misdirected and ineffective: regional financial cooperation in asia c.p.chandrasekhar

TRANSCRIPT

Misdirected and ineffective: Regional financial cooperation in Asia C.P.Chandrasekhar

Regulatory lessons from the crisis

Need for regulation at the national level to influence the behaviour of financial firms and the monetary authority

Need for supra-national regulation given financial consolidation and integration through cross-border flows

An affliction in one country affects others through multiple means of transmission requiring an insurance tool-kit and measures of regulation.

Lessons learnt early in Asia

Asia, especially East and Southeast Asia had learnt a number of lessons at the time of the 1997 crisis.

Deregulation by exposing countries to cross-border flows determined by decisions in metropolitan financial centres also exposes them to boom-bust cycles.Liberalisation makes countries prone to contagion, even if their own macroeconomic variables—fiscal, trade and current account balances—are impeccable. When Thailand slipped so did South Korea. Liberalisation had not just integrated them, but also linked them as a combined entity to the rest of the world.

Some features of the crisis period

The region as whole characterised by savings surpluses, though there were individual countries that recorded savings deficits. The savings surpluses were being invested in dollar denominated assets, and deficit countries were increasingly dependent on capital flowsfrom outside the region.

The external exposure of these countries prior to 1997 involved excessive exposure to foreign debt, especially short term debt. The three countries where such exposure was large in 1997 were Thailand, Indonesia and South Korea, in whose case short term foreign debt amounted to 110 per cent, 167 per cent and 195 per cent of their reserves respectively. When creditors, for whatever reason, turned wary and choose to hold back on debt rollovers or provision of new debt, a crisis ensued.

The surpluses

In 1997 only three East Asian countries ran current account surpluses: Japan, China and Singapore. Their combined surpluses totalled $135 billion.

The combined deficits of the ASEAN 5 (Thailand, Indonesia, Malaysia, Philippines and Singapore) stood at $3.3 billion and the surpluses of the Plus 3 (Korea, China and Japan) at $125.5 billion, after accounting for Korea’s deficit of $8.3 billion.

There was a net surplus in the group of $122 billion.

Conclusions drawnExcess exposure to short term flows relative to reserves, makes countries prone to crisis.

When one country hit by crisis the affliction spread to better placed countries in the region, largely because of capital exit.

Given regional surpluses problem could be addressed if crisis-hit countries had the option of swapping their own currencies for “hard currencies” and neutralizing the effects of capital flight.

The other response that was recognised but largely ignored, except for a short period in Malaysia, was to insulate economies from boom-bust cycles with capital controls.

The first phase of regional cooperation

Developing an arrangement under which such swaps were possible.

Defensive action that presumed that the crisis could not have been prevented in the first place by abjuring or calibrating financial opening and liberalization, or by using regional surpluses for financing regional development projects without relying excessively on extra-regional finance.

A positive externalityIf dependence on extra-regional finance did result in crises that necessitated turning to organizations like the IMF for balance of payments support, it was accompanied by conditonalities that countries in the region, their economic strengths notwithstanding, had little influence on.

Such conditionalities were not only procyclical, but required countries to pursue and intensify the same policies of external and internal financial liberalization that led, in the first instance, to their difficulties.

This provided a second reason for cooperation based on regional surpluses. If you could borrow locally, conditionalities would be more sensitive to country needs.

The real needAvoiding measures of liberalization that enhanced external and internal vulnerability.

Adopting such a policy of “avoidance” was also difficult for any single country independent of the rest

It resulted in regulatory arbitrage, which diverted capital flows to more “liberal” destinations in the region.It cut off access of the interventionist regimes to the external resources needed to pursue development.

That put the hold-out country at a disadvantage vis-à-vis the rest in terms of the relative ability to retain and exploit even “useful” and “not-so-harmful” capital flows. Real need for regulatory cooperation that was ignored.

A lesson from the past Countries in the East Asian region chose to largely restrict themselves to the regional borrowing option. This was not just the soft option but easy to implement because of a platform from the past.

Even before the 1997 crisis, in August 1977 central banks and monetary authorities from the ASEAN-5 came together to establish the ASEAN Swap Arrangement (ASA) with a corpus of $100 million, which was raised to $200 million in 1978.

This proved to be grossly inadequate at the time of the 1997 financial crisis.

Stage 2Japan made the first move after the 1997 crisis when in the IMF meetings in Hong Kong in September 1997 it mooted the idea of an Asian Monetary Fund (AMF).

The AMF idea came to a quick end and in Manila in November 1997 finance and central bank officials from Asia formulated the “Manila Framework” for regional cooperation to promote financial stability. Others, including the US, IMF and the World Bank had representatives.

The Manila Framework was endorsed at a meeting of finance ministers from ASEAN; Australia; PRC; Hong Kong, China; Japan; Korea; and the United States, in Kuala Lumpur, Malaysia, on 2 December 1997

The Chiang Mai Initiative

This led in May 2000 to the launch of the CMI, described as “a regional financing arrangement to supplement the existing international facilities”.

Its first pillar was an enhanced ASA with funding raised from $200 million to $1 billion, with members eligible to borrow up to two times their contribution for a period of six months (extendable for another six).

The second was a network of bilateral swap arrangements (BSAs) under which countries could opt for a swap of currencies upto an agreed amount. Initially any swap in excess of 10 per cent of the agreed amount required IMF surveillance. That was raised to 20 per cent subsequently.

Obvious weaknesses

It was estimated in 2010 that if all the BSAs entered into by Thailand was available to it in 1997, it would have been able to raise $2 billion from the CMI swap arrangement. The IMF’s bail-out package for Thailand at that time amounted to $17.2 billion.

If in addition countries had to accept an IMF programme or IMF-designed conditionalities, the second reason for opting for a regional fund was defeated.

The CMI had been killed at the very start.

The problem with CMIJapan’s decision to propose an AMF was seen as reflective of the exposure of its own banks in the region, and the conviction that after the 1997 crisis the US and the IMF are unlikely to work to restructure Asian debt to save the banks, as they did in Latin America in the 1980s. However, once mooted the proposal was seen as reflective of Asian solidarity against the US and the IMF.

In time, two factors worked to undermine the proposal.Fear of Japanese dominance in the region—a fear which the US is seen as having exploited, especially via-a-vis China.Dependence of many ASEAN countries on US markets and US-mediated capital flows resulted in these countries softening their stance once the US and the IMF expressed their opposition.

At Hong Kong ASEAN members and South Korea supported the AMF proposal, Hong Kong and Australia remained neutral, and China was silent.

Manila framework

From summary of proceedings:“This framework, which recognizes the central role of the IMF in the international monetary system, includes the following initiatives: (a) a mechanism for regional surveillance to complement global surveillance by the IMF; (b) enhanced economic and technical cooperation particularly in strengthening domestic financial systems and regulatory capacities; (c) measures to strengthen the IMF’s capacity to respond to financial crises; and (d) a cooperative financing arrangement that would supplement IMF resources.”

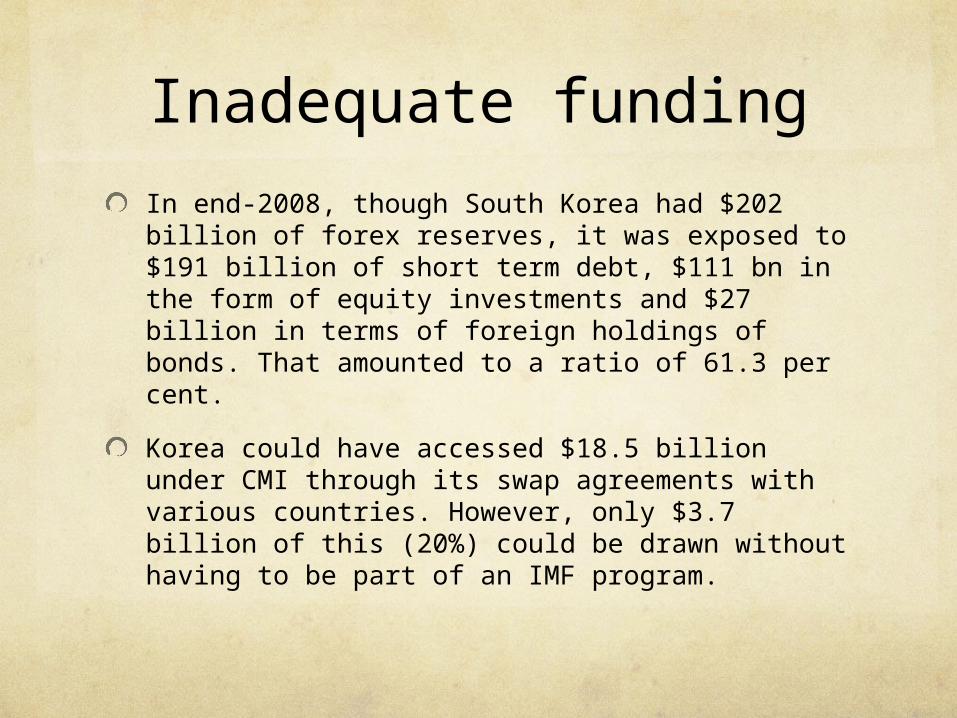

Inadequate funding

In end-2008, though South Korea had $202 billion of forex reserves, it was exposed to $191 billion of short term debt, $111 bn in the form of equity investments and $27 billion in terms of foreign holdings of bonds. That amounted to a ratio of 61.3 per cent.

Korea could have accessed $18.5 billion under CMI through its swap agreements with various countries. However, only $3.7 billion of this (20%) could be drawn without having to be part of an IMF program.

The CMI multilateralisedNot surprisingly, even the CMI proved inadequate at the time of the 2008 crisis. Capital exit at that time led to South Korea and Singapore borrowing from the Federal Reserve and Indonesia from the World Bank and other lenders.

This experience resulted in one more round of expansion when the CMI was multilateralized and became the CMIM. The members now include: Brunei, Cambodia, Hong Kong, Indonesia, Japan, Laos, Malaysia, Myanmar, the People`s Republic of China, Philippines, Singapore, South Korea, Thailand, Vietnam.

The facility with a corpus of $120 billion was established in March 2010, with the ASEAN-5 contributing 20 per cent and Korea, Japan and China providing 16, 32 and 32 per cent respectively. The size of the corpus was doubled to $240 billion in 2012.

The CMIM

When faced with balance of payments difficulties a country can swap its currency for US dollars through the facility.

Each country's borrowing quota is based on its contribution multiplied by its respective borrowing multiplier. The borrowing multiplier was set at 5 for Brunei Darussalam, Cambodia, Lao PDR, Myanmar, and Viet Nam, at 2.5 for Hong Kong, Indonesia, Malaysia, Singapore and Thailand, at 1 for Korea, and 0.5 for Japan and China it is 0.5.

One more failure?The CIMM has not emerged a major alternative to balance of payments financing from the IMF or developed country sources. One factor seen as responsible for this is the troubled relationship between the two major funders, China and Japan.

They would prefer to be seen as directly supporting distressed nations rather than doing so through an ‘impersonal’ organizational form.

Though the size of the corpus or common liquidity pool available under CMIM is defined, it remains a reserve pooling arrangement under which the commitments made by various countries remained with their central banks to be made available in the event of a crisis. The fund was made up of promises to pay by these central banks.

AMRODespite the creation of an ASEAN + 3 Macroeconomic Research Office no centralised monitoring.

Tensions were seen as ensuring that neither of the major donors were in a position to ensure that the funds accessed by member countries would be put to proper use. Any attempt to impose ex ante or ex post conditions on use of the resources would risk alienating the borrower and losing influence.

The major donors settled for a system in which large volume borrowing from the facility required an IMF programme (though now a country was allowed to borrow up to 30 per cent of its quota without submitting to IMF conditionality). This meant that, when financing requirements were large, countries would choose to approach the IMF directly.

Meek recognitionThere are now plans to create a CMIM Precautionary Line (CMIM-PL), which will operate in parallel with the CMIM mechanism (now renamed the Stability Facility, or CMIM-SF).

While CMIM would require IMF clearance, the Precautionary Line would reportedly be based on ex ante conditionality, or an assessment of the quality of a country’s economic polices (without being subject to ex post performance targets). But whether “quality” would be defined by the IMF and correspond to typical IMF type conditions is not too clear.

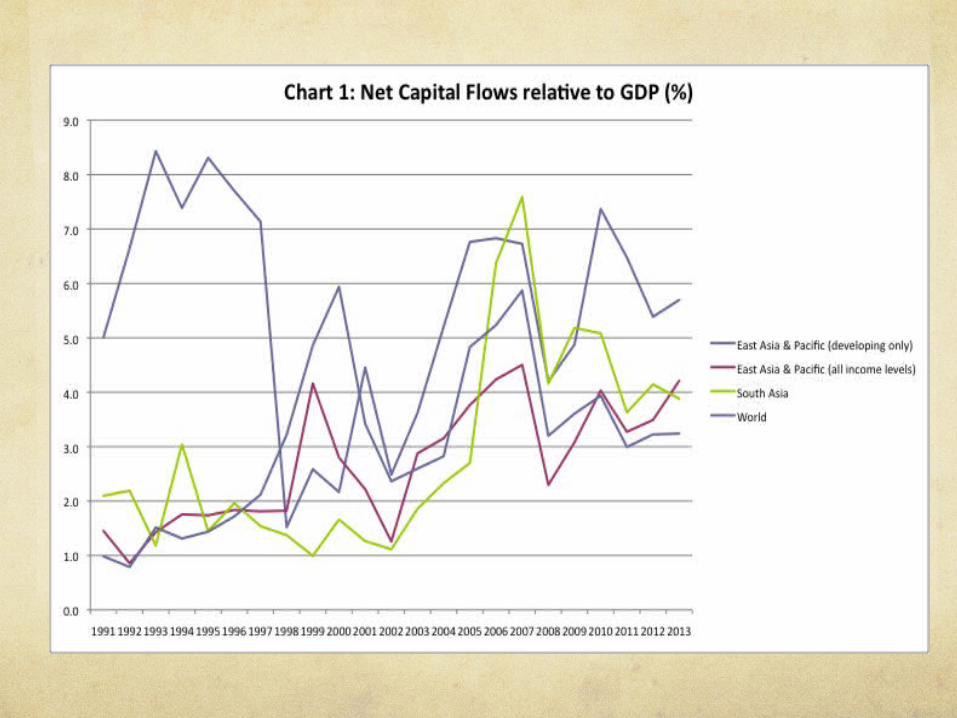

Autonomous integrationWith no effort to reduce dependence on external capital flows, autonomous trends led to a greater degree of financial integration between Asian countries as a group and the world as a whole.

Three surges of capital inflows into Asia over the last twenty five years:

First from the early 1990s till 1997, when Southeast Asia was hit by a crisisThe second from 2002 till the global financial crisis of 2008The third from 2008 to 2010 which coincided with the easing of monetary policy in the US.

In each of these periods, the ratio of net capital inflows to GDP rose steeply, followed by a period of capital exit or flight.

Two trends

While crises are episodes precipitated by capital exit, they don’t preclude the possibility of a revival soon thereafter. When the exit occurs and when it is reversed is a result of decisions outside the ambit of policy.

While in the early 1990s the inflows into Asia were focused on the NICs and second-tier industrialisers, the phenomenon is more generalized now making the region as a whole prone to boom bust cycles.

Intra-regional flows

Interestingly despite the availability of large surpluses in the region intra-regional portfolio flows are still small. Countries prefer to invest in dollar denominated assets (especially US Treasury bonds), rather than in regional assets that investors from the developed countries seem to covet.

For example, the share of developing Asia in the aggregate portfolio investment by the ASEAN + 3 grouping, while rising, is still only 15 per cent. And much of this goes to the ASEAN + 3 itself. Financial liberalization strengthens links with developed country, especially Anglo-Saxon, markets rather than between markets in the region.

ConsequenceThe increase in the presence of foreign capital has necessitated changes in the regulatory framework governing finance in these countries. Governments in the region have adopted more liberal rules with regard to the functioning of different kinds of markets and institutions, provided greater space for new instruments such as derivatives, and shown a willingness to shift to globally accepted rules for regulation.

The message seems to be that if countries choose to adopt a policy framework that emphasises the need to attract large volumes of foreign capital, reform of the regulatory structure governing finance in a common, globally dictated direction seems to be a prerequisite.

This exposes these countries to new kinds of vulnerability.

Impact on the cooperation effort

Cooperation to improve and exploit markets.

Financial liberalisation undermines the ability of governments to finance capital intensive, long gestation lag projects either directly through the budget, as China and South Korea did for long, or through government and central bank supported funding by development finance institutions, as in India.

This has given rise to a second, parallel effort at regional financial cooperation that seeks to develop regional bond markets as a means of mobilising savings for long term, less liquid investments, such as in infrastructure. Bonds and securitised instruments are considered to have better risk sharing characteristics and as facilitating the diversification of risk.

Asian Bond Market Initiative

Launched by ASEAN + 3 in 2003 with two initiatives.

Credit Guarantee and Investment Facility (CGIF), set up as a trust by ASEAN+3 and the Asian Development Bank (ADB) in 2010, which provides guarantees for bonds issued by firms facing constraints in securing long-term funding from the local bond market.

Strengthen the mutual fund infrastructure, providing smaller savers with the option of buying into liquid mutual funds that in turn invest in debt securities.

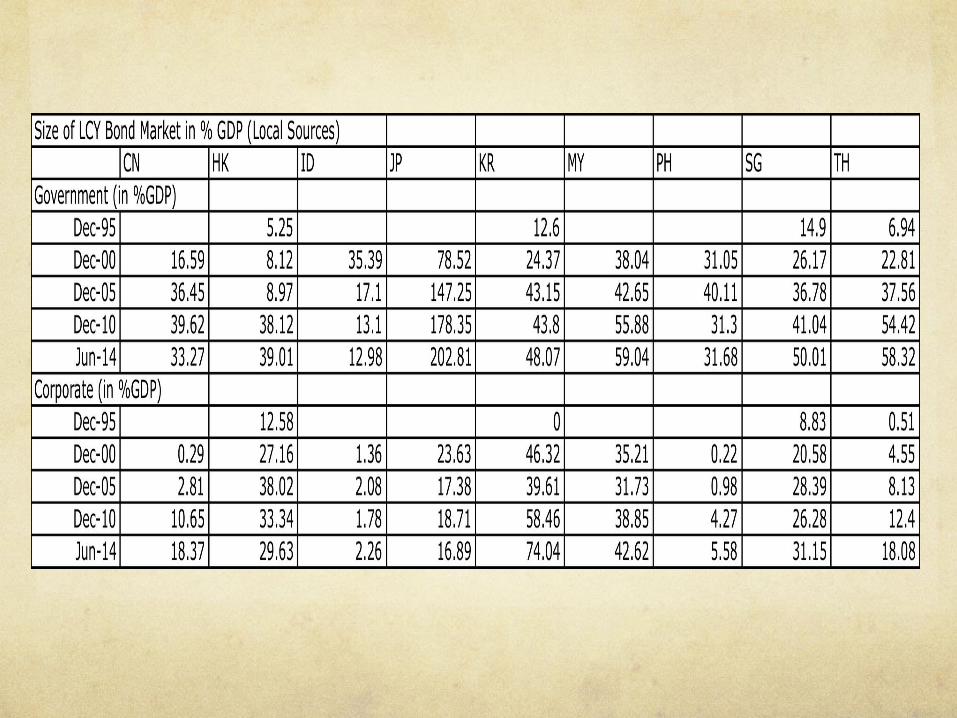

Has it worked?Even where local currency bond markets are developed, government securities seem to account for a significant share of all securities issued in the domestic market.

Bond market growth largely the result of capital inflow, with foreign investor interest in Asian bonds rising. According to Deutsche Bank Research: “Corporate bond market capitalisation reached 24.2% of the region’s GDP by 2012 from just 16.7% in 2008. In value terms, the stock of outstanding corporate bonds amounted to USD 3.2 trillion by Q3 2013 – almost triple the value recorded at the end of 2008.”

A new initiativeChina mooted and successfully managed to get 21 Asian nations to come together in October 2014 to establish the Asian Infrastructure Investment Bank (AIIB) with headquarters in Beijing.

Starting with a capital base of $50 billion contributed by China (out of the authorized capital of $100 billion), the AIIB appears a poor cousin to the Asian Development Bank with around $160 billion of capital and the World Bank with around $220 billion. But this is just the beginning and significant for an institution that is expected to focus on infrastructure.

A role for politicsClearly an instance of China’s push for dominance in the Asia-Pacific.

America has lobbied against the creation of the AIIB, Japan, which leads the ADB, is out of the AIIB, and Australia and South Korea stayed away. So did Indonesia initially, only to change tack and join the club.

While it is too early to even speculate on how the AIIB would evolve, to the extent it reduces Asian dependence on external finance in general and the World Bank and IMF in particular, it would increase the ability of countries in the region to regulate cross-border flows and reduce their vulnerability to boom-bust cycles.

Concluding remarksRegional cooperation in regulation would be substantive and can make any difference only if it involves imposing controls that help avoid boom-bust cycles rather than finding ways to adjust when confronted with crises.

Only then can the effort to build a regional financial network catering to regional interests is possible.

Discussions also need to focus on how the internal financial structure in these countries should be shaped, given their levels of development, requirements, and the availability of large investible surpluses.

The AIIB is only a small and as yet half-formed step in that direction.