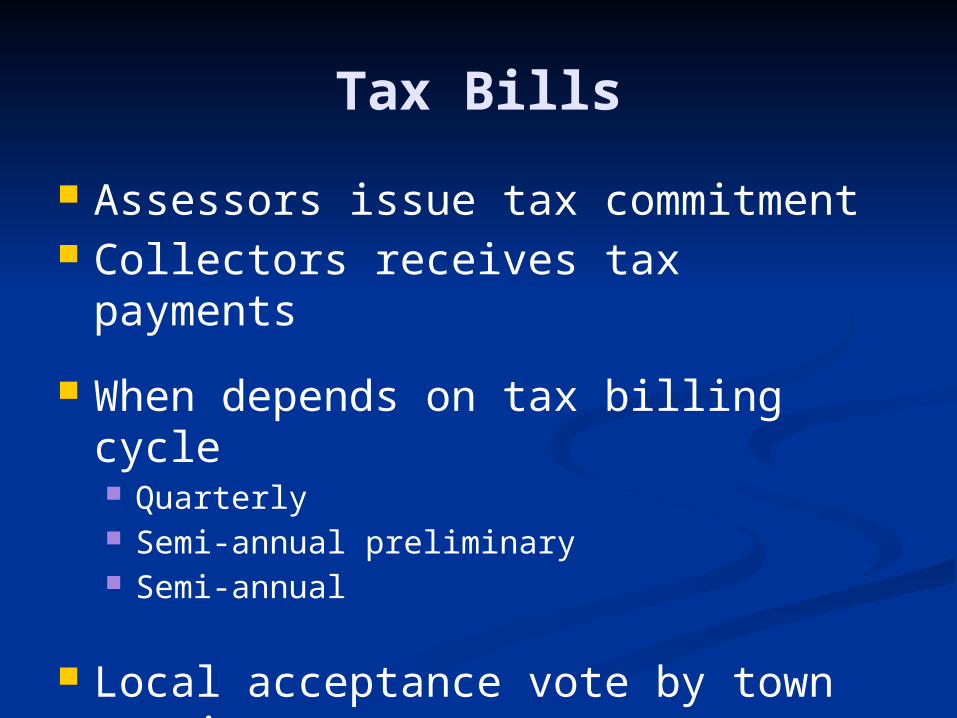

Tax Bills

Assessors issue tax commitment Collectors receives tax payments

When depends on tax billing cycle Quarterly Semi-annual preliminary Semi-annual

Local acceptance vote by town meeting

Tax Recap Sheet

Assessors: page 1 Accountant: pages 2 & 3 Town Clerk: page 4

Basis for DOR approval of taxation / rate Due date: depends on billing cycle

Prior to Oct. 1 or Jan. 1 Critical information

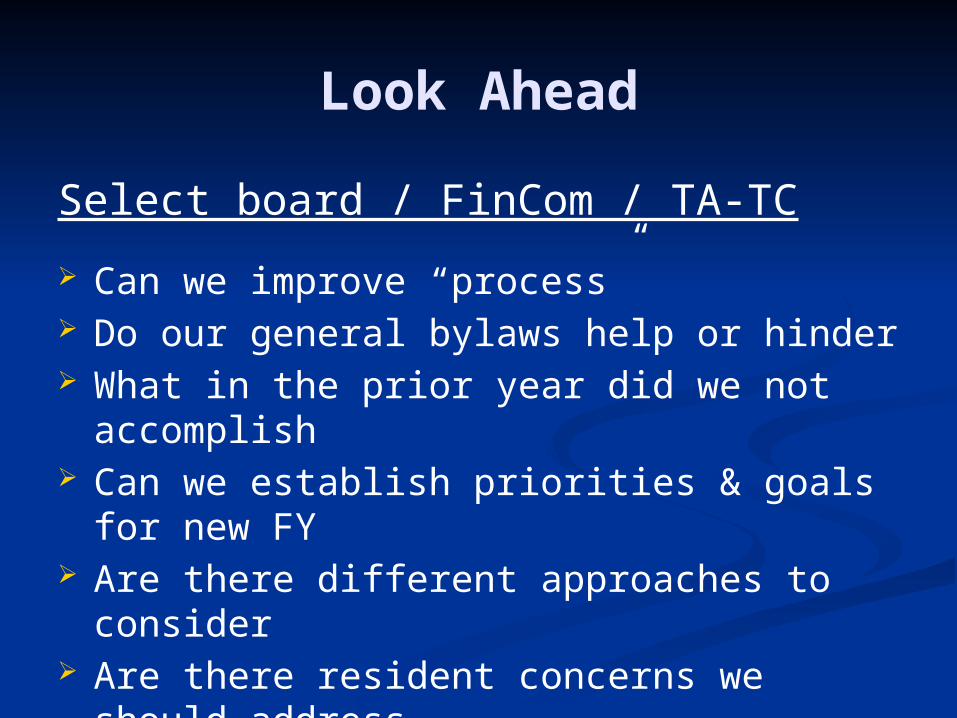

Look Ahead

Select board / FinCom / TA-TC

Can we improve “process” Do our general bylaws help or hinder What in the prior year did we not accomplish Can we establish priorities & goals for new FY Are there different approaches to consider Are there resident concerns we should address Can planning begin for major projects in future

Look Ahead (cont)

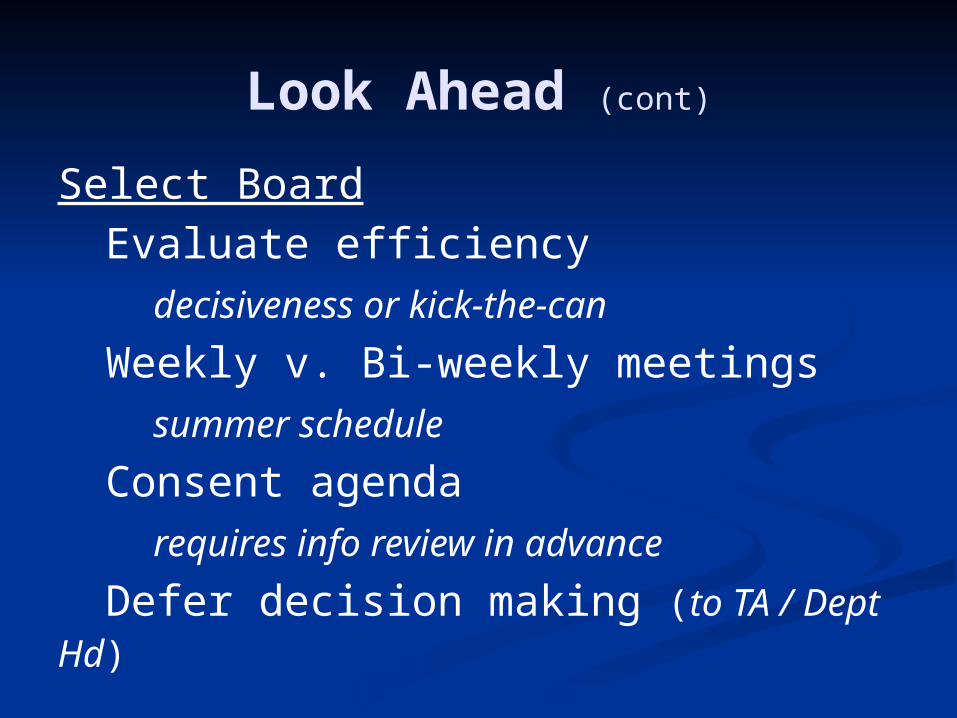

Select Board

Evaluate efficiency

decisiveness or kick-the-can

Weekly v. Bi-weekly meetings

summer schedule

Consent agenda

requires info review in advance

Defer decision making (to TA / Dept Hd)

Look Ahead (cont)

Finance Committee

Evaluate role & efficiency

reduce number of meetings

use budget modules

improve forms

evaluate budget format

Review budget calendar

Finance Committee Role

1) All municipal questions vs. Finance articles only

2) Budget formulator vs. Budget watchdog

3) Report / Budget Message

4) Recommendations

5) Transfers

6) Monitoring fiscal activity

7) Revenue projections

8) A resource

9) A policy maker

10) Dual role as capital improvement committee

11) Advocate on ballot questions 12) Web page

Ongoing / Sept - March

Monitor the budget (expenditure reports)

Cash reconciliations (accountant/treasurer)

Receivable reconciliations (accountant/collector)

Monitor Committees Prepare for Town Meeting Communicate: SB & TA/TC; Dept mtgs

Best Practices

Community Compact Best Practice Areas Finance related:

Budget documentFinancial policiesLong range planning / forecastingCapital planningReview financial management structureRegionalization / Shared Services

Budget Document

Components Budget message Narrative Line-item appropriations Articles Supplemental information

Product of good budget process

Budget Process

1) Identify those with roles/responsibilities

2) Agreement on a budget calendar

3) Lineal process

4) Formalize (codify) the process

5) Recommend a balanced budget

6) Strive for structural balance

7) Terms / concepts to understand

Calendar Milestones

Revenue projections / Five year forecast Departmental guidelines / requests Data assemblage – working budget Meetings / hearings Balanced budget recommendation Board of Selectmen approval Finance Committee review Town Meeting vote

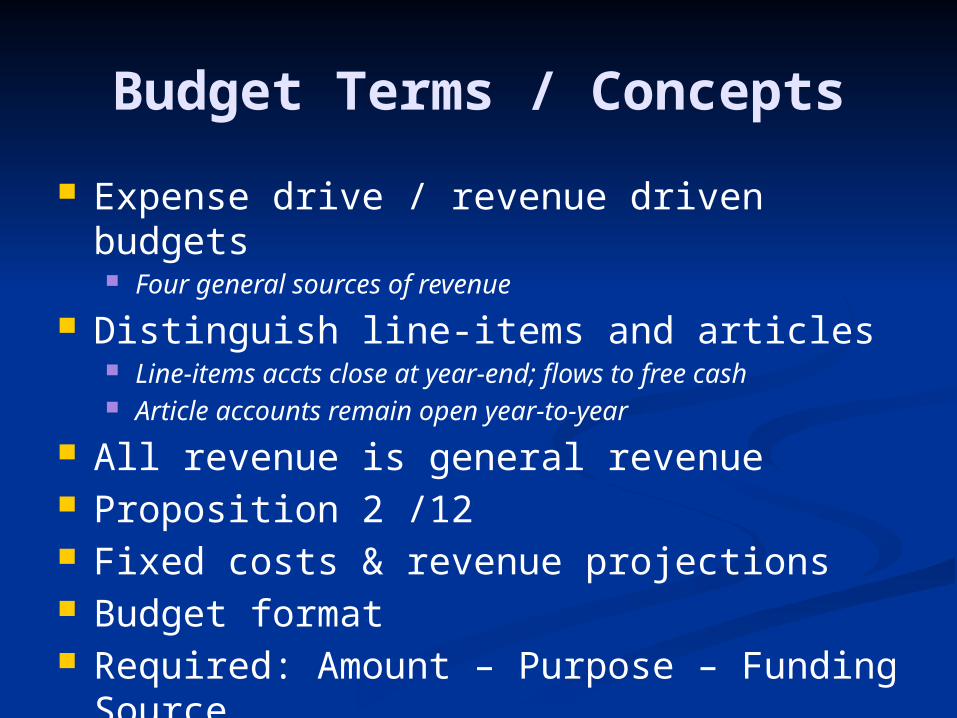

Budget Terms / Concepts

Expense drive / revenue driven budgets Four general sources of revenue

Distinguish line-items and articles Line-items accts close at year-end; flows to free cash Article accounts remain open year-to-year

All revenue is general revenue Proposition 2 /12 Fixed costs & revenue projections Budget format Required: Amount – Purpose – Funding Source

Revenue Projections & Fixed costs

Deduct fixed costs:-debt service

-pension obligations

-OPEB (retirees’ health)

-health insurance (active)

-property / casualty insurance

-workers’ compensation

-Medicare

-utilities

-known deficits

Results in discretionary revenue

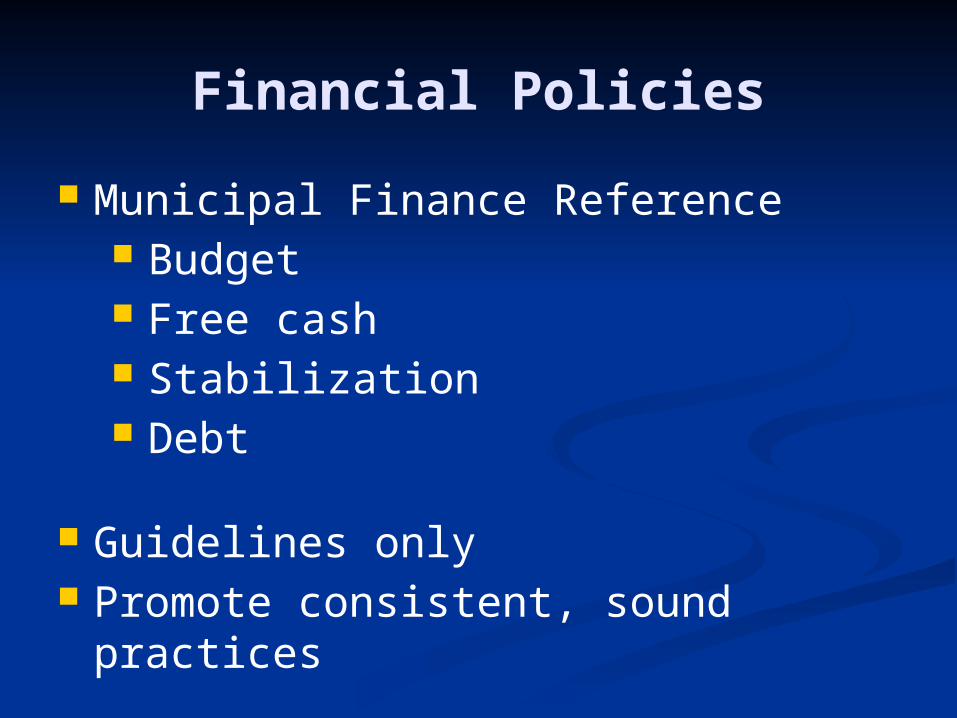

Financial Policies

Municipal Finance Reference Budget Free cash Stabilization Debt

Guidelines only Promote consistent, sound practices

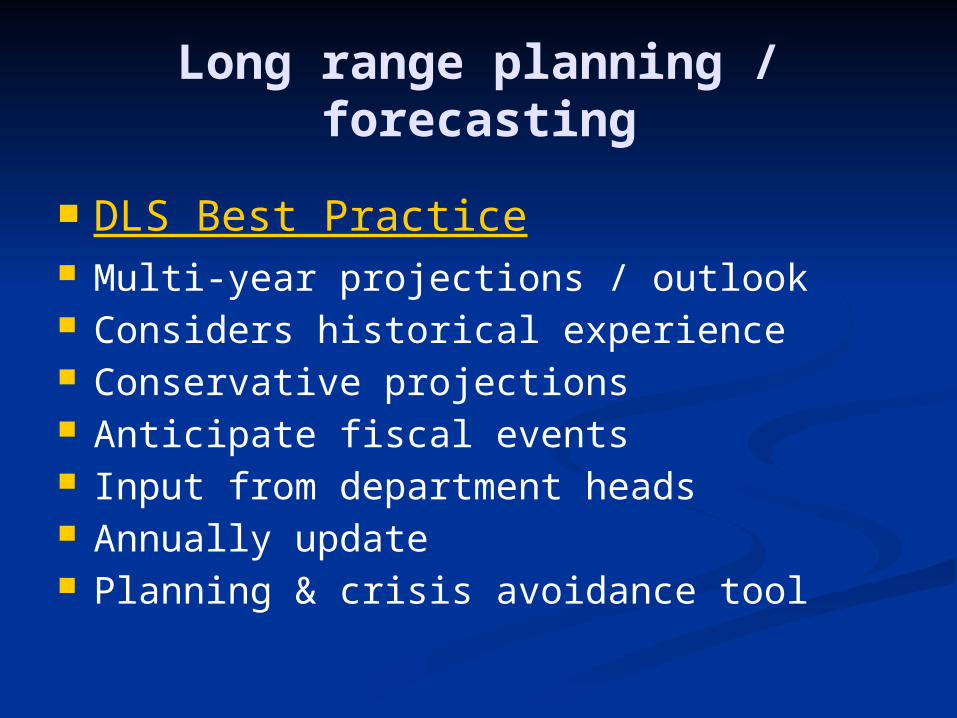

Long range planning / forecasting

DLS Best Practice Multi-year projections / outlook Considers historical experience Conservative projections Anticipate fiscal events Input from department heads Annually update Planning & crisis avoidance tool

Capital Planning - Why?

Ensure long-range physical integrity of the town

Track condition / needed investment in:

Buildings Rolling stockInfrastructure TechnologyRoads Equipment

Prioritize town-wide needs

Allocate resources among competing needs

Establish level playing field

Improve credit standing

Goals of CIC / CIP

Credibility

Establish a well-defined process Commit to year-to-year consistency Demonstrate open-minded/objectivity Be engaged, but also challenge Arrive at well-founded decisions

Exercise good judgment & common sense

Capital Planning

Role of a Capital Improvement Committee Determine who serves on the CIC Be clear who the CIC reports out to Define the Capital budget process? Calendar milestones Determine information to collect Set ranking criteria / basis of analysis Provide funding & place in budget

Financial Management Structure

Accountability

How to get there: Appointed positions (v. elected) Appointing authority Budget control Clear job descriptions Departmental goals Clear expectations

Regionalization / Shared Services

Reasons to explore:

Positions increasingly harder to fill Appeal: two towns sharing a F-T w/ benefits Shared training costs: higher quality service Fewer reasons for town hall visits

To start: internal conversations

communicate with other towns

Pitfalls to Avoid

Failure to keep current with duties

Neglect of checks & balances

Failure to monitor

Indecisiveness

Lack of communication

Adversarial government

Mission to Mars

Hawaii Space Exploration Analog and Simulation (HI-SEAS)

Boston Globe Sept. 6

Visit to Mars simulation

3 women & 3 men

Two-story dome

Mauna Loa volcano

8 months

Mission to Mars (cont)

Question: Is there any relevance of findings to town government.

-Defined roles, but not always. With rotation, work improved. Understand others’ role.

-Debriefs were critical following an important assignment. Communication =>solutions

Mission to Mars (cont)

-Orientation mattered. Advanced discussions helped smooth way.

-Leadership is flexible. Success occurs when all voices are heard.

-Teamwork is more powerful than individual performance.

The End

Supplemental Slides

Statutory Source of Authority

Massachusetts General LawsChapter 39 Section 16

Every town whose valuation for the purpose of apportioning the state tax exceeds one million dollars shall, and any other town may, by by-law provide for the election or the appointment and duties of appropriation, advisory or finance committees, who shall consider any or all municipal questions for the purpose of making reports or recommendations to the town; and such by-laws may provide that committees so appointed or elected may continue in office for terms not exceeding three years from the date of appointment or election.

In every town having a committee appointed under authority of this section, such committee, or the selectmen if authorized by a by-law of the town, and, in any town not having such a committee, the selectmen, shall submit a budget at the annual town meeting.

State Ethics Law

Massachusetts State Ethics Commission

www.mass.gov/ethics/

MGL Chapter 268A

Advisory Opinions

Guide for Municipal Finance Committee Members

Open Meeting Law

Office of the Massachusetts Attorney General

MGL Chapter 30A §§18-25

Definition: “Meeting” & “Deliberation”

Open Meeting Law Guide

Notice RequirementsMinutes

Executive Session

Public Records Law

Office of the State Secretary

Public Records Division

MGL Chapter 66

Guide to the Massachusetts Public Records Law

Public Records Definition MGL c. 4, § 7, cl. (26)

Record Retention Schedules“Administrative Use”

Office of Campaign & Political Finance

http://ocpf.cloudapp.net/

Search Legal Opinions

Financial Activity

Fiscal Year:

Departments authorized to spend on July 1

Procurement rules (MGL Chapter 30B)

Personal Service Contracts

Goods or services must be received (c. 41 § 56) Purchase Order System

Accountant verification process

Expenditure Reports (c. 41 § 58)

Finance Committee Role

Ultimate goal: Committee Credibility

ConsistentObjective

Well informedWell reasoned

RespectfulConsensus over conflict

Town interest over personal preference

Four Major Revenue Sources

DLS Article: Municipal Budget Revenues

Revenue Sources:Tax Levy

State Aid

Local Receipts

Miscellaneous (non-recurring)

Increase Revenue Detail

Tax Levy: Levy Limit Calculation FormNew Growth Estimate

State aid: Cherry Sheet - Chapter 70 & Unrestricted General Government Aid

Cherry Sheet Manual

Local Receipts: Tax Recap page 3

Misc: Close look at available funds – free cash, assessors’ overlay, other.

Expense side Budget format

No required format or level of detail for towns Format impacts Dept. Heads’ ability to manage Review format vs. Town Meeting presentation

Role of Policies Guidelines, not rules

Revenue deficits Deduct from free cash & raise on next year’s Recap

Appropriation deficits Deduct from free cash

Taxpayer recourse 10 taxpayer suit; order of mandamus

Proposition 2 ½

MGL C. 59 § 21C

Levy CeilingLevy Limit

LevyNew Growth

Overrides & UnderridesDebt & Capital Exclusions

Special ExclusionStabilization Fund Override

Excess Levy Capacity

Annual Levy Ceiling

To Calculate the New Levy Ceiling

Total Assessed Valuation

Property values are reviewed and adjusted annuallyIf values increase, ceiling rises

If values decrease, ceiling decreases

Annual Levy Limit

To Calculate New Levy Limit

Begin with Last Year’s Levy Limit

New Growth

To Calculate theNew Growth Factor

Proposition 2½ Limit Exceptions

Overrides

Underrides

Debt Exclusions

Capital Outlay Exclusions

Stabilization Fund Overrides

Special Exclusions

Non-specific After year 1

Comparison of Referenda Questions

Overrides Exclusions

Operating Budget

Only Capital Purchases

PermanentTemporary

Debt(Life of Bond)

Capital(1 Year)

Overrides Limited by CeilingNo Limit on the Number

Or Dollar Amount

Stabilization Fund Override

DLS IGR 04-201MGL c. 59 § 21C (g)

Alternative for funding special purpose stabilization fund

Year 1: 2/3s Town Meeting – maj. voter approval Year 2+: 2/3s Selectmen approval

-can continue, reduce, defer/resume Authorized amount increases 2½% annually If lowered, continues at lower amount + 2½% Change of purpose by voters via BOS 2/3s vote

Special ExclusionsSee Levy Limits Primer, page 12

-Water, sewer debt exclusion for capital projects &assist homeowners: faulty septic, UST, lead paint

-BOH contracts for work / costs added to tax bill

-Temporary increase not added to tax base

-Allows raising water or sewer debt service on tax rate, but requires corresponding decrease in rates

-Adopted by majority vote of Selectmen

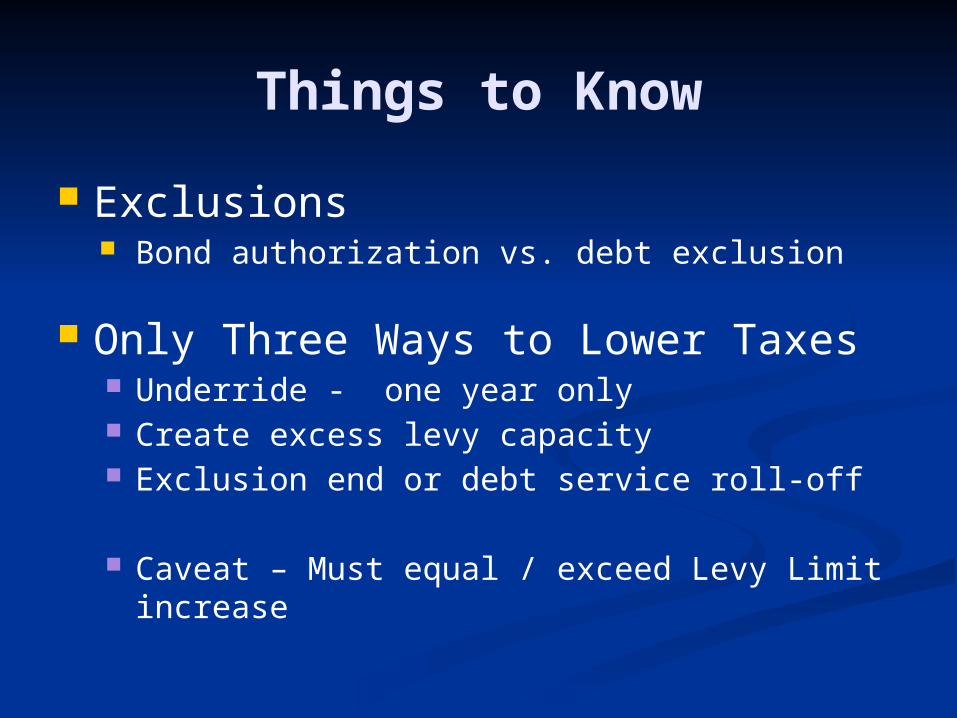

Things to Know

Exclusions Bond authorization vs. debt exclusion

Only Three Ways to Lower Taxes Underride - one year only Create excess levy capacity Exclusion end or debt service roll-off

Caveat – Must equal / exceed Levy Limit increase

Property Taxes

Tax rate = levy / total AV x 1000

Property tax = home AV /1000 x tax rate

DLS Financial Calculators Debt Service calculator Tax Impact Calculator

Revenues

Statutory Treatment of Municipal Revenues

All revenue, received or collected from any source and by any department is General Fund revenue.

General Fund money is unrestricted and available for expenditure for any lawful purpose.

Money can only be segregated for specific purposes if authorized a general law or special act.

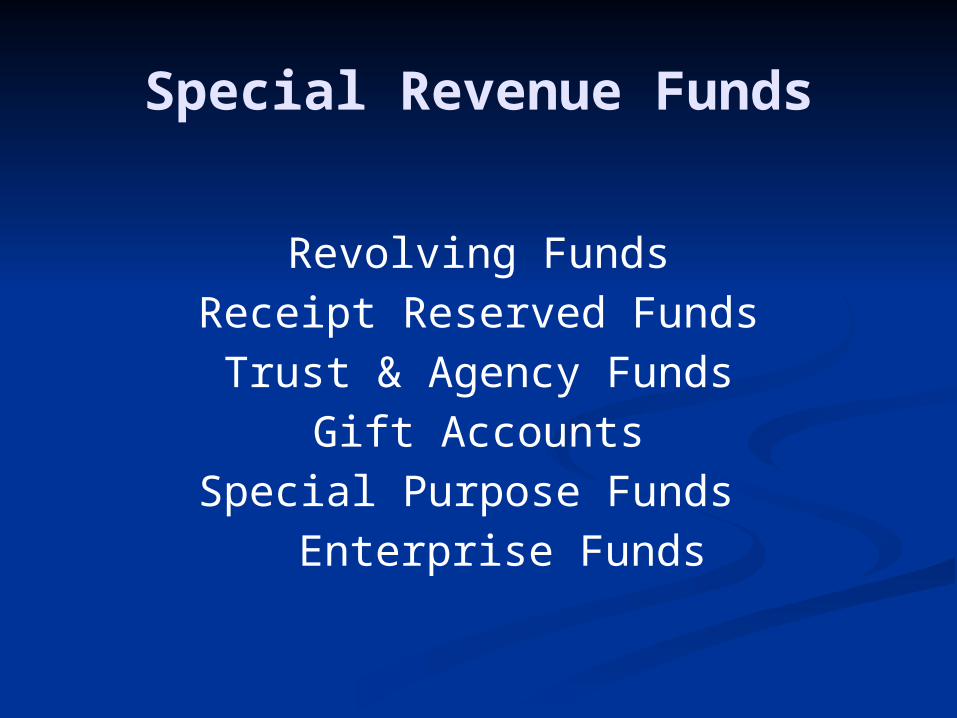

Special Revenue Funds

Revolving Funds

Receipt Reserved Funds

Trust & Agency Funds

Gift Accounts

Special Purpose Funds

Enterprise Funds

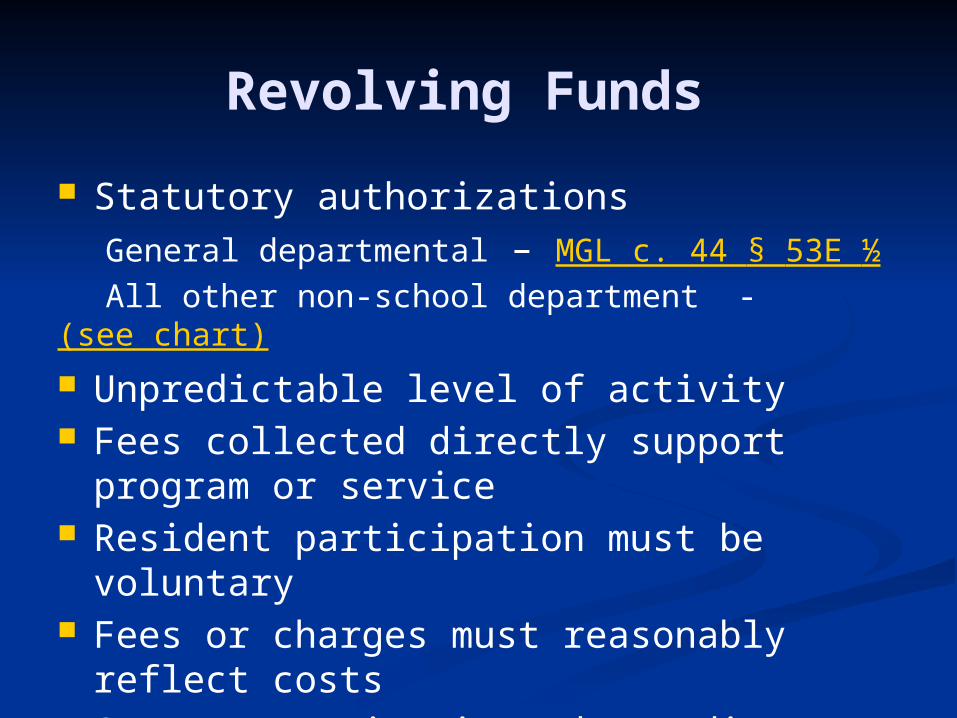

Revolving Funds

Statutory authorizations

General departmental – MGL c. 44 § 53E ½

All other non-school department - (see chart) Unpredictable level of activity Fees collected directly support program or service Resident participation must be voluntary Fees or charges must reasonably reflect costs Statutory criteria and spending restrictions apply Town Meeting approval required

Receipt Reserve Accounts

Authorized by statute; established by Town Meeting

Revenue held in separate account for a particular purpose

Year-end balances roll-over to next year

Funds must be appropriated

Funds must be received before appropriated

Trust & Agency Funds

A fiduciary fund

Funds collected by town but intended for another government entity

Not credited to town as a cash receipt

Gift Accounts Money given generally to town must be

accepted and appropriated by Town Meeting

Money given to board, department or official, can be spent with approval of Selectmen

Spending purpose must be in accordance with donor’s wishes

Not subject to Ant-Aid Amendment

Gift of real estate requires Town Meeting acceptance

Enterprise Funds

MGL c. 44, § 53F 1/2

Enterprise Fund Manual

DLS Information Guideline Release 08-101

Enterprise Funds (cont.)

May be set up forwater, sewer, trash disposal

ambulance service, nursing homes

skating rinks, pools, golf courses

airports, docks, marinas

Two Town Meeting votes required:

-create the enterprise fund

-approve the budget

Enterprise Funds (cont.)

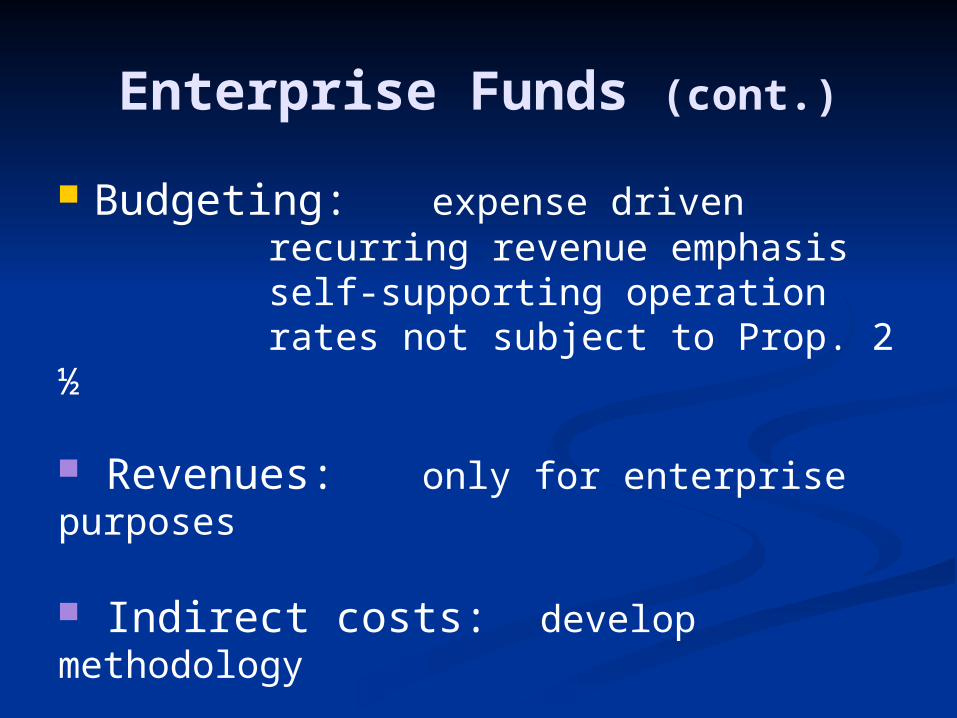

Budgeting: expense driven recurring revenue emphasis self-supporting operation rates not subject to Prop. 2 ½

Revenues: only for enterprise purposes

Indirect costs: develop methodology

Retained earning: like free cash

Reserves

FinCom Reserve

Free Cash

General Stabilization Fund

Special Purpose Stabilization

Enterprise Fund Reserves

Overlay

FinCom Reserve

Chapter 40 § 6 Extraordinary or unforeseen

Includes emergency Includes “inconvenience” factor

Reserve amount: look to historical demand Require transfer request form / copy accountant Town Administrator approval first Approval at discretion of FinCom / Consistency

Free Cash

Unrestricted funds from prior year operations Calculated from Balance Sheet as of June 30 Available for appropriation only on DOR cert. Results from:

Actual receipts in excess of revenue estimates Unspent departmental appropriations Unexpended free cash from prior year Offset by receivables and certain deficits

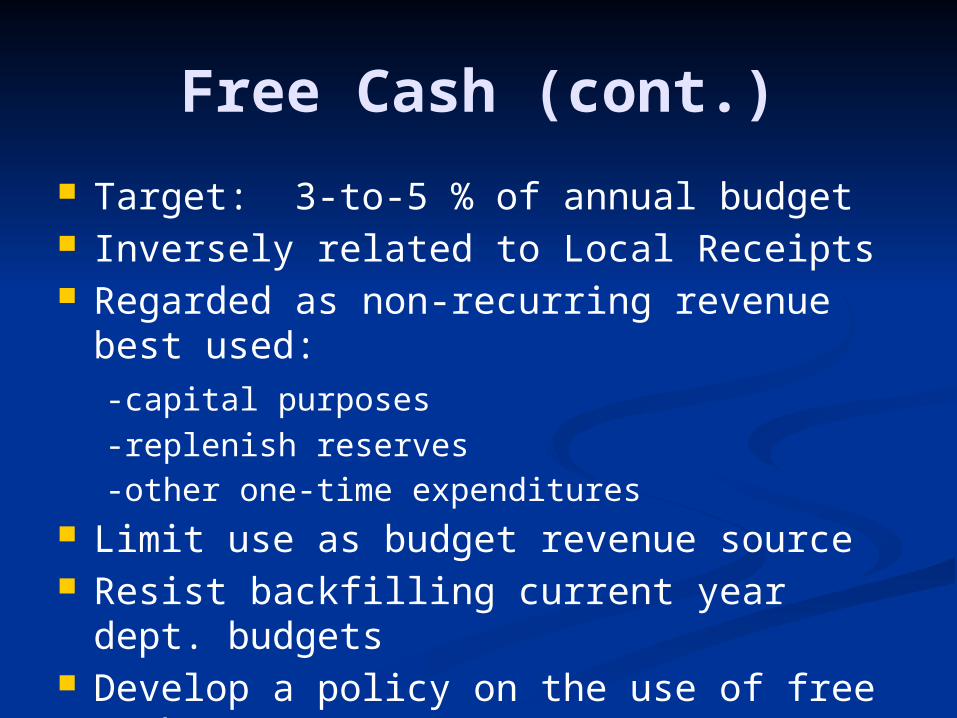

Free Cash (cont.)

Target: 3-to-5 % of annual budget Inversely related to Local Receipts Regarded as non-recurring revenue best used:

-capital purposes

-replenish reserves

-other one-time expenditures Limit use as budget revenue source Resist backfilling current year dept. budgets Develop a policy on the use of free cash

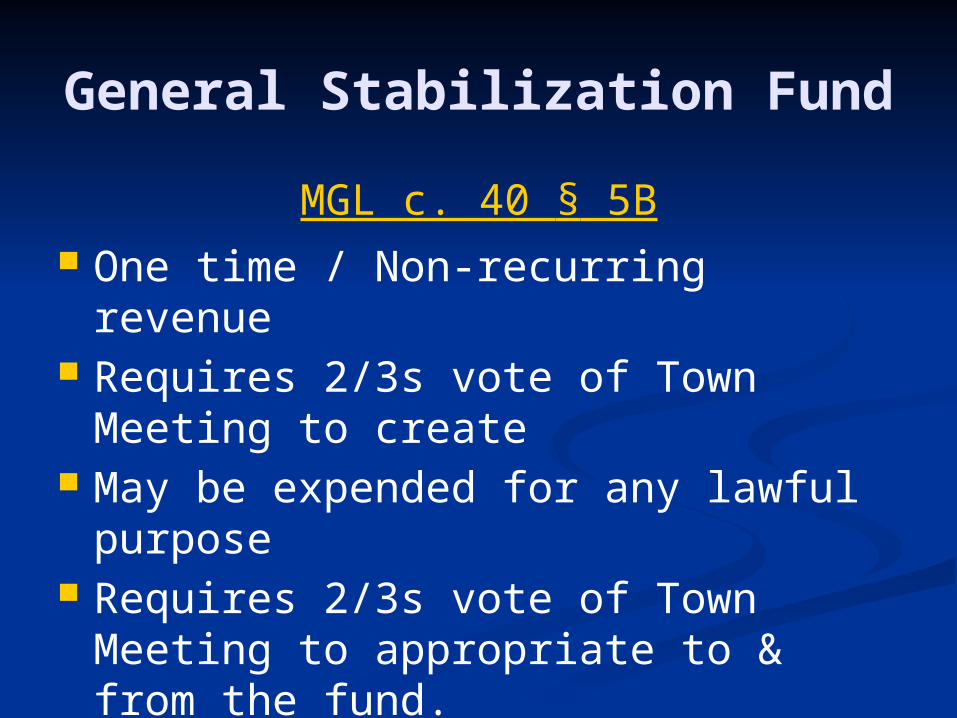

General Stabilization Fund

MGL c. 40 § 5B One time / Non-recurring revenue Requires 2/3s vote of Town Meeting to

create May be expended for any lawful purpose Requires 2/3s vote of Town Meeting to

appropriate to & from the fund.

Special Purpose Stabilization

DLS IGR 04-201

DLS Article: Long Term Planning Tool