modul-4- the financial statement part iiii- statement of ... · the financial statement part iii :...

TRANSCRIPT

MODUL-4

Financial Accounting

The Financial Statement Part III :

Statement of Cash FlowBy

MUH. ARIEF EFFENDI,SE,MSI,AK,QIA

Magister Accounting Program (MAKSI)

BUDI LUHUR UNIVERSITY

Jakarta - Indonesia

2010

The Financial Statement Part III :

Statement of Cash Flow

1. Understand the Basic of the Statement of Cash Flow.

2. Understand the Usefullness of the Statement of Cash Flow.

3. Understand the Elements / Components of the Statement of Cash Flow.

4. Understand the Concepts of the Statement of Cash Flow.

5. Understand Preparing the Statement of Cash Flow.

6. Understand the Indirect & Direct Methods.

7. Understand Two Approaches to Producing the Cash Flow Statement.

8. Understand the Uses of the Statement of Cash Flow.

9. Understand the Exposure Draft PSAK #2 : the Statement of Cash Flow

(Indonesian GAAP : 2009 Revised).

10. Understand the International perspective of the Statement of Cash Flow

(International Accounting Standard # 7 : The Statement of Cash Flow).

After studying this topic, students should be able to:

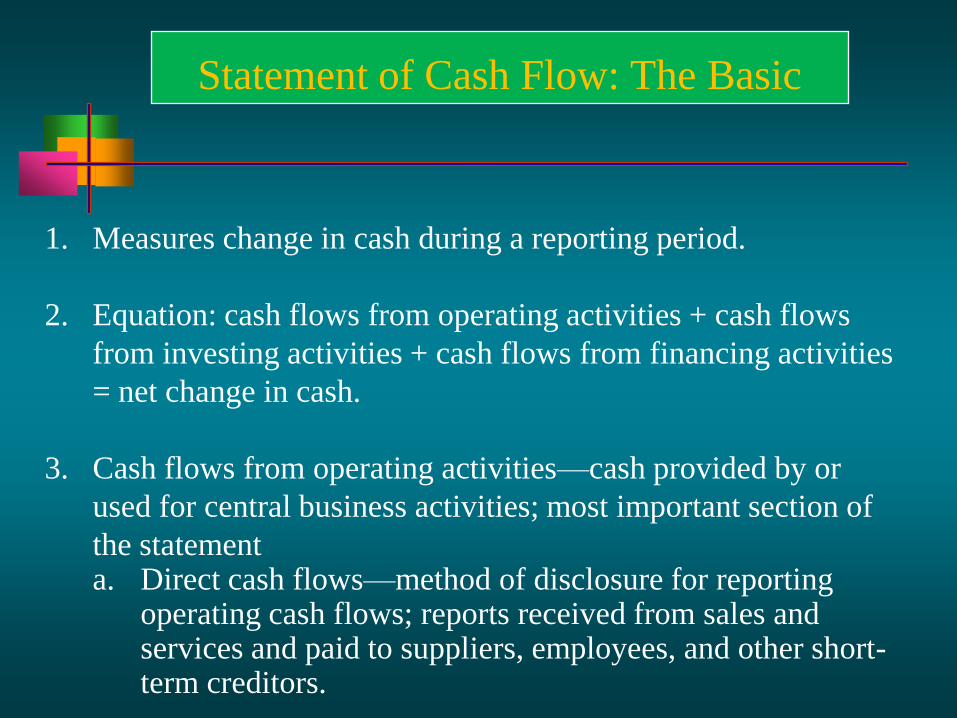

Statement of Cash Flow: The Basic

1. Measures change in cash during a reporting period.

2. Equation: cash flows from operating activities + cash flows

from investing activities + cash flows from financing activities

= net change in cash.

3. Cash flows from operating activities—cash provided by or

used for central business activities; most important section of

the statementa. Direct cash flows—method of disclosure for reporting

operating cash flows; reports received from sales and services and paid to suppliers, employees, and other short-term creditors.

Statement of Cash Flow: The Basic

b. Indirect cash flows—alternative operating cash flow reporting method; reconciles net income to operating cash flow to report operating cash flows.

4. Cash flows from investing activities—cash provided or used

by the disposal and acquisition of long-term assets.

5. Cash flows from financing activities—cash provided or used

by issuing and retiring stocks and bonds and paying dividends.

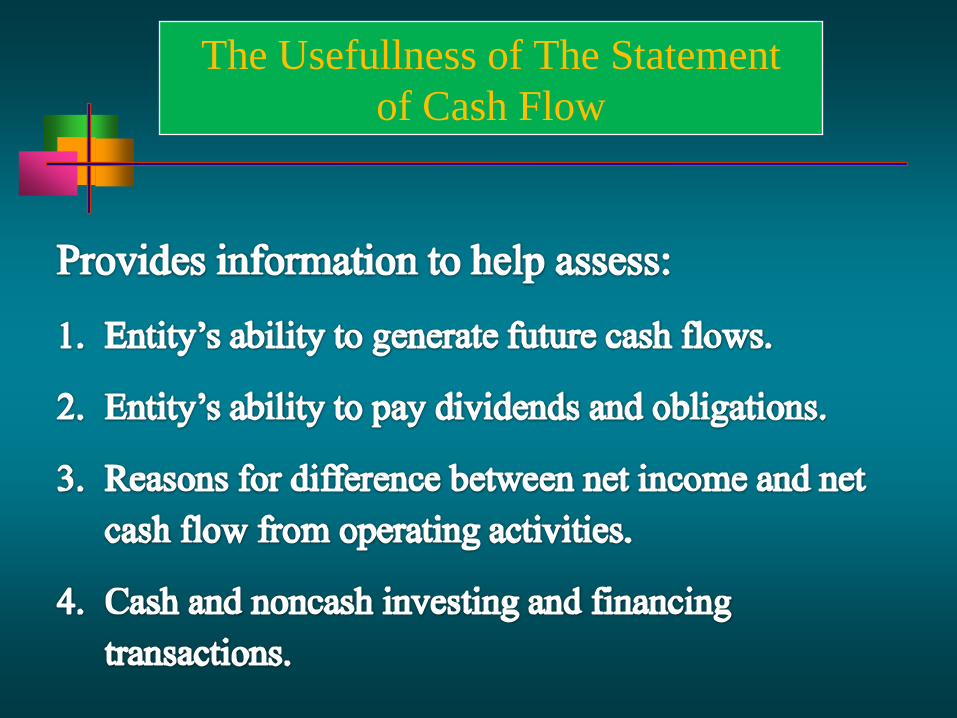

The Usefullness of The Statement

of Cash Flow

Components of The Statement of Cash Flow

Reports the amount of cash

collected and paid out by a

company in operating, investing,

and financing activities.

How did the company

receive cash?

How did the company

use its cash?

Statement of Cash Flows

Cash inflows

Sell goods or services.

Sell other assets or by borrowing.

Receive cash from investments by owners.

Cash outflows

Pay operating expenses.

Expand operations, repay loans.

Pay owners a return on investment.

Elements of The Statement of Cash Flow

Cash

Pool

Operating

activities

Investing

activities

Financing

activities

inflows

Operating

activities

Investing

activities

Financing

activities

outflows

The Statement of Cash Flow :

Concept - 1

Operating

ActivitiesInvesting

Activities

CASH

OUTFLOWS

Financing

Activities

CASH

INFLOWS

Financing

Activities

Operating

Activities

Investing

Activities

The Statement of Cash Flow :

Concept - 2

The Statement of Cash Flow :

Concept - 3

(payments for

expenses)

Operating

Increases in Cash Decreases in Cash

(receipts from sales of

noncurrent assets)

Investing

(receipts from issuing

equity and debt securities)

Financing

(payments for acquiring

noncurrent assets)

Investing

(receipts from

revenues)

Operating

(payments for treasury stock,

dividends, and redemption of debt

securities)

Financing

The Statement of Cash Flow : Concept – 4

Reporting Cash Flow

Preparing The Statement of Cash Flow

Firms could prepare the cash flow statement directly from the cash account. Most, however, find it more efficient to prepare the cash flow statement from the balance sheet and income statement.

1. Direct and indirect methods.

2. Algebraic formulation will present the underlying concept of the cash flow statement.

3. Two approaches to producing the cash flow statement: columnar worksheet and t-account worksheet

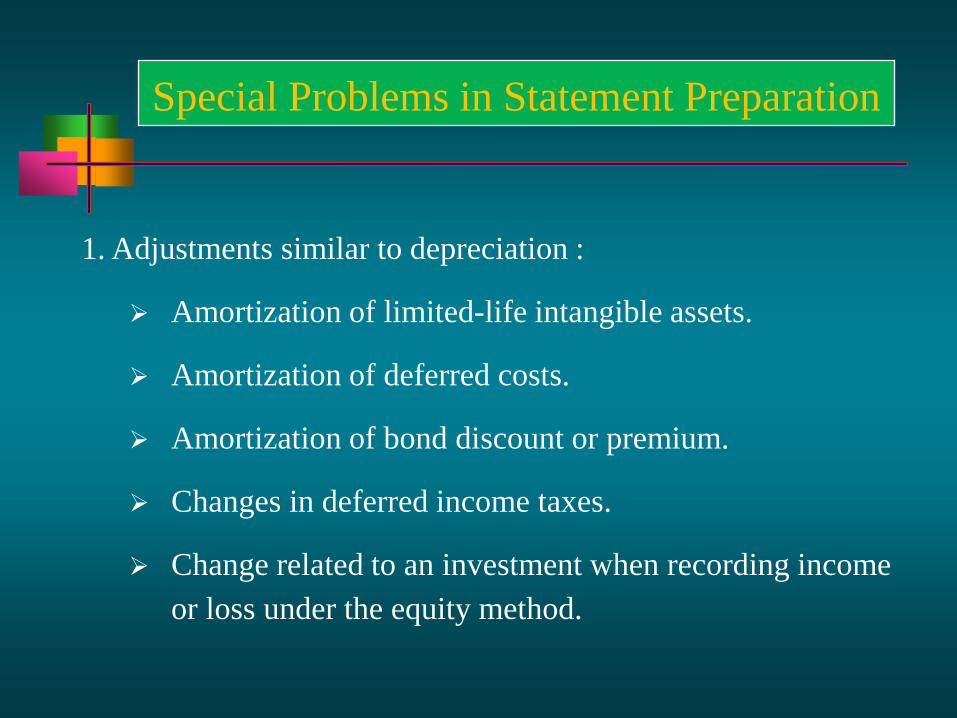

Special Problems in Statement Preparation

1. Adjustments similar to depreciation :

Amortization of limited-life intangible assets.

Amortization of deferred costs.

Amortization of bond discount or premium.

Changes in deferred income taxes.

Change related to an investment when recording income

or loss under the equity method.

Special Problems in Statement Preparation

2. Accounts receivable, net

3. Other working capital changes

4. Net losses

5. Gains

6. Stock options

7. Postretirement benefits

8. Extraordinary items

9. Significant noncash transactions

Three Steps in Preparation

Three Sources of Information :

1. Comparative balance sheets.

2. Current income statement.

3. Selected transaction data.

Three Major Steps:

Step 1. Determine change in cash.

Step 2. Determine net cash flow from operating activities.

Step 3. Determine net cash flows from investing and

financing activities.

Indirect method

calculates cash flow from operations by adjusting net income for noncash revenues and expenses.

Direct method

of presentation calculates cash flow from operations by subtracting cash disbursements to supplies, employees, and others from cash receipts from customers.

Most firms present their cash flows using the indirect method.

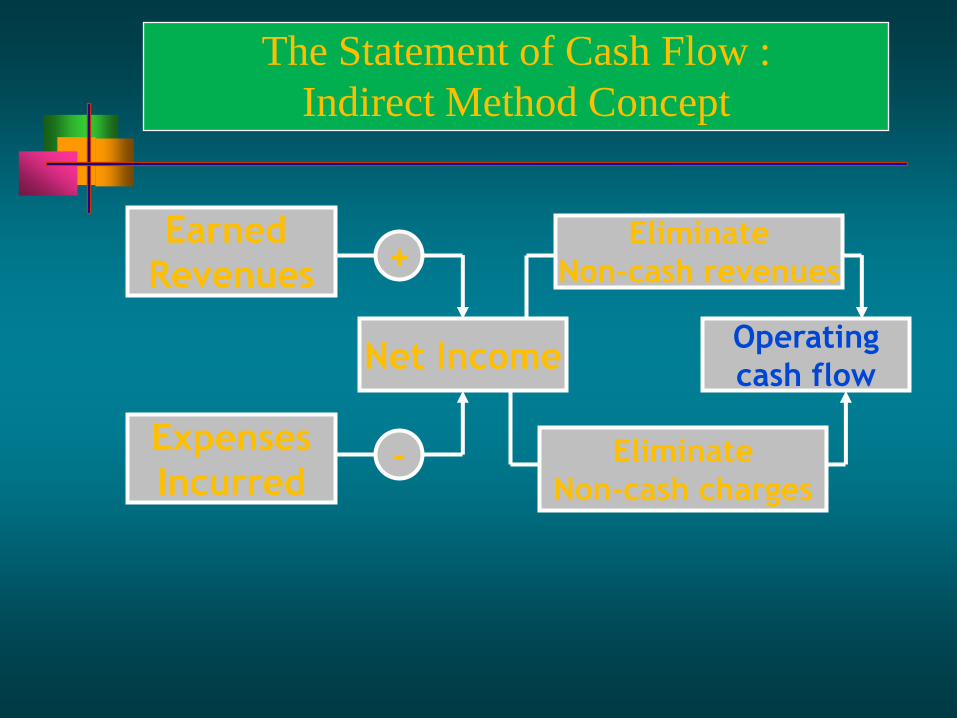

The Statement of Cash Flow :

Indirect & Direct Method Concepts

The Statement of Cash Flow :

Indirect Method Concepts

In Favor of the Indirect Method :

Focuses on the differences between net income and net

cash flow from operating activities.

Provides link between the statement of cash flows and the

income statement and balance sheet.

Special Rules Applying to Indirect Methods :

Disclose Interest paid.

Disclose Income taxes paid.

Earned

Revenues

Expenses

Incurred

Net Income

+

-

Operating

cash flow

Eliminate

Non-cash revenues

Eliminate

Non-cash charges

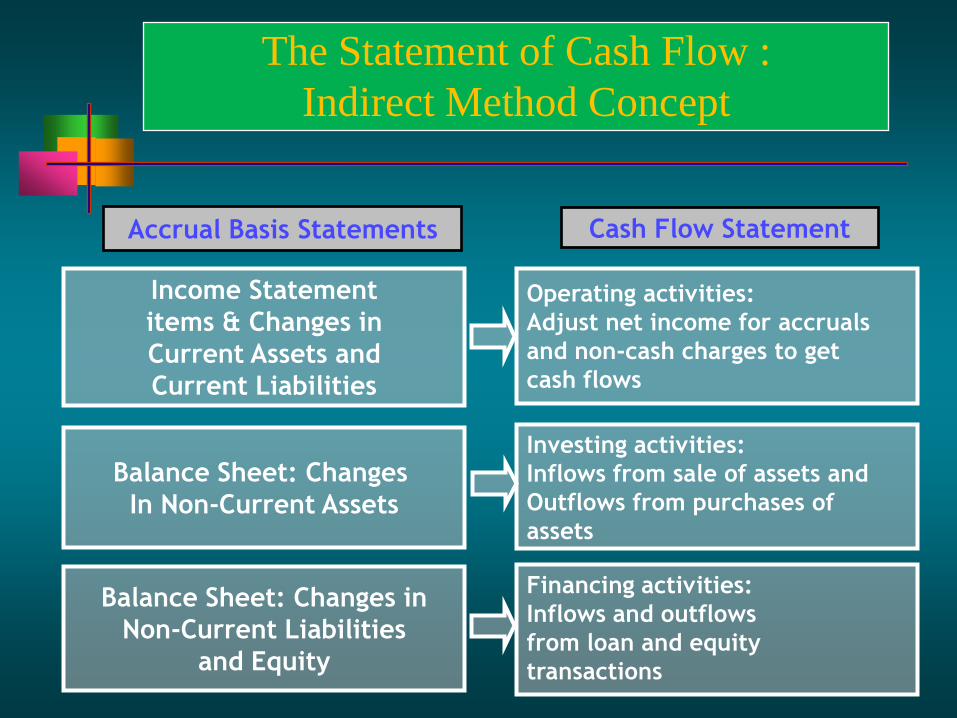

The Statement of Cash Flow :

Indirect Method Concept

Accrual Basis Statements Cash Flow Statement

Income Statement

items & Changes in

Current Assets and

Current Liabilities

Operating activities:

Adjust net income for accruals

and non-cash charges to get

cash flows

Balance Sheet: Changes

In Non-Current Assets

Investing activities:

Inflows from sale of assets and

Outflows from purchases of

assets

Balance Sheet: Changes in

Non-Current Liabilities

and Equity

Financing activities:

Inflows and outflows

from loan and equity

transactions

The Statement of Cash Flow :

Indirect Method Concept

Positive Items

Net incomeDepreciation/amortizationLoss on sale of long-term assetsDecreases in current assets other than cashIncreases in current liabilities

Negative Items

Net lossGain on sale of long-term assetsIncreases in current assets other than cashDecreases in current liabilities

The Statement of Cash Flow : Indirect

Method Concepts – Operating Activities

Positive Items

Sale of plant assetsSale of investments that are not cash equivalentsCollections of loans receivable

Negative Items

Acquisition of plant assetsPurchase of investments that are not cash

equivalentsMaking loans to others

The Statement of Cash Flow : Indirect

Method Concepts – Investing Activities

Positive Items

Issuing stockSelling treasury stockBorrowing money

Negative Items

Payment of dividendsPurchase of treasury stockPayment of principal amounts of debts

The Statement of Cash Flow : Indirect

Method Concepts – Financing Activities

The Statement of Cash Flow :

Direct Method Concepts

In Favor of the Direct Method :

Shows operating cash receipts and payments.

Information about cash receipts and payments is more

revealing of a company’s ability :

1. to generate sufficient cash from operating activities to pay its

debts,

2. to reinvest in its operations, and

3. to make distributions to its owners.

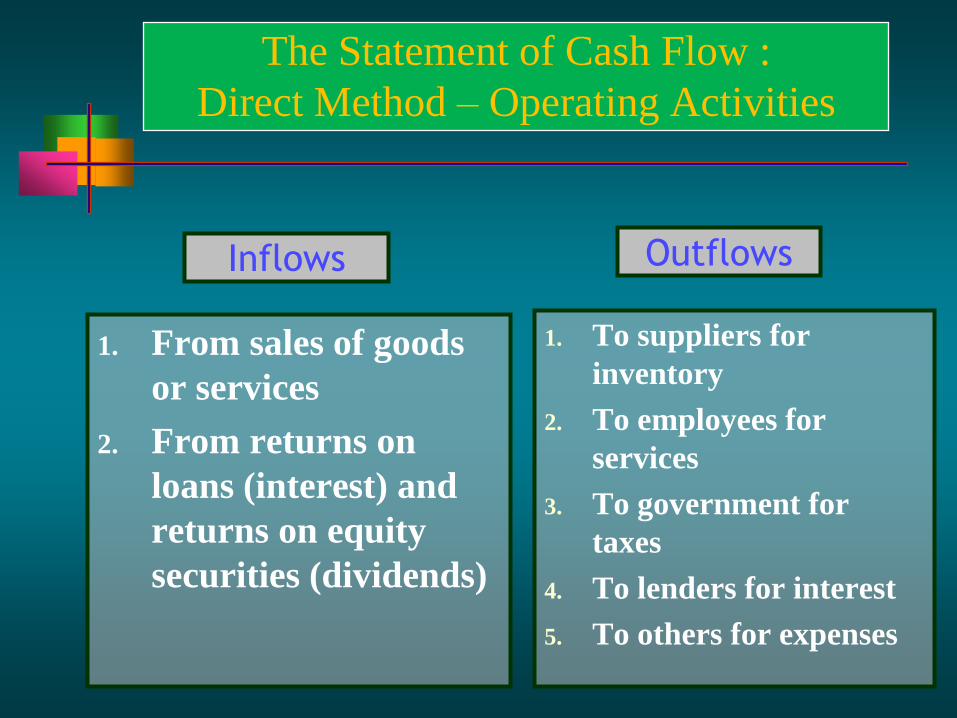

1. From sales of goods

or services

2. From returns on

loans (interest) and

returns on equity

securities (dividends)

1. To suppliers for

inventory

2. To employees for

services

3. To government for

taxes

4. To lenders for interest

5. To others for expenses

Inflows Outflows

The Statement of Cash Flow :

Direct Method – Operating Activities

1. For the direct and indirect methods the sections reporting investing andfinancing activities are the same.

2. The net inflows or outflows for each section (under the two methods) are identical.

3. The operating activities are reported differently.

The Statement of Cash Flow : Direct Method

– Investing & Financing Activities

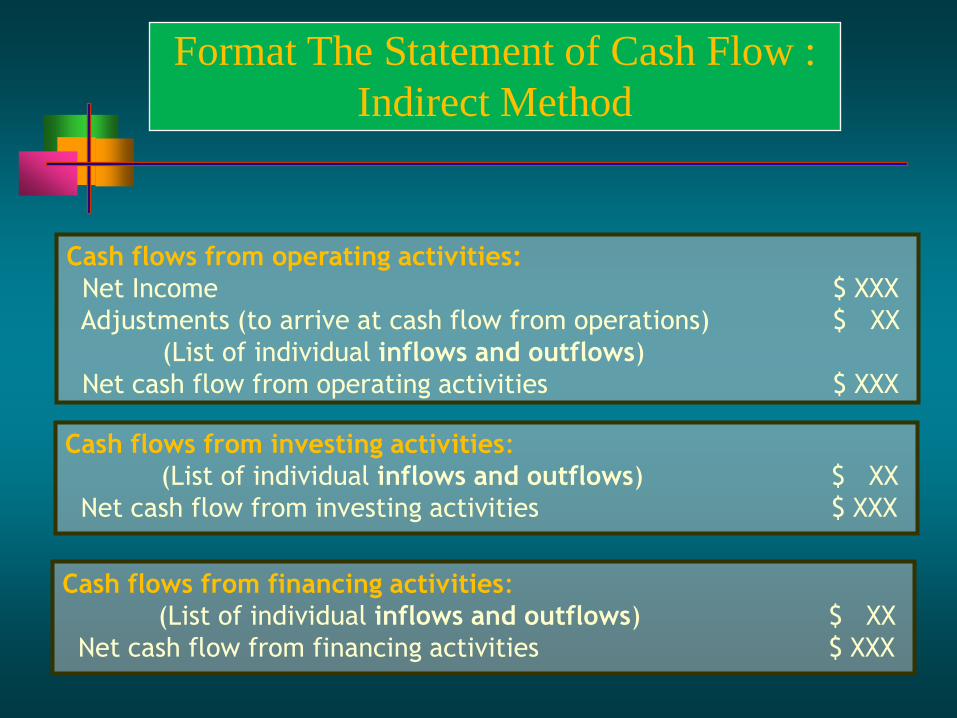

Cash flows from operating activities:

Net Income $ XXX

Adjustments (to arrive at cash flow from operations) $ XX

(List of individual inflows and outflows)

Net cash flow from operating activities $ XXX

Cash flows from investing activities:

(List of individual inflows and outflows) $ XX

Net cash flow from investing activities $ XXX

Cash flows from financing activities:

(List of individual inflows and outflows) $ XX

Net cash flow from financing activities $ XXX

Format The Statement of Cash Flow :

Indirect Method

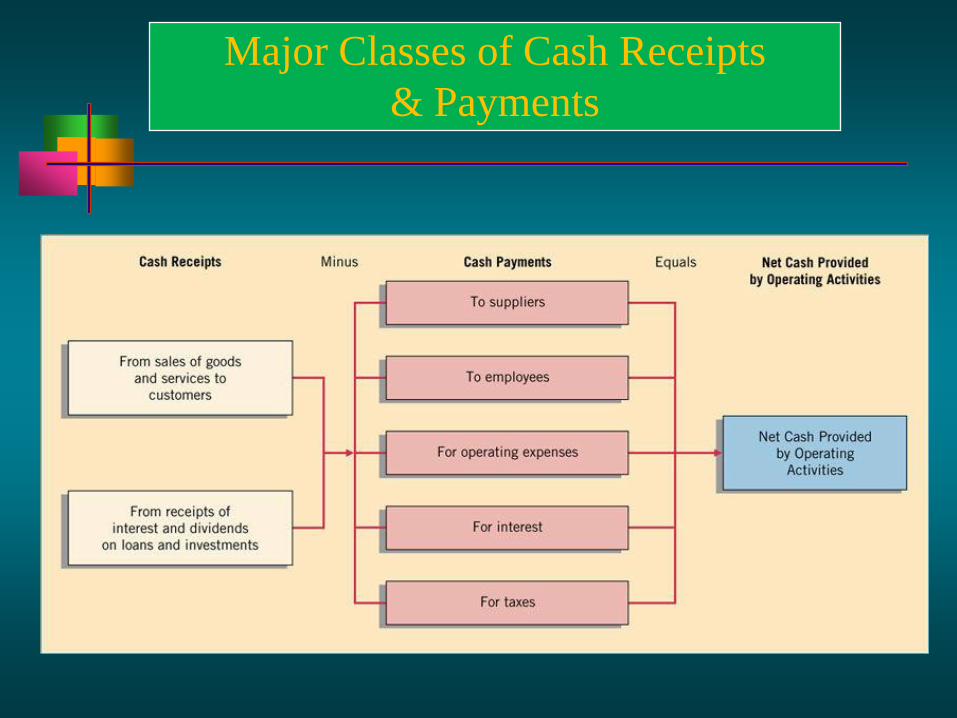

Major Classes of Cash Receipts

& Payments

Formula to Compute Cash Receipts

from Customers

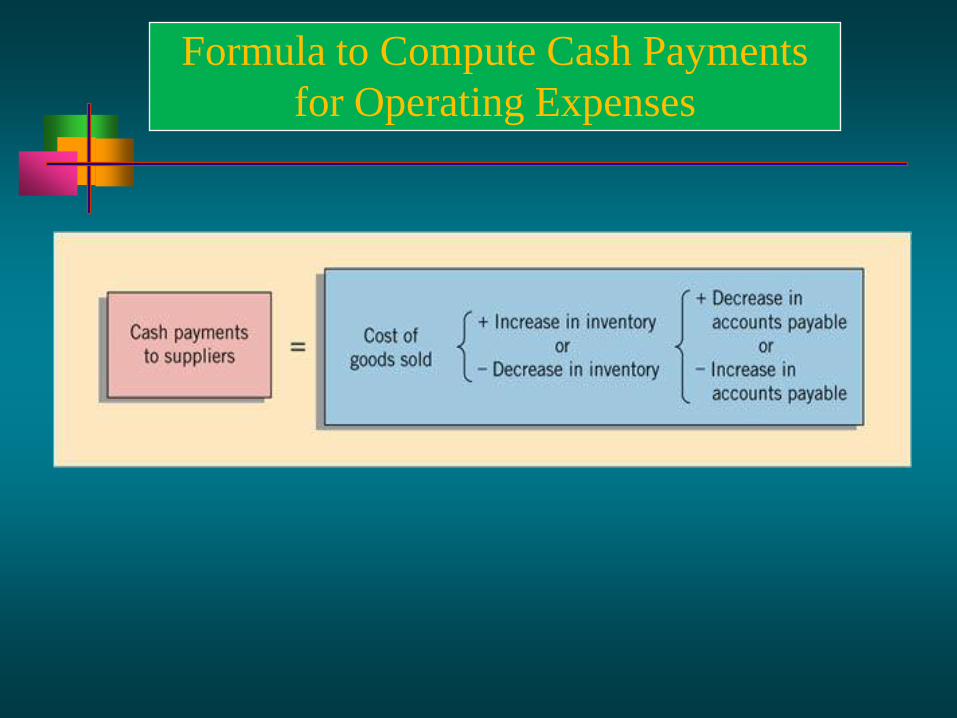

Formula to Compute Cash Payments

for Operating Expenses

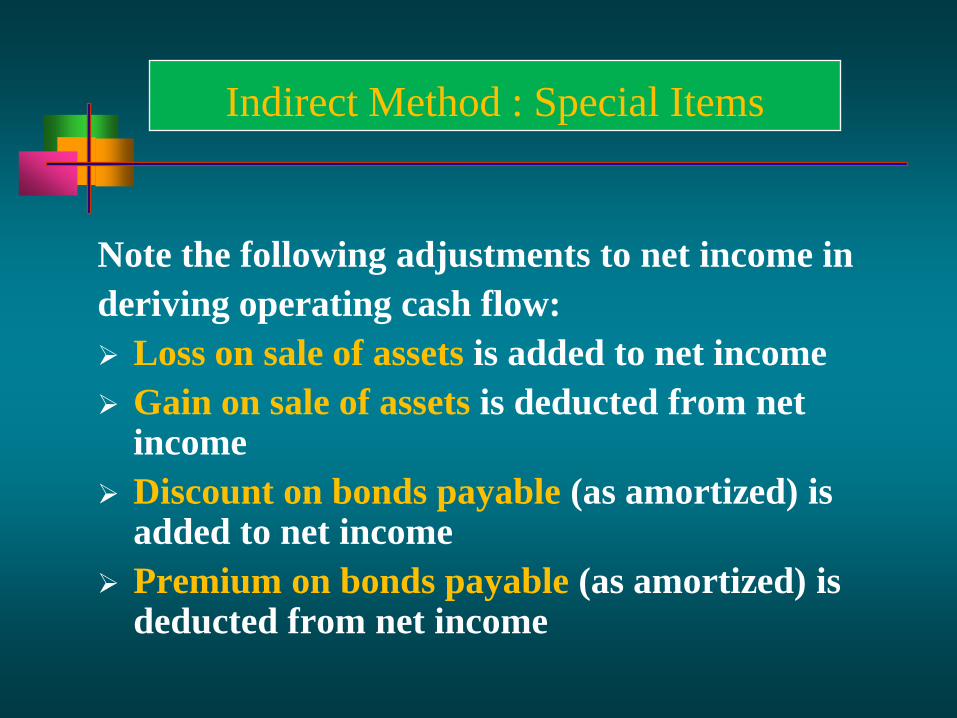

Note the following adjustments to net income in

deriving operating cash flow:

Loss on sale of assets is added to net income

Gain on sale of assets is deducted from net income

Discount on bonds payable (as amortized) is added to net income

Premium on bonds payable (as amortized) is deducted from net income

Indirect Method : Special Items

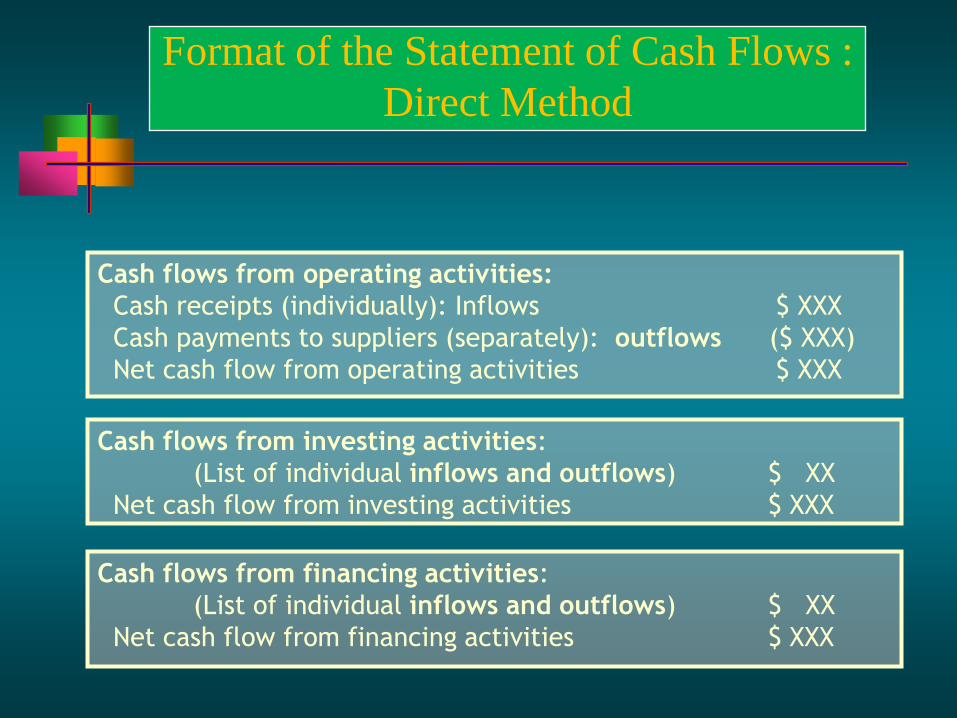

Cash flows from operating activities:

Cash receipts (individually): Inflows $ XXX

Cash payments to suppliers (separately): outflows ($ XXX)

Net cash flow from operating activities $ XXX

Cash flows from investing activities:

(List of individual inflows and outflows) $ XX

Net cash flow from investing activities $ XXX

Cash flows from financing activities:

(List of individual inflows and outflows) $ XX

Net cash flow from financing activities $ XXX

Format of the Statement of Cash Flows :

Direct Method

less equals

Cash Receipts

From sale of

goods and

services to

customers

From receipts

of interest and

dividends

Cash Payments

To suppliers

To employees

For operating exp

For interest

For taxes

Cash

flow

from

operations

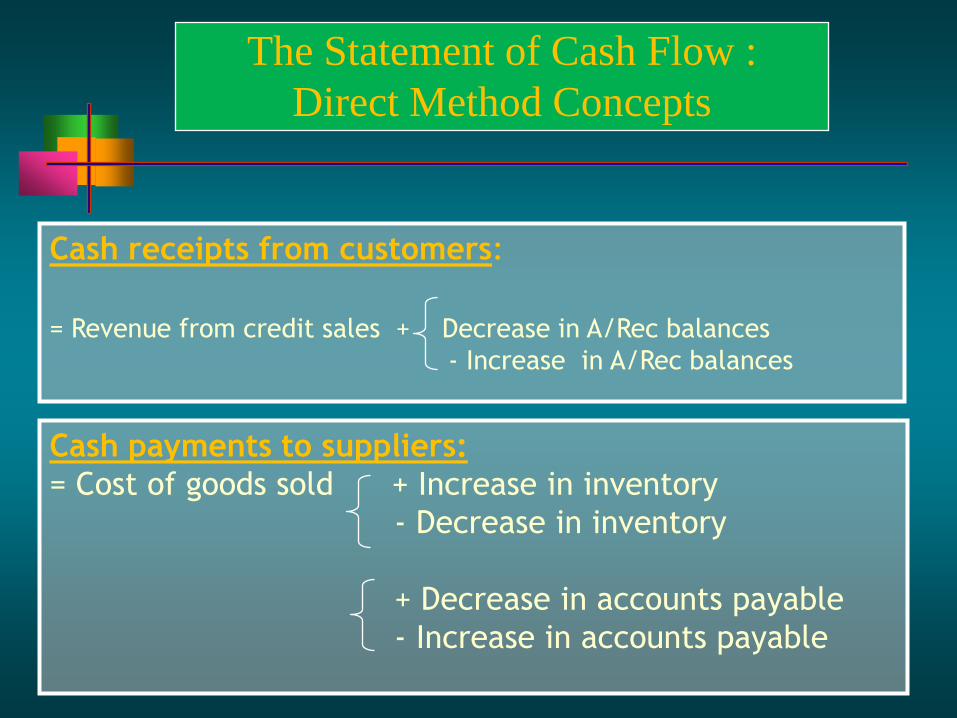

The Statement of Cash Flow :

Direct Method Concepts

Cash receipts from customers:

= Revenue from credit sales + Decrease in A/Rec balances

- Increase in A/Rec balances

Cash payments to suppliers:

= Cost of goods sold + Increase in inventory

- Decrease in inventory

+ Decrease in accounts payable

- Increase in accounts payable

The Statement of Cash Flow :

Direct Method Concepts

Algebraic Formulation

Recall the basic accounting equation:

Assets = Liabilities + Shareholders’ Equity

or A = L + SE

Assets are either cash (C) or not cash assets (NCA), so

C + NCA = L + SE

C + NCA = L + SE

Where means the change in the balance,

Rearranging gives the basic equation for the statement of cash flows:

C = L + SE - NCA

Algebraic Formulation

C = L + SE - NCA

The change in cash, C, is the increase or

decrease in the cash account.

This amount must equal changes in liabilities

plus changes in shareholders’ equity minus

changes in assets other than cash.

Thus, we can identify the causes in the change

in the cash account by studying the changes in

non-cash accounts.

Two Approaches to Producing the

Cash Flow Statement

The basic formula can be implementedusing either of two approaches:

1. Columnar worksheet - changes in balance sheet accounts are classified by definition using a multicolumn worksheet.

2. T-Account worksheet - changes are classified by analysis of the t-accounts.

The Cash Flow Statement :

Columnar Worksheet

Works well for relatively simple situations involving few transactions.

Enhances understanding of the cash flow statement.

Does not work as well as the T-account method when the number and complexity of transactions increases.

The Cash Flow Statement :

Columnar Worksheet

Begin with a comparative balance sheet :

1. Compute the change in each balance sheet account.

2. Classify each change as operating, investing or financing activity.

3. Make any needed adjustments (for example, for a sale of a long-lived asset).

4. Recast the classified changes in the form of a cash flow statement.

The Cash Flow Statement :

Columnar Worksheet

Non Cash Expense :

Noncash expenses, such as depreciation

expense, are added back.

Not truly sources of cash, even though they are

associated with cash inflows; rather, a reversal

of the accrual process that required the

expenses to be recognized without regard for

the cash flow.

If noncash assets

are increased,

then cash was spent,

so cash is an outflow,

so negative sign.

If noncash assets

are decreased,

then they provided cash

so cash is an inflow,

so positive sign.

If liab. or S.E.

increased, then cash

was obtained,

so cash in an inflow,

so positive sign.

If liab. or S.E.

decreased, then cash

was spent,

so cash in an outflow,

so negative sign.

Non-cash Assets

Liabilitiesand Shareholders’Equity

increase decrease

The Cash Flow Statement : Columnar Worksheet -

Changes in Specific Accounts

The Cash Flow Statement :

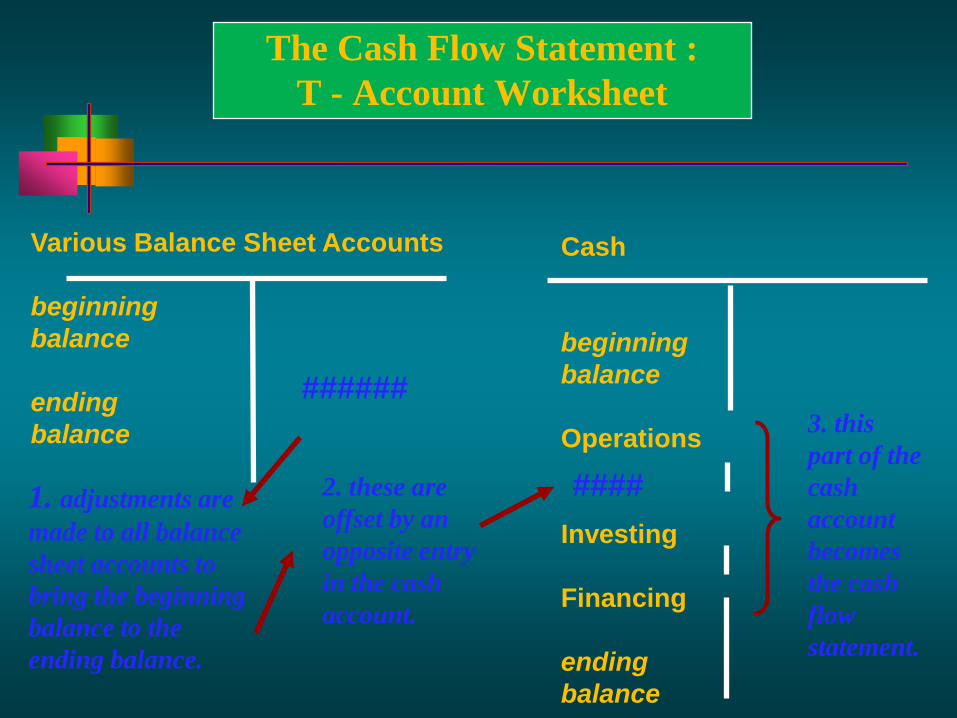

T - Account Worksheet

The columnar works well when the change in each

balance sheet account affects only one of the three

types of activities. It becomes cumbersome for more

complex (and realistic) situations.

The T-account approach is a direct extension of T-

accounts - facilitates analysis of a transaction which

involves more than one activity.

For example, the change in Retained Earnings can be

due to both net income (operating activity) and

dividends (financing activity).

The Cash Flow Statement :

T - Account Worksheet

1. Obtain beginning and ending balance sheets.

2. Prepare a T-account worksheet with a master account,

cash, divided into operating, investing and financing

sections.

3. Explain the change in the master cash account by

reconstructing the original entries in a summary form.

4. Make any necessary adjustments.

5. Recast the master account in the format of a cash flow

statement.

Cash

beginning

balance

Operations

Investing

Financing

ending

balance

Various Balance Sheet Accounts

beginning

balance

ending

balance

######

####1. adjustments are

made to all balance

sheet accounts to

bring the beginning

balance to the

ending balance.

2. these are

offset by an

opposite entry

in the cash

account.

3. this

part of the

cash

account

becomes

the cash

flow

statement.

The Cash Flow Statement :

T - Account Worksheet

Effects of a Sale of a Long-Term

Assets on Cash Flows

A few transactions complicate the derivation of a cash flow statement from a comparative balance sheet, for example, the sale of a long-term (or fixed) asset.

Recall the journal entry for the sale of an asset:

1. Each of the four parts of the above journal entry require an

adjustment in the cash flow statement.

2. The first line, cash, adds a line to the investing section.

3. The second line, a debit to accumulated depreciation, increases the

depreciation expense above the change in the change in the

accumulated depreciation account.

4. The third line, a credit to the asset, increases the amount of cash

invested in long-lived assets above the change in the fixed asset

accounts.

5. The fourth line, a gain or loss, is reversed out in the operating sections

since this is not a cash flow.

Comparison of Cash Flow

to Net Income

Net income is an accrual based concept and

purports to show the long-term.

Cash flows attempt to show the short term.

Consider the outlook for both short-term and

long-term and consider that each is either good

or poor.

A strong growing firm shows both good long-

and short-term outlooks.

Comparison of Cash Flow

to Net Income

A failing firm shows both poor long- and short-

term outlooks.

What about a firm with good cash flows (short-

term) but poor net income (long-term)?

What about a firm with poor cash flows (short-

term) but good net income (long-term)?

Perbedaan PSAK 2 (revisi 2009) &

PSAK 2 (1994)

Secara umum perbedaan antara Exposure Draft Pernyataan Standar

Akuntansi keuangan / ED PSAK 2 (revisi 2009): Laporan Arus

Kas dengan PSAK 2 (1994): Laporan Arus Kas :

Perbedaan Exposure Draft Pernyataan Standar

Akuntansi / ED PSAK 2 : Laporan Arus Kas (revisi

2009) & PSAK 2 : Laporan Arus Kas (1994)

NO PERIHAL PSAK 2 (1994) ED PSAK 2 (REVISI 2009)

1 Arus kas yang berasal

dari beberapa

Transaksi serta keuntungan

atau kerugian dari transaksi

tersebut.

Tidak diatur secara

eksplisit.

- Arus kas dari beberapa transaksi, misalnya

penjualan peralatan pabrik diakui sebagai arus

kas investasi.

- Arus kas dari keuntungan atau kerugian dari

transaksi di atas diakui sebagai arus kas operasi.

2 Metode tidak

langsung

Penyesuaian atas laba atau

rugi termasuk berasal dari

hak minoritas dalam

laba/rugi konsolidasi.

Dihilangkan.

3 Arus kas dari

pos luar biasa.

Terdapat pengaturan

mengenai arus kas dari pos

luar biasa.

Dihilangkan

4 Arus kas dari pelepasan

Kepemilikan pada entitas

anak yang tidak

mengakibatkan hilangnya

pengendalian

Tidak ada

pengaturan.

Arus kas dari transaksi tersebut diakui sebagai

arus kas pendanaan.

The Cash Flow Statement :

International Perspective

The International Accounting Standards

Board (IAS No. 7) recommends but does not

require a statement of cash flows.

An approximation to a cash flow statement can

be prepared from a comparative balance sheet

with some additional information.

Identify the Major Classifications of

Cash Flow Statement

Typical Company Product Life Cycle (PLC)

Source : Kieso, Weygandt & Warfield, Intermediate Accounting, John Wiley & Sons, Inc, 13Ed, 2010.

REFERENCES

1. American Institute of Certified Public Accountants (AICPA),

http://www.aicpa.org

2. Financial Accounting Standard Board (FASB), http://www.fasb.org

3. Indonesian Institute of Accountants, Dewan Standard AkuntansiKeuangan (DSAK), Exposure Draft (ED) Pernyataan Standar Akuntansi Keuangan / PSAK 2 (revisi 2009): Laporan Arus Kas , http://www.iaiglobal.or.id

4. International Accounting Standard Board (IASB), International Accounting Standard (IAS) # 7, Statement of Cash Flows, 2009.

5. International Financial Reporting Standard (IFRS), http://www.ifrs.org

6. Kieso, Donald E., Jerry J. Weygandt & Terry D. Warfield, Intermediate Accounting, John Wiley & Sons, Inc, 13th Ed, 2010.

7. Warren, Carl S., James M. Reeve & Philip E. Fess, Accounting, South-Western College Publishing, 21th Ed, 2004.