mr. sanjay moolji - petrochem 2017 conclave. sanjay moolji global product manager ... india, sanjay...

TRANSCRIPT

Mr. Sanjay Moolji

Global Product Manager Tricon Energy Ltd.USA

Mr. Sanjay has more than 25 years of Sales and Marketingexperience in a spectrum of industries ranging fromPolymers, Industrial Chemicals, ConsumerDurables, Pharmaceuticals and Bulk Drugs.

Prior to his current assignment, he was the General Manager forExports of Reliance Industries Limited for Polymer Sector.

An Economics Graduate from the Calcutta University inIndia, Sanjay has also done Post graduation in Internationaltrade. He is widely traveled and has participated in variousinternational forums.

STRICTLY CONFIDENTIAL

Sanjay Moolji Tricon Energy Ltd.

Global Polymer Business – Trends & Market Dynamics

IOCL Conclave - 2013

STRICTLY CONFIDENTIAL

ContentsContents

World Polymer Business

Polymers – Trade balance & Global Markets

Challenges & Uncertainties

About Tricon Energy

STRICTLY CONFIDENTIAL

Polymer Business – Global Overview

STRICTLY CONFIDENTIAL

Global Polymer MarketGlobal Polymer Market

Polymer Market 205 MMT

• Polyethylene Market: 75.9 MMTHDPE

17%

PET

8%

PS

5%

ABS

4%

PVC

18%PC

2%

PP

26%

LDPE

9%

LLDPE

11%

• Polypropylene Market: 53.3 MMT

• PVC Market: 36.9 MMT

STRICTLY CONFIDENTIAL

PP Top 10 Producers

Source – CMAI/IHS

PE CapacityPE Capacity

NE

Asi

a

NE

Asi

a

NE

Asi

a

W E

uro

pe

W E

uro

pe

W E

uro

pe

N A

mer

ica

N A

mer

ica

N A

mer

ica

SE A

sia

SE A

sia

SE A

sia

M E

ast

M E

ast

M E

ast

S A

mer

ica

S A

mer

ica

S A

mer

ica

I Su

bco

n

I Su

bco

n

I Su

bco

n

C E

uro

pe

C E

uro

pe

C E

uro

pe

CIS

& B

S

CIS

& B

S

CIS

& B

S

Afr

ica

Afr

ica

Afr

ica

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2007 2012 2017

78 MMT 94 MMT 117 MMT

NE Asia --> 25% of global PE capacities by 2017

STRICTLY CONFIDENTIAL

PP Top 10 Producers

Source – CMAI/IHS

PP CapacityPP Capacity

NE

Asi

a

NE

Asi

a

NE

Asi

a

W E

uro

pe

W E

uro

pe

W E

uro

pe

N A

mer

ica

N A

mer

ica

N A

mer

ica

SE A

sia

SE A

sia

SE A

sia

M E

ast

M E

ast

M E

ast

S A

mer

ica

S A

mer

ica

S A

mer

ica

I Su

bco

n

I Su

bco

n

I Su

bco

n

C E

uro

pe

C E

uro

pe

C E

uro

pe

CIS

& B

S

CIS

& B

S

CIS

& B

S

Afr

ica

Afr

ica

Afr

ica

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2007 2012 2017

49 MMT 65 MMT 80 MMT

NE Asia --> 41% of global PP capacities by 2017

STRICTLY CONFIDENTIAL

PP Top 10 Producers

Source – CMAI/IHS

PVC Capacity

NE

Asi

a

NE

Asi

a

NE

Asi

a

W E

uro

pe

W E

uro

pe

W E

uro

pe

N A

mer

ica

N A

mer

ica

N A

mer

ica

SE A

sia

SE A

sia

SE A

sia

M E

ast

M E

ast

M E

ast

S A

mer

ica

S A

mer

ica

S A

mer

ica

I Su

bco

n

I Su

bco

n

I Su

bco

n

C E

uro

pe

C E

uro

pe

C E

uro

pe

CIS

& B

S

CIS

& B

S

CIS

& B

S

Afr

ica

Afr

ica

Afr

ica

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2007 2012 2017

40 MMT 54 MMT 56 MMT

NE Asia --> 54% of global PVC capacities by 2017

STRICTLY CONFIDENTIAL

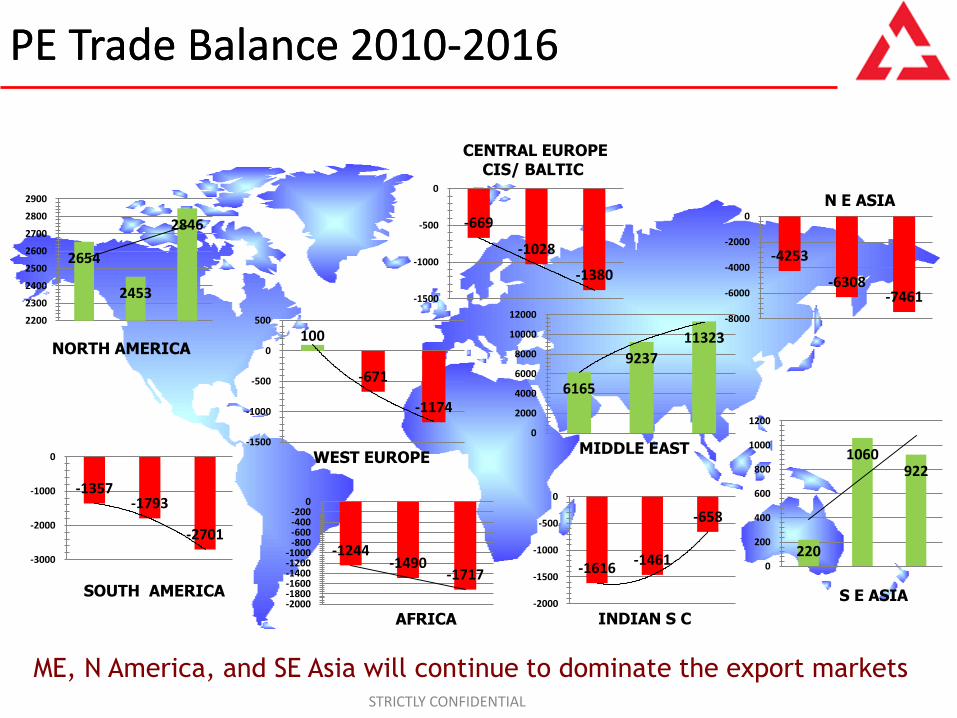

Polymer Trade Polymer Trade BalanceBalance

STRICTLY CONFIDENTIAL

2654

2453

2846

2200

2300

2400

2500

2600

2700

2800

2900

NORTH AMERICA

-1357-1793

-2701

-3000

-2000

-1000

0

SOUTH AMERICA

100

-671

-1174

-1500

-1000

-500

0

500

WEST EUROPE

-669

-1028

-1380

-1500

-1000

-500

0

CENTRAL EUROPECIS/ BALTIC

-1244-1490

-1717

-2000-1800-1600-1400-1200-1000

-800-600-400-200

0

AFRICA

-4253

-6308-7461

-8000

-6000

-4000

-2000

0

N E ASIA

220

1060922

0

200

400

600

800

1000

1200

S E ASIA

6165

9237

11323

0

2000

4000

6000

8000

10000

12000

MIDDLE EAST

-1616-1461

-658

-2000

-1500

-1000

-500

0

INDIAN S C

PE Trade Balance 2010PE Trade Balance 2010--20162016

ME, N America, and SE Asia will continue to dominate the export markets

STRICTLY CONFIDENTIAL

PE International Markets PE International Markets -- 20122012

ME the largest exporter for PE 35 %

N America739223%

S America11323%

W. Europe26638%

C Europe & CIS

13724%

Middle East

1139035%

India2101%

NEA367711%

SEA488615%

Source: CMAI/IHS

China, 8419, 25%

W Europe, 2911,

9%

N America, 4842

, 15%S America, 2724

, 8%

Turkey, 1055, 3%

Other Asia & SEA, 5217, 16

%

Africa, 2220, 7%

C Europe & CIS, 2524, 8%

ISC, 1534, 5%

Middle East, 1401, 4%

Exporting Regions Importing Regions

Market of 32.5 MMT

STRICTLY CONFIDENTIAL

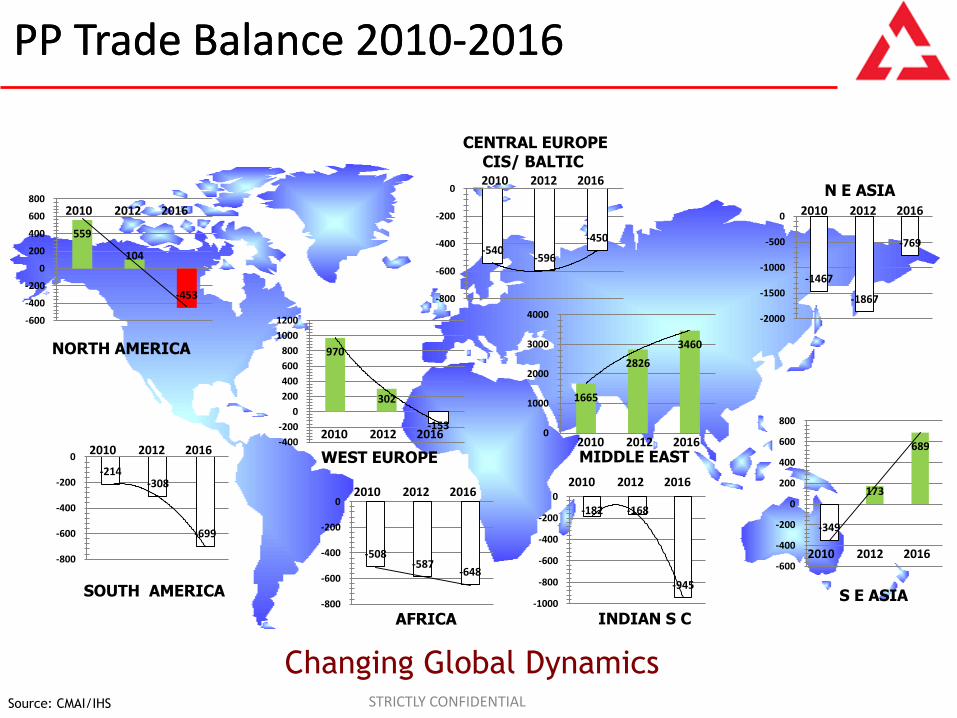

559

104

-453

-600

-400

-200

0

200

400

600

800

-214-308

-699

-800

-600

-400

-200

0

970

302

-153

-400

-200

0

200

400

600

800

1000

1200

-540-596

-450

-800

-600

-400

-200

0

NORTH AMERICA

SOUTH AMERICA

WEST EUROPE

CENTRAL EUROPECIS/ BALTIC

-508-587

-648

-800

-600

-400

-200

0

AFRICA

-1467

-1867

-769

-2000

-1500

-1000

-500

0

-349

173

689

-600

-400

-200

0

200

400

600

800

N E ASIA

S E ASIA

-182 -168

-945

-1000

-800

-600

-400

-200

0

1665

2826

3460

0

1000

2000

3000

4000

MIDDLE EAST

INDIAN S C

PP PP Trade Balance 2010Trade Balance 2010--20162016

Changing Global DynamicsSource: CMAI/IHS

2010 2012 2016

2010 2012 2016

2010 2012 2016

2010 2012 2016

2010 2012 2016

2010 2012 20162010 2012 2016

2010 2012 2016

2010 2012 2016

STRICTLY CONFIDENTIAL

PP International Markets PP International Markets -- 20122012

ME the largest exporter for PP 31 %

Americas203513%

W. Europe180012%

C Europe & CIS8756%

Africa3202%

Middle East, 5005,

31%

India8005%

NEA280018%

SEA210013%

Source: CMAI/IHS

China, 4500, 29%

W Europe, 1500,

10%

Americas, 2260, 14%

Turkey, 1480, 9%

Other Asia & SEA, 2140, 14

%

Africa, 910, 6%

C Europe & CIS, 1350, 9%

ISC, 870, 5%

Middle East, 620, 4%

Market of 15.7 MMT

Exporting Regions Importing Regions

STRICTLY CONFIDENTIAL

PVC :Trade PVC :Trade Balance Balance 20112011--20162016

USA most competitive production

China fastest growing export region; but not regular

South America

-784-930

-1,072-1,500

-1,000

-500

0

2011 2014 2016

North America2,615 2,900

3,254

0

1,000

2,000

3,000

4,000

2011 2014 2016

Europe680

400300

0

200

400

600

800

2011 2014 2016

CIS

-600-500 -420

-1,000

-500

0

2011 2014 2016

Middle East

-1,500

-1,400-1,300

-1,200

-1,100

2011 2014 2016

Africa

-588

-610

-640-650

-600

-550

2011 2014 2016

ISC

-933

-1,500

-2,100-3,000

-2,000

-1,000

0

2011 2014 2016

NE Asia

722

1,300

2,000

0

500

1,000

1,500

2,000

2,500

2011 2014 2016

SE Asia

144

150 150

140

145

150

155

2011 2014 2016

STRICTLY CONFIDENTIAL

PVC International Markets PVC International Markets -- 20122012

N. America is the largest exporter for PVC 44 %

Africa491%

C Europe & CIS4996%

Middle East1502%

N America354244%

NE Asia, 2000,

31%

S America3134%

SE Asia5216%

W Europe99512%

Source: CMAI/IHS

Africa, 561, 7% Brazil, 450, 6%

C Europe & CIS, 554, 7%

China, 1000, 12%

India, 1000, 12%

ISC, 160, 2%

Middle East, 597, 7%

N America, 850,

11%

NE Asia, 112, 1%

Russia, 550, 7%

S America, 659,

8%

SE Asia, 356, 5%

Turkey, 821, 10%

W Europe, 399, 5

%

Exporting Regions Importing Regions

Market of 7.7 MMT

STRICTLY CONFIDENTIAL

Trade Flow Trade Flow –– PastPast

Western World Feeding the Global Markets… N. America

W. Europe

STRICTLY CONFIDENTIAL

Trade Flow Trade Flow –– CurrentCurrent

N. America

W. Europe

Middle EastMiddle East the supplier to the world…Polyolefins

North America the ME of PVCKorea

STRICTLY CONFIDENTIAL

Logistics & Supply Logistics & Supply ChainChain

Polymer

Manufacturer

Demand

Transportation

Purc

hase

Purch

ase

Sch

edulin

g

Polymer

Processor

30 – 90 days

STRICTLY CONFIDENTIAL

Polymer Markets: EvolutionPolymer Markets: Evolution

Production has shifted from High consumption Areas to Low Cost Feedstock Areas

Consumption Growth has shifted from Developed Areas to Low Labor Cost Areas

Trade flow patterns have changed

Size of Plants have changed to Mega projects huge production volumes

Logistics & supply chain have become more complex

A New World Order……….

STRICTLY CONFIDENTIAL

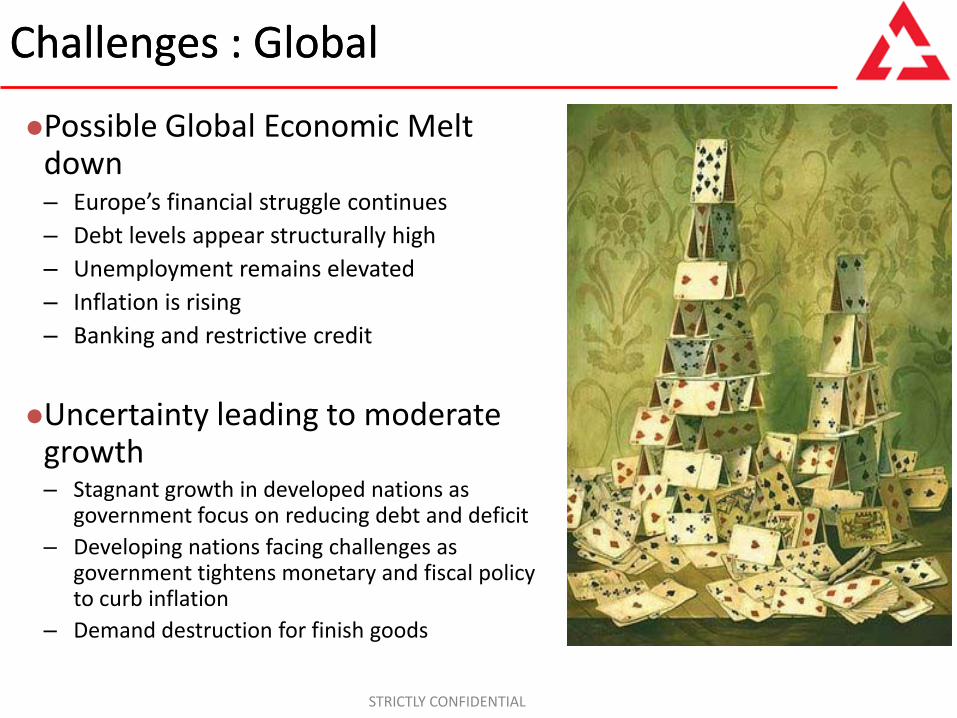

Challenges & Challenges & UncertaintiesUncertainties

STRICTLY CONFIDENTIAL

Global Economic EnvironmentGlobal Economic Environment

Recession in developed economies collateral damage across globe

STRICTLY CONFIDENTIAL

Managing Payment Managing Payment RisksRisks

Can your business afford the loss if it is not paid?

Will extending credit and the possibility of waiting several months for payment still make the sale profitable?

Can the sale be made only by extending credit? - How long have the buyers been operating, and what is their credit history?

Are there reasonable alternatives for collecting if the buyer does not pay?

If shipment is made but not accepted, can alternative buyers be found?

STRICTLY CONFIDENTIAL

Movement of documents, Movement of documents, goods & goods & paymentspayments

Issuing / Opening BankAdvising /

Confirming Bank

Applicati

on

Beneficiary

Seller

ExporterContract

Goods

Letter of Credit (Sight/Time)

Documents

Applicant / BuyerImporter

Many risks to be contained

• Bankruptcy or insolvency by the buyer

• Protracted default

• Problems with payment arrangements

• Problems with the merchandise

• Contract disputes

• Additional costs for financing, insurance, and shipping

STRICTLY CONFIDENTIAL

CACM

FTAA

PR China

Canada

USA

Mexico

Chile

UruguayParaguay

BrazilArgentina

Mercosur

Bolivia

Colombia

Venezuela

Peru

Ecuador

Costa

Rica

Nicaragua

El Salvador

HondurasGuatemala

Trinidad & Tobago

Antigua & Barbuda

Barbados

Belize

DominicaGrenada

GuyanaJamaica

Suriname

St. Lucia

St. Vincent & Grenadines

St. Kitts & Nevis

CARICOM

Panama

Dominican

Republic

AndeanCommunity

Bahamas

Haiti

Brunei

Cambodia

Indonesia

Laos

Malaysia

Myanmar

Philippines

Singapore

Thailand

Vietnam

Japan

New Zealand

Australia

ASEAN

South Korea

Hong Kong

Taiwan

Russia

Papua New Guinea

APECIntra-LAC

in forceIntra-Asia-

Pacific in forceIntra-LAC

Under NegotiationTrans-Pacific

Under NegotiationNegotiations under

strong consideration

APEC

Trade Agreements …..a barrierTrade Agreements …..a barrier

Where Does the world Sell……?

Nafta

Source: WTO

STRICTLY CONFIDENTIAL

Pricing…..a game of witsPricing…..a game of wits

Market has fewer buyers & sellers.

Transactions are more “Transparent”

Better “margin retention” capability long term

Hundreds of seller, thousands of transactions.

Salesman need to “ask the right questions” – but

they still may not get the right answers.

Prices are not always transparent.

Polymer margins can go negative in a soft market.

Polymer market is a challenging environment!!Source: CMAI

STRICTLY CONFIDENTIAL

Petrochemical Industry DynamicsPetrochemical Industry Dynamics

Crude Price and operating rates fundamental for Price

Price

Demand

Supply New InvestmentsTurnaroundsDisruptions

World EconomyGeopolitical SituationDemand SupplyWeatherFuture markets

US DemandChina DemandGDP

Elasticity

Crude

OperatingRate

Sentiments

Source: RIL APLA 2006

STRICTLY CONFIDENTIAL

Possible Global Economic Melt down– Europe’s financial struggle continues

– Debt levels appear structurally high

– Unemployment remains elevated

– Inflation is rising

– Banking and restrictive credit

Uncertainty leading to moderate growth– Stagnant growth in developed nations as

government focus on reducing debt and deficit

– Developing nations facing challenges as government tightens monetary and fiscal policy to curb inflation

– Demand destruction for finish goods

Challenges : GlobalChallenges : Global

STRICTLY CONFIDENTIAL

Market Needs Market Needs ––Producer & CustomerProducer & Customer

STRICTLY CONFIDENTIAL

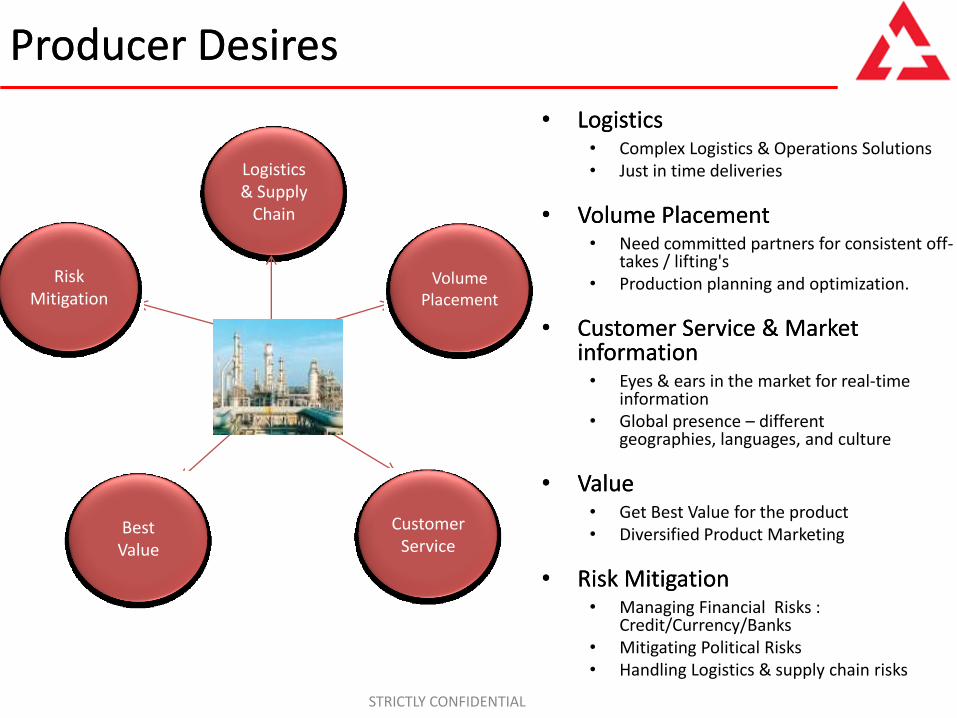

Producer DesiresProducer Desires

Logistics & Supply

Chain

•• LogisticsLogistics• Complex Logistics & Operations Solutions• Just in time deliveries

•• Volume PlacementVolume Placement• Need committed partners for consistent off-

takes / lifting's• Production planning and optimization.

•• Customer Service & Market Customer Service & Market informationinformation• Eyes & ears in the market for real-time

information• Global presence – different

geographies, languages, and culture

•• ValueValue• Get Best Value for the product• Diversified Product Marketing

•• Risk MitigationRisk Mitigation• Managing Financial Risks :

Credit/Currency/Banks• Mitigating Political Risks• Handling Logistics & supply chain risks

Customer Service

Best Value

Risk Mitigation

Volume Placement

STRICTLY CONFIDENTIAL

Customer Demands Customer Demands

VolumesPayment

Logistics

Pricing

•• PricingPricing• Competitive market pricing in line with

volumes and local markets

•• Customer ServiceCustomer Service• Real-time information – Order

placement and tracking• Redress technical issues

•• VolumesVolumes• Consistent volume avails • Consistent quality• Supply options – competitive prices

from other sources

•• PaymentPayment• Payment options to work within the

financial constraints• Flexibility in terms

•• LogisticsLogistics• Reliability• Timely shipments & Deliveries• Innovative logistics solutions

Customer Service

STRICTLY CONFIDENTIAL

Tricon EnergyTricon Energy

STRICTLY CONFIDENTIAL

HistoryHistoryFounded in 1996

Global Physical Trader in Bulk Chemicals and Plastics. – Focus on marketing and distribution of chemicals and plastics

World Leaders in Caustic Soda, Styrene, Xylenes & Pygas trade

Headquarters in Houston, Texas in USA

Global presence with footsteps in every markets.

High reputation for:– Customer service– Creativity– Reliability and Integrity– Quality of staff– Financial strength– Ability to make rapid decisions

STRICTLY CONFIDENTIAL

Organization Organization -- Global coverageGlobal coverage

Footprints in all major consumption regions…

STRICTLY CONFIDENTIAL

Value addition…….Value addition…….

+ +MarketingOperations &

Logistics

Financing &

Banking

Customer service, Operations

& Logistics…

…is the heart of the value chain

CUSTOMER

Operations & Finance

…to customer

Adding a world of value

Technical

Services

STRICTLY CONFIDENTIAL

Plastics 2012Plastics 2012

“We have build global relationships with more than“We have build global relationships with more than

600 customers and 50 producers 600 customers and 50 producers

based on trust, transparency and performance.”based on trust, transparency and performance.”

STRICTLY CONFIDENTIAL

Plastics 2012Plastics 2012

STRICTLY CONFIDENTIAL

“ It is not the strongest of the species that survive, nor the

most intelligent that survives. It is the one most adaptable

to change….”

Charles Darwin

Concluding Remarks……..Concluding Remarks……..

STRICTLY CONFIDENTIAL

Conquering Far Horizons

Thank you