merrill lynch conference - aviva plc · merrill lynch conference ... with dabur group from june...

TRANSCRIPT

Richard HarveyGroup Chief Executive

Merrill Lynch conference“Living in a 1% world”8 October 2003

© Aviva plc

Disclaimer

This presentation may contain certain “forward-looking statements” with respect to certain of Aviva’s plans and its current goals and expectations relating to its future financial condition, performance and results. By their nature, all forward-looking statements involve risk and uncertainty because they relate to future events and circumstances which are beyond Aviva’scontrol including among other things, UK domestic and global economic business conditions, market related risks such as fluctuations in interest rates and exchange rates, the policies and actions of regulatory authorities, the impact of competition, inflation, deflation, the timing impact and other uncertainties of future acquisitions or combinations within relevant industries, as well as the impact of tax and other legislation and other regulations in the jurisdictions in which Aviva and its affiliates operate. As a result, Aviva’sactual future financial condition, performance and results may differ materially from the plans, goals and expectations set forth in Aviva’s forward-looking statements.

Aviva undertakes no obligation to update the forward-looking statements contained in this presentation or any other forward-looking statements we may make.

2

© Aviva plc

Aviva in a “1% world”

• Long-term savings:

– Investing for higher growth and margin

– Low unit costs key to new business margins

• General insurance:

– Invest for superior claims performance

– Cost reduction

• Allocate capital to higher growth and margin businesses

3

© Aviva plc

Investing in high growth opportunitiesInvesting in high growth opportunities

Spain: created leading life business Singapore & HK:

bancassurance with DBS

UK: bancassurance JV

with RBOS

France: bancassurance from 2004 China:

JV life business from 2003Italy: created top

6 life business

Netherlands:bancassurance JV with ABN AMRO

EnteredLithuania life from Poland

India: bancassurance and DSF from 2002

4

© Aviva plc

0

150

300

450

2000 2001 2002 H1 2003

Aviva bancassurance life & pension sales£m

+56% vs HY 2002APE

Aviva bancassurance in H1 2003(25% of total life & pensions sales)

• Early phase of development (most deals post 2000)• But expertise back to 1989 with UniCredito• Margins 35.5%………. vs group average of 24.5%

HY

HY

FY

FY

FY

HY

5

© Aviva plc

Leading cost positions in Italy & SpainLeading cost positions in Italy & Spain

Source: ANIA

ItalyExpense as % premiums, 2001

ConsolidatedAviva life

companies

Top 15Italian life

companies

• One “factory” leads to scaleable cost advantages

Source: ICEA, data regarding H102

SpainExpenses as % of premiums, H102

0

1

2

3

4

5

Aviva(Aseval)

TotalSpanish

life market

% %

0

1

2

3

4

5

6

© Aviva plc

AvivaAviva in Eastern Europein Eastern Europe“Asia on our doorstep”“Asia on our doorstep”

7

Czech Republic•Population: 10m•Life = 1.31% of GDP •Launched 1997 Turkey

•Population: 65m•Life = 0.25% of GDP•Life launch 1996•15% market share, No.1

Hungary•Population: 10m•Life = 1.16% of GDP•Acquisition of Top-6

life assurer 2001

Lithuania•Population: 4m•Life = 0.30% of GDP•Launched 2001•11% market share, No. 4

Romania•Population: 22m•Life = 0.18% of GDP•Launched 2000, top 5

Poland•Population: 39m•Life = 1.07% of GDP•1992 £5m greenfield investment•In 2002:

•No 1 private Pensions (29% of market)•18% of total life market•40% of individual life•Over 3m customers

© Aviva plc

• India

• JV partnership (26%) with Dabur Group from June 2002

• Distribution agreements provide access to over 25 million potential customers:

– Canara Bank (ranked 2nd with 2,400 branches)– Lakshmi Vilas Bank (regional bank, 209 branches)

– ABN AMRO– American Express

China

– Aviva-COFCO Life Insurance launched 1 Jan 2003

– Initially operating in Guangzhou

India & China growth opportunitiesIndia & China growth opportunities

8

© Aviva plc

UK life:

• Norwich Union is the market leader

• Market share 1996 5.2% 11.8% H1 2003

• Capital advantage including orphan estate estimated at £4.5bn (30.6.03)

• Market leading product range

• Multi-distribution expertise in place

• Pricing increases

• Management actions to reduce expenses

9

© Aviva plc

Future of UK life with-profits

10

• Smoothed investment philosophy remains attractive

• With-profits has outperformed equity-linked!

• Sandler supports concept

• Consolidation around few providers with strong estates

– 40 out of 62 WP funds closed in last 2 years

© Aviva plc

Where 1% charge in the UK is profitable

• 1% charge can work where case premiums are large and persistency is high

• Cat standard ISAs (max charge 1%) unsuccessful

– Similar to “Sandler” proposed products

• Larger end of 1% pensions market is profitable

– Includes Group schemes (fee basis)

– Aviva structures its commission rates to avoid unprofitable segments

11

© Aviva plc

UK life price cap decides reachable market

* Individual cases

Source:Oliver Wyman research using regular premium contracts

Bank Worksiteenrollers

Direct sales force

IFAs0

100200300400500

600700800900

Breakeven case size by distribution channel*

£APE

Reduction in yield

1%

1.5%

12

© Aviva plc

General insurance: Strong statutory General insurance: Strong statutory earnings support longerearnings support longer--term life growthterm life growth

*Continuing operations

5877713

Combined operating ratios6months

2003 2002

UK 99% 101%

France 100% 100%

Ireland 97% 100%

Neths 98% 102%

Canada 115%** 103% (** Pilot added 13pp)

Group* 101% 101%

% of total* GI premiums

Group 99%(excl Pilot)

13

© Aviva plc

Pricing environment

• Orderly pricing market

14

Lower inv return from bonds vs equities

Credit rating agencies

Balance sheet

disciplines

DisciplineNever been so little capital in general insurance

market at this point of the pricing cycle

© Aviva plc

Expense ratio benefiting from merger Expense ratio benefiting from merger savings and ongoing efficiency reviewssavings and ongoing efficiency reviews

*Continuing operations

Aviva general insurance expense ratio*

10

11

12

13

12m2000

12m2001

12m2002

6m 2003

%

15

© Aviva plc

Leveraging cost advantage out of Aviva’sgrowing expertise in India

• Call centre / claims processes supports UK general insurance capacity and efficiency

• Live from July 2003 (1,000 jobs by end 2003)

• Consider other applications

Virtual callcentre/claims

processes

1,000employeesend 2003

16

© Aviva plc

Investing in superior claims performanceInvesting in superior claims performance

Expense ratio

Claims costs

• Re-underwritten portfolios

• Total incident management

• India claims processing

• Pay As You Drive pilot

• Digital flood mapping

Commissions UK

17

© Aviva plc

Digital flood mapping

Aeroplane digitally mapped height of UK

Add data on river water flows and soil moisture

Captured flood risk data on every house

+

=

18

© Aviva plc

Shrewsbury: Upper Severn Catchment

1 in 100 year flood outline

SH

19

© Aviva plc

SY3 7 (postcode)

Previously, all properties thought to flood

20

© Aviva plc

SY3 7 (postcode)

Properties that flood

Only 28% of properties in this postcode flood

Properties that don’t flood

21

© Aviva plc

Flood mapping benefits

• Underwrite more accurately than competitors

– Avoid vulnerable properties

– Estimated saving of £80m (of £195m) from UK floods in 2000

• Reduce earnings volatility

• Underwriting data advantage across all of book

22

© Aviva plc

Aviva cost saving initiatives in first half 2003

• Estimated P&L net benefit of £60m for 2003

– after cost to achieve saves and incremental investment spend on GFTP and offshoring

– includes cost of UK job reduction of 1,600 announced to July 2003

• Estimated full year 2004 P&L gross benefit of £175m

– will be offset by inflation and £40m incremental GFTP spend

23

© Aviva plc

Aviva summary

• Geographical choice for capital allocation

• Scale advantages

• Reducing costs

• Gaining market share in profitable life markets

• Targeting consistent across cycle earnings from general insurance

• ROCE 11% for 6m 2003 (9.7% 12m 2002)24

© Aviva plc

Appendix

25

© Aviva plc

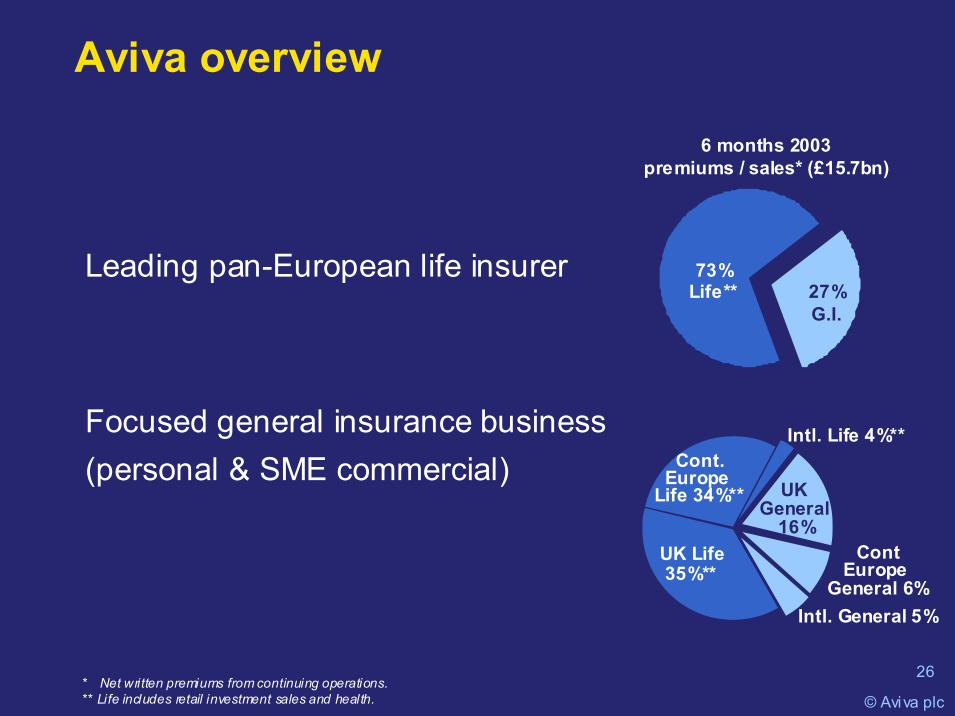

Aviva overview

• Leading pan-European life insurer

• Focused general insurance business (personal & SME commercial)

72%Life*

6 months 2003 premiums / sales* (£15.7bn)

* Net written premiums from continuing operations. ** Life includes retail investment sales and health.

72%Life*

Cont.Europe

Life 34%**

UK Life35%**

UK General

16%Cont

Europe General 6%

Intl. General 5%

Intl. Life 4%**

73%Life** 27%

G.I.

26

© Aviva plc

Valuable business franchises from Valuable business franchises from strong market positionsstrong market positions

RankLife

Market shareLife (est.)

RankGI

Market shareGI (est.)

UK 1 12% 1 14%France 10 4% Top 15 2.5%Netherlands 4 10%* 3 9%*Spain 1 12% - -Italy 6 5% n/a <1%Ireland 4 11% 1 24%Canada - - 2 9%Poland 2 18% - -Singapore 3 11% 2 9%Turkey 1 15% - -Australia Top 10 4% - -

* 2001 pro forma ABN AMRO Joint Venture27

© Aviva plc

Capital: resilient position

• Enhanced by sub-debt issue of £1.6bn Sept 2003

• Self financing model

– strong statutory profits from general insurance– 2002 dividend cut

• Resilient CGUII structure (holds major overseas subs)

– can withstand significant equity market falls

• Strong UK life with-profit “realistic” capital

– orphan estate £4.5bn(after >£4bn for guarantees, glidepath etc…)

– manage bonuses / MVAs / asset mix (36% equities) 28