mgmt 30a: midterm 2

DESCRIPTION

Midterm 2 Solutions for MGMT 30ATRANSCRIPT

M30A: PRINCIPLES OF ACCOUNTING

PRACTICE EXAM

MIDTERM #2

CHAPTER 4

1. The Golden Petting Zoo operates a drive-through tourist attraction in Colorado. The company adjusts its accounts at the end of each month. The selected accounts appearing below reflect balances after adjusting entries were prepared on April 30. The adjusted trial balance shows the following:

Prepaid Rent $ 18,000

Buildings 42,000

Accumulated Depreciation—Buildings 5,500

Unearned Ticket Revenue 600

Other data:

a) Three months' rent had been prepaid on April 1.

b) The buildings are being depreciated at $6,000 per year.

c) The unearned ticket revenue represents tickets sold for future zoo visits. The tickets were sold at $4.00 each on April 1. During April, twenty of the tickets were used by customers.

Instructions:

Prepare the adjusting entries that were made by the Golden Petting Zoo on April 30.

Solution

a) Rent Expense ........................................................................... 9,000

Prepaid Rent .................................................................. 9,000

b) Depreciation Expense ............................................................... 500

Accumulated Depreciation—Buildings ........................... 500

c) Unearned Ticket Revenue ........................................................ 80

Ticket Revenue .............................................................. 80

(20 X $4 = $80)

2. The following ledger accounts are used by the Heartland Race Track:

Accounts Receivable

Prepaid Advertising

Prepaid Rent

Unearned Sales Revenue

Sales Revenue

Advertising Expense

Rent Expense

Instructions:

For each of the following transactions below, prepare the journal entry (if one is required) to record the initial transaction and then prepare the adjusting entry, if any, required on November 30, the end of the fiscal year.

(a) On November 1, paid rent on the track facility for three months, $150,000.

(b) On November 1, sold season tickets for admission to the racetrack. The racing season is year-round with 25 racing days each month. Season ticket sales totaled $960,000.

(c) On November 1, borrowed $250,000 from First National Bank by issuing a 6% note payable due in three months.

(d) On November 5, programs for 20 racing days in November, 25 racing days in December and 15 racing days in January were printed for $3,000.

(e) The accountant for the concessions company reported that gross receipts for November were $140,000. Ten percent is due to Heartland and will be remitted by December 10.

Solution

(a) Journal Entry

Prepaid Rent ........................................................................... 150,000

Cash ............................................................................... 150,000

Adjusting Entry

Rent Expense ......................................................................... 50,000

Prepaid Rent .................................................................. 50,000

($150,000 /3 = $50,000)

(b) Journal Entry

Cash ....................................................................................... 960,000

Unearned Sales Revenue............................................... 960,000

Adjusting Entry

Unearned Sales Revenue ....................................................... 80,000

Sales Revenue ............................................................... 80,000

($960,000 X 12 = $80,000)

(c) Journal Entry

Cash ....................................................................................... 250,000

Note Payable ................................................................. 250,000

Adjusting Entry

Interest Expense ..................................................................... 1,250

Interest Payable ............................................................. 1,250

([$250,000 X 6%] 12 = $1,250)

(d) Journal Entry

Prepaid Advertising ................................................................. 3,000

Cash ............................................................................... 3,000

Adjusting Entry

Advertising Expense ............................................................... 1,000

Prepaid Advertising ........................................................ 1,000

($3,000X 20 X 60 = $1,000)

(e) Journal Entry

None

Adjusting Entry

Accounts Receivable .............................................................. 14,000

Sales Revenue ............................................................... 14,000

3. Prepare the required end-of-period adjusting entries for each independent case listed below.

Case 1

The Thoma Company began the year with a $3,000 balance in the Supplies account. During the year, $8,500 of additional supplies were purchased. A physical count of supplies on hand at the end of the year revealed that $8,300 worth of supplies had been used during the year. No adjusting entry has been made until year end.

Case 2

The Leno Company has a calendar year-end accounting period. On July 1, the company purchased office equipment for $30,000. It is estimated that the office equipment will depreciate $200 each month. No adjusting entry has been made until year end.

Case 3

Yeats Realty is in the business of renting several apartment buildings and prepares monthly financial statements. It has been determined that 2 tenants in $900 per month apartments and one tenant in the $1,000 per month apartment had not paid their December rent as of December 31st.

Solution

Case 1—December 31

Supplies Expense ............................................................... 8,300

Supplies .................................................................. 8,300

(To record supplies used during the year)

Case 2—December 31

Depreciation Expense......................................................... 1,200

Accumulated Depreciation—Equipment.................. 1,200

(To record depreciation expense for six months)

$200 X 6 months = $1,200 Depreciation

Case 3—December 31

Accounts Receivable .......................................................... 2,800

Rent Revenue ......................................................... 2,800

(To accrue rent recognized but not yet received)

[(2 x $900) + $1,000)]

4. Sunkan Company prepares monthly financial statements. Below are listed some selected accounts and their balances on the September 30 trial balance before any adjustments have been made for the month of September.

SUNKAN COMPANY

Trial Balance (Selected Accounts)

September 30, 2014

____________________________________________________________________________

Debit Credit

Supplies ................................................................................................. $ 2,700

Prepaid Insurance ................................................................................. 4,800

Equipment ............................................................................................. 16,200

Accumulated Depreciation—Equipment ................................................ $ 1,000

Unearned Rent Revenue ....................................................................... 1,200

(Note: Debit column does not equal credit column because this is a partial listing of selected account balances.)

An analysis of the account balances by the company's accountant provided the following additional information:

1. A physical count of office supplies revealed $1,000 on hand on September 30.

2. A two-year life insurance policy was purchased on June 1 for $4,800.

3. Office equipment depreciates $3,000 per year.

4. The amount of rent received in advance that remains unearned at September 30 is $300.

Instructions:

Using the information given, prepare the adjusting entries that should be made by Sunkan Company on September 30.

Solution

1. Supplies Expense ............................................................................ 1,700

Supplies .................................................................................. 1,700

(To record the amount of office supplies used $2,700 – 1,000)

2. Insurance Expense .......................................................................... 200

Prepaid Insurance ................................................................... 200

(To record insurance expired $4,800 24)

3. Depreciation Expense ..................................................................... 250

Accumulated Depreciation—Equipment ................................. 250

(To record monthly depreciation $3,000 12)

4. Unearned Rent Revenue ................................................................. 900

Rent Revenue ......................................................................... 900

(To record rent revenue recognized $1,200 – $300)

5. Prepare year-end adjustments for the following transactions. Omit explanations.

1. Accrued interest on notes receivable is $30.

2. $1,000 of unearned service revenue has been recognized.

3. Three years’ rent, totaling $45,000, was paid in advance at the beginning of the year.

4. Services totaling $2,900 had been performed but not yet billed at the end of the year.

5. Depreciation on equipment totaled $6,500 for the year.

6. Supplies purchased totaled $850. By year end, only $250 of supplies remained.

7. Salaries owed to employees at the end of the year total $960

Solution

1. Interest Receivable........................................................................... 30

Interest Revenue..................................................................... 30

2. Unearned Service Revenue............................................................. 1,000

Service Revenue .................................................................... 1,000

3. Rent Expense ................................................................................. 15,000

Prepaid Rent .......................................................................... 15,000

($45,000X 3 = $15,000)

4. Accounts Receivable..................................................................... 2,900

Service Revenue....................................................................... 2,900

5. Depreciation Expense ................................................................... 6,500

Accumulated Depreciation—Equipment ................................. 6,500

6. Supplies Expense ............................................................................ 600

Supplies .................................................................................. 600

($850 – $250)

7. Salaries and Wages Expense ......................................................... 960

Salaries and Wages Payable ............................................... 960

CHAPTER 5

6. Horner Corporation reported net sales of $150,000, cost of goods sold of $96,000, operating expenses of $35,000, other expenses of $10,000, net income of $9,000. Calculate the following values. 1. Profit margin. 2. Gross profit rate.

Solution

1. Profit margin =Net income

=$ 9,000

= 6 %Net sales $150,000

2. Gross profit rate =Gross profit

=($150,000 - $96,000)

= 36%Net sales $150,000

7. On September 1, Pennington Supply had an inventory of 20 backpacks at a cost of $25 each. The company uses a perpetual inventory system. During September, the following transactions and events occurred.

Sept. 4 Purchased 50 backpacks at $25 each from Sievert, terms 2/10, n/30.

6 Received credit of $100 for the return of 4 backpacks purchased on September 4 that were defective

9 Sold 25 backpacks for $40 each to Lilly Books, terms 2/10, n/30.

13 Sold 15 backpacks for $40 each to Stoner Office Supply, terms n/30.

14 Paid Sievert in full, less discount.

Instructions

Prepare the journal entries for the September transactions for Pennington Supply.

Solution

Sept. 4 Inventory ........................................................................... 1,250

Accounts Payable .................................................... 1,250

6 Accounts Payable ............................................................. 100

Inventory .................................................................. 100

9 Accounts Receivable ........................................................ 1,000

Sales Revenue.......................................................... 1,000

Cost of Goods Sold ........................................................... 625

Inventory .................................................................. 625

13 Accounts Receivable ........................................................ 600

Sales Revenue.......................................................... 600

Cost of Goods Sold ........................................................... 375

Inventory .................................................................. 375

14 Accounts Payable ($1,250 - $100) ................................... 1,150

Cash ($1,150 x .98).................................................. 1,127

Inventory ($1,150 x .02) ............................................. 23

8. Petersen Book Store entered into the transactions listed below. In the journal provided, prepare Petersen’s necessary entries, assuming use of the perpetual inventory system.

July 6 Purchased $1,600 of merchandise on credit, terms n/30.

8 Returned $100 of the items purchased on July 6.

9 Paid freight charges of $90 on the items purchased July 6.

19 Sold merchandise on credit for $4,400, terms 1/10, n/30. The merchandise had an inventory cost of $2,700.

22 Of the merchandise sold on July 19, $300 of it was returned. The items had cost the store $150.

28 Received payment in full from the customer of July 19.

31 Paid for the merchandise purchased on July 6.

Solution

July 6 Inventory 1,600

Accounts Payable……………………………………… 1,600

8 Accounts Payable……………………………………………… 100

Inventory 100

9 Inventory 90

Cash …………………………………………………… 90

19 Accounts Receivable …………………………………………. 4,400

Sales Revenue………………………………………… 4,400

Cost of Goods Sold……………………………………………. 2,700

Inventory 2,700

22 Sales Returns and Allowances……………………………….. 300

Accounts Receivable…………………………………. 300

Inventory 150

Cost of Goods Sold…………………………………… 150

28 Cash ($4,100 x .99) …………………………………………… 4,059

Sales Discounts………………………………………………… 41

Accounts Receivable 4,100

31 Accounts Payable ($1,600 - $100)…………………………… 1,500

Cash 1,500

CHAPTER 6

9. Johnson Company reports the following for the month of June.

Date Explanation Units Unit Cost Total Cost

June 1 Inventory 225 $5 $1,125

12 Purchase 525 6 3,150

23 Purchase 750 7 5,250

30 Inventory 280

(a) Compute the cost of the ending inventory and the cost of goods sold under (1) FIFO, (2) LIFO, and (3) average cost.

Solution (a) (1) FIFO

Beginning inventory (225 $5) ........................................... $1,125

Purchases

June 12 (525 $6) ........................................................ $3,150

June 23 (750 $7) ........................................................ 5,250 8,400

Cost of goods available for sale ........................................... 9,525

Less: Ending inventory (280 $7) ...................................... 1,960

Cost of goods sold ............................................................... $7,565

(2) LIFO

Cost of goods available for sale ........................................... $9,525

Less: Ending inventory (225 $5) + (55 $6).................... 1,455

Cost of goods sold ............................................................... $8,070

(3) AVERAGE COST

Cost of Goods Total Units Weighted Average

Available for Sale ÷ Available for Sale = Unit Cost

$9,525 1,500 $6.35

Ending inventory (280 $6.35) $1,778

Cost of goods sold (1,220 $6.35) $7,747

or $9,525 – $1,778 = $7,747

10. Hansen Company uses the periodic inventory method and had the following inventory information available:

Units Unit Cost Total Cost

1/1 Beginning Inventory 100 $3 $ 300

1/20 Purchase 500 $4 2,000

7/25 Purchase 100 $5 500

10/20 Purchase 300 $6 1,800

1,000 $4,600

A physical count of inventory on December 31 revealed that there were 380 units on hand.

Instructions

Answer the following independent questions and show computations supporting your answers.

1. Assume that the company uses the FIFO method. The value of the ending inventory at December 31 is $__________.

2. Assume that the company uses the average cost method. The value of the ending inventory on December 31 is $__________.

3. Assume that the company uses the LIFO method. The value of the ending inventory on December 31 is $__________.

4. Determine the difference in the amount of income that the company would have reported if it had used the FIFO method instead of the LIFO method. Would income have been greater or less?

Solution

1. FIFO: Ending inventory $2,200

300 units @$6 = $1,800

80 units @$5 = 400

380 units $2,200

2. Average Cost: Ending inventory $1,748

$4,600 1,000 = $4.60 per unit 380 units = $1,748

3. LIFO: Ending Inventory $1,420

100 units @$3 = $ 300

280 units @$4 = 1,120

380 units $1,420

4. FIFO: Cost of goods sold $2,400

100 units @$3 = $ 300

500 units @$4 = 2,000

20 units @$5 = 100

620 units $2,400

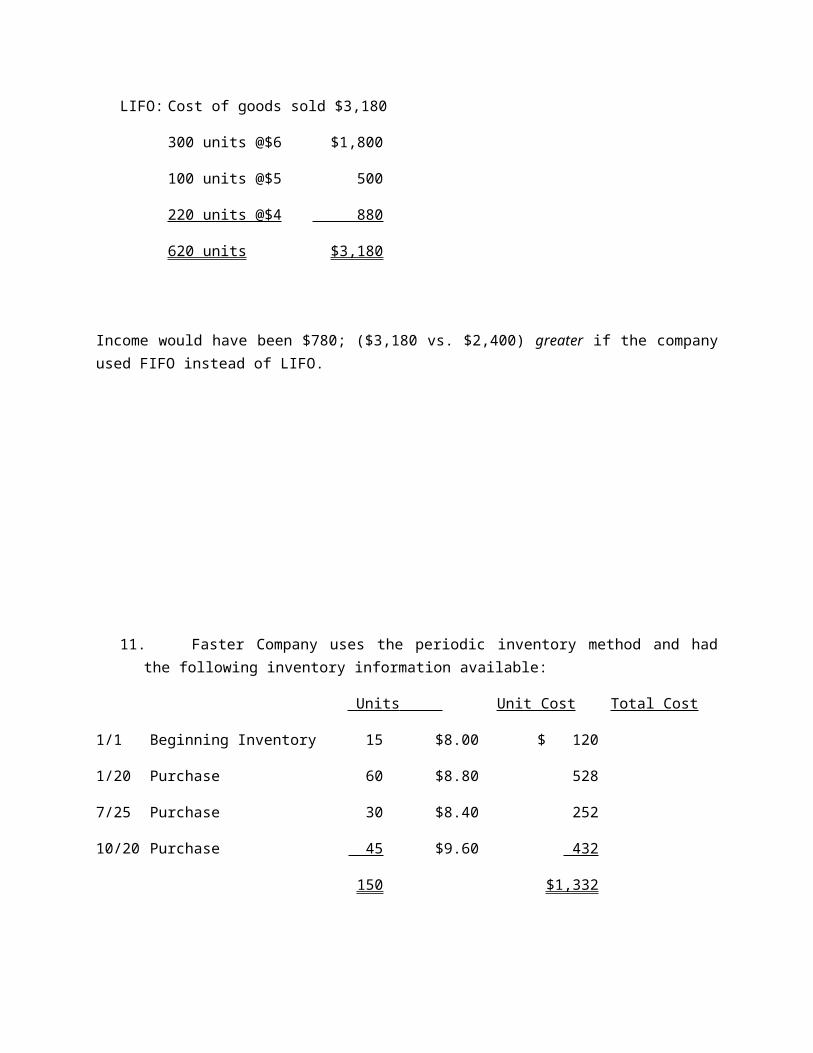

LIFO: Cost of goods sold $3,180

300 units @$6 $1,800

100 units @$5 500

220 units @$4 880

620 units $3,180

Income would have been $780; ($3,180 vs. $2,400) greater if the company used FIFO instead of LIFO.

11. Faster Company uses the periodic inventory method and had the following inventory information available:

Units Unit Cost Total Cost

1/1 Beginning Inventory 15 $8.00 $ 120

1/20 Purchase 60 $8.80 528

7/25 Purchase 30 $8.40 252

10/20 Purchase 45 $9.60 432

150 $1,332

A physical count of inventory on December 31 revealed that there were 55 units on hand.

Instructions

Answer the following independent questions and show computations supporting your answers.

1. Assume that the company uses the FIFO method. The value of the ending inventory at December 31 is $__________.

2. Assume that the company uses the Average Cost method. The value of the ending inventory on December 31 is $__________.

3. Assume that the company uses the LIFO method. The value of the ending inventory on December 31 is $__________.

4. Assume that the company uses the FIFO method. The value of the cost of goods sold at December 31 is $__________.

Solution

1. FIFO: Ending inventory $516

45 units @$9.60 = 432

10 units @$8.40 = 84

55 units $516

2. Average Cost: Ending inventory $488

$1,332 150 = $8.88 per unit 55 units = $488

3. LIFO: Ending Inventory $472

15 units @$8.00 = $ 120

40 units @$8.80 = 352

55 units $472

4. FIFO: Cost of goods sold $816

15 units @$8.00 = $ 120

60 units @$8.80 = 528

20 units @$8.40 = 168

95 units $ 816

12. This information is available for Groneman, Inc. for 2013 and 2014.

(in millions) 2013 2014

Beginning inventory $ 2,290 $ 2,522

Ending inventory 2,522 2,618

Cost of goods sold 24,351 23,099

Sales 43,251 43,232

Instructions

Calculate the inventory turnover, days in inventory, and gross profit rate for Groneman., Inc. for 2013 and 2014.

Solution

2013 2014

Inventory $24,351 $23,099

turnover ($2,290 + $2,522) 2 ($2,522 + $2,618) 2

Ratio

$24,351 = 10.1 times $23,099 = 9.0 times

$2,406 $2,570

Days in 365 = 36.1 days 365 = 40.6 days

inventory 10.1 9.0

Gross $43,251–$24,351 = .44 $43,232–$23,099 = .47

profit rate $43,251 $43,232

13. Dalton Company was undergoing an end of year audit of its financial records. The auditors were in the process of reviewing Dalton’s inventory for year end, December 31, 2014. They completed an end of year inventory. The value of the ending inventory prior to any adjustments was $185,000, but before finishing up they had a few questions. Discussion with Dalton’s accountant revealed the following:

(a) Dalton sold goods costing $60,000 to Summey Company FOB shipping point on December 28. The goods are not expected to reach Summey until January 12. The goods were not included in the physical inventory because they were not in the warehouse.

(b) The physical count of the inventory did not include goods costing $95,000 that were shipped to Dalton FOB destination on December 27 and were still in transit at year-end.

(c) Dalton received goods costing $25,000 on January 2. The goods were shipped FOB shipping point on December 26 by Strong Company. The goods were not included in the physical count.

(d) Dalton sold goods costing $40,000 to Hampton Company FOB destination on December 30. The goods were received by Hampton Company on January 8. Because the goods had been shipped, they were excluded from the physical inventory count.

(e) Dalton received goods costing $42,000 on January 2 that were shipped FOB destination on December 29. The shipment was a rush order that was suppose to arrive December 31. This purchase was included in the ending inventory of $192,000.

(f) Dalton Company, as the consignee, had goods on consignment that cost $3,000. Because these goods were on hand as of December 31, they were included in the physical inventory count.

InstructionsAnalyze the above information and calculate a corrected amount for the ending inventory. Explain the basis for your treatment of each item.

Solution

Start with $185,000

Item (a) – (Because the goods were shipped FOB shipping point title passed to Button upon shipping. Properly excluded.)

Item (b) – (Goods should be excluded. Title does not pass to Dalton until goods are received).

Item (c) +25,000 (Goods belong to Dalton. Title passed when supplier delivered the goods to the transportation company.)

Item (d) +40,000 (Because the goods were shipped FOB destination point Dalton has title to these goods.)

Item (e) –42,000 (Goods were shipped FOB destination. Dalton does not take title until they receive them no matter when expected.)

Item (f) – 3,000 (These goods are owned by the consignor, not the consignee, and should not be included in Dalton's inventory.)

Corrected inventory $205,000

14. The Cain Company has just completed a physical inventory count at year end, December 31, 2014. Only the items on the shelves, in storage, and in the receiving area were counted and costed on the FIFO basis. The inventory amounted to $80,000. During the audit, the independent CPA discovered the following additional information:

(a) There were goods in transit on December 31, 2014, from a supplier with terms FOB destination, costing $10,000. Because the goods had not arrived, they were excluded from the physical inventory count.

(b) On December 27, 2014, a regular customer purchased goods for cash amounting to $1,000 and had them shipped to a bonded warehouse for temporary storage on December 28, 2014. The goods were shipped via common carrier with terms FOB shipping point. The customer picked the goods up from the warehouse on January 4, 2015. Cain Company had paid $500 for the goods and, because they were in storage, Cain included them in the physical inventory count.

(c) Cain Company, on the date of the inventory, received notice from a supplier that goods ordered earlier, at a cost of $4,000, had been delivered to the transportation company on December 28, 2014; the terms were FOB shipping point. Because the shipment had not arrived on December 31, 2014, it was excluded from the physical inventory.

(d) On December 31, 2014, there were goods in transit to customers, with terms FOB shipping point, amounting to $800 (expected delivery on January 8, 2015). Because the goods had been shipped, they were excluded from the physical inventory count.

(e) On December 31, 2014, Cain Company shipped $2,500 worth of goods to a customer, FOB destination. The goods arrived on January 5, 2014. Because the goods were not on hand, they were not included in the physical inventory count.

(f) Cain Company, as the consignee, had goods on consignment that cost $3,000. Because these goods were on hand as of December 31, 2014, they were included in the physical inventory count.

Instructions

Analyze the above information and calculate a corrected amount for the ending inventory. Explain the basis for your treatment of each item.

Solution

Start with $80,000

Item (a) – (Because the goods were shipped FOB destination title will pass to Cain upon arrival. Properly excluded.)

Item (b) – 500 (Goods should be excluded. The customer accepted title when the goods left Cain FOB shipping point.)

Item (c) + 4,000 (Goods belong to Cain. Title passed when supplier delivered the goods to the transportation company.)

Item (d) – (Because the goods were shipped FOB shipping point Cain no longer has title to these goods. Properly excluded.)

Item (e) + 2,500 (Goods were shipped FOB destination. Cain retains title until the customer receives them.)

Item (f) – 3,000 (These goods are owned by the consignor, not the consignee, and should not be included in Cain's inventory.)

Corrected inventory $83,000