mena weekly monitor (46) 13-11-2015 - …images.mofcom.gov.cn/lb/201511/20151118184502796.pdfey said...

TRANSCRIPT

1Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

Bank Audi sal - Group Research Department - Bank Audi Plaza - Bab Idriss - PO Box 11-2560 - Lebanon - Tel: 961 1 994 000 - email: [email protected]

CONTACTS

RESEARCH

Treasury & Capital Markets

Bechara Serhal(961-1) [email protected]

Nadine Akkawi(961-1) [email protected]

Private Banking

Toufic Aouad(961-1) [email protected]

Corporate Banking

Khalil Debs(961-1) [email protected]

Marwan Barakat(961-1) [email protected]

Jamil Naayem(961-1) [email protected]

Salma Saad Baba(961-1) [email protected]

Fadi Kanso(961-1) [email protected]

Sarah Borgi(961-1) [email protected]

Gerard Arabian(961-1) [email protected]

Farah Nahlawi(961-1) [email protected]

Nivine Turyaki(961-1) [email protected]

MENA MARKETS: WEEK OF NOVEMBER 08 - NOVEMBER 14, 2015

The MENA WEEKLY MONITOR

Economy___________________________________________________________________________p.2 EFG HERMES SAYS STRONG US DOLLAR COULD AMPLIFY THE STRESSES ON MENA ECONOMIESEFG Hermes recently released a report on the MENA region, arguing that the steep appreciation of the US dollar since June 2014 has repercussions for the external accounts of MENA economies.

Also in this issuep.3 S&P revises Egypt outlook to stable on potential decrease in GCC support p.4 UAE central bank expects slower economic growth in 2015

Surveys___________________________________________________________________________p.5 91 ANNOUNCED M&A DEALS AT US$ 5.4 BILLION IN Q3-15, AS PER EYEY said deal activity in the MENA region decreased by 13% from 104 deals in Q3-14 to 91 deals in Q3-15.

Also in this issuep.5 Middle Eastern property investments outside the region up by 64% in 1H15, as per CBREp.6 UAE home to a number of success stories in FinTech and innovation, as per Strategy &

Corporate News___________________________________________________________________________p.7 DUBAI BUILDER ARABTEC SUBMITS PROPOSAL TO EGYPT'S GOVERNMENT TO CONSTRUCT 13,000 HOMES Dubai builder Arabtec submitted a proposal to Egypt's government to construct 13,000 homes in the North African country, as per the firm's Chairman.

Also in this issuep.7 UAE's Dana Gas plans further cost cuts amidst low oil prices p.7 Hill International wins Oman airport contract extension p.7 Qatar-based broadcaster BeIN Media Group in talks to acquire the Miramax film company p.8 NMC Health withdraws bid for rival Al Noor Hospitals due to valuation concerns p.8 Mumtalakat buys 49% stake in Spain’s Aleastur p.8 Petrofac wins contract by Saudi Aramco for engineering, procurement and construction of a Sulphur recovery plant p.8 Ducab wins US$ 130 million orders from oil and gas firms in Abu Dhabi and Kuwait p.8 Majid Al Futtaim to open shopping centre in Riyadh and seeks expansion in other Gulf markets

Markets In Brief___________________________________________________________________________p.9 WEAK OIL PRICES CONTINUE TO WEIGH ON REGIONAL CAPITAL MARKETSMENA equity markets continued to follow a downward streak this week, as reflected by a 0.4% decrease in the S&P Pan Arab Composite Index, mainly driven by falling oil prices and some unfavorable financial results. The Egyptian Exchange led the decline (-7.4%), followed by the Qatar Exchange and the UAE equity markets (-4.9% each), while the heavyweight Saudi Tadawul posted a 1.8% increase in prices. Also, regional bond markets saw extended price declines across the board, within the context of weaker investor sentiment and thinner liquidity driven by an oil price slump, and tracking declines in US Treasuries amidst bets the US Fed would raise its benchmark interest rate before year-end 2015.

2Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

ECONOMY______________________________________________________________________________EFG HERMES SAYS STRONG US DOLLAR COULD AMPLIFY THE STRESSES ON MENA ECONOMIES

EFG Hermes recently released a report on the MENA region, arguing that the steep appreciation of the US dollar since June 2014 has repercussions for the external accounts of MENA economies. The extent and nature of the impact is mostly contingent on the country’s choice of exchange rate regime.

Countries with US dollar pegs are the most vulnerable to unfavorable movements in the current and financial accounts of their balance of payments. These effects may be reflected in external data with a lag and so are difficult to quantify, according to the same source.

The drop in the oil price from the highs seen in June 2014 coincided with a strengthening of the US dollar by 13% year-on-year in November. The US dollar could rise further into 2016 once the US Federal Reserve begins to raise interest rates, as per EFG Hermes analysts. Meanwhile, this could precipitate further declines in the oil price, compounded by the oil supply glut in international markets.

A strong US dollar could be bad news for the GCC at this time. As a matter of fact, EFG Hermes believes that at a time of lower growth prospects and policy uncertainty, coupled with tightening fiscal and monetary conditions in the GCC, the strong dollar poses additional problems for GCC economies.

Theoretically, this can materialize through two tracks as per EFG Hermes: first, a loss of competitiveness which affects the non-oil goods trade balance and the ability to attract foreign direct investment inflows; and/or second, higher purchasing value of domestic currency abroad which may encourage capital outflows as residents diversify their holdings internationally at a time when economic opportunities at home seem less certain.

EFG Hermes yet argues that for other pegged non-GCC economies, it is a relief. The combination of a strong dollar and weak commodity prices is positive news for Jordan and Lebanon as it greatly alleviates pressure on the twin deficit amidst general economic weakness. Risk of capital outflows persists given the stronger purchasing power, though the risk is lower than in the GCC due to limited inflows in the first place and a relatively smaller wealth base.

REAL GDP GROWTH EVOLUTION FOR COVERED MENA COUNTRIES

Source: EFG Hermes

3Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

Egypt would face further pressure to devalue, as per the same source. A stronger dollar only adds to the pressure on the Egyptian pound to weaken further. The considerable depreciation of the Euro versus the US dollar (bearing in mind that the Euro Area is Egypt’s largest trading partner) has exacerbated the loss of competitiveness which was already being driven by the notable inflation differential between Egypt and its trading partners. EFG Hermes analysts estimate the real effective exchange rate has appreciated by 28% since 2011 despite a loss of nearly a third in nominal terms in the USD-EGP exchange rate.

As to oil prices, EFG Hermes views them as lower for longer, and revised down its base case scenario for oil prices to an average of US$ 55 per barrel next year and to US$ 60 per barrel in 2017. EFG Hermes analysts expect the oil supply glut to continue to weigh on prices and for the oil market rebalancing to be delayed until 2017. _____________________________________________________________________________S&P REVISES EGYPT OUTLOOK TO STABLE ON POTENTIAL DECREASE IN GCC SUPPORT

S&P has recently lowered Egypt’s credit rating outlook from positive to stable, while affirming its “B-/B” long- and short-term foreign and local currency ratings. The cut in the credit outlook comes on expectations that Egypt may receive reduced financial support from the GGC states.

The outlook revision reflects the rating agency’s view that the economic recovery will not outperform its previous expectations, with GDP growth projected at 4.0% on average over the next three years. It also believes that Egypt's external imbalances will persist, with gross external financing needs exceeding 100% of the country's current account receipts and usable reserves in the next few years. The strong external support that Egypt has received over the past few years could be affected by fiscal pressures in GCC countries. In S&P’s view, economic growth will be supported by broad political stability, alongside policymakers' commitments to embark on a new round of economic and fiscal reforms. The new fiscal reforms include measures on both the expenditure and revenue sides, such as the wage reform and the more recently introduced VAT system on goods and services. According to S&P, Egypt needs also to address bottlenecks and structural shortcomings in the energy and the foreign exchange markets. S&P’s ratings on Egypt remain constrained by wide fiscal deficits, high domestic debt, low income levels, and institutional and social fragility. Although the rating agency expects GCC states to continue to provide financial and economic assistance to Egypt in the form of direct investment, participation in new projects, and concessional loans to purchase petroleum products, given Egypt's strategic importance in the region and in present-day conflicts in the Middle East, it also expects that fiscal pressures in GCC countries could affect such support, in particular the level of grants.

S&P projects Egypt's real GDP growth to accelerate to 4.2% in 2015, which represents a significant rebound from the average 2.1% recorded in 2011-2014. The economic recovery is supported by improved political conditions, a recovery in construction, manufacturing, services and tourism, and came off a low base recorded during the 2011-2014 political turmoil. S&P projects Egypt's economic growth to remain at about 4% per year on average in 2016-2018, supported by domestic consumption and investment. Also, it expects Egypt to continue to benefit from resilient remittances from Egyptians working abroad and from inward foreign investment. In S&P’s view, Eni's discovery of "Zohr", a natural gas field offshore of Egypt, could support growth through investment in the oil and gas sector, and could improve the country's energy and trade imbalances in the medium term. Moreover, improving demand from Europe and a depreciating currency should help exports to recover over the medium term.

Saudi Arabia, the UAE, Kuwait, and Oman pledged US$ 12.5 billion in assistance to Egypt in early 2015. They have already provided substantial financing, totaling almost US$ 25 billion over the past three years. At the end of April 2015, the Central Bank of Egypt received US$6 billion in deposits from the GCC states, which helped increase Egypt's foreign currency reserves to just above US$ 20 billion as of June 30, 2015. Nevertheless, Egypt's international reserve position has since weakened to US$ 16 billion, partially due to the redemption of US$ 2.3 billion in external debt. The current level of foreign currency reserves represents a limited buffer to absorb any further downward pressure on the Egyptian pound, in S&P’s view.

4Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

In short, the stable outlook reflects S&P’s expectation that Egypt will largely remain politically stable, and its economy will continue to progressively grow in the face of important macroeconomic headwinds. The stable outlook also reflects S&P’s view that fiscal deficits will improve, but remain at high levels. The rating agency could raise its ratings on Egypt if the economic recovery outperformed its current expectations, or if narrower-than-expected current account deficits lead to a stronger external position. It could lower the ratings if fiscal or external indicators were to deteriorate significantly, or if Egypt's fiscal funding options were to deteriorate. _____________________________________________________________________________UAE CENTRAL BANK EXPECTS SLOWER ECONOMIC GROWTH IN 2015

The UAE central bank has recently expected that economic growth to slow to 3% this year from 4% last year, as the weaker oil price hits investment.

In the central bank’s governor words, it is arguable that for governments like the UAE, maybe it’s an opportune time to execute projects at a lower cost. Accordingly, the UAE will continue necessary projects but would try to reduce unnecessary costs as the economy slows.

The slump in oil, which has shed more than half of its value in the past year amid an increase in production from North America and a decrease in demand from big guzzlers such as China and other emerging markets, has been the main driver behind the slowdown of the UAE’s economic growth. The latter is the sixth-largest producer of oil and uses revenue from crude sales to fund more than 60% of its federal budget.

As to UAE banks, they are becoming increasingly risk-averse when weighing loans to businesses. Still, according to the central bank, loan books are growing, with the average capital adequacy ratio for the banking sector hovering at around 18%, well above regulatory requirements. Indeed, thanks to a satisfactory, albeit tightening liquidity situation, the UAE banking sector was able to expand credit despite a noticeable slowdown in deposit growth. Still, the Central Bank said last month that loan growth slowed to an annual 7% in September from 8.6% in August, the slowest rate of growth since February last year. As a result, many bank chiefs expect loan growth to cool next year. For instance, the National Bank of Abu Dhabi expects UAE loan growth to rise by about 5% next year, nearly half the expansion rate over the past few years.

On another level, the central bank said that interest rates on deposits would rise if the US Federal Reserve started raising interest rates after a stretch of seven years of low rates, as is widely expected to happen soon. However, rates at local banks are already rising not because of liquidity, but because the expectations that the Fed will increase rates are already in the system. Moreover, the UAE dirham is pegged to the US dollar and broadly follows the monetary policy of the US Fed. The central bank reiterated its stance on the peg amid concern by some observers that the dirham may be overvalued because of the strengthening greenback.

5Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

SURVEYS_____________________________________________________________________________91 ANNOUNCED M&A DEALS AT US$ 5.4 BILLION IN Q3-15, AS PER EY

According to EY’s Q3 MENA M&A Update, announced deal activity in the MENA region decreased by 13% from 104 deals in Q3-14 to 91 deals in Q3-15. Deal value also declined from US$ 8.5 billion in Q3-14 to US$ 5.4 billion in Q3-15, a drop of 37%.

Moreover, EY’s latest bi-annual MENA Capital Confidence Barometer (CCB) infers quiet confidence in the regional and global economic outlook, despite the continued pressure on oil price through 2015. Optimism about economy prospects in MENA appears to have firmed since April 2015.

In fact, the CCB survey finds that 18% of MENA respondents believe that the regional economy is on a strong recovery path, up from the 6% who believed so in April 2015. There is an underlying sense that executives believe that the hydrocarbon-dependent economies have been able to weather the storm. Governments appear to be committed to key projects, and most have sufficient reserves to run deficits for a few years yet, as per EY.

The M&A update shows increased cross-border M&A activity in the MENA region. Indeed, combined outbound and inbound deal activity in MENA showed an increase of 40% from 45 deals in Q3-14 to 63 in Q3-15. Domestic announced deal activity on the other hand decreased from 59 deals in Q3-14 to only 28 deals Q3-15. As to the main sectors for cross-border deals, the three main ones were chemicals, consumer products, and healthcare.

According to EY, it is clear that the recent macro-economic uncertainties and the extended summer and other holidays in the region have had an effect on domestic deal activity in Q3-15. However, there is compelling evidence that the MENA deal pipeline remains robust; 71% of MENA respondents expected their deal pipeline to increase in the coming year, compared to 56% in April 2015. The most marked improvement was in the UAE, where 70% of respondents saw the deal pipeline improving, compared to 14% in April 2015.

The CCB survey also shows that the allocation of capital in the oil and gas sector has clearly moved from upstream to downstream. EY expects to see many more petrochemical deals in 2015.

As to destinations’ attractiveness, Egypt has emerged as an attractive destination for foreign investors over the past year. These acquisitions in Egypt underline a greater readiness among foreign companies to conceive inorganic growth as the best approach in getting a foothold in an important growth market with favorable demographics.

According to the CCB survey, Egypt, as a net oil importer, has clearly benefited from the weaker oil prices with a robust 4.2% GDP growth rate in the year to June 2015. That has fed into a sizeable increase in the numbers of Egypt-based respondents who see the local economy as modestly improving, rising from 27% six months ago to 47% in October 2015. _____________________________________________________________________________MIDDLE EASTERN PROPERTY INVESTMENTS OUTSIDE THE REGION UP BY 64% IN 1H15, AS PER CBRE

According to CBRE, the value of Middle East investments in real estate outside the region surged by 64% to US$11.5 billion in the first half of 2015.

It is noteworthy to mention that two deals by sovereign funds accounted for nearly half this year’s total. The CBRE said sovereign wealth funds accounted for US$8.3 billion of the spending in the first six months of this year, almost quadruple their outlay of US$2.27 billion in the prior-year period. The splurge came despite a 44 % drop in U.S. light crude oil prices in the 12 months to June 30. Property purchases by non-sovereign wealth funds fell to US$3.2 billion in the first half of 2015, from US$4.7 billion a year earlier, according to Reuters calculations based on CBRE data.

6Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

In CBRE’s view, the size of the region’s foreign investment makes the Middle East the third-largest source of cross regional capital globally as Arab investors look for brighter investment prospects internationally.

These deals helped make London, with US$2.75 billion, and Hong Kong, with US$2.4 billion, the top destinations for Middle Eastern property investors. New York was third with US$1.1 billion and Milan’s US$990 million placed it fourth. This year’s spending includes Qatar’s US$ 2.5 billion investment in Melbourne Hotels and Abu Dhabi Investment Authority’s (ADIA) US$ 2.4 billion purchase of a 50% stake in three Hong Kong hotels.

In terms of sectors, hotel investments rose 437% to US$6.75 billion, or 59% of total Middle East spending. According to CBRE, this category is growing in importance as sovereign wealth funds and high-net-worth individuals focus on real assets that generate long-term revenue. In parallel, office acquisitions fell by nearly half to US$1.99 billion and retail purchases dropped 40% to US$708 million. Other buys, which include residential property, jumped 144% to US$1.66 billion._____________________________________________________________________________UAE HOME TO A NUMBER OF SUCCESS STORIES IN FINTECH AND INNOVATION, AS PER STRATEGY &

According to Strategy&’s “Developing a FinTech ecosystem in the GCC” study, the GCC has a strong foundation to develop a vibrant financial technologies (FinTech) sector. Little investment has been made in FinTech to date across the region, however Strategy& predicts this will likely change.

Today financial technologies in the GCC still face obstacles to development and many financial e-services and digitized financial interactions have stalled. Despite these challenges, critical success factors for developing a healthy FinTech environment exist, such as government driven funding programs and the financial advisory services necessary for technology start-ups to sustainably grow.

According to the study, in order to capitalize on this potential governments and financial institutions must take aligned steps to further develop the region’s FinTech sector. According to Strategy&, the role of GCC governments is more critical than it is in established markets to help better establish FinTech. GCC governments must enforce policies and a regulatory environment that will ease the development of FinTech. This will eventually attract more talent to the region, boost entrepreneurial and business activities, and most importantly improve the country’s overall competitiveness.

As per Strategy&, there are already some success stories in the GCC, particularly in the UAE, where incubators and innovation hubs are supporting the creation and growth of digital enterprises. The UAE Academy, for example, aims to stimulate enterprise in the country by increasing awareness of entrepreneurship. FinTech start-ups, government backing, and support programs are creating pockets of innovation across the UAE.

In the less-mature FinTech environments, such as Saudi Arabia and Jordan, governments must be heavily involved to regulate, set policies and provide the necessary infrastructure so that the industry can grow sustainably. The UAE’s approach to developing a healthy and sustainable FinTech environment could potentially be considered in other GCC nations and help them to grow their own FinTech industries.

According to Strategy&, GCC governments, particularly the UAE’s, can encourage a region-wide FinTech ecosystem by connecting a multitude of different stakeholders to support innovation. If the region can rise to this challenge, the rewards for the financial industry and the broader regional economy could be significant.

Moreover, the study estimates that the global investment in FinTech has jumped three-fold between 2008 and 2014, reaching US$ 3 billion, and is expected to double again by 2018, and may even hit US$ 8 billion.

On a final note, the study mentions that most FinTech investment is currently in the U.S., which captures about 80% of this spending, however meaningful innovation is also occurring in the European Union, particularly in the U.K. Although relatively little FinTech investment has occurred in the GCC to date, that could and should change.

7Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

CORPORATE NEWS_____________________________________________________________________________DUBAI BUILDER ARABTEC SUBMITS PROPOSAL TO EGYPT'S GOVERNMENT TO CONSTRUCT 13,000 HOMES

Dubai builder Arabtec submitted a proposal to Egypt's government to construct 13,000 homes in the North African country, as per the firm's Chairman.

Arabtec Holding PJSC offers residential and commercial construction, industrial, and infrastructure services. The company's projects include hotels, airports, higher education developments, residential apartment buildings, and distribution facilities. Arabtec Holdings was founded in 1975, and operates throughout the United Arab Emirates, Middle East, and North Africa regions. _____________________________________________________________________________UAE'S DANA GAS PLANS FURTHER COST CUTS AMIDST LOW OIL PRICES

United Arab Emirates energy firm Dana Gas plans to cut costs in 2016 as the company gears up for a prolonged period of low crude prices, as per the company’s Chief Executive.

The Abu Dhabi-listed firm plans to cut general and administrative expenses by 55% in 2016 and operating expenses by a smaller amount.

Since the beginning of the year the firm has cut US$ 5 million in costs by lowering general and administrative expenses, as well as reducing the workforce in the fourth quarter of this year, according to a company statement.

On a positive note, Dana Gas expects production to increase significantly in 2016, as the company expects initial production from the Balsam Field in the Nile Delta to come on stream before the end of the year. _____________________________________________________________________________HILL INTERNATIONAL WINS OMAN AIRPORT CONTRACT EXTENSION

Hill International won an extension of a contract to provide consulting engineering services for the Muscat International Airport and Salalah Airport.

The initial contract to provide consulting engineering services for Muscat International Airport and Salalah Airport was awarded to Hill in 2012. The one-year extension is valued at approximately OMR 30.1 million (US$ 78.3 million).

The extension was given by Oman’s Ministry of Transport and Communications and the Public Authority for Civil Aviation of the Sultanate of Oman. The expansion of Muscat International Airport, the largest airport in Oman, includes a new terminal that would have a capacity of 12 million passengers annually.

The expansion of Salalah Airport, the second largest airport in Oman, involved upgrading it from primarily a domestic airport to make it more suitable for international travelers. ____________________________________________________________________________QATAR-BASED BROADCASTER BEIN MEDIA GROUP IN TALKS TO ACQUIRE THE MIRAMAX FILM COMPANY

Qatar-based broadcaster BeIN Media Group is in talks to buy the Miramax film company, as per Bloomberg.

The owners of Miramax, which includes Qatar Investment Authority (QIA), are in advanced talks to sell the company, with a deal likely to be completed by the end of this year.

A deal to buy Miramax would give the Qatar-based broadcaster a significant base in Hollywood and an opportunity to broaden its programming into the entertainment sector, as per the same source.

8Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

_____________________________________________________________________________NMC HEALTH WITHDRAWS BID FOR RIVAL AL NOOR HOSPITALS DUE TO VALUATION CONCERNS

NMC Healthcare withdrew its bid for rival UAE-based healthcare provider Al Noor Hospitals due to valuation concerns, as per NMC Health’s Vice Chairman and Chief Executive.

The company offers healthcare services. It operates hospitals, day surgery centers, medical centers, and pharmacies. Additionally, it provides pharmaceutical, fast-moving consumer goods, food, veterinary, and education product distribution services. The company was founded in 2012 and is based in Abu Dhabi, United Arab Emirates. NMC Healthcare LLC operates as a subsidiary of NMC Holding LLC.______________________________________________________________________________MUMTALAKAT BUYS 49% STAKE IN SPAIN’S ALEASTUR

Bahrain’s Mumtalakat plans to buy a 49% stake in Spanish aluminum products group Aleastur.

Mumtalakat is a sovereign wealth fund of the Kingdom of Bahrain. The firm seeks to invest in private equity, bonds, stocks, and equities. It primarily invests in non-oil and gas related assets. The firm also seeks to invest in aluminum production, aviation, financial services, logistics, industrials, telecommunications, real estate, tourism, transportation, and food production. It primarily invests in Kingdom of Bahrain. However, the firm also seeks investment outside Bahrain, including Europe and the United States and select pockets in the Far East.______________________________________________________________________________PETROFAC WINS CONTRACT BY SAUDI ARAMCO FOR ENGINEERING, PROCUREMENT AND CONSTRUCTION OF A SULPHUR RECOVERY PLANT

Petrofac was awarded a contract by Saudi Aramco to undertake the engineering, procurement, and construction of a Sulphur recovery plant as part of the company’s Fadhili programme. Fadhili is a greenfield development located 30 km west of the city of Jubail in the Eastern Province of Saudi Arabia.

When completed, the gas plant would have a capacity for around 2.5 billion cubic feet and would process sour gas from the Khursaniyah oil field and the Hasbah non-associated gas field. ______________________________________________________________________________DUCAB WINS US$ 130 MILLION ORDERS FROM OIL AND GAS FIRMS IN ABU DHABI AND KUWAIT

UAE’s Ducab Cable Manufacturing Company (Ducab) secured orders worth US$ 60 million in the oil, gas and petrochemical sectors in Abu Dhabi and US$ 70 million in Kuwait.

Jointly-owned by the Investment Corporation of Dubai and General Holding Corporation, which is part of the Abu Dhabi government, Ducab operates five manufacturing facilities in the UAE, which include Ducab Jebel Ali, Ducab Mussafah 1 Factory, Ducab Mussafah 2 Factory, Copper Rod Factory, and Ducab High Voltage Cable Systems Factory. It also acquired its first overseas plant, AEI Cables UK, earlier in 2014. The company has a manufacturing capability of over 115,000 metal tons of high, medium and low voltage cables and 110,000 tons of copper rods and wires per annum.______________________________________________________________________________MAJID AL FUTTAIM TO OPEN SHOPPING CENTRE IN RIYADH AND SEEKS EXPANSION IN OTHER GULF MARKETS

Majid Al Futtaim, the owner and operator of seven malls in the UAE, plans to open a shopping centre in the Saudi capital. The company is also looking to expand in other Gulf markets as well, according to a senior official at the company.

The company recently announced the completion of its expansion plans at the Muscat City Centre mall, and plans to open another mall there, called the Mall of Oman. The construction works on the new mall would start next year, and the project is expected to be completed in 2019.

9Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

EQUITY MARKETS INDICATORS (NOVEMBER 08, 2015 TILL NOVEMBER 14, 2015)

Sources: S&P, Bloomberg, Bank Audi's Group Research Department

CAPITAL MARKETS_____________________________________________________________________________EQUITY MARKETS: EXTENDED PRICE DECLINES IN REGIONAL EQUITY MARKETS, DRIVEN BY OIL PRICE SLUMP AND UNFAVORABLE FINANCIAL RESULTS

MENA equity markets continued to follow a downward streak this week, as reflected by a 0.4% decrease in the S&P Pan Arab Composite Index, mainly driven by falling oil prices and some unfavorable financial results.

The UAE equity markets posted a 4.9% fall in prices week-on-week, mainly dragged by some unfavorable financial results. In Dubai, Arabtec Holding Company’s share price plunged by 19.2% to AED 1.180. Arabtec posted a net loss of AED 945 million during the third quarter of 2015 as compared to net profits of AED 69 million during the corresponding period of 2014, on charges against a limited number of challenging projects and the reversal of AED 379 million of previously recognized claims. Union Properties’ share price tumbled by 9.8% to AED 0.745. Union Properties announced 2015 third quarter net profits of AED 111 million as compared to net profits of AED 128 million during the same period of 2014. Air Arabia’s share price dropped by 8.2% to AED 1.230. Air Arabia announced 2015 third quarter net profits of AED 235 million as compared to net profits of AED 251 million a year earlier. In Abu Dhabi, Taqa’s share price fell by 14.9% to close at AED 0.40. Taqa posted a net loss of AED 416 million during the third quarter of 2015 as compared to net profits of AED 107 million a year earlier. Aldar Properties’ share price shed 7.0% to AED 2.25.

Similarly, the Qatar Exchange registered a 4.9% drop in prices week-on-week, driven by a 7.7% decline in oil prices and some unfavorable financial results. Gulf International Services, which is engaged in establishing, acquiring, leasing, and managing companies specializing in the field of oil and gas services, posted a 4.3% decrease in prices to QR 57.80. Industries Qatar’s share price plummeted by 6.7% to QR 111.00. Vodafone Qatar’s share price plunged by 8.9% to QR 12.62. Vodafone Qatar posted a net loss of QR 214 million during the first half of fiscal year 2015/2016, as compared to a net loss of QR 81 million in the corresponding period of the previous year.

The Egyptian Exchange posted a 7.4% fall in prices week-on-week, within the context of a foreign sell-off and driven by some unfavorable market-specific and company-specific factors. Moody’s said that suspensions of flights and travel warnings following the Sinai plane crash are likely to reduce tourism to Egypt, which will have credit negative implications for the country’s balance of payments and will

10Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

pose downside risks to the country’s growth outlook. Talaat Moustafa Group’s share price plunged by 5.6% to LE 6.29. Ezz Steel’s share price shed 15.3% to LE 8.33. Palm Hills Development’s share price dropped by 8.9% to LE 2.04. Medinet Nasr Housing’s share price plummeted by 8.9% to LE 22.49. The company reported net profits of LE 154 million during the first nine months of 2015 as compared to net profits of LE 162 million a year earlier.

In contrast, the heavyweight Saudi Tadawul registered a 1.8% rise in prices week-on-week, driven by some favorable market-specific and company-specific factors. The Saudi Oil Ministry said that the scale of the global oil and gas industry's spending cuts are making another surge in energy prices possible by diminishing future supply. SABIC’s share price rose by 1.6% to SR 82.55. Yansab’s share price jumped by 6.9% to SR 44.14. Sipchem’s share price closed 3.2% higher at SR 17.21. STC’s share price jumped by 11.5% to SR 66.61. STC pledged to adopt a minimum one-riyal-per-share quarterly dividend for the next three years, starting the fourth quarter of 2015. Saudi Real Estate Company’s share price went up by 2.4% to SR 22.50. Saudi Real Estate Company signed a Letter of Intent with Starwood Hotels & Resorts Worldwide Inc. for the operation and management of its hotels. _____________________________________________________________________________BOND MARKETS: FURTHER PRICE DECLINES ACROSS REGIONAL BOND MARKETS AMIDST TIGHTER LIQUIDITY AND TRACKING US TREASURIES

MENA fixed income markets saw extended price declines across the board over this week, within the context of weaker investor sentiment and thinner liquidity driven by an oil price slump, and tracking declines in US Treasuries amidst bets the US Federal Reserve would raise its benchmark interest rate before year-end 2015.

In the Dubai space, sovereigns maturing between 2017 and 2043 registered price falls ranging between 0.13 pt and 1.88 pt week-on-week. Amongst quasi-sovereigns, DEWA’16, ’18 and ’20 were down by 0.25 pt, 0.63 pt and 0.75 pt respectively. DP World’17, ’20 and ’37 saw price drops of up to 2.50 pts. Prices of Emirates Airline’16 and ’23 declined by 0.25 pt and 0.38 pt respectively. Emirates Airline said that it could issue a conventional or Islamic bond in 2016 to raise as much as US$ 1 billion to be used to fund around 30 aircraft that are scheduled to be delivered that year. As to corporates, Emaar’16 and ’19 closed down by 0.38 pt each. Emaar’24 was down by 0.88 pt. Majid Al Futtaim’17, ’19 and ’24 posted price decreases of 0.13 pt, 0.38 pt and 0.88 pt respectively.

As to papers issued by financial institutions, DIB’17 traded down by 0.38 pt over the week. DIB Perpetual bonds (offering a coupon of 6.25% and 6.75% respectively) registered price decreases of 1.50 pt and 2.13 pts respectively. Commercial Bank of Dubai’18 closed down by 0.38 pt. Commercial Bank of Dubai sold this week US$ 400 million worth of five-year bonds at 232 bps over the US Dollar five-year mid swap rate. The final allocation was 11% to Asian investors, 39% to European investors and 50% to investors from the Middle East.

In Abu Dhabi, sovereigns maturing in 2019 were down by 0.63 pt week-on-week. Prices of Mubadala’19, ’21 and ’22 decreased by 0.56 pt, 0.81 pt and 1.00 pt respectively. IPIC papers maturing between 2016 and 2041 witnessed price declines ranging between 0.13 pt and 1.00 pt. Taqa papers maturing between 2016 and 2036 registered price falls ranging between 0.13 pt and 3.00 pts. In the financial space, ADIB’16 closed down by 0.25 pt. ADIB Perpetual was down by 2.00 pts. ADIB repaid a US$ 750 million Sukuk that has matured on November 4, 2015. ADCB papers maturing between 2016 and 2023 saw price drops of up to 1.38 pt. Capital Intelligence affirmed the financial strength rating of ADCB at “A-” with a “stable” outlook, with its improving asset quality and particularly its good loan loss reserve coverage, good and rising operating profitability and ROAA and solid capital adequacy being major supporting factors.

In the Bahraini space, sovereigns maturing between 2018 and 2044 witnessed price declines ranging between 0.88 pt and 2.63 pts over the week. Batelco’20 was down by 1.00 pt. Prices of Mumtalakat’21 decreased by 1.00 pt. The Kingdom of Bahrain mandated Bank ABC, BNP Paribas, Citi, HSBC and JPM to arrange a series of investor meetings in Asia, the Middle East, the US and the UK for a US Dollar-denominated benchmark-sized bond sale.

11Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

MIDDLE EAST 5Y CDS SPREADS V/S INTL BENCHMARKS

Sources: Bloomberg, Bank Audi's Group Research Department

Z-SPREAD BASED AUDI MENA BOND INDEX V/S INTERNATIONAL BENCHMARKS

Sources: Bloomberg, JP Morgan, Bank Audi's Group Research Department

In Saudi Arabia, SABIC’18 and ’20 traded down by 0.63 pt each over the week. SECO papers maturing between 2017 and 2044 registered price falls ranging between 0.31 pt and 4.00 pts. Dar Al Arkan’16, ’18 and ’19 were down by 0.25 pt, 1.25 pt and 3.00 pts respectively. As to financials, Banque Saudi Fransi’17 saw no price change week-on-week. Standard & Poor's revised its outlook on Banque Saudi Fransi from “stable” to “negative”. The outlook revision stems from S&P’s view of increased economic risk for banks in Saudi Arabia following the sovereign downgrade on October 30, 2015. The sharp decline of oil prices and the resulting pressure on the government's fiscal position will weigh on Saudi Arabia's banking sector, as per S&P.

Finally, Qatari sovereigns maturing between 2017 and 2042 posted price declines of up to 1.75 pt week-on-week. Qtel papers maturing between 2016 and 2043 traded down by up to 1.13 pt. Amongst financials, QIB’17 and ’20 were down by 0.38 pt and 0.50 pt respectively. QNB’17, ’18 and ’20 posted price drops of up to 1.06 pt. As to plans for new issues, International Bank of Qatar mandated Citi, QNB Capital and Standard Chartered Bank as joint lead managers to arrange series of fixed income investors meetings in Asia, the Middle East and Europe.

12Week 46 November 08 - November 14, 2015

NOVEMBER 08 - NOVEMBER 14, 2015

WEEK 46

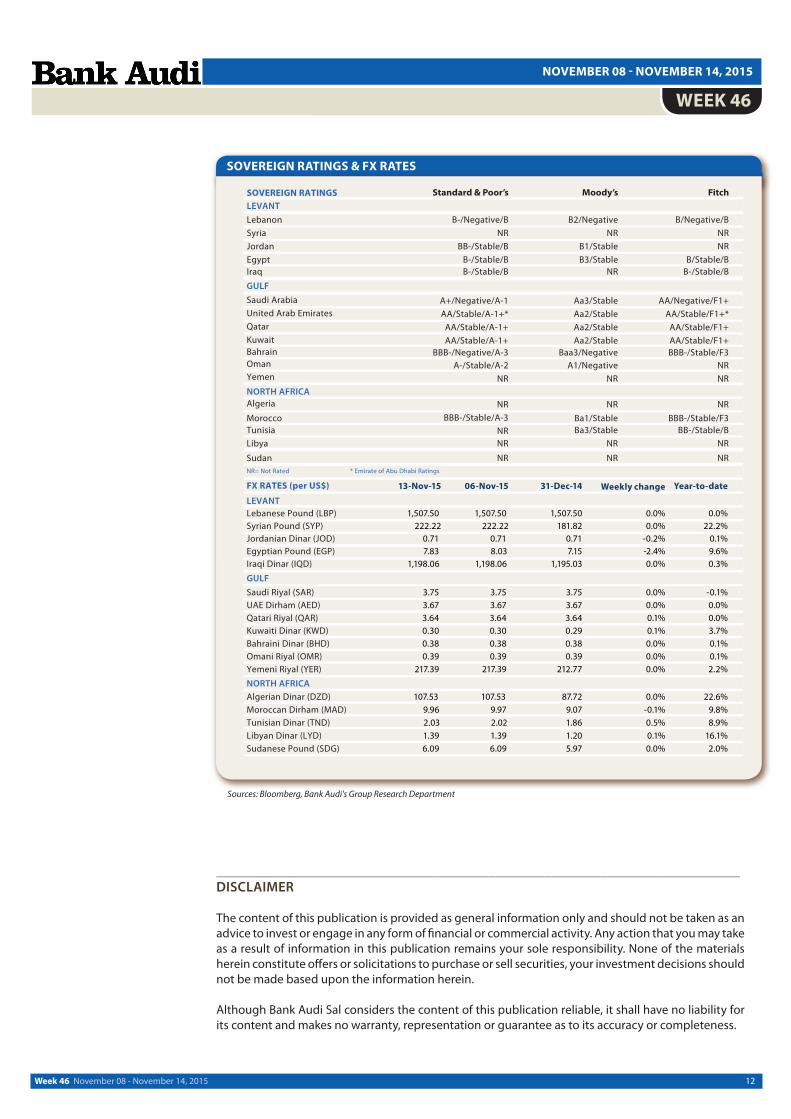

SOVEREIGN RATINGS & FX RATES

Sources: Bloomberg, Bank Audi's Group Research Department

___________________________________________________________________________DISCLAIMER

The content of this publication is provided as general information only and should not be taken as an advice to invest or engage in any form of financial or commercial activity. Any action that you may take as a result of information in this publication remains your sole responsibility. None of the materials herein constitute offers or solicitations to purchase or sell securities, your investment decisions should not be made based upon the information herein.

Although Bank Audi Sal considers the content of this publication reliable, it shall have no liability for its content and makes no warranty, representation or guarantee as to its accuracy or completeness.