mitchell: legislative changes for py2015 · form 8962, part 3, repayment of excess aptc . ......

TRANSCRIPT

Legislative Changes For PY2015

Melodye Mitchell, Branch Chief EFS Development Services

A Premium Tax Credit (PTC) may be requested through the Federal or State marketplace. Factors that are considered in determining the amount of the subsidy include:

• Household family size

• Household Income between 100% to 400% of the Federal Poverty Line (e.g., $23,550 – $94,200 for a family of four in 2013)

• Not eligible for other health benefits coverage (e.g., Medicaid, Medicare) other than the individual insurance market

• Be a U.S. citizen or be lawfully present

• Not be incarcerated (with some exceptions)

• Not be claimed as a dependent by another individual

Who is eligible for premium tax credit?

Prisoners, undocumented immigrants, and Indian tribal members will be

exempt from shared responsibility payments. Members of certain

religious sects or health care sharing ministries also can apply for a

religious exemption.

Other U.S. residents who will be exempt include:

• Certain low-income individuals: Those who cannot afford coverage,

or live in states that have opted out of the Medicaid expansion;

• People who have no plan options in their state's health insurance

exchange.

• Other individuals who meet certain criteria: Specifically, individuals

who have suffered a hardship or a coverage gap of three or fewer

months.

Who’s Exempt from the Shared Responsibility Payment?

• Employee's required premium co-share for the lowest-cost (bronze plan), self-only coverage that provides minimum value is not greater than 9.5 percent of an employee's W-2 taxable (Box 1) income. If it is higher, the employee may be eligible for a Premium Tax Credit.

NOTE:The cost of dependent coverage is not calculated in the determination of whether the employer is offering affordable coverage.

• Starting in 2014, individuals offered employer-sponsored coverage that’s affordable and provides minimum value won’t be eligible for a premium tax credit either for themselves or for their dependents.

What's ‘Affordable’ Coverage Under Health Care Reform?

Affordability Guidelines

• If employer coverage becomes affordable during the course of a

year, eligibility for premium tax credits cease.

• A determination that employer-sponsored coverage is unaffordable

must be redetermined each year and is not automatically extended.

• If an employer imposes a waiting period of up to ninety days before

coverage can begin, as permitted by the ACA, premium tax credit

eligibility continues until employer-sponsored coverage is available.

When preparing TY2014 income tax, each

taxpayer must

(1) Indicate on form 1040 or form 1040A that

the taxpayer and all dependents listed on

the form had minimum essential health care

coverage for all 12 months, OR

(2) Include form 8965 which identifies

exemptions obtained from the marketplace

for months where insurance coverage was

not obtained, OR

(3) Include a shared responsibility payment with

the submission

Reporting Insurance Coverage at Filing

ACA Forms Depicted in this Presentation

Form 8962 must be attached to Form

1040/1040A/1040NR if

• You are claiming the premium tax credit

on Form 8962, line 26.

• You received an advance payment of the

premium tax credit.

• You have an excess advance payment of

the premium tax credit you must repay

on Form 8962, line 29.

• You shared a policy with another tax filer.

• You are using the alternative calculation

for the year of marriage

Claiming a Premium Tax Credit (PTC)

Form 8962, Part 1 Annual and Monthly Contribution Amount

Modified Adjusted Gross Income (MAGI). • Modified adjusted gross income is your adjusted gross income, plus (1) any amounts excluded from your

gross income under section 911 (the exclusion of foreign earned income for taxpayers living in a foreign

country), and (2) tax-exempt interest you receive or accrue during the year.

• If you file Form 1040:

– Your adjusted gross income is on line 37 of Form 1040

– Amounts excluded from gross income under section 911, if any, are on Form 2555 (add amounts

from lines 45 and 50) or Form 2555EZ (line 18)

– Your tax-exempt interest, if any, is on line 8b of Form 1040

• If you file Form 1040A:

– Your adjusted gross income is on line 21 of Form 1040A

– You did not have any amounts excluded from gross income under section 911

– Your tax-exempt interest, if any, is on line 8b of Form 1040A

• If you file Form 1040EZ:

– Your adjusted gross income is on line 4 of Form 1040EZ

– You did not have any amounts excluded from gross income under section 911

– Your tax-exempt interest , if any, is in the space to the left of line 2 on Form 1040EZ

Form 8962, Part 2, PTC Credit Claim and Reconciliation of APTC

Form 8962, Part 3, Repayment of Excess APTC

Reconciliation: • A “reconciliation” must then occur between the advanced payment for the tax credit already

received and the total amount of the premium tax credit to which the individual is actually

entitled.

• If over the course of the year household income turns out to be greater or less than projected,

or if household composition or income has changed, the final tax credit may turn out to be

greater or less than the amount already paid.

• If the taxpayer turns out to have been eligible for more than had been paid, the taxpayer gets

a refund. If, however, the government has paid more than the taxpayer in fact turns out to be

entitled to, the taxpayer must pay the money back.

Form 8962, Part 4, Shared Policy Allocation

Form 8962 Part V

Form 8965 Taxpayers may submit Form 8965 ito report exemptions they were granted from insurance coverage

Form 8965 Pts 1 and 2

If anyone in your tax

household has been

granted one or more

exemptions from the

Marketplace, complete

Part I for each

Marketplace-granted

exemption.

Form 8965 Pt 3

ACA Information Returns

Form 1095-A

Form 1095-A is filed by the State and Federal Marketplace in accordance with an interagency agreement. A recipient copy will be mailed to the individual policyholder by January 31st for use in filing their PY2015 tax returns. There is no requirement to submit the 1095-A with your tax return. In PY2015, Heath Care Coverage provided by State and Federal Marketplaces is mandatory.

Form 1094-B

• This form is used by the Health Insurance Policy Issuers to report Health Care coverage.

• Health care coverage reporting is optional for PY2015 and mandatory for PY2016

• This transmittal must be submitted with one or more 1095-B detailed records.

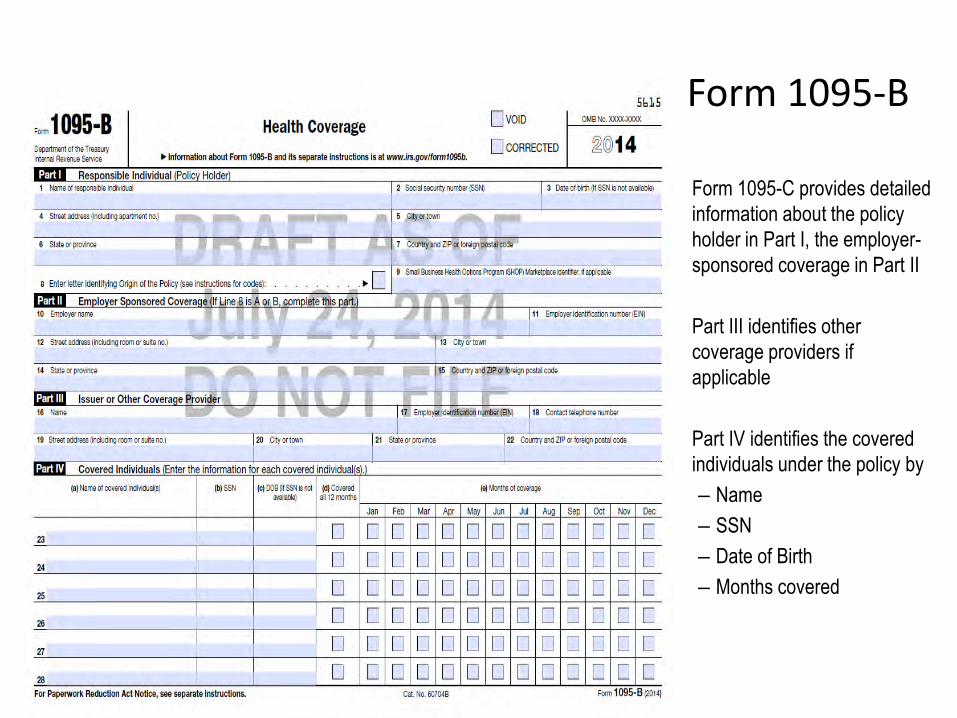

Form 1095-B

• Form 1095-C provides detailed

information about the policy

holder in Part I, the employer-

sponsored coverage in Part II

• Part III identifies other

coverage providers if

applicable

• Part IV identifies the covered

individuals under the policy by

– Name

– SSN

– Date of Birth

– Months covered

Form 1094-C Parts 1 and 2

•

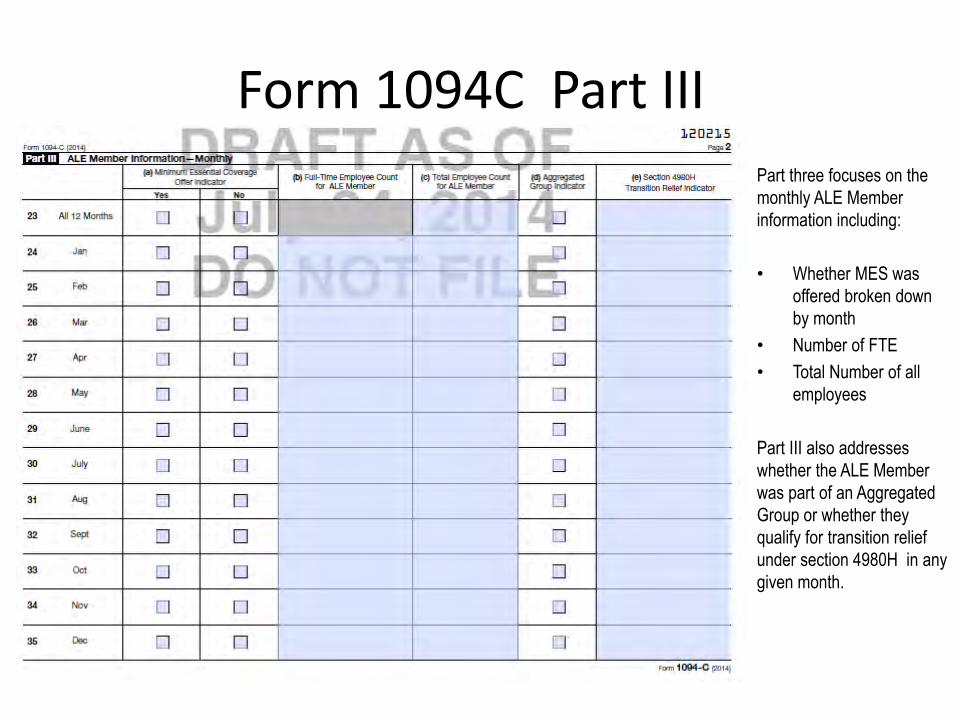

Form 1094C Part III

Part three focuses on the

monthly ALE Member

information including:

• Whether MES was

offered broken down

by month

• Number of FTE

• Total Number of all

employees

Part III also addresses

whether the ALE Member

was part of an Aggregated

Group or whether they

qualify for transition relief

under section 4980H in any

given month.

Form 1094C – Part IV

Part IV request that the issuer provide the names and Employer Identification Numbers for other members of the Aggregated ALE Group

Questions??