multi-stage capital investment opportunities as compound real options

TRANSCRIPT

This article was downloaded by: [Princeton University]On: 05 October 2013, At: 15:20Publisher: Taylor & FrancisInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House,37-41 Mortimer Street, London W1T 3JH, UK

The Engineering Economist: A Journal Devoted to theProblems of Capital InvestmentPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/utee20

MULTI-STAGE CAPITAL INVESTMENT OPPORTUNITIES ASCOMPOUND REAL OptionsHEMANTHA S.B. HERATH a & CHAN S. PARK ba University of Northern British Columbiab Auburn UniversityPublished online: 31 May 2007.

To cite this article: HEMANTHA S.B. HERATH & CHAN S. PARK (2002) MULTI-STAGE CAPITAL INVESTMENT OPPORTUNITIES ASCOMPOUND REAL Options, The Engineering Economist: A Journal Devoted to the Problems of Capital Investment, 47:1, 1-27

To link to this article: http://dx.doi.org/10.1080/00137910208965021

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the “Content”) containedin the publications on our platform. However, Taylor & Francis, our agents, and our licensors make norepresentations or warranties whatsoever as to the accuracy, completeness, or suitability for any purpose of theContent. Any opinions and views expressed in this publication are the opinions and views of the authors, andare not the views of or endorsed by Taylor & Francis. The accuracy of the Content should not be relied upon andshould be independently verified with primary sources of information. Taylor and Francis shall not be liable forany losses, actions, claims, proceedings, demands, costs, expenses, damages, and other liabilities whatsoeveror howsoever caused arising directly or indirectly in connection with, in relation to or arising out of the use ofthe Content.

This article may be used for research, teaching, and private study purposes. Any substantial or systematicreproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

HEMANTHA S.B. HERATH University of Northern British Columbia

CHAN S. PARK Auburn University

Real options provide a new and productive way to view corporate investment decisions as options. Multi-stage or sequential-investment decisions are an important class of real options with embedded managerial flexibility. These multi-stage real options involve a bundle of interrelated investment opportunities. with the early upstream opportunities creating potentially valuable discretionary downstream opportunities. We investigate a multi-stage project setting where each investment opportunity derives revenue's from different markets but share common technological resources. In such a setting, one should consider the underlying asset volatility of each investment opportunity in a compoundsptions framework. In this paper, we extend the binomial lattice framework to model a multi-stage investment as a compound real option when several uncorrelated underlying variables exist. Volatility estimation is important for implementingreal option models. Therefore. we develop the theoretical framework for estimating the volatility parameter of an underlying variable using Monte Carlo simulation technique.

Real option analysis is a relatively new and insightful way to think about

corporate investment decisions. It is based on the premise that any corporate

decision either to invest in or divest real assets can be viewed as an option. This

type of option is similar to a financial call option in that it gives the holder a

right but not an obligation to undertake an investment. Viewed in this way, the

use of real options provides corporate decision-makers with greater flexibility

and in the process also with a better method to value alternative investment

actions. Managerial flexibility is quite important in an uncertain and changing

economic environment from a strategic decision-making perspective. It enables

corporate decision-makers to keep investment options open and thus allows

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

uncertain market conditions to be converted into more favorable market opportunities, as new information becomes available.

Many researchers have emphasized the importance of real option analysis for corporate investments decisions, including Myers [17,18,19], Trigeorgis and Mason [25], Mason and Merton [16], Brennan and Schwartz [2], Paddock, Siegel and Smith [21], Luehrman [15], Copeland and Keenan 141, Dixit and Pindyck [7], and Ross [24]. Using the concept of time, intrinsic value and opportunity loss concept, Park and Herath [231 illustrate the value of managerial flexibility to delay a project. In addition, other researchers have used real option analysis to value natural resource development projects, patents, and licenses with limiting quotas, software development and insurance policy decisions, among many other applications.

When undertaking new investments, firms may have the option to invest in stages. Often firms may also find that it is better to recast a lumpy investment project with high.uncertainty, into a series of options to expand with each option being dependent on the earlier option. Undertaking the investment in stages has several advantages. Projects that turn out to have negative NPV on a full-scale basis may actually create value if undertaken in stages. Also, projects that may look attractive on a full-scale basis may look more attractive if undertaken in stages after resolving uncertainty. Research and development (R&D) projects, phased-out new product or market entry decisions, and sequential business acquisition decisions are only a few examples of multi-stage investment decisions in which the initial investment often leads to future opportunities.

Any multi-stage investment, such as R&D, should be valued u h g option pricing technology. The characteristics of R&D projects include high uncertainty associated with project cash flows, unavailability of immediate payoffs to justify the initial investment and existence of multiple sources of uncertainty at different project phases. Application of real option pricing has been proposed for valuing R&D projects in the capital budgeting literature (Myers [18,19], Nichols [2O], Faulkner [S], Herath and Park [12], Herath, Jahera and Park [ l l ] , and Angelis [I]). Using Gillette's Mach 3 project case as an example. Herath and Park [12] illustrate how R&D valuation can be combined with strategic decision-making. Panayi and Trigeorgis [22], as another example, examine multi-stage real options using the standard R&D example. They analyze two actual case studies involving an information technology infrastructure decision and an international expansion opportunity by a bank. The standard Black and Scholes model is used to price the multi-stage real options. In this particular case, although multi-stage real options have been

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

correctly identified as a compound option, they have not been modeled as a compound real option.

More recently, however, researchers have emphasized that most capita1 investments, including R&D, should be modeled as compound options (Cortazar and Schewartz [ 5 ] , Copeland and Keenan [4], Darnodaran [6], Copeland and Antikarov (31, Herath and Barth [lo]). Compound options are options whose value depends on other options. There are two types of compound options. Geske [9] obtained a close form solution to a compound option problem by replacing the standard normal distribution in a simple option model with a bi- variate normal distribution. Geske's compound option is a simultaneous option because the options are alive at the same time. Copeland and Antikarov [3] solve this simultaneous compound option problem using a binomial lattice approach to evaluate a multi phased construction project. Most capital investment decisions including R&D are multi-stage investments or sequential compound options. When the first option is exercised it creates another option.

Copeland and Antikarov [3] model two types of sequential compound options using the binomial lattice approach. First, they model a twephase construction project that depends on a single underlying variable. Second, they consider a rainbow type compound option in which the value of the underlying asset is driven by two sources of uncertainty. Both cases of correlated and un-

correlated uncertainties are considered. Copeland and Antikarov compound options are restrictive in that they deal with only a single underlying variable. In this paper, we develop a sequential compound option model contingent on several un-correlated underlying variables using the lattice framework. In this setting, the down stream investment opportunity would require the acceptance of the upstream investment opportunity. The series of investment opportunities

would share technological resources but each project would derive revenues from different markets. The model is general as each underlying variable refers to an incremental downstream project. Further, we also develop and illustrate the theoretical framework for estimating the volatility parameter of an underlying variable using Monte Carlo simulation. Volatility estimation is important for implementing real option models.

The remainder of the paper is organized as follows. First, we present the multi-stage decision framework using an R&D example. Second, we develop a compound real option valuation model contingent on several uncorrelated underlying variables by extending the binomial lattice approach with-in the multi-stage decision framework. Third, we develop and illustrate the theoretical framework for estimating the volatility parameter for a project. Fourth, we illustrate our model using a hypothetical case in manufacturing. Lastly, we

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

discuss how the compound option model can be used as a value creating strategy in contrast to the traditional net present value (NPV) method.

Valuation of R&D projects is quite complex due to the substantial uncertainties in a project's life-cycle phases. A series of sequential decisions has to be made throughout out the project life cycle moving from the R&D phase into the commercialization phase. Each of these phases has different associated risks and uncertainties. The sequential nature of R&D projects continuously provides decision-makers with choices regarding whether and when to undertake future potential investment opportunities. This means that when valuing R&D projects decision-makers should take these factors into account. Consequently, the economic value of an RgiD investment should include the option values associated with various opportunities to alter the course of a project as it progresses through the sequential life-cycle phases.

An initial R&D investment provides the company with the right to invest even more to introduce the new product if the R&D is successful. If there is a favorable market for the new product then the real option to introduce the new product wiIl be exercised. This course of action in turn, provides the management with the right to expand commercialization, preferably in several stages depending on how events proceed so as to minimize unnecessary costs and inventory. Suppose, after the new product is introduced, the management concludes that the initial cash flow estimates of the first expansion opportunity can be realized. Then they would exercise the first expansion option, which in turn would give them the right to a second expansion later if conditions are favorable. The value of an R&D project should thus be viewed as the value of a compound option with nested investment opportunities that can potentially generate future cash flows and other real options. This multi-stage decision framework is shown in FIGURE 1.

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

TABLE 4: Parameters for the binomial lattices

Incremental gross project values

Volatility

~nvesbnent cost

Upside potential

Downside potential

Risk-free probability of upside change

R&D Investment

$35M

Product Introduction

VI = $182 M

First Expansipn

V2 = $245 M

a, = 30%

S250M

u2=1.35

dl= 0.74

pl= 0.54

2 1

Second Expansion

Vl= 5322M

a, = 35%

S275M

u3= 1.42

d,= 0.70

p3= 0.5 1

Using the binomial parameters in TABLE 4, we next develop the three lattices. Instead of the graphical presentation of a binomial lattice we used the spreadsheet form as shown in FIGURE 8. In the spreadsheet form, an upward movement is shown directly to the right and a downward movement is shown directly to the right but one step down. To develop the binomial lattice for each of the three real calls we work forward. For the one period real call C,. the initial gross project value is V , = 182. Therefore the two values at T= 1 would be Vl'= 182(1.49) = 27 1 or Vl- = 182(0.67) = 122. Similarly, for the one period real call C1, we obtain the following two values at T=2, an upward movement of V2+ = 245(1.35) = 331 and a downward movement of V;= 245(0.74) = 181. The initial gross project value is V2 = 245. We repeat the above procedure for the t w e period real call C3 to obtain the gross project values shown in the left-hand side of FIGURE 8. There are two values at T = 3, an upward movement V3+ =

322(1.49) = 457 and a downward movement of V{ = 322(0.70) = 227. At T= 4, the lattice has the following three vaIues: V3* = 457(1.42) = 649. V3-+ = 227(1.42) = 322 and V3- = 227(0.70) = 160.

Using the formulas developed in the preceding section, we calculate the real call option values shown in the lattice on the right-hand side (FIGURE 8). To price the compound R&D option we start with the inne'r most real call option C3 and then work backwards to value the nested real options C2 and C1,The real call C3 of the second expansion opportunity is a two period European-type call and would be valued by multiplying the terminal call values by the risk-free probabilities and then discounting by the short term interest rate at each node in the two period lattice. The terminal call values are,

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

Then by risk-neutral discounting we obtain the following values of C3+ and c,-:

Repeating the risk-neutral discounting again, we find the value of the real call C3. It is

To price the real call of the first expansion C2, recall that we need to consider both the incremental cash flow of the first expansion opportunity and the real option to undertake the second expansion C3. Therefore, the teiminal payoffs are

Lattices for the Gross Project Values ($Million)

Real Call Option Value: Nested Model ($ Million)

FIGURE 8: Gross project values and real call values

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

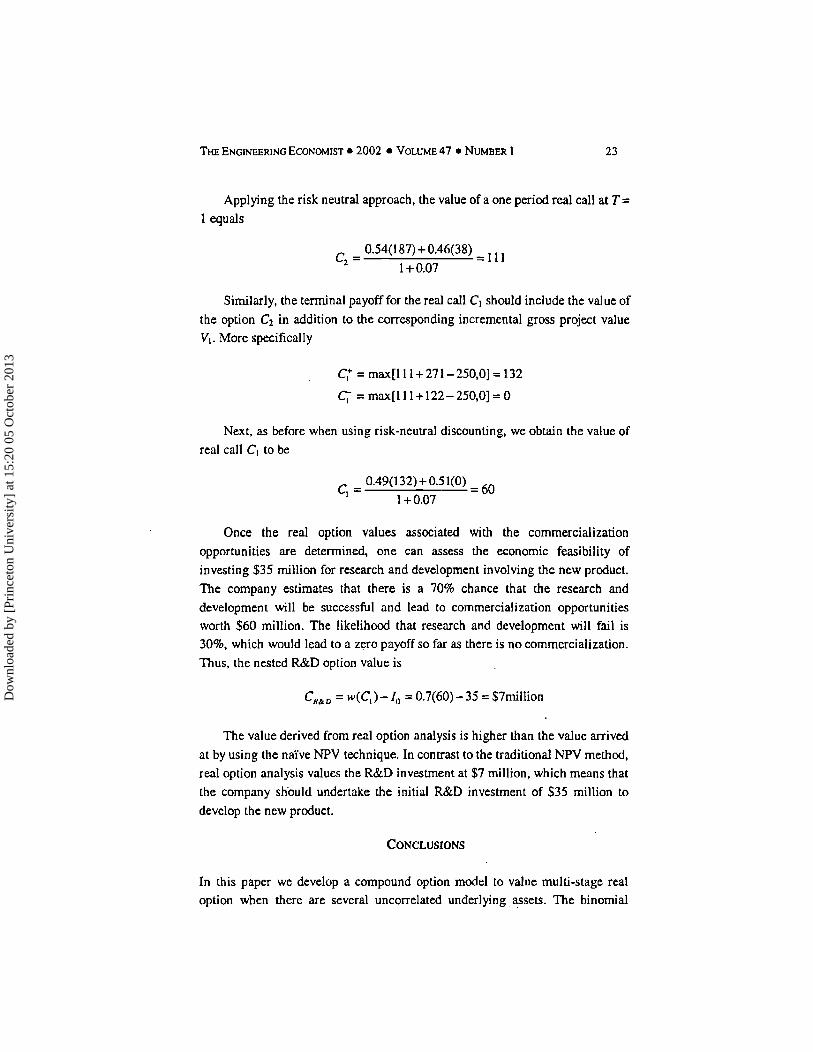

Applying the risk neutral approach, the value of a one period real call at T = 1 equals

Similarly, the terminal payoff for the real call C1 should include the value of the option C2 in addition to the corresponding incremental gross project value V, . More specifically

Next, as before when using risk-neutral discounting, we obtain the value of real call C, to be

Once the real option values associated with the commercialization opportunities are determined, one can assess the economic feasibility of investing $35 million for research and development involving the new product. The company estimates that there is a 70% chance that the research and development will be successfd and lead to commercialization opportunities worth $60 million. The likelihood that research and development will fail is 30%, which would lead to a zero payoff so far as there is no commercialization. Thus, the nested R&D option value is

C,,, = w(C, ) - I,, = O.7(60) - 35 = $7million

The value derived from real option analysis is higher than the value arrived at by using the nahe NPV technique. In contrast to the traditional NPV method, real option analysis values the R&D investment at $7 million, which means that the company should undertake the initial R&D investment of $35 million to develop the new product.

In this paper we develop a compound option model to value multi-stage real option when there are several uncorrelated underlying assets. The binomial

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

lattice framework provides greater modeling flexibility to analyze complex real options that exist in the real world. Our model is also consistent with the risk- free arbitrage method for pricing options. Standard option pricing models are often used to value complex real options, such as multi-stage investment because of modeling complexities. A major limitation of the application of standard option models to value real options is that an analyst can only consider a single source of uncertainty. Consequently, such models tend to be overly simplistic and therefore require substantial fine-tuning in the valuations before even attempting to use them. Our model allows an analyst to consider multiple underlying variables and thus multiple sources of uncertainty. This approach appears to be practical becausesin a muIti-stage red option the down-stream investment opportunities have different uncertainties than the upstream opportunities.

Our model also recognizes that multi-stage real options are nested within one another and thus values them accordingly. For example, the innermost option is valued as a standard option, whereas the others are valued as compound options. When valuing a compound real option the model considers both the values of the future real options that an exercise would generate as well as the incremental cash flows that could be realized. The limitation of the models is that we have assumed that the gross project values are un-correlated. We suggest that future research be directed at analyzing the situation in which they are correlated. While we have illustrated the modeling framework using the multi-stage R&D investment,. the framework is very general and appears to be

quite practical. We also illustrate the theoretical framework to estimate the volatility

parameter for a real option by developing the rate of return distribution using Monte Carlo simulation. This approach is flexible since any type and number of input distributions can be used to estimate the cash flows. Further, the volatility parameter is estimated directly using the gross project value, which is the underlying rather than a comparable stock.

'. The intrinsic value of a real call option at expiration is the net present value (NPV) of the project; the value if an immediate acceptance or rejection decision is made. NPV equals max [present value of cash flows - present value of investment, 01 or max [ V c , -I , 0] ((Park and Herath [23] and Luehrman [15]).

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

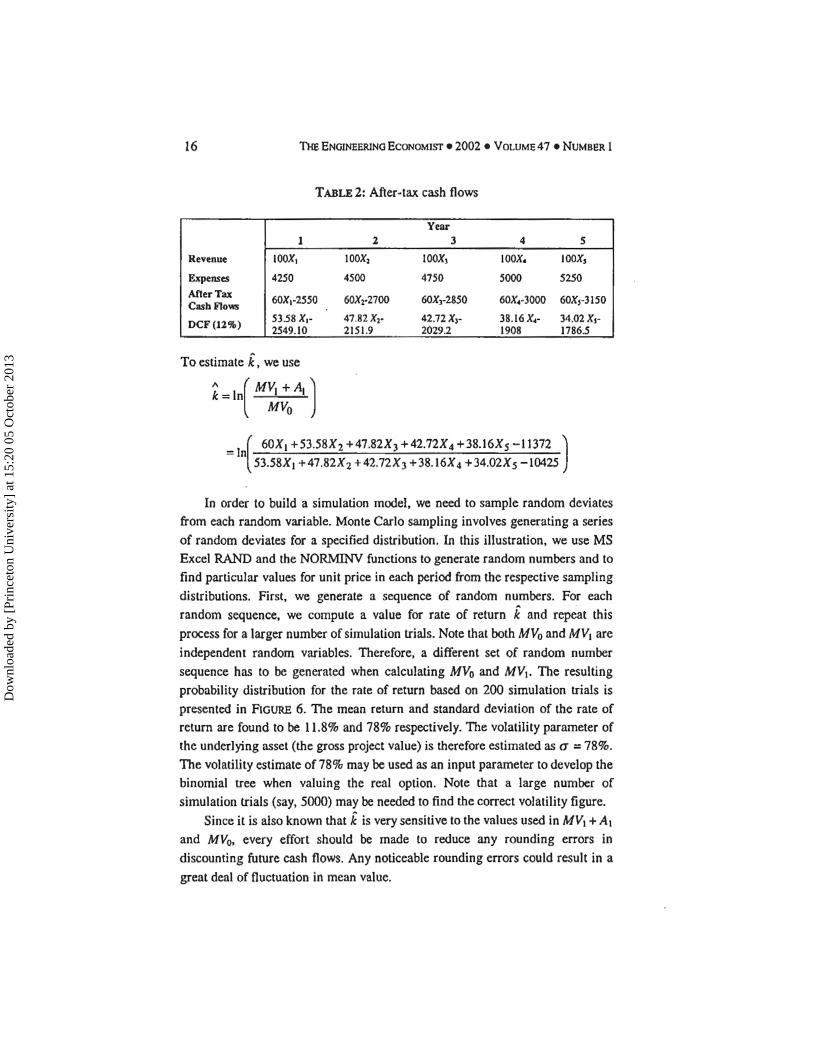

2. In the case of discrete compounding, it is easy to show that the rate of return is given byk = MV, -My-, +A, l MV,-,, where MV, is the market value of the project at time t and A, is the net cash flow at time t.

One can, also use the rate return formula based on wealth = I~[PW, / PY,] to generate the return distribution. Both approaches

will give equivalent results. The rate of return expression based on market value however, is more comparable with volatility estimation for stock option pricing

ANGELIS D.L. "Capturing the Option Value of R&D," Research Technology Management, (JulyIAugust), 2000, pp. 31-34. BRENNAN M.J., and E.S. SCHWARTZ, "Evaluating Natural Resource Investments," Journal of Business, Vol. 58, No. 2, 1985, pp. 135-157. COPELAND T., and V. ANTIKAROV, Real Options - A Practitioner's Guide, TEXERE Publishing Limited, 200 1. COPELAND T.E., and P.T. KEENAN, "Making real options real," The McKinsey Quarterly, No. 3, 1998, pp. 128-141. CORTAZAR G., and E.S. SCHWARTZ, " A Compound Option Model of Production and Intermediate Inventories," Journal of Business, Vol. 66, No. 4, 1993, pp. 51 7-540. DAMODARAN A., "The Promise of Real Options," Journal of Applied Corporate Finance, (Summer), Vol. 13, No. 9,2000, pp. 29-44. .

DINT A.K., and R.S. PINDYCK, Investment Under Uncertainty, Princeton University Press, 1994. FAULKNER T.W., "Applying Options Thinking to R&D Valuation," Research-Technology Management, May-June 1996, pp. 50-56. GESKE R., 'The Valuation of Compound Options", Journal of Financial Economics, Vol. 7 , 1979, pp. 63-81. HERATH, H.S.B. and J.R. BARTH, "A Nested Option Model for Multi-stage Capital Investment Decisions," Eighth Asia Pacific Finance Association (APFA) Annual Conference, Bangkok, Thailand, (July 22-25), 2001. HERATH H.S.B., J.S. JAHERA JR., and C.S. PARK, "Deciding which R&D Project to Fund," Corporate Finance Review, (MarchIApril), Vol. 5 , No. 5, 2001, pp. 33-45. HERATH H.S.B, and C.S. PARK, "Economic Analysis of R&D Projects: An Options Approach," The Engineering Economist, Vol. 44, No. 1, 1999, pp.

1-35.

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

13. KESTER W.C., "Today's Option for Tomorrow's Growth," Harvard Business Review, March-April 1984, pp. 153-160.

14. KULATILAKE N., "The Value of Flexibility: The Case of a Dual-Fuel Industrial Steam Boiler," Financial Management, Autumn 1993, pp. 271- 280.

15. LUEHRMAN T.A., "Strategy as a Portfolio of Real Options," Haward Business Review, September -October 1998, pp. 89-99.

16. MASON S.P., and R.C. MERTON, 'The Role ofcontingent Claim Analysis in Corporate Finance," Recent Advances in Corporate Finance, edited by Altman E. and Subrahmanyam M.. 1985. Irwin Publications.

17. MYERS S.C., "Fischer Black's Contribution to Corporate Finance," Financial Management, Val. 25, NO. 4, Winter 1996, pp. 95-103.

18. MYERS S.C., "Financial Theory and Financial Strategy," Interface, Vol. 14, January-February 1984, pp. 126-137.

19. MYERS S.C., "Determinants of Corporate Borrowing." Journal of Financial Economics, Vol. 5, NO. 2, 1977, pp. 147-176.

20. NICHOLS N.A., "Scientific Management at Merck: An Interview with CFO Judy Lewent," Harvard Business Review, Vol. 72, January-February 1994, pp. 89-99.

2 1. PADDOCK J.L., D.R SIEGEL and J.L. SMITH, "Options Valuation of Claims on Real Assets: The Case of Offshore Petroleum Leases," The Quarrerly Journal of Economics, August 1988, pp. 479-508.

22. PANAYI S., and L. 'TRIGEORGIS, "Multi-stage Real options: The Case of Information Infrastructure and International Bank Expansion," The Quarterly Journal of Economics and Finance, Vol. 38, Special Issue, 1998, pp. 675-692.

23. PARK C.S., and H.S.B. HERATH, "Exploiting Uncertainty-Investment Opportunities as Real Options: A New Way of Thinking in Engineering Economics," The Engineering Economist, Vol. 45, NO. 1, 2000, pp. 1-36.

24. Ross S.A., "Uses. Abuses, and Alternatives to the Net-Present-Value Rule," Financial Management, Vol. 24, NO. 3, Autumn 1995, pp. 96- 102.

25. TRIGEORGIS L. and S.P. MASON, "Valuing Managerial Flexibility," Midland Corporate Financial Journal, Vol. 5 , NO. 1, 1987, pp. 14-21.

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013

DR. HEMANTHA HERATH is an assistant professor of accounting at University of Northern British Columbia, British Columbia, Canada ([email protected]). Previously, he worked as a consultant in the Oil and Gas Division of the World Bank. He is a graduate of the University of Kelaniya (B.Sc.), the University of Jayawardenapura (M.B.A.), and .Auburn University (M.S.I.E. and Ph.D. Industrial and Systems Engineering). He is a Junior Fulbright Scholar and has been an ~ssociate Member of the Chartered Institute of Management Accountants (U.K.) since 1992. His research interests include real options, economic decision analysis, and managerial accounting.

DR. CHAN S. PARK is a professor of industrial and systems engineering at Auburn University, Alabama ([email protected]). He received his B.S. from Hanyang University, his M.S.I.E. from Purdue University and his Ph.D. in industrial engineering from Georgia Institute of Technology. His main research interests include engineeringtmanufacturing economics, decision analysis, and real options analysis. Dr. Park has published numerous articles on these topics and received several research awards for his publications from the Society of Manufacturing Engineers, the American Society of Engineering Education, the . Institute of Industrial Engineers, and the Sigma Xi. He has also authored several texts, including Advanced Engineering Economics (John Wiley) and Contemporary Engineering Economics (Addison Wesley Longman). Since 1997, he has been serving as Editor of the Engineering Economist.

Dow

nloa

ded

by [

Prin

ceto

n U

nive

rsity

] at

15:

20 0

5 O

ctob

er 2

013