monthly state of the market report november 2012

TRANSCRIPT

Monthly State of the Market Report

November 2012

Published December 17, 2012

SPP Market Monitoring Unit

Table of Contents

Executive Summary .....................................................................................................................................2

Figure 1 – SPP EIS Price Contour Map ...........................................................................................3

Figure 2 – Congestion by Shadow Price Impact – November 2012 ................................................4

Figure 3 – Congestion by Shadow Price Impact – Previous 12 months ..........................................5

Figure 4 – Congestion by Interval ...................................................................................................6

Figure 5 – LIP / Gas Cost Comparison ............................................................................................7

Figure 6 – Average Hourly Price by Market Participant – November 2012 ...................................7

Figure 7 – Average Hourly Price by Market Participant – Previous 12 months .............................9

Figure 8 – Regional Monthly Prices ..............................................................................................10

Figure 9 – Energy Generation by Fuel Type .................................................................................11

Figure 10 – Wind Generation & Capacity .....................................................................................13

Figure 11 – Fuel on the Margin .....................................................................................................14

Figure 12 – EIS Settlements - GWh ..............................................................................................15

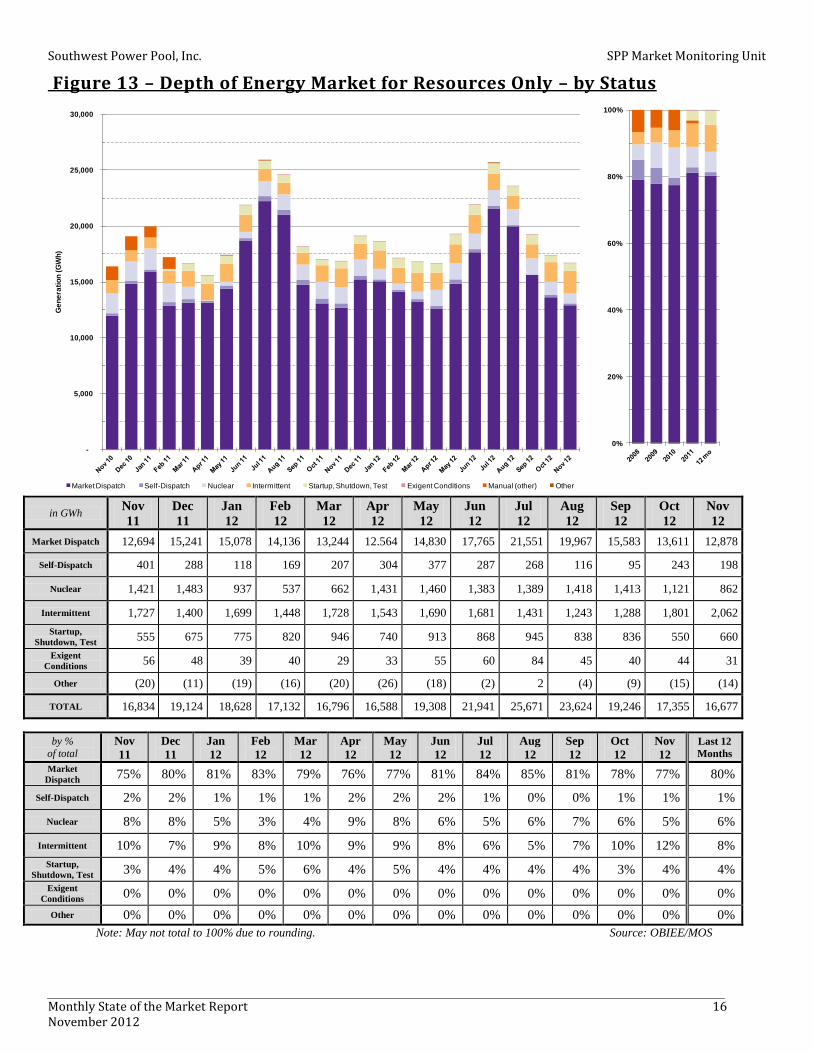

Figure 13 – Depth of Energy Market for Resources Only – by Status ..........................................16

Figure 14 –Market Ramp Rate Deficiency and Availability .........................................................17

Figure 15 – Dispatchable Range ....................................................................................................18

Figure 16 – Transmission Owner Revenue ....................................................................................19

Figure 17 – Average Transmission Reservations and Schedules ..................................................20

Figure 18 – RNU Components ......................................................................................................21

DISCLAIMER

The data and analysis in this report are provided for informational purposes only and shall not be considered or relied upon as market

advice or market settlement data. The Southwest Power Pool Market Monitoring Unit (SPP MMU) makes no representation or warranties

of any kind, express or implied, with respect to the accuracy or adequacy of the information contained herein.

The SPP MMU shall have no liability to recipients of this information or third parties for the consequences arising from errors or

discrepancies in this information, or for any claim, loss or damage of any kind or nature whatsoever arising out of or in connection with (i)

the deficiency or inadequacy of this information for any purpose, whether or not known or disclosed to the authors, (ii) any error or

discrepancy in this information, (iii) the use of this information, or (iv) a loss of business or other consequential loss or damage whether or

not resulting from any of the foregoing.

Copyright © 2012 by Southwest Power Pool, Inc. All rights reserved.

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 2 November 2012

Executive Summary

Congestion across the SPP Energy Imbalance Service (EIS) footprint abated

somewhat in November with only 6.5% of intervals having at least one breached

flowgate, compared to 11.5% of intervals in October (Figure 4). Congestion for the

year continues to exceed that experienced in prior years. The primary contributors to

localized congestion in the SPP EIS market during November included:

• High levels of wind generation and fluctuation of wind generation

• External impacts

• Planned transmission and generation outages, which typically take place during

“shoulder” months outside of the peak seasons.

Areas that saw much of the localized congestion in November (Figures 1 & 2)

included:

• Kansas City – Omaha corridor

• Texas Panhandle

• Southeast Kansas.

Wind generation in the SPP EIS Market continues to increase. Penetration into the

total generation mix is at an all-time high with 1,901 GWh of wind generation

during November. This represents 11.4% of all generation during November, which

is up from 9.6% in October (Figure 10).

The SPP EIS market continues to operate efficiently and effectively, with just over

1% of total generation self-scheduled for November, while 77% of generation was

available for market dispatch and 12% produced by intermittent resources (Figure

13).

Average LIP for the SPP EIS market for November was $23.68/MWh, a 3% decrease

from October. Gas cost at the Panhandle Eastern hub increased by 7% during this

same period (Figure 5). Even with the increase in gas cost, the large amount of low-

cost wind output in the generation mix helped to decrease the LIP from October to

November.

Good availability of ramp resulted in only three intervals having a ramp deficiency

during November (Figure 14). Although dispatchable range decreased from October

to November, this is a typical seasonal pattern. However, the dispatchable range for

November 2012 is significantly higher than the same month in prior years (Figure

15).

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 3 November 2012

Figure 1 – SPP EIS Price Contour Map

November 2012

12 Month EIS Price Contour Map

500 kV

345 kV

230 kV

161 kV

138 kV

115 kV

69 kV

Oklahoma City

Tulsa

500 kV

345 kV

230 kV

161 kV

138 kV

115 kV

69 kV

Oklahoma City

Tulsa

Texas Panhandle

Kansas City –

Omaha

Corridor

SE Kansas

NE Texas

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 4 November 2012

Figure 2 – Congestion by Shadow Price Impact – November 2012

Region Flowgate Name Flowgate Location (kV)

[Balancing Authority]

Average

Hourly

Shadow

Price

($/MWh)

Total %

Intervals

(Breached

or

Binding)

Detailed Description

Kansas City –

Omaha PENMUNSTRCRA

Pentagon – Mund (115) [WR] ftlo Stranger Creek – Craig

(345) [WR-KCPL] $ 43.76 28.8%

Congested due to high external impacts, along

with planned outages in the area.

Texas

Panhandle

OSGCANBUSDEA

Osage Switch - Canyon East (115) ftlo Bushland - Deaf

Smith (230) [SPS] $ 22.93 23.2%

Congestion due to fluctuating wind generation

along with limited generation in the area to

respond to congestion. SPSNORTH_STH

5 element PTDF flowgate

north to south through west Texas

$ 6.40 28.9%

SE Kansas

NEORIVNEODEL

Neosho - Riverton (161) ftlo

Neosho - Delaware (345) [WR-EDE-CSWS]

$ 14.74 8.8%

Planned transmission outage in the area

contributed to congestion. NEORIVNEOMOR

Neosho - Riverton (161) ftlo

Neosho - Morgan (345) [WR-EDE]

$ 6.85 2.4%

NEORIVASBLIT

Neosho - Riverton (161) ftlo

Asbury - Litchfield (161)

[WR-EDE] $ 3.75 3.0%

NE Texas VALIANTLYDIA Valiant-Lydia (345) [CSWS] $ 9.69 11.0% Planned transmission outage in the area

contributed to congestion.

Western

Kansas

MEDXFRSPEMUL

Medicine Lodge Xfmr

(138/155) ftlo Spearville -

Mullergren (230) [SECI] $ 5.98 1.3%

Congestion due to fluctuating wind generation

along with limited generation in the area to

respond to congestion. In addition, planned

transmission and generation outages in the area

contributed to congestion.

TEMP03_18670

Flat Ridge - Harper (138) ftlo Spearville - Mullergren (230)

[SECI] $ 3.99 1.1%

TEMP28_18528

Hayes - Vine (115) ftlo

Postrock - Knoll (230) [SECI-MIDW]

$ 3.75 1.6%

0%

10%

20%

30%

40%

50%

$0

$10

$20

$30

$40

$50

%T

ota

l In

terv

als

Co

ng

este

d

Avera

ge H

ou

rly S

had

ow

Pri

ce

($/M

Wh

)

Average Hourly Shadow Price ($/MWh) % Total Intervals Congested

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 5 November 2012

Figure 3 – Congestion by Shadow Price Impact – Previous 12 months

Region Flowgate Name Flowgate Location (kV)

Average

Hourly

Shadow

Price

($/MWh)

Total %

Intervals

(Breached or

Binding)

Projects Expected to Provide Some

Positive Mitigation

(Estimated In Service Date –

Upgrade Type)

Texas

Panhandle

OSGCANBUSDEA

Osage Switch - Canyon East (115)

ftlo Bushland - Deaf Smith (230)

[SPS] $ 10.81 15.0%

1. Tuco Int. – Woodward 345 kV line (May 2014 -

Balanced Portfolio)

2. Castro County Int. – Newhart 115 kV line (April 2015 - Regional Reliability)

3. Tuco Int. – Amoco – Hobbs 345 lines (January

2020 – ITP10)

SPSNORTH_STH 5 element PTDF flowgate north to

south through west Texas $ 2.94 16.8%

1. Tuco Int. – Woodward 345 kV line (May 2014 -

Balanced Portfolio)

GRAXFRSWEELK

Grapevine Xfmr (230/115) [SPS]

ftlo Sweetwater – Elk City (230)

[CSWS] $ 2.70 1.2%

1.Bowers – Howard 115 kV line (June 2016 – ITPNT)

2. Altus Jct Tap – Russell 138 kV

Kansas

City –

Omaha

Corridor

PENMUNSTRCRA

Pentagon – Mund (115) [WR] ftlo

Stranger Creek – Craig (345) [WR-KCPL]

$ 6.76 5.5%

1. 1. Tap existing Swissvale – Stilwell 345 kV line at

West Gardner (Dec 2012 - Balanced Portfolio) 2. 2. Terminal upgrade for Pentagon – Mund 115 kV line

(TBD – ITPNT)

3. Iatan – Nashua 345 kV line (June 2015 - Balanced Portfolio)

CIRKNGIATSTJ Circleville - King Hill [WR] (115)

ftlo Iatan - St. Joe (345) [KCPL] $ 4.24 1.0%

1. Iatan – Nashua 345 kV line (June 2015 - Balanced

Portfolio)

LAKALASTJHAW

Lake Road – Alabama [GMOC] (161) ftlo St. Joe – Hawthorn

[GMOC] (345) $ 2.64 1.0%

1. Axtell – Post Rock – Spearville 345 kV line, two Spearville – Comanche – Flat Ridge –Woodward

345 kV lines, and two Flat Ridge – Wichita 345 kV

lines (Dec 2014 - Balanced Portfolio/Priority Projects)

2. Iatan – Nashua 345 kV line (June 2015 - Balanced

Portfolio)

3. Nebraska City – Maryville – Sibley 345 kV line

(June 2017 - Priority Projects)

4. Eastowne Transformer (345/161) and decommission of Lake Road – Alabama 161 kV

line (Jan 2013 – not NTC but is sponsored)

IASCLKNASJHA*

Iatan – Stranger Creek (345)

[KCPL/WR] ftlo Lake Road –

Alabama (161) [KCPL/GMOC]; St. Joe – Hawthorn (345)

[GMOC/KCPL]

$ 2.47 10.8%

1. Axtell – Post Rock – Spearville 345 kV line, two

Spearville – Comanche – Flat Ridge –Woodward 345 kV lines, and two Flat Ridge – Wichita 345 kV

lines (Dec 2014 - Balanced Portfolio/Priority

Projects) 2. Iatan – Nashua 345 kV line (June 2015 - Balanced

Portfolio)

3. Nebraska City – Maryville – Sibley 345 kV line (June 2017 - Priority Projects)

SUBTEKFTCRAU*

Sub 1226 - Tekamah (161) ftlo

Fort Calhoun - Raun (345)

[OPPD/MEC] $ 2.46 0.5%

1. Nebraska City – Maryville – Sibley 345 kV line

(June 2017 - Priority Projects)

Western

Kansas MINXFRMINSET

Mingo Xfmr (345/115) ftlo

Mingo - Setab (345) [SECI] $ 3.16 4.6%

1. Axtell-Post Rock-Spearville 345 kV (June 2013 –

Balanced Portfolio 2. Hitchland – Woodward 345 kV (July 2014 – High

Priority)

South

Central

Kansas

MEDXFRREDMIN

Medicine Lodge Xfmr (138/115) ftlo Red Willow – Mingo (345)

[SECI – NPPD] $ 2.40 2.3%

1. Axtell – Post Rock – Spearville 345 kV lines (June

2013 - Balanced Portfolio)

* Reciprocal Coordinated Flowgate (MISO)

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 6 November 2012

Figure 4 – Congestion by Interval

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

last 12

months

Uncongested

Intervals % 36.3% 17.3% 14.0% 4.1% 12.1% 12.3% 35.7% 18.7% 12.7% 3.2% 11.7% 7.3% 13.6% 13.6%

Intervals

with

Binding

Only %

60.6% 78.8% 81.8% 92.5% 82.7% 79.1% 58.0% 75.6% 78.9% 91.9% 81.9% 81.2% 80.0% 80.1%

Intervals

with a

Breach %

3.2% 3.8% 4.2% 3.4% 5.2% 8.6% 6.3% 5.6% 8.4% 4.9% 6.4% 11.5% 6.5% 6.3%

Source: MOS

0%

20%

40%

60%

80%

100%

Uncongested Intervals Intervals with Binding Only Intervals with a Breach

0%

20%

40%

60%

80%

100%

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 7 November 2012

Figure 5 – LIP / Gas Cost Comparison

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

12 month

average

Electricity

(LIP)

[$/MWh] 24.43 23.32 20.90 21.16 18.80 18.42 22.25 21.33 27.33 25.00 22.19 24.34 23.68 22.41

Gas

Panhandle

[$/MMBtu] 3.17 3.15 2.66 2.54 2.02 1.85 2.29 2.33 2.80 2.72 2.70 3.19 3.42 2.63

$0

$10

$20

$30

$40

$50

$0

$2

$4

$6

$8

$10

Ele

ctr

icit

y P

rice (

LIP

) $/M

Wh

Gas C

ost

$/M

MB

tu

Gas (Panhandle) Electricity (LIP)

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 8 November 2012

Figure 6 – Average Hourly Price by Market Participant – November 2012

in $ AECC AEPM BEPM EDEP GMOC GRDX GSEC INDN KBPU KCPS KPP LESM MEAN MIDW OGE OMPA OPPM SECI SPSM TEAC TEAN WFES WRGS

Max 181 185 152 178 170 182 58 171 171 171 171 163 159 139 189 190 165 120 58 177 160 197 171

Avg 26 26 20 27 24 25 24 25 28 25 22 21 20 21 23 23 21 20 24 26 21 23 21

Min -37 -24 -157 -49 -51 -53 -21 -51 -51 -51 -56 -195 -179 -66 -58 -59 -187 -72 -20 -48 -175 -65 -55

Volatility 43% 48% 71% 55% 45% 44% 32% 47% 59% 50% 50% 74% 72% 55% 48% 48% 72% 63% 31% 44% 71% 53% 48%

Volatility is measured by the Coefficient of Variation, which is the standard deviation across all hours

divided by the average of all hours. Higher percentages mean more volatility in hourly prices.

AECC

AEPM

BEPM

EDEP

GMOC

GRDX

GSEC

INDN

KBPU

KCPS

KPP

LESM

MEAN

MIDW

OGE OMPA

OPPM

SECI

SPSM

TEAC

TEAN

WFES

WRGS

23.68

$18

$20

$22

$24

$26

$28

AECC AEPM BEPM EDEP GMOC GRDX GSEC INDN KBPU KCPS KPP LESM MEAN MIDW OGE OMPA OPPM SECI SPSM TEAC TEAN WFES WRGS

$18

$20

$22

$24

$26

$28

Pri

ce

s ($

/MW

h)

Market Participant

MP Average SPP Average

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 9 November 2012

Figure 7 – Average Hourly Price by Market Participant – Previous 12 months

in $ AECC AEPM BEPM EDEP GMOC GRDX GSEC INDN KBPU KCPS KPP LESM MEAN MIDW OGE OMPA OPPM SECI SPSM TEAC TEAN WFES WRGS

Max 470 231 225 254 229 233 239 231 235 232 228 225 225 246 234 242 359 218 243 396 225 238 226

Avg 23 22 20 23 22 22 24 23 23 23 22 21 20 23 22 23 21 22 24 23 21 22 22

Min -139 -138 -185 -140 -142 -138 -69 -142 -141 -141 -142 -225 -204 -148 -137 -138 -228 -179 -70 -140 -204 -140 -142

Volati l i ty 54% 38% 61% 46% 41% 37% 39% 42% 46% 43% 39% 58% 57% 61% 39% 39% 65% 71% 42% 51% 57% 39% 36%

AECC

AEPM

BEPM

EDEP

GMOC

GRDX

GSEC

INDN

KBPU

KCPS

KPP

LESM

MEAN

MIDW

OGE OMPA

OPPM

SECI

SPSM

TEAC

TEAN

WFES

WRGS

22.41

$18

$20

$22

$24

$26

AECC AEPM BEPM EDEP GMOC GRDX GSEC INDN KBPU KCPS KPP LESM MEAN MIDW OGE OMPA OPPM SECI SPSM TEAC TEAN WFES WRGS

$18

$20

$22

$24

$26

Pri

ces (

$/M

Wh

)

Market Participant

MP Average SPP Average

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 10 November 2012

Figure 8 – Regional Monthly Prices

Region Average

Price

Maximum

Price

Minimum

Price Volatility

Average On-Peak

Price

Average Off-Peak

Price

SPP $23.68 $152.81 $(42.04) 40% $24.99 $22.44

MISO $29.11 $157.97 $1.40 52% $34.01 $25.19

ERCOT $27.37 $229.30 $7.21 67% $30.63 $24.76

Note: This table is a “rough comparison” because of inherent differences in the structure of the three markets and also because of the differences in how prices for SPP, MISO, and ERCOT are calculated. For SPP, load weighted averages are used, while the data from MISO and ERCOT are not load weighted. Volatility is measured by the Coefficient of Variation, which is the standard deviation across all hours divided by the average of all hours.

$0

$10

$20

$30

$40

Nov 11 Dec 11 Jan 12 Feb 12 Mar 12 Apr 12 May 12 Jun 12 Jul 12 Aug 12 Sep 12 Oct 12 Nov 12

$/M

Wh

SPP MISO ERCOT

0%

100%

200%

Nov 11 Dec 11 Jan 12 Feb 12 Mar 12 Apr 12 May 12 Jun 12 Jul 12 Aug 12 Sep 12 Oct 12 Nov 12

Regional Price VolatilitySPP Volatility

MISO Volatility

ERCOT Volatility

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 11 November 2012

Figure 9 – Energy Generation by Fuel Type

in

GWh Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

Coal 10,756 12,872 12,238 11,190 9,867 8,678 10,479 12,365 14,303 13,677 11,726 11,344 11,041

Gas - SC 1,047 1,113 1,069 1,062 1,493 1,994 2,358 2,666 3,986 3,171 1,795 1,232 929

Gas - CC 1,986 2,281 2,723 2,946 3,100 2,949 3,396 3,965 4,681 4,098 3,136 1,939 1,907

Nuclear 1,421 1,483 937 537 662 1,431 1,460 1,383 1,389 1,408 1,413 1,121 862

Wind 1,505 1,236 1,552 1,252 1,498 1,325 1,484 1,480 1,226 1,037 1,111 1,664 1,901

Hydro 96 118 83 119 148 180 105 48 55 47 38 25 16

Other 23 21 25 26 28 31 26 34 31 32 28 28 21

Total 16,834 19,124 18,628 17,132 16,796 16,588 19,308 21,941 25,671 23,470 19,247 17,354 16,677

0

5,000

10,000

15,000

20,000

25,000

Gen

era

tio

n (

GW

h)

Coal Gas - SC Gas - CC Nuclear Wind Hydro Other

0%

20%

40%

60%

80%

100%

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 12 November 2012

0%

10%

20%

30%

40%

50%

60%

70%

80%

% o

f T

ota

l G

en

era

tio

n

Coal Gas - SC Gas - CC

0%

10%

20%

30%

40%

50%

60%

70%

80%

by % Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

12

month

average

Coal 63.9% 67.3% 65.7% 65.3% 58.7% 52.3% 54.3% 56.4% 55.7% 58.3% 60.9% 65.4% 66.2% 60.3%

Gas-SC 6.2% 5.8% 5.7% 6.2% 8.9% 12.0% 12.2% 12.2% 15.5% 13.4% 9.3% 7.1% 5.6% 9.8%

Gas-CC 11.8% 11.9% 14.6% 17.2% 18.5% 17.8% 17.6% 18.1% 18.2% 17.6% 16.3% 11.2% 11.4% 16.0%

Nuclear 8.4% 7.8% 5.0% 3.1% 3.9% 8.6% 7.6% 6.3% 5.4% 6.0% 7.3% 6.5% 5.2% 6.1%

Wind 8.9% 6.5% 8.3% 7.3% 8.9% 8.0% 7.7% 6.7% 4.8% 4.4% 5.8% 9.6% 11.4% 7.2%

Hydro 0.6% 0.6% 0.4% 0.7% 0.9% 1.1% 0.5% 0.2% 0.2% 0.2% 0.2% 0.1% 0.1% 0.4%

Other 0.1% 0.1% 0.1% 0.1% 0.2% 0.2% 0.1% 0.2% 0.1% 0.1% 0.1% 0.2% 0.1% 0.1%

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 13 November 2012

Figure 10 – Wind Generation & Capacity

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

Capacity

(MW) 4,887 4,887 4,887 4,907 4,907 5,122 5,122 6,190 6,190 7,337 7,337 7,474 7,474

Generation

(GWh) 1,505 1,236 1,552 1,252 1,498 1,325 1,484 1,480 1,226 1,037 1,105 1,664 1,901

Capacity

Factor 43% 34% 43% 37% 41% 36% 39% 33% 27% 19% 21% 30% 35%

# of

Resources 70 70 70 71 71 73 73 81 81 91 91 93 93

Source: OBIEE/MOS

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Win

d G

en

era

tio

n (

GW

h)

Win

d C

ap

acit

y (M

W)

Wind Capacity (MW) Wind Generation (GWh)

-

1,000

2,000

3,000

4,000

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Win

d G

en

era

tio

n (

GW

h)

Win

d C

ap

acit

y (M

W)

20%

30%

40%

50%Wind Capacity Factor

2008 2009 2010 2011 last 12

months

Average

Monthly

Capacity

(MW)

1,950 2,985 3,468 4,263 5,986

Capacity

Factor 35.5% 32.5% 34.9% 36.4% 31.9%

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 14 November 2012

Figure 11 – Fuel on the Margin

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

last 12

months

Gas 40.2% 38.8% 42.3% 44.7% 49.5% 65.7% 62.1% 61.0% 74.5% 67.8% 55.1% 44.1% 44.0% 54.2%

Coal 59.7% 61.2% 57.7% 55.3% 50.4% 34.1% 37.8% 38.9% 25.4% 32.1% 44.8% 55.7% 55.8% 45.8%

Other 0.1% 0.0% 0.0% 0.0% 0.0% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.2% 0.2% 0.1%

Source: MOS

Note:

During non-congested periods, one resource sets the price for the entire market. During

congested periods, the market is effectively segmented into several sub-areas, each with

its own marginal resource. Each congested interval counts the same as a non-congested

period, but the marginal fuel type for each sub-area is represented proportionally in the

congested period.

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al C

oal

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al C

oal

Co

al

Gas

Gas Gas

Gas

Gas

Gas G

as

Gas

Gas

Gas

Gas G

as

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas G

as

Gas

Gas

Gas

0%

20%

40%

60%

80%

100%

Co

al C

oal

Co

al Co

al

Co

al

Gas

Gas

Gas G

as

Gas

0%

20%

40%

60%

80%

100%

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 15 November 2012

Figure 12 – EIS Settlements - GWh

in GWh Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

Resource EI 3,038 3,381 3,765 3,395 4,095 3,549 3,487 3,904 4,190 4,204 3,571 3,495 3,479

Load EI 672 712 677 618 708 751 728 827 963 968 692 592 768

Scheduled

Transaction 29,551 33,621 32,421 29,887 28,503 28,434 34,253 39,302 47,019 42,194 33,715 30,044 29,023

Total Energy 33,261 37,713 36,864 33,900 33,306 32,734 38,467 44,033 52,172 47,365 37,979 34,131 33,270

by % Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

Last 12

Months

Resource EI 9.1% 9.0% 10.2% 10.0% 12.3% 10.8% 9.1% 8.9% 8.0% 8.9% 9.4% 10.2% 10.5% 9.6%

Load EI 2.0% 1.9% 1.8% 1.8% 2.1% 2.3% 1.9% 1.9% 1.8% 2.0% 1.8% 1.7% 2.3% 1.9%

Scheduled

Transactions 88.9% 89.1% 88.0% 88.2% 85.6% 86.9% 89.0% 89.2% 90.1% 89.1% 88.8% 88.0% 87.2% 88.4%

Totals may not equal 100% due to rounding.

5%

7%

9%

11%

13%

15%

17%

0

10,000

20,000

30,000

40,000

50,000

60,000

EIS

Tra

nsacti

on

s a

s %

of

To

tal

GW

h

Scheduled Transactions (GWh) Load EI GWh Resource EI GWh % EIS Transactions

5%

7%

9%

11%

13%

15%

17%

2008 2009 2010 2011 12 mo

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 16 November 2012

Figure 13 – Depth of Energy Market for Resources Only – by Status

in GWh Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

Market Dispatch 12,694 15,241 15,078 14,136 13,244 12.564 14,830 17,765 21,551 19,967 15,583 13,611 12,878

Self-Dispatch 401 288 118 169 207 304 377 287 268 116 95 243 198

Nuclear 1,421 1,483 937 537 662 1,431 1,460 1,383 1,389 1,418 1,413 1,121 862

Intermittent 1,727 1,400 1,699 1,448 1,728 1,543 1,690 1,681 1,431 1,243 1,288 1,801 2,062

Startup,

Shutdown, Test 555 675 775 820 946 740 913 868 945 838 836 550 660

Exigent

Conditions 56 48 39 40 29 33 55 60 84 45 40 44 31

Other (20) (11) (19) (16) (20) (26) (18) (2) 2 (4) (9) (15) (14)

TOTAL 16,834 19,124 18,628 17,132 16,796 16,588 19,308 21,941 25,671 23,624 19,246 17,355 16,677

by %

of total Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

Last 12

Months

Market

Dispatch 75% 80% 81% 83% 79% 76% 77% 81% 84% 85% 81% 78% 77% 80%

Self-Dispatch 2% 2% 1% 1% 1% 2% 2% 2% 1% 0% 0% 1% 1% 1%

Nuclear 8% 8% 5% 3% 4% 9% 8% 6% 5% 6% 7% 6% 5% 6%

Intermittent 10% 7% 9% 8% 10% 9% 9% 8% 6% 5% 7% 10% 12% 8%

Startup,

Shutdown, Test 3% 4% 4% 5% 6% 4% 5% 4% 4% 4% 4% 3% 4% 4%

Exigent

Conditions 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Other 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Note: May not total to 100% due to rounding. Source: OBIEE/MOS

-

5,000

10,000

15,000

20,000

25,000

30,000

Ge

ne

rati

on

(G

Wh

)

Market Dispatch Self-Dispatch Nuclear Intermittent Startup, Shutdown, Test Exigent Conditions Manual (other) Other

0%

20%

40%

60%

80%

100%

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 17 November 2012

Figure 14 –Market Ramp Rate Deficiency and Availability

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

12 month

average

UP Ramp

Deficiency

Intervals 6 0 1 0 0 1 1 1 0 1 3 0 1 1

DOWN Ramp

Deficiency

Intervals 7 7 2 0 4 2 16 19 1 0 4 5 2 5

Total Ramp

Deficiency

Intervals 13 7 3 0 4 3 17 20 1 1 7 5 3 6

% of Total

Market

Dispatch

Intervals

0.15% 0.08% 0.03% 0.00% 0.04% 0.03% 0.19% 0.23% 0.01% 0.01% 0.08% 0.06% 0.03% 0.07%

MW / Minute /

100 MW of

Online Capacity 0.87 0.89 0.93 0.96 1.00 1.04 1.09 1.06 1.19 1.10 1.02 0.96 0.94 1.02

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-

10

20

30

40

50

60

70

MW

/ M

inu

te o

f R

am

p /

100 M

W o

f O

nli

ne C

ap

acit

y

Ram

p D

efi

cie

ncy I

nte

rvals

UP Ramp Deficiency Intervals DOWN Ramp Deficiency Intervals MW / Minute / 100 MW of Online Capacity

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2008 2009 2010 2011 12 mo

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 18 November 2012

Figure 15 – Dispatchable Range

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12 last 12

mo

Average 37.7% 41.2% 42.1% 42.7% 43.6% 40.2% 38.0% 40.3% 38.4% 40.3% 41.6% 43.4% 41.5% 41.1%

Dispatchable Range is calculated as the average dispatachable range available (in MW)

divided by the average of the daily peak demand (MW) for the month.

32%

36%

40%

44%

Avg Dispatchable Range / Peak Demand

32%

36%

40%

44%

2008 2009 2010 2011 last 12 mo

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 19 November 2012

Figure 16 – Transmission Owner Revenue

in millions $ JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

2009 35.7 34.2 33.4 43.8 41.0 43.1 43.4 43.7 42.7 41.3 40.0 43.5

2010 44.7 43.9 46.6 54.3 52.0 52.3 53.8 65.1 55.8 52.9 52.5 53.8

2011 62.3 76.8 76.4 65.4 69.8 67.5 74.7 77.7 83.7 69.8 68.6 71.6

2012 72.5 81.2 80.5 81.6 87.1 89.2 88.3 91.7 91.1 84.6 83.5

$0

$20

$40

$60

$80

$100

Mil

lio

ns

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 20 November 2012

Figure 17 – Average Transmission Reservations and Schedules

in thousands

MWh Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

12 month

average

Average Daily

Reservations 506 479 476 468 389 483 499 505 532 467 453 500 515 481

Average Daily

Schedules 101 104 96 89 91 91 107 103 118 91 75 81 90 95

% 19.9% 21.8% 20.1% 18.9% 23.5% 18.9% 21.4% 20.4% 22.2% 19.5% 16.7% 16.3% 17.4% 19.8%

0%

10%

20%

30%

40%

50%

60%

0

100

200

300

400

500

600

Th

ou

san

ds M

Wh

Avg. Daily Transmission Reservations Schedules as a % of Reservations

0%

10%

20%

30%

40%

50%

60%

0

100

200

300

400

500

600

Southwest Power Pool, Inc. SPP Market Monitoring Unit

Monthly State of the Market Report 21 November 2012

Figure 18 – RNU Components

$ (thousands) Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

EIS 1,035 -521 -985 -546 -618 -414 351 -222 -521 -149 -578 1,271 -410

O/S -68 -38 -25 -33 -53 -103 -41 -27 -28 -41 -101 -117 -60

U/S -48 -86 -170 -169 -200 -730 -32 -99 -202 -327 -213 -169 -567

UDC -33 -31 -24 -20 -23 -24 -50 -54 -76 -67 -47 -43 -37

SP Loss -1 -1 1 4 0 1 5 3 11 3 0 -5 -3

Net RNU 886 -677 -1,203 -764 -896 -1,269 233 -399 -815 -580 -938 937 -1,077

Absolute

RNU 2,539 2,096 2,072 1,790 2,612 3,115 2,400 1,602 2,572 2,536 2,814 4,098 3,126

EIS (Energy Imbalance Charge/Credit) – All energy deviations between actual generation or load and schedules are settled as (EIS).

O/S (Over-Scheduling Charge) - During any hour, if Locational Imbalance Prices diverge and a Market Participant’s Load imbalance is more than 4% (but at least 2 MW) at an applicable Settlement Location in that hour, that MP may be subject to an Over-Scheduling Charge.

U/S (Under-Scheduling Charge) - During any hour, if Locational Imbalance Prices diverge and a Market Participant’s Load imbalance is more than 4% (but at least 2 MW) at an applicable Settlement Location in that hour, that MP may be subject to an Under-Scheduling Charge.

UDC (Uninstructed Resource Deviation) – the difference between the dispatch instructions and the actual performance of a Resource.

SP Loss - Self-Provided Losses

-$4

-$2

$0

$2

$4

$6

Mil

lio

ns

SP LOSS UDC U/S O/S EIS Net RNU Absolute RNU

-$20

$0

$20

$40

$60

$80

Millions

Net RNU Absolute RNU