modelling mining and oil projects & fiscal regimes -...

TRANSCRIPT

© Alistair Watson & OpenOil CC BY-SA 4.0

PLACEMENT TEST

PRESENTATION (ADAPTED)

Alistair Watson: [email protected] +44(0)787 965 7669

Modelling Mining and Oil Projects & Fiscal Regimes

© Alistair Watson & OpenOil CC BY-SA 4.0

GOOGLE HANGOUT NOVEMBER 2015

Alistair Watson: [email protected] +44(0)787 965 7669

Modelling Mining and Oil Projects & Fiscal Regimes

SERIES 1 SESSION 1

© Alistair Watson & OpenOil CC BY-SA 4.0

Agenda1. Economic rent: why mining and oil are special

2. What drives commodity prices & why they are volatile

3. Mining• Mining project lifecycle

• Mineral valuation

• Cost categories for modelling

• Case study 1: Building an industry cost-curve

• Case study 2: Building a single-period mining model

• Mining fiscal regimes

• Case study 3: Adding a fiscal regime to the single-period model

• Investor decision making: NPV and IRR

• Case study 4: Building an annualized model

• Case study 5: building in the fiscal regime

• Case study 6: Evaluating results

4. Oil & Gas• Life cycle of an oil project

• Oil (and other hydrocarbons) valuation

• Oil project cost categories

• Case study 1: Building a single-period model

• Oil & Gas fiscal regimes

• Case study 2: Adding a production sharing regime to the single-period model

• Case study 3: building an annualized model

• Case study 4: Implementing the production sharing fiscal regime

• Case study 5: Evaluating results

• Case study 6: Expected Net Present Value

Week 1

Week 2

3

© Alistair Watson & OpenOil CC BY-SA 4.0

Agenda (continued)5. Modelling best practices

6. Where to from here?◦ Building fully fledged models

◦ Resources available on-line• Example models (FARI etc.)

• Online Excel training

• AUSIMM and other modelling standards

◦ Process for evaluating projects in your country

4

© Alistair Watson & OpenOil CC BY-SA 4.0

Industry Characteristics

5

© Alistair Watson & OpenOil CC BY-SA 4.0

• Projects exploit a finite resource

• Long, costly exploration periods

• Significant geological, technical, political, environmental risks

• Large up-front investments

• Sophisticated management and specialized technology

• Prices (mostly) set on international markets; price volatility

• High costs of abandonment

• Significant environmental impact & risks

• High community impact

Common to mining and oil & gas

6

© Alistair Watson & OpenOil CC BY-SA 4.0

Economic rent

• Deposits vary in size, location & quality. Each therefore has a different production cost

• Investors needs to earn at least the production cost plus an acceptable return on investment

• Prices for most commodities are set on international markets. The price needs to be high enough so that the highest-cost project necessary to meet world demand is made just viable

• But that means lower cost projects will make super profits – this is “Economic Rent”: the surplus return above the minimum return necessary to induce the investment

• Economic Rent could (in theory) be captured by the resource owner - not by the extractor – without deterring the investment

• The trouble is, economic rent is (1) Unknown in advance; (2) Uncertain; and (3) Volatile

• Also, to invest in risky exploration investors need to earn enough profit on successful projects to cover failed exploration

• So, “Economic Rent” is a subtle, somewhat subjective concept, but with profound implications for fiscal regime design

7

© Alistair Watson & OpenOil CC BY-SA 4.0

Feasibility study: Mineral Resources

Development plan: Resources reclassified as Mineral Reserves

Remote sensing; regional

geochemistry; airborne geophysics; seismic surveys

Exploration process

Acquire rights

Initial exploration

Identify targets

Exploration drilling

Appraisal drilling

Feasibility study

Development planning

8

© Alistair Watson & OpenOil CC BY-SA 4.0

Mining project life cycleP

rod

uct

ion

Co

sts

Exploration$5 - 20MM

Operating Cost

Appraisal$20 – 50MM

Reclamation workcommences during production period

Initial Development$50MM – 3.0Bn (?)

Further Development phases

Production Phase 1

Production Phase 2

Production Phase 3

Operating Costs

Time

9

© Alistair Watson & OpenOil CC BY-SA 4.0

(basic) Cost categoriesExploration Searching for deposits

AppraisalDelineating the size and characteristics of a discovered deposit: Evaluating technical and economic viability

Development costs Building the project

Operating costs Producing the mineral: Fixed versus Variable with production

Overheads Fixed costs of managing production

Sustaining capitalReplacing equipment periodically. Treated as capital cost for tax purposes

Rehabilitation and Decommissioning

Costs of clean up during and after production

"Capital” versus “Operating” costs:• Capital costs have a benefit beyond a single year, and therefore usually have to be depreciated for tax purposes. • Operating costs are recurring costs with no lasting benefit, so are expensed immediately for tax

Most economic analysis is done using cashflows where the distinction does not matter, except to calculate tax payments

Capital expenditure often referred to as “Capex”. Operating Expenditure as “Opex”

10

© Alistair Watson & OpenOil CC BY-SA 4.0

GOOGLE HANGOUT NOVEMBER 2015

Alistair Watson: [email protected] +44(0)787 965 7669

Modelling Mining and Oil Projects & Fiscal Regimes

SERIES 1 SESSION 2

© Alistair Watson & OpenOil CC BY-SA 4.0

Recap on last weekKey extractive industry characteristics

Economic Rent concept

Lifecycle of a mining project

Cost categories

12

© Alistair Watson & OpenOil CC BY-SA 4.0

This sessionDrivers of commodity prices

Constructing an industry “cost curve”

Mining model case study: single period model

Mining model case study: adding a simple fiscal regime

13

© Alistair Watson & OpenOil CC BY-SA 4.0

Commodity Prices

14

© Alistair Watson & OpenOil CC BY-SA 4.0

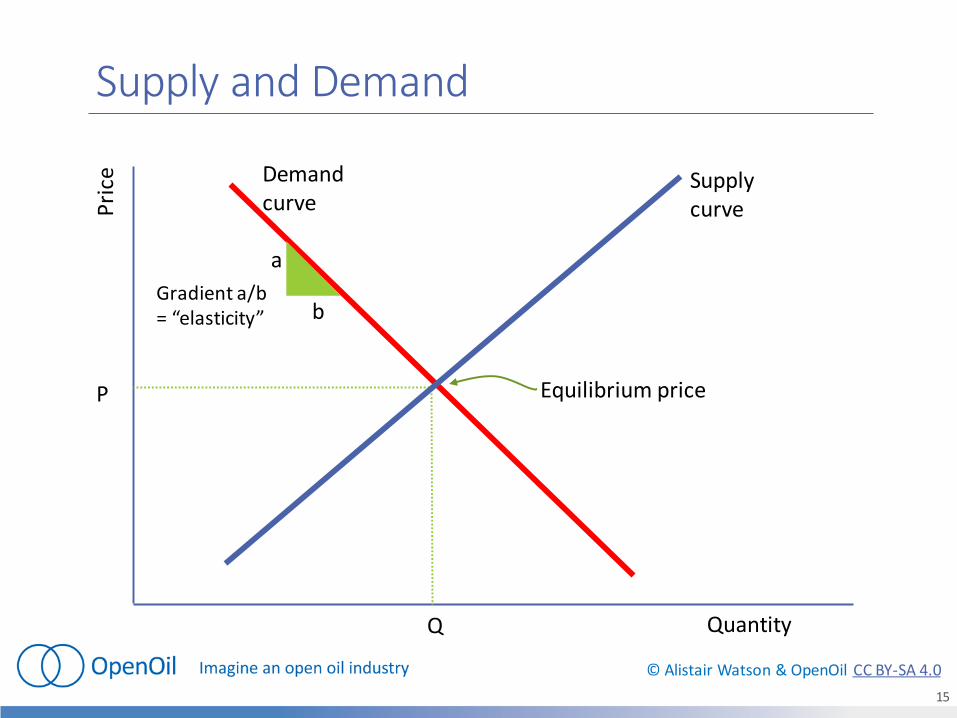

Quantity

Pri

ce

P

Q

Supply curve

Demand curve

Equilibrium price

Gradient a/b = “elasticity”

a

b

Supply and Demand

15

© Alistair Watson & OpenOil CC BY-SA 4.0

What determines the shape of the Supply and Demand curves

Demand Supply

Sho

rt T

erm

• Prices and demand curves for end-use products

• Availability & price of substitutes

• Cost to switch

• Flexibility in mine production e.g. putting mines on care and maintenance in price slump

• Opec (oil)

Lon

g te

rm

• Prices and demand curves for end-use products

• Availability & price of substitutes

• Cost to switch

• Depletion of existing mines• Geology: unexploited resources

and cost to find and extract• Opec Cartel (for oil)• Government policy: e.g.

• Access to resources• Fiscal regimes (cost to extract)• Carbon reduction policies• Nuclear power plant usage• Etc.

16

© Alistair Watson & OpenOil CC BY-SA 4.0

Inelastic demand

Quantity

Pri

ce

P

Q

Supply curve

Inelastic Demand

P1Small decrease in supply, large increase in price

Q1

17

© Alistair Watson & OpenOil CC BY-SA 4.0

Inelastic supply

Quantity

Pri

ce

P

Q1

Inelastic Supply

Demand

P1Small increase in demand, large increase in price

Q

18

© Alistair Watson & OpenOil CC BY-SA 4.0

Does this help explain recent oil prices?

Quantity

Pri

ce

P

P1

Increase in short term supply (US production; growing inventories)

Slowing of demand increase from Asian economies

11

2

2

Massive reduction in price required to clear the market

19

© Alistair Watson & OpenOil CC BY-SA 4.0

The “Lower for Longer” view on oil

Quantity

Pri

ce

P1

Implies prices may not return to recent highs for quite a while…

Supply curve has flattened due to Shale

P2

Demand growth resumes

20

© Alistair Watson & OpenOil CC BY-SA 4.0

Commodity prices are a function of marginal costs

Goldman Sachs paper suggests long dated (futures) prices for oil andcopper are set consistent with marginal costs for highest cost producer

Source: Goldman Sachs Global Economics Paper No: 194 Commodity Prices and Volatility: Old Answers to NewQuestions. http://www.goldmansachs.com/korea/ideas/global-growth/commodity-prices-doc.pdf

21

© Alistair Watson & OpenOil CC BY-SA 4.0

But it's not simple…Marginal cost is volatile, depending on the shape of the supply curve

For oil, policy decisions by Opec (reducing or increasing supply); US and othergovernments

Commodities increasingly used as investments: Particularly Gold, Oil, Copper

Impact of speculators (though much debated…)

… All of which leads to price volatility

0

20

40

60

80

100

120

140

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

US$

Bb

lAxis Title

Brent Crude Oil

Brent history (monthly averages) Futures ICE 24Sept2015

22

© Alistair Watson & OpenOil CC BY-SA 4.0

0

100

200

300

400

500

600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Real terms 2014 Commodity Price Indices (2005 = 100)

Crude oil

Copper

Aluminium

Iron Ore

Nickel

Zinc

Lead

Uranium

Gold

Forecast

Source: IMF WEO Database Oct 2014. 2005 = 100; adjusted using US CPI

Real-terms 2014 Commodity Prices

Steep price increase resulting

from rapid Asian growth & perceived shortages

Declining prices: lack of

investment

Supply response:

investment

Prices

fall

23

© Alistair Watson & OpenOil CC BY-SA 4.0

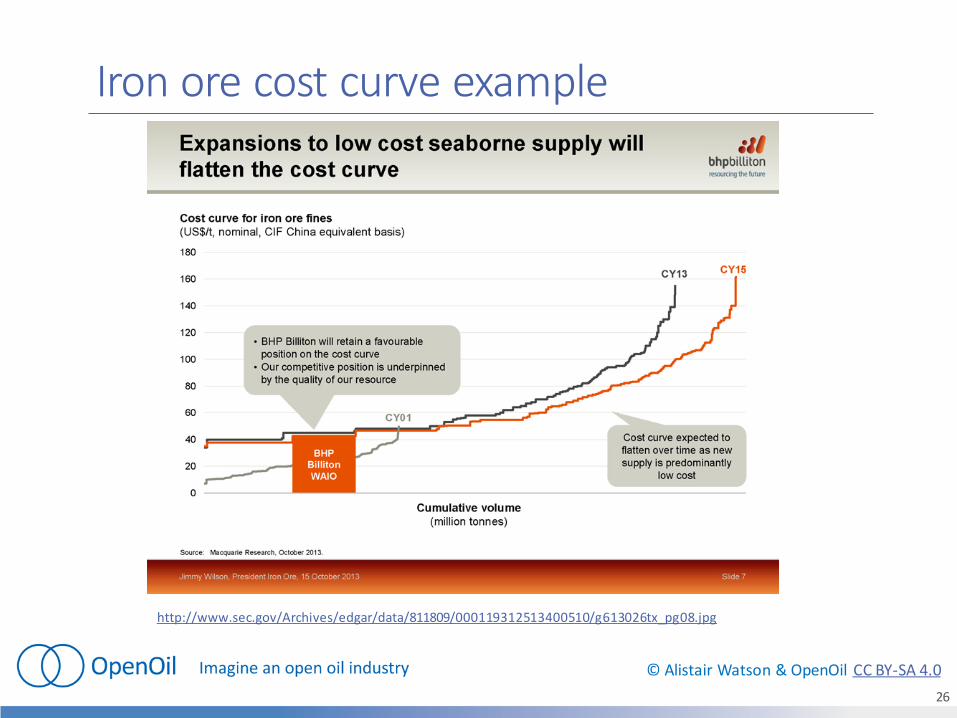

Iron ore cost curve example

http://www.bing.com/images/search?q=iron+ore+cost+curve&id=AE5391761DC3976D4885155D9B61F418A28B03FC&FORM=IQ

FRBA#view=detail&id=AE5391761DC3976D4885155D9B61F418A28B03FC&selectedIndex=0

24

© Alistair Watson & OpenOil CC BY-SA 4.0

Remember this?

25

© Alistair Watson & OpenOil CC BY-SA 4.0

Iron ore cost curve example

http://www.sec.gov/Archives/edgar/data/811809/000119312513400510/g613026tx_pg08.jpg

26

© Alistair Watson & OpenOil CC BY-SA 4.0

Coal example

http://www.iea.org/etp/resourcestoreserves/

27

© Alistair Watson & OpenOil CC BY-SA 4.0

http://www.commodityintelligence.com/7-11Feb11.htm

Copper example

28

© Alistair Watson & OpenOil CC BY-SA 4.0

Copper example

How can costs be negative? Answer: by-products

29

© Alistair Watson & OpenOil CC BY-SA 4.0

Gold example

Note new metric “All-in Sustaining Cost” discussed

later in the course

30

© Alistair Watson & OpenOil CC BY-SA 4.0

Oil

http://www.iea.org/etp/resourcestoreserves/

Price today

31

© Alistair Watson & OpenOil CC BY-SA 4.0

Oil

http://s3.amazonaws.com/zanran_storage/www.sais-jhu.edu/ContentPages/137274942.pdf

32

© Alistair Watson & OpenOil CC BY-SA 4.0

33

Case study 1Constructing an industry cost curve

© Alistair Watson & OpenOil CC BY-SA 4.0

Constructing a cost curveImagine a particular mineral which can be produced by only 10 projects in the world.

◦ For simplicity, let’s assume these projects are all either in production, or capable of immediate startup

The projects have the following production capacity and unit cost. The unit costs include return on investment the projects need to earn

34

Source data

Project Production Unit cost

A 100 4.00

B 125 3.00

C 10 9.00

D 50 8.00

E 20 10.00

F 200 2.00

G 50 5.20

H 100 2.75

I 150 2.50

J 45 7.00

© Alistair Watson & OpenOil CC BY-SA 4.0

35

© Alistair Watson & OpenOil CC BY-SA 4.0

Cost curve cast study (questions)1. If global demand for the mineral is 675 million tonnes, what does the price

need to be to ensure production is sufficient?

2. At this price, what profit margins do projects F, make? What profit (as a % ofrevenue) does project A make?

3. If demand increased to 725 million tonnes, what would that imply for theprice?

4. If demand decreased to 575 million tonnes, what would that imply for theprice?

5. With demand 675 and price $4.00, what are the implications of Project Iexpanding production to 250?

36

© Alistair Watson & OpenOil CC BY-SA 4.0

Of course its not that simple…Projects in production need only to cover current (cash) costs

Undeveloped projects need a price high enough to cover investment plus return

◦ Each therefore has a different concept of “break-even” (We discuss this later in petroleum case study)

Companies will take a short term loss and hope for a price recovery

Stockpiles

Producers use Hedging to lock in a price different from the current spot price, may enable them to ride out a temporary downturn

37

© Alistair Watson & OpenOil CC BY-SA 4.0

38

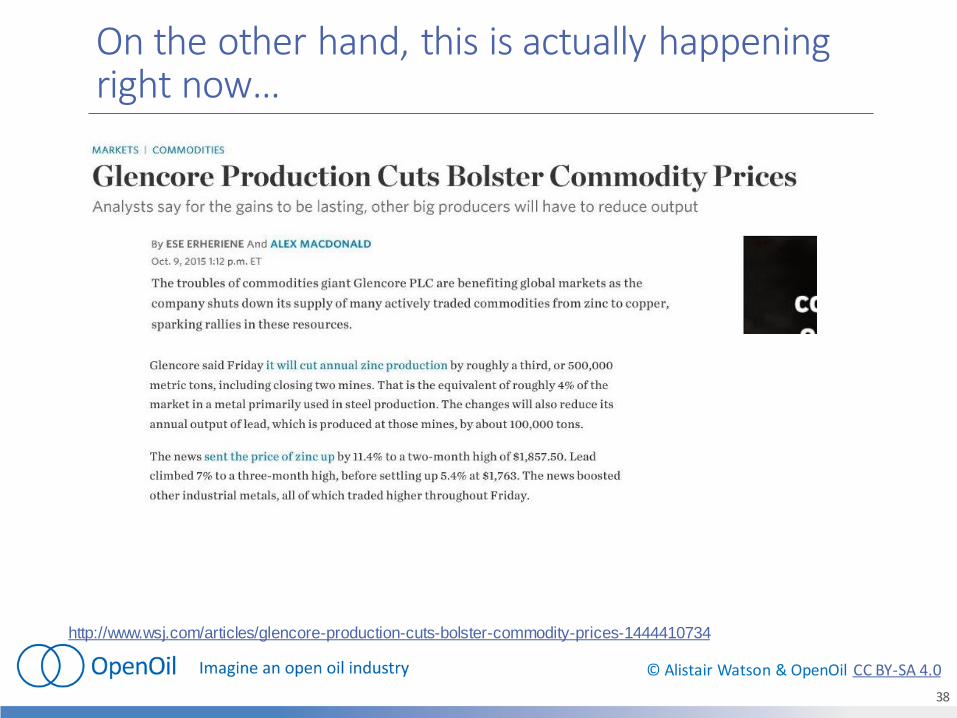

On the other hand, this is actually happening right now…

http://www.wsj.com/articles/glencore-production-cuts-bolster-commodity-prices-1444410734

© Alistair Watson & OpenOil CC BY-SA 4.0

GOOGLE HANGOUT NOVEMBER 2015

Alistair Watson: [email protected] +44(0)787 965 7669

Modelling Mining and Oil Projects & Fiscal Regimes

SERIES 1 SESSION 3

© Alistair Watson & OpenOil CC BY-SA 4.0

RecapFirst two sessions:

Characteristics; economic rent; lifecycle of a mining project; cost categories; industry cost curves

This session:

Mineral valuation for a specific project

Single-period mining model

Mining Fiscal regimes

40

© Alistair Watson & OpenOil CC BY-SA 4.0

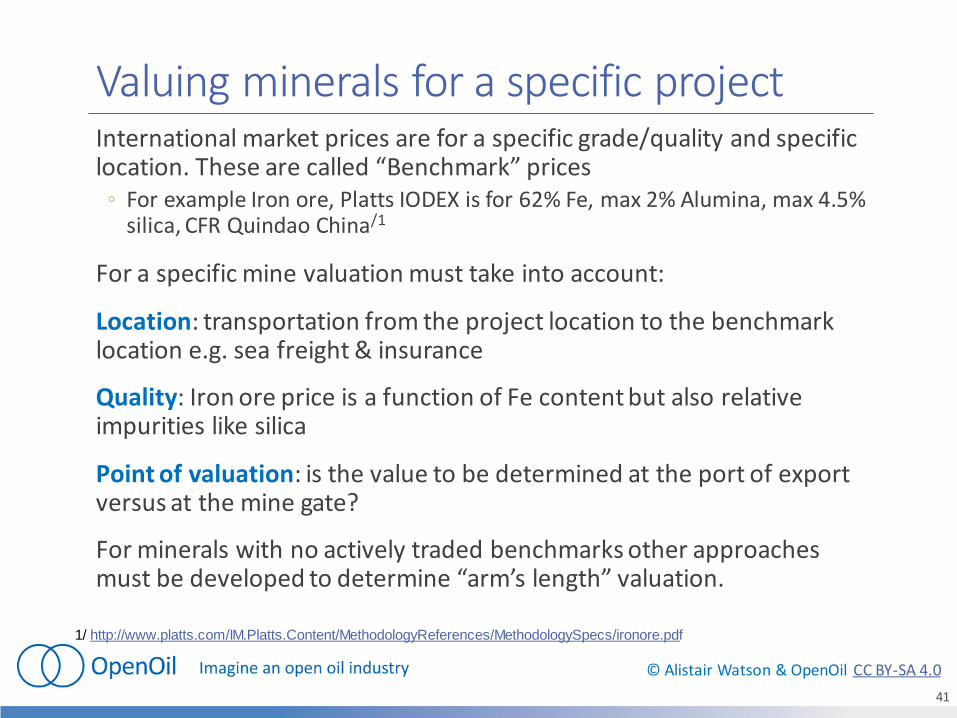

Valuing minerals for a specific project International market prices are for a specific grade/quality and specific location. These are called “Benchmark” prices

◦ For example Iron ore, Platts IODEX is for 62% Fe, max 2% Alumina, max 4.5% silica, CFR Quindao China/1

For a specific mine valuation must take into account:

Location: transportation from the project location to the benchmark location e.g. sea freight & insurance

Quality: Iron ore price is a function of Fe content but also relative impurities like silica

Point of valuation: is the value to be determined at the port of export versus at the mine gate?

For minerals with no actively traded benchmarks other approaches must be developed to determine “arm’s length” valuation.

41

1/ http://www.platts.com/IM.Platts.Content/MethodologyReferences/MethodologySpecs/ironore.pdf

© Alistair Watson & OpenOil CC BY-SA 4.0

Mineral valuation: coal example

PortFinal

Market

Rail

ShipMiningTreat-

ment

Fair Market Value

FOB (Free on Board)

mine

FMV. FOB Port Benchmark price

CFR (Cost and

Freight)

Value of coal in final market Coal price benchmark

- Shipping costs Shipping benchmark

+ Other selling costs (insurance etc.) Arm’s length charges

= Fair Market Vale FOB Port Calculated

- Port handling Arm’s length charges by port

- Rail costsArm’s length charges by rail company or actual costs incurred

= Fair Market Value FOB Mine Calculated

42

© Alistair Watson & OpenOil CC BY-SA 4.0

Building a single-period model

Mining Model Case Study 1

43

© Alistair Watson & OpenOil CC BY-SA 4.0

Project “X”

Stylized mining project

Generic bulk mineral product, measured and sold in Tonnes

Significant transport costs

Similar to a coal or iron ore project

Relatively opex intensive

Mine PortRailway (3rd party)

International Market

44

© Alistair Watson & OpenOil CC BY-SA 4.0

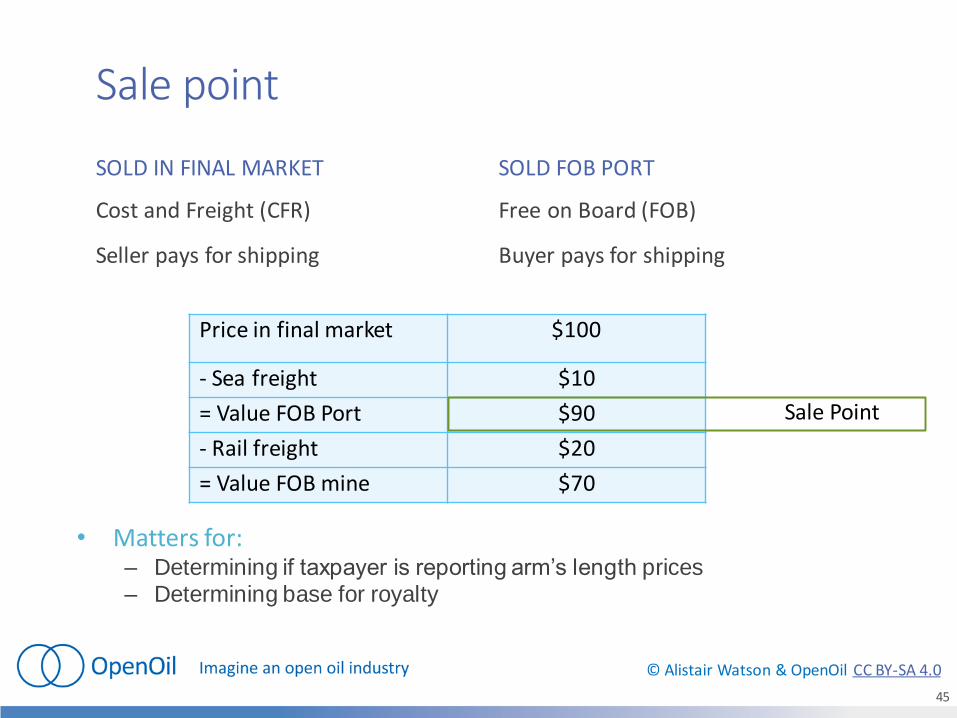

Sale point

SOLD IN FINAL MARKET

Cost and Freight (CFR)

Seller pays for shipping

SOLD FOB PORT

Free on Board (FOB)

Buyer pays for shipping

Price in final market $100

- Sea freight $10

= Value FOB Port $90

- Rail freight $20

= Value FOB mine $70

• Matters for:– Determining if taxpayer is reporting arm’s length prices– Determining base for royalty

Sale Point

45

© Alistair Watson & OpenOil CC BY-SA 4.0

Project assumptions

• Each item here could be broken down further: detailed cost sub-categories etc.

• Choice depends on modelling objective and access to data• Focus in this course is on fiscal regime modelling: even this aggregated level of detail

will give us plenty to analyse

Project Assumptions

Total production M Tonnes 100 11 years

Sales price: CFR $T 100

Sea freight $T 10

Sales price: FOB port $T 90

Capital costs (Capex) Operating costs (Opex)

Exploration costs: cash $M 50 Operating costs $T 30

Exploration costs: sunk $M - Overheads $M per year 5

Development capital $M 750 Rail transport $T 20

Sustaining capital * $M per year 20

* From yr 2 till 3rd year before production stops

Decommissioning costs % DevCapEx 10%

46

© Alistair Watson & OpenOil CC BY-SA 4.0

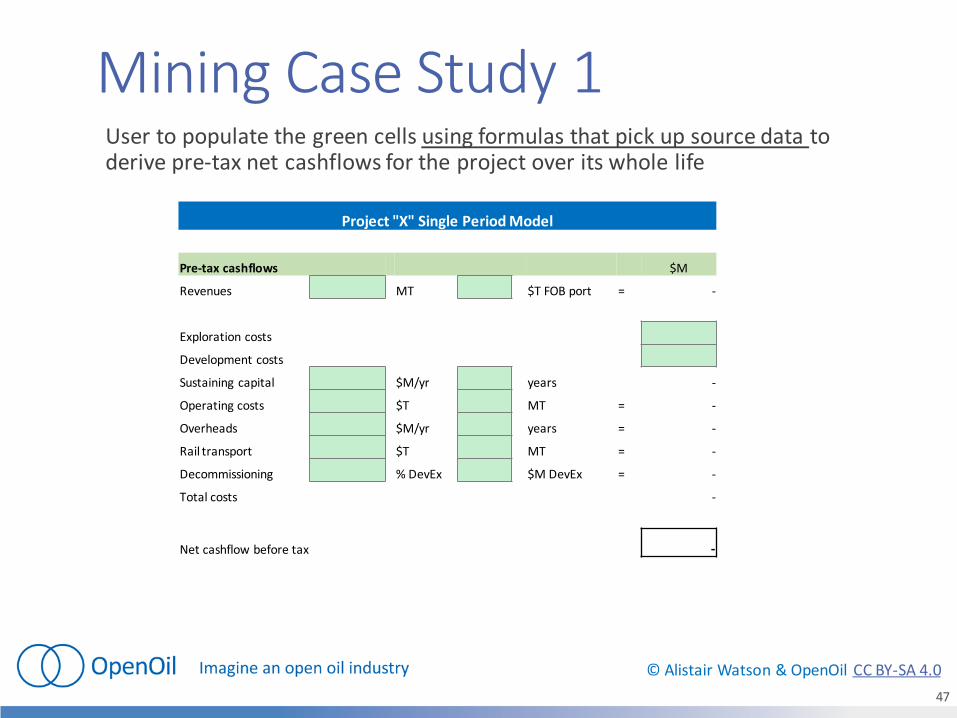

Mining Case Study 1User to populate the green cells using formulas that pick up source data to derive pre-tax net cashflows for the project over its whole life

Project "X" Single Period Model

Pre-tax cashflows $M

Revenues MT $T FOB port = -

Exploration costs

Development costs

Sustaining capital $M/yr years -

Operating costs $T MT = -

Overheads $M/yr years = -

Rail transport $T MT = -

Decommissioning % DevEx $M DevEx = -

Total costs -

Net cashflow before tax -

47

© Alistair Watson & OpenOil CC BY-SA 4.0

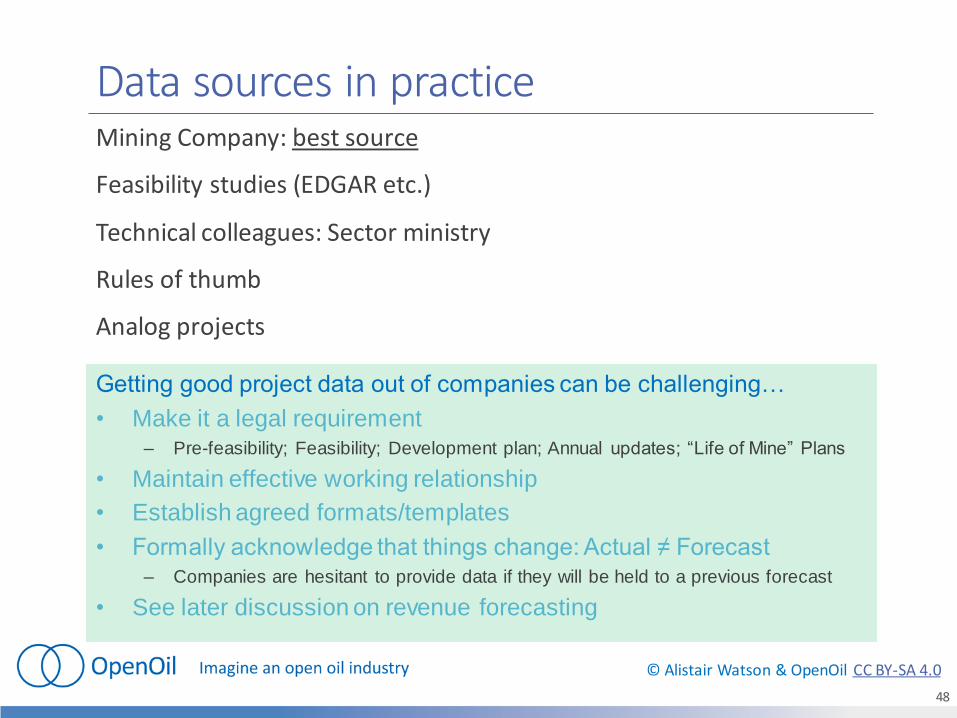

Data sources in practiceMining Company: best source

Feasibility studies (EDGAR etc.)

Technical colleagues: Sector ministry

Rules of thumb

Analog projects

Getting good project data out of companies can be challenging…

• Make it a legal requirement– Pre-feasibility; Feasibility; Development plan; Annual updates; “Life of Mine” Plans

• Maintain effective working relationship

• Establish agreed formats/templates

• Formally acknowledge that things change: Actual ≠ Forecast– Companies are hesitant to provide data if they will be held to a previous forecast

• See later discussion on revenue forecasting

48

© Alistair Watson & OpenOil CC BY-SA 4.0

Is this a good project?It looks pretty good, but…

What else do we need to know:

1. Fiscal regime: how much does the government take?

2. …?

49

© Alistair Watson & OpenOil CC BY-SA 4.0

Mining fiscal regimes

50

© Alistair Watson & OpenOil CC BY-SA 4.0

Government fiscal regime objectives

• Maximize Revenues

• Attract exploration investment

• Ensure discovered projects go ahead (neutrality)

• Incentives to maximize production at minimum cost (efficiency)

• Capture an increasing share from more profitable projects (progressivity)

• Stability

http://www.imf.org/external/np/pp/eng/2012/081512.pdf

IMF paper

51

© Alistair Watson & OpenOil CC BY-SA 4.0

Fiscal mechanisms Royalty A share of the value of production

3-5% pretty common, rates often vary by mineral

Income tax A share of profit, determined under tax rules30% rate pretty common

Resource Rent Tax Special tax designed to capture a share of economic rent. Uncommon but often recommended by the IMF

Import duties % of the value of imports

Value Added Tax % of sales (output VAT) and % of costs (input VAT)Under properly functioning VAT the consumer should bear the cost – not the mining company. But in practice…

State participation Government owned company owns a share in the project

Others Withholding taxes on subcontractorsWithholding taxes on dividends and interest

52

© Alistair Watson & OpenOil CC BY-SA 4.0

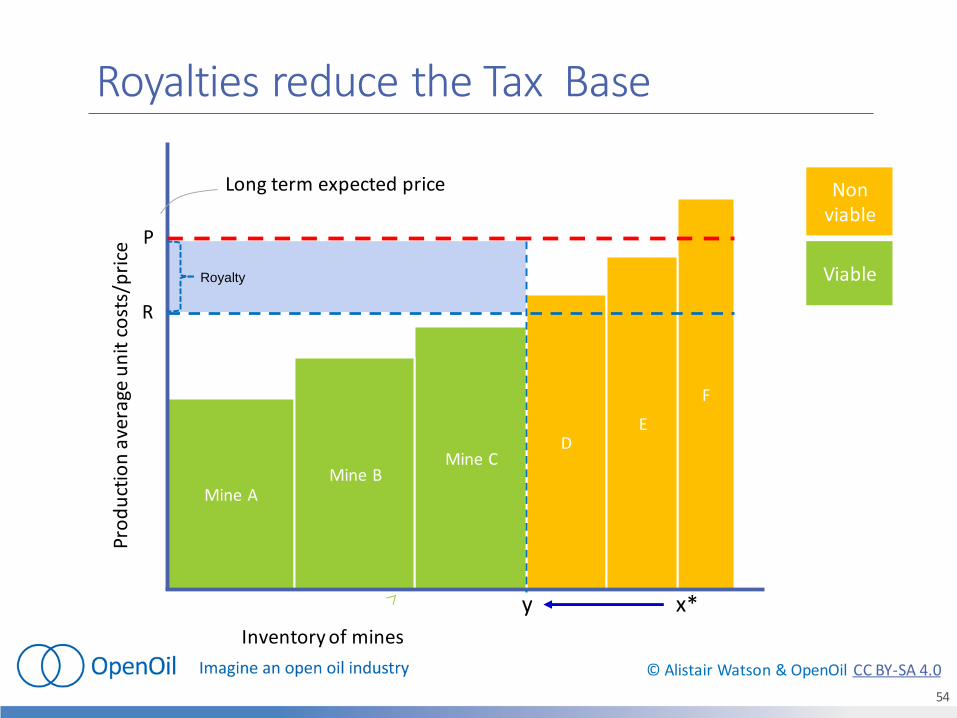

RoyaltiesUsually percent of gross revenue (or unit fee)

Widely applied

Early, dependable income

Distorts production and investment decisions

Limited rent capture

Regressive, not progressive

Internationally accepted at modest levels

Administratively simple?

53

© Alistair Watson & OpenOil CC BY-SA 4.0

F

DE

Mine C

Mine AMine B

Royalties reduce the Tax Base

Inventory of mines

Pro

du

ctio

n a

vera

ge u

nit

co

sts/

pri

ce

P

Non viable

Viable

Long term expected price

R

x*y

54

Royalty

© Alistair Watson & OpenOil CC BY-SA 4.0

Profit based fiscal mechanismsProfit = Revenues minus Costs

Revenues = valuation of minerals sold (or produced?)

Costs = which costs are deductible, and when

For example, with income tax

• Operating costs deductible when incurred

• Capital costs deductible over time via depreciation

So, depreciation rules matter

• Faster depreciation = income tax paid later

• Slower depreciation = income tax paid sooner

55

© Alistair Watson & OpenOil CC BY-SA 4.0

Further detail on mechanismsIncome taxes: need for special rules

◦ Mineral valuation

◦ Ring fencing

◦ Depreciation

◦ Loss carry forward

◦ Decommissioning

Resource Rent Taxes◦ Additional tax that applies only to profits (or cashflows) earned in excess of a

threshold rate of return

◦ Increasingly common in Mining

◦ Parameters needed:◦ Threshold rate of return

◦ Resource Rent Tax Rate

56

© Alistair Watson & OpenOil CC BY-SA 4.0

“Fiscal Regime”

A “Fiscal Regime” is the combination of all of the mechanisms thatdetermine how project benefits are shared between government(resource owner) and the mining company (the extractor)

General IMF advice for developing economies: fiscal regimes shouldinclude:

1. Modest Royalty: guarantee some revenue

2. Income tax with mining specific rules

3. A progressive mechanism; such as

◦ Resource Rent Tax; or

◦ Variable Income tax

57

© Alistair Watson & OpenOil CC BY-SA 4.0

Generic Mining Fiscal regime

Recettes totales

RedevanceCoûtsBénéfices

Taxe de Rente Eco (éventuelle)

Revenu imposable

Impôt sur le revenu

Bénéfice après impôt

Recettes totales

Bénéfices Coûts RedevanceCoûts

Recettes totales

RedevanceCoûtsBénéfices

Recettes totales

RedevanceCoûts

Taxe de Rente Eco (éventuelle)

Bénéfices

Recettes totales

RedevanceCoûts

Revenu imposableTaxe de Rente Eco (éventuelle)

Bénéfices

Recettes totales

RedevanceCoûts

Bénéfice après impôt

Revenu imposableTaxe de Rente Eco (éventuelle)

Bénéfices

Recettes totales

RedevanceCoûts

Impôt sur le revenu

Bénéfice après impôt

Revenu imposableTaxe de Rente Eco (éventuelle)

Bénéfices

Recettes totales

RedevanceCoûtsBénéfices

Recettes totales

CoûtsBénéfices

Recettes totales

RedevanceCoûtsBénéfices

Recettes totales

Taxe de Rente Eco (éventuelle)

RedevanceCoûtsBénéfices

Recettes totales

Revenu imposableTaxe de Rente Eco (éventuelle)

RedevanceCoûtsBénéfices

Recettes totales

Bénéfice après impôt

Revenu imposableTaxe de Rente Eco (éventuelle)

RedevanceCoûtsBénéfices

Recettes totales

Income tax

Profit after tax

Taxable incomeResource RentTax (if any) /1

RoyaltyCostsProfit

Total revenues

58

1/ Assuming the RRT is deductible

© Alistair Watson & OpenOil CC BY-SA 4.0

BUILDING IN THE FISCAL REGIME

Case Study 2

59

© Alistair Watson & OpenOil CC BY-SA 4.0

Case study 2: building fiscal regime into single period model

Add simple fiscal regime to single period model:

◦ 5% Royalty

◦ 30% Income tax

60

© Alistair Watson & OpenOil CC BY-SA 4.0

Is This a Good Project?After government fiscal share it still looks pretty good, but…

How do we know how much net cashflow is enough?

◦ Just $1? $100; $1million; $50 million?

Simple net cashflow is not enough information

Consider 2 projects identical except one produces 100MT over 5 years and another over 10 years. They have the same net cash flow after tax. Would a mining company be indifferent between these?

No, they would prefer earning that net cashflow in 5 rather than 10 years.

We need a way of taking into account Timing and Risk

This is done through Net Present Value calculations

61

© Alistair Watson & OpenOil CC BY-SA 4.0

Next sessionNPV and IRR

Annualized model

62