monday 21 march 2016 investing with the experts

TRANSCRIPT

Monday 21 March 2016

Investing with the experts

We had a terrific turn up at our Switzer Investing Strategy days last week in Sydney and Melbourne.Over 600 investors were eager to learn from our experts, who shared some valuable investment ideas,which I share with you today. Also in today’s Switzer Super Report, Paul Rickard tells us about thesecrets behind dividend imputation and tax deferred income.

Hyperion’s Mark Arnold gives us three stock picks for tomorrow and our chartist Gary Stone looks atthe recent rise in the S&P/ASX 200 and finds there could be a resistance zone.

Sincerely,

Peter Switzer

Inside this Issue

The tax secrets everyinvestor must knowby Paul Rickard02

02 The tax secrets every investor must knowThe thirst to learnby Paul Rickard

05 5 investment insights from the Switzer giantsLearn from the legendsby Peter Switzer

08 3 growth stocks for tomorrowSustainable earningsby Mark Arnold

10 Buy, Sell, Hold – what the brokers sayMedibank Private and Myerby Rudi Filapek-Vandyck

13 S&P/ASX200 not yet out of the woodsShort-term peaksby Gary Stone

15 Super Stock Selectors – Oil Search and Rio TintoRio Tinto and Wesfarmersby Christine St Anne

Switzer Super Report is published by Switzer Financial Group Pty Ltd AFSL No. 286 53136-40 Queen Street, Woollahra, 2025T: 1300 SWITZER (1300 794 8937) F: (02) 9327 4366

Important information: This content has been prepared without taking accountof the objectives, financial situation or needs of any particular individual. It doesnot constitute formal advice. For this reason, any individual should, beforeacting, consider the appropriateness of the information, having regard to theindividual's objectives, financial situation and needs and, if necessary, seekappropriate professional advice.

The tax secrets every investor must knowby Paul Rickard

What a fantastic response to the Switzer InvestorStrategy days in Melbourne and Sydney (next time, Ihope we can cover Adelaide, Brisbane and Perth)!The thing that blew me away, apart from the level ofengagement and the quality of the questions, was thethirst to learn more about tax effective investing.While you should never invest for tax reasons alone,understanding how you are taxed is so important,because the return you get to keep is after theAustralian Taxation Office (ATO) takes their share.Here are the questions I get asked most often.

Why aren’t all dividends franked?

Dividend imputation is a system that is unique toAustralia. It was introduced in 1987 by Treasurer PaulKeating to eliminate what was then referred to as thedouble taxation of company profits.

For example, if a company made a profit of $100, itpaid company tax of $30. If the after tax amount of$70 was then paid as a dividend to a shareholderpaying tax at the highest marginal rate of 49%, theshareholder paid another $34.30 in tax and got tokeep $35.70. Of the original $100 profit, $64.30 hadbeen paid in tax to the ATO.

Dividend imputation eliminates double taxation byallowing each shareholder to recognize that thecompany has already paid (in this case) $30 in tax.Shareholders only pay tax if their marginal tax rate isabove the company tax rate, or if below, get a full orpartial refund of the tax the company has paid.

So, why aren’t all dividends franked?

It is an Australian system and the ATO onlyrecognises tax that has been paid to it. WhenAustralian companies have business operations andearn revenue overseas, they usually pay tax in those

jurisdictions. Back in Australia, the ATO recognisesthat they have already paid tax overseas, so they arenot required to pay tax here. If they haven’t paid anyAustralian tax, they can’t frank their dividends.

Companies like CSL (CSL) or Resmed (RMD), whichearn more than 90% of their revenue outsideAustralia, pay little or virtually no Australian companytax. Accordingly, their dividends are unfranked. Some companies have a more even split betweenonshore and offshore business and can partly franktheir dividends (an example is Macquarie, which has40% franking).

The other reason that companies can’t frank theirdividends is that although they might have anoperating cash surplus and are in a position to pay adividend, they aren’t paying any tax due to the use ofnon-cash taxation deductions, such as amortizationor depreciation. Examples include Transurban (TCL)and Sydney Airport (SYD). Both these companieshave substantial depreciation or amortization charges(due to the capital investment required to build theinfrastructure), and are now spinning off considerablecash, which can be paid as a dividend. As they aren’tpaying any company tax, they can’t frank thesedividends.

How does dividend imputation work?

So that every shareholder gets the same benefit (thetax to be paid is reduced by the tax that the companyhas already paid), it works as follows.

Firstly, both the dividend in cash, and the non-cashfranking credit (sometimes called an imputationcredit) is included in your taxable income. Bothamounts are included upfront, so that the whole profitis being taxed in the hands of the shareholder.

02Monday 21 March 2016

Next, tax is assessed at your marginal rate.

And then, the imputation credit is applied again like arefundable tax offset.

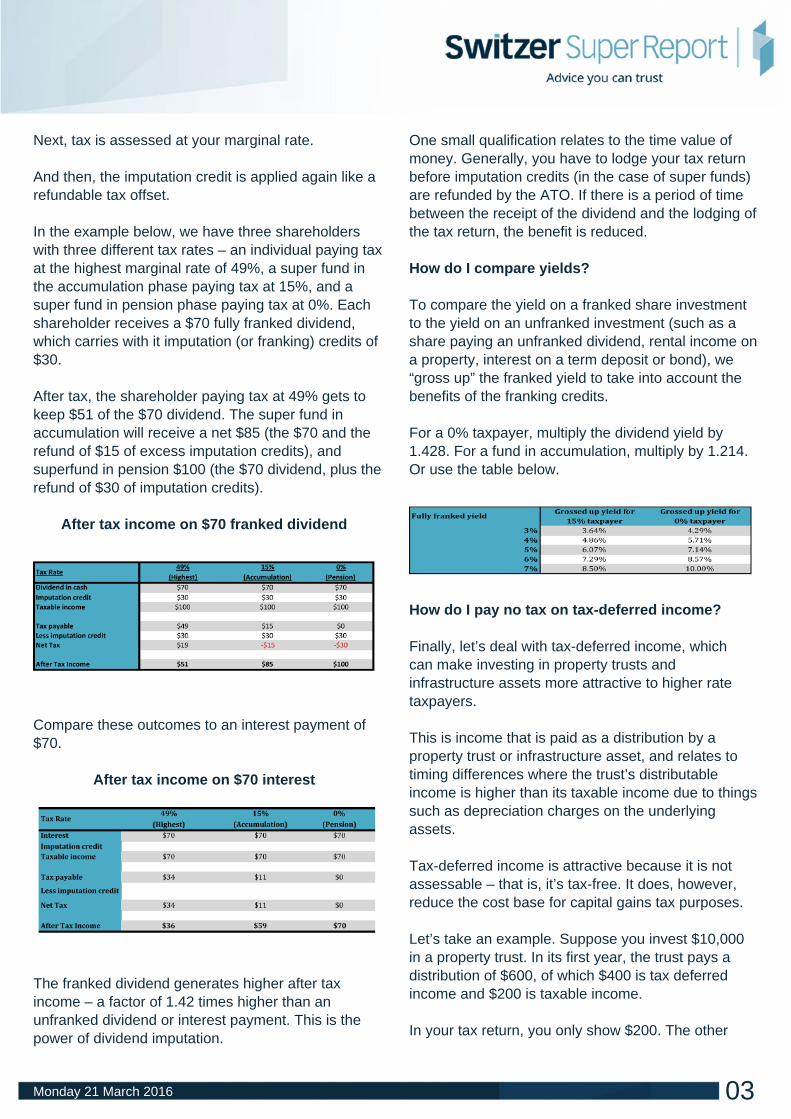

In the example below, we have three shareholderswith three different tax rates – an individual paying taxat the highest marginal rate of 49%, a super fund inthe accumulation phase paying tax at 15%, and asuper fund in pension phase paying tax at 0%. Eachshareholder receives a $70 fully franked dividend,which carries with it imputation (or franking) credits of$30.

After tax, the shareholder paying tax at 49% gets tokeep $51 of the $70 dividend. The super fund inaccumulation will receive a net $85 (the $70 and therefund of $15 of excess imputation credits), andsuperfund in pension $100 (the $70 dividend, plus therefund of $30 of imputation credits).

After tax income on $70 franked dividend

Compare these outcomes to an interest payment of$70.

After tax income on $70 interest

The franked dividend generates higher after taxincome – a factor of 1.42 times higher than anunfranked dividend or interest payment. This is thepower of dividend imputation.

One small qualification relates to the time value ofmoney. Generally, you have to lodge your tax returnbefore imputation credits (in the case of super funds)are refunded by the ATO. If there is a period of timebetween the receipt of the dividend and the lodging ofthe tax return, the benefit is reduced.

How do I compare yields?

To compare the yield on a franked share investmentto the yield on an unfranked investment (such as ashare paying an unfranked dividend, rental income ona property, interest on a term deposit or bond), we“gross up” the franked yield to take into account thebenefits of the franking credits.

For a 0% taxpayer, multiply the dividend yield by1.428. For a fund in accumulation, multiply by 1.214.Or use the table below.

How do I pay no tax on tax-deferred income?

Finally, let’s deal with tax-deferred income, whichcan make investing in property trusts andinfrastructure assets more attractive to higher ratetaxpayers.

This is income that is paid as a distribution by aproperty trust or infrastructure asset, and relates totiming differences where the trust’s distributableincome is higher than its taxable income due to thingssuch as depreciation charges on the underlyingassets.

Tax-deferred income is attractive because it is notassessable – that is, it’s tax-free. It does, however,reduce the cost base for capital gains tax purposes.

Let’s take an example. Suppose you invest $10,000in a property trust. In its first year, the trust pays adistribution of $600, of which $400 is tax deferredincome and $200 is taxable income.

In your tax return, you only show $200. The other

03Monday 21 March 2016

$400 is tax-free. However, your cost base for capitalgains tax purposes is reduced by that $400 to $9,600.When you finally come to sell the asset, you will paycapital gains tax on the difference between the saleprice and the reduced cost price of $9,600.

If you are an individual, you will only pay tax on halfthe gain. If your fund is in accumulation, it will pay taxon two thirds of the gain. And if your fund has nowmoved into pension phase, it won’t pay any tax onthe capital gain. In this case, your fund won’t havepaid any tax at all on the tax-deferred income.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

04Monday 21 March 2016

5 investment insights from the Switzer giantsby Peter Switzer

Sir Isaac Newton made famous a wonderfulobservation on the insights that are delivered to usalong the way: “If I have seen further, it is bystanding on the shoulders of giants.”

And on Wednesday in Melbourne and Thursday inSydney, we held the Switzer Investor Strategy Daysand yep, I was hanging out with giants.

The Switzer giants were Charlie Aitken (AitkenInvestment Management), George Boubouras(Contango Asset Management), John Julian (AMPCapital), John Murray (Perennial ValueManagement), Michael Blake (Centuria Capital),David Poppenbeeck (K2 Asset Management), KrisWalesby (Head of ANZ’s ETFS) and, of course, myold mate, Paul Rickard.

Of course, none of these people consider themselvesas giants, well maybe Charlie might, but they are allvery insightful professionals and considering ourfeedback from the events, they certainly delivered ina giant way.

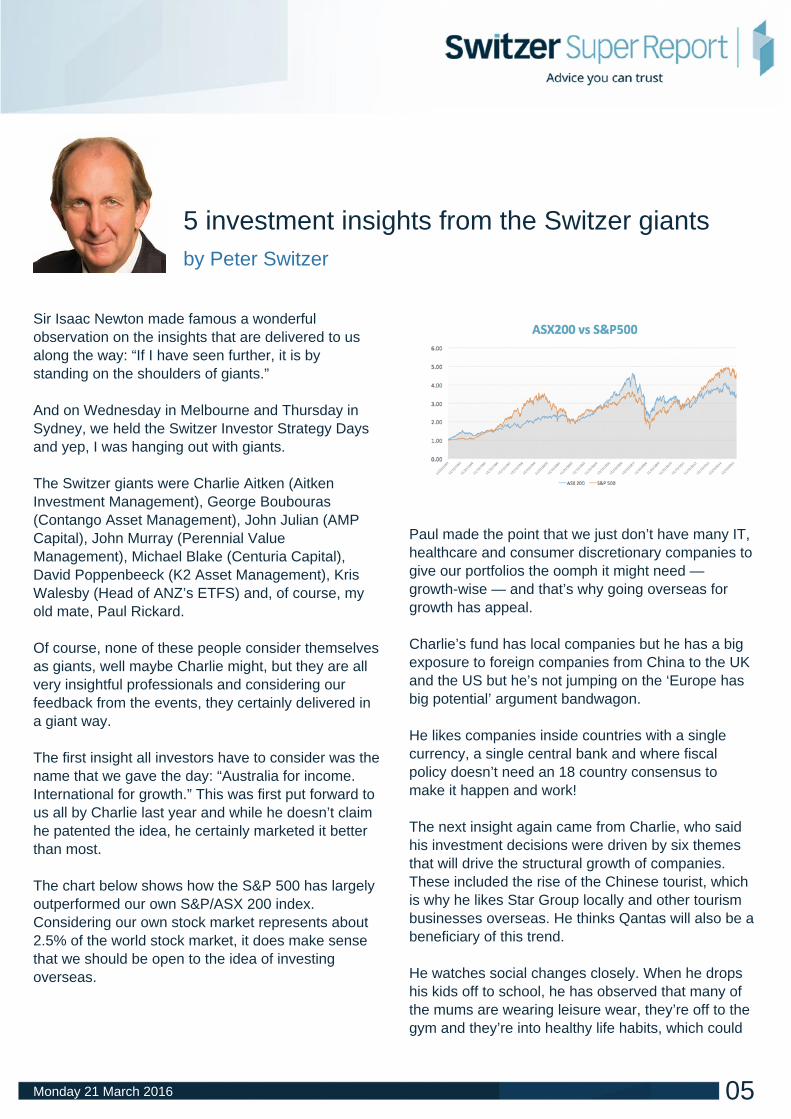

The first insight all investors have to consider was thename that we gave the day: “Australia for income.International for growth.” This was first put forward tous all by Charlie last year and while he doesn’t claimhe patented the idea, he certainly marketed it betterthan most.

The chart below shows how the S&P 500 has largelyoutperformed our own S&P/ASX 200 index.Considering our own stock market represents about2.5% of the world stock market, it does make sensethat we should be open to the idea of investingoverseas.

Paul made the point that we just don’t have many IT,healthcare and consumer discretionary companies togive our portfolios the oomph it might need —growth-wise — and that’s why going overseas forgrowth has appeal.

Charlie’s fund has local companies but he has a bigexposure to foreign companies from China to the UKand the US but he’s not jumping on the ‘Europe hasbig potential’ argument bandwagon.

He likes companies inside countries with a singlecurrency, a single central bank and where fiscalpolicy doesn’t need an 18 country consensus tomake it happen and work!

The next insight again came from Charlie, who saidhis investment decisions were driven by six themesthat will drive the structural growth of companies.These included the rise of the Chinese tourist, whichis why he likes Star Group locally and other tourismbusinesses overseas. He thinks Qantas will also be abeneficiary of this trend.

He watches social changes closely. When he dropshis kids off to school, he has observed that many ofthe mums are wearing leisure wear, they’re off to thegym and they’re into healthy life habits, which could

05Monday 21 March 2016

be bad for CCL but great for a US company like Fitbit.Next, the cashless society will be great for the likes ofVisa, as we all tap and go and leave this US companya small fee every time we tap!

He invests in companies that are into technology,disruption, superannuation and he loves the notion ofmonopoly toll bridges.The theme is clear: these businesses create theirown opportunities and some don’t even have anypotential threats. Not surprisingly, Charlie likesSydney Airports and Transurban.

Charlie’s lecture opened our minds to what weshould be thinking about to grab growth but thenGeorge argued that we should never ignorediversification. He actually threw in the observationthat “if you can sleep when stock markets have theirone in four bad years, you can be 100% invested instocks”, but few of us can live with that pressure.

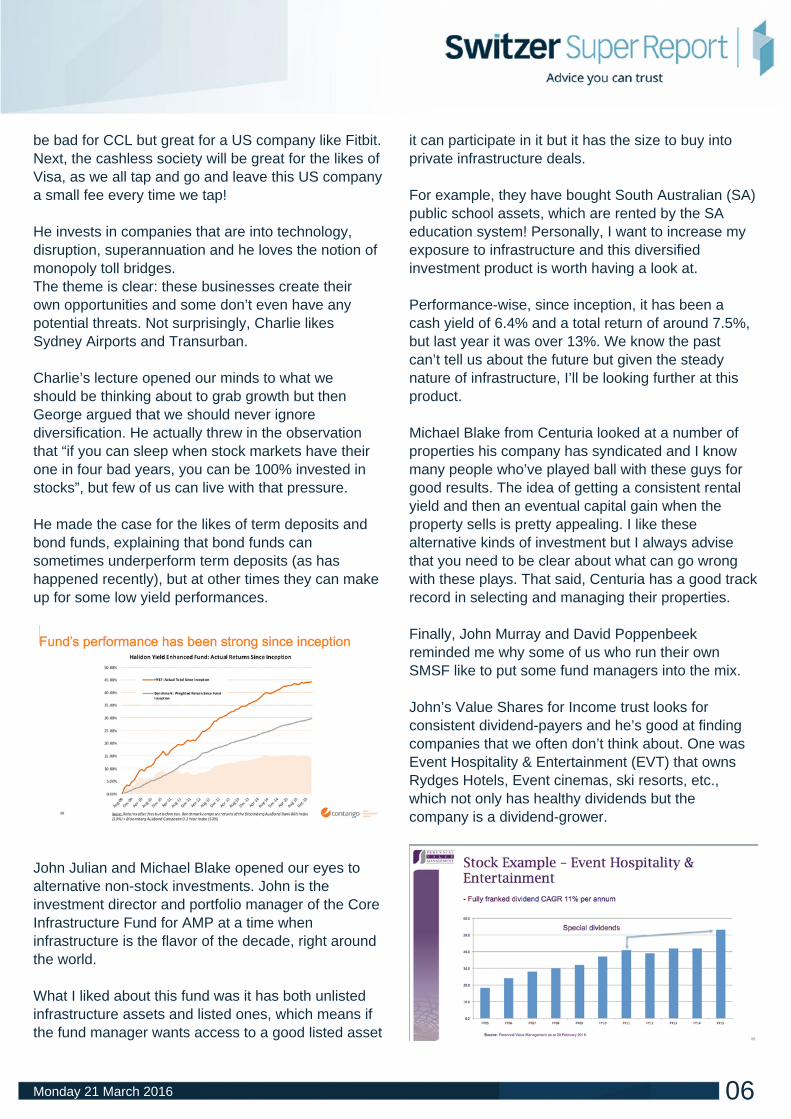

He made the case for the likes of term deposits andbond funds, explaining that bond funds cansometimes underperform term deposits (as hashappened recently), but at other times they can makeup for some low yield performances.

John Julian and Michael Blake opened our eyes toalternative non-stock investments. John is theinvestment director and portfolio manager of the CoreInfrastructure Fund for AMP at a time wheninfrastructure is the flavor of the decade, right aroundthe world.

What I liked about this fund was it has both unlistedinfrastructure assets and listed ones, which means ifthe fund manager wants access to a good listed asset

it can participate in it but it has the size to buy intoprivate infrastructure deals.

For example, they have bought South Australian (SA)public school assets, which are rented by the SAeducation system! Personally, I want to increase myexposure to infrastructure and this diversifiedinvestment product is worth having a look at.

Performance-wise, since inception, it has been acash yield of 6.4% and a total return of around 7.5%,but last year it was over 13%. We know the pastcan’t tell us about the future but given the steadynature of infrastructure, I’ll be looking further at thisproduct.

Michael Blake from Centuria looked at a number ofproperties his company has syndicated and I knowmany people who’ve played ball with these guys forgood results. The idea of getting a consistent rentalyield and then an eventual capital gain when theproperty sells is pretty appealing. I like thesealternative kinds of investment but I always advisethat you need to be clear about what can go wrongwith these plays. That said, Centuria has a good trackrecord in selecting and managing their properties.

Finally, John Murray and David Poppenbeekreminded me why some of us who run their ownSMSF like to put some fund managers into the mix.

John’s Value Shares for Income trust looks forconsistent dividend-payers and he’s good at findingcompanies that we often don’t think about. One wasEvent Hospitality & Entertainment (EVT) that ownsRydges Hotels, Event cinemas, ski resorts, etc.,which not only has healthy dividends but thecompany is a dividend-grower.

06Monday 21 March 2016

David Poppenbeek of K2 Asset Management lookedat the wild and wacky things his team looks at to findvalue here and around the world. They look atcomplex relationships between commodity prices, thedollar, the greenback, households and, ultimately, onshare prices. He also showed how the strangestinformation can show up if you look in odd butsensible places, such as The Economist’sIntelligence Unit that showed Australia has five of themost livable cities in the top 20, with four in the top10!

Like Charlie, David’s team is looking for ideas thatare linked to trends that one day will explain highershare prices.

Finally, Kris Walesby explained how ANZ’constructed its S&P500 Yield Low Volatlity ETF. Insimple terms, they have created a process that givesthem the 50 highest yielding US companies with theleast volatility. And by the way, there isn’t a W-8BENform to fill out for US taxes!

The most recent result was a yield of 4.2%, while thecomparative S&P500 yield was 2.2%.

The bottom line is simple and I have given the sameadvice to aspirational entrepreneurs who’ve beentrying to build their businesses — leave yourself openfor new tricks and learn from legends or giants.

P.S. I thought I had five insights but as I wrote andreflected on the strategy days, I realised that therewere way more than five insights. Consider the extrasa Switzer bonus!

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

07Monday 21 March 2016

3 growth stocks for tomorrowby Mark Arnold

Commentary from companies over recent reportingseasons has highlighted the anaemic growth in thecurrent economic environment.

The economy is now well and truly in an environmentof low growth and with a lack of revenue growthoptions available to most companies, there has beenan increasing focus by management to reduce costs,thereby increasing margins and earnings. It is notsurprising then that companies that are achievingstrong revenue growth are being rewarded with shareprice performance.

Outperformance has prompted caution for growthstocks given an increasing dispersion in the price toearnings ratio (PER) between growth companies andlow growth companies. There is no doubt that currentstrong share price performance diminishes expectedreturns in the future, however, the consideration for acompany’s valuation should be guided by its longterm earnings potential, rather than short termearnings and short term valuation metrics. Over time,share prices should follow a company’s earnings,and we look for businesses that can grow theirearnings predictably and consistently.

The difficulty, we believe, is selecting companies thathave a way of protecting outsized returns sustainablyover the long term and whether the current shareprice adequately compensates investors based onthe earnings potential. We focus on some of theattributes that we believe to be important below:

A large market potential

Ability to sustainably generate substantial organicgrowth depends on the size of the market opportunity.Domino’s Pizza Enterprises (DMP) is an example ofa company that has been able to leverage its worldclass technology and franchising model from

Australia to the globe, currently in seven keycountries. Other factors to consider includefavourable structural shifts within a market, such asthe transition from print-based advertising to onlineadvertising.

Sustainable competitive advantage

There is no use capturing a large market if you areunable to protect outsized returns. Typically, when anindustry’s economics are favourable, competitors willenter the market, eroding the returns on capital thatare available. Companies that can consistentlygenerate high returns and achieve high margins tendto have a sustainable competitive advantage. REAGroup’s (REA) sustainable competitive advantagecomes from the strong network effect on its propertyadvertising website, which provides it considerablepricing power.

Consumers in the market for property are drawn tothe website with the greatest number of listings, whileagents will place listings on the site with the greatestnumber of eyeballs, creating a virtuous cycle. Further,given the advertising cost represents a smallpercentage of the cost of a house, this places REA ina strong position.

08Monday 21 March 2016

Ability to reinvest capital

Companies need to invest capital back into theirbusiness to drive future earnings growth and protecttheir sustainable competitive advantages. We look forcompanies that have capital light balance sheets andare able to reinvest that capital at high rates of return.

There is a balancing act required between investingand meeting short-term earnings expectations. Largerinvestments come at the cost of reduced earnings inthe short term, however, provide the potential foradditional gains in future years. The market’s shortterm focus on earnings can result in opportunities andthis was evident with SEEK (SEK) when it reported its2015 full year results in August 2015.

Control over destiny

Generating returns from a portfolio of stocks is asmuch about what you exclude from your portfolio aswhat you include. We exclude companies that haveno or limited control over their destiny in terms of theproduct or service they sell. The weakness in theresources sector highlights the lack of controlcompanies in this sector have over their revenuesand profits. This cyclicality makes it very difficult toprovide comfort that earnings can be generatedsustainably over the long term. Other factors that welook negatively on include excessive gearing, lack oforganic growth options and high capital intensity.

Mark Arnold is the chief investment officer ofHyperion Asset Management.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

09Monday 21 March 2016

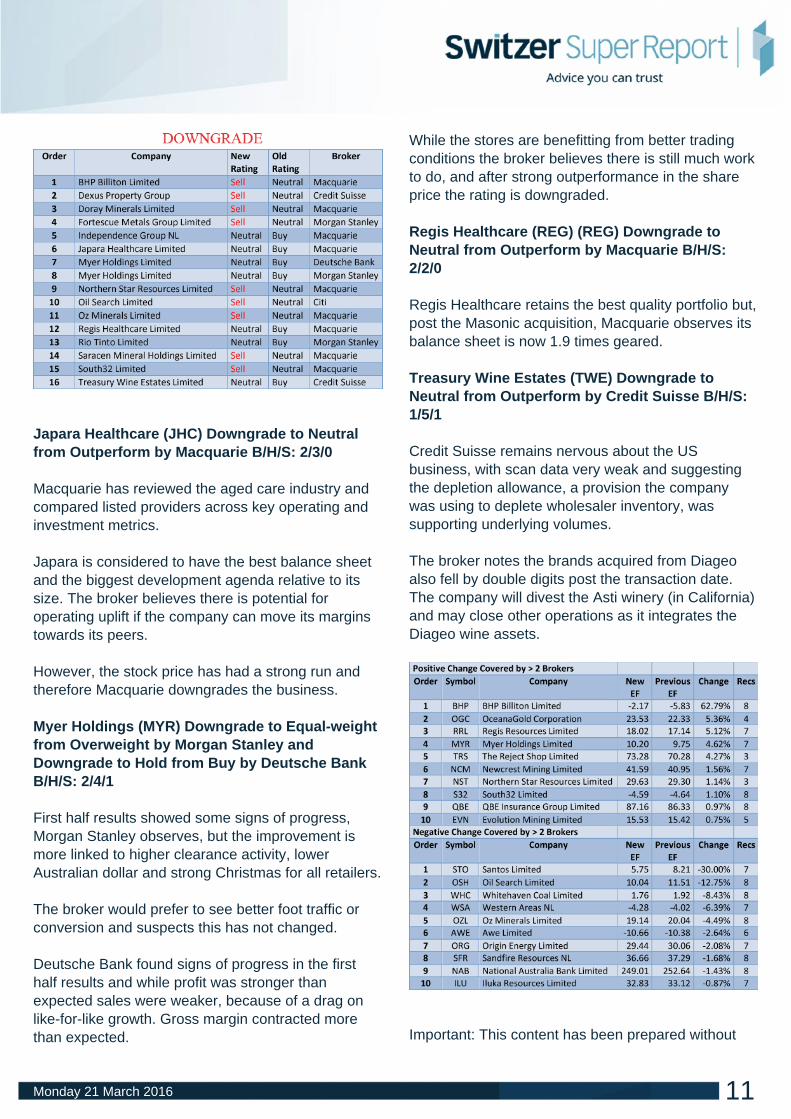

Buy, Sell, Hold – what the brokers sayby Rudi Filapek-Vandyck

In the good books

Estia Health Limited (EHE) Upgrade toOutperform from Neutral by Macquarie B/H/S:3/1/0

Macquarie has reviewed the aged care industry andcompared listed providers across key operating andinvestment metrics. Estia Health disappointed thebroker in the first half because of a ramp up in costs.

Still, it offers the most attractive valuation after recentweakness and the rating is upgraded.

See downgrade for Japara Healthcare and RegisHealthcare.

Medibank Private (MPL) Upgrade to Outperformfrom Neutral by Macquarie B/H/S: 2/4/1

The Australian Medical Association has released its2016 private health insurance report. Macquariebelieves health insurers are across the issuesoutlined in the report.

The broker believes Medibank Private’s FY16earnings risk is skewed to the upside and claimsgrowth risk is on the downside. Regulatory risk ismoderating as the 2016 budget approaches and thefederal election looms.

Macquarie therefore upgrades the business.

The Reject Shop (TRS) Upgrade to Equal-weightfrom Underweight by Morgan Stanley B/H/S: 2/1/0

Morgan Stanley analysts admit the operationalturnaround has occurred much quicker thanexpected. They have now gained sufficientconfidence in that positive momentum is sustainable.

They do, however, have a problem with the shareprice, hence why the upgrade stops at Equal-Weight.

In the not-so-good books

Dexus Property group (DXS) Downgrade toUnderperform from Neutral by Credit SuisseB/H/S: 0/2/2The stock has performed strongly over the pastmonth, despite delivering the worst relativeperformance at the results, in Credit Suisse’s view.

The broker attributes the recent rally to increasedprobability on Dexus walking away from the InvestaOffice (IOF) bid. This would be a positive outcome forDexus unit holders.

But the broker observes emerging details suggestthere is minimal earnings upside for Dexus in terms ofInvesta’s existing management and feearrangements.

10Monday 21 March 2016

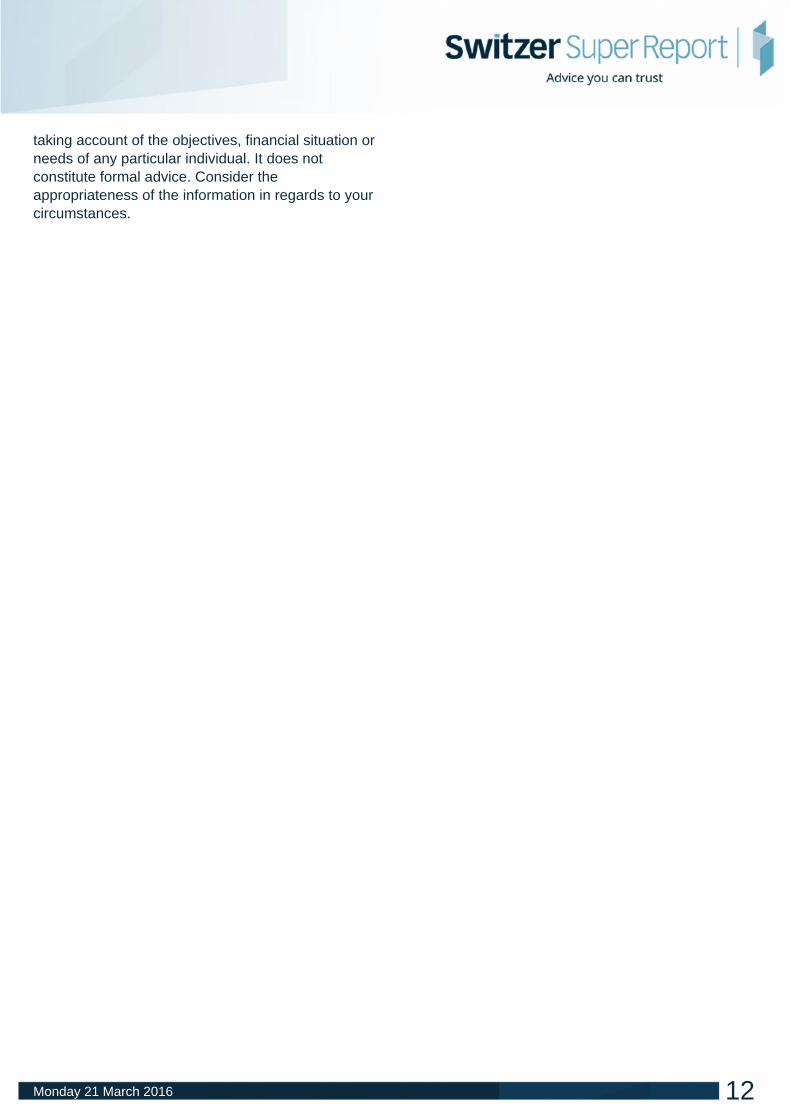

Japara Healthcare (JHC) Downgrade to Neutralfrom Outperform by Macquarie B/H/S: 2/3/0

Macquarie has reviewed the aged care industry andcompared listed providers across key operating andinvestment metrics.

Japara is considered to have the best balance sheetand the biggest development agenda relative to itssize. The broker believes there is potential foroperating uplift if the company can move its marginstowards its peers.

However, the stock price has had a strong run andtherefore Macquarie downgrades the business.

Myer Holdings (MYR) Downgrade to Equal-weightfrom Overweight by Morgan Stanley andDowngrade to Hold from Buy by Deutsche BankB/H/S: 2/4/1

First half results showed some signs of progress,Morgan Stanley observes, but the improvement ismore linked to higher clearance activity, lowerAustralian dollar and strong Christmas for all retailers.

The broker would prefer to see better foot traffic orconversion and suspects this has not changed.

Deutsche Bank found signs of progress in the firsthalf results and while profit was stronger thanexpected sales were weaker, because of a drag onlike-for-like growth. Gross margin contracted morethan expected.

While the stores are benefitting from better tradingconditions the broker believes there is still much workto do, and after strong outperformance in the shareprice the rating is downgraded.

Regis Healthcare (REG) (REG) Downgrade toNeutral from Outperform by Macquarie B/H/S:2/2/0

Regis Healthcare retains the best quality portfolio but,post the Masonic acquisition, Macquarie observes itsbalance sheet is now 1.9 times geared.

Treasury Wine Estates (TWE) Downgrade toNeutral from Outperform by Credit Suisse B/H/S:1/5/1

Credit Suisse remains nervous about the USbusiness, with scan data very weak and suggestingthe depletion allowance, a provision the companywas using to deplete wholesaler inventory, wassupporting underlying volumes.

The broker notes the brands acquired from Diageoalso fell by double digits post the transaction date.The company will divest the Asti winery (in California)and may close other operations as it integrates theDiageo wine assets.

Important: This content has been prepared without

11Monday 21 March 2016

taking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

12Monday 21 March 2016

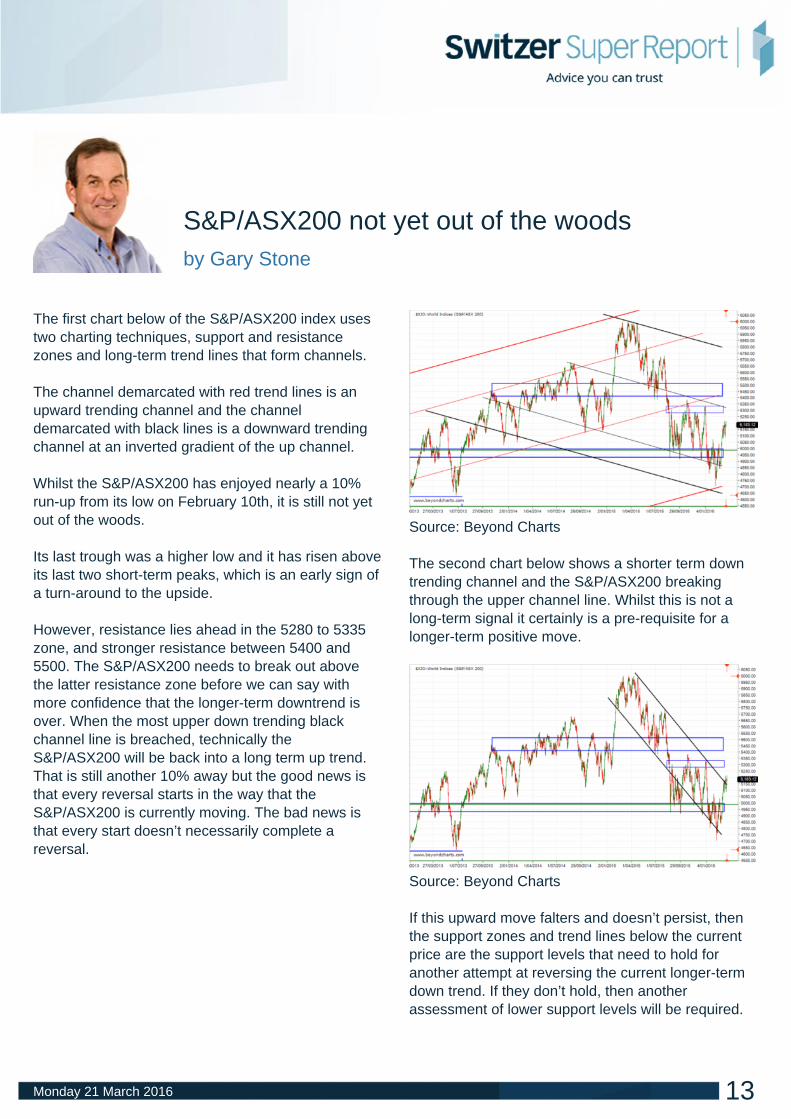

S&P/ASX200 not yet out of the woodsby Gary Stone

The first chart below of the S&P/ASX200 index usestwo charting techniques, support and resistancezones and long-term trend lines that form channels.

The channel demarcated with red trend lines is anupward trending channel and the channeldemarcated with black lines is a downward trendingchannel at an inverted gradient of the up channel.

Whilst the S&P/ASX200 has enjoyed nearly a 10%run-up from its low on February 10th, it is still not yetout of the woods.

Its last trough was a higher low and it has risen aboveits last two short-term peaks, which is an early sign ofa turn-around to the upside.

However, resistance lies ahead in the 5280 to 5335zone, and stronger resistance between 5400 and5500. The S&P/ASX200 needs to break out abovethe latter resistance zone before we can say withmore confidence that the longer-term downtrend isover. When the most upper down trending blackchannel line is breached, technically theS&P/ASX200 will be back into a long term up trend.That is still another 10% away but the good news isthat every reversal starts in the way that theS&P/ASX200 is currently moving. The bad news isthat every start doesn’t necessarily complete areversal.

Source: Beyond Charts

The second chart below shows a shorter term downtrending channel and the S&P/ASX200 breakingthrough the upper channel line. Whilst this is not along-term signal it certainly is a pre-requisite for alonger-term positive move.

Source: Beyond Charts

If this upward move falters and doesn’t persist, thenthe support zones and trend lines below the currentprice are the support levels that need to hold foranother attempt at reversing the current longer-termdown trend. If they don’t hold, then anotherassessment of lower support levels will be required.

13Monday 21 March 2016

However, given the recent rise in the S&P/ASX200,the potential upside scenario should still be the focusfor the time being. Keep an eye on the overheadresistance levels to confirm the current short tomedium term uptrend continuing to strengthen into alonger term uptrend.

Gary Stone is the founder and managing director ofShare Wealth Systems.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

14Monday 21 March 2016

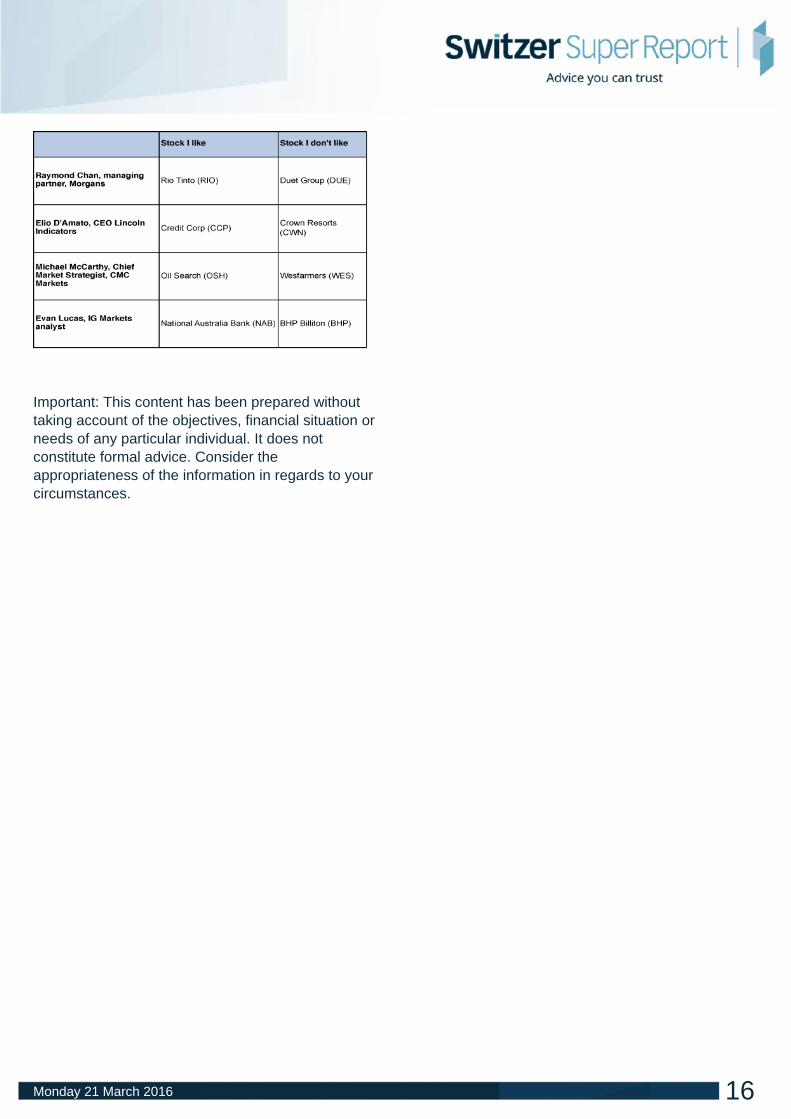

Super Stock Selectors – Oil Search and RioTintoby Christine St Anne

Out of all the banks, IG markets’ Evan Lucas likesthe National Australia Bank (NAB). Lucas remains ofthe view that the banks will be the ones doing theheavy lifting but notes that with the sale of its UKbanking business, NAB should improve its assetquality.

“We think its earnings report in a few weeks may giveit a fundamental reason to leg up on ANZ (ANZ) andstart to really hone in on the Commonwealth Bank ofAustralia (CBA) and Westpac (WBC),” Lucas says.

While Lucas is not as bearish on BHP Billiton (BHP)as he was a year ago, he says now is the right timefor some profit taking in the stock.

“I believe there is a longer-term fundamental story tobuy into, however, the short term pain is still there.BHP itself is bearish on iron ore and is battling withwhat to do with its thermal coal assets. I see BHPeasing back this week,” he says.

On the mining theme, Morgans’ Raymond Chan likesRio Tinto (RIO).

“Before the China-led resource boom, investors werebuying Rio for copper exposure. The chief executiveelected (Sebastien Jacques) is currently the head ofthe smaller copper division. Based in UnitedKingdom, we believe he’s the right candidate asWalsh’s successor,” Chan says.

Chan still does not like the utility Duet (DUE), despiteits attractive yield and notes that the “technical trendlooks weak”.

The energy theme continued with CMC Markets’Michael McCarthy picking Oil Search (OSH) as hispreferred stock this week.

“In my opinion the answer to a carbon constrained

world is natural gas. Oil Search has quality globalasset and a good track record,” he says.

The share rice of $7 could signal excellent long-termvalue, according to McCarthy.

McCarthy does not like Wesfarmers (WES) becausethe stock is too expensive, given its growth prospects.

This week, Lincoln Indicators Elio D’Amato likes theAustralian receivables management company CreditCorp (CCP). Although there has been negative mediaattention on payday lending, it is not expected toimpact on the business, says D’Amato.

This is because the business is primarily focused onbuying distressed consumer debt ledgers from banks,finance and telecommunication companies forsubsequent recovery.

“We anticipate strong growth in the near term with asubstantial increase in purchased debt ledgeracquisitions,” he says.

However, D’Amato does not like gaming andentertainment business Crown Resorts.

The company has recently struggled to growprofitability, with half-year net profit down 22% withdeclining contributions from the Macau businesses.Gaming revenue over the same period fell 31%

“While the business maintains a positive medium tolong term growth outlook, the Macau operationscontinue to weaken in response to ChineseGovernment policy affecting all casino operators,” hesays.

15Monday 21 March 2016

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regards to yourcircumstances.

Powered by TCPDF (www.tcpdf.org)

16Monday 21 March 2016