mccombs 2007 valuation presentation 103007

TRANSCRIPT

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 1/71

O C T O B E R 3 0 , 2 0 0 7

M & A V A L U A T I O N O V E R V I E W

S T R I C

T L Y

P R I V A T E

A

N D

C O

N F I D E N T I

A L

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 2/71

Agenda

LBO analysis

Discounted cash flow analysis

Transaction comparables

Trading comparables

Introduction

1

1

6

20

31

59

M

&

A

V

A L U A T I O

N

O

V E R

V I E W

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 3/71

Why valuation is important

Acquisitions

How much should wepay to buy the

company?

Divestitures

How much should wesell our

company/division for?

Fairness opinions

Is the price offeredfor our

company/division fair(from a financialpoint of view)?

Public equityofferings

For how much shouldwe sell our

company/division inthe public market?

Debt offerings

What is the underlyingvalue of the

business/assets againstwhich debt is being

issued?

New businesspresentations

Various applications

Research

Should our clients buy,sell or hold positions in

a given security?

Hostile defense

Is our companyundervalued/vulnerable

to a raider

Valuation

2 I N T R O

D U C T I O

N

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 4/71

Valuation methodologies

Publicly tradedcomparable

companies analysis

Comparabletransactions

analysis

Valuationmethodologies

Discountedcash flowanalysis

Leveragedbuyout/recap

analysisOther

“Public Market

Valuation”

Value based on

market trading

multiples of

comparable

companies

Applied using

historical and

prospectivemultiples

Does not include a

control premium

“Private Market

Valuation”

Value based on

multiples paid for

comparable

companies in sale

transactions

Includes control

premium

“Intrinsic” value

of business

Present value of

projected free

cash flows

Incorporates both

short-term and

long-term

expected

performance Risk in cash flows

and capital

structure captured

in discount rate

Value to a

financial/LBO

buyer

Value based on

debt repayment

and return on

equity investment

Liquidation

analysis

Break-up analysis

Historical trading

performance

Expected IPO

valuation

EPS impact

Dividend discount

model

3 I N T R O

D U C T I O

N

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 5/71

The valuation process

Leveraged Buy Out:

Used to determine

range of potentialvalue for a company

based on maximum

leverage capacity.

Comparable

Acquisition

Transactions:Utilizes data from

M&A transactions

involving similar

companies.

Publicly Traded

ComparableCompanies: Utilizes

market trading

multiples from

publicly traded

companies to derive

value.

Discounted Cash

Flow: Analyzesthe present

value of a

company's free

cash flow.

Determining a final valuation recommendation is a process of triangulation using insight from each of the relevant valuationmethodologies

Determining a final valuation recommendation is a process of triangulation using insight from each of the relevant valuationmethodologies

4 I N T R O

D U C T I O

N

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 6/71

1,350

2,850

1,400

1,8001,400

1,5001,100

1,100

1,6501,350

1,3001,100

3,000

1,850

1,100

500 1,000 1,500 2,000 2,500 3,000 3,500

Va lua t i on met r i cs

Comparable publiccompanies analysis

FV/2005 EBITDA(7.5x – 9.0x) – bank andmanagement cases

FV/2006P EBITDA(7.0x – 8.5x) – bank case

FV/2006P EBITDA(7.0x – 8.5x) – management case

Precedent transactions

analysis

FV/2005 EBITDA(7.5x – 9.5x) – bank andmanagement cases

Discounted cash flowanalysis

Bank case

Management case

Leveraged buyoutanalysis

Bank case

Management case

Implied FV/2005

EBITDA Multiple

9.5x –12.3x

20.5x –27.4x

7.5 – 9.0x

7.5x –9.2x

7.5x – 9.5x

7.5x –10.3x

12.7x –19.5x

9.2 – 11.3x

4,000

The science is performing each valuation method correctly, the art is using each method to develop a valuation recommendationThe science is performing each valuation method correctly, the art is using each method to develop a valuation recommendation

Firm value ($ in millions)

The valuation summary is the most important slide in a

valuation presentation

5 I N T R O

D U C T I O

N

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 7/71

Agenda

LBO analysis

Discounted cash flow analysis

Transaction comparables

Trading comparables

Introduction

6

1

6

20

31

59

M

&

A

V

A L U A T I O

N

O

V E R V I E W

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 8/71

Trading comparables analysis as a valuation methodology

Publicly tradedcomparable

companies analysis

Comparabletransactions

analysis

Valuationmethodologies

Discountedcash flowanalysis

Leveragedbuyout/recap

analysisOther

“Public Market

Valuation”

Value based on

market tradingmultiples of

comparable

companies

Applied using

historical and

prospective

multiples

Does not include a

control premium

“Private Market

Valuation”

Value based on

multiples paid forcomparable

companies in sale

transactions

Includes control

premium

“Intrinsic” value

of business

Present value of

projected freecash flows

Incorporates both

short-term and

long-term

expected

performance

Risk in cash flows

and capital

structure captured

in discount rate

Value to a

financial/LBO

buyer

Value based ondebt repayment

and return on

equity investment

Liquidation

analysis

Break-up analysis

Historical trading

performance

Expected IPO

valuation

EPS impact

Dividend discount

model

Publicly tradedcomparablecompanies

analysis

7 T R A D I

N G

C O

M

P A R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 9/71

ProsPros ConsCons

Trading multiples analysis is a key technique based on the

assumption that the market is efficient / correct

Market values incorporate perception of all

investors reflecting firm prospects, industry

trends, business risk, market growth, etc.

Basic tool for estimating market value

Provides check for DCF

Values obtained are reliable indicator of the

value of firm for minority investment

Difficult to identify 100% comparable

companies

Must make the difficult decision whether the

company being analyzed is valued higher,

lower or the same as the average of the

sample

May be short term divergences from

fundamental value

Stock market may reflect "sentiment” and

not the "true picture”

Thinly traded, small capitalization and

poorly followed stocks may not reflect

fundamental value Different accounting standards

Publicly tradedcomparablecompanies

analysis

8 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 10/71

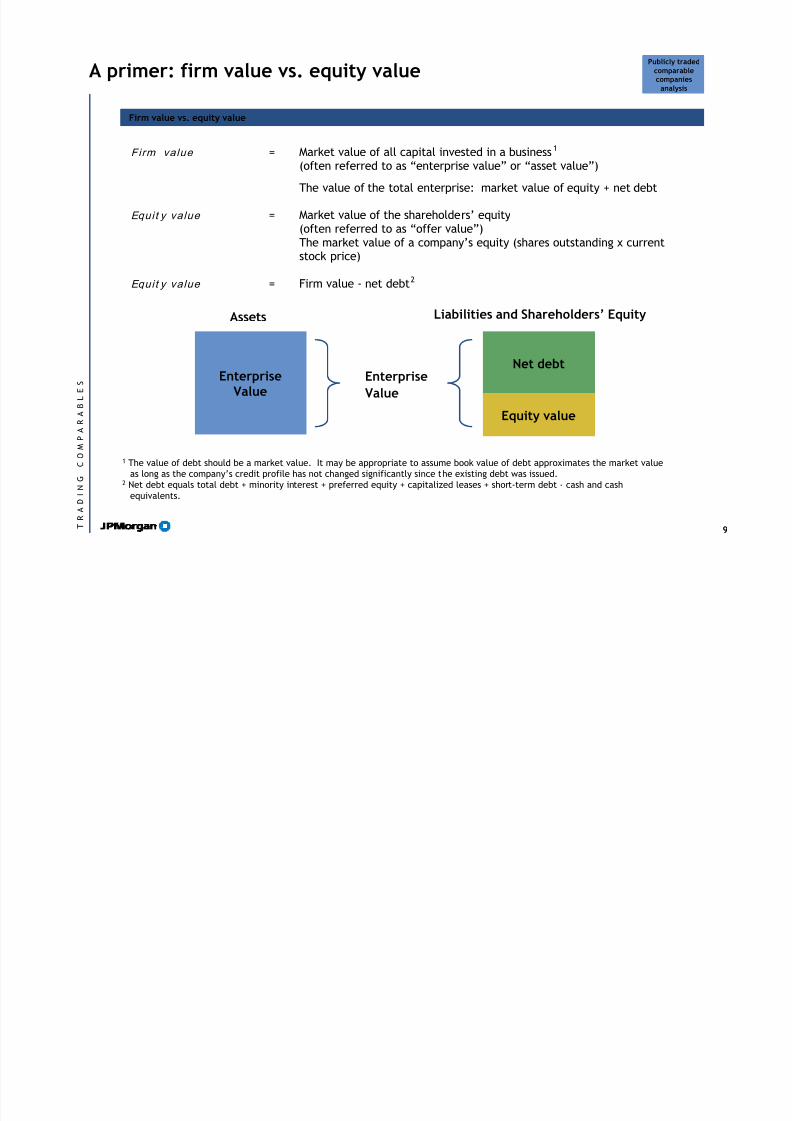

A primer: firm value vs. equity value

Firm value = Market value of all capital invested in a business1 (often referred to as “enterprise value” or “asset value”)

The value of the total enterprise: market value of equity + net debt

Equit y value = Market value of the shareholders’ equity(often referred to as “offer value”)The market value of a company’s equity (shares outstanding x currentstock price)

Equit y value = Firm value - net debt2

Liabilities and Shareholders’ EquityAssets

Enterprise

Value

Net debt

Equity value

Enterprise

Value

1 The value of debt should be a market value. It may be appropriate to assume book value of debt approximates the market valueas long as the company’s credit profile has not changed significantly since the existing debt was issued.

2 Net debt equals total debt + minority interest + preferred equity + capitalized leases + short-term debt - cash and cash

equivalents.

Firm value vs. equity valueFirm value vs. equity value

Publicly tradedcomparablecompanies

analysis

9 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 11/71

Different multiples apply to equity value and firm value

Equity valueEquity value Firm valueFirm value

Value for owners of business (after interest

expense)

Multiples of:

Net income After tax cash flow

Book value

Value available to all providers of capital

(before interest expense)

Multiples of:

Sales EBITDA

EBIT

CommentsComments

The defining difference lies in the treatment of debt and its associated cost (interest expense)

A multiple that has debt in the numerator must have a statistic before interest expense in the

denominator

Publicly tradedcomparablecompanies

analysis

10 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 12/71

Key comparables must be in same business as target

OperationalOperational FinancialFinancial

Industry

Product

Markets

Distribution channels

Customers

Seasonality

Cyclicality

Growth prospects

Size

Margins

Leverage

Shareholder base (influence of a largeshareholder)

CommentsComments

Consider the perspective of equity investors (can use equity research as a proxy) – to what

would they compare target?

You want to identify companies that closely resemble the composition and function of the

company you are evaluating

Publicly tradedcomparablecompanies

analysis

11 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 13/71

Choosing the right multiples

It is important to understand what metric the companies in a peer group trade off of (revenue, EBITDA, EPS, etc.)It is important to understand what metric the companies in a peer group trade off of (revenue, EBITDA, EPS, etc.)

Typical valuation measures include

Firm value multiples

— Firm value/sales

— Firm value/EBITDA— Firm value/EBIT

Equity value multiples

— (Equity value/net income) or (price/EPS (P/E))

— Equity value/after-tax cash flow

— Equity value/book equity

Valuation multiple can be calculated on both a latest twelve months (“LTM”) and a forecasted

basis

Companies trade most typically off expected future performance (analysts’ estimates)

EPS estimates are available from I/B/E/S on Bloomberg

Other income statement projections are found in equity research reports

Publicly tradedcomparablecompanies

analysis

12 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 14/71

Performance measures

Growth ratesGrowth rates Margins / ProfitabilityMargins / Profitability

Sales

Operating income

Net income

Gross margin

EBITDA margin

EBIT margin

Net income margin

Operating margin

Return on total invested

capital (industrialcompanies)

Return on equity (financial

institutions companies)

CommentsComments

Comparing various statistics and performance measures among the companies in your

comparable universe can help shed light on why companies may trade the way they do

Capitalization / CreditCapitalization / Credit

Leverage and liquidity

ratios

Coverage ratios

Off-balance sheet

debt/operating leases

Publicly tradedcomparablecompanies

analysis

13 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 15/71

ExampleExample Issues / PitfallsIssues / Pitfalls

JPMorgan uses the treasury method to calculate diluted

shares outstanding

Break out each tranche of outstanding

options and warrants separately

Avoid double counting of options - do not

include “Total” line in calculation

Equity value should be calculated using all

options and warrants outstanding (not just

exercisable)

Stock splits

Pro forma adjustments

Note accounting convention for diluted EPS

in financial statements uses average stock

price over the prior year - not correct for

calculating current shares outstanding

The treasury method assumes all in-the-money options are exercised and the proceeds used to buy-back sharesThe treasury method assumes all in-the-money options are exercised and the proceeds used to buy-back shares

ExampleCo Inc.

Total basic shares outstanding (latest 10K/10Q) 1,772,199,483.0

Current ExampleCo share price $40.0

OutstandingExerciseprice

In themoney?

Sharesissueduponexercise

Proceeds fromexercise

Treasurysharespurchasedwith proceeds

Tranche 1 2,975.0 $8.56 Yes 2,975.0 $25,466.0 636.7

Tranche 2 77,165.0 $24.99 Yes 77,165.0 $1,928,353.4 48,208.8

Tranche 3 96,782.0 $39.13 Yes 96,782.0 $3,787,079.7 94,677.0

Tranche 4 110,975.0 $57.00 No 0.0 $0.0 0.0

Total 287,897.0 176,922.0 5,740,899.0 143,522.5

Total shares issued upon exercise of options 176,922.0

Treasury shares purchased with proceeds (143,522.5)

Incremental shares outstanding 33,399.5

Diluted shares outstanding 1,772,232,882.5

Publicly tradedcomparablecompanies

analysis

14 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 16/71

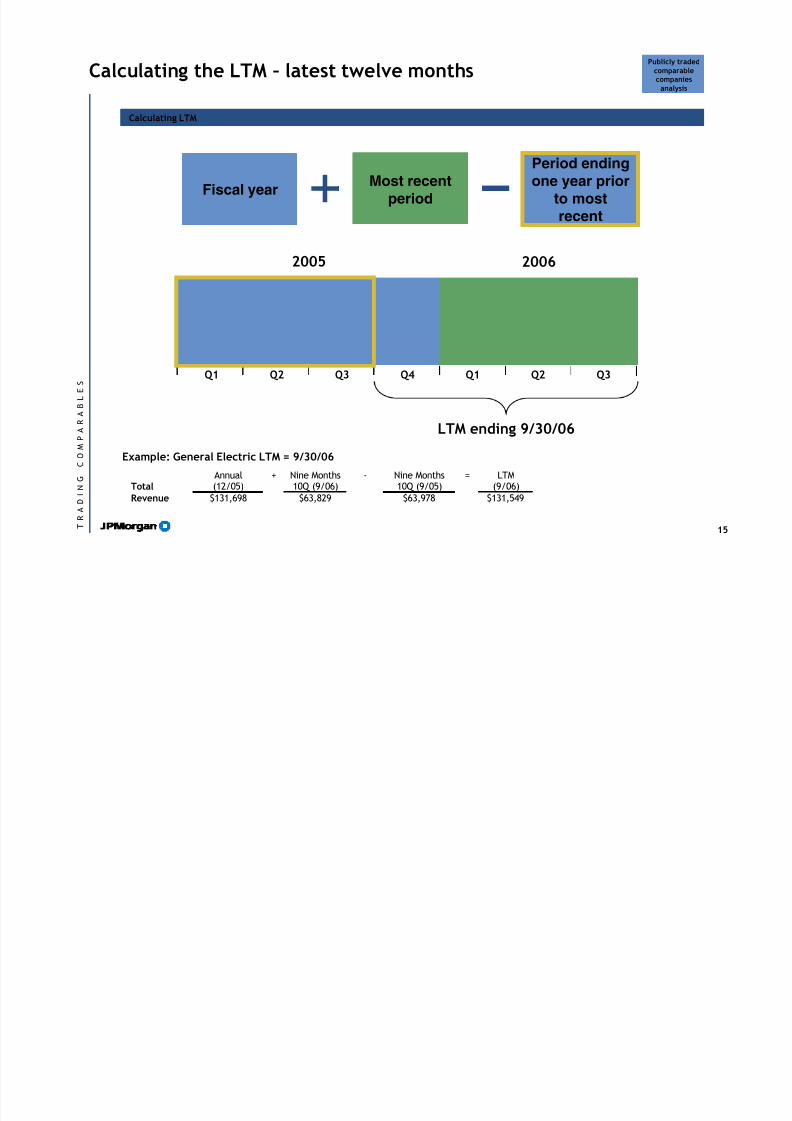

Calculating the LTM – latest twelve months

Calculating LTMCalculating LTM

Total

Annual(12/05)

+ Nine Months10Q (9/06)

- Nine Months10Q (9/05)

= LTM(9/06)

Revenue $131,698 $63,829 $63,978 $131,549

Example: General Electric LTM = 9/30/06

Publicly tradedcomparablecompanies

analysis

Fiscal yearMost recent

period

Period endingone year prior

to mostrecent

2005 2006

Q1 Q2 Q3 Q4 Q1 Q2

LTM ending 9/30/06

Q3

15 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 17/71

Calendarizing financial data

Calendarization methodologyCalendarization methodology

When companies in the comparable universe have fiscal years ending at a date other than that

of the client or focus company, it is common to employ the technique of calendarization

Calendarization adjusts the financial data of one company to reflect results representative of

the period in time corresponding to the latest fiscal year of the client or focus company

This insures that the financial data of both companies is truly comparable by eliminating

seasonal or cyclical differences that may arise as a result of dissimilar fiscal year ends

Example: Client has fiscal year end (“FYE”) 12/31 while Comp has FYE 10/31

Comp FYE 2006 Net Income = $120, Target FYE 2007E Net Income = $150 Calendarize Comp from 10/31/06 FYE to Client 12/31/06 FYE

Target CY2006E Net Income =

Ideally could use quarterly estimates

However, availability and consistency are an issue

Publicly tradedcomparablecompanies

analysis

10 x $120 2 x $15012

+12

= $100 + $25 = $125

16 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 18/71

Other standards when spreading comps

Other standardsOther standards

Use income from continuing operations (i.e. income before discontinued operations,

extraordinary charges/income and effect of change in accounting principles)

Eliminate non-recurring items

Restructuring charges

Gains/losses on sale of assets

One-time write-offs

Read all footnotes and Management Discussion and Analysis (“MD&A”) sections

Tax effect all adjustments, if they relate to an after-tax financial statistic and aretax-deductible

Check MD&A and footnotes for actual tax impact if available

Use marginal rate if tax impact not available

Double-check your calculations

“Reality” check on multiples, margins, etc. (ruler check, brokerage report check) Don’t assume model is always right

Publicly tradedcomparablecompanies

analysis

17 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 19/71

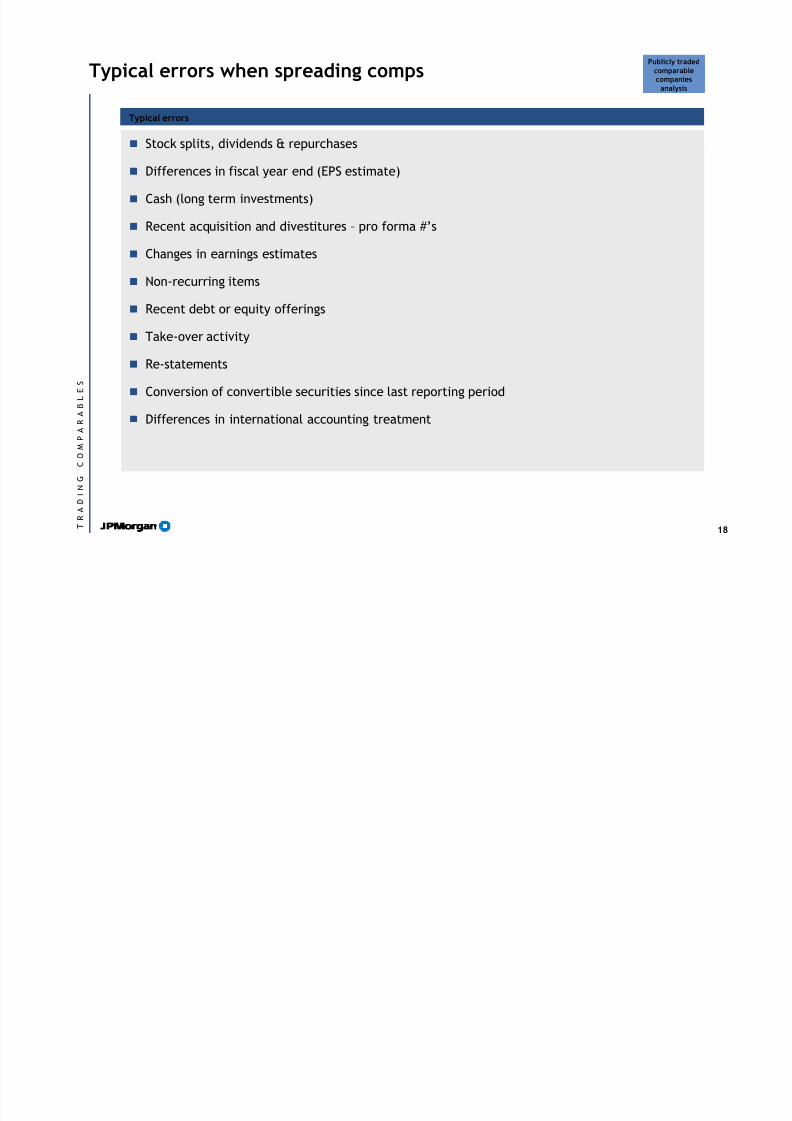

Typical errors when spreading comps

Typical errorsTypical errors

Stock splits, dividends & repurchases

Differences in fiscal year end (EPS estimate)

Cash (long term investments)

Recent acquisition and divestitures – pro forma #’s

Changes in earnings estimates

Non-recurring items

Recent debt or equity offerings

Take-over activity

Re-statements

Conversion of convertible securities since last reporting period Differences in international accounting treatment

Publicly tradedcomparablecompanies

analysis

18 T R A D I

N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 20/71

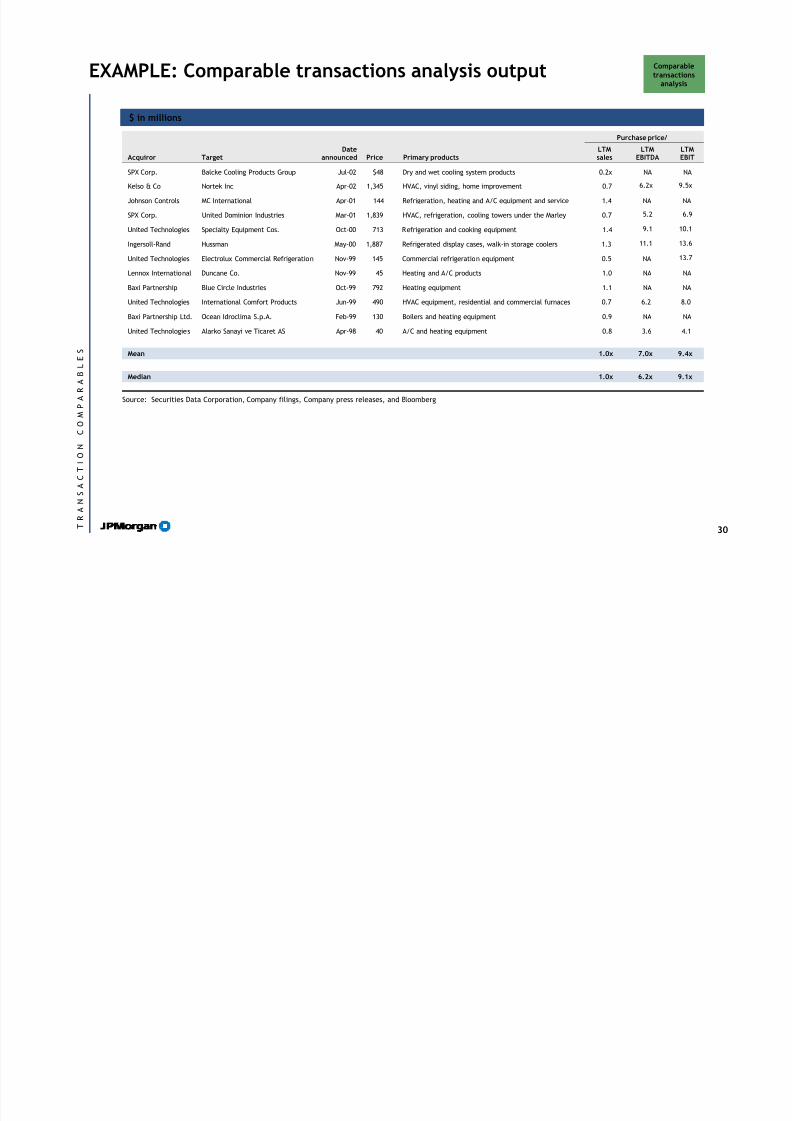

EXAMPLE: Trading comparables output

Firm valueStock

price at10/25/06

52-weekhigh

52-weeklow

Mkt.cap

Firmvalue

LTMsales

2006Esales

2007Esales

LTMEBITDA

2006EEBITDA

2007EEBITDA

LTMEBIT

2006EEBIT

2007EEBIT

2006EP/E

2007EP/E LTGR

2006EPEG

Company A $11.81 $12.30 $4.47 $102 $290 1.78x 1.06x 0.76x 15.7x 9.3x 6.7x 18.3x 11.4x 8.3x 15.8x 13.2x 16.5% 1.0x

Company B 15.51 25.75 13.48 262 238 0.43 0.45 0.43 5.1 6.0 5.3 6.2 7.6 6.7 13.9 11.4 15.3% 0.9

Company C 6.65 6.85 2.35 162 350 0.37 0.36 0.35 8.1 5.9 5.6 11.3 7.3 7.0 11.6 10.5 10.0% 1.2

Company D 48.44 57.50 32.05 2,683 3,504 1.02 0.96 0.87 7.1 6.7 6.2 9.8 9.2 8.3 15.1 13.1 17.2% 0.9

High 1.78x 1.06x 0.87x 15.7x 9.3x 6.7x 18.3x 11.4x 8.3x 15.8x 13.2x 17.2% 1.2x

Mean 0.72x 0.70x 0.59x 7.6x 6.3x 5.9x 10.6x 8.4x 7.6x 14.5x 12.2x 15.9% 0.9x

Median 0.90x 0.71x 0.60x 9.0x 7.0x 5.9x 11.4x 8.8x 7.6x 14.1x 12.1x 14.8% 1.0x

Low 0.37x 0.36x 0.35x 5.1x 5.9x 5.3x 6.2x 7.3x 6.7x 11.6x 10.5x 10.0% 0.9x

Target Company$18.44 $19.25 $10.00 $107 $116 0.70x 0.68x 0.62x 6.3x 6.2x 5.5x 7.3x 7.2x 6.2x 10.5x 9.3x 20.0% 0.5x

LTM margin analysis LTM leverage analysis

LTMsales

LTMEBITDA

Grossprofit

EBITDAmargin EBIT margin

Netincome

Debt/cap.

Debt/EBITDA

LTM EBITDA/interest

LTM CAPEX/sales

Returnon equity

Returnon assets

Company A $162.64 $18.53 33.3% 11.4% 9.7% 4.2% 74.6% 9.4x 2.7x 1.4% 20.3% 2.4%

Company B 558.39 46.86 25.9% 8.4% 6.8% 4.1% NM 0.0 85.5 0.8% 11.6% 9.3%

Company C 943.78 43.25 8.3% 4.6% 3.3% 0.3% 58.5% 6.0 1.8 1.7% 1.7% 0.6%Company D 3,446.34 491.98 46.9% 14.3% 10.4% 5.5% 38.5% 1.4 13.4 5.9% 19.4% 7.8%

High 46.9% 14.3% 10.4% 5.5% 74.6% 9.4x 85.5x 5.9% 20.3% 9.3%

Mean 29.6% 9.9% 8.3% 4.2% 58.5% 3.7x 8.0x 1.5% 15.5% 5.1%

Median 28.6% 9.7% 7.6% 3.5% 57.2% 4.2x 25.8x 2.4% 13.2% 5.0%

Low 8.3% 4.6% 3.3% 0.3% 38.5% 0.0x 1.8x 0.8% 1.7% 0.6%

Target Company $164.83 $18.42 21.0% 11.2% 9.6% 5.8% 14.4% 0.6x 67.2x 0.3% 15.3% 10.1%

Operating statistics (do l lars in mi l l ions) Operating statistics (do l lars in mi l l ions)

Source: Company filings, Analyst reports, Bloomberg

Trading statistics (do l lars in mi l l i ons except per share dat a) Trading statistics (do l lars in mi l l i ons except per share dat a)

Publicly tradedcomparablecompanies

analysis

19 T R A D I N G

C O

M

P A R A B L

E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 21/71

Agenda

LBO analysis

Discounted cash flow analysis

Transaction comparables

Trading comparables

Introduction

20

1

6

20

31

59

M

&

A V

A L U A T I O

N

O

V E

R V I E W

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 22/71

Transaction comparables analysis as a valuation methodology

Publicly tradedcomparable

companies analysis

Comparabletransactions

analysis

Valuationmethodologies

Discountedcash flowanalysis

Leveragedbuyout/recap

analysisOther

“Public Market

Valuation”

Value based on

market tradingmultiples of

comparable

companies

Applied using

historical and

prospective

multiples

Does not include a

control premium

“Private Market

Valuation”

Value based on

multiples paid forcomparable

companies in sale

transactions

Includes control

premium

“Intrinsic” value

of business

Present value of

projected freecash flows

Incorporates both

short-term and

long-term

expected

performance

Risk in cash flows

and capital

structure captured

in discount rate

Value to a

financial/LBO

buyer

Value based ondebt repayment

and return on

equity investment

Liquidation

analysis

Break-up analysis

Historical trading

performance

Expected IPO

valuation

EPS impact

Dividend discountmodel

21 T R A N S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 23/71

Comparable transactions analysis

CommentsComments

Assists investment bankers, clients, lenders to understand the:

Valuation of a company

Structuring of a potential transaction

Current state of M&A in a specific industry (number and relative value)

Examines a group of transactions to identify a median/range/trend of:

The multiple (of cash flow, operating profit, earnings or other industry metrics) paid for a

target

The premium paid to gain control of a target (“control premium”)

Business fundamentals of a target (revenue/earnings growth, profitability)

Technical transaction elements (deal protection, conditions to closing)

Social issues (board seats, management)

Other value drivers (synergies, tax benefits)

Comparabletransactions

analysis

22 T R A N S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 24/71

Sources used to locate comparable transactions

Reference sourcesReference sources

Thompson Financial database

Locates targets based on SIC code, business description, industry

Identifies transactions based on hostile vs. friendly, transaction size, announcement date,

and several other deal elements The “Comprehensive Summary Report” is very helpful in hand-picking transactions since it

includes a synopsis of the deal in addition to general information regarding both parties andthe transaction

Senior bankers who work in the industry

Will be able to point you toward previously used presentations or valuations Ensures you do not exclude any landmark deals or other deals they would specifically like to

include

Merger proxies for similar transactions

Fairness opinions of financial advisors disclose the comparable transactions used in their

valuation of the target Other sources include:

Proprietary transaction comps databases

News runs

Equity research reports

Comparabletransactions

analysis

23 T R A N S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 25/71

Selecting comparable transactions

Selecting transactionsSelecting transactions

When valuing a company, key objective is to find the most comparable businesses

Similar industries with similar products or services

Size, margins, relative market position, major potential liabilities

When seeking guidance regarding structure, the situation surrounding the acquisition is crucial

Scenarios could include: LBO’s, bankruptcy-related acquisitions, hostile transactions,

reverse mergers, divestitures, asset vs. stock acquisitions, form of consideration, Morris

Trust transactions, and many others

If possible, try to locate transactions in a similar industry as well

Some types of transactions should, generally, not be considered as a comparable transaction

Acquisitions of a minority interest (not a change of control transaction)

Rumored or withdrawn transactions

Recent deals are typically a more accurate reflection of the values buyers are willing to pay

Remember that some transactions are more relevant than others when selecting a range of

multiples for valuation

Comparabletransactions

analysis

24 T R A N S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 26/71

Definitions of equity value and firm value similar to trading comparables:

Equity value Value received by the target / target shareholders (100%)

+

Net debt Debt assumed by acquirer minus cash received

Firm value Total value of business acquired (100%)

BE CAREFUL: Transaction value for a change of control transaction will differ from equity and/or firm valuewhen >50% but <100% is acquired

Equity value:

Cash consideration: (fully-diluted target shares @ offer price) x (cash consideration per share)

Stock consideration: (fully-diluted target shares @ offer price) x (exchange ratio) x (price per acquirershare @ the closing price prior to announcement)

Cash and stock consideration: (fully-diluted target shares @ offer price) x (cash consideration per share)plus (fully-diluted target shares @ offer price) x (exchange ratio) x (price per acquirer share @ the closingprice prior announcement)

Firm value:

In all cases: Add the indebtedness and subtract the cash items that are to be transferred to the acquirerthrough the transaction to the target equity value

Be careful not to add any convertible debt or preferred securities which were converted into commonshares (and already included in the fully-diluted share count)

May be appropriate to include certain other unfunded liabilities in the calculation of firm value for a

transaction

Calculating equity and firm value

Calculating equity and firm valueCalculating equity and firm value

Comparabletransactions

analysis

25 T R A N S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 27/71

Other equity and firm value issues

Other issuesOther issues

Timing (announcement vs. closing)

Typically want to assess what buyer was willing to pay for business, so most interested in valuation based

on stock prices as of announcement date

Information regarding shares outstanding, options, debt, cash as of most recent publicly disclosed source as

of announcement date (i.e. 10-K, 10-Q, or Proxy, 8-K)

However, if terms of the transaction change (exchange ratio, amount of cash consideration), should look to

valuation on date of announcement of revised terms

Valuing a deal with stock consideration as of the closing date will give a sense for how market reacted to

value of two companies together

Transaction fees

Typically M&A fees/financing fees are not included in firm value of business acquired as they are not

consideration received by seller

However, in extreme cases (i.e., LBO/recap) it may be instructive to know amount of fees and indicate

how they may have impacted business valuation

Asset purchases

Note that debt can be transferred with businesses/assets being sold and must be added to theconsideration paid by the acquirer

Other liabilities

In some instances it may be appropriate to include the assumption of a non-debt other unfunded liability in

firm value (such as an existing restructuring reserve) but never NWI / working capital items

Earn-outs/purchase price adjustments

Comparabletransactions

analysis

26 T R A N

S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 28/71

LTM financial information issues

LTM issuesLTM issues

Time horizon

LTM financial information should reflect what buyer bought the business “off-of” and is generally

backward-looking (typically last twelve months of financial information available prior the announcement

date)

In certain industry-specific circumstances (i.e. technology, biotech) it is more useful to look at projectedfinancial information as well (typically IBES consensus estimates / median of several analyst reports)

However, the outlook of equity analysts may be quite different than the outlook of the buyer at the

time of acquisition

Adjustments

Exclude impact of extraordinary items on a tax-affected basis

Pro forma adjustments (i.e. acquisitions and divestitures) must be considered

Currencies

If target is foreign, most-commonly taught method is to apply average exchange rates over LTM period

because it is the accounting convention

Is this always appropriate for valuation purposes? Not necessarily

Need to consider carefully / discuss with team-members in extreme cases (i.e. when currency has de-valued / re-valued substantially vs. US Dollar)

Comparabletransactions

analysis

27 T R A N

S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 29/71

Other general considerations

Other considerationsOther considerations

Synergies

Synergies are not generally incorporated into the financial information but it may be useful to consider

their value when comparing transactions to each other

Sometimes will indicate announced synergies as a % of sales, SG&A, SG&A + COGS, transaction value

Tax benefits

In certain cases a buyer will receive substantial benefits from depreciating / amortizing a write-up and

receiving incremental tax deductions

An acquirer can often justify a higher purchase price and multiples may be higher in such circumstances

Can attempt to estimate the value of tax benefits received by acquirer but depends on a lot of unknown

variables (discount rate, amortization period, tax basis)

However, should know which transactions are tax-advantaged and which aren’t

Comparabletransactions

analysis

28 T R A N

S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 30/71

Most common errors

Common errorsCommon errors

Unaffected stock prices (for premium analyses)

Stock splits

Proper interpretation of exchange ratio

Target share price / acquirer share price

Using the correct acquirer share price

Most recent common shares outstanding (use the merger agreement if available)

Use all outstanding, not exercisable, options and warrants and assume that all in-the-money securities are

exercised in this analysis

Check for warrants

Repriced options

New issuances of debt or equity since most recent 10Q or 10K

Forgetting debt in an asset transaction

Acquisitions or divestitures completed by the target over LTM period

Exclude all extraordinary items - only tax affect those items that are tax deductible

Publicly-available information only

Comparabletransactions

analysis

29 T R A N

S A C T I O

N

C O

M

P A

R A B L E S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 31/71

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 32/71

Agenda

LBO analysis

Discounted cash flow analysis

Transaction comparables

Trading comparables

Introduction

31

1

6

20

31

59

M

&

A

V A L U A T I O

N

O

V E

R V I E W

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 33/71

Valuation methodologies

Publicly tradedcomparablecompanies analysis

Comparabletransactionsanalysis

Valuationmethodologies

Discountedcash flowanalysis

Leveragedbuyout/recapanalysis

Other

“Public Market

Valuation”

Value based on

market tradingmultiples of

comparable

companies

Applied using

historical and

prospective

multiples

Does not include a

control premium

“Private Market

Valuation”

Value based on

multiples paid forcomparable

companies in sale

transactions

Includes control

premium

“Intrinsic” value

of business

Present value of

projected freecash flows

Incorporates both

short-term and

long-term

expected

performance

Risk in cash flows

and capital

structure captured

in discount rate

Value to a

financial/LBO

buyer

Value based ondebt repayment

and return on

equity investment

Liquidation

analysis

Break-up analysis

Historical trading

performance

Expected IPO

valuation

EPS impact

Dividend discountmodel

32 D I S C O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 34/71

Overview of DCF analysis

CommentsComments

Discounted cash flow analysis is based upon the theory that the value of a business is the sum of

its expected future free cash flows, discounted at an appropriate rate

DCF analysis is one of the most fundamental and commonly-used valuation techniques

Widely accepted by bankers, corporations and academics

– Corporate clients often use DCF analysis internally

One of several techniques used in M&A transactions; others include:

– Comparable companies analysis

– Comparable transaction analysis

– Leveraged buyout analysis

– Recapitalization analysis, liquidation analysis, etc.

DCF analysis may be the only valuation method utilized, particularly if no comparable

publicly-traded companies or precedent transactions are available

Discountedcash flowanalysis

33 D I S C O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 35/71

Overview of DCF analysis (cont’d)

CommentsComments

DCF analysis is a forward-looking valuation approach, based on several key projections and

assumptions

Free cash flows

– What is the projected operating and financial performance of the business?

Terminal value

– What will be the value of the business at the end of the projection period?

Discount rate

– What is the cost of capital (equity and debt) for the business?

Depending on practical requirements and availability of data, DCF analysis can be simple or

extremely elaborate

There is no single “correct” method of performing DCF analysis, but certain rules of thumb

always apply

Do not simply plug numbers into equations

You must apply judgment in determining each assumption

Discountedcash flowanalysis

34 D I S C O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 36/71

The process of DCF analysis

Project the operating results and free cash flows of the business overthe forecast period (typically 10 years, but can be 5–20 yearsdepending on the profitability horizon)

Estimate the exit multiple and/or growth rate in perpetuity of thebusiness at the end of the forecast period

Estimate the company’s weighted-average cost of capital to determinethe appropriate discount rate range

Determine a range of values for the enterprise by discounting theprojected free cash flows and terminal value to the present

Adjust the resulting valuation for all assets and liabilities not accountedfor in cash flow projections

Projections/FCF

Terminal value

Discount rate

Present value

Adjustments

Discountedcash flowanalysis

Process overviewProcess overview

35 D I S C O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 37/71

Projecting financial statements

Ideally projections should go out as far into the future as can reasonably be estimated to reduce

dependence on the terminal value

Most important assumptions:

Sales growth: Use divisional, product-line or location-by-location build-up or simple growth

assumptions

Operating margins: Evaluate improvement over time, competitive factors, SG&A costs

Synergies: Estimate dollars in Year 1 and evaluate margin impact over time

Depreciation: Should conform with historic and projected capex Capital expenditures: Consider both maintenance and expansion capex

Changes in net working capital: Should correspond to historical patterns and grow as the

business grows

Should show historical financial performance and sanity check projections against past results.

Be prepared to articulate why projections may or may not be similar to past results (e.g.

reasons behind margin improvements, increased sales growth, etc.)

Analyze projections for consistency

Sales increases usually require working capital increases

Capex and depreciation should converge over time

CommentsComments

Discountedcash flowanalysis

36 D I S C O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

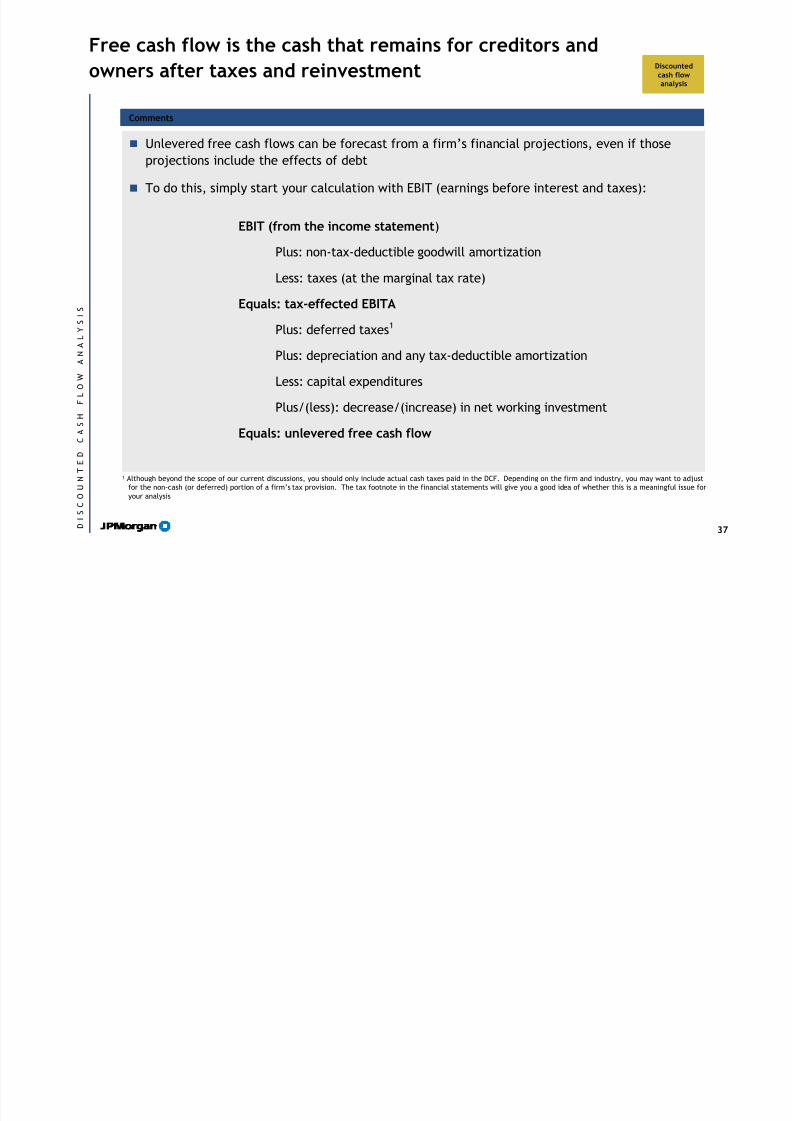

Free cash flow is the cash that remains for creditors and

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 38/71

Unlevered free cash flows can be forecast from a firm’s financial projections, even if those

projections include the effects of debt

To do this, simply start your calculation with EBIT (earnings before interest and taxes):

CommentsComments

Free cash flow is the cash that remains for creditors and

owners after taxes and reinvestment

EBIT (from the income statement)

Plus: non-tax-deductible goodwill amortization

Less: taxes (at the marginal tax rate)

Equals: tax-effected EBITA

Plus: deferred taxes1

Plus: depreciation and any tax-deductible amortization

Less: capital expenditures

Plus/(less): decrease/(increase) in net working investment

Equals: unlevered free cash flow

1 Although beyond the scope of our current discussions, you should only include actual cash taxes paid in the DCF. Depending on the firm and industry, you may want to adjustfor the non-cash (or deferred) portion of a firm’s tax provision. The tax footnote in the financial statements will give you a good idea of whether this is a meaningful issue foryour analysis

Discountedcash flowanalysis

37 D I S C O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 39/71

2003 2004 2005 2006E 2007E 2008E 2009E 2010E

Net sales $400.0 $440.0 $484.0 $532.4 $585.6 $644.2 $708.6 $779.5

EBITDA 80.0 88.0 96.8 106.5 117.1 128.8 141.7 155.9

Less: depreciation 12.0 13.2 14.5 16.0 17.6 19.3 21.3 23.4

EBITA 68.0 74.8 82.3 90.5 99.6 109.5 120.5 132.5Less: taxes at marginal rate 27.2 29.9 32.9 36.2 39.8 43.8 48.2 53.0

Tax-effected EBITA $40.8 $44.9 $49.4 $54.3 $59.7 $65.7 $72.3 $79.5

Plus: depreciation 16.0 17.6 19.3 21.3 23.4

Plus: deferred taxes – – – – –

Less: capital expenditures 20.0 22.0 24.2 26.6 29.3

Less: incr./(decr.) in working capital 10.0 8.5 7.0 5.5 4.0Unlevered free cash flow 40.3 46.8 53.8 61.4 69.6

Adjustment for deal date (40.3) – – – –

Unlevered FCF to acquirer $0.0 $46.8 $53.8 $61.4 $69.6

Stand-alone DCF analysis of Company X ($ millions)Stand-alone DCF analysis of Company X ($ millions)

Example: Calculating unlevered free cash flows

Key assumptions:Deal/valuation date = 12/31/06Marginal tax rate = 40%

Discountedcash flowanalysis

38 D I S C O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

Once unlevered free cash flows are calculated, they must

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 40/71

The standard present value calculation takes into account the cost of capital by attributing

greater value to cash flows generated earlier in the projection period than later cash flows

Since most businesses do not generate all of their free cash flows on the last day of the year,

but rather more-or-less continuously during the year, DCF analyses often use the so-called

“mid-year convention,” which takes into account the fact that free cash flows occur during theyear

This approach moves each cash flow from the end of the applicable period to the middle of the

same period (i.e., cash flows are moved closer to the present)

CommentsComments

FCF1 FCF2 FCF3 FCFn

Present value = (1+r)1 + (1+r)2 + (1+r)3 + . . . + (1+r)n

FCF1 FCF2 FCF3 FCFn Present value =

(1+r)0.5 +

(1+r)1.5 +

(1+r)2.5 +

. . .+

(1+r)n-0.5

, y

be discounted to the present

JPMorganstandard

Discountedcash flowanalysis

39 D I S C O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

It is important to differentiate between the transaction

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 41/71

p

date and the mid-year convention

Transaction date: 01/01

Year 0 1 2 30.5 1.5 2.5 3.5

First cash flow,mid-year 1

Second cash flow,mid-year 2

Third cash flow,mid-year 3

Discounting =CF1

(1+r)0.5+

CF2

(1+r)1.5+

CF3

(1+r)2.5+ ….

Example 1Example 1

Transaction date: 06/30

Year 0 1 2 30.5 1.5 2.5 3.5

First cash flow,mid-period 1

Second cash flow,mid-year 2

Third cash flow,mid-year 3

Discounting =CF1

(1+r)(0.75-0.5)+

CF2

(1+r)(1.5-0.5)+

CF3

(1+r)(2.5-0.5)+ ….

Example 2Example 2

0.75

Discountedcash flowanalysis

40 D I S C

O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 42/71

Discounting free cash flows

Key assumptions:Deal/valuation date = 12/31/06Marginal tax rate = 40%

Discount rate = 10%

$189.6 =$46.8

(1+.10)0.5

$53.8

(1+.10)1.5

$61.4

(1+.10)2.5

$69.6

(1+.10)3.5+ + +Formula

2003 2004 2005 2006E 2007E 2008E 2009E 2010E

Net sales $400.0 $440.0 $484.0 $532.4 $585.6 $644.2 $708.6 $779.5

EBITDA 80.0 88.0 96.8 106.5 117.1 128.8 141.7 155.9

Less: Depreciation 12.0 13.2 14.5 16.0 17.6 19.3 21.3 23.4

EBITA 68.0 74.8 82.3 90.5 99.6 109.5 120.5 132.5

Less: Taxes at marginal rate 27.2 29.9 32.9 36.2 39.8 43.8 48.2 53.0

Tax-effected EBITA $40.8 $44.9 $49.4 $54.3 $59.7 $65.7 $72.3 $79.5

Plus: Depreciation 16.0 17.6 19.3 21.3 23.4

Plus: Deferred taxes – – – – –

Less: Capital expenditures 20.0 22.0 24.2 26.6 29.3

Less: Incr./(decr.) in working capital 10.0 8.5 7.0 5.5 4.0

Unlevered free cash flow 40.3 46.8 53.8 61.4 69.6Adjustment for deal date (40.3) – – – –

Unlevered FCF to acquirer $0.0 $46.8 $53.8 $61.4 $69.6

Memo: discounting factor 0.0 0.5 1.5 2.5 3.5

Discounted value of unlevered FCF $0.0 $44.6 $46.7 $48.4 $49.9

Discounted value of FCF 2007E–2010E 189.6

Stand-alone DCF analysis of Company X ($ millions)Stand-alone DCF analysis of Company X ($ millions)

Discountedcash flowanalysis

41 D I S C

O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

Terminal value can account for a significant portion of

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 43/71

value in a DCF analysis

Terminal value represents the business’s value at the end of the projection period; i.e., theportion of the company’s total value attributable to cash flows expected after the projectionperiod

Terminal value is typically based on some measure of the performance of the business in theterminal year of the projection (which should depict the business operating in a steady-state/normalized manner)

Terminal (or “Exit”) multiple method

– Assumes that the business is valued/sold at the end of the terminal year at a multipleof some financial metric (typically EBITDA)

Growth in perpetuity method

– Assumes that the business is held in perpetuity and that free cash flows continue togrow at an assumed rate

A terminal multiple will have an implied growth rate and vice versa. It is essential toreview the implied multiple/growth rate for sanity check purposes

Once calculated, the terminal value is discounted back to the appropriate date using therelevant rate

Attempt to reduce dependence on the terminal value What is appropriate projection time frame? What percentage of total value comes from the terminal value?

CommentsComments

Discountedcash flowanalysis

42 D I S C

O

U N T E D

C A S H

F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 44/71

Terminal multiple method

This method assumes that the business will be valued at the end of the last year of theprojected period

The terminal value is generally determined as a multiple of EBIT, EBITDA, or EBITDAR; this

value is then discounted to the present, as were the interim free cash flows

The terminal value should be an asset (firm) value; remember that not all multiples

produce an asset value

Note that in the exit multiple method terminal value is always assumed to be calculated at

the end of the final projected year, irrespective of whether you are using the mid-year

convention

Should the terminal multiple be an LTM multiple or a forward multiple?

If the terminal value is based on the last year of your projection then the multiple should

be based on an LTM multiple (most common)

There are circumstances where you will project an additional year of EBITDA and apply aforward multiple

CommentsComments

Discountedcash flowanalysis

43 D I S C

O

U N T E D

C A S H F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 45/71

Fiscal year ending December 31,

2003 2004 2005 2006E 2007E 2008E 2009E 2010E

Net sales $400.0 $440.0 $484.0 $532.4 $585.6 $644.2 $708.6 $779.5

EBITDA 80.0 88.0 96.8 106.5 117.1 128.8 141.7 155.9

Less: Depreciation 12.0 13.2 14.5 16.0 17.6 19.3 21.3 23.4

EBITA 68.0 74.8 82.3 90.5 99.6 109.5 120.5 132.5

Less: Taxes at marginal rate 27.2 29.9 32.9 36.2 39.8 43.8 48.2 53.0

Tax-effected EBITA $40.8 $44.9 $49.4 $54.3 $59.7 $65.7 $72.3 $79.5

Plus: Depreciation 16.0 17.6 19.3 21.3 23.4

Plus: Deferred taxes – – – – –

Less: Capital expenditures 20.0 22.0 24.2 26.6 29.3

Less: Incr./(decr.) in working capital 10.0 8.5 7.0 5.5 4.0

Unlevered free cash flow $40.3 $46.8 $53.8 $61.4 $69.6

Adjustment for deal date (40.3) – – – –

Unlevered FCF to acquirer $0.0 $46.8 $53.8 $61.4 $69.6

Memo: Discounting factor 0.0 0.5 1.5 2.5 3.5

Discounted value of unlevered FCF $0.0 $44.6 $46.7 $48.4 $49.9

Discounted value of FCF 2007E–2010E 189.6

EBITDA in 2010E $155.9

Exit multiple 7.0x

Firm value at exit 1,091.3

Discounted terminal value 745.4

Total present value to acquirer $934.9

Stand-alone DCF analysis of Company X ($ millions)Stand-alone DCF analysis of Company X ($ millions)

EXAMPLE: Terminal multiple method

$745.4 =($155.9 * 7.0x)

(1+.10)4

Formula

Note: Key assumptions:Deal/valuation date = 12/31/06

Marginal tax rate = 40%Discount rate = 10%Exit multiple of EBITDA = 7.0x

Discountedcash flowanalysis

44 D I S C

O

U N T E D

C A S H F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 46/71

A + B = C

Discounted

FCF

Discounted terminal value

at 2010E multiple of

Firm value at 2010E

EBITDA multiple of

Discount rate 2006-2010 6.0x 7.0x 8.0x 6.0x 7.0x 8.0x

8% $196.8 $687.5 $802.1 $916.7 $884.4 $999.0 $1,113.6

9% 193.1 662.6 773.1 883.5 855.8 966.2 1,076.7

10% 189.6 638.9 745.4 851.8 828.4 934.9 1,041.4

11% 186.1 616.2 718.9 821.6 802.3 904.9 1,007.6

12% 182.7 594.5 693.5 792.6 777.2 876.3 975.3

- D = E

Net debt

Equity value at 2010E

EBITDA multiple of

Equity value per share1 at

2010E EBITDA multiple of

Discount rate 12/31/06 6.0x 7.0x 8.0x 6.0x 7.0x 8.0x

8% $100.0 $784.4 $899.0 $1,013.6 $19.17 $21.97 $24.77

9% 100.0 755.8 866.2 976.7 $18.47 $21.17 $23.87

10% 100.0 728.4 834.9 941.4 $17.80 $20.41 $23.01

11% 100.0 702.3 804.9 907.6 $17.16 $19.67 $22.18

12% 100.0 677.2 776.3 875.3 $16.55 $18.97 $21.39

Stand-alone DCF analysis of Company X ($ millions, except per share data)Stand-alone DCF analysis of Company X ($ millions, except per share data)

EXAMPLE: Terminal multiple method (cont’d)

1 Based on 40.0 million basic shares outstanding and 2.0 million options with a weighted exercise price of $8.13 calculated using the treasury methodNote: DCF value as of 12/31/06 based on mid-year convention

Discountedcash flowanalysis

45 D I S C

O

U N T E D

C A S H F

L O

W

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 47/71

G th i t it th d ( t’d) Discounted

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 48/71

Note that when using the mid-year convention, terminal value is discounted as if cash flowsoccur in the middle of the final projection period

Here the growth-in-perpetuity method differs from the exit-multiple method

Typical adjustments to normalize free cash flow in Year n include revising the relationshipbetween revenues, EBIT and capital spending, which in turn affects CAPEX and depreciation

Working capital may also need to be adjusted

Often capex and depreciation are assumed to be equal

CommentsComments

Growth in perpetuity method (cont’d) Discountedcash flowanalysis

47 D I S C

O

U N T E D

C A S H F

L O

W

A N A L Y S I S

EXAMPLE G th i t it th d Discounted

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 49/71

Fiscal year ending December 31,

2003 2004 2005 2006E 2007E 2008E 2009E 2010E

Net sales $400.0 $440.0 $484.0 $532.4 $585.6 $644.2 $708.6 $779.5

EBITDA 80.0 88.0 96.8 106.5 117.1 128.8 141.7 155.9

Less: Depreciation 12.0 13.2 14.5 16.0 17.6 19.3 21.3 23.4

EBITA 68.0 74.8 82.3 90.5 99.6 109.5 120.5 132.5

Less: Taxes at marginal rate 27.2 29.9 32.9 36.2 39.8 43.8 48.2 53.0

Tax-effected EBITA $40.8 $44.9 $49.4 $54.3 $59.7 $65.7 $72.3 $79.5

Plus: Depreciation 16.0 17.6 19.3 21.3 23.4

Plus: Deferred taxes – – – – –

Less: Capital expenditures 20.0 22.0 24.2 26.6 29.3

Less: Incr./(decr.) in working capital 10.0 8.5 7.0 5.5 4.0

Unlevered free cash flow 40.3 46.8 53.8 61.4 69.6

Adjustment for deal date (40.3) – – – –

Unlevered FCF to acquirer $0.0 $46.8 $53.8 $61.4 $69.6

Memo: Discounting factor 0.0 0.5 1.5 2.5 3.5

Discounted value of unlevered FCF $0.0 $44.6 $46.7 $48.4 $49.9

Discounted value of FCF 2007E–2010E 189.6

Value 2010E - Terminal Value 733.7

Total present value to acquirer $923.3

Stand-alone DCF analysis of Company X ($ millions)Stand-alone DCF analysis of Company X ($ millions)

EXAMPLE: Growth in perpetuity method

$733.7 =$69.6 * (1 + .03)

(.10-.03)*(1+.10)3.5

Formula

Note: Key assumptions:Deal/valuation date = 12/31/06Marginal tax rate = 40%Discount rate = 10%Perpetuity growth rate = 3%

Discountedcash flowanalysis

48 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

EXAMPLE: Growth in perpetuity method (cont’d) Discounted

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 50/71

A + B = C

Discounted

FCF

Discounted terminal value

at perpetuity growth rate of

Firm value at perpetuity

growth rate of

Discount rate 2006-2010 2.5% 3.0% 3.5% 2.5% 3.0% 3.5%

8% $196.8 $991.0 $1,095.4 $1,223.0 $1,187.8 $1,292.2 $1,419.8

9% 193.1 811.9 883.8 968.9 1,005.0 1,077.0 1,162.0

10% 189.6 681.5 733.7 794.0 871.1 923.3 983.6

11% 186.1 582.6 622.0 666.7 768.7 808.1 852.8

12% 182.7 505.1 535.8 570.1 687.9 718.5 752.8

- D = E

Net debt

Equity value at perpetuity

growth rate of

Equity value per share1 at

perpetuity growth rate of

Discount rate 12/31/06 2.5% 3.0% 3.5% 2.5% 3.0% 3.5%

8% $100.0 $1,087.8 $1,192.2 $1,319.8 $26.59 $29.14 $32.26

9% 100.0 905.0 977.0 1,062.0 $22.12 $23.88 $25.96

10% 100.0 771.1 823.3 883.6 $18.84 $20.12 $21.59

11% 100.0 668.7 708.1 752.8 $16.34 $17.31 $18.40

12% 100.0 587.9 618.5 652.8 $14.37 $15.12 $15.95

Stand-alone DCF analysis of Company X ($ millions, except per share data)Stand-alone DCF analysis of Company X ($ millions, except per share data)

EXAMPLE: Growth in perpetuity method (cont’d)

1 Based on 40.0 million basic shares outstanding and 2.0 million options with a weighted exercise price of $8.13 calculated using the treasury methodNote: DCF value as of 12/31/06 based on mid-year convention

Discountedcash flowanalysis

49 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

Terminal multiples and perpetuity growth rates are often

considered side by side Discounted

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 51/71

Assumptions regarding exit multiples are often checked for reasonableness by calculating thegrowth rates in perpetuity that they imply (and vice versa)

To go from the exit-multiple approach to an implied perpetuity growth rate:

g = [(WACC*terminal value) / (1+WACC)0.5 - FCFn] / [FCFn + (terminal value / (1 + WACC)0.5)]

To go from the growth-in-perpetuity approach to an implied exit multiple:

multiple = [FCFn * (1 + g)(1 + WACC)0.5] / [EBITDAn * (WACC - g)]

These formulas adjust for the different approaches to discounting terminal value when using

the mid-year convention

CommentsComments

considered side-by-side cash flowanalysis

50 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

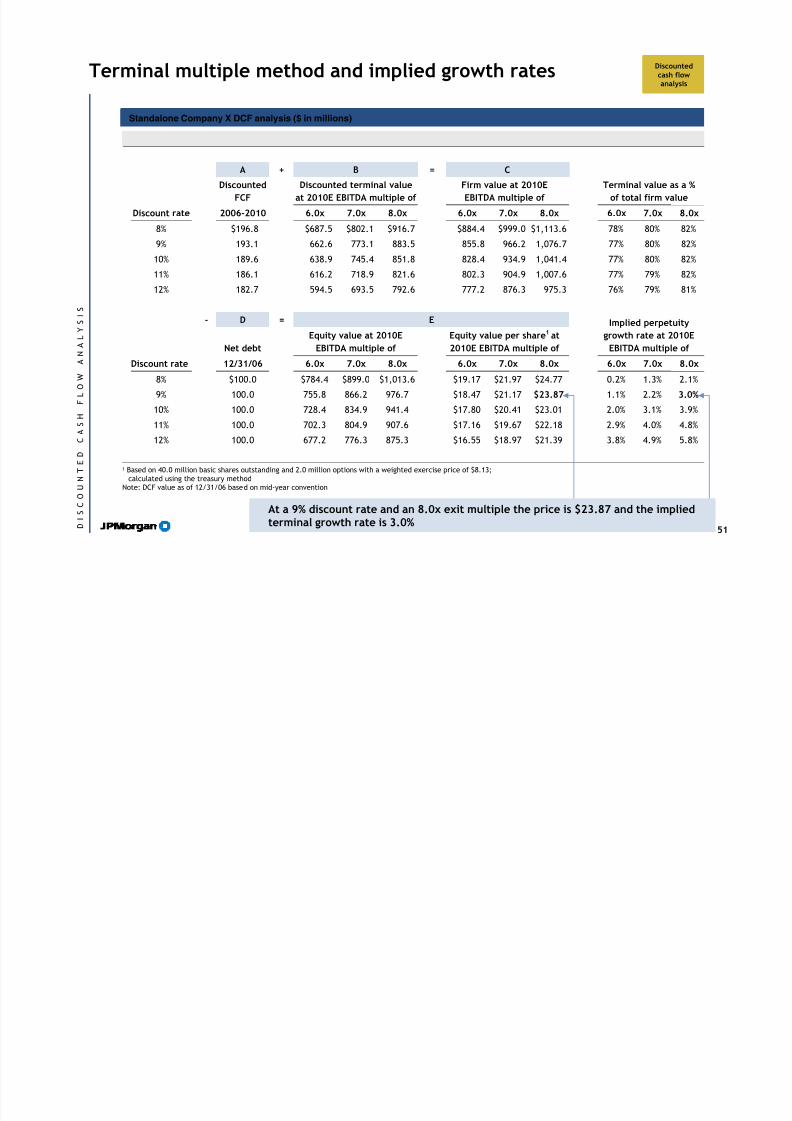

Terminal multiple method and implied growth rates

Discounted

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 52/71

A + B = C

Discounted

FCF

Discounted terminal value

at 2010E EBITDA multiple of

Firm value at 2010E

EBITDA multiple of

Terminal value as a %

of total firm value

Discount rate 2006-2010 6.0x 7.0x 8.0x 6.0x 7.0x 8.0x 6.0x 7.0x 8.0x

8% $196.8 $687.5 $802.1 $916.7 $884.4 $999.0 $1,113.6 78% 80% 82%

9% 193.1 662.6 773.1 883.5 855.8 966.2 1,076.7 77% 80% 82%

10% 189.6 638.9 745.4 851.8 828.4 934.9 1,041.4 77% 80% 82%

11% 186.1 616.2 718.9 821.6 802.3 904.9 1,007.6 77% 79% 82%

12% 182.7 594.5 693.5 792.6 777.2 876.3 975.3 76% 79% 81%

- D = E

Net debt

Equity value at 2010E

EBITDA multiple of

Equity value per share1 at

2010E EBITDA multiple of

Implied perpetuity

growth rate at 2010E

EBITDA multiple of

Discount rate 12/31/06 6.0x 7.0x 8.0x 6.0x 7.0x 8.0x 6.0x 7.0x 8.0x

8% $100.0 $784.4 $899.0 $1,013.6 $19.17 $21.97 $24.77 0.2% 1.3% 2.1%

9% 100.0 755.8 866.2 976.7 $18.47 $21.17 $23.87 1.1% 2.2% 3.0%

10% 100.0 728.4 834.9 941.4 $17.80 $20.41 $23.01 2.0% 3.1% 3.9%

11% 100.0 702.3 804.9 907.6 $17.16 $19.67 $22.18 2.9% 4.0% 4.8%

12% 100.0 677.2 776.3 875.3 $16.55 $18.97 $21.39 3.8% 4.9% 5.8%

Terminal multiple method and implied growth rates

1 Based on 40.0 million basic shares outstanding and 2.0 million options with a weighted exercise price of $8.13;calculated using the treasury method

Note: DCF value as of 12/31/06 based on mid-year convention

At a 9% discount rate and an 8.0x exit multiple the price is $23.87 and the impliedterminal growth rate is 3.0%

Standalone Company X DCF analysis ($ in millions)Standalone Company X DCF analysis ($ in millions)

cash flowanalysis

51 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

Perpetuity growth rate and implied terminal multiples

Discountedh l

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 53/71

A + B = C

Discounted

FCF

Discounted terminal value

at perpetuity growth rate of

Firm value at perpetuity

growth rate of

Terminal value as a %

of total firm value

Discount rate 2006-2010 2.5% 3.0% 3.5% 2.5% 3.0% 3.5% 2.5% 3.0% 3.5%

8% $196.8 $991.0 $1,095.4 $1,223.0 $1,187.8 $1,292.2 $1,419.8 83% 85% 86%

9% 193.1 811.9 883.8 968.9 1,005.0 1,077.0 1,162.0 81% 82% 83%

10% 189.6 681.5 733.7 794.0 871.1 923.3 983.6 78% 79% 81%

11% 186.1 582.6 622.0 666.7 768.7 808.1 852.8 76% 77% 78%

12% 182.7 505.1 535.8 570.1 687.9 718.5 752.8 73% 75% 76%

- D = E

Net debt

Equity value at perpetuity

growth rate of

Equity value per share1 at

perpetuity growth rate of

Implied EBITDA exit

multiple at perpetuity

growth rate of

Discount rate 12/31/06 2.5% 3.0% 3.5% 2.5% 3.0% 3.5% 2.5% 3.0% 3.5%

8% $100.0 $1,087.8 $1,192.2 $1,319.8 $26.59 $29.14 $32.26 8.6x 9.6x 10.7x

9% 100.0 905.0 977.0 1,062.0 $22.12 $23.88 $25.96 7.4 8.0 8.8

10% 100.0 771.1 823.3 883.6 $18.84 $20.12 $21.59 6.4 6.9 7.5

11% 100.0 668.7 708.1 752.8 $16.34 $17.31 $18.40 5.7 6.1 6.5

12% 100.0 587.9 618.5 652.8 $14.37 $15.12 $15.95 5.1 5.4 5.8

Perpetuity growth rate and implied terminal multiples

1 Based on 40.0 million basic shares outstanding and 2.0 million options with a weighted exercise price of $8.13;calculated using the treasury method

Note: DCF value as of 12/31/06 based on mid-year convention

At a 9% discount rate and terminal growth rate of 3.0%, the price is $23.88 and theimplied EBITDA exit multiple is 8.0x

Standalone Company X DCF analysis ($ in millions)Standalone Company X DCF analysis ($ in millions)

cash flowanalysis

52 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

Choosing the discount rate is a critical step in DCF analysis Discountedh fl

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 54/71

The discount rate represents the required rate of return given the risks inherent in the business,its industry, and thus the uncertainty regarding its future cash flows, as well as its optimalcapital structure

Typically the weighted average cost of capital (WACC) will be used as a foundation for settingthe discount rate

The WACC is always forward-looking and is predicted based on the expectations of aninvestment's future performance; an investor contributes capital with the expectation that theriskiness of cash flows will be offset by an appropriate return

The WACC is typically estimated by studying capital costs for existing investment opportunitiesthat are similar in nature and risk to the one being analyzed

The WACC is related to the risk of the investment, not the risk or creditworthiness of theinvestor¹

CommentsComments

Choosing the discount rate is a critical step in DCF analysis

1 In valuing a company, always use the riskiness of its cash flows or comparable companies in estimating a weighted average cost of capital. Never use the acquirer’scost capital unless, by some chance, it is engaged in an extremely similar line of business. However, if a business is small relative to an acquirer's, sometimes ti maybe appropriate to consider the use of the acquirer's WACC in performing the valuation. The additional value created by using the acquirer's WACC can be viewed as a

synergy to the acquirer in the context of the transaction.

cash flowanalysis

53 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

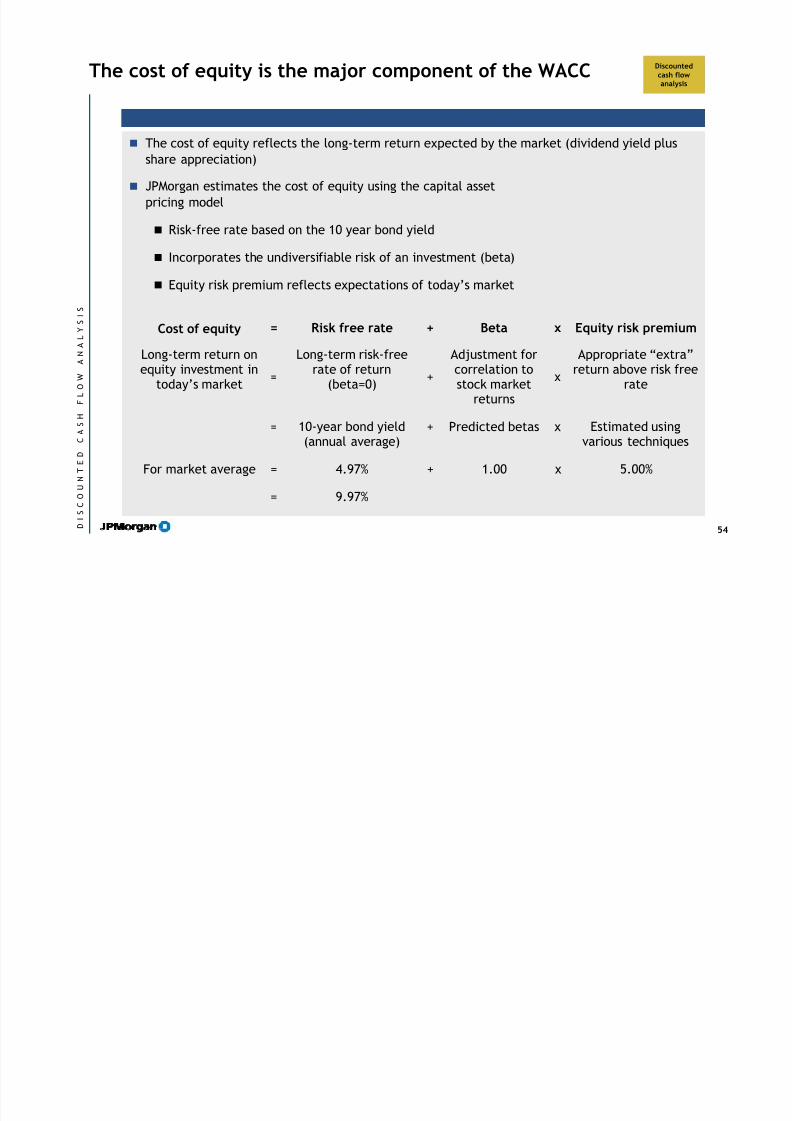

The cost of equity is the major component of the WACC Discountedcash flow

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 55/71

The cost of equity reflects the long-term return expected by the market (dividend yield plusshare appreciation)

JPMorgan estimates the cost of equity using the capital assetpricing model

Risk-free rate based on the 10 year bond yield

Incorporates the undiversifiable risk of an investment (beta)

Equity risk premium reflects expectations of today’s market

The cost of equity is the major component of the WACC

Cost of equity = Risk free rate + Beta x Equity risk premium

Long-term return onequity investment in

today’s market=

Long-term risk-freerate of return

(beta=0)+

Adjustment forcorrelation tostock market

returns

x

Appropriate “extra”return above risk free

rate

= 10-year bond yield(annual average)

+ Predicted betas x Estimated usingvarious techniques

For market average = 4.97% + 1.00 x 5.00%

= 9.97%

cash flowanalysis

54 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

The cost of equity and debt are blended together based

on a target capital structure

Discountedcash flow

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 56/71

The target capital structure reflects the company’s rating objective

Firms generally try to minimize the cost of capital through the appropriate use of leverage

The percentage weighting of debt and equity is usually based on the market value of a firm’s equity and debtposition

Most firms are at their target capital structure

Adjustments should be made for seasonal or cyclical swings, as well as for firms moving toward a target

Using a weighted average cost of capital assumes that all investments are funded with the same mix of equityand debt as the target capital structure

CommentsComments

Cost of equity Cost of debtCost of capital10-year T-bond (Avg) 4.97%

Market risk premium 5.00%(x) Beta (current predicted) 0.62Adjusted market premium 3.10%

Cost of equity = 8.07%

Cost of debt 6.25%

(-) Tax shield1 2.19%

After-tax cost of debt 4.06%

on a target capital structure

Target capital structure(Assumes current = optimal)

Debt/total capital = 6.1%

Nominal WACC = 7.82%1 Assumes 35% marginal tax rate

WACC = rd * [D *(1-T)] + re * ED+E D+E Where:

E = Market value of equityD = Market value of debt

T = Marginal tax ratere = Return on equityrd = Return on debt

WACC formula

Illustrative Weighted Average Cost of Capital calculationIllustrative Weighted Average Cost of Capital calculation

cash flowanalysis

55 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

The appropriate cost of capital will depend on the entity

which is being valued

Discountedcash flow

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 57/71

g

Note: Assumes 35% marginal tax rate1 Assuming an equity risk premium of 6.5%2 Assuming an equity risk premium of 7.5%

Debt/equity

10% 20% 30% 40%

0.65 7.8% 7.5% 7.3% 7.0%

0.70 8.1% 7.7% 7.5% 7.2%

0.75 8.3% 7.9% 7.7% 7.4%

0.80 8.5% 8.2% 7.8% 7.6% L e v e r e d

b e t a

0.85 8.8% 8.4% 8.0% 7.8%

WACC sensitivityWACC sensitivity

Debt/equity

10% 20% 30% 40%

0.70 9.1% 8.7% 8.4% 8.2%

0.75 9.4% 9.0% 8.7% 8.4%

0.80 9.7% 9.3% 8.9% 8.7%

0.85 10.0% 9.6% 9.2% 8.9% L e v e r e d

b e t a

0.90 10.3% 9.8% 9.4% 9.1%

$1 billion target WACC sensitivity1$1 billion target WACC sensitivity1

Debt/equity

10% 20% 30% 40%

0.70 9.8% 9.4% 9.1% 8.9%

0.75 10.1% 9.8% 9.4% 9.1%

0.80 10.5% 10.1% 9.7% 9.4%

0.85 10.8% 10.4% 10.0% 9.7% L e v e r e d

b e t a

0.90 11.2% 10.7% 10.3% 10.0%

$200 million target WACC sensitivity2$200 million target WACC sensitivity2

For illustrative purposesFor illustrative purposes

CompanyRisk

premiumUnlevered

betaOptimal

debt/equityRe-levered

betaCost ofequity

Cost offinancing WACC

$1 billion target 5.0% - 6.5% 0.70 20% 0.80 9.0% - 10.3% 6.25% - 7.50% 8.3% - 9.3%

$500 million target 5.0% - 7.0% 0.70 20% 0.80 9.0% - 10.6% 6.25% - 8.00% 8.4% - 9.7%

$200 million target 5.0% - 7.5% 0.70 20% 0.80 9.0% - 11.0% 6.25% - 8.50% 8.4% - 10.1%

analysis

56 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

Most common errors in calculating WACC

Discountedcash flow

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 58/71

Equity risk premium based on very long time frame (post 1926: Ibbotson data)

Substitute hurdle rate (goal) for cost of capital

Use of historical (or predicted) betas that are clearly wrong

Investment specific risk not fully incorporated (e.g., country risk premiums)

Incorrect releveraging of the cost of equity

Cost of equity based on book returns, not market expectations

Cost of equityCost of equity

g

The actual, not target, capital structure is used

WACC calculated based on book weights

Target capital structureTarget capital structure

analysis

57 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

EXAMPLE: DCF output

Discountedcash flow

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 59/71

p

Projected FY ending March 31,LTMSept 30, 2006 2007 2008 2009 2010 2011

Sales $803.5 $900.0 $1,000.0 $1,030.0 $1,060.9 $1,092.7

EBITDA 55.1 63.0 75.0 77.3 79.6 82.0

% EBITDA Margin 6.9% 7.0% 7.5% 7.5% 7.5% 7.5%

Less: depreciation & amortization 17.8 20.5 21.8 23.1 24.5 25.9EBIT 37.3 42.5 53.2 54.1 55.1 56.1

Less: taxes @ 38.0% 14.2 16.1 20.2 20.6 20.9 21.3

EBIAT $23.1 $26.3 $33.0 $33.6 $34.2 $34.8

Plus: depreciation & amortization $20.5 $21.8 $23.1 $24.5 $25.9

Less: capital expenditures 8.8 9.0 9.3 9.5 9.8

Less: Incr./(decr.) in working capital 8.1 8.8 2.6 2.7 2.8

Unlevered free cash flow $30.0 $37.0 $44.8 $46.4 $48.1

Summary financials ($ in millions)Summary financials ($ in millions)

Source: Historical information from 10-K dated 3/31/06 and 10Q dated 9/30/06; Projections are Illustrative JPMorgan estimates, assumes revenue of $900 million for FYE3/31/07, $1 billion for FYE 3/31/08, 3% revenue growth thereafter, and constant EBITDA margins after FYE 3/31/08

Firm value atperpetuity growth

rate of

0.0% 1.0% 2.0%

10.00% $474 $512 $560

10.50% $451 $485 $527

D i s c o u n t

R a t e

11.00% $430 $461 $498

Implied EBITDA exit multipleImplied EBITDA exit multipleFirm value ($ in millions)Firm value ($ in millions)

Implied 2011 EBITDAmultiple at perpetuity

growth rate of

0.0% 1.0% 2.0%

10.00% 6.2x 6.9x 7.8x

10.50% 5.9x 6.6x 7.4x

D i s c o u n t

R a t e

11.00% 5.6x 6.2x 7.0x

Implied stock price atperpetuity growth

rate of

0.0% 1.0% 2.0%

10.00% $31.28 $34.49 $38.52

10.50% $29.36 $32.22 $35.75

D i s c o u n t

R a t e

11.00% $27.62 $30.17 $33.29

Implied equity value per shareImplied equity value per share

analysis

58 D I S C

O

U N T E D

C A S H

F L O

W

A N A L Y S I S

Agenda

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 60/71

LBO analysis

Discounted cash flow analysis

Transaction comparables

Trading comparables

Introduction

59

1

6

20

31

59

M

& A

V A L U A T I O

N

O V

E R V I E W

Valuation methodologies

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 61/71

Publicly traded

comparablecompanies analysis

Comparable

transactionsanalysis

Valuationmethodologies

Discounted

cash flowanalysis

Leveraged

buyout/recapanalysis

Other

“Public Market

Valuation”

Value based on

market trading

multiples ofcomparable

companies

Applied using

historical and

prospective

multiples

Does not include a

control premium

“Private Market

Valuation”

Value based on

multiples paid for

comparablecompanies in sale

transactions

Includes control

premium

“Intrinsic” value

of business

Present value of

projected free

cash flows

Incorporates both

short-term and

long-term

expected

performance

Risk in cash flowsand capital

structure captured

in discount rate

Value to a

financial/LBO

buyer

Value based on

debt repaymentand return on

equity investment

Liquidation

analysis

Break-up analysis

Historical tradingperformance

Expected IPO

valuation

EPS impact

Dividend discount

model

60 L B O

A N A L Y S I S

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 62/71

The process of LBO analysis Leveragedbuyout/recap

analysis

8/12/2019 McCombs 2007 Valuation Presentation 103007

http://slidepdf.com/reader/full/mccombs-2007-valuation-presentation-103007 63/71

a alys s

Develop an integrated model of the business that projects EBITDA andcash available for debt repayment over the investment horizon(typically 3–5 years)

Estimate the multiple at which the sponsor can be expected to exit theinvestment at the end of the investment period

Determine a transaction structure and a pro forma capital structure thatresult in realistic financial coverage

Calculate returns (IRR) to the equity sponsor

Tweak the transaction/capital structure as needed to achieve harmony(if possible) between IRR, leverage and valuation

Projections/FCF

Terminal value

Discount rate

Present value

Adjustments

Process overviewProcess overview

62 L B O