mc corvie - healthcare reform: how to get here from there

TRANSCRIPT

Health Care ReformHealth Care ReformHow to Get from Here to ThereHow to Get from Here to There

Major Plan Design ChangesMajor Plan Design Changes

For plans years beginning after September 23, 2010

(2011 Calendar Year Plans)

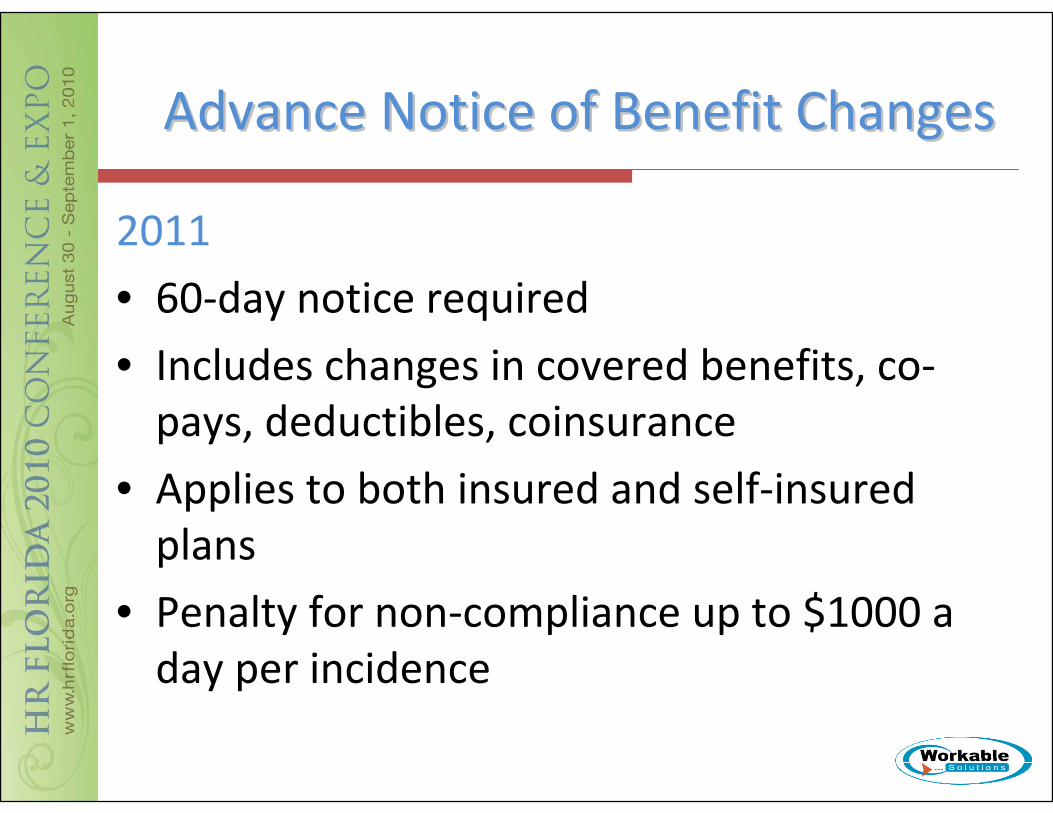

Advance Notice of Benefit ChangesAdvance Notice of Benefit Changes

2011

• 60‐day notice required

• Includes changes in covered benefits, co‐pays, deductibles, coinsurance

• Applies to both insured and self‐insured plans

• Penalty for non‐compliance up to $1000 a day per incidence

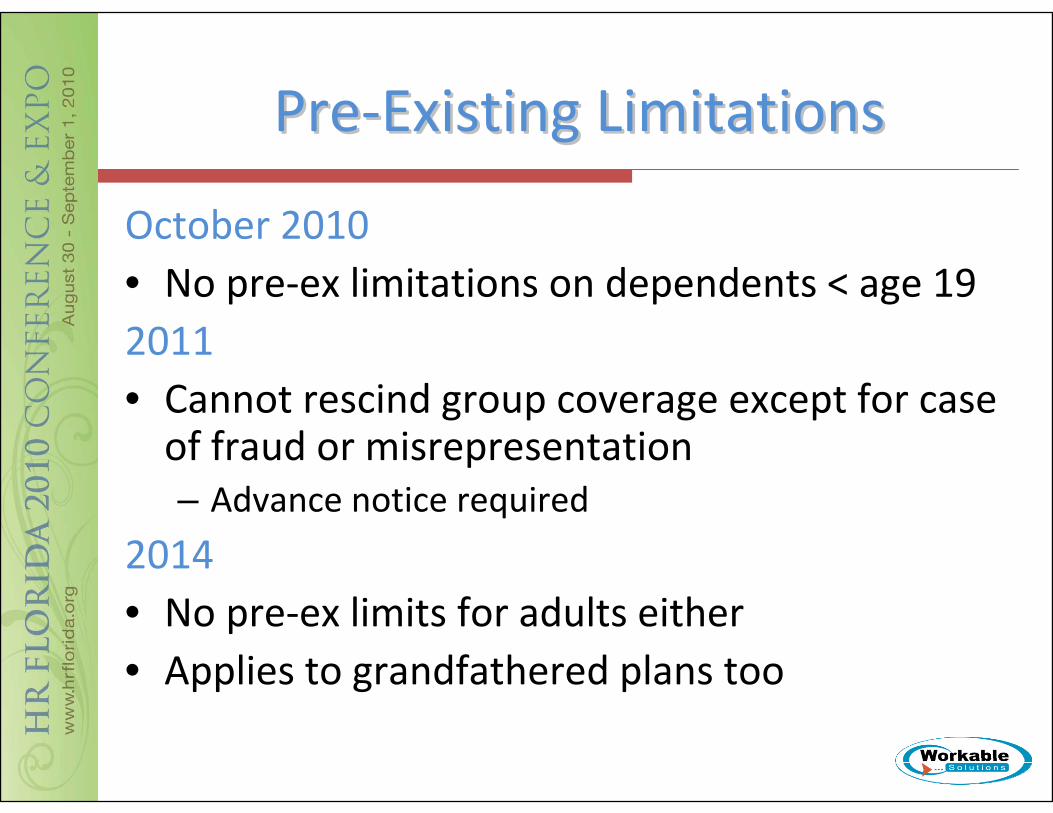

PrePre‐‐Existing LimitationsExisting Limitations

October 2010• No pre‐ex limitations on dependents < age 192011• Cannot rescind group coverage except for case of fraud or misrepresentation– Advance notice required

2014• No pre‐ex limits for adults either• Applies to grandfathered plans too

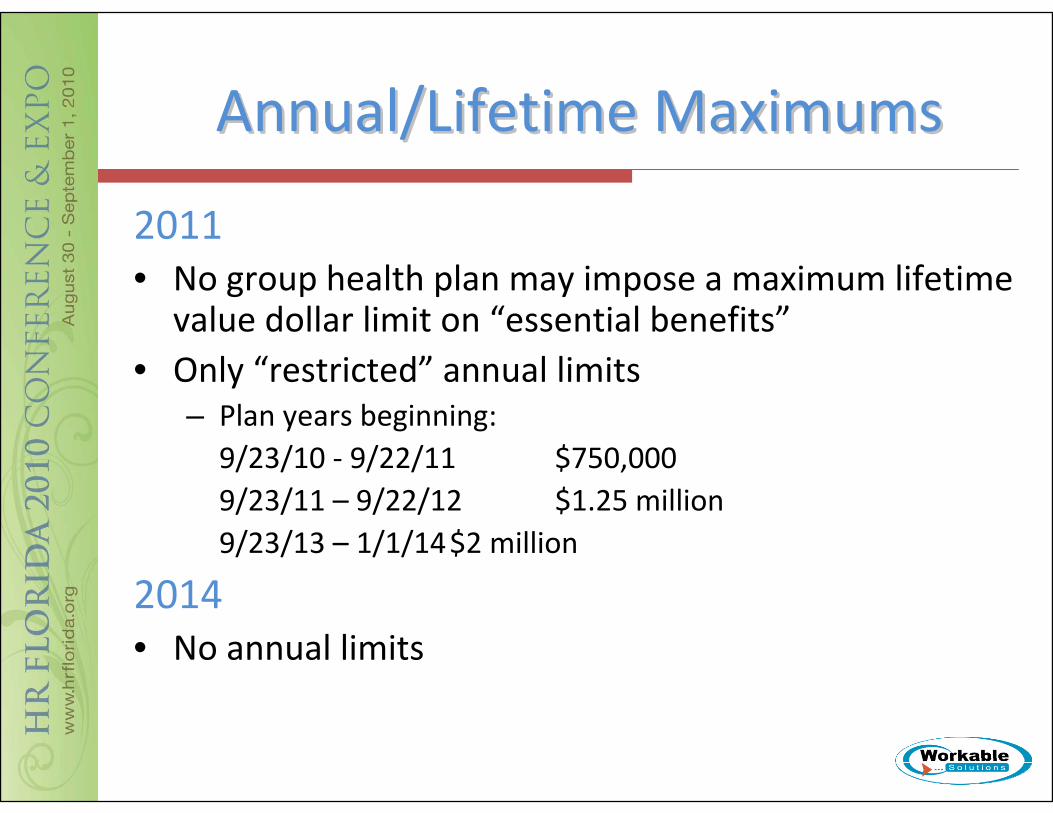

Annual/Lifetime MaximumsAnnual/Lifetime Maximums

2011• No group health plan may impose a maximum lifetime

value dollar limit on “essential benefits”• Only “restricted” annual limits

– Plan years beginning:9/23/10 ‐ 9/22/11 $750,0009/23/11 – 9/22/12 $1.25 million9/23/13 – 1/1/14$2 million

2014• No annual limits

Coverage for Adult DependentsCoverage for Adult Dependents

2011• Must allow dependent coverage till age 26

– Even if married

– Even if they do not meet tax definition of dependent

• Penalty for non‐compliance $100 a day per incident

Other Plan Design ChangesOther Plan Design Changes

2011• Emergency Services

– Must be covered without pre‐authorization

– Must be covered in or out‐of‐network

• OB/GYN may be designated as PCP

• Preventive Care must be fully covered – No cost sharing

Consumer Driven Plan ChangesConsumer Driven Plan Changes

• January 2011– OTC meds no longer qualified expenses

• FSA, HRA, HSA

– Can get doctor’s order– OTC supplies still eligible– Switchover will vary by merchant (IIAS)– Penalty for non-qualified use of HSA funds

increased from 10% to 20%• January 2013

– FSA plan year contributions capped at $2500

Wellness IncentivesWellness Incentives

2011• $200 billion in grants available over 5 years for employers who

• Have fewer than 100 employers who work more than 25 hours a week and did not have a workplace wellness program as of 3/23/2010

• Employers may create up to 20% incentive for completion of wellness program

– Programs must meet minimum criteria established by HHS.

2014• Incentives of 30% (or up to 50% with HHS approval)

WW––2 Reporting2 Reporting

2011• Beginning in 2011 tax year, employers must report value of health benefits on employees W‐2.– Report aggregate cost of employer sponsored coverage including both employer and employee contributions (COBRA rate)

– Informational only. Not counted as income

Small Employer Tax CreditsSmall Employer Tax Credits

2010 – 2013• Up to 35% tax credit for employer contribution

– Small businesses with 25 or fewer EEs and avg. wages of $50,000 or less (full credit for 10 EE s and less)

– Who pay at least 50% of health insurance costs

2014

• Increase to 50% for businesses who buy through Exchange (for up to two years.)

• CBO estimates 12% of small business will qualify

20142014When Things Really Get Serious

Small Group RedefinedSmall Group Redefined

Beginning 2014

• Defined as 1 – 100– States can delay 51‐100 until January 2016

• Below 50 exempt from many provisions

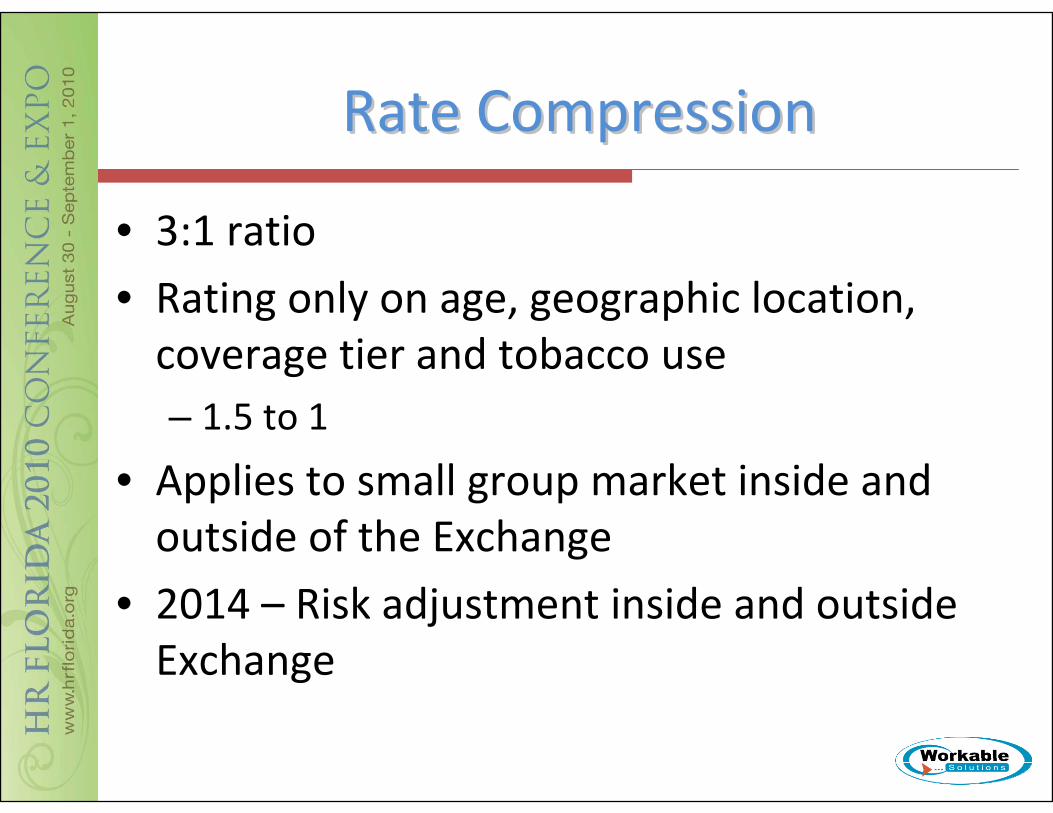

Rate CompressionRate Compression

• 3:1 ratio

• Rating only on age, geographic location, coverage tier and tobacco use– 1.5 to 1

• Applies to small group market inside and outside of the Exchange

• 2014 – Risk adjustment inside and outside Exchange

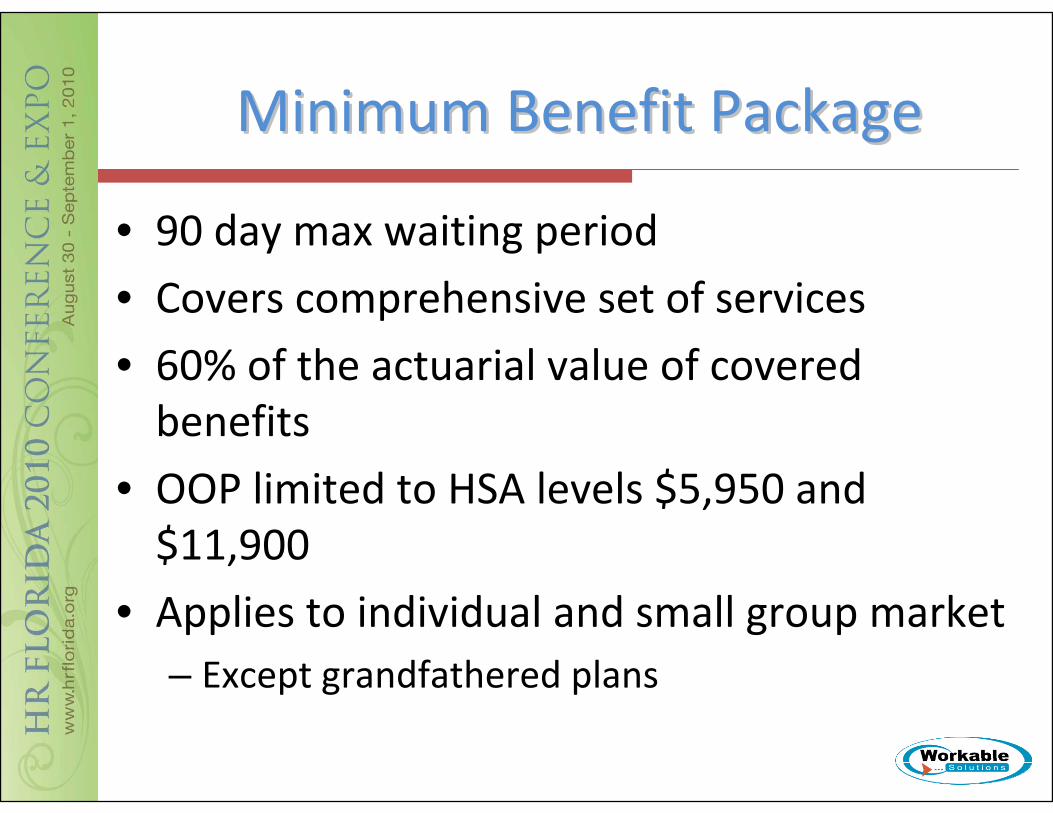

Minimum Benefit PackageMinimum Benefit Package

• 90 day max waiting period

• Covers comprehensive set of services

• 60% of the actuarial value of covered benefits

• OOP limited to HSA levels $5,950 and $11,900

• Applies to individual and small group market– Except grandfathered plans

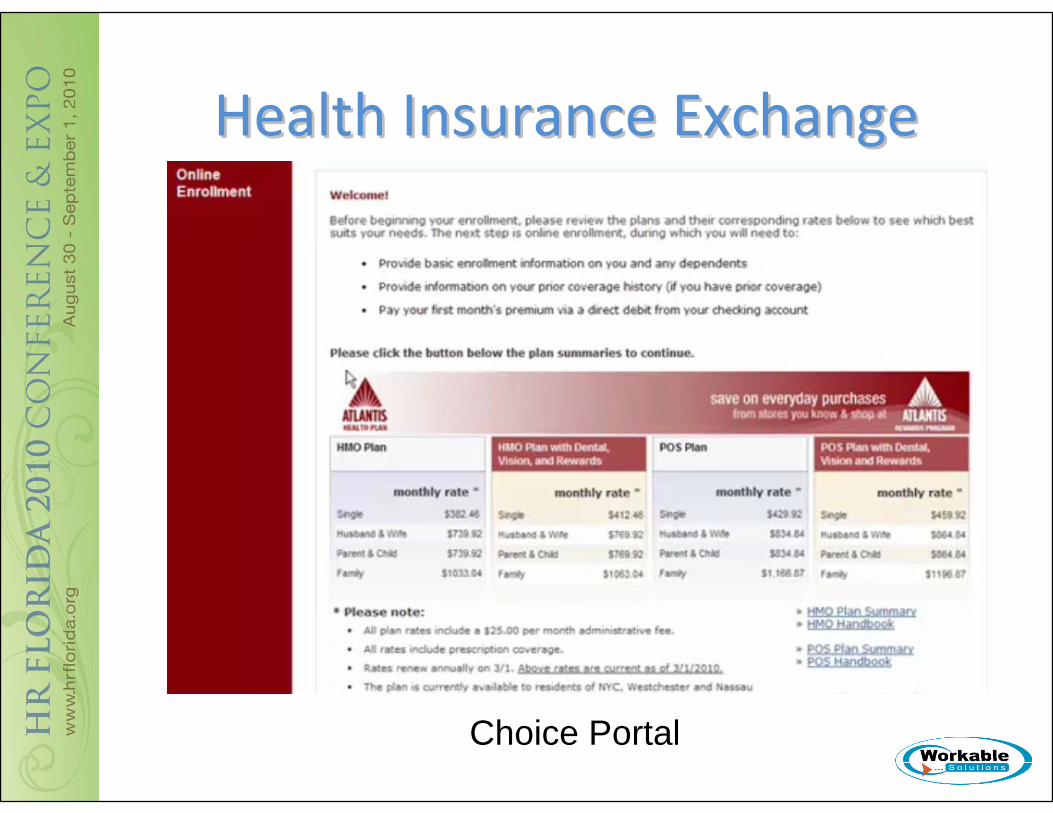

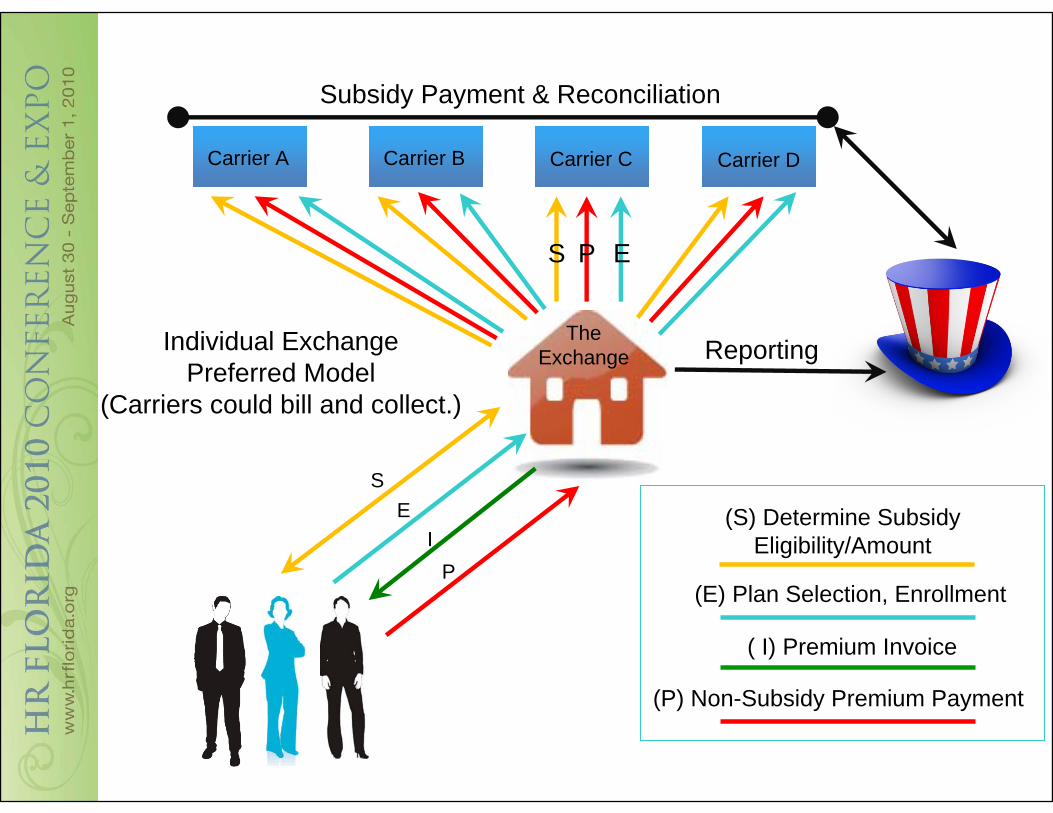

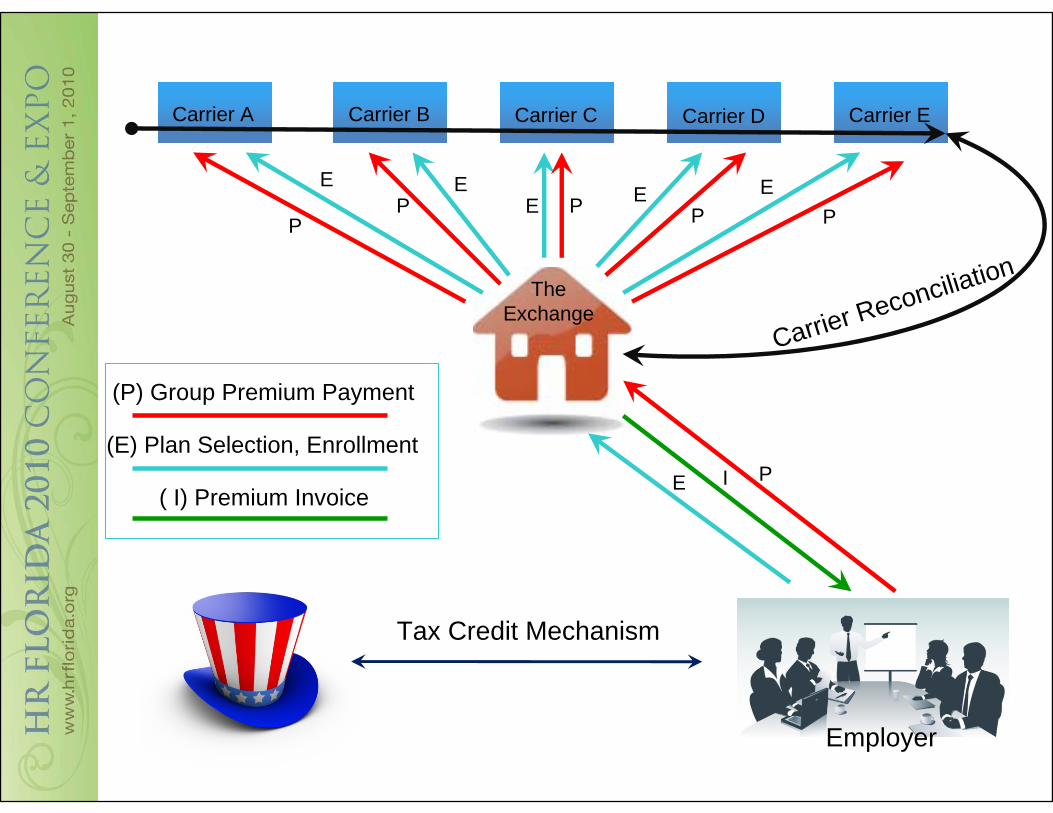

Health Insurance ExchangeHealth Insurance Exchange

Choice Portal

Carrier CCarrier A Carrier B Carrier D

The Exchange

Subsidy Payment & Reconciliation

(E) Plan Selection, Enrollment

( I) Premium Invoice

(P) Non-Subsidy Premium Payment

Reporting

(S) Determine Subsidy Eligibility/Amount

SE

IP

Individual ExchangePreferred Model

(Carriers could bill and collect.)

S EP

Carrier CCarrier A Carrier B Carrier D Carrier E

The Exchange

(E) Plan Selection, Enrollment

( I) Premium Invoice

(P) Group Premium Payment

Employer

Tax Credit Mechanism

E

P

I

PP

P

P P

E EE E E

Carrier Reconciliation

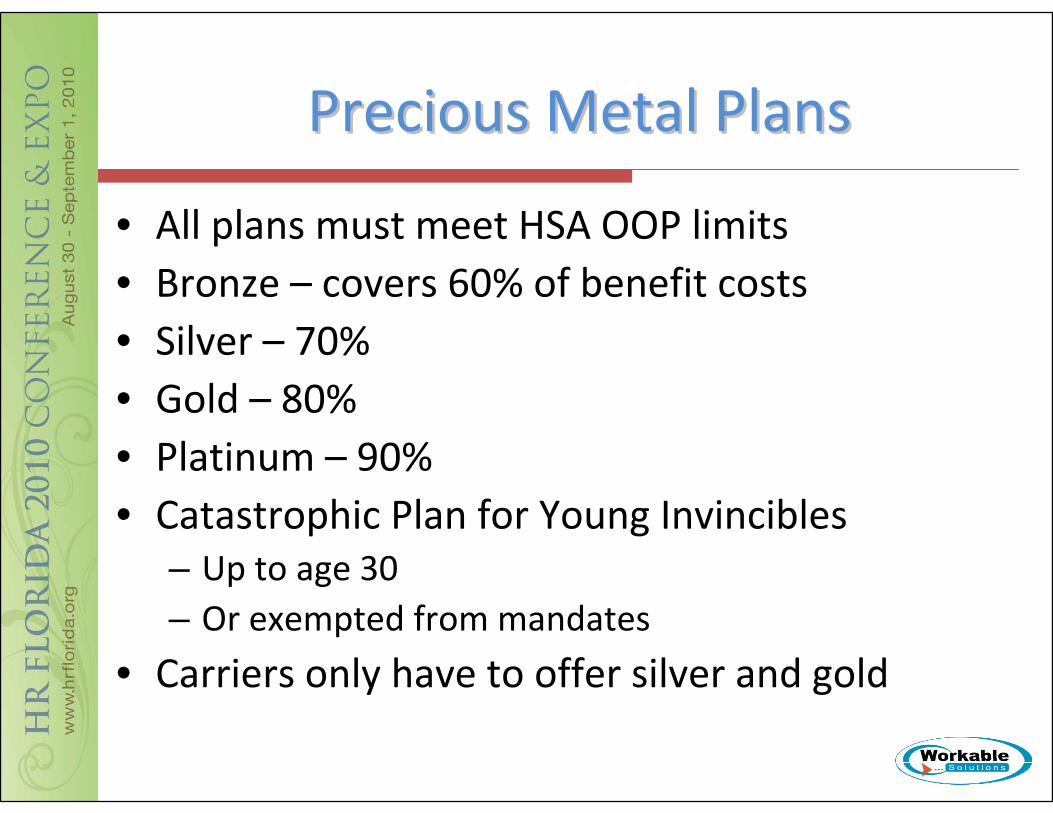

Precious Metal PlansPrecious Metal Plans

• All plans must meet HSA OOP limits• Bronze – covers 60% of benefit costs• Silver – 70%• Gold – 80%• Platinum – 90%• Catastrophic Plan for Young Invincibles

– Up to age 30 – Or exempted from mandates

• Carriers only have to offer silver and gold

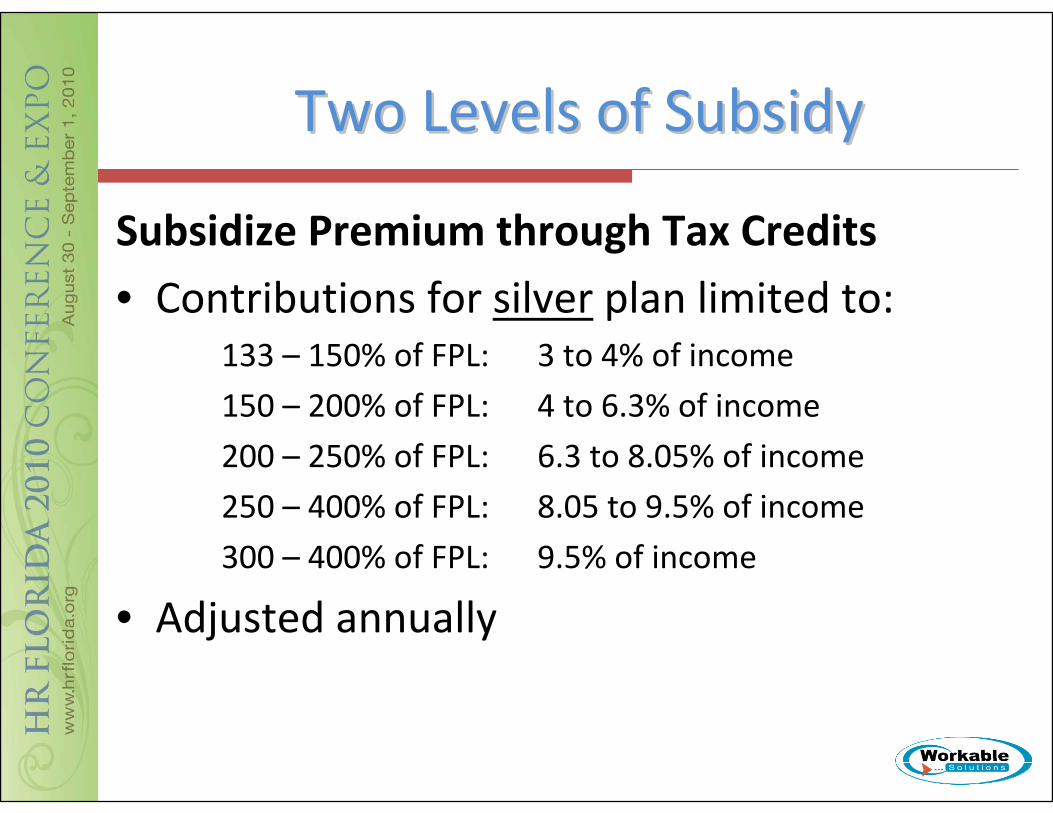

Two Levels of SubsidyTwo Levels of Subsidy

Subsidize Premium through Tax Credits

• Contributions for silver plan limited to:133 – 150% of FPL: 3 to 4% of income

150 – 200% of FPL: 4 to 6.3% of income

200 – 250% of FPL: 6.3 to 8.05% of income

250 – 400% of FPL: 8.05 to 9.5% of income

300 – 400% of FPL: 9.5% of income

• Adjusted annually

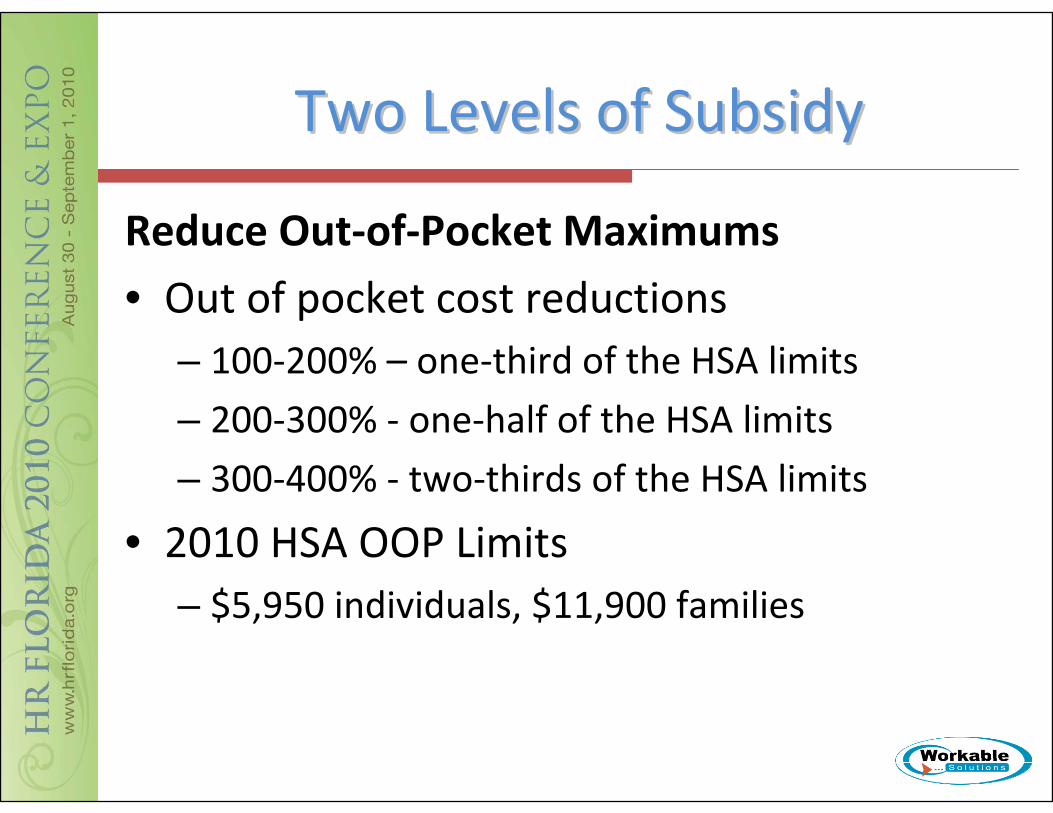

Two Levels of SubsidyTwo Levels of Subsidy

Reduce Out‐of‐Pocket Maximums

• Out of pocket cost reductions– 100‐200% – one‐third of the HSA limits

– 200‐300% ‐ one‐half of the HSA limits

– 300‐400% ‐ two‐thirds of the HSA limits

• 2010 HSA OOP Limits– $5,950 individuals, $11,900 families

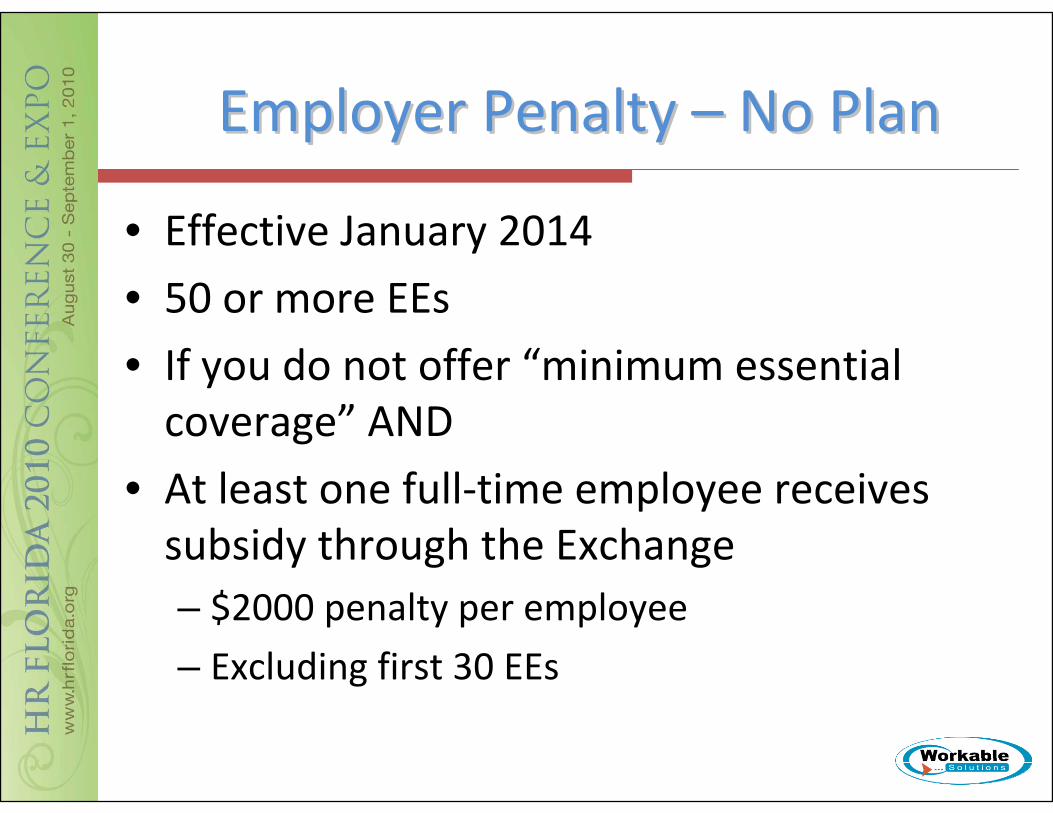

Employer Penalty Employer Penalty –– No PlanNo Plan

• Effective January 2014

• 50 or more EEs

• If you do not offer “minimum essential coverage” AND

• At least one full‐time employee receives subsidy through the Exchange– $2000 penalty per employee

– Excluding first 30 EEs

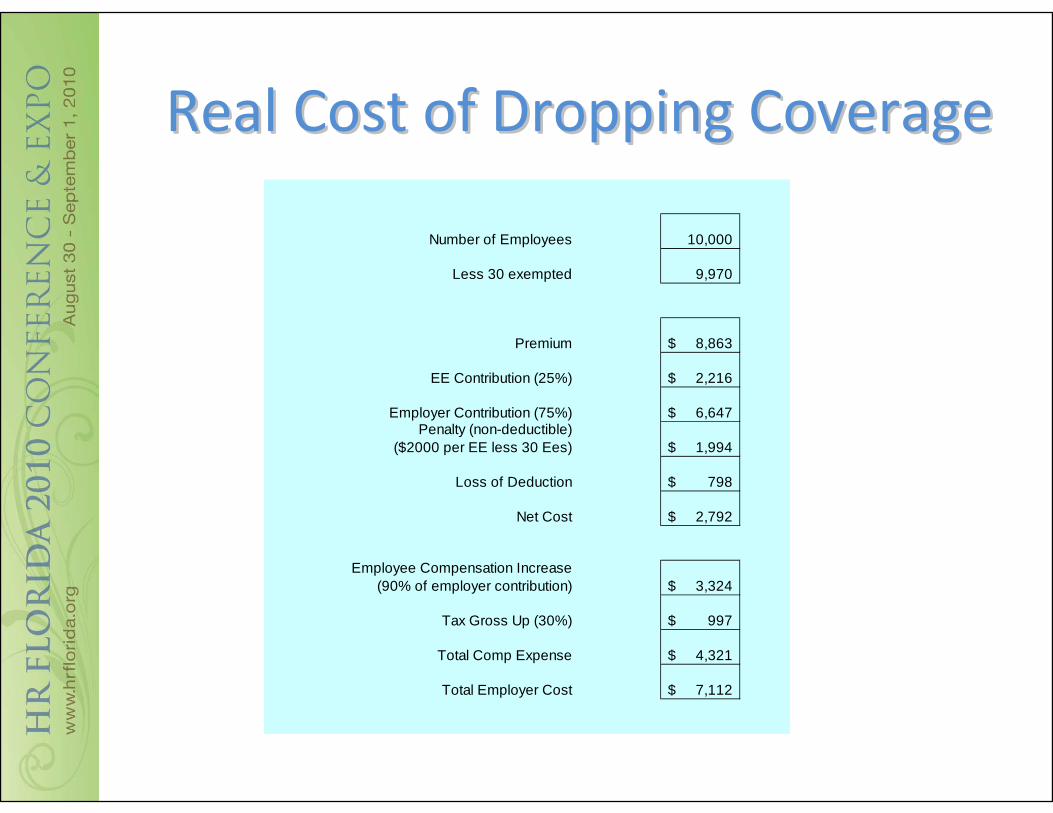

Real Cost of Dropping CoverageReal Cost of Dropping Coverage

Number of Employees 10,000

Less 30 exempted 9,970

Premium 8,863$

EE Contribution (25%) 2,216$

Employer Contribution (75%) 6,647$ Penalty (non-deductible)

($2000 per EE less 30 Ees) 1,994$

Loss of Deduction 798$

Net Cost 2,792$

Employee Compensation Increase (90% of employer contribution) 3,324$

Tax Gross Up (30%) 997$

Total Comp Expense 4,321$

Total Employer Cost 7,112$

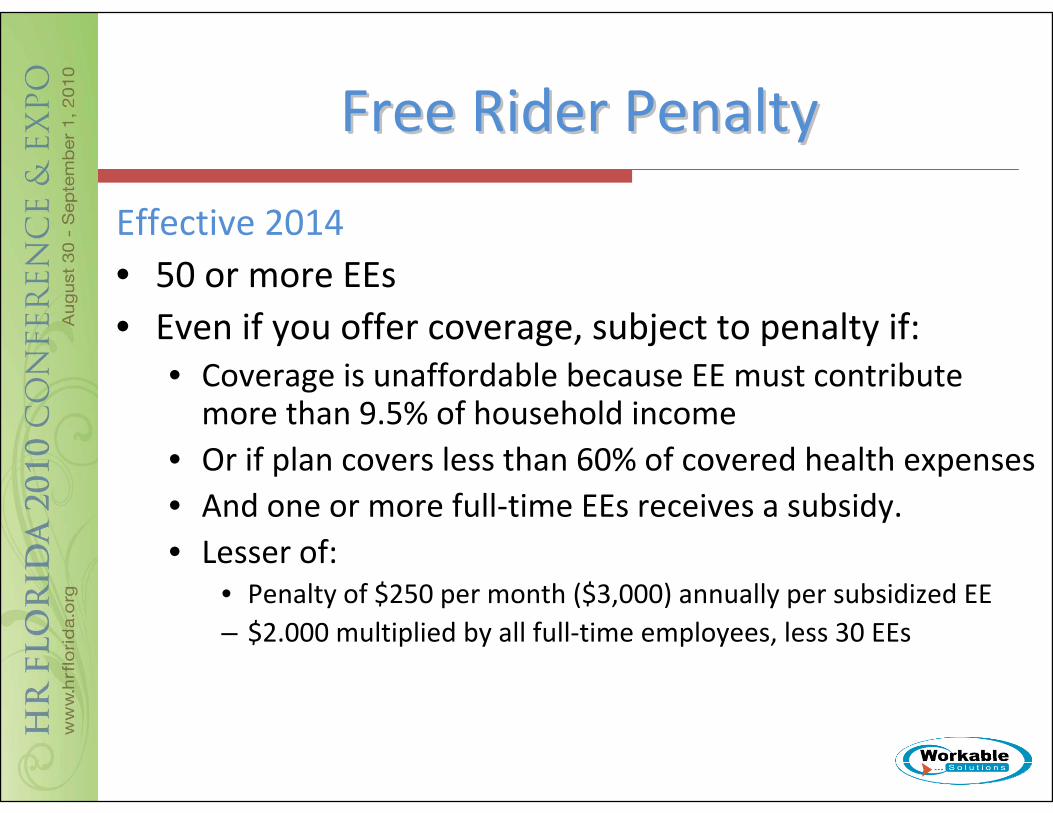

Free Rider PenaltyFree Rider Penalty

Effective 2014• 50 or more EEs• Even if you offer coverage, subject to penalty if:

• Coverage is unaffordable because EE must contribute more than 9.5% of household income

• Or if plan covers less than 60% of covered health expenses• And one or more full‐time EEs receives a subsidy.• Lesser of:

• Penalty of $250 per month ($3,000) annually per subsidized EE– $2.000 multiplied by all full‐time employees, less 30 EEs

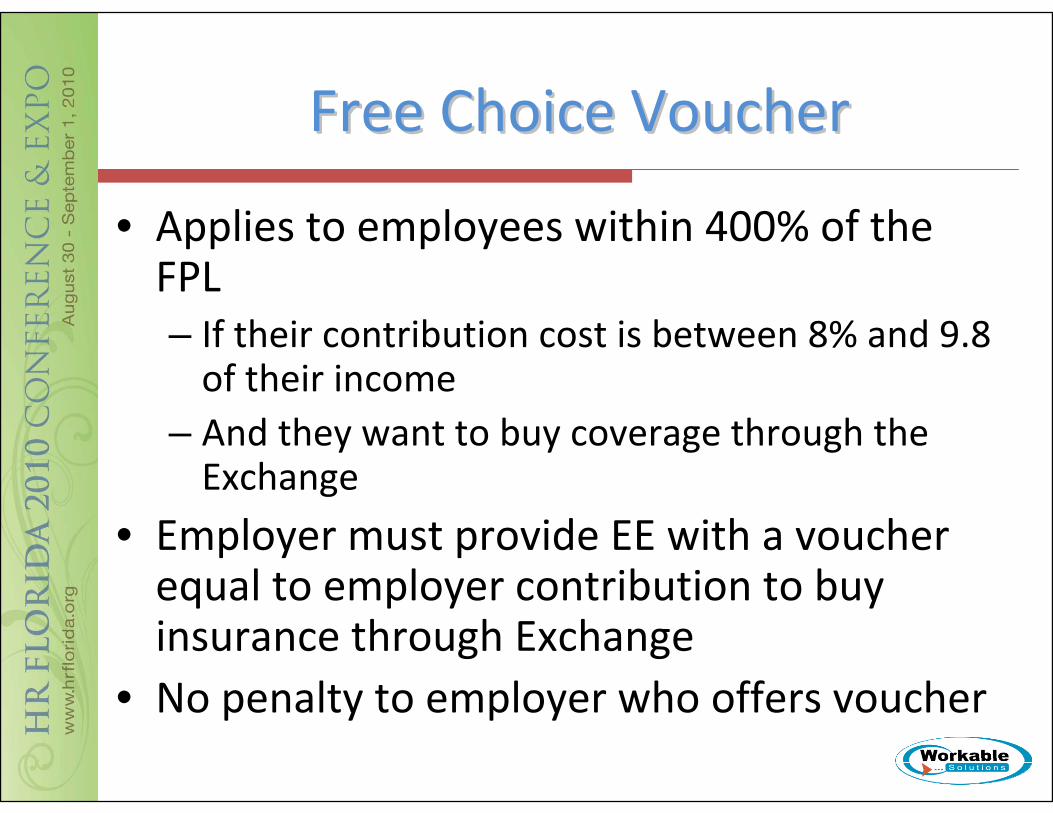

Free Choice VoucherFree Choice Voucher

• Applies to employees within 400% of the FPL– If their contribution cost is between 8% and 9.8 of their income

– And they want to buy coverage through the Exchange

• Employer must provide EE with a voucher equal to employer contribution to buy insurance through Exchange

• No penalty to employer who offers voucher

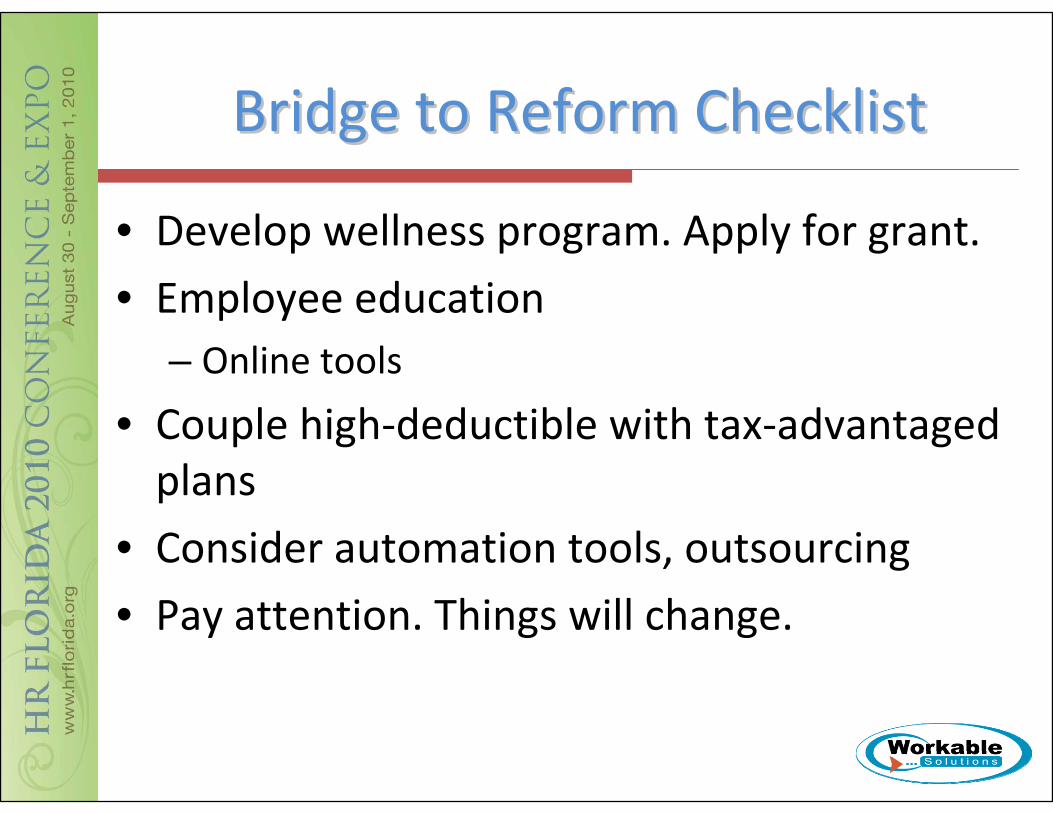

Bridge to Reform ChecklistBridge to Reform Checklist

• Develop wellness program. Apply for grant.

• Employee education– Online tools

• Couple high‐deductible with tax‐advantaged plans

• Consider automation tools, outsourcing

• Pay attention. Things will change.

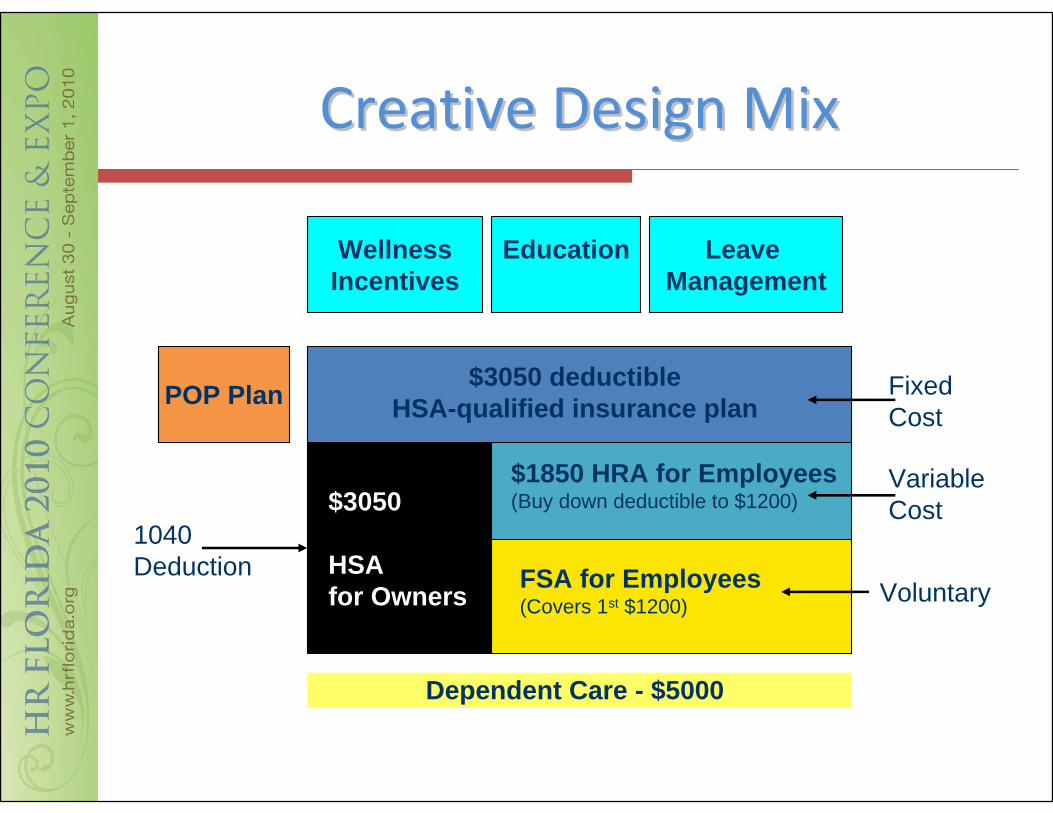

Creative Design MixCreative Design Mix

$3050

HSA for Owners

$1850 HRA for Employees (Buy down deductible to $1200)

FSA for Employees(Covers 1st $1200)

$3050 deductible HSA-qualified insurance planPOP Plan

VariableCost

Fixed Cost

1040Deduction

Voluntary

WellnessIncentives

Education Leave Management

Dependent Care - $5000

Timeline & ChecklistTimeline & Checklist

Questions?Questions?