mfis refinancing october 2009 by : christine karangwayire brd director of investments department

Post on 21-Dec-2015

215 views

TRANSCRIPT

MFIs REFINANCING October 2009

By : Christine KARANGWAYIRE BRD Director of Investments Department

2

BRD MFIs Refinancing

Introduction

To support Microfinance sector, the GoV established the credit and the capacity building funds. The capacity building fund aims at developing professional management and financial sustainability of Microfinance Institutions. The purpose of the credit fund is to provide sustainable refinancing access to MFIs in form of external lines of credit and enable MFIs access liquidity to invest and obtain earnings. The managing institutions of the capacity building fund are AMIR and CAPMER whereas the managing institution of the credit fund is BRD.

BRD had already identified the refinancing and the capacity building of MFIs as the main pillars in the development of the Microfinance industry. That is why it created a microfinance program according to the decision of its Board meeting held on July 9th 2002.

3

“To become the Government of Rwanda’s investment arm by financing the nation’s development objectives with a focus on the priority sectors of the economy.”

Mobilize financial resources to drive Rwanda’s development

Develop special financing programs for key export sectors

Expand BRD’s product portfolio to meet customers needs

Engage and support key customers and partners

Promote Microfinance Services

Increase BRD’s effectiveness through reconfiguration and

training

MissionMission

Strategic Priorities

Strategic Priorities

VisionVision “To be the most profitable bank at the service of poverty in financing priority sectors of the Rwandan Economy”.

BRD MFI REFINANCING

BRD Vision, Mission and Strategic Priorities

4

LOANS

LEASING

AGENCY FUNCTIONS

GUARANTEE FUND

EQUITY

TRADE FINANCE

MICROFINANCE

ADVISORY SERVICES

BRD Agriculture Financing

BRD New and Old Products

DEPOSIT MOBILISATION

5

A detailed feasibility study or business plan for the A detailed feasibility study or business plan for the projectproject

Proven technical capacity in the field of the project Proven technical capacity in the field of the project

Demonstrated capacity to manage the projectDemonstrated capacity to manage the project

Adequate market share Adequate market share

30-50% participation by promoter of investment 30-50% participation by promoter of investment (15% for cooperatives)(15% for cooperatives)

GE

NE

RA

L

CO

ND

ITIO

NS

Guarantee to secure the loanGuarantee to secure the loan

Interest rate of 10-16%. Interest rate of 10-16%.

Repayment period: Varies and can be up to 10 yearsRepayment period: Varies and can be up to 10 yearsFIN

AN

CIA

L

CO

ND

ITIO

NS

BRD MFI REFINANCING

BRD Lending Conditions

6

Mortgages with title deedsMortgages with title deeds

Pledge of receivables or resourcesPledge of receivables or resources

The joint guarantee of spouse or any other partnerThe joint guarantee of spouse or any other partner

Guarantee fundGuarantee fund

Gu

aran

tees

Accidents and fire insurance, etc..Accidents and fire insurance, etc..

Project financedProject financed

Solidarity guarantee / caution solidaireSolidarity guarantee / caution solidaire

BRD MFI REFINANCING

BRD General Lending Conditions

7

BRD MFI REFINANCING

BRD Experience Financing - Figures

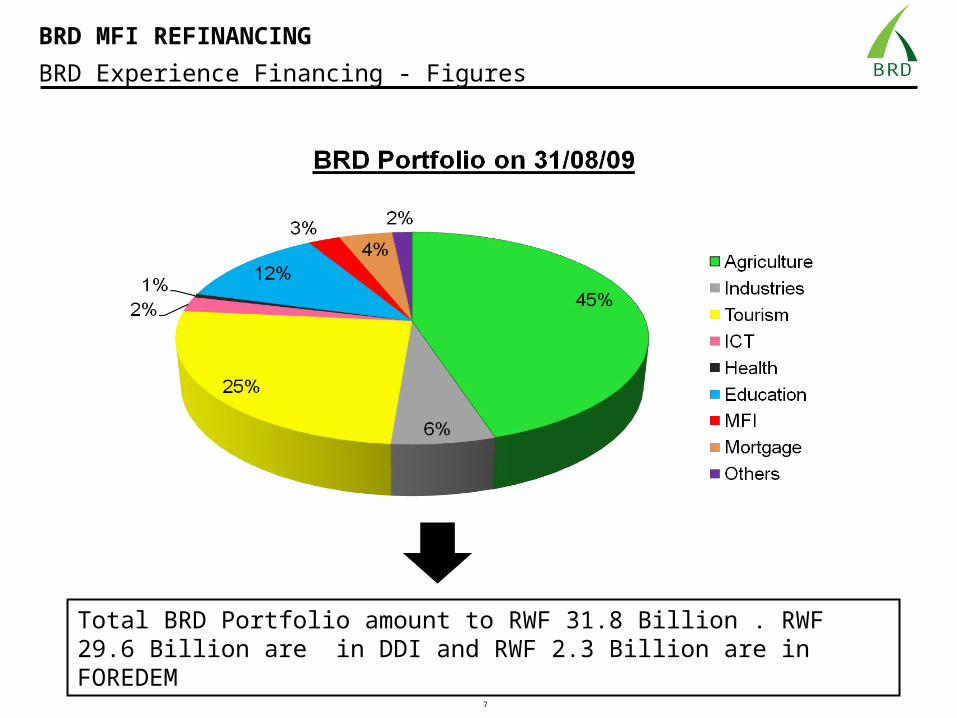

Total BRD Portfolio amount to RWF 31.8 Billion . RWF 29.6 Billion are in DDI and RWF 2.3 Billion are in FOREDEM

8

BRD MFI Refinancing

BRD Experience in MFI Refinancing

Activities Number of

Projects

Value of projects

Comments

Loans applications 22 4 003 717 172

Loans approved 10 1 600 000 000 Loan agreement in process for 2 MFIs

Loans disbursed 8 1 320 000 000Loans rejected 8 2 524 156 400 The reasons of

rejection differ from the institutions to another.

Portfolio as at 31st August 09

8 796 493 030 87% are loan in class 1, 9% in class 2 and 4% in class 4, 3% are in arrears.

Pipeline as at 30th September 09

2 70 000 000

9

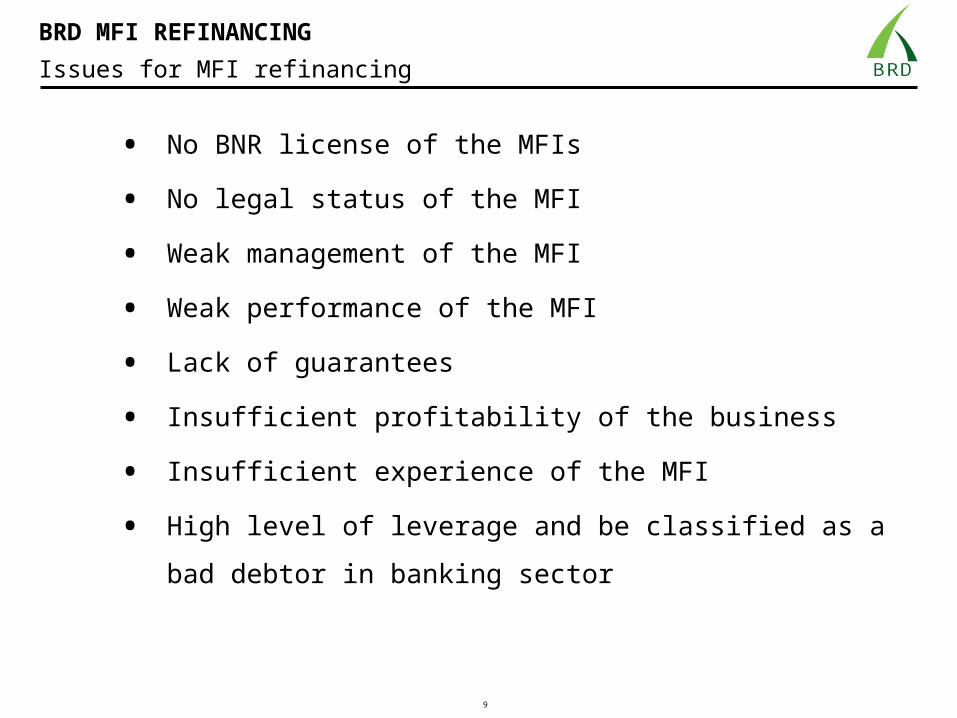

• No BNR license of the MFIs

• No legal status of the MFI

• Weak management of the MFI

• Weak performance of the MFI

• Lack of guarantees

• Insufficient profitability of the business

• Insufficient experience of the MFI

• High level of leverage and be classified as a bad debtor in

banking sector

BRD MFI REFINANCING

Issues for MFI refinancing

10

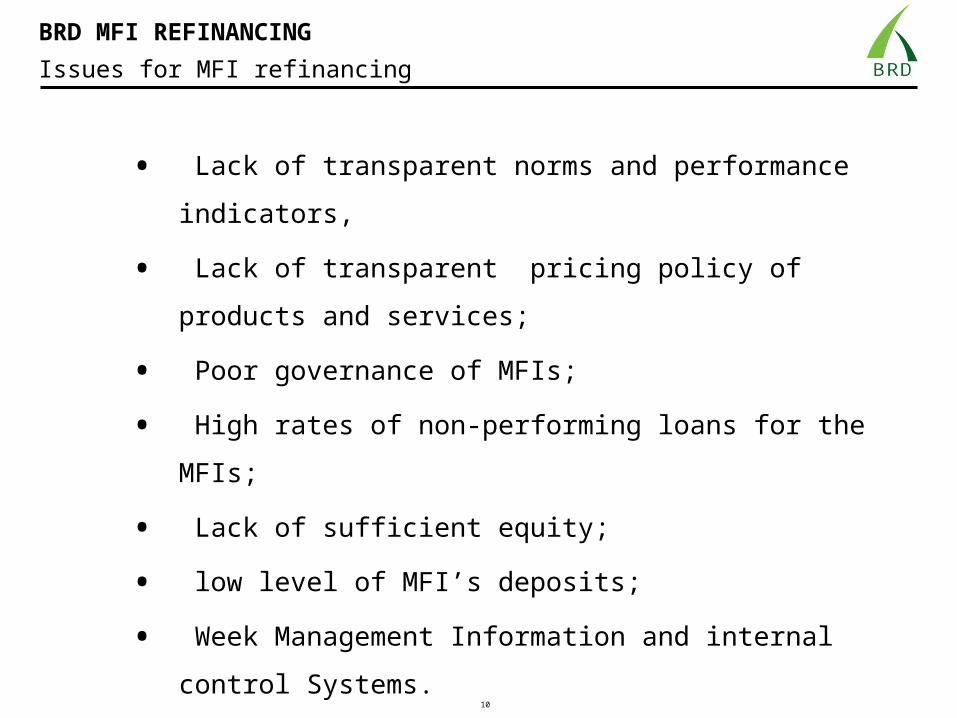

• Lack of transparent norms and performance indicators,

• Lack of transparent pricing policy of products and services;

• Poor governance of MFIs;

• High rates of non-performing loans for the MFIs;

• Lack of sufficient equity;

• low level of MFI’s deposits;

• Week Management Information and internal control Systems.

BRD MFI REFINANCING

Issues for MFI refinancing

11

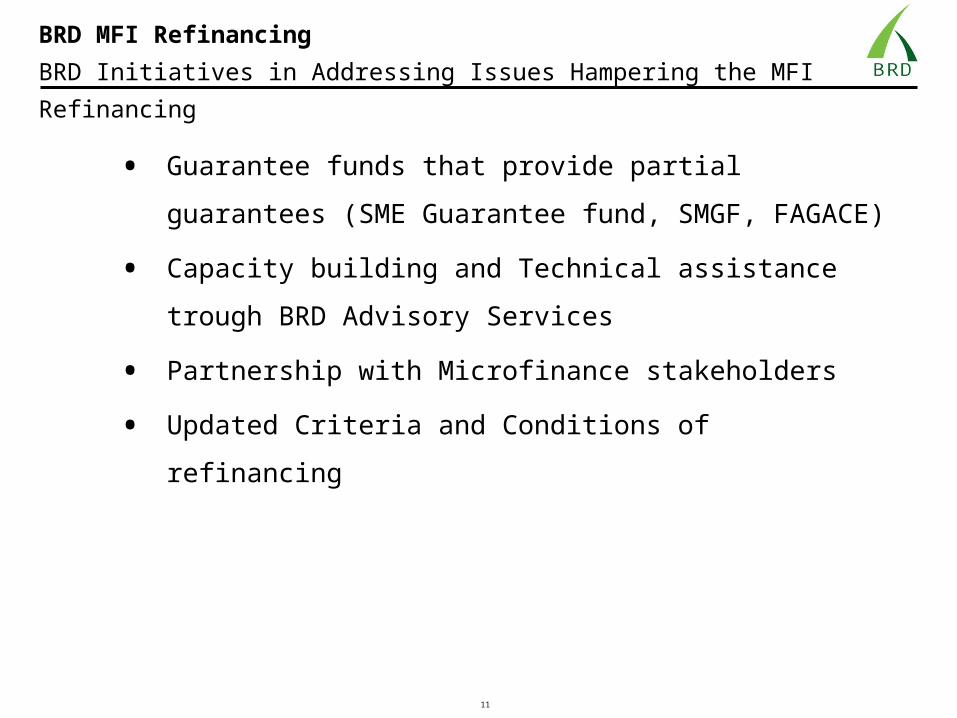

BRD MFI Refinancing

BRD Initiatives in Addressing Issues Hampering the MFI Refinancing

• Guarantee funds that provide partial guarantees (SME

Guarantee fund, SMGF, FAGACE)

• Capacity building and Technical assistance trough BRD

Advisory Services

• Partnership with Microfinance stakeholders

• Updated Criteria and Conditions of refinancing

12

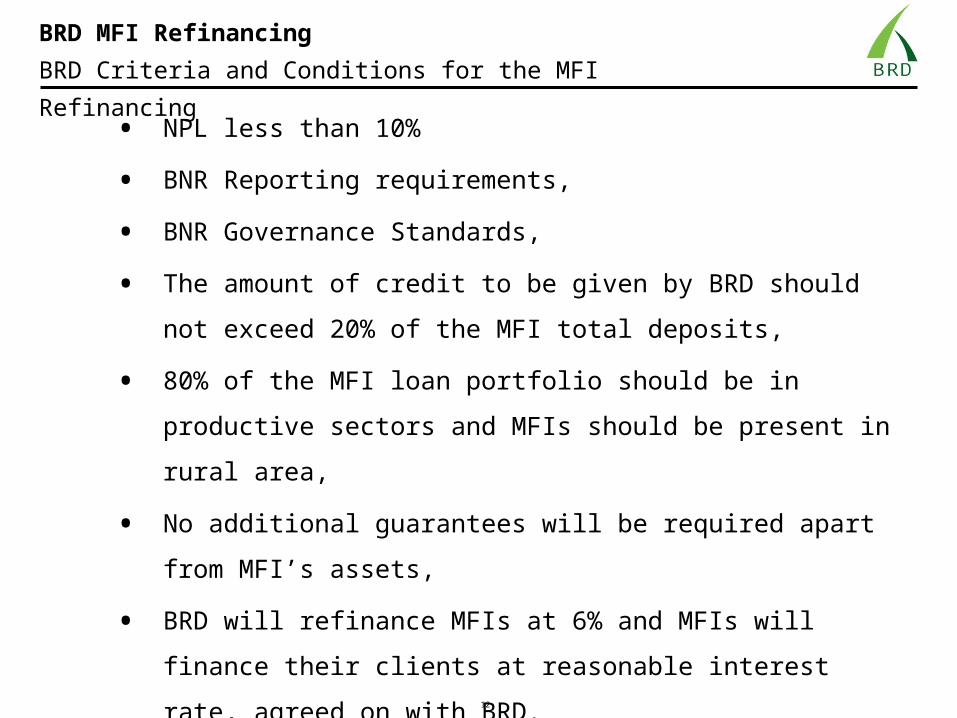

BRD MFI Refinancing

BRD Criteria and Conditions for the MFI Refinancing

• NPL less than 10%

• BNR Reporting requirements,

• BNR Governance Standards,

• The amount of credit to be given by BRD should not exceed 20%

of the MFI total deposits,

• 80% of the MFI loan portfolio should be in productive sectors and

MFIs should be present in rural area,

• No additional guarantees will be required apart from MFI’s assets,

• BRD will refinance MFIs at 6% and MFIs will finance their clients

at reasonable interest rate, agreed on with BRD.

NB: Microfinance Banks are excluded from eligible MFIs to be refinanced, they have access to other resources,

13

BRD MFI Refinancing

Documents to presents when requesting refinancing

• Application letter

• BNR License

• BNR’s report for 3 quarters

• Legal Status ( Ubuzima gatozi)

• Business Plan for 5 years,

• Audited Financial statements for 3 years,

• Portfolio and loan aging reports,

• Credit Policy,

• Memorandum and articles of association( statuts)

14

THANK YOU !!THANK YOU !!

QUESTIONS, COMMENTS QUESTIONS, COMMENTS ??