market participants can follow certain foolproof...

TRANSCRIPT

For Pr ivate Circulat ion Volume 1 Issue 55 19th Sept ’11

Market par ticipants can fol low cer tain foolproof fundamentals to

pick right stocks and diversify their por tfol io in t imes l ike these,

when volati l i ty rules the roost

QUEST FORQUALITY

It’s simplified...Beyond Market 19th Sept ’11 3

DB Corner – Page 5

Restrained EnthusiasmFear and uncertainty among investors has forced companies to defer or in some cases abandon their plans to go in for IPOs – Page 6

Code DecodedThe new ‘game changing’ takeover norm by SEBI aims to strike a balance between the stakeholders in a win-win manner - Page 9

Quest For QualityMarket participants can follow certain foolproof fundamentals to pick right stocks and diversify their portfolio in times like these, when volatility rules the roost - Page 12

Increasing AccountabilityThe need for a more comprehensive legal framework necessary to promote growth of private pools of capital led the SEBI to formulate a set of guidelines to regulate alternative investment funds - Page 18

New Offerings With A Global AppealThe introduction of new global indices futures trading by NSE will enable market participants to benefit from S&P 500 and DJIA - Page 22

In Your Best InterestBorrowers would be better off if they prepay their loan amount or get the tenure of their loan extended when interest rates rise - Page 24

Clouded By GloomThe turbulence in the US economy and the uncertainty in the Eurozone do not bode well for an export–led Asian economy like India- Page 26

Getting The Act RightThe dynamics of film production have changed a great deal; nowadays films are produced with the main focus on breaking-even much before a movie hits theatres - Page 29

Under Construction. Inconvenience RegrettedDespite opportunities, the construction sector is besieged with hurdles that are hampering growth - Page 32

Fortnightly Outlook For Commodities. - Page 35

Fortnightly Outlook For Currencies - Page 36

Guru MantraMaintaining the characteristics of the fund, while trying to marry growth and value is one of the many keys to being a successful fund manager, says Tridib Pathak - Page 38

Keeping Date With Debt FundsMore and more retail investors are turning to long-term debt funds in turbulent times like we are witnessing at present - Page 42

Back Door Entry?Of the many changes being considered by SEBI to revive the mutual fund industry, the introduction charges is one of them and it is hoped to benefit distributors too – Page 44

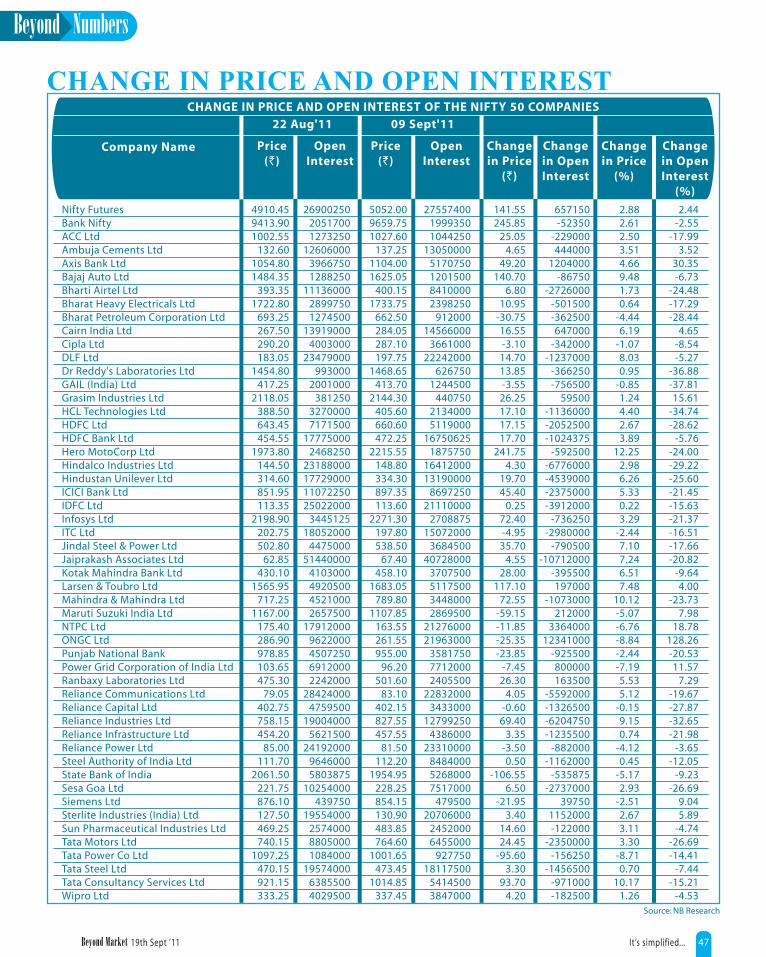

Important Statistics For The Fortnight Gone By – Page 47

Four Seasons In A Stock’s Life CycleEvery stock follows a cyclical path and is therefore, imperative for the market participants to know the exact stage at which a stock is trading, to make the right investment decision – Page 52

Volume 1 Issue: 55, 19th Sept ’11

Editor-in-Chief & Publisher: Rakesh BhandariEditor: Tushita NigamSenior Sub-Editor: Kiran V Uchil

Art Director: Sachin KambleJunior Designer: Sagar Padwal

Marketing & Operations:Savio Pashana

We, at Beyond Market welcome your views, comments and feedback. Do help us to grow better as per your liking. This is our attempt to reach you better while crossing horizons...

Web: www.nirmalbang.com [email protected] No: 022 - 3926 8047

HEAD OFFICE Nirmal Bang Financial Services Pvt LtdSonawala Building, 25 Bank Street, Fort, Mumbai - 400001 Tel. 022-3926 7500/7501

CORPORATE OFFICE B-2, 301/302, Marathon Innova,Off Ganpatrao Kadam Marg,Lower Parel (W), Mumbai - 400 013Tel: 022 - 3926 8000/8001

Research Team: Sunil Jain, Kunal Shah, Michael Pillai, Sunit Mehta, Vikash Bairoliya, Runjhun Jain, Amish Pansuriya,Kavita Vempalli, Ruchita Maheshwari, Silky Jain

DIRECTIONAL VIEWS

Tushita NigamEditor

Investing in the stock markets is now treated at par with having a job or a profession. It is looked at as a fruitful investment avenue that each one seeks to benefit from. But considering the volatility in the stock markets, many investors seek to know when is the right time to enter the markets or make fresh or additional purchases.

While every market expert has his own way of interpreting this question, we at Beyond Market have simplified the process of stock-picking for you in times of volatility in the markets. By using fundamen-tals, market participants can identify right stocks and diversify their portfolio to achieve long-term gains. Our cover story will help you understand these fundamentals better and enable you to take cues from the stocks we have chosen.

Apart from this, there is an article on how companies that were planning to come out with IPOs have either deferred or abandoned their plans fearing lack of response and volatility in the markets. Another article dwells on the revamped takeover code, which is hoped to benefit investors and stakeholders of the target company, alike.

There are also articles on the guidelines by SEBI to regulate alternative investment funds, the introduc-tion of new global indices futures trading by NSE, the modes of repayment before home loan takers in the current scenario where interest rates are rising constantly and the changing face of film production, among others.

In our Beyond Basics section, there is an interesting piece on the latest developments made by the market regulator SEBI to bring about a change in the mutual fund industry, which had been performing poorly since the abolition of entry load.

Beyond Market constantly endeavours to bridge the gap between individuals and the financial world. We have, therefore, introduced a new section called ‘Beyond Work’ where we plan to highlight the lighter side of fund managers and corporate honchos by giving an insight into their life outside work. In the current issue, Tridib Pathak, Director Equity and Senior Fund Manager at IDFC Mutual Fund, speaks about his life and experiences and what led him to becoming a successful fund manageR.

It’s simplified...Beyond Market 19th Sept ’114

It’s simplified...Beyond Market 19th Sept ’11 5

Traders should avoid keeping

overnight positions.

Disclaimer It is safe to assume that my clients and I may have an investment interest in the stocks/sectors discussed. Investors are required to take an independent decision before investing. Investment in equity is subject to market risk. Our research should not be considered as an advertise-ment or advice, professional or otherwise. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and the like and take professional advice before investing.

Nifty: 5,012.55Sensex: 16,709.60(As on 14th Sept ’11)

he sovereign debt crisis in Europe continued to weigh heavily on the global markets in the

previous fortnight.

Greece’s two-year government bond yield rate of over 66% and the 10-year bond yield rate of over 23% clearly indicate the growing possibility of a default by the country.

Although Greece’s GDP is only 2% of the Eurozone and has a 3% loan of the total loan in the Eurozone, the bigger problem, however, is the contagious impact of the default by Greece on other high-debt countries like Italy. In fact, Italy is the third largest economy in the Eurozone with the second highest debt in the world.

In the US, President Barack Obama recently proposed a $447 billion package to revive a stalled job market there. The package includes $240 billion in short-term payroll and investment spending tax cuts.

However, its implication on the US economy and subsequently the rest of the world will be known only after it is passed as it is currently facing opposition from the Republicans.

Talking about India, the IIP numbers have been low due to the de-growth in the capital goods segment. However, the consumer durables segment continues to grow, showing that consumer demand is yet strong. Rainfall too has been good at 3% above normal.

Inflation continues to be a source of worry for the government. The inflation numbers for the month of August have been higher than expected at 9.78%.

Also, the sharp depreciation of the rupee on the back of uncertainties in the global economy and rising trade

T deficit in India, has taken corporates by surprise. This can impact companies, both positively and negatively, depending on their exposure to the international markets.

Market participants should avoid buying at the upper levels as the markets are expected to be range-bound.

The Nifty has resistance at the 5,150 – 5,200 levels. Traders should avoid keeping overnight positions. However, investors can consider buying stocks on declines.

Stocks like Everest Kanto Cylinder Ltd (LTP: `74.10), Munjal Showa Ltd (LTP: `64.05), Petronet LNG Ltd (LTP: `177.10), Mahindra & Mahindra Ltd (LTP: `792.70), Praj Industries Ltd (LTP: `71.40) and Yes Bank Ltd (LTP: `276.70) can be looked at on declines from an investment perspective.

Further, traders and investors should be watchful of the Eurozone crisis and how it unfolds as the situation in this region will determine the course of the global equity markets in the near term.

Market participants can also expect the RBI to hike key interest rates by 25 basis points in line with market expectations, while addressing slow growth in the economY.

It’s simplified...Beyond Market 19th Sept ’116

Fear and uncertainty

among investors has

forced companies to

defer or in some cases

abandon their plans to

go in for IPOs

RESTRAINEDhe storm brewing in the stock markets, has taken with it the dreams of many Indian companies that want

to go in for public listing. India’s benchmark index, the Sensex, has declined by 5.21% in the last one year and with the possibility of a double dip recession in the US, investors are staying away from the equity markets.

Fear and uncertainty among investors has put the lid on the initial public offerings of 15 companies, including the likes of Anil Ambani Group’s Reliance Infratel, Jindal Power (`7,200 crore), Reliance Infra (`5,000 crore), Lodha Developers (`2,500 crore) and Gujarat State Petroleum Corp Ltd (`3,067 crore).

T The 15 companies would have raised an estimated `25,000 crore from the market had they gone ahead with their IPO plans. It was a deliberate decision by the companies to let their plans lapse, even though they had received the initial nod for their IPOs from the market regulator, the Securities and Exchange Board of India (SEBI).

SEBI gives a one-year window to companies to go through with their IPO, once they receive the regulatory nod. After the one-year window lapses, companies need to re-file their updated draft red herring prospectus with SEBI. But, perhaps, looking at the lack of interest among investors and the volatile market, these 15 companies have decided not to go

ahead with their IPO plans.

Not surprisingly, a majority of companies, that have let their IPOs lapse, are from the real estate sector, which is currently out of favour with investors, both Foreign Institutional Investors and retail investors.

The Bombay Stock Exchange Realty Index, an index of 14 real estate stocks, has lost 50% in value in the last one year. The loss has been on account of declining residential sales, high debt of companies and concerns over corporate governance in real estate companies.

Companies such as BPTP Ltd, Ambience Ltd and Kumar Urban

ENTHUSIASM

It’s simplified...Beyond Market 19th Sept ’11 7

ENTHUSIASMDevelopment Ltd, among others have forgone their public funding plans, although real estate companies are in dire need of funds.

The problem with real estate IPOs goes beyond weak market sentiments. Expensive valuation of real estate developers is keeping investors away. In the year 2007, when the market was at a high, many real estate developers listed at high valuations. Things went downhill for companies when the global economy crashed in September ’08.

The crash hit the Indian real estate sector, with real estate prices correcting up to 50% and real estate company stocks losing more than half

of their share value. For instance, DLF, the largest developer by market value, is now trading at around `197, more than half of its listing price of `525.

Analysts say that now when their peers are looking at listing themselves, they expect the same valuations, but investors do not want to blindly put money in real estate IPOs anymore.

Investors have begun looking at the valuations and cash flow of developers, instead of merely investing in a company based on its land bank valuation. And any developer, who is not able to justify its valuation, is finding it tough to

obtain investors who would be willing to put money in his company.

The rush for IPOs from the real estate sector is similar to the one seen in the year 2007 when the country’s largest realtor, DLF Ltd, went public, except for the fact that this time around, barring a few companies, the rest have been unsuccessful in raising money from the equity market.

The IPO fever began in late 2009 and early 2010 when real estate developers filed for IPOs, encouraged by the revival in the stock market. The successful IPO of Godrej Properties, which was subscribed by 4 times also gave hope to companies that the IPO market is back.

It’s simplified...Beyond Market 19th Sept ’118

Analysts believe that a real estate IPO will go through, only if promoters offer a heavy discount to its investors and keep the valuation at a realistic level. This, however, seems unlikely given the fact that most developers are going in for an IPO to raise cash to repay their debt obligations or to meet working capital requirements.

For instance, New Delhi-based BPTP was planning to use one-fourth of the IPO proceeds of ̀ 1,500 crore to lower its debt. Listing at a discount, therefore, does not make any sense for them. It is a catch-22 situation for developers. Unless builders blink and offer discounts, their dreams of an IPO will remain just that.

Lapsed initial public offerings is not the only problem. A lot of companies have either shelved or delayed their IPO plans because of weak markets. While Galaxy Surfactants Ltd withdrew its IPO in May this year because of poor response to its IPO, public sector companies like Steel Authority of India Ltd (SAIL) and Oil & Natural Gas Corp (ONGC) have deferred their follow-on public offerings. Analysts believe that given the weak IPO market, the government will find it difficult to meet its $9 billion divestment target for the year 2011-12.

Recently, Micromax Informatics Ltd, India’s third-largest mobile handset maker by sales, withdrew its `466-crore IPO on 17th Jun ’11. In a statement, Micromax said the company board recommended withdrawing the IPO to “allow the company to focus on new product launches and product development.”

Micromax, which is backed by private equity investors such as TA Associates, Sandstone Capital LLC, Madison Capital Management LLC and Sequoia Capital India, had filed a draft red herring prospectus in

October last year, which was approved by SEBI in January ’11.

The company had earlier cut its issue size in March, from $150 million to $105 million. Mircomax had also gone on road shows and met investors globally before it decided to withdraw its IPO. Now, the company has said it will look at renewing its IPO plans in FY13.

Analysts believe that companies are consciously withdrawing from IPOs, for mainly two reasons. One, they feel the issue may not get a very good response and the other, going by the recent IPOs, companies feel that after listing, their stock will trade below the issue price.

According to data from Prime Database, 157 companies raised `70,627 crore from the IPO market, between 2007 and 2009. Of the 157 IPOs, around 84 are currently trading below their issue price.

The proof of the lackluster IPO market lies in the fact that the amount of funds raised by companies through IPOs and rights issue fell 75% month-on-month to `1,195.6 crore in June ’11, over the amount raised in May this year.

“During June ’11, `1,195.6 crore was mobilized in the primary market through seven issues, compared to `4,781.1 crore mobilized through five issues in May ’11, showing a decrease of 75% over the previous month,” said a ‘Capital Market Review’ released by SEBI.

Data provider Dealogic says the amount of money raised through IPOs in India has fallen by more than 80% year-on-year. The company says that in the past six months there have been 22 listings in India, raising a combined $780 million compared to $4 billion raised from 28 IPOs during

the same period last year. On the contrary, global IPO fundraising for year-to-date till July ’11 is up 14% at $114 billion, led by listings in Hong Kong and the US. Analysts, however, are of the opinion that while the number of lapsed or withdrawn IPOs is high, this is still better than 2008-09, when the market condition was worse than it is now. In early 2008, when the Sensex hit an all-time high of 21,200, many companies filed for an IPO, in the hope of raising easy money.

But the global economic downturn which came in September of 2008, hit the stock market so badly that the Sensex dropped to 8,000 points in March ’09. During this time, nearly 29 companies, which had received regulatory approval, either withdrew their IPOs or let them lapse. This time around, the situation is not as bad.

Companies whose IPOs have lapsed are now looking at other funding options, such as private equity or debt instruments like non-convertible debentures. The IPO story is however not completely over. Analysts say companies with strong fundamentals and cash flow will still find interest among investors.

For instance, in the last one year, small companies such as Lovable Lingerie Ltd, have given phenomenal returns to investors. The lingerie maker’s IPO, was subscribed by over ten times and has given 82.7% returns to investors in just a span of around five months.

Once the volatility in the market subsides and there is more clarity on the future course of the global markets, we could see some IPOs hitting the market. Whether the IPO will do well or not, will depend entirely on the valuation and the timing of the issuE.

It’s simplified...Beyond Market 19th Sept ’11 9

CODE DECODEDThe new ‘game changing’ takeover norm by SEBI aims to strike a balance between the stakeholders in a win-win manner

ndia hopped on to the economic reforms’ bandwagon in the year 1991, and thus began its journey of

liberalization. Six years later, in the year 1997, the government instituted a formal takeover code which governed mergers and acquisitions in corporate India.

While liberalization was followed by globalization, the takeover code remained intact, until much later in September ’09 when the market regulator the Securities Exchange Board of India constituted a Takeover Regulation Advisory Committee (TRAC) to review the then prevailing norms and make them more relevant for the present day scenario.

The TRAC recommendations were made public in July last year. However, it was followed by internal

I

It’s simplified...Beyond Market 19th Sept ’1110

deliberations by SEBI. And on 28th July this year, at its board meeting, SEBI cleared the decks for the revamped takeover code.

While the fine prints are yet to be unveiled, SEBI has considered most recommendations by TRAC and made sweeping changes to the old norms. As a starter, the trigger point for open offer has been increased to 25% from 15% and the open offer size, after the 25% trigger is hit, has been enhanced to 26% from the current 20%.

What does the enhanced trigger mean? It means that a potential acquirer, who would have either paused below 15%, or would have come out with an open offer, can now continue making creeping acquisitions of an additional 10% stake in the target company. Take the case of Hotel Leela Ventures Ltd, wherein ITC Ltd currently holds a 14.5% stake. Under the new code, ITC can buy another 10% and continue to be a substantial shareholder of Hotel Leela and still stay away from making an open offer for additional 26% stake.

Equally interesting is the case of EIH Ltd. This hospitality company which owns and operates the Oberoi chain of hotels also has Reliance, apart from ITC as its 14.5% shareholder. These are some of the cases where the effectiveness of the new takeover code will be tested in the days to come.

Beyond the 25% trigger, if an acquirer makes an open offer and successfully acquires an additional 26%, then the result of the two would be a ‘controlling’ 51% stake in the target company. That is the ‘game changer’.

Under the old norms, it was not easy for an acquirer to obtain a controlling stake in a target company, informs an

investment banker. With the new norms, the concept of a buyout will now be a reality in India, he adds.

The revised norms would certainly change the dynamics of mergers and acquisitions in India. In the distant past, corporate India has seen some interesting cases of hostile takeover attempts. While not many tasted success, Bombay Dyeing & Manufacturing and the erstwhile GESCO Corporation (now Mahindra Lifescapes) did manage to grab headlines. However, the hostile attempts turned out to be futile.

Coming back to the TRAC recommendation, the so-called dynamic revisions have not taken all the recommendations into consideration. Against the 26% open offer, TRAC had proposed an open offer size of 100%; post the 25% trigger being hit. Had the 100% recommendation been implemented, small investors in the target company would have been freed up. And delisting, in that case, would have been the subsequent corporate action for the acquired company.

No doubt, the acquirer in that case would have been compelled to commit more resources and be even more serious about the target company. That, for an Indian company planning to acquire another Indian company would have been a bit tougher, considering that banks, according to the norms laid down by the Reserve Bank of India, are not supposed to finance takeovers.

While the new norms widen the enhanced shareholding window for the acquirer, owing to the additional 10% buffer with 15% trigger norm changed to 25% , it also gives respite for the target company.

Unlike earlier norms where the acquirer was supposed to get a total

35% of the company, 20% open offer after the 15% trigger, the new norms require the acquirer to buy 51% at the end of the open offer. That is an additional cost. Here, SEBI, believe experts, has actually achieved two important goals.

Firstly, with the new code, India will be able to woo investors and secondly, the additional cost will ensure that only financially stronger players will enter the fray for takeovers. In addition to this, the recommendation by the board of the target company has been made mandatory under the new code.

Needless to say, prominent Indian companies operate with their promoter holdings ranging from 25% to 30%, where special resolutions can be blocked above 25%. Strategic investors like venture capitalists and private equity players would be the most excited among investors with the new code by SEBI.

At the earlier 15% trigger, it was not sensible for such investors as promoters would totally sideline them. Under the new code, an investor can acquire up to 24.99% in the company, avoid making any open offer and also comfortably block promoter’s special resolutions as substantial shareholders along with some scattered support.

What next? While investors have reasons to cheer with the new code, the promoters of Indian companies would soon get busy exploring methods to counter possible hostile bids that could hurt them in the coming days. While average shareholding in Indian companies is in the range of 20% to 40%, BSE 500 index has 210 companies where promoter holding is below 51%. There are 24 companies in the same index where promoter holding is currently below 26%. Therefore, it

It’s simplified...Beyond Market 19th Sept ’11 11

would not be surprising to see instances of promoters being allotted convertible warrants.

Beyond the tug of war of percentages and prices, there is both good and bad news. Good news for small investors in target companies and bad news for promoters of such target companies. The old regulations permitting the payment of non-compete fee up to 25% of the offer price to the exiting promoters of the target company, in addition to the decided offer price, now stands deleted.

This means promoters’ years of hard work towards building the company would not fetch them an extra buck, unless the offer price to other shareholders is revised to the same extent. Not all acquirers would be generous in rewarding shareholders in order to reward the promoters.

This, by and large, serves the purpose of protecting the interests of minority shareholders, says an investment banker who cites the case of the Cairn-Vedanta deal. Going forward, we will not see such non-compete fee

element in the mergers and acquisition deals, he explains.

Until the fine prints are out and the new takeover code is used as the base for acquisitions, the new norms reflect a meticulous attempt by the market regulator - SEBI to juggle with the interests of all the stakeholders in the game. Needless to say, the new norms make ‘takeovers’ a reality from erstwhile acquisitions. But the cost, price and tenability of the code will get decoded with its authentic use in the days to comE.

COMMODITY FUTURESCrude Oil $98/barrel

Nickel$28,000/tonne

Pepper`25,000/quintal

Silver $32/troy ounce

Zinc $2,100/tonne

Aluminium $2,450/tonne

Chana`2,500/quintal

Copper $8,500/tonne

Jeera`14,000/quintal

Cardamom `1,000/kg

Gold $1,500/troy ounce

Guar Seed `3,200/quintal

Our research goes beyond numbers to identify the forces that affect the kundali of commodities - global events, domestic issues, and everything in between. Which is why, our predictions have invariably come true on several occasions, proving that we are among the best in the industry when it comes to commodity trading.

Predicting Accurate Results. Consistently.

w w w.nirmalbang.com

E Q U I T I E S * | D E R I V AT I V E S * | C O M M O D I T I E S | C U R R E N C Y * | M U T U A L F U N D S ^ | I P O s ^ | I N S U R A N C E ^ | D P *

CORPORATE OFFICE: B-2, 301/302, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel: 022 - 39268000 / 8001; Fax: 022 - 39268010R E G D. O F F I C E : S onawala Bui ld ing, 25 Bank Street , For t , Mumbai - 400 001. Tel : 022 - 39267500 / 7501; Fax : 022 - 39267510

BSE SEBI REGN No. INB011072759, INF011072759 & INE011072759, NSE SEBI REGN No. INB230939139, INF230939139 & INE230939139 DP SEBI REGN. No NSDL: IN-DP-NSDL-136-2000, CDS(I)l: IN-DP-CDSL-37-99, AMFI REGN. No. arn-49454 NCDEX REGN. NO. 00362, FMC Code-0075, MCX REGN. No. 16590, FMC Code-MCX/TCM/CORP/0490, MCX SX-INE260939139, PMS-INP000002981

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme related document carefully before investing. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. The PMS Service is not o�ering for commodity segment. *Through Nirmal Bang Securities Pvt. Ltd. ^Distributors #Prepared by Research Analyst of Nirmal Bang Commodities Pvt. Ltd.

For job openings at Nirmal Bang, visit http://www.nirmalbang.com/careers.aspx

ust when we thought that the economies around the world were showing signs of improvement, the situation

in the US and the Eurozone sent markets into a tizzy.

While President Barrack Obama is working out a proposal to inject more dollars into the US economy mainly

J through tax cuts and direct aid to states through the whole of next year, bailout packages are been chalked out for Greece and other Eurozone countries. This clearly indicates that world leaders have been doing everything in their capacity to salvage the situation and prevent the world from delving into another recession. Needless to say, while momentary

bouts of good news are propping up stocks sporadically, the volatility that we are witnessing in the markets is here to stay.

So what should an investor do at this point in time? Should he stay away from the markets? No, doing so would mean going against the fundamentals of investing. Instead,

Market par ticipants can fol low cer tain foolproof fundamentals to pick right stocks and diversify their por tfol io in t imes l ike these, when volati l i ty rules the roost

QUEST FORQUALITY

It’s simplified...Beyond Market 19th Sept ’1112

It’s simplified...Beyond Market 19th Sept ’11 13

he should go back to the basics. There are certain principles you cannot go wrong with and we are here to tell you the same. Some classic investing norms can be used to bottom fish or buy the cheapest investments in times of volatility. Besides, valuations are attractive and instead of just watching the depressing red on the tickers you could actually land up with some gems in times like these!

GOOD QUALITY MANAGEMENT

Although there are no mathematical parameters to judge the quality of the management, there are certain things you could watch out for. Check the dividend-paying history of the company. If a company has been paying regular dividends to investors even during unfavourable times, it is a keep over those who do not pay any dividend at all.

Also watch out for companies with high promoter holding. If company insiders themselves do not believe in the company, then investors too have no business in believing in it. The quantum of pledged shares of a promoter is also something an investor needs to be wary of. At a time when everything around is crashing at a breakneck speed, the quantity of shares pledged by a company is a good reason to stay away from the stock. It is especially relevant in smaller companies.

In a cash crunch scenario there is a big risk of margin calls on these companies by lenders. This essentially means that when markets fall, banks ask for either higher collateral or more cash to maintain their credit line.

With smaller companies, there is always a risk of not being able to meet these margin calls and ending up losing control over the company.

But do not be sceptical of all the companies that have pledged shares. There are several large corporate houses that have pledged shares as collateral in order to mobilize resources. The Tata Group, for instance, pledged shares to raise some cash and restructure its high cost debt.

Lastly while looking out for a company with good quality management do a thorough background check on the history of the company and its promoters. It is only fair to be sceptical at a time when there are numerous scam-tainted individuals who may be promising the moon to investors but have fly-by-night business models. It is best to do a thorough check on the company and its management before making any investment decision.

THE GROWTH FACTOR

If you have been a regular investor, you are no stranger to the fact that share prices are driven by growth. Hence, you need to look at the growth trajectory of a company before you make your investment decision.

Little or no growth does not augur well for a company or an industry. Markets are bothered about the future growth prospects of a company for capacity expansion plans or the order book of the company.

In a scenario like this, high interest rates and rising input costs have impacted the growth of the manufacturing sector. Core sectors such as cement, steel and electricity show a veritable slowdown in growth in difficult times. But what is working for a country like ours, where demographics are in our favour, is the domestic consumption theme.

Therefore, while the cement industry is growing at a CAGR of 8% to 10 %, the consumer durable industry is

growing at a CAGR of 15% pa. Also, watch out for the past growth rate of the company. It is especially relevant in the case of the financial sector. HDFC Bank, known to be a lender with a conservative approach, has been growing at a CAGR of more than 30% over the past few years. Look out for instances like this.

The compound annual growth rate is an important ratio traditionally looked at to measure growth. However, make sure that you do not restrict growth to growth in sales alone (net interest income in case of banks) while looking at growth.

Hence, broaden your horizon and look for growth in earnings per share to get a clearer picture. If a company is able to increase sales and profit after tax, with the dilution of equity then EPS may not grow and share prices may not be able to perform.

LOW DEBT EQUITY RATIO

Ideally, when you are looking out for debt equity ratio, the companies that have a debt equity ratio of 1 and below should be on your list. Especially at a time when the economy is slowing down, a company with heavy debt would see their profitability erode.

The high debt component goes even higher, as the working capital cycle gets stretched further and banks as well as financial institutions turn sceptical about doling out loans at these times. The companies that start borrowing to repay the debt and interest, may fall into a further debt trap. Rising interest cost to service the high debt is bad news to the company.

At such times, companies resort to desperate measures such as selling assets at unattractive prices. In a slowdown like situation, companies with a high debt component are likely

It’s simplified...Beyond Market 19th Sept ’1114

to get de-rated and this impacts their valuation negatively.

On the other hand, companies that have low debt can not only keep their interest costs down successfully, they can also invest the cash back into the business in times of trouble. If a company has a history of high debt to equity ratio, it indicates inefficient management of cash flows. Companies may have painted a rosy picture, showing great expansion plans and justifying the need to leverage, but it all comes to naught when bad times fall upon them.

During a slowdown, companies with high debt may even face critical risks to their business in the absence of adequate cash flows. An investor should carefully look at the debt equity ratio and avoid companies that are high on this parameter.

HIGH ROE

While making an investment decision you may obviously want to invest in a company that generates profits more efficiently than its rivals. The Return on Equity or ROE gauges the profit-generating efficiency of a

company. For an investor, the ROE can be the single most powerful tool to analyse the efficiency of a company and can give you a clearer picture instead of just looking at the PE ratio of the company.

The thumb rule here is that the ROE has to be more than the cost of capital. The Return on Equity is calculated on the basis of profit after tax as percentage of networth, whereas cost of capital is risk-free rate of interest plus risk weighted premium. (10 years GOI bond yield at 8.25% + risk weighted premium rate of say 6%, so cost of capital is 14.25%). If a company is not able to generate a consistent ROE of over say 14.25% in the long run, there is no point of investing in that company.

High growth companies with an ROE of around 20% or more are considered as good companies in the Indian context. You can say that these companies have good fundamentals and a defined growth path.

If the ROE of a company has been increasing over the years, it means that the company is operating in an improved business environment and is making efficient use of capital. This

generally translates into improved valuations for the company.

On the other hand, if the ROE of the company is decreasing, one needs to be cautious. However, sometimes decreasing ROE could be an implication of cyclical factors that are short term.

However, if it continues for a longer period of time, you can consider exiting. A high ROE company is, therefore, a definite pick. Companies which have a low debt component as well as a high ROE are definite winners and can be considered by market players.

REASONABLE VALUATIONS

Last but not the least, remember that you have to find a growth stock at a reasonable valuation. Despite all the above parameters working in favour of the company, if the valuation is excessively high as compared to its peer group, something is definitely amiss. The stock may have lost its steam and is fairly valued at this stage. Hence, it does not make sense to feature it in a portfolio. But take a through look at the historical valuations before your decide.

Some of the stocks that can be picked based on the discussed criteria for creating a quality portfolio are:

D/E(x)

ROE Correctedfrom 52W

P/E(x)

CMP(`)

FY12 EPS(`)

52 W High(`)

1.90 20.23% -45% 11 162.20 14.8 295.1

IRB Infrastructure Developers Ltd

NHAI's is likely to award 7,300km of projects in FY12. And the IRB Management intends to bid for projects worth `15 billion and above, to achieve targeted IRR of 16%. Moreover, competition is likely to ease, given individual balance sheet constraints. IRB hiked toll rates at major stretches – Mumbai-Pune Expressway in Apr’11 by 18% and Bharuch-Surat-Dahisar Expressway by 8% in Jul’ 11. The Management has also indicated that the toll rate for Surat-Dahisar is likely to increase 9%-10% in Sep ‘11. This will enhance tolling revenue for FY12. The two projects – Surat-Dahisar (expected in Sep ’11) and Kolhapur BOT would be completed in FY12. IRB has a strong unexecuted order book of `111.7 billion. The debt to equity of 1.9x is normal for the industry it operates in.

It’s simplified...Beyond Market 19th Sept ’11 15

Cadila Healthcare Ltd

Cadila Healthcare Ltd is the fifth largest research-oriented Indian pharmaceutical company having presence across the Pharma value chain. Cadila is expected to post strong sales and profit growth over the next two years on account of sales from newer territories, new product launches and deeper penetration in existing regions.

Coromandel International Ltd

Coromandel is a leading player in the Indian fertilizer industry and manufactures a wide range of products like fertilizers, specialty nutrients, crop protection, etc. It is the second largest phosphatic fertilizer player in India and set to benefit the most with nutrient-based subsidy scheme announced for complex fertilizers. It has grown at 38.7% CAGR over the last four years.

Infosys Ltd

Infosys is known for its good management and corporate governance. Currently, the stock is available at 16.5x the FY12E earnings. The management has guided for 18%-20% growth for FY12 and historically, the company has always succeeded its guidance

0.51 32.70% -15.9% 20.4 827.25 40.5 984

0.85 40.10% -20.80% 12.3 297.85 24.2 376

D/E(x)

ROE Correctedfrom 52W

P/E(x)

CMP(`)

FY12 EPS(`)

52 W High(`)

0.00 27.90% -36.30% 16.2 222.40 136.9 3494

D/E(x)

ROE Correctedfrom 52W

P/E(x)

CMP(`)

FY12 EPS(`)

52 W High(`)

Dena Bank

We expect Dena Bank to improve its core operating metrics going forward driven by focus on its liability franchise with operating efficiency. Dena Bank has been able to sustain growth in advances above industry average and has major presence in the state of Gujarat, which has the highest GDP among the Indian states. Higher exposure in Gujarat, increasing focus on high-yield retail credit, strengthening of balance sheet, coupled with lower operating costs would improve efficiency and drive earnings, going forward.

ROE Corrected From 52W P/BVROE 52 W High(`)

CMP(`)

20% -47.30% 0.7 151

FY12BV(`)

10779.60

D/E(x)

ROE Correctedfrom 52W

P/E(x)

CMP(`)

FY12 EPS(`)

52 W High(`)

It’s simplified...Beyond Market 19th Sept ’1116

Ajanta Pharma Ltd

Ajanta Pharma is a NDDS (New Drug Delivery System)-based pharmaceutical company. It is enhancing its spectrum of products with new therapeutic areas and its reach by hiring more sales people. After making its strong footing in domestic and emerging markets, the company is now targeting the US market with its first ANDA approval and poised for filing more ANDAs in the coming years.

Yes Bank’s return ratios have been consistently good for over three years. Moreover, the asset quality is the best in the listed Indian banking industry with net NPAs of 0.01%. In addition, the bank’s business and CASA are expected to improve going forward along with the scope to improve other income.

Yes Bank Ltd

Axis Bank Ltd

We remain positive on Axis Bank, owing to its attractive CASA franchise, rapid branch expansion, healthy asset book, sustainable fee income, strong growth outlook and good management. We believe that the recent decline has made Axis Bank’s valuation attractive, both in absolute and relative terms. The stock has corrected sharply and is currently trading at 2.1x FY12E BV.

Maruti Suzuki Ltd

Maruti Suzuki continues to hold a dominant position in the passenger car segment with a 51% market share. We expect Maruti Suzuki’s volumes to improve once the deliveries of new Swift cars take place on a larger scale from the current month. In addition to this, the company’s installed capacity will rise to 1.65 million units pa once the second plant at Manesar facility becomes operational in September ’11. We believe that the expansion in capacity will enable the company to cater to higher demand in the festive season.

0.04 17.80% -32.80% 12.5 1075.1 86 1600

D/E(x)

ROE Correctedfrom 52W

P/E(x)

CMP(`)

FY12 EPS(`)

52 W High(`)

0.83 22.20% -11.40% 5.7 326.20 57.30 368

D/E(x)

ROE Correctedfrom 52W

P/E(x)

CMP(`)

FY12 EPS(`)

52 W High(`)

ROE

21% -29.40% 2.10 388 131.70273.8

Corrected From 52W P/BVROE 52 W High(`)

CMP(`)

FY12BV(`)

ROE

19% -34.60% 2 1608 537.81051.4

Corrected From 52W P/BVROE 52 W High(`)

CMP(`)

FY12BV(`)

It’s simplified...Beyond Market 19th Sept ’11 17

Bajaj Electricals Ltd

The recent decline in the share prices of Bajaj Electricals was due to poor Q1FY12 results on account of specific reasons. We believe these reasons would correct in the coming quarters, easing concerns about the company. The company is among the few listed players who have a presence in small consumer appliances market. The industry is riding high on the growing India consumer story. Bajaj Electricals derives 70% of its revenues from consumer businesses — lighting and kitchen appliances. It enjoys a leadership position in the northern and eastern regions in appliances such as fans, compact fluorescent bulbs and mixer-grinders. The recent correction in copper and aluminium prices and efforts to control working capital and inventory may help the company contain margin pressures in this business.

At a time when there is rampant fear in the markets about a further decline, you as an investor, should not despair. Instead you should remain focussed on how you can catch the bottom. Make use of this time to diversify and invest in 4 or 5 parts in every decline. The good news is that though valuations are below their historical averages, the long-term India story is still intact. Therefore, make the most of the opportunities that the markets are providing noW.

0.19 26.20% -48.60% 10.5 178.45 17 374

D/E(x)

ROE Correctedfrom 52W

P/E(x)

CMP(`)

FY12 EPS(`)

52 W High(`)

EQUITIES | DERIVATIVES | COMMODITIES* | CURRENC Y | MUTUAL FUNDS # | IPOs # | INSURANCE # | DPDisclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme related document carefully before investing. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. The PMS Service is not o�ering for commodity segment. *Through Nirmal Bang Commodities Pvt. Ltd. #Distributors

SMS ‘BANG’ to 54646Contact at: 022-3926 9404, E-mail: [email protected]

BSE SEBI REGN No. INB011072759, INF011072759 & INE011072759, NSE SEBI REGN No. INB230939139, INF230939139 & INE230939139 DP SEBI REGN. No NSDL: IN-DP-NSDL-136-2000, CDS(I)l: IN-DP-CDSL-37-99, AMFI REGN. No. arn-49454 NCDEX REGN. NO. 00362, FMC Code-0075, MCX REGN. No. 16590, FMC Code-MCX/TCM/CORP/0490, MCX SX-INE260939139, PMS-INP000002981

Registered O�ce: 38-B, Khatau Building, 2nd Floor, Alkesh Dinesh Mody Marg, Fort, Mumbai - 400 001. Tel: 264 1234 / 3027 2000 / 2005; Fax: 30272006Corporate O�ce: B-2, 301/302, 3rd Floor, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel.: 39268000 / 8001 Fax: 39268010

The need for a more comprehensive legal framework necessary to promote

growth of private pools of capital led the SEBI to formulate a set of

guidelines to regulate alternative investment funds

increasingaccountability

It’s simplified...Beyond Market 19th Sept ’1118

It’s simplified...Beyond Market 19th Sept ’11 19

arket regulator, the Securities and Exchange Board of India (SEBI) recently

issued a draft proposal to regulate alternative investment funds (AIF) such as private equity funds, real estate funds, infrastructure funds, debt funds and hedge funds, among others. The watchdog is making an attempt to bring these alternative investment funds under its purview and regulate the private pool of money flowing into them.

At present, the regulation is limited to mutual funds, collective investment schemes (CIS), venture capital funds (VCF) and portfolio managers. As far as mutual funds and CIS from the retail segment are concerned, the SEBI has done a commendable job. However, the existing rules and regulations in the non-retail segment are not comprehensive.

With the AIF regulations, the SEBI wishes to bring an umbrella rule catering to such pool of capital. Let us look at the draft proposal, the rationale behind it and the reaction to it by those from the industry.

WHY THE NEED?

SEBI (Venture Capital Funds) Regulations, which were framed in 1996 to encourage funding of entrepreneurs in early‐stage companies, has lost its context.

Of late, funds have found their way into listed companies or real estate (through Private Investment in Public Entity deals or special purpose vehicles), which already have easy access of funds through other routes. Hence, the very purpose of venture fund is defeated.

The AIF guideline is the result of such regulatory gap. This has been necessitated to keep a check on the

M kind of money flowing into venture capital funds, considering the risk of money laundering. Over the years, the definition of venture capital and private equity has blurred with an overlap in their investment avenues.

There was also a need to formulate a regulatory framework for the AIF industry so that the necessary concessions or restrictions reach the desired kind of funds.

Taking cues from the western markets, especially the United States, which recently imposed strict regulations on hedge funds as well as private equity funds, the SEBI has come up with the draft paper with a three-fold objective.

First, to avoid any kind of systemic risks as funds manage huge amount of money and some funds may also be highly leveraged.

Second, to make clear distinction between the different types of private pooled investment vehicles and channelize them in the desired space in a regulated manner and third, to improve disclosures and avoid frauds by adequate reporting requirements and legal agreements. THE DRAFT PROPOSAL, INVESTMENT CONDITIONS AND RESTRICTIONS

can register itself into any of the following categories - (i) Venture Capital Fund (ii) PIPE Funds (iii) Private Equity Fund (iv) Debt Funds (v) Infrastructure Equity Fund (vi) Real Estate Fund (vii) SME Fund (viii) Social Venture Funds (ix) Strategy Fund (Residual Category, including all varieties of funds such as hedge funds, if any) - as per its investment strategy.

required to be close ended and mandatorily registered with the market regulator along with their individual schemes.

investment strategy, investment purpose as well as business model in an information memorandum to all the investors.

be `20 crore and the initial size should be specified to the SEBI. The fund size can be revised upwards up to 25% after giving suitable reasons.

by an investor should be 0.1% of the total fund size subject to a minimum of `1 crore.

contribute from its own account an amount of investment equal to at least 5% of the fund whose investment shall be locked-in till the redemption by all investors in the fund.

minimum period of 5 years and the extension of the tenure of the fund may be permitted up to 2 years only at a time and to be approved by 75% of the beneficiaries.

of the fund’s corpus in a single investee company.

(i) Non Banking Financial Companies (excluding Infrastructure Finance Company, Asset Finance Company, Core Investment Company or companies engaged in microfinance activity in case AIF is not a Strategy Fund) (ii) Gold Financing (excluding gold financing for jewellery) (iii) Activities not permitted and under Industrial Policy of the Government of India.

It’s simplified...Beyond Market 19th Sept ’1120

ALTERNATIVE INVESTMENT FUNDREGULATION [PROPOSED]

VENTURE CAPITAL FUNDS REGULATION[EXISTING]

It is mandatory for all funds and their schemes to register

The minimum investment by an investor proposed to the

higher of 0.1% of fund size or `1 crore. [Impact: Will

limit retail money into AIFs]

Increase the minimum size of the fund to `20 crore

The AIF regulations requires the sponsor to commit

to invest at least 5% of the fund

It is not mandatory to register

It is `5 lakh

Commitment of `5 crore for the launch of the scheme

The VCF regulations do not stipulate a sponsor

commitment

TYPE OF FUND CONDITIONS FOR EACH CATEGORY

Venture Capital Fund

PIPE Fund

Private Equity Fund

Debt Fund

Infrastructure Fund

SME Fund

Real Estate Fund

Total investment in the fund cannot be more than `250 crore. The fund can be used

to promote only ventures with new innovative ideas or new technology in the start-up

stage or early stage. Not permitted to invest in any company that is promoted,

directly or indirectly by any of the top 500 listed companies by market capitalization

or by their promoters.

Invest in shares of listed companies which are not part of any market index. PIPE funds

will be exempt from applicability of insider trading restriction, which will help funds

conduct due diligence on the investee company.

Invest in unlisted equity, equity-linked instruments of companies which require medium

to long-term capital. Invest at least half of the fund in equity shares or equity-linked

instruments of an unlisted company and shall not invest more than half in the equity

or equity-linked instruments of a company which is proposed to be listed. A PE fund

shall not invest more than 50% in unlisted debt of a portfolio company.

60% of the corpus in debt or debt instruments of unlisted companies,

not more than 25% of which may be in convertible debt, with a minimum maturity

of 5 years. Remaining 40% in securitized debt instruments, debt securities of listed

company and equity shares of unlisted portfolio company.

Can invest at least two-thirds of its corpus in the equity or equity-linked instruments

of infrastructure companies or SPVs of infrastructure projects.

Should invest primarily in the unlisted equity or equity-linked instruments of SMEs

or SMEs proposed to be listed on the SME exchange. Can take delivery of securities

in the process of market-making.

75% of its corpus in real estate projects or fully built properties or in real estate special

purpose vehicles. Up to 25% of the corpus in allied sectors of real estate.

CONDITIONS SPECIFIED FOR EACH CATEGORY OF AIF

Some Of The Important Conditions For Each Category Of AIF Are As Follows:

It’s simplified...Beyond Market 19th Sept ’11 21

THE MOOT POINT

The draft proposal has evinced mixed reaction in the industry. Many experts are of the opinion that ‘too-much’ categorization will increase the regulatory cost for the funds. Also, the need for individual schemes to stick to their pre-defined investment strategy will rob the fund of the advantage of diversification into different avenues to mitigate risk. Clearly, the SEBI has concentrated more on micromanaging the fund and the way they should invest instead of safeguarding the risk in investing in AIF, they feel. The minimum

participation of `1 crore from the investor in the fund will keep retail investors at bay, thus prohibiting them from taking advantage of private equity as an asset class.

Also, the requirement by the sponsor to commit to invest at least 5% of the fund effectively means start-up fund managers cannot raise large funds even if they have the capability to do so as they will have to put forward 5% of the asset under management from their own pocket. It also means that only big funds with deep pockets will dominate the industry.

Other worrying prospect of the draft

is the reservation of the PIPE fund to invest in non-index companies. This requirement will severely affect the interest of reputable foreign funds in index stocks and they will have to register as a FII or P-note.

SEBI has admitted that the capital flow through AIF is “good quality money” and “plays a very important role in the growth of the corporate sector”. With this as background and the slowdown in FDI in the past few years, the timing of the draft paper has surprised many and the last thing that the SEBI and the government want is a pause in activity due to such a regulatioN.

TYPE OF FUND CONDITIONS FOR EACH CATEGORY

Social Venture Fund

Strategy Fund

Targeted to investors who are willing to accept muted returns. Required to invest in

social enterprises as per norms laid down by the fund, such as micro finance institutions.

May specify any strategy in any class of financial instruments and may invest in

derivatives and complex structural products, subject to requirement of suitability

and disclosure to investors.

QUALWe understand and value the equation of our relationships. Which is why, we offer our sub-broker/authorized person/remisier equal independence and status that our partner merits.

That apart, we provide unparalleled knowledge and exceptional market analysis to keep you ahead of the curve, to the advantage of your customers.

After all, at NIRMAL BANG, it’s a relationship beyond broking.

BSE SEBI REGN No. INB011072759, INF011072759 & INE011072759, NSE SEBI REGN No. INB230939139, INF230939139 & INE230939139 DP SEBI REGN. No NSDL: IN-DP-NSDL-136-2000, CDS(I)l: IN-DP-CDSL-37-99, AMFI REGN. No. arn-49454 NCDEX REGN. NO. 00362, FMC Code-0075, MCX REGN. No. 16590, FMC Code-MCX/TCM/CORP/0490, MCX SX-INE260939139, PMS-INP000002981

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme-related document carefully before investing. Security is subject to market risk. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. The PMS Service is not offering for commodity segment. *Through Nirmal Bang Commodities Pvt. Ltd. #Distributors

Registered Office: 38-B, Khatau Building, 2nd Floor, Alkesh Dinesh Mody Marg, Fort, Mumbai - 400 001. Tel: 39268600 / 8601; Fax: 39268610, Corporate Office: B-2, 301/302, 3rd Floor, Marathon Innova, Off Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel.: 39268000 / 8001 Fax: 39268010

AT NIRMAL BANG, YOU’RE MORE THANJUST A BUSINESS ASSOCIATE,YOU’RE AN EQUAL PARTNER.

Contact Person: Gaurav Mohta - 7738380299 & Nilesh Sonawane - 7738380027

Address: B-2, 301/302, 3rd Floor, Marathon Innova, O�. G. K. Marg, Lower Parel (W), Mumbai - 400013.

EQUITIES | DERIVATIVES | COMMODITIES* | CURRENCY | MUTUAL FUNDS | IPOs | INSURANCE | DP www.nirmalbang.com# # #

It’s simplified...Beyond Market 19th Sept ’1122

The introduction of new

global indices futures trading

by NSE will enable market

par ticipants to bene�t from

S&P 500 and DJIA

ndian retail investors are becoming more sophisticated in their investment approach. With more educated people taking interest in investment, even those from the middle class are seen taking up

trading and/or investing as a part-time activity. They are not only taking keen interest in equities, but also in forex, commodities and other asset classes. The introduction of new global indices futures trading by the National Stock Exchange (NSE) is a step forward in that direction.

People who have long wanted to take exposure in popular equity indices in the overseas market can do so now. NSE will offer futures trading in S&P 500 and DJIA, two of the world’s most followed indices and considered as the barometers of the US equity market. The trading will take place during Indian market hours and will certainly help the Indian investors in managing their risk, as well.

I

NEW OFFERINGSWITH A GLOBAL

APPEAL

It’s simplified...Beyond Market 19th Sept ’11 23

WHAT IS S&P 500?

It is a free-float market capitalization weighted index of 500 leading companies of the US economy and is considered as a benchmark index in the US equity market. Introduced in 1957, the index mainly covers large and mid-cap stocks. It captures 75% of the total US equity market. Hence, is a good indicator of the economy. The index selects its companies based on their market size, liquidity and the sector they belong to.

WHAT IS DJIA?

Dow Jones Industrial Average, also known as Dow 30, is a price-weighted stock index. The Industrial portion of the name is largely historical, as many of the modern 30 components have little or nothing to do with traditional heavy industry.

First introduced in the year 1896, the index consists of 30 most actively traded liquid blue-chip stocks. Though this index captures only 28% of the US equity market, its performance is closely linked to that of S&P 500. The index value gets influenced only by changes in market prices of individual stocks. Sole change in the number of shares does not impact its value.

NSE GLOBAL INDICES OFFER

Indian investors are currently permitted to trade in foreign securities subject to a limit as stipulated by the RBI. Many investors either do not know about real good brokers who offer trading in these foreign securities or are sceptical about others. They may also have to incur higher transaction costs if they don’t have the right information about these foreign brokers. Further, trading in the US equity means exposing oneself to the foreign

exchange risk, in addition to the equity market risk. Futures contracts offered by NSE are denominated in rupees. Hence, investors need not take any currency risk. This will provide an opportunity to investors to diversify their portfolio and make it more global.

It can also be used as a hedging tool by investors who want to hedge their sector-specific risk for those sectors whose performance is highly linked to the US economy.

For example, the Indian IT sector derives more than one-third of its revenue from the US and one can hedge the Indian IT portfolio by taking appropriate positions in the S&P and DJIA. Finally, traders can devise appropriate trading strategies by looking at different kinds of relationships that exist between the US and Indian indices.

USE OF GLOBAL INDEX FUTURES

Depending upon the risk profile of individual investors, these contracts can be used for different purposes. Some of the participants who can benefit from these contracts are investors with directional views, spread traders, HNIs and persons or companies with business having a high overseas exposure.

DIRECTIONAL VIEWS

Investors, who track the US economy and the markets on a regular basis, can take a position on the movement of these indices, which reflect the state of affairs of the US economy. They can make direct profits from the positions they have undertaken.

For example, based on the recent job market, US GDP growth data you think that S&P 500 will increase in value and long the futures contract. If

your forecast turns out to be true, then you can make money.

DIVERSIFICATION

Investors, who invest in various global asset classes like bonds and stocks of various countries, commodities, foreign currencies, etc, can diversify the risk of their overall portfolio by taking positions in S&P and DJIA futures contract.

The US economy has a big impact on various asset classes. Hence, S&P and DJIA can be considered as good instruments for diversification, like an investor holds stocks of emerging economies like India, China, Brazil, Taiwan, South Korea, etc.

Consider a scenario where because of a high inflation situation the stocks from these countries start moving down. At the same time, the US economy, without getting affected by inflation, might be doing well. In such a scenario, stocks from the US will perform better than their US counterparts. If the investor also holds the S&P and DJIA futures position, then his portfolio will not suffer much. TRADING

Various correlations exist between S&P500, DJIA and other global indices, including Nifty and Sensex. Investors/traders should carry out their own research and find out the correlation. They can devise trading strategies to generate profits.

For example, historically, the US and Indian indices moved in tandem. However, due to some critical economic events, there can be some temporary divergence between the two equity indices. Traders could benefit from such happenings in the market and take appropriate positions in both these index futureS.

It’s simplified...Beyond Market 19th Sept ’1124

n an attempt to control inflation, the Reserve Bank of India (RBI) has revised key interest rates as many as 11 times since March ’10, despite slowing growth in the country and uncertain growth demand.

The hike in key policy rates subsequently results in the hike in home loan rates, thus impacting home loan takers directly. However, if there is no rise in interest rate or that the rate falls, the EMIs would also come down.

But the rise in key policy rates and the following rise in interest rates can be quite damaging on the home loan taker as it would either lead to an increase in EMI with no change in the tenure of the loan or an increase in the tenure of the loan with no impact on the EMI.

This can be better explained with an example. If Ram has taken a home loan of `30 lakh at an interest rate of 11% per annum for a tenure of 20 years, his EMI would be `30,966.

I

INYOURBEST

INTERESTBorrowers would be

better o� if they prepay their loan

amount or get the tenure of their loan

extended wheninterest rates rise

Particulars

Original Loan

Loan Amt

30,00,000

Tenure

20

ROI

11%

EMI

30,966

Interest Due

44,31,840

Total Amt

Payable

74,31,840

Particulars

Case 1: Change in EMI

Case 2: Change in tenure with

the EMI remaining the same

Loan Amt

30,00,000

30,00,000

Tenure

20

23

ROI

11.50%

11.50%

EMI

31,933

30,966

Interest Due

46,78,320

55,25,620

Total Amt

Payable

76,78,320

85,25,620

Suppose the interest rates were to increase by 50 bps to 11.5%, then:

When Ram originally took the home loan, he was paying an EMI of `30,966 per month. But after the interest rate increases from 11% to 11.5%, two possibilities arise:

Case 1: If the tenure of the loan were to be kept constant, with an increase in interest rate by 50 bps, the increase in EMI would be `967 per month and an annual increase of `11,604 and the total outflow on the 20-year loan along with the interest component would be `76,78,320, which is `2,46,480 higher than his original outflow. Ram would be fine with this arrangement provided the increase in the EMI does not materially impact his cash flows.

Case 2: If the EMIs were to be left constant in line with the original loan but the tenure were to be increased to incorporate the effect of the 50 bps hike in interest rates, Ram would have to pay EMIs for 36 more months than originally planned. By increasing the tenure of the loan, you are essentially changing the mix of your principal and interest repayment. Since your principal repayment will be extended to more than 20 years on which you will be paying interest,

It’s simplified...Beyond Market 19th Sept ’11 25

your total cost of the loan would increase by `10,93,780 which is much higher than Case 1. If Ram’s finances start getting stretched due to the increase in the EMI, he is left with this option and will have more time to pay the loan. Some banks offer people the choice to select either the option under case 1 or case 2.

However, banks are sceptical to increase the tenure of the loan beyond 20 years. If such is the case, you may find yourself in a tight spot.

In a rising interest rate scenario, individuals should look for options to prepay some portion of the loan their financial situation permits. Prepaying a loan means you are repaying a part of the principal, which will automatically bring down the interest component of the loan.

Before you opt for prepayment of the loan, go through the fine print of the loan document, which has a clause on prepayment. There is likely to be a prepayment penalty, which needs to be taken into consideration if you are re-financing your loan because the penalty can be as high as 2% to 3% of the outstanding loan amount.

MODES OF PREPAYMENT

Personal Funds: If this is your source of fund, you can negotiate with the bank and get the penalty lowered or waived off. Most banks are willing to waive off the prepayment penalty provided you prove that the proceeds from repayment belong to you or your co-borrower. The best way is through the bank account statement.

Hence, if you are borrowing money from friends or relatives, make sure it comes to you through your bank account. In a rising interest rate scenario, there are many requests for prepayment and banks have become more stringent.

As long as you are able to prove that the source of funds is personal, you can expect a waiver from the bank on prepayment penalty. Also, when a borrower partially prepays the loan, banks tend to waive off the prepayment penalty. But you need to check the quantum with the bank.

HDFC Bank allows prepayment of up to 25% of the outstanding loan amount without charging any prepayment penalty.

If you have fixed deposits yielding you less than the interest you are paying on your home loan, it makes sense to liquidate it, invest and prepay your home loan.

Prepaying your loan will reduce your EMI burden as you’re repaying the principal. But make sure you don’t have outstanding unsecured loans such as credit card loans or personal loans. These should get first preference as far as repayment is concerned as they carry a very high interest rate due to the risk element.

Refinancing/ Switching Of Loans: If you find it is an attractive proposition to take a new loan to prepay your existing home loan due to attractive terms and conditions, then do so after thoughtfully considering your prepayment penalty.

It is advisable to negotiate about the prepayment penalty especially if you have a good credit history. However, it is harder in case of re-financing because it means loss of business to a competitor in case of a bank. If you have to incur a penalty for prepaying your loan amount, you need to figure out how much interest you will save after taking into consideration the outflow on account of the penalty. If you find that savings on interest payments are much higher than the prepayment penalty, then it

makes more sense to prepay the loan.

SHOULD YOU PREPAY YOUR LOAN?

If you are able to refinance your loan with another one with better terms and conditions after taking into consideration the prepayment penalty, it makes sense to go for it.

If you have surplus funds, straight away prepay the loan to whatever extent possible and reduce your principal amount. It will thus bring down the interest component.

In a rising interest rate scenario, very few investments will give you a post-tax return that will be greater than the interest rate charged on the home loan. Hence, it is better to liquidate investments to prepay outstanding unsecured loans.

IF PREPAYMENT IS NOT AN OPTION?

Home loan is an investment of a life time for an individual. So it is quite possible that one would have already stretched himself financially and, hence, would find it difficult to pay a higher EMI.

In such a scenario extending the tenure of the loan is the only option. Increasing the tenure of the loan raises the total interest outflow significantly as is indicated in the example mentioned earlier.

If it is possible for the home loan- taker to bear the stress of an increase in the EMI, it is certainly better than opting for an increase in tenure. Even better would be to mop up funds to prepay the loan to the extent needed to keep the EMI constant.

Whatever be the case, it is in the best interest of a home loan taker to act after weighing his optionS.

It’s simplified...Beyond Market 19th Sept ’1126

The turbulence in the US economy and the uncer tainty

in the Eurozone do not bode well for an expor t-led Asian

economy like India

ndia’s exports registered a whopping growth of 81.8% at $29.3 billion in July this year as compared to the previous year. The growth was led by good performance by sectors such as engineering, petrochemical products and gems and jewellery. In fact, this is not a monthly

aberration, exports have been showing robust growth over the past few months.

However, looking at the global scenario, there is a high probability that the trend might reverse. The same is true for Indian companies which are largely dependent on the export markets. The economic instability and uncertainty in the euro zone and the US and the expected slowdown could impact the demand for Indian companies’ products and services.

I

It’s simplified...Beyond Market 19th Sept ’11 27

Meanwhile, the debate is on and the views are several as no one is sure about the situation that could unfold in the coming times. However, as informed investors, the best thing is to keep an eye on these developments and stay cautioned about companies with high exposure to exports or overseas markets, particularly those with a high exposure to countries in the developed world, especially in the US and the Euro zone.

USA AND EUROPEAN COUNTRIES

THE BIGGER ISSUE

During the global financial crisis of 2008-09, exports from emerging markets were severely hit and declined by 7.5% by the end of 2009. In the case of India, export growth tumbled to negative 3.6% in FY10 as compared to about 30% in FY08. However, with the economies recovering in the western world by the end of 2010, exports growth in the emerging markets was strong at 14.5%.

Economists are not forecasting a similar slump in the world trade as we saw in the last global financial crisis, but surely a decline is on the cards. In its note on the outlook of the world economy published in April, the IMF said in the current year the growth in exports from the emerging economies, including India could just be half of last year.

policy handicap.

This is also evident from the recent downgrade of the US by the global ratings agency Standard’s & Poor to AA+ from AAA, with a negative outlook.

According to reports, the downgrade of the US economy would impact exports and affect liquidity positions of Asia-Pacific countries. Further, the IMF expects the US economy to grow just 2.5% in the current year as against 2.8% last year.

The situation in the Euro zone is equally worrying where most nations are going through difficult times and the governments are busy cutting corners to trim their deficits and bring down debt levels.

Overall, the most troubled economies across the globe, namely the US and Europe, which also happen to be major contributors to India’s exports, including sectors like textile, IT, gems and jewellery and leather and machinery, among others, could continue to affect exports for some time, at least.

POCKETS OF WEAKNESS

The IT sector has already come in the limelight, which is logical given that most large Indian IT companies generate almost 80% to 90% of their revenues from the international markets, mainly the developed markets of the US, Europe and others.

Even the most diversified player would not be able to escape the aftereffects of the slowdown across regions and sectors. The only saving grace that these companies could have is that unlike during the last crisis, the financial sector is not impacted or may not get impacted significantly; the most prominent Banking, Financial Services and Insurance (BFSI) sectors’ revenues of the Indian IT companies could see some relief.

During the financial meltdown of 2008-09, BFSI was the most impacted segment, given that a large number of banks, insurance companies and firms on the Wall Street were battered heavily or went bankrupt, forcing them to cut spending. However, the overall impact on demand could be seen in the coming months and will be reflected in the share prices of most Indian IT companies, which are significantly down from their peaks in the recent past.

During the economic crisis, IT majors like Infosys, Wipro

2009 2010

World Trade Volume Growth (%)Emerging Market Export Growth (%)

–10.9–7.5

12.414.5

2011E

7.48.8

2012E

6.98.7

Export Growth

Source: IMF

2009 2010

U S A EurozoneJapan

–2.6–4.1–5.2

2008

00.5

–1.2\

2007Country

2.12.72.3

2.81.73.9

2011E

2.81.61.4

2012E

2.91.82.1

GDP Growth

Source: IMF

This could still be conservative estimates, given that a lot of things and fresh concerns over the likelihood of double dip in the US economy and a further slowdown in the European countries have recently sprung up.

In fact, in its note, the IMF has already cut its GDP forecast for developed countries to about 2.2% as against the earlier estimate of 3%.

In the US, there are enough indications of a slowdown as unemployment is seen returning to its crisis levels and the slump in the housing market persists. Besides, fiscal concerns and high debt in the United States have led to uncertainty over its economic environment, leading to a

It’s simplified...Beyond Market 19th Sept ’1128

and TCS reported a significant fall in volumes growth.

The global research firm Forrester has already lowered its growth forecast for the IT market in the US to about 6.5% compared to 7% earlier. However, these estimates are still considered to be more optimistic or on the little higher side as recent news flow is yet to be factored in to the estimates.

CONSUMER SENTIMENTS

Apart from the IT sector, companies from sectors such as textiles, leather, gems and jewellery that supply products to US retailers like Wal-Mart, could see a shrinkage in demand owing to the cut in spending by consumers and buyers in America.

The signs of weakness are already visible; the confidence among the US consumers plunged to 54.9% (63.7% in the previous month) in the month of August to the lowest level since mid 1980, fuelling concerns that weak employment gains could put pressure on spending.

Apart from consumer goods companies, Tata Motors, Tata Steel, Hindalco and Suzlon to name a few have a large presence in the overseas markets like the US and Europe through their subsidiaries, although they are not majorly into exports and could be affected due to the turmoil in these markets.

Interestingly, the subsidiaries of these companies account for a majority of their Group’s revenues. This means any slowdown in these markets would hit the overall performance of Indian businesses, as well.

MIDDLE EAST COUNTRIES

Market participants also need to keep an eye on companies such as L&T and Punj Lloyd from the engineering and construction space as they have huge exposure in Middle East countries, which are susceptible to crude oil prices.

If the propellers of the world economic growth and the largest consumers like the US, Europe and Japan

slowdown, this would certainly have a negative impact on the demand for crude oil, and subsequently its prices.

This, to some extent, will also hit the Middle East economies as their large government spendings are financed through the proceeds from crude oil exports.

Also, the global investments in the hydrocarbon sectors will get impacted leading to further spill over in demand for engineering and other ancillary services like offshore, oil and gas pipes, etc.

Most Indian steel pipe companies generate their revenues from these markets. Crude oil prices are already down from their recent peaks mainly due to concerns over growth in the western world. DOLLAR-RUPEE RATE

In addition to the demand-side issues, which are linked to the economic growth of these regions, the rupee to dollar rate will equally impact export growth of the Indian companies, especially the earnings and profitability of these companies.

The rupee to dollar rate has been very volatile in the recent past. This year the rupee depreciated against the dollar to touch a high of 45.95 in January, but it later appreciated.