mock test paper 1 solution mock test paper 2 · mock test paper – 1 solution may, 2018 ca final...

TRANSCRIPT

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

1

Mock Test Paper – 2 (Solutions)

Compute the taxable income of Mr. Singh for the P.Y. 2017-18. Following are the details of income provided by Mr Singh, for the financial year ended 31st March 2018. (i) Rental income from property at Bangalore – Rs. 2,00,000/- / Standard rent – Rs. 1,50,000 Lakhs /

Fair rent Rs. 1,80,000. (ii) Municipal & Water tax paid during PY 2017-2018 for Current year – Rs. 35,000, previous year

Arrears – Rs. 1,50,000. (iii) Interest on Loan borrowed for major repairs to the property – Rs. 6,00,000. (iv) Unrealized rent of Rs. 5,00,000 received during the year which was not charged to tax in earlier

year.

Mr. Singh, engaged in Rubber Trading business with Turnover amounting Rs. 1.50 crore, has opted for business income to be computed u/s 44AD.

Mr Singh sold a house property in Chennai, the details are as under:

(i) Mr Singh’s father acquired a residential house in April, 1992 for Rs. 25,000 and thereafter gifted property to Mr Singh on 01-03-1993.

(ii) The property so gifted was sold by him on 10-06-2017 for consideration amounting Rs. 25,00,000 (iii) Stamp duty charges paid by the purchaser at the time of registration @ 13% was Rs. 3,90,000. The

stamp duty value as on the date of agreement was Rs. 35,00,000. (iv) On 02-01-2018, the assesse had purchased 2 adjacent flats in the same building and made suitable

modifications to make it as 1 unit. The investment was made by separate sale deeds, of Rs. 18,00,000 & Rs. 17,00,000 respectively. rM btpi ayt pma s hT. hmniM of sb . 4,05, 555 at 21 % f tM btpi ayt apsy f symsamni.

On 15-03-2018, Rs. 15 lakhs was invested in bonds issued by NHAI, but allotment was made on 3-04-2018. Mr. Singh being one of the investors of Securitisation Trust received Rs. 5 lakh during the previous year 2017-18.The Securitisation Trust had the following incomes in previous year 2017-18: Interest Income : Rs. 5 lakhs Dividend Income : Rs. 7 Lakhs STCG: Rs. 15 lakhs Mr Singh received dividend from investment in various companies during financial year 2017-18 to the tune of Rs. 11.5 lakhs.

Compute the taxability for A.Y – 2018-19. ( CII : F.Y - 2017-18 : 272, F.Y – 2012-13 : 200, F.Y – 1992-93 : 100 ). hT. hmniM Mpb pma h.A. rpx n 35/56/1528. N paapnc tpx wpb pma s Mmi.

Solution:

Computation of Total Income

For the A.Y. 2018-19

Particulars Amount Amount

Income from House Property:

Qu

es

tio

n :

1

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

2

Expected Rent (Lower of Standard Rent and Fair rent): Rs. 1,50,000 Actual Rent: Rs. 2,00,000

∴ GAV [Actual Rent or Expected Rent, whichever is higher] (-) Municipal Tax Net Annual Value (-) Standard Deduction @ 30% (-) Interest on Loan Unrealised Rent (-) 30% Standard Deduction

2,00,000 1,85,000

(2,00,000)

12,00,000

NIL

2,77,777

6,22,222

15,000 4,500

6,00,000

(5,89,500) 3,00,000

Loss under the head House Property [Note: 1] (2,39,500)

Profits and Gains from Business or Profession: Under Section 44AD: Presumptive Income (1.5 Crore x 8%)

Capital Gains: FVC (Note: 2) u/s 50C (-) ICOA [25,000 x 272/100] (-) Exemption u/s 54 (Note: 3) (-) Exemption u/s 54EC (Note: 4) Long Term Capital Gains Short Term Capital Gains (Rs. 5 Lakh x 15/27)

35,00,000

68,000

34,32,000 34,32,000

NIL

Income from Other Sources:

Section 56(2)(x)(b) [(4,50,000/12%) = 37,50,000 – 35,00,000]

Interest (Rs. 5 Lakh x 5/27)

Dividend (Rs. 5 Lakh x 7/27) = Rs. 1,29,630/-

Dividend = Rs. 11,50,000/-

(-) Exemption u/s 10(34)

2,50,000 92,592

2,79,630

Gross Total Income (-) Chapter VIA Deduction:

Section 80C Eligible Amount = Rs. 4,50,000/- Maximum Allowed = Rs. 1,50,000/-

19,00,000

(1,50,000)

Total Income 17,50,000

Computation of Tax Liability

Particulars Amount Amount

Tax at Special Rates u/s 115BBDA: 10% x Rs. 2,79,630/-

Tax on Balance Income (i.e., 14,70,370/-) at Slab Rate

Upto Rs. 2,50,000 Rs. 2.5 L – 5L = 5% Rs. 5L – 10L = 20% Rs. 10L = 30%

NIL 12,500

1,00,000 1,41,111

Total Tax Liability (+) Education Cess @ 3%

27,963

2,53,611

2,81,574 8,447

Tax Liability 2,90,021

Rs. 12,79,630/-

Rs. 10,00,000/-

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

3

Interest u/s 234B Since 90% of assessed tax is not paid as advance tax, interest u/s 2354B @ 1% for 3 months = 2,90,021 x 1% x 3 Months Interest u/s 234C Instalment of advance tax

Due Date % Income Tax Liability

Advance Tax Due

Interest u/s

234C

15th June 15 2,70,369* - - -

15th Sept. 45 2,70,369 - - -

15th Dec. 75 2,70,369 - - -

15th March 100 (2,70,369 + 12L) =

14,70,369

2,61,219 2,61,219 2,61,219 x 1% x 1 month =

2,612 31st March 100 17,50,000 2,90,021 28,802

(2,90,021 –

2,61,219)

28,802 x 1% x 1

month = 288

Total Interest u/s 234C 2,900

Note: It is assumed entire dividend is received on 31/03/2018.

8,700

2,900

Total Tax Liability 3,01,621

Mr. DS aged 62 Years, a NRI, furnishes the following particulars of asset during the previous year ended 2017-18:

(A) Asset Transferred Date of Transfer Net Sale Consideration

(1) Listed equity shares of Indian companies purchased in June, 2012 at a cost of Rs. 2 Lakhs (STT paid both at the time of purchase and transfer)

15/03/2018 Rs. 4,00,000

(2) Unlisted shares purchased in June, 2016 at a cost of Rs. 1,75,000. FMV on the date of transfer is Rs. 3,50,000

15/03/2018 Rs. 3,25,000

(3) Preference Share of private company (A Ltd.) purchased in June, 2015 at a cost of Rs. 2,00,000. The said preference shares were converted on 15/04/2017 to receive 18% equity shares of the said company. FMV of the equity shares was Rs. 3,50,000. The equity shares were finally sold on 31/12/2017. FMV as on this date was Rs. 4,50,000.

31/12/2017 Rs. 4,25,000

(4) He has purchased Reliance ADR on 01/06/2015 at Rs. 5,00,000. The ADR is converted into shares of RIL on 30/06/2017. The FMV of the shares is Rs. 6,00,000. The shares are sold on 31/01/2018 on recognised stock exchange on which STT has been paid.

31/01/2018 Rs. 12,00,000

(B) Asset Purchased Date of Purchase

Amount Paid

Qu

es

tio

n :

2

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

4

Purchased shares of B Pvt. Ltd. (FMV = Rs. 4,50,000) 10/01/2018 Rs. 3,75,000

NHAI Bond 20/03/2018 Rs. 2,00,000

(C) Other Information:

Mr. DS received loan from A Pvt. Ltd. of Rs. 5,00,000 on 30/09/2017. The accumulated profit of the company as on this date is Rs. 4,50,000. He repaid the loan on 01/11/2017.

He has paid medical insurance premium for himself of Rs. 32,000.

Compute taxability of Mr. DS for AY 2018-19.

Solution:

Computation of Total Income For the A.Y. 2018-19

Particulars Amount Amount

(1) Equity Shares – Exempt u/s 10(38)

NIL

1,75,000

50,000

1,00,000

6,00,000

(2) Unlisted Shares: Section 50CA – FMV (-) COA (POH < 2Yrs.)

3,50,000 1,75,000

Short Term Capital Gain

(3) Preference Shares: Section 50CA – FMV (-) COA (POH = June, 15 to Dec., 17)

4,50,000

2,00,000 (-) Section 54EC

2,50,000 2,00,000

Long Term Capital Gain

(4) ADR: FMV (-) COA (POH < 36 months)

6,00,000

5,00,000 Short Term Capital Gain Share Transfer (STCA):

FMV (-) COA

12,00,000 6,00,000

Short Term Capital Gain

Income from Other Sources: 1) Section 56(2)(x)(c) 2) Deemed Dividend u/s 2(22)(e)

75,000

4,50,000

5,25,000

Gross Total Income Less: Chapter VIA Deductions

- Section 80D

14,50,000

25,000

Total Income 14,25,000

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

5

Computation of Tax Liability

Particulars Amount Amount

1) Taxable at special rates - U/s 112, LTCG on Preference shares @ 10%

(Rs. 50,000 x 10%) - STCG on shares sold after conversion from ADR @ 15%

(Rs. 6,00,000 x 15%) 2) Taxable at Normal Rates

STCG on Unlisted Shares 1,75,000 STCG on ADR 1,00,000 Income Taxable u/s 56(2)(x)(c) 75,000 Deemed Dividend u/s 2(22)(e) 4,50,000 Less: Deduction u/s 80D 25,000 7,75,000

Upto Rs. 2,50,000 Rs. 2.5 L – 5L = 5% Above 5L = 20%

NIL 12,500 55,000

5,000

90,000

67,500

95,000

67,500

Tax Liability (+) Education Cess @ 3%

1,62,500 4,875

Total Tax Liability 1,67,375

Note: As per section 112, In case of non-resident, capital gain on equity shares of A Ltd. received on conversion of preference shares would be taxable @ of 10% (being unlisted share) without giving effect to first and second proviso to section 48. The provisions of chapter XIIA and section 115E shall not apply as the equity share are not purchased in convertible foreign exchange.

Answer the following questions: a) Bingo Inc. (resident of UK), engaged in shipping business had appointed 4 agents in India for booking

cargo and for clearing goods. Bingo Inc. had set up and maintained ‘Vault’ (an integrated and centralized communication system) for its agents across globle. Bingo Inc. incurred Rs. 1 crore on developing the system. The Indian agents shared cost of system & paid Rs. 10 Lakh on prorata basis without deducting tax. Contending to be reimbursed of expenses. The AO treated the payments by agent as fees for technical services and issued notice to agents u/s 201(1) treating them assessee in default. Examine the transaction. Solution:

Director of Income-Tax (International Taxation) v. A.P. Moller Maersk [2017] – SC Facts: 1. The assessee was a

foreign company engaged in shipping

Provision: Sec.9(1)(vii) provides that income by way of fees for technical services payable by a person who is a resident in India is deemed to accrue or arise in India.

Qu

es

tio

n :

3

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

6

business and was a tax resident of Denmark.

2. The assessee had agents working for it across the globe, who booked cargo and acted as clearing agents.

3. In India, the assessee had three agents.

4. The assessee had set up and maintained a vertically integrated communication system called Maersk net system in order to help all its agents.

5. The agents paid for the system on a pro rata basis.

6. The Assessing Officer contended that the amounts paid by the Indian agents were fees for technical services taxable under Article 13(4) of the India and Denmark DTAA.

7. The assessee argued that the arrangement was merely a cost sharing system and the payments were only a reimbursement of expenses.

Analysis: 1. Centralised communication system was an integral part of the

international shipping business of the assessee The Supreme Court observed that, for the sake of convenience of its agents, the assessee had set up a centralised communication system which was an integral part of the international shipping business of the assessee and common facility was provided to all the agents.

2. Sharing of Expenditure Towards Common Facilities: The expenditure incurred for running this system was shared by all the agents and payments to assessee were merely as reimbursement of expenses incurred. The payments could not be treated as fees for technical services.

3. Transaction at ARM’s Length: No profit element was embedded in the payments, also the TPO had accepted that the payments were in the nature of reimbursement (in assessee’s hands at arm's length)

4. DTAA applied: Moreover, the Revenue authorities had accepted that assessee’s freight income in the relevant assessment years was not chargeable to tax as it arose from the operation of ships in international waters in terms of Article 9 of the India and Denmark DTAA (DS Comment: as per Article 9, shipping profits are taxable in the country where POEM is established).

5. Business Profit v/s Technical Services: Once that was accepted and it was found that the communication system was an integral part of the shipping business, payments received from agents could not be treated as in lieu of any technical services.

6. It was only a facility that was allowed to be shared by the agents and it can not be treated as any technical services SC relied on Kotak Securities Ltd. ruling wherein it was held that “use of facility does not amount to technical services, as technical services denote services catering to the special needs of the person using them and not a facility provided to all”; Thus, SC ruled that “it is only a facility that was allowed to be shared by the agents and by no stretch of imagination it can be treated as any technical services provided to the agents”

Issue Raised: Whether payments made by the agents, , to use a centralized communication system

Conclusion: The Supreme Court, accordingly, held that amounts paid by Indian agents to the non-resident company would not be liable to tax as fee for technical services under Article 13(4) of the India and Denmark DTAA.

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

7

maintained by the assessee-company, can be treated as fees for technical services?

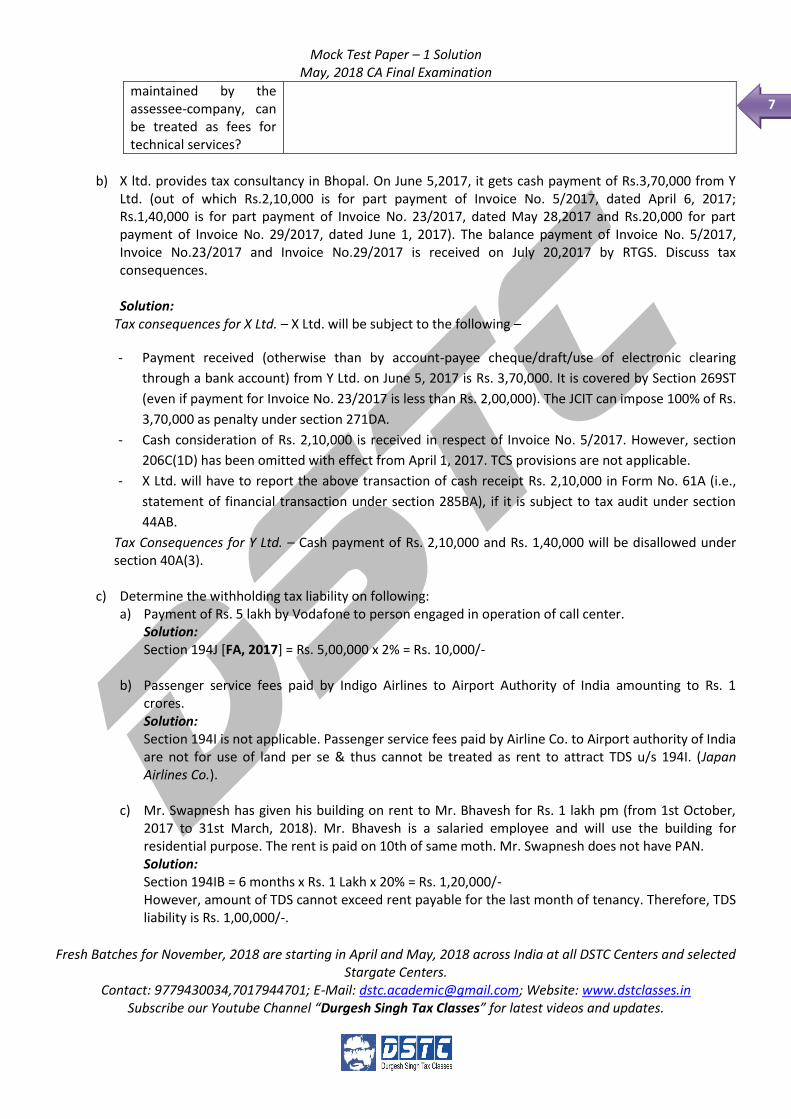

b) X ltd. provides tax consultancy in Bhopal. On June 5,2017, it gets cash payment of Rs.3,70,000 from Y

Ltd. (out of which Rs.2,10,000 is for part payment of Invoice No. 5/2017, dated April 6, 2017; Rs.1,40,000 is for part payment of Invoice No. 23/2017, dated May 28,2017 and Rs.20,000 for part payment of Invoice No. 29/2017, dated June 1, 2017). The balance payment of Invoice No. 5/2017, Invoice No.23/2017 and Invoice No.29/2017 is received on July 20,2017 by RTGS. Discuss tax consequences. Solution:

Tax consequences for X Ltd. – X Ltd. will be subject to the following –

- Payment received (otherwise than by account-payee cheque/draft/use of electronic clearing

through a bank account) from Y Ltd. on June 5, 2017 is Rs. 3,70,000. It is covered by Section 269ST

(even if payment for Invoice No. 23/2017 is less than Rs. 2,00,000). The JCIT can impose 100% of Rs.

3,70,000 as penalty under section 271DA.

- Cash consideration of Rs. 2,10,000 is received in respect of Invoice No. 5/2017. However, section

206C(1D) has been omitted with effect from April 1, 2017. TCS provisions are not applicable.

- X Ltd. will have to report the above transaction of cash receipt Rs. 2,10,000 in Form No. 61A (i.e.,

statement of financial transaction under section 285BA), if it is subject to tax audit under section

44AB.

Tax Consequences for Y Ltd. – Cash payment of Rs. 2,10,000 and Rs. 1,40,000 will be disallowed under section 40A(3).

c) Determine the withholding tax liability on following: a) Payment of Rs. 5 lakh by Vodafone to person engaged in operation of call center.

Solution: Section 194J [FA, 2017] = Rs. 5,00,000 x 2% = Rs. 10,000/-

b) Passenger service fees paid by Indigo Airlines to Airport Authority of India amounting to Rs. 1 crores. Solution: Section 194I is not applicable. Passenger service fees paid by Airline Co. to Airport authority of India are not for use of land per se & thus cannot be treated as rent to attract TDS u/s 194I. (Japan Airlines Co.).

c) Mr. Swapnesh has given his building on rent to Mr. Bhavesh for Rs. 1 lakh pm (from 1st October, 2017 to 31st March, 2018). Mr. Bhavesh is a salaried employee and will use the building for residential purpose. The rent is paid on 10th of same moth. Mr. Swapnesh does not have PAN. Solution: Section 194IB = 6 months x Rs. 1 Lakh x 20% = Rs. 1,20,000/- However, amount of TDS cannot exceed rent payable for the last month of tenancy. Therefore, TDS liability is Rs. 1,00,000/-.

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

8

Answer the following questions: a) Sharanya, an individual resident & a retired employee, aged 60 years, is a well-known dramatist,

deriving income of Rs. 1,10,000 p.a. from theatrical works played abroad. Tax of Rs. 11,000 was deducted in the country where the plays were performed. India does not have any Double Tax Avoidance Agreement under section 90 of the Income-tax Act, 1961, with that country. Her income in India amounted to Rs. 5,10,000. In view of tax planning, she has deposited Rs. 1,50,000 in Public Provident Fund and paid contribution to approved Pension Fund of LIC Rs. 32,000. She also contributed Rs. 28,000 to Central Government Health Scheme during the previous year and gave payment of medical insurance premium of Rs. 26,000 to insure the health of her father, a non-resident aged 84 years, who is not dependent on her. Compute the tax liability of Sharanya for the Assessment year 2018-19. Solution:

Computation of tax liability of Sharanya for the A.Y. 2018-19:

Particulars Amount (Rs.)

Indian Income 5,10,000 Foreign Income 1,10,000 Gross Total Income 6,20,000 Less: Deduction under section 80C

Deposit in PPF

1,50,000

Under section 80CCC Contribution to approved Pension Fund of LIC

32,000

1,82,000 Under section 80CCE The aggregate deduction under section 80C, 80CCC and 80CCD(1) has to be restricted to Rs. 1,50,000

1,50,000

Under section 80D Contribution to Central Government Health Scheme Rs. 28,000 is also allowable as deduction under section 80D. Since she is a senior citizen, the deduction is allowable to a maximum of Rs. 30,000 (See Note 1) Medical insurance premium of Rs. 26,000 paid for father aged 84 years. Since the father is a non-resident in India, he will not be entitled for the higher deduction of Rs. 30,000 eligible for a senior citizen, who is resident in India. Hence, the deduction will be restricted to maximum of Rs. 25,000.

28,000

25,000

2,03,000

TOTAL INCOME 4,17,000

Particulars Amount (Rs.)

TAX ON TOTAL INCOME Income-tax (See Note below) 5,850 Less: Rebate u/s 87A (See Note below) Nil 5,850 Add: Education cess @ 2% 117 Add: Secondary and higher education cess @ 1% 59 6,026 Average rate of tax in India

(i.e. Rs. 6,026/Rs. 4,17,000 100)

1.45%

Average rate of tax in foreign country

Qu

es

tio

n :

4

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

9

(i.e. Rs. 11,000/Rs. 1,10,000 100) 10%

Rebate under section 91 on Rs. 1,10,000 @ 1.45% (lower of average Indian-tax rate or average foreign tax rate)

1,595

Tax payable in India (Rs. 6,026 – Rs. 1,595) 4,431

Notes: 1. Section 80D allows a higher deduction of up to Rs. 30,000 in respect of the medical premium

paid to insure the heath of a senior citizen. Therefore, Sharanya will be allowed deduction of Rs. 18,000 under section 80D, since she is 60 years old.

2. The basic exemption limit for senior citizens is Rs. 3,00,000 and the age criterion for qualifying as a "senior citizen" for availing the higher basic exemption limit is 60 years. Accordingly, Sharanya, being a resident, is eligible for the higher basic exemption limit of Rs. 3,00,000, since she is 60 years old.

3. For A.Y. 18-19, an individual resident whose total income does not exceed Rs. 3,50,000 is eligible for rebate of Rs. 2,500. Since, the total income of Sharanya exceeds Rs. 3,50,000 she would not be eligible for any rebate u/s 87A

4. An assessee shall be allowed deduction under section 91 provided all the following conditions are fulfilled:— (a) The assessee is a resident in India during the relevant previous year. (b) The income accrues or arises to him outside India during that previous year. (c) Such income is not deemed to accrue or arise in India during the previous year. (d) The income in question has been subjected to income-tax in the foreign country in the

hands of the assessee and the assessee has paid tax on such income in the foreign country.

(e) There is no DTAA between India and that country.

b) Answer the following questions –

(i) An Indian company, X Ltd., is a closely held company and it is a subsidiary of company Y Ltd. incorporated in country C1. X Ltd. was regularly distributing dividends but stopped distributing dividends from 1.4.2003, the date when dividend distribution tax was introduced in India. X Ltd. allowed its reserves to grow by not paying out dividends. As a result, no DDT was paid by the company. Subsequently, buyback of shares was offered by X Ltd. to its shareholder company Y Ltd. Y Ltd. paid taxes on the capital gains arising on buyback of shares at the applicable rate. Can GAAR be invoked on the ground that there is a deferral of tax liability by X Ltd., the Indian company? Solution: Whether to pay dividend to its shareholder, or buy back its shares or issue bonus shares out of the accumulated reserves is a business choice of a company. Further, at what point of time a company makes such a choice is its strategic policy decision. Such decisions cannot be questioned under GAAR.

(ii) In the above case (i), let us presume, there is a DTAA between India and Country C1 which provides that capital gains arising in India to a resident of country C1 shall not be taxed in India provided that the resident incurs $200,000 annually as operating expenditure. The shareholder Y Ltd. incurs an operating expenditure above that limit and is entitled to the treaty benefit. Y Ltd. therefore does not pay any tax on capital gains.

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

10

Can GAAR be invoked on the ground that accumulation of profits by company X Ltd. and subsequent buyback is an arrangement mainly to obtain tax benefit? Solution: Payment of dividend to its shareholder or buy back of its shares or issuing bonus shares out of the accumulated reserves is a business choice of a company, which a company is entitled to exercise at any point of time. It should be interpreted as incidental that the shareholder is entitled to a treaty benefit which exempts capital gains, but it is subject to SAAR (i.e. Limitation of Benefit clause). The decision of X Ltd. cannot be questioned under GAAR.

c) Company X borrowed money from Company Y and used it to buy shares in three 100% subsidiary companies of X. Though the fair market value per share was Rs. 100, X paid Rs. 600. The amount received by the said subsidiary companies was transferred back to another company connected to Y. The said shares were sold by X for Rs. 100/ each and a short-term capital loss was claimed. This was set off against short-term capital gains from other sources. All the companies are Indian companies. Can GAAR be invoked? Solution: By the above arrangement, the tax payer has obtained a tax benefit and created rights or obligations which are not ordinarily created between persons dealing at arm‘s length. Since transactions of purchase and sale of shares of a closely held company at a price other than the fair market value are covered under section 56 of the Act, GAAR may not be invoked as section 56, being SAAR, is applicable. However, if SAAR is not applicable considering the limited scope of section 56 to the shares of closely held companies only, then GAAR may be invoked.

d) M/s Global Architects Inc is a company incorporated in country F1. It is engaged in the business of providing architectural design services all over the world. It receives an offer from Lovely Resorts Pvt Ltd, an Indian company, for design and development of resorts all over India. India-F1 tax treaty provides that architectural services are technical services and payment for the same to a company may be taxed in India. However, if such professional services are provided by a firm or individual, then payment for such services are taxable only if the firm has a fixed base in India or stay of partners/ employees in India exceed 180 days. M/s Global Architects Inc forms a partnership firm with a third party (director of the company) having only a nominal share in the F1. The firm enters into an agreement to carry out the services in India. The company seconded its trained manpower to the firm. Thus, the partnership firm claimed the treaty benefit and no tax was paid in India. Can such an arrangement be examined under GAAR? Solution: It is obvious that there was no commercial necessity to create a separate firm except to obtain the tax benefit. The firm was only on paper as the manpower was drawn from the company. The firm did not have any commercial substance. Moreover, it is a case of treaty abuse. Hence, GAAR may be invoked to disregard the firm and tax payment for architectural services as fee for technical services. However, the rate of tax on such payment shall be as applicable under the treaty, if more beneficial.

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

11

Answer the following questions: a) DS Inc. is an UK subsidiary of DS Ltd. an Indian Co. It has earned total income of INR 65 Millions

during P.Y. 2016-17. The break of which is as under:

Particulars %

Interest Income 10

Royalty Income 20

Income from purchase from AE & sold to non AE 30

Income from purchase from non AE & sold to AE 30

Income from purchase from AE & sold to AE 10

Total Income 100

The HO of DS Inc. is also located in India. It has 100 employees out of which 30% employees are Indian resident. The total payroll expenses during the year are Rs. 10 cr. Out of which payroll expenses in respect of 30% Indian residents employees was Rs. 7 crs. Its total assets are worth Rs. 50 crs. Out of which assets worth of Rs. 10 cr are situated in India. During the year, 8 BOD meetings were conducted out of which 5 were held in UK. The MD & CEO are UK residents & take all operational decisions & sign all contracts including contract of entering into new business venture, acquisition of business. However these contracts are all key decisions requires approval of DS Ltd. Determine residential status of DS Inc. Solution:

(i) Mere fact that DS Inc is subsidiary of Indian Co does not render POEM in India. A Co. is said to be engaged in active business outside India if all conditions are fulfilled:

(a) In this case passive inc is 40% of the total income of the Co. ie.

Interest Income 10%

Royalty Income 20%

Income from purchase from AE & sold to AE 10%

Total 40%

(b) It has 60% of its employees situated outside India. (c) Assets worth more than 50% are situated outside India. (d) Out of total payroll expenses more than 50% of payroll expenses is incurred on Indian

resident employees. Since condition (d) is not fulfilled, DS Inc is not engaged in active business outside India. (ii) It appears that all key decisions are taken by MD & CEO who are UK residents. (iii) Further HO of DS inc is in India, but that shall not alter the determination of POEM in the

present case. (iv) Accordingly, POEM shall be outside India & DS Inc shall be Non - resident Co in India.

b) ABC Ltd. is an Indian Company in which XYZ Inc., a French company, has 32% shareholding and voting power. Following transactions were effected between these two companies during the financial year 2016-17. (i) ABC Ltd. sold 50,000 pieces of tie at $ 2 per tie to XYZ Inc. The identical ties were sold to

unrelated party namely PQR Inc., at $ 3 per tie.

Qu

es

tio

n :

5

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

12

(ii) ABC Ltd. borrowed $ 1,50,000 from a foreign lender based on the guarantee of XYZ Inc. For this, ABC Ltd. paid $ 8,000 guarantee fee to XYZ Inc. From an unrelated party for the same amount of loan, XYZ Inc. collected $ 6,000 as guarantee fee.

(iii) ABC Ltd. paid $ 12,000 to XYZ Inc. for getting various potential customers details to improve its business. XYZ Inc. provided the same service to unrelated parties for $ 8,000. Assume the rate of exchange as 1 $ = ₹ 64

ABC Ltd. is located in a Special Economic (SEZ) and its income before pricing adjustments for the year ended 31st March, 2017 was ₹ 900 lakhs.

Compute the adjustments to be made to the total income of ABC Ltd. State whether it can claim deduction under section 10AA for the income enhanced by applying transfer pricing provisions. Solution: ABC Ltd, the Indian company and XYZ Inc., the French company are deemed to be associated enterprises as per section 92A(2)(a), since XYZ Inc. holds shares carrying not less than 26% of the voting power in ABC Ltd. As per Explanation to section 92B, the transactions entered into between these two companies for sale of product, lending or guarantee and provision of services relating to market research are included within the meaning of “international transaction”. Accordingly, transfer pricing provisions would be attracted and the income arising from such international transactions have to be computed having regard to the arm’s length price. In this case, from the information given, the arm’s length price has to be determined taking the comparable uncontrolled price method to be the most appropriate method.

Particulars Amount (in Lakhs)

Amount by which total income of ABC Ltd. is enhanced on account of adjustment in the value of international transactions:

(i) Difference in price of tie @ $ 1 each for 50,000 pieces sold to XYZ Inc. ($ 1 x 50,000 x 64)

(ii) Difference for excess payment of guarantee fee to XYZ Inc. for loan borrowed from foreign lender ($ 2,000 x 64)

(iii) Difference for excess payment for services to XYZ Inc. ($ 4,000 x 64)

32.00

1.28 2.56

Total 35.84

ABC Ltd. cannot claim deduction under section 10AA in respect of Rs. 35.84 lakhs, being the amount of income by which the total income is enhanced by virtue of the first proviso to section 92C(4).

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

13

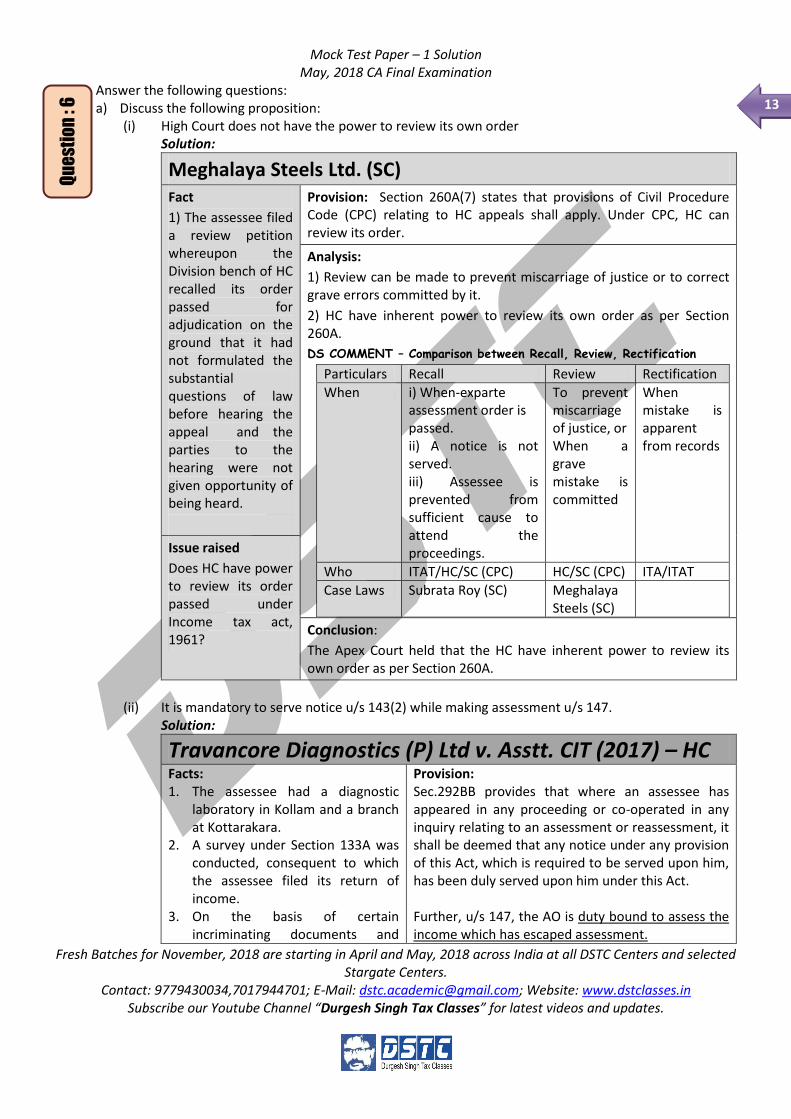

Answer the following questions: a) Discuss the following proposition:

(i) High Court does not have the power to review its own order Solution:

Meghalaya Steels Ltd. (SC) Fact

1) The assessee filed a review petition whereupon the Division bench of HC recalled its order passed for adjudication on the ground that it had not formulated the substantial questions of law before hearing the appeal and the parties to the hearing were not given opportunity of being heard.

Provision: Section 260A(7) states that provisions of Civil Procedure Code (CPC) relating to HC appeals shall apply. Under CPC, HC can review its order.

Analysis:

1) Review can be made to prevent miscarriage of justice or to correct grave errors committed by it.

2) HC have inherent power to review its own order as per Section 260A.

DS COMMENT – Comparison between Recall, Review, Rectification

Particulars Recall Review Rectification

When i) When-exparte assessment order is passed. ii) A notice is not served. iii) Assessee is prevented from sufficient cause to attend the proceedings.

To prevent miscarriage of justice, or When a grave mistake is committed

When mistake is apparent from records

Who ITAT/HC/SC (CPC) HC/SC (CPC) ITA/ITAT

Case Laws Subrata Roy (SC) Meghalaya Steels (SC)

Issue raised

Does HC have power to review its order passed under Income tax act, 1961?

Conclusion:

The Apex Court held that the HC have inherent power to review its own order as per Section 260A.

(ii) It is mandatory to serve notice u/s 143(2) while making assessment u/s 147.

Solution:

Travancore Diagnostics (P) Ltd v. Asstt. CIT (2017) – HC Facts: 1. The assessee had a diagnostic

laboratory in Kollam and a branch at Kottarakara.

2. A survey under Section 133A was conducted, consequent to which the assessee filed its return of income.

3. On the basis of certain incriminating documents and

Provision: Sec.292BB provides that where an assessee has appeared in any proceeding or co-operated in any inquiry relating to an assessment or reassessment, it shall be deemed that any notice under any provision of this Act, which is required to be served upon him, has been duly served upon him under this Act. Further, u/s 147, the AO is duty bound to assess the income which has escaped assessment.

Qu

es

tio

n :

6

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

14

materials unearthed during the survey, a notice under section 148 was issued. Subsequently, the incomes were assessed for assessment years 2009-10 and 2010-11 under section 143(3) read with section 147.

4. The assessee raised additional jurisdictional grounds before the Appellate Tribunal. The assessee contended that for the assessment year 2009-10, the assessment was completed under section 143(3) read with section 147. However, a notice under section 143(2) was not issued.

5. The Tribunal held that in view of section 292BB, the assessee’s participation in the reassessment proceedings would condone the omission to issue a notice.

Analysis: 1. Without the statutory notice under section

143(2), the Assessing Officer could not assume jurisdiction.

2. Non-issuance of notice u/s 143(2) is not a procedural defect Here, Assessing Officer recorded his inability to generate a notice as the return was not filed electronically. Such defect cannot be cured subsequently, since it is not procedural but one that goes to the root of the jurisdiction.

3. Sec.292BB would not apply in absence of mandatory issuance of notice u/s 143(2) Even though the assessee had participated in the proceedings, in the absence of mandatory notice, section 292BB cannot help the Revenue officers who have no jurisdiction. Section 292BB helps Revenue in countering claims of assessees who have participated in proceedings once a due notice has been issued.

Issue Raised: Whether failure to issue notice under section 143(2) would vitiate the assessment under section 147, notwithstanding the assessee’s participation in the proceedings? Would section 292BB come to the rescue of the Revenue authority if they omit to issue notice under section 143(2)?

Conclusion: HC thus held that Sec. 292BB would not apply where no notice was issued u/s 143(2)

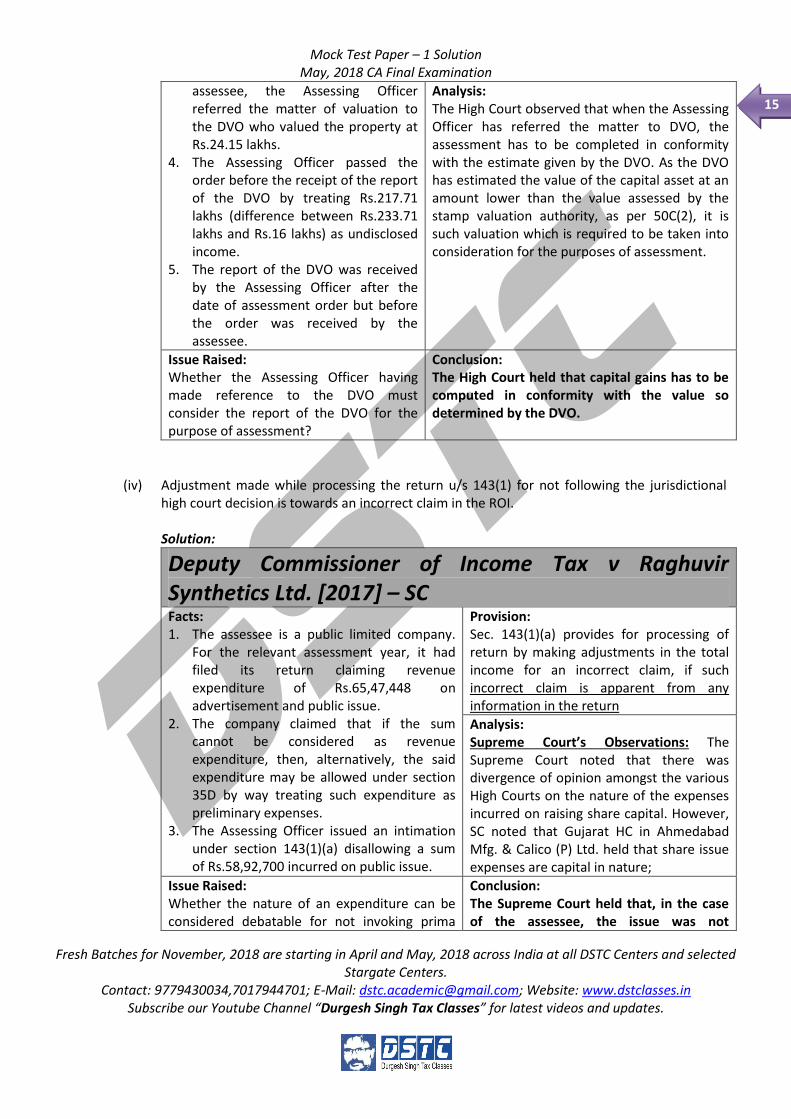

(iii) It is not mandatory for AO to consider the DVO report where he has made a reference to the

DVO for valuation. Solution:

Principal CIT v. Ravjibhai Nagjibhai Thesia (2016) – HC Facts: 1. The assessee sold his property for

Rs.16 lakhs. 2. The State stamp valuation authority

valued the property at Rs.233.71 lakhs.

3. During the course of assessment proceedings, at the request of the

Provision: Sec.50C(2) provides that where the assessee claims before any Assessing Officer that the value adopted by the stamp valuation authority under sub-section (1) exceeds the fair market value of the property as on the date of transfer, the Assessing Officer may refer the valuation of the capital asset to a Valuation Officer.

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

15

assessee, the Assessing Officer referred the matter of valuation to the DVO who valued the property at Rs.24.15 lakhs.

4. The Assessing Officer passed the order before the receipt of the report of the DVO by treating Rs.217.71 lakhs (difference between Rs.233.71 lakhs and Rs.16 lakhs) as undisclosed income.

5. The report of the DVO was received by the Assessing Officer after the date of assessment order but before the order was received by the assessee.

Analysis: The High Court observed that when the Assessing Officer has referred the matter to DVO, the assessment has to be completed in conformity with the estimate given by the DVO. As the DVO has estimated the value of the capital asset at an amount lower than the value assessed by the stamp valuation authority, as per 50C(2), it is such valuation which is required to be taken into consideration for the purposes of assessment.

Issue Raised: Whether the Assessing Officer having made reference to the DVO must consider the report of the DVO for the purpose of assessment?

Conclusion: The High Court held that capital gains has to be computed in conformity with the value so determined by the DVO.

(iv) Adjustment made while processing the return u/s 143(1) for not following the jurisdictional high court decision is towards an incorrect claim in the ROI. Solution:

Deputy Commissioner of Income Tax v Raghuvir Synthetics Ltd. [2017] – SC Facts: 1. The assessee is a public limited company.

For the relevant assessment year, it had filed its return claiming revenue expenditure of Rs.65,47,448 on advertisement and public issue.

2. The company claimed that if the sum cannot be considered as revenue expenditure, then, alternatively, the said expenditure may be allowed under section 35D by way treating such expenditure as preliminary expenses.

3. The Assessing Officer issued an intimation under section 143(1)(a) disallowing a sum of Rs.58,92,700 incurred on public issue.

Provision: Sec. 143(1)(a) provides for processing of return by making adjustments in the total income for an incorrect claim, if such incorrect claim is apparent from any information in the return

Analysis: Supreme Court’s Observations: The Supreme Court noted that there was divergence of opinion amongst the various High Courts on the nature of the expenses incurred on raising share capital. However, SC noted that Gujarat HC in Ahmedabad Mfg. & Calico (P) Ltd. held that share issue expenses are capital in nature;

Issue Raised: Whether the nature of an expenditure can be considered debatable for not invoking prima

Conclusion: The Supreme Court held that, in the case of the assessee, the issue was not

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

16

facie adjustment under section 143(1)(a), where the jurisdictional High Court has taken a view that the expenditure is capital in nature even though some other High Courts have held that the same is revenue in nature?

debatable. Since the registered office of the assessee is in Gujarat, the law laid down by the Gujarat High Court is binding on the assessee and the prima facie adjustment can be made by the AO u/s 143(1)(a).

(v) Immunity from prosecution shall be withdrawn where the dues are paid after the time allowed (including extension thereof) by the settlement commission. Solution:

Sandeep Singh v Union of India [2017] – SC Facts: 1. The petitioner is a dealer in real

estate at Amritsar. 2. A search was conducted on August

21, 2009 at his business and residential premises under section 132(1) subsequent to which the assessee filed an application before the Settlement Commission under section 245C(1).

3. The case was settled before the Settlement Commission on December 12, 2014.

4. Pursuant to the assessment after settlement, the petitioner was unable to pay the amount due by the stipulated date. He sought an extension for 14 months but was only given time until July 31, 2015.

5. The assessee filed a writ petition before the High Court seeking quashing / modification of the Settlement Commission’s order granting partial extension of time.

6. By the time the matter was heard by the Supreme Court, he had paid off all pending amounts.

Provision: Sec. 245H(1A) provides that an immunity granted to a person shall stand withdrawn if;

such person fails to pay any sum specified in the order of settlement passed within the time specified in such order or within such further time as may be allowed by the Settlement Commission, or

fails to comply with any other condition subject to which the immunity was granted

and thereupon the provisions of this Act shall apply as if such immunity had not been granted.

Analysis: 1. The Supreme Court explained that in case

payments are not made within the time granted by the Settlement Commission or in case the person fails to comply with any other condition, subject to which the immunity was granted, the immunity shall stand withdrawn.

2. All sums having been paid before approaching Supreme Court, Supreme Court observed that there is no need to relegate the assessee to the Settlement Commission. Settlement Commission has the power to extend the timelines. Hence, in the instant case, it shall be taken that the assessee has made the payments within the time granted under section 245H(1A).

Issue Raised: Whether payment of sums due, after the deadline stipulated by the Settlement Commission, would save the petitioner from withdrawal of immunity from prosecution?

Conclusion: The Supreme Court held that the assessee having cleared all taxes due vide order of Settlement Commission, albeit after stipulated deadline, is immune from prosecution.

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

17

b) The authorised officer shall be under obligation to disclose the reasons for search once the assessee

files the ROI in response to the notice u/s 153A and demands for the same. Solution: No, As per amendment by FA 2017, the RTB that prompted authorisation of search u/s 132 shall not be disclosed to any person or tribunal.

c) The Commissioner of Income-tax can revise an order during the pendency of an appeal before the First Appellate Authority. Solution: Yes, but only in respect of the matter not considered by the first appellate authority.

DLF Housing Ltd. is wholly owned subsidiary of DLF REIT. The Net Profit for the PY 2017-18 is Rs. 200 Lakhs after debiting / crediting the following items: (i) Interest of Rs. 5 Lakhs paid towards loan taken from DLF REIT to construct commercial property on

which Tax is not deducted. (ii) Cost of construction incurred during the previous year Rs. 300 Lakhs in respect of luxurious

residential apartment project completed during the previous year. The said cost includes Rs. 50 Lakhs towards interest on loan taken from scheduled bank which was paid after the due date of the filing of the ROI. Out of 50 Units constructed during the previous year, 10 Units remained unsold.

(iii) Profit include Rs. 30 Lakhs i.r.t., affordable housing scheme for which deduction u/s 80IBA is available.

(iv) Profits of Rs. 20 lakhs from transfer of unquoted shares credited to profit & loss account (FVC: Rs. 80 lakhs, FMV: Rs. 90 lakhs). The shares were held for 6 months.

Calculate the tax payable of DLF Housing Ltd.

Solution:

Particulars Amount (in lakhs)

Profits and Gains from Business or Profession Net Profit (-) Profit of unquoted shares (treated in CG head) (+) Cost attributable to unsold units

- 250 x 1/5 - 50 x 1/5

(+) Section 40(a)(ia) (+) Section 43B – Interest Profits and Gains from Business or Profession House Property:

Gross Annual Value (GAV) – 10 Units NIL (-) Municipal Taxes -

200

20 180

50

10 240 NIL

40 280

Qu

es

tio

n :

7

Mock Test Paper – 1 Solution May, 2018 CA Final Examination

Fresh Batches for November, 2018 are starting in April and May, 2018 across India at all DSTC Centers and selected Stargate Centers.

Contact: 9779430034,7017944701; E-Mail: [email protected]; Website: www.dstclasses.in Subscribe our Youtube Channel “Durgesh Singh Tax Classes” for latest videos and updates.

18

Net Annual Vale (NAV) - (-) Interest (not on payment basis) 10 lakh

Capital Gains:

FVC 90 lakh (-) COA [80-20] 60 lakh

Gross Total Income (-) Chapter VIA Deduction

Section 80IBA (100% Deduction)

(2)

30 308

30

Total Income 278

For Most Important Mock Test Paper – 3 Solution Subscribe our Youtube Channel “Durgesh Singh Tax Classes”

Video will be uploaded by 10th April, 2018 by 8:00PM Thanks

All the Very Very Best!!!