monthly report 201512e-jpy

TRANSCRIPT

7/25/2019 Monthly Report 201512E-JPY

http://slidepdf.com/reader/full/monthly-report-201512e-jpy 1/2

Investment Objective and Strategy

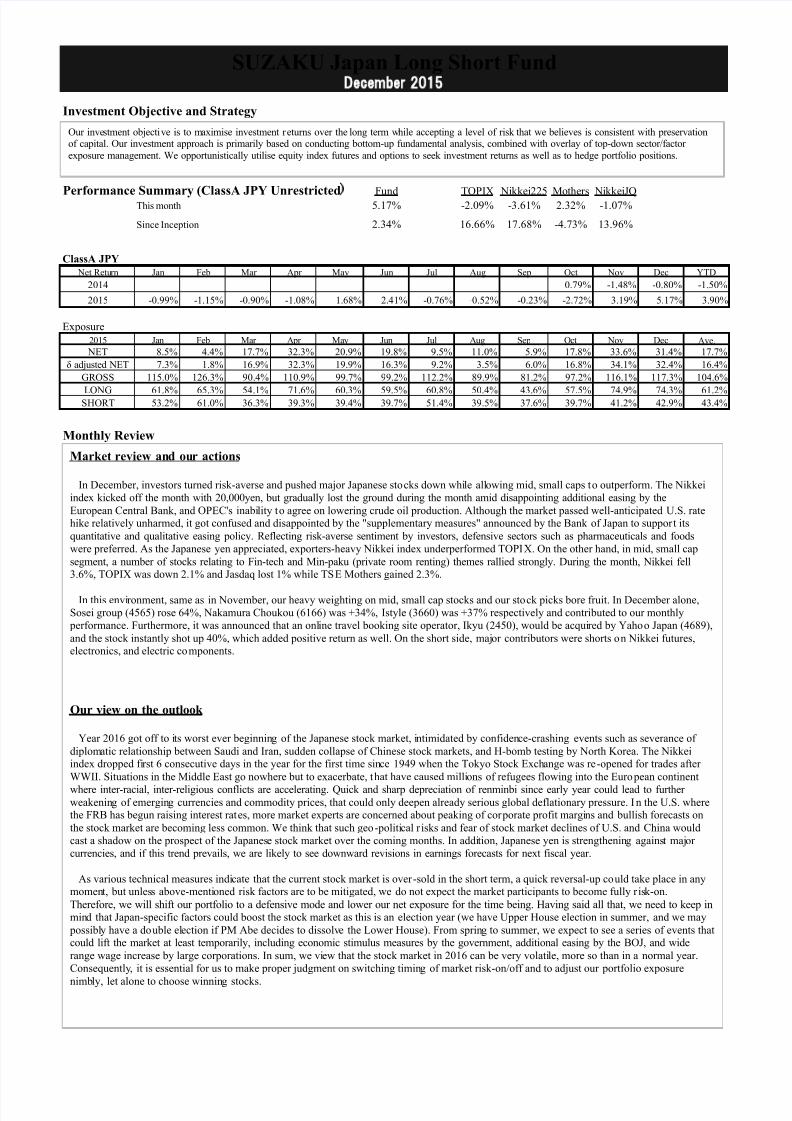

Performance Summary (ClassA JPY Unrestricted

Fund TOPIX Nikkei225 Mothers NikkeiJQ

5.17% -2.09% -3.61% 2.32% -1.07%

2.34% 16.66% 17.68% -4.73% 13.96%

ClassA JPY

Net Return Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec YTD

2014 0.79% -1.48% -0.80% -1.50%

2015 -0.99% -1.15% -0.90% -1.08% 1.68% 2.41% -0.76% -0.52% -0.23% -2.72% 3.19% 5.17% 3.90%

Exposure

2015 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Ave.

NET 8.5% 4.4% 17.7% 32.3% 20.9% 19.8% 9.5% 11.0% 5.9% 17.8% 33.6% 31.4% 17.7%

δ adjusted NET 7.3% 1.8% 16.9% 32.3% 19.9% 16.3% 9.2% 3.5% 6.0% 16.8% 34.1% 32.4% 16.4%

GROSS 115.0% 126.3% 90.4% 110.9% 99.7% 99.2% 112.2% 89.9% 81.2% 97.2% 116.1% 117.3% 104.6%

LONG 61.8% 65.3% 54.1% 71.6% 60.3% 59.5% 60.8% 50.4% 43.6% 57.5% 74.9% 74.3% 61.2%SHORT 53.2% 61.0% 36.3% 39.3% 39.4% 39.7% 51.4% 39.5% 37.6% 39.7% 41.2% 42.9% 43.4%

Monthly Review

I

This month

Since Inception

SUZAKU Japan Long Short FundDecember 2 15

Market review and our actions

In December, investors turned risk-averse and pushed major Japanese stocks down while allowing mid, small caps to outperform. The Nikkei

index kicked off the month with 20,000yen, but gradually lost the ground during the month amid disappointing additional easing by the

European Central Bank, and OPEC's inability to agree on lowering crude oil production. Although the market passed well-anticipated U.S. ratehike relatively unharmed, it got confused and disappointed by the "supplementary measures" announced by the Bank of Japan to support its

quantitative and qualitative easing policy. Reflecting risk-averse sentiment by investors, defensive sectors such as pharmaceuticals and foods

were preferred. As the Japanese yen appreciated, exporters-heavy Nikkei index underperformed TOPIX. On the other hand, in mid, small cap

segment, a number of stocks relating to Fin-tech and Min-paku (private room renting) themes rallied strongly. During the month, Nikkei fell3.6%, TOPIX was down 2.1% and Jasdaq lost 1% while TSE Mothers gained 2.3%.

In this environment, same as in November, our heavy weighting on mid, small cap stocks and our stock picks bore fruit. In December alone,

Sosei group (4565) rose 64%, Nakamura Choukou (6166) was +34%, Istyle (3660) was +37% respectively and contributed to our monthly

performance. Furthermore, it was announced that an online travel booking site operator, Ikyu (2450), would be acquired by Yahoo Japan (4689),

and the stock instantly shot up 40%, which added positive return as well. On the short side, major contributors were shorts on Nikkei futures,electronics, and electric components.

Our view on the outlook

Year 2016 got off to its worst ever beginning of the Japanese stock market, intimidated by confidence-crashing events such as severance of

diplomatic relationship between Saudi and Iran, sudden collapse of Chinese stock markets, and H-bomb testing by North Korea. The Nikkeiindex dropped first 6 consecutive days in the year for the first time since 1949 when the Tokyo Stock Exchange was re-opened for trades after

WWII. Situations in the Middle East go nowhere but to exacerbate, that have caused millions of refugees flowing into the European continent

where inter-racial, inter-religious conflicts are accelerating. Quick and sharp depreciation of renminbi since early year could lead to furtherweakening of emerging currencies and commodity prices, that could only deepen already serious global deflationary pressure. I n the U.S. wherethe FRB has begun raising interest rates, more market experts are concerned about peaking of corporate profit margins and bullish forecasts on

the stock market are becoming less common. We think that such geo-political r isks and fear of stock market declines of U.S. and China would

cast a shadow on the prospect of the Japanese stock market over the coming months. In addition, Japanese yen is strengthening against major

currencies, and if this trend prevails, we are likely to see downward revisions in earnings forecasts for next fiscal year.

As various technical measures indicate that the current stock market is over-sold in the short term, a quick reversal-up could take place in anymoment, but unless above-mentioned risk factors are to be mitigated, we do not expect the market participants to become fully r isk-on.

Therefore, we will shift our portfolio to a defensive mode and lower our net exposure for the time being. Having said all that, we need to keep inmind that Japan-specific factors could boost the stock market as this is an election year (we have Upper House election in summer, and we may

possibly have a double election if PM Abe decides to dissolve the Lower House). From spring to summer, we expect to see a series of events thatcould lift the market at least temporarily, including economic stimulus measures by the government, additional easing by the BOJ, and wide

range wage increase by large corporations. In sum, we view that the stock market in 2016 can be very volatile, more so than in a normal year.

Consequently, it is essential for us to make proper judgment on switching timing of market risk-on/off and to adjust our portfolio exposure

nimbly, let alone to choose winning stocks.

Our investment objective is to maximise investment returns over the long term while accepting a level of risk that we believes is consistent with preservationof capital. Our investment approach is primarily based on conducting bottom-up fundamental analysis, combined with overlay of top-down sector/factor

exposure management. We opportunistically utilise equity index futures and options to seek investment returns as well as to hedge portfolio positions.

7/25/2019 Monthly Report 201512E-JPY

http://slidepdf.com/reader/full/monthly-report-201512e-jpy 2/2

SUZAKU Japan Long Short FundDecember 2 15

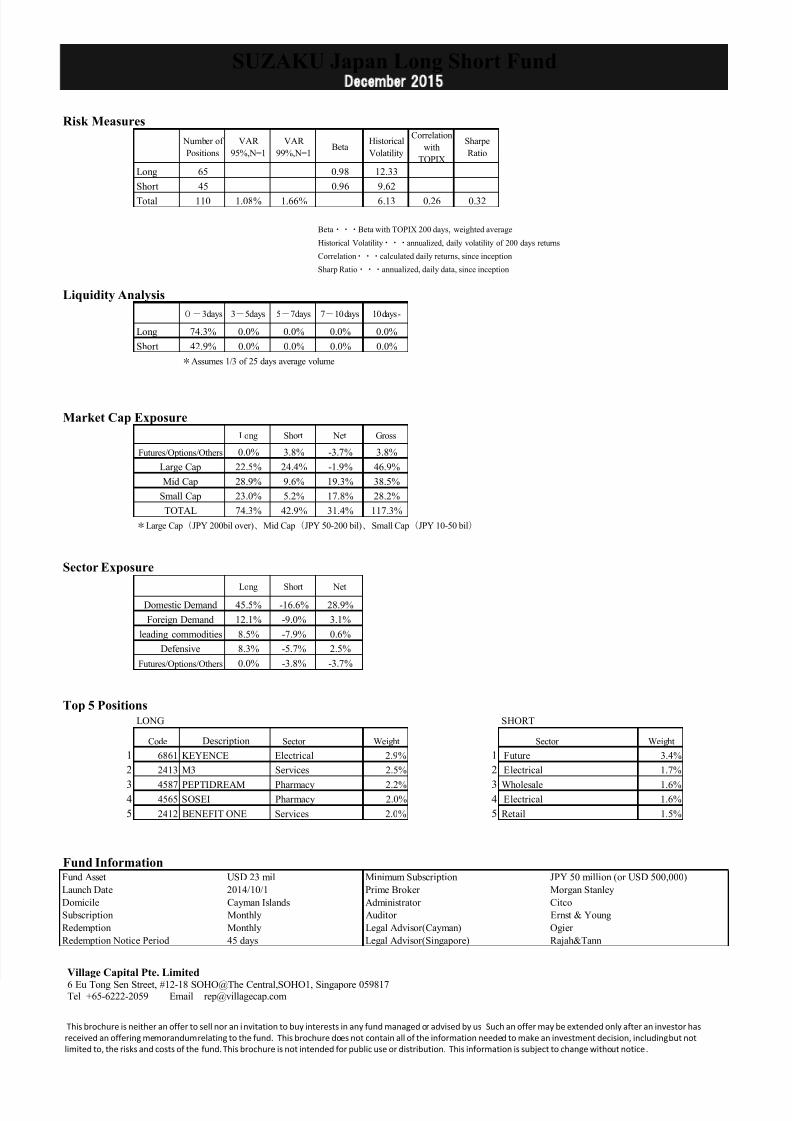

Risk Measures

Number of

Positions

VAR

95%,N=1

VAR

99%,N=1Beta

Historical

Volatility

Correlation

with

TOPIX

Sharpe

Ratio

Long 65 0.98 12.33

Short 45 0.96 9.62

Total 110 1.08% 1.66% 6.13 0.26 0.32

Beta・・・Beta with TOPIX 200 days, weighted average

Historical Volatility・・・annualized, daily volatility of 200 days returns

Correlation・・・calculated daily returns, since inception

Sharp Ratio・・・annualized, daily data, since inception

Liquidity Analysis

0-3days 3-5days 5-7days 7-10days 10days-

Long 74.3% 0.0% 0.0% 0.0% 0.0%

Short 42.9% 0.0% 0.0% 0.0% 0.0%

*Assumes 1/3 of 25 days average volume

Market Cap Exposure

Long Short Net Gross

0.0% 3.8% -3.7% 3.8%

22.5% 24.4% -1.9% 46.9%

28.9% 9.6% 19.3% 38.5%

23.0% 5.2% 17.8% 28.2%

74.3% 42.9% 31.4% 117.3%

*Large Cap(JPY 200bil over)、Mid Cap(JPY 50-200 bil)、Small Cap(JPY 10-50 bil)

Sector Exposure

Long Short Net

45.5% -16.6% 28.9%

12.1% -9.0% 3.1%

8.5% -7.9% 0.6%

8.3% -5.7% 2.5%

0.0% -3.8% -3.7%

Top 5 PositionsLONG SHORT

Code Sector Weight Weight

1 6861 KEYENCE Electrical 2.9% 1 Future 3.4%

2 2413 M3 Services 2.5% 2 Electrical 1.7%

3 4587 PEPTIDREAM Pharmacy 2.2% 3 Wholesale 1.6%4 4565 SOSEI Pharmacy 2.0% 4 Electrical 1.6%

5 2412 BENEFIT ONE Services 2.0% 5 Retail 1.5%

Fund InformationFund Asset USD 23 mil Minimum Subscription JPY 50 million (or USD 500,000)

Launch Date 2014/10/1 Prime Broker Morgan Stanley

Domicile Cayman Islands Administrator Citco

Subscription Monthly Auditor Ernst & Young

Redemption Monthly Legal Advisor(Cayman) Ogier

Redemption Notice Period 45 days Legal Advisor(Singapore) Rajah&Tann

Small Cap

Futures/Options/Others

Large Cap

Mid Cap

Futures/Options/Others

Description Sector

TOTAL

Domestic Demand

Foreign Demand

leading commodities

Defensive

Village Capital Pte. Limited

6 Eu Tong Sen Street, #12-18 SOHO@The Central,SOHO1, Singapore 059817Tel +65-6222-2059 Email [email protected]

This brochure is neither an offer to sell nor an invitation to buy interests in any fund managed or advised by us Such an offer may be extended only after an investor has

received an offering memorandum relating to the fund. This brochure does not contain all of the information needed to make an investment decision, including but not

limited to, the risks and costs of the fund. This brochure is not intended for public use or distribution. This information is subject to change without notice .