mongolia - iflr · mongolia our outlook for mongolia’s banking system is negative. this outlook...

TRANSCRIPT

BANKING SYSTEM OUTLOOK

BANKING APRIL 11, 2013

Table of Contents:

SUMMARY OPINION 1 MONGOLIAN BANKS RATED BY MOODY’S 3 KEY DRIVERS OF OUR OUTLOOK 4

Strengths 4 Weaknesses 4

OPERATING ENVIRONMENT 4 Economic Environment 4 Competitive Environment 6

ASSET QUALITY AND CAPITAL 7 Asset Quality 7 Capital 9

FUNDING AND LIQUIDITY 11 PROFITABILITY AND EFFICIENCY 12 SYSTEMIC SUPPORT 13 APPENDICES 14

Appendix 1: Sovereign Credit Opinion 14 Appendix 2: Overview of banking system outlooks 17 Appendix 3: Global Comparison Charts 18 Appendix 4: BFSR / BCA Mapping Table 21

Analyst Contacts:

HONG KONG +852.3551.3077

Hyun Hee Park +852.3758.1514 Analyst [email protected]

Stephen Long +852.3758.1306 Managing Director - Financial Institutions [email protected]

Mongolia Our outlook for Mongolia’s banking system is negative. This outlook expresses our expectations for the fundamental credit conditions in this system over the next 12-18 months.

Summary Opinion

Our outlook for Mongolia’s banking system is negative, reflecting the challenges banks face in managing what will likely be a period of rapid loan growth in an economy that is increasingly exposed to commodity-driven boom-bust cycles. Further underpinning our negative banking system outlook are structural features, such as high loan concentrations, weak risk-monitoring systems, and the developing nature of the regulatory framework.

Mining and government spending have become the two dominant sources of economic growth behind the current double-digit growth rates for gross domestic product (GDP) and loans. These concentrated growth drivers raise concerns over overheating and undermine the banks’ ability to diversify their loan portfolios. Although current inflation has declined from the high levels of 2012, it still poses a risk that could hurt confidence in the banking system.

Our analysis also considers the banks’ limited capital resources which provide only a weak buffer to absorb losses in a downside scenario. Under our central scenario, limited capital will put a strain on banks’ ability to maintain their current high loan growth.

The negative banking system outlook contrasts with the stable rating outlooks for the four rated Mongolian banks .These stable bank rating outlooks reflect the view that the current levels of B1 for all four rated banks already incorporate substantial downside risks. Nonetheless, we believe that, on balance, negative rating actions are more likely than positive actions over the next 12-18 months. The stable outlook on Mongolia’s B1 government bond rating also reflects the risks highlighted in this report, but balanced by improved government finances and foreign exchange reserves.

Operating environment. Our baseline scenario assumes GDP growth of around 12% in 2013,1 up from 10% in the first nine months of 2012, as Mongolia’s two main mines, Oyu Tolgoi and Tavan Tolgoi, enter production. Inflation declined to 11.3% year-on-year in February 2013, well below the peak of 34% seen in August 2008, though still above the official target of 8%. The central bank has eased its monetary policies and has indicated further loosening. We also expect expansionary fiscal policies. Under this central scenario, loan growth will likely rebound to 30%-40% in 2013, up from around 24% in 2012. Such high growth will test the banks’ ability to control risks, build capital and maintain liquidity.

1 Moody’s Asia-Pacific 2013 Sovereign Outlook: Resilient to Global Headwinds, 11 January 2013

BANKING

2 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Asset quality and capital. In our view, current low reported non-performing loan (NPL) ratios largely reflect recent double-digit loan growth which inflates this ratio’s denominator. We expect these ratios to rise as these new loans season, especially in the fast-growing mortgage and mining-related segments. Mongolian banks’ loan portfolios continue to exhibit high concentration risks, high inter-related lending, and under-provisioning, which all add to our asset quality concerns. While the banks exhibit headline capital ratios that compare well with other systems in Asia, we assess these levels to be weak relative to the high pace of asset growth and the asset quality challenges apparent. Our analysis indicates that most rated banks will need to raise capital in the coming 1-3 years.

Funding and liquidity. We expect that funding and liquidity conditions for the banks will remain tight despite some benefit from further monetary easing. The central bank, the Bank of Mongolia (BOM), has hinted at further cuts to both its policy rate and to the minimum reserve requirement for banks. Such cuts will help ease, but will not eliminate, liquidity tensions in this system which saw its overall loan-to-deposit ratio (LDR) rise to 89.5% at end-September 2012, from 65.7% at end-2010. The key driver of underlying liquidity pressures is the very high pace of loan growth.

Profitability and efficiency. We expect profitability to stabilize in 2013 after a modest decline in 2012, based on our assumption that the period will continue to see double-digit loan growth and a slight widening in margins. Margins will initially benefit from further rate cuts. We expect, however, that these top-line gains will be offset by rising operating costs in a high-inflation environment, and by rising credit costs as the banks’ loan books season.

Systemic support. We do not incorporate any systemic support in our ratings for Mongolian banks, because we do not consider Mongolia a high-support country. This view is consistent with the resolution of Zoos Bank and Anod Bank in 2009. In both cases, while the government protected depositors with blanket deposit guarantees, it also opted to liquidate the banks.

EXHIBIT 1

Overview

Key Credit Drivers Assessment (Negative/Positive/Stable)

Operating Environment Stable

Asset Quality and Capital Negative

Funding and Liquidity Negative

Profitability and Efficiency Stable

Systemic Support Stable

Banking System Outlook Negative

BANKING

3 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Banking System Outlook Definition Banking system outlooks represent our forward-looking assessment of fundamental credit conditions that will affect the creditworthiness of banks in a given system over the next 12-18 months. As such, banking system outlooks provide our view of how the operating environment for banks, including macroeconomic, competitive and regulatory trends, will affect asset quality, capital, funding, liquidity and profitability. Banking system outlooks also consider our forward-looking view of the systemic support environment for bank creditors.

Since banking system outlooks represent our forward-looking view on credit conditions that factor into our bank ratings, a negative (positive) outlook suggests that negative (positive) rating actions are more likely on average.

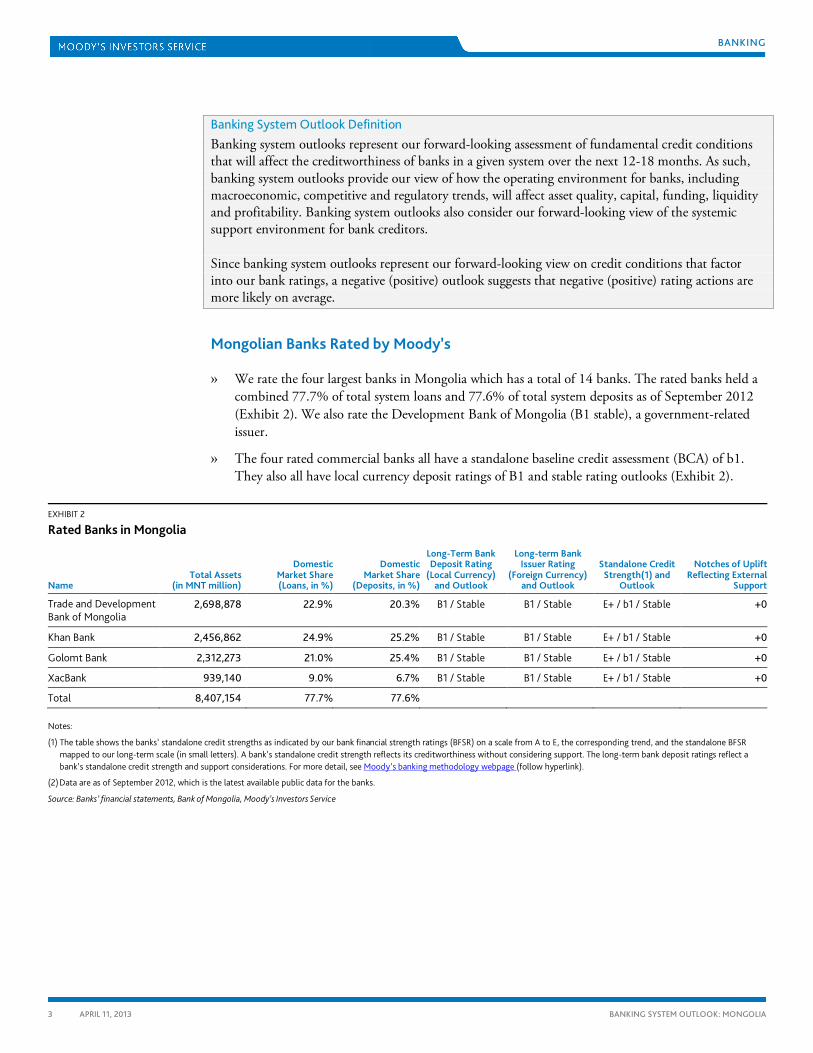

Mongolian Banks Rated by Moody’s

» We rate the four largest banks in Mongolia which has a total of 14 banks. The rated banks held a combined 77.7% of total system loans and 77.6% of total system deposits as of September 2012 (Exhibit 2). We also rate the Development Bank of Mongolia (B1 stable), a government-related issuer.

» The four rated commercial banks all have a standalone baseline credit assessment (BCA) of b1. They also all have local currency deposit ratings of B1 and stable rating outlooks (Exhibit 2).

EXHIBIT 2

Rated Banks in Mongolia

Name Total Assets

(in MNT million)

Domestic Market Share (Loans, in %)

Domestic Market Share

(Deposits, in %)

Long-Term Bank Deposit Rating

(Local Currency) and Outlook

Long-term Bank Issuer Rating

(Foreign Currency) and Outlook

Standalone Credit Strength(1) and

Outlook

Notches of Uplift Reflecting External

Support

Trade and Development Bank of Mongolia

2,698,878 22.9% 20.3% B1 / Stable B1 / Stable E+ / b1 / Stable +0

Khan Bank 2,456,862 24.9% 25.2% B1 / Stable B1 / Stable E+ / b1 / Stable +0

Golomt Bank 2,312,273 21.0% 25.4% B1 / Stable B1 / Stable E+ / b1 / Stable +0

XacBank 939,140 9.0% 6.7% B1 / Stable B1 / Stable E+ / b1 / Stable +0

Total 8,407,154 77.7% 77.6%

Notes:

(1) The table shows the banks’ standalone credit strengths as indicated by our bank financial strength ratings (BFSR) on a scale from A to E, the corresponding trend, and the standalone BFSR mapped to our long-term scale (in small letters). A bank’s standalone credit strength reflects its creditworthiness without considering support. The long-term bank deposit ratings reflect a bank’s standalone credit strength and support considerations. For more detail, see Moody’s banking methodology webpage (follow hyperlink).

(2) Data are as of September 2012, which is the latest available public data for the banks.

Source: Banks’ financial statements, Bank of Mongolia, Moody’s Investors Service

BANKING

4 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Key Drivers of Our Outlook

Strengths

» Fast-growing economy. Mongolia has enjoyed strong growth, largely owing to its investments in two large mines. As these mines start production in 2013, they will generate income that will fuel the next round of economic expansion. Accordingly, the banks have ample opportunities to grow their assets and earnings.

» Young demographics. An average age range of 20-24 years means that the economy can look forward to strong growth in its working-age population.

Weaknesses

» Still-developing supervision and regulations have contributed to banks being exposed to high borrower and industry concentration risk and weak governance.

» High cross-ownership linkages among banks, and between banks and industrial companies result in related-partly lending, both directly and indirectly, and increase the risks of spillovers.

» Weak legal framework. Lenders face challenges accessing collateral. Although a registry exists for lenders to record claims on property, pursuing claims through the courts can be protracted owing to debtor challenges and the weakness of the legal system.

» Capital and liquidity under pressure because of rapid loan growth. Credit growth as high as 73% in 2011 means that general asset-side challenges are apparent on the banks’ balance sheets2. Banking system assets – as a share of GDP – rose to an estimated 78% at end-2012, from 55.7% at end-2008, as a result of the 73% growth in credit in 2011.

» Unhedged borrowers expose system to foreign-exchange risks. Approximately 30% of the system’s loans and deposits are US dollar-denominated, exposing the banks to losses on foreign currency loans to unhedged borrowers, if Mongolia’s currency depreciated.

Operating Environment

Economy seen to maintain double-digit growth, but faces risks from overheating and volatile external demand for Mongolia’s mineral exports.

Economic Environment

» Our baseline scenario assumes GDP growth of around 12% in 2013.3 GDP grew 10% year-on-year in the first nine months of 2012, and 17% in 2011. Mineral exports, mostly coking coal and copper, accounted for 91% of Mongolia’s total exports in 2012.

» The following will be the main drivers of economic growth in 2013:

– The start of production at the Oyu Tolgoi mine and expansion of the Tavan Tolgoi mine. 4 According to the International Monetary Fund (IMF), export earnings from these mines

2 Consolidated Balance Sheet of Banks, Bank of Mongolia, December 2011 3 Moody’s: Asia-Pacific 2013 Sovereign Outlook: Resilient to Global Headwinds, published on 11 January 2013. 4 The Oyu Tolgoi copper mine in the Gobi Desert is the world’s largest underdeveloped copper-gold mine, while Tavan Tolgoi – which is in southern Mongolia and close

to China -- is one of the world’s largest untapped coal deposits.

BANKING

5 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

could total $2 billion in 2013, or one-fifth of the country’s 2012 nominal GDP projection5. While we expect copper prices in 2013 to trend below 2012, they will likely remain at a level that will support Mongolia’s economy.6

– Large infrastructure investments by the government and the Development Bank of Mongolia (DBM). The investments include transportation and utility projects, urban housing and industrialization. Expenditure by DBM is expected to total $1.6 billion in 2013.

– Monetary easing. The BOM shifted to an easing stance in 2013 for the first time since 2009 after determining that the outlook for inflation was “consistent with its target.” It cut its policy rate by a cumulative 175 basis points in January and April to the current level of 11.5%.

– Housing construction. The government is trying to promote home ownership. Its “100,000 Homes” project, unveiled in 2011, includes preferential mortgages rates and subsidies and a plan to build 100,000 homes which would – based on current production volumes – take 10 years.

» The following are downside risks:

– Overheating. The risk of overheating has receded as a result of the policy tightening evident in 2012, but remains a concern, given our growth assumptions. In particular, despite the implementation of the 2010 Fiscal Stability Law (FSL) in 2013, the government may continue its expansionary fiscal policy by running capital spending off-budget, through the DBM, or under build-transfer arrangements, thereby side-stepping the FSL’s limits on the country’s structural deficit or expenditure growth. The potential rapid increase in home construction could also distort supply and demand in the housing market.

– Inflation. The latest headline inflation of around 14% for 2012 compares with the BOM’s target of 8% for 2013. The BOM has shifted to an easing stance, due to its confidence that inflation will continue to trend down from its peak of 34% in August 2008, but the risk of a rebound is clearly present.

– External demand shock. With its two new mines, the economy is increasingly exposed to the commodity cycle in general, and to commodity demand from China in particular. Of its total exports in 2012, some 91% were mineral exports of mostly coking coal and copper, of which, 93% went to China.7 This lack of diversification exposes the economy to downturns in either China or the global environment.

– Pressure on short-term external position. We expect the pipeline of public infrastructure projects to add to the government’s borrowing needs. This contrasts with the mining sector investments in recent years that have largely been Foreign Direct Investment (FDI)-funded, and could subject the economy to additional short-term payment pressure. We note in particular that a substantial portion of the country’s coming mining income will be diverted to repay investment costs, and thus may not be available for covering the government’s new spending plans.

5 IMF: Staff Report for the 2012 Article IV Consultation and Third Post-Program Monitoring, published in November 2012. 6 See Moody’s Industry Outlook: Base Metals Industry Faces Challenging Road in 2013, published on 13 December 2012, where we state: “Copper remains the best-

positioned of the base metals over the medium-to long-term, based on its favorable supply and demand characteristics, the declining grades and recoveries, and absence of new greenfield developments in more politically stable countries.”

7 IMF: Mongolia Balance of Payment, 2012 Article IV Consultation and Third Post-Program Monitoring, published in November 2012.

BANKING

6 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Credit growth to rebound after recent slowdown. We anticipate loan growth of 30%-40% in 2013, versus 24% in 2012, supported by a rebound in headline growth and accommodative fiscal and monetary policies. The banks are likely to face the strongest growth in demand for credit from the construction and mining sectors.

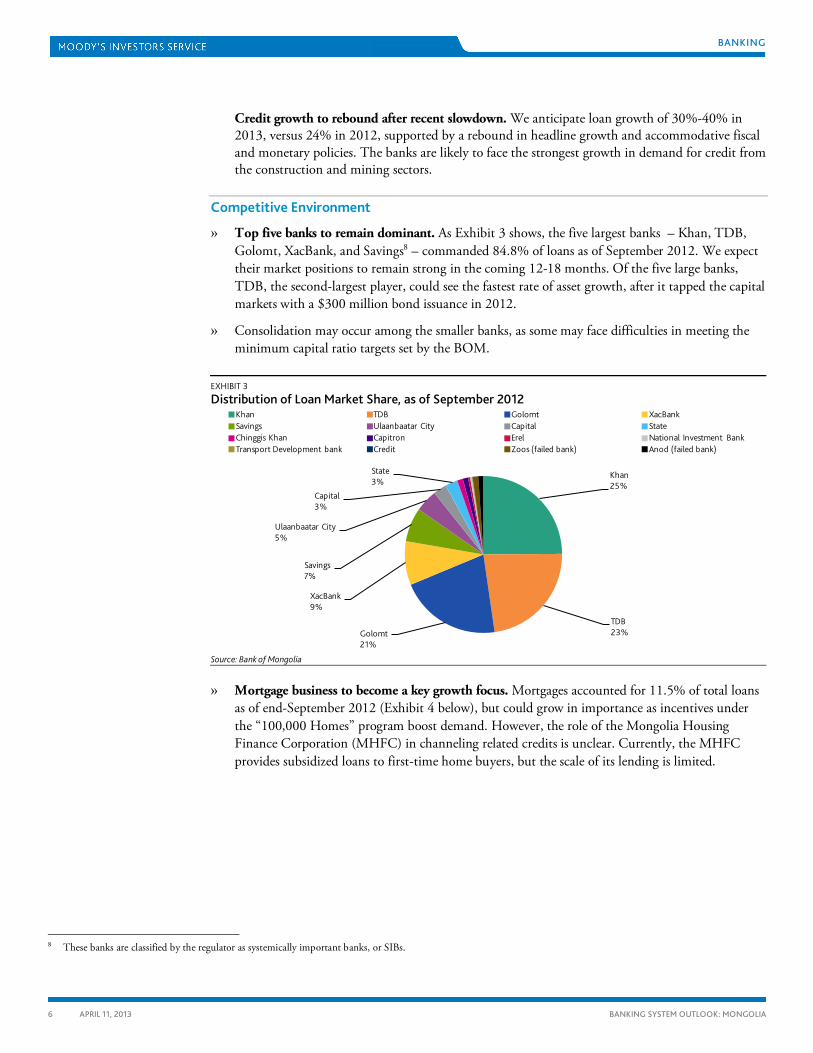

Competitive Environment

» Top five banks to remain dominant. As Exhibit 3 shows, the five largest banks – Khan, TDB, Golomt, XacBank, and Savings8 – commanded 84.8% of loans as of September 2012. We expect their market positions to remain strong in the coming 12-18 months. Of the five large banks, TDB, the second-largest player, could see the fastest rate of asset growth, after it tapped the capital markets with a $300 million bond issuance in 2012.

» Consolidation may occur among the smaller banks, as some may face difficulties in meeting the minimum capital ratio targets set by the BOM.

EXHIBIT 3 Distribution of Loan Market Share, as of September 2012

Source: Bank of Mongolia

» Mortgage business to become a key growth focus. Mortgages accounted for 11.5% of total loans as of end-September 2012 (Exhibit 4 below), but could grow in importance as incentives under the “100,000 Homes” program boost demand. However, the role of the Mongolia Housing Finance Corporation (MHFC) in channeling related credits is unclear. Currently, the MHFC provides subsidized loans to first-time home buyers, but the scale of its lending is limited.

8 These banks are classified by the regulator as systemically important banks, or SIBs.

Khan25%

TDB23%Golomt

21%

XacBank9%

Savings7%

Ulaanbaatar City5%

Capital3%

State3%

Khan TDB Golomt XacBankSavings Ulaanbaatar City Capital StateChinggis Khan Capitron Erel National Investment BankTransport Development bank Credit Zoos (failed bank) Anod (failed bank)

BANKING

7 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Asset Quality and Capital

Our negative assessment of asset quality and capital reflects the rising risks from cyclical and structural factors. These risks are important factors underpinning our negative banking system outlook.

Asset Quality

» Banks to see weaker asset quality following strong lending. We believe the strong spurt of unseasoned loans originating in 2011 and 2012 occurred in an underwriting environment that was more relaxed compared with that of 2008 and 2009, when banks were more cautious owing to the global crisis. As a result, the NPL ratio of 4.5% as of September 2012 likely understates the true extent of problem assets in the banks’ loan portfolios, and could increase in the coming 12-18 months. As our earlier assessment suggests, this cyclical risk is exacerbated by the boom/bust commodity-driven operating environment.

» Supervision, regulation and transparency issues also weigh on our asset quality assessment. Mongolian banks have not adopted a forward-looking approach in their provisioning rules – a practice common for other Asian banks – and may be under-provisioned. Transparency is also an issue, as the BOM does not publish data on loan-loss reserves. Consequently, NPL coverage levels are difficult to estimate.

» Concentration risks are increasing. The economy’s rising dependence on mining-related sectors also contributes to high and increasing concentration risks. (Mining-related exposures include ancillary industries and are much larger than the 12.4% of total loans classified as direct mining exposures in Exhibit 4 below.)

EXHIBIT 4 Loan Book Composition as of September 2012

Source: Bank of Mongolia Loan Report Note: Loans to Individuals include small business loans and personal loans.

» Specific areas of asset quality concerns include:

– Mining – Nominal NPLs in the mining sector have risen, despite a fall in the overall NPL ratio (Exhibits 5 and 6). The risks that could heighten credit stress in this sector are a fall in global commodity demand, especially from China, and a delay in the government’s infrastructural spending pipeline. The risk of volatile demand from China is highlighted by recent trade numbers which indicate a sharp 27% year-on-year fall in shipments in January-

Mining 12.4%

Wholesale and Retail Trade11.8%

Construction10.2%

Manufacturing9.7%

Transportation2.2%Agriculture

1.6%Real Estate1.2%

Financial and Insurance0.6%

Others5.9%

Loans to Individuals32.8%

Mortgage11.5%

BANKING

8 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

February 20139. A sustained decline would adversely affect the cash flows of companies and undermine their credit positions.

– Housing-related sectors such as construction, real estate and mortgage

» Construction companies. Despite the onset of a strong housing boom, the construction sector is under pressure from capacity constraints, with labor shortages and increasing input costs threatening to narrow the industry’s margins.10

» Mortgages. Rapid mortgage market growth increases credit risk pressure on households. Household indebtedness has risen in recent years. The household debt-to-income 11 ratio of 50%-70% is high in historical terms. This has been driven by an almost four-fold increase in total mortgages outstanding between 2009 and 2012 on the back, in turn, of strong property price appreciation. Increasing leverage exposes households to potential setbacks in the economy and property market. Nonetheless, the banks’ mortgage portfolios are buffered against the direct impact of falling house prices by their comparatively low loan-to-value ratios, which averaged 56.4% in 201212.

EXHIBIT 5 NPLs in Mining, Construction, Transportation and Real Estate

Source: Bank of Mongolia

EXHIBIT 6 NPL Ratio by Industries

Source: Bank of Mongolia

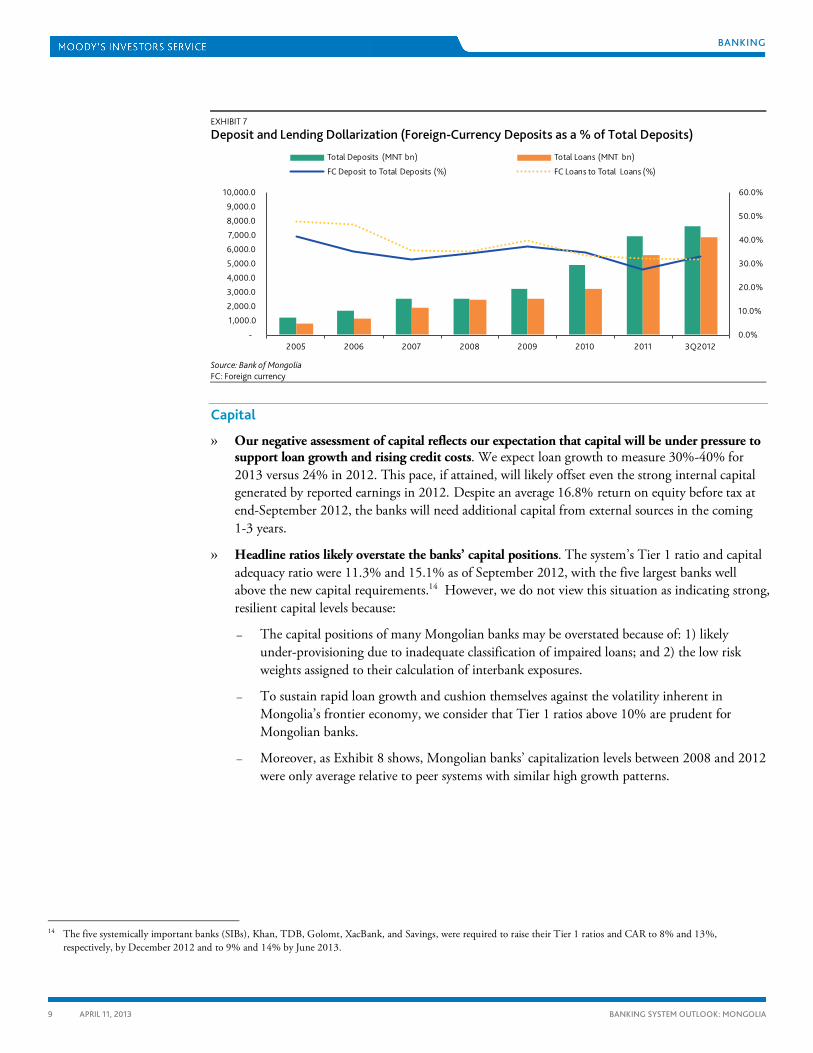

– Unhedged foreign-currency borrowers expose system to foreign exchange-induced credit risks. Approximately 30% of system deposits and loans are USD-denominated (Exhibit 7), which raises the risks that some foreign-currency borrowers, in particular retail borrowers, may suffer repayment pressure if the local currency depreciates.13

9 Imports of almost all major commodities fell significantly in Jan-Feb 2013. The value of unwrought copper and copper products fell by 27.2% from a year ago. The fall

of major commodity imports suggest that China’s economic recovery remains weak. 10 Mongolia Quarterly Economic Update, World Bank, published in October 2012. 11 Net-of-tax payment-to income ratio; Housing Finance Technical Note, World Bank, published in June 2012. 12 Data from the Mongolia Mortgage Corporation. 13 According to interviews with the four banks, they tend to extend loans in foreign currency to borrowers with foreign-currency earnings and/or foreign-currency working

capital requirements. However, in practice, the banks cannot check whether every obligor with foreign currency loans has cash flows in foreign currency, especially in the case of individual borrowers.

-

20

40

60

80

100

120

Mining Construction Transportation Real Estate

MN

T Bi

llion

s

2008 2009 2010 2011 3Q 2012

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2008 2009 2010 2011 3Q 2012

Mining Construction

Real Estate Transportation

Total NPL ratio

BANKING

9 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

EXHIBIT 7 Deposit and Lending Dollarization (Foreign-Currency Deposits as a % of Total Deposits)

Source: Bank of Mongolia FC: Foreign currency

Capital

» Our negative assessment of capital reflects our expectation that capital will be under pressure to support loan growth and rising credit costs. We expect loan growth to measure 30%-40% for 2013 versus 24% in 2012. This pace, if attained, will likely offset even the strong internal capital generated by reported earnings in 2012. Despite an average 16.8% return on equity before tax at end-September 2012, the banks will need additional capital from external sources in the coming 1-3 years.

» Headline ratios likely overstate the banks’ capital positions. The system’s Tier 1 ratio and capital adequacy ratio were 11.3% and 15.1% as of September 2012, with the five largest banks well above the new capital requirements.14 However, we do not view this situation as indicating strong, resilient capital levels because:

– The capital positions of many Mongolian banks may be overstated because of: 1) likely under-provisioning due to inadequate classification of impaired loans; and 2) the low risk weights assigned to their calculation of interbank exposures.

– To sustain rapid loan growth and cushion themselves against the volatility inherent in Mongolia’s frontier economy, we consider that Tier 1 ratios above 10% are prudent for Mongolian banks.

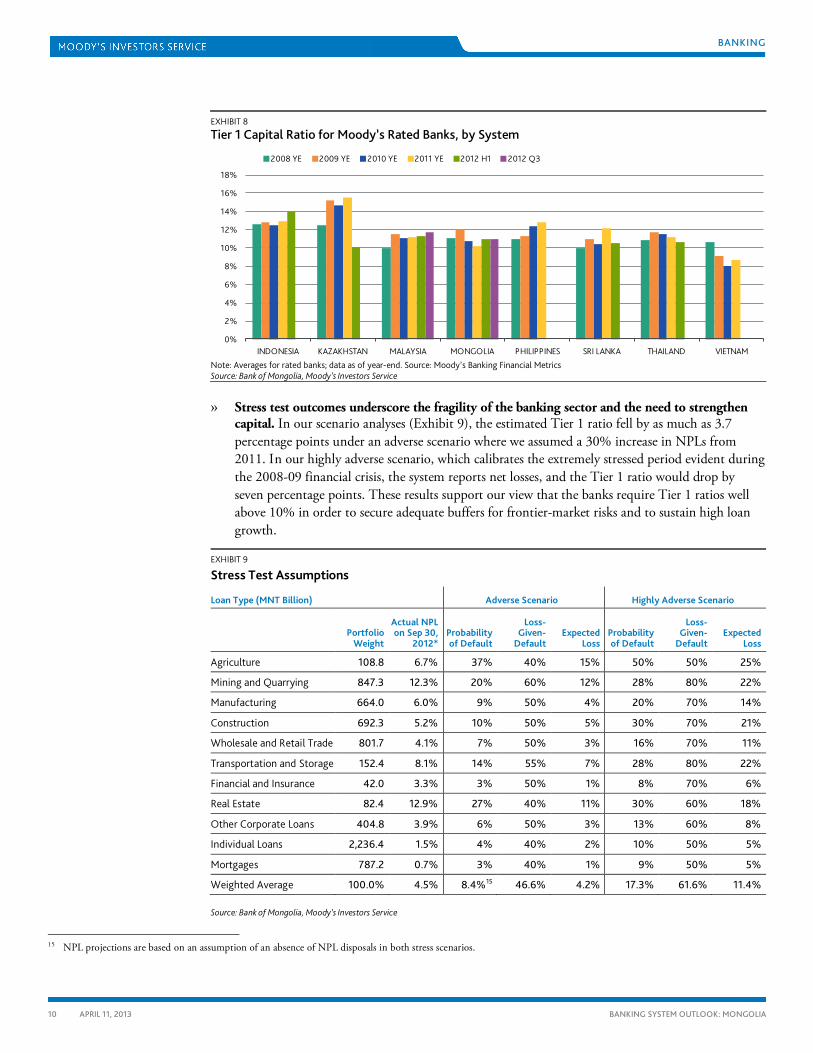

– Moreover, as Exhibit 8 shows, Mongolian banks’ capitalization levels between 2008 and 2012 were only average relative to peer systems with similar high growth patterns.

14 The five systemically important banks (SIBs), Khan, TDB, Golomt, XacBank, and Savings, were required to raise their Tier 1 ratios and CAR to 8% and 13%,

respectively, by December 2012 and to 9% and 14% by June 2013.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

-

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

7,000.0

8,000.0

9,000.0

10,000.0

2005 2006 2007 2008 2009 2010 2011 3Q2012

Total Deposits (MNT bn) Total Loans (MNT bn)

FC Deposit to Total Deposits (%) FC Loans to Total Loans (%)

BANKING

10 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

EXHIBIT 8 Tier 1 Capital Ratio for Moody’s Rated Banks, by System

Note: Averages for rated banks; data as of year-end. Source: Moody’s Banking Financial Metrics Source: Bank of Mongolia, Moody’s Investors Service

» Stress test outcomes underscore the fragility of the banking sector and the need to strengthen capital. In our scenario analyses (Exhibit 9), the estimated Tier 1 ratio fell by as much as 3.7 percentage points under an adverse scenario where we assumed a 30% increase in NPLs from 2011. In our highly adverse scenario, which calibrates the extremely stressed period evident during the 2008-09 financial crisis, the system reports net losses, and the Tier 1 ratio would drop by seven percentage points. These results support our view that the banks require Tier 1 ratios well above 10% in order to secure adequate buffers for frontier-market risks and to sustain high loan growth.

EXHIBIT 9

Stress Test Assumptions

Loan Type (MNT Billion) Adverse Scenario Highly Adverse Scenario

Portfolio

Weight

Actual NPL on Sep 30,

2012* Probability of Default

Loss-Given-

Default Expected

Loss Probability of Default

Loss-Given-

Default Expected

Loss

Agriculture 108.8 6.7% 37% 40% 15% 50% 50% 25%

Mining and Quarrying 847.3 12.3% 20% 60% 12% 28% 80% 22%

Manufacturing 664.0 6.0% 9% 50% 4% 20% 70% 14%

Construction 692.3 5.2% 10% 50% 5% 30% 70% 21%

Wholesale and Retail Trade 801.7 4.1% 7% 50% 3% 16% 70% 11%

Transportation and Storage 152.4 8.1% 14% 55% 7% 28% 80% 22%

Financial and Insurance 42.0 3.3% 3% 50% 1% 8% 70% 6%

Real Estate 82.4 12.9% 27% 40% 11% 30% 60% 18%

Other Corporate Loans 404.8 3.9% 6% 50% 3% 13% 60% 8%

Individual Loans 2,236.4 1.5% 4% 40% 2% 10% 50% 5%

Mortgages 787.2 0.7% 3% 40% 1% 9% 50% 5%

Weighted Average 100.0% 4.5% 8.4%15 46.6% 4.2% 17.3% 61.6% 11.4%

Source: Bank of Mongolia, Moody’s Investors Service

15 NPL projections are based on an assumption of an absence of NPL disposals in both stress scenarios.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

INDONESIA KAZAKHSTAN MALAYSIA MONGOLIA PHILIPPINES SRI LANKA THAILAND VIETNAM

2008 YE 2009 YE 2010 YE 2011 YE 2012 H1 2012 Q3

BANKING

11 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

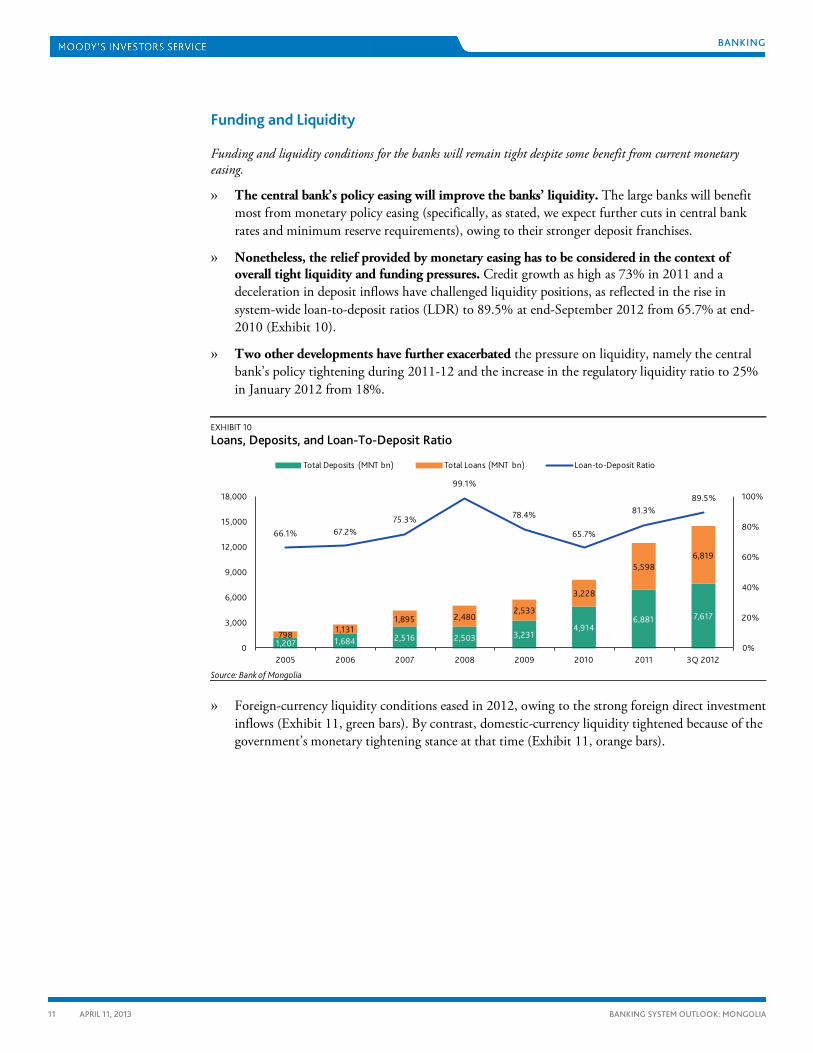

Funding and Liquidity

Funding and liquidity conditions for the banks will remain tight despite some benefit from current monetary easing.

» The central bank’s policy easing will improve the banks’ liquidity. The large banks will benefit most from monetary policy easing (specifically, as stated, we expect further cuts in central bank rates and minimum reserve requirements), owing to their stronger deposit franchises.

» Nonetheless, the relief provided by monetary easing has to be considered in the context of overall tight liquidity and funding pressures. Credit growth as high as 73% in 2011 and a deceleration in deposit inflows have challenged liquidity positions, as reflected in the rise in system-wide loan-to-deposit ratios (LDR) to 89.5% at end-September 2012 from 65.7% at end-2010 (Exhibit 10).

» Two other developments have further exacerbated the pressure on liquidity, namely the central bank’s policy tightening during 2011-12 and the increase in the regulatory liquidity ratio to 25% in January 2012 from 18%.

EXHIBIT 10 Loans, Deposits, and Loan-To-Deposit Ratio

Source: Bank of Mongolia

» Foreign-currency liquidity conditions eased in 2012, owing to the strong foreign direct investment inflows (Exhibit 11, green bars). By contrast, domestic-currency liquidity tightened because of the government’s monetary tightening stance at that time (Exhibit 11, orange bars).

1,207 1,684 2,516 2,503 3,2314,914

6,881 7,617

798 1,1311,895 2,480

2,533

3,228

5,5986,819

66.1% 67.2%75.3%

99.1%

78.4%

65.7%

81.3%89.5%

0%

20%

40%

60%

80%

100%

0

3,000

6,000

9,000

12,000

15,000

18,000

2005 2006 2007 2008 2009 2010 2011 3Q 2012

Total Deposits (MNT bn) Total Loans (MNT bn) Loan-to-Deposit Ratio

BANKING

12 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

EXHIBIT 11 Foreign -Currency Liquidity and Domestic-Currency Liquidity

Source: Bank of Mongolia

» Increased dependency on wholesale funding. The banks have managed their liquidity pressures by: (1) raising deposit rates to attract additional funds; and by (2) raising wholesale funding. The four banks we rate have paid higher deposit rates to obtain additional domestic currency liquidity, and raised funds through either syndicated loans, private subordinated bond offerings or public bond offerings in foreign currency.

» Mortgage funding mismatch is a concern. The banks are challenged in asset and liability management, as they grow their mortgage businesses. Fixed-rate long-term mortgages, with maturities of 5-15 years, are common even though banks started to introduce variable-rate long-term mortgages in 2011. But, according to the BOM, banks finance 98% of such lending from short-term deposits and bank capital. This potential funding mismatch is more pronounced now than in previous years, and is likely to continue, given the strong growth in mortgages. While some relief is provided by the Mongolia Mortgage Corporation, which purchases mortgage loans from originating banks, such support accounted for less than 1% of total mortgages in 2011. Mongolia’s undeveloped asset backed securities (ABS) market is unlikely to provide a source of stable long-term funding for mortgages.

Profitability and Efficiency

Profitability is likely to be stable on rapid loan growth, despite rising costs.

» Profitability to remain stable. We expect pre-provision income to be driven by double-digit loan growth and improving lending margins, the latter a result of the banks re-pricing liabilities downwards faster than loans in a falling interest rate environment.

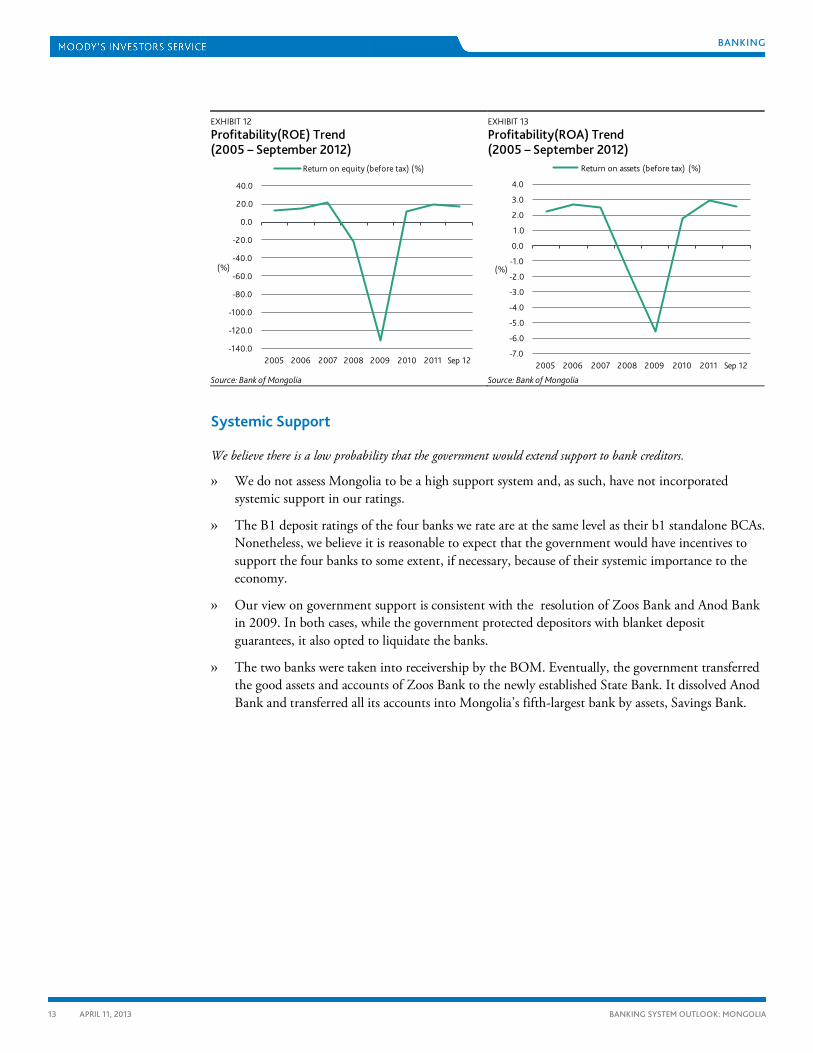

» This development, in turn, will be partly offset by rising operating costs from: 1) continued efforts by the banks to retain domestic currency deposits in order to maintain liquidity; 2) ongoing wage pressures as a result of inflation; and 3) ongoing capital spending for branch expansions and technology upgrades. The first two factors were the main reasons the banks reported a decline in returns in 2012, with a return on assets of 2.5% in 3Q 2012 versus 2.9% in 2011, and a return on equity of 16.8% in 3Q 2012 versus 18.6% in 2011. Going forward, we also expect rising credit costs, as newly booked loans season (Exhibit 12 and 13).

76%

88%84%

101%

84%

63%

96%87%

59% 56%

71%

98%

75%67%

76%

91%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2005 2006 2007 2008 2009 2010 2011 3Q2012

Foreign Currency Loan-to-Deposit ratio (%) Domestic Currency Loan-to-Deposit ratio (%)

BANKING

13 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

EXHIBIT 12 Profitability(ROE) Trend (2005 – September 2012)

Source: Bank of Mongolia

EXHIBIT 13 Profitability(ROA) Trend (2005 – September 2012)

Source: Bank of Mongolia

Systemic Support

We believe there is a low probability that the government would extend support to bank creditors.

» We do not assess Mongolia to be a high support system and, as such, have not incorporated systemic support in our ratings.

» The B1 deposit ratings of the four banks we rate are at the same level as their b1 standalone BCAs. Nonetheless, we believe it is reasonable to expect that the government would have incentives to support the four banks to some extent, if necessary, because of their systemic importance to the economy.

» Our view on government support is consistent with the resolution of Zoos Bank and Anod Bank in 2009. In both cases, while the government protected depositors with blanket deposit guarantees, it also opted to liquidate the banks.

» The two banks were taken into receivership by the BOM. Eventually, the government transferred the good assets and accounts of Zoos Bank to the newly established State Bank. It dissolved Anod Bank and transferred all its accounts into Mongolia’s fifth-largest bank by assets, Savings Bank.

-140.0

-120.0

-100.0

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

2005 2006 2007 2008 2009 2010 2011 Sep 12

(%)

Return on equity (before tax) (%)

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2005 2006 2007 2008 2009 2010 2011 Sep 12

(%)

Return on assets (before tax) (%)

BANKING

14 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Appendices

Appendix 1: Sovereign Credit Opinion

Credit Strengths Support factors for Mongolia include:

» Early progress in developing abundant mineral resources

» A fiscal stability law

» Access to concessional bilateral and multilateral external financing

Credit Challenges Concerns are focused in the following areas:

» Fiscal and BOP dependence on cyclical mining revenues

» A narrow economy vulnerable to commodity price shocks

» Livestock sector vulnerable to harsh weather cycles

» Low per-capita income and high social welfare demands

» Unpredictability of the investment regime

Rating Rationale Mongolia’s B1 government bond rating is consistent with our methodology scores of low economic and institutional strengths, moderate government financial strength and high event risk. Long-term economic prospects are potentially bright, but the near-term fiscal outlook is clouded by spending pressures.

Mongolia’s rating has been constrained by susceptibility to destabilizing boom-bust cycles stemming from (1) an undiversified, dual mining/agricultural economy subject to mineral price vulnerability on one front and occasional extremely severe winters on the other, and (2) pro-cyclical monetary and fiscal policies.

Mongolia pulled through the 2008-2009 boom-bust cycle with the assistance of an 18-month IMF Stand-by-Arrangement, successfully completed in the fall of 2010. Under the program, inflation was reined in and international reserves were rebuilt. The health of government finances over the long term will in large part depend on the implementation of the country’s fiscal stability law, key measures of which come into play in 2013-2014.

Predictability with foreign investment agreements would ensure benefits to Mongolia from the country’s substantial mineral endowments. After many years of delay, Mongolia’s parliament approved the government’s agreement with Ivanhoe Mines and Rio Tinto in October 2009 to develop the very rich Oyu Tolgoi copper and gold deposit; although the terms of the project have recently been under dispute. The exploitation of this and other large mineral deposits, such as high-grade coking coal in Tavan Tolgoi will be transformational for the Mongolian economy, but the management of the windfall will pose considerable challenges to the authorities.

BANKING

15 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Rating Outlook The change in the rating outlook to stable from negative in October 2009 was prompted by a shoring up of official foreign exchange reserve holdings, the containment of the burgeoning budget deficit and the elimination of nearly runaway inflation. Also, the enactment into law of a fiscal responsibility rule holds promise for avoiding future boom-bust cycles in government finances. However, spending and overheating pressures may set in ahead of the full implementation of the fiscal responsibility law in 2013-2014. Ongoing mining disputes are a threat to operations and foreign investment, and any significant escalation would be credit negative.

What Could Change the Rating - Up Credit positive events over the rating outlook horizon include the maintenance of price and exchange rate stability and a further replenishment of official foreign exchange reserves. A track record of adherence to the fiscal rule would be credit positive. Furthermore, steady mineral resource development under a stable and predictable investment regime would improve the country’s long-term fiscal and economic prospects.

What Could Change the Rating - Down A significant setback in the development of the mining sector. A relapse into economic instability. A collapse of the newly adopted fiscal policy framework as seen in an inability to maintain budgetary discipline against rising social welfare demands.

Recent Developments Preliminary estimates of full year 2012 economic growth show real GDP moderating to 12.3% year-on-year, from a high of 17.3% in 2011. These results are in line with projections made by the IMF that growth would recede, as prices decline for the Mongolia’s largest commodity exports and growth slows in China - the country’s main trading partner.

Monetary tightening to curb signs of overheating, combined with the slowing growth in 2012, contributed to a moderation of CPI inflation from a peak of 17.8% year-on-year in April 2012 to 11.1% in February 2013. Likewise, the growth of bank credit declined throughout the year from highs of close to 70% year-on-year in early 2012 to average 35% in the first two months of 2013. In this context, and although inflation had not yet reached the central bank target of under ten percent, the Bank of Mongolia cut its policy rate to 12.5% from 13.25% in January of this year.

The budget deficit in 2012 widened to an estimated 4.7% of GDP, largely due to revenue shortfalls from lower than expected earnings from coal and copper exports, as well as elevated public spending. The execution of the 2013 budget will be closely watched, given that a key requirement of the 2010 Fiscal Stability Law - the limitation of the structural budget deficit to 2% of GDP - comes into effect this year. However the revenue assumptions appear optimistic, and are premised on : (1) a real GDP expansion of 18.5% in 2013, and (2) a renegotiation of the Oyu Tolgoi mining agreement. Although we also forecast real GDP to accelerate in 2013, the authorities’ assumptions are significantly higher and hence we expect revenues will reflect the somewhat slower expansion. Moreover, these levels of growth are contingent on the successful operation of the Oyu Tolgoi mine, as commercial shipments are scheduled to begin in June 2013, but it is still unclear if this timeline will be met.

BANKING

16 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Oyu Tolgoi mine operator Rio Tinto, and the government are currently engaged in a dispute over management fees, cost-overruns, and transparency. The government’s effort to claim management of the mine has mounted since late last year, even while Rio Tinto has been rejecting attempts to alter the mining agreement. Talks between the mining company and the government began earlier this year and may continue until June.

Gross international reserves were close to $4.0 billion in February 2012, up from $2.6 billion in October, as the funds from the $1.5 billion Chinggis bond flowed into Mongolia. Proceeds from the debut sovereign issuance will go towards financing power plants near the capital city of Ulaanbaatar and the large mining projects in the South Gobi, as well as other needed infrastructure projects.

BANKING

17 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

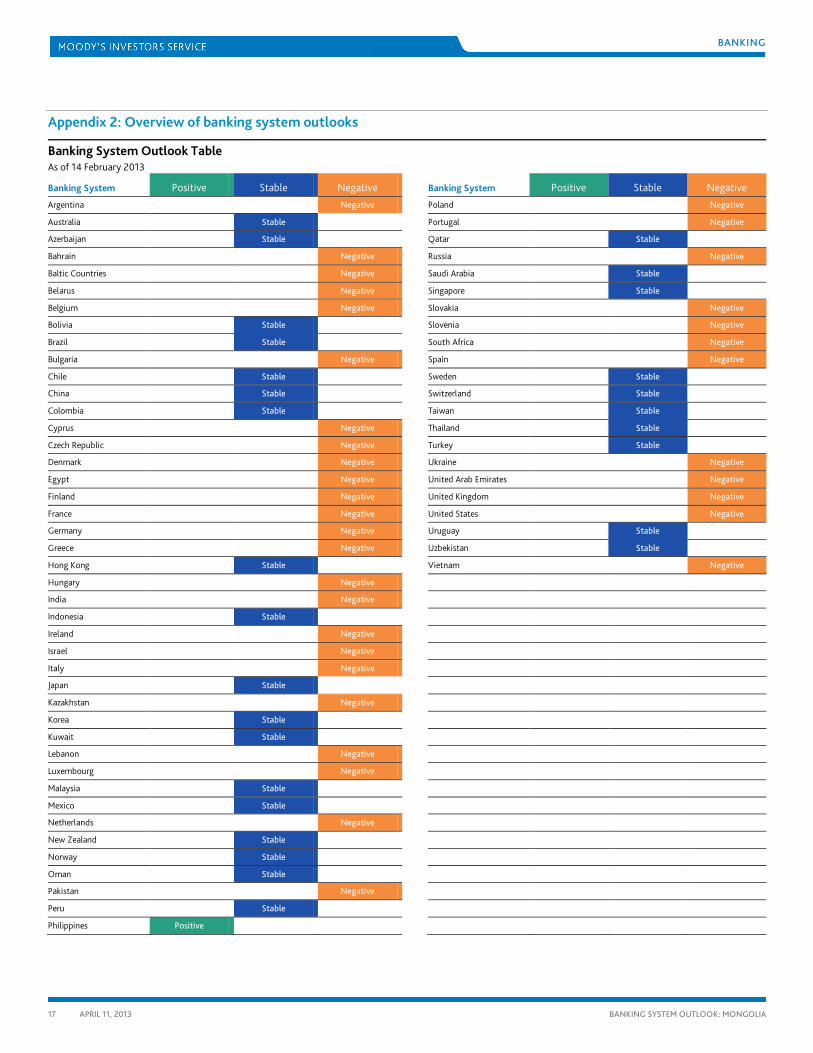

Appendix 2: Overview of banking system outlooks

Banking System Outlook Table As of 14 February 2013

Banking System Positive Stable Negative Banking System Positive Stable Negative Argentina Negative Poland Negative

Australia Stable Portugal Negative

Azerbaijan Stable Qatar Stable

Bahrain Negative Russia Negative

Baltic Countries Negative Saudi Arabia Stable

Belarus Negative Singapore Stable

Belgium Negative Slovakia Negative

Bolivia Stable Slovenia Negative

Brazil Stable South Africa e Negative

Bulgaria Negative Spain Negative

Chile Stable Sweden Stable Negative

China Stable Switzerland Stable

Colombia Stable Taiwan Stable

Cyprus Negative Thailand Stable

Czech Republic Negative Turkey Stable

Denmark Negative Ukraine Negative

Egypt Negative United Arab Emirates Negative

Finland Negative United Kingdom Negative

France Negative United States Negative

Germany Negative Uruguay Stable

Greece Negative Uzbekistan Stable

Hong Kong Stable Vietnam Negative

Hungary Negative

India Negative

Indonesia Stable

Ireland Negative

Israel Negative

Italy Negative

Japan Stable

Kazakhstan Negative

Korea Stable

Kuwait Stable

Lebanon Negative

Luxembourg Negative

Malaysia Stable

Mexico Stable

Netherlands Negative

New Zealand Stable

Norway Stable Negative

Oman Stable

Pakistan Negative

Peru Stable

Philippines Positive

BANKING

18 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Appendix 3: Global Comparison Charts

Asset-Weighted Average Bank Financial Strength Ratings (as of 9 April 2013)

E E+ D- D D+ C- C C+ B- B B+ A- A

BANKING

19 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Asset-Weighted Average Local Currency Long-Term Bank Deposit Ratings (as of 9 April 2013)

C Ca Caa3

Caa2

Caa1

B3 B2 B1 Ba3

Ba2

Ba1

Baa3

Baa2

Baa1

A3 A2 A1 Aa3

Aa2

Aa1

Aaa

BANKING

20 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Asset-Weighted Average Foreign Currency Long-Term Bank Deposit Ratings (as of 9 April 2013)

C Ca Caa3

Caa2

Caa1

B3 B2 B1 Ba3

Ba2

Ba1

Baa3

Baa2

Baa1

A3 A2 A1 Aa3

Aa2

Aa1

Aaa

BANKING

21 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

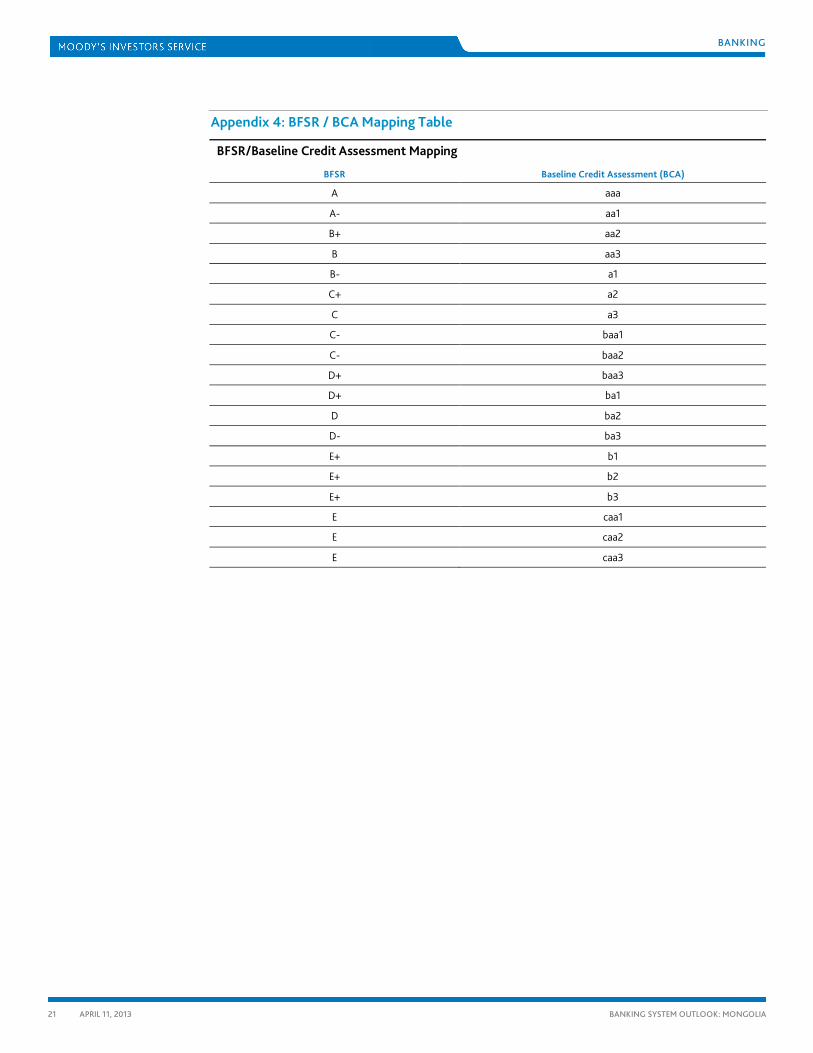

Appendix 4: BFSR / BCA Mapping Table

BFSR/Baseline Credit Assessment Mapping BFSR Baseline Credit Assessment (BCA)

A aaa

A- aa1

B+ aa2

B aa3

B- a1

C+ a2

C a3

C- baa1

C- baa2

D+ baa3

D+ ba1

D ba2

D- ba3

E+ b1

E+ b2

E+ b3

E caa1

E caa2

E caa3

BANKING

22 APRIL 11, 2013

BANKING SYSTEM OUTLOOK: MONGOLIA

Report Number: 151325

Author Hyun Hee Park

Production Specialist Kerstin Thoma

© 2013 Moody’s Investors Service, Inc. and/or its licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY’S INVESTORS SERVICE, INC. (“MIS”) AND ITS AFFILIATES ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY’S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY’S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the information contained herein must make its own study and evaluation of each security it may consider purchasing, holding or selling.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

For Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail clients. It would be dangerous for retail clients to make any investment decision based on MOODY’S credit rating. If in doubt you should contact your financial or other professional adviser.