mark fields president and ceo - ford · · 2017-12-11mark fields president and ceo january 12,...

TRANSCRIPT

Mark Fields President and CEO

January 12, 2016

DEUTSCHE BANK GLOBAL AUTOMOTIVE CONFERENCE

SLIDE 2

CREATING VALUE

The Drivers Of Value

RISK REWARDS

GROWTH RETURNS

�!

�

SLIDE 3

G L O B A L M A R K E T S H A R EFord global market share estimated at 7.3%, up 0.2 percentage points

F O R D C R E D I TManaged receivables grew 13% from 2014 reflecting our Automotive growth and higher Ford Credit share of f inancing

R E V E N U EAutomotive revenue highest since 2007

V O L U M EWholesale volume highest since 2005

2015 A BREAKTHROUGH YEAR – GROWTH

Wholesale Volume, Revenue, And Global Market Share Increased In 2015

SLIDE 4

A U T O M O T I V E O P E R A T I N G C A S H F L O WBest since at least 2001

A U T O M O T I V E O P E R A T I N G M A R G I NHighest since at least the 1990s

C O M P A N Y P R E - T A X P R O F I T (Exc l . Spec ia l I t ems)

All-time record

2015 A BREAKTHROUGH YEAR – RETURNS

Record Financial Performance In 2015

C O R P O R A T E A F T E R - T A X R O I CHigher than cost of capital and improved year-over-year

SLIDE 5

2015 A BREAKTHROUGH YEAR – RISK

Company Risk Profile Improved

C A S H A N D L I Q U I D I T YMore than $23 bill ion cash and $34 billion of liquidity

B A L A N C E S H E E TLeverage – Consistent with single-A ratingGlobal funded pensions – Nearly fully funded and de-risked

B R E A K E V E NAutomotive – Healthy…about 80% of wholesale volumeNorth America – On target…about 2/3 of wholesale volume

R E G I O N A L P R O F I T A B I L I T YAll business units profitable except South AmericaReturned Europe to profitability

F O R D C R E D I TRobust asset performance and liquidity; return on equity > 10%Managed leverage temporarily higher than 8 to 9 to 1 target

SLIDE 6

2015 A BREAKTHROUGH YEAR – REWARDS

Increased Regular Dividend; Profitable Growth For All

2015 shareholder

distributions:

$2.5 billion

20% increase

in regular dividend

D e a l e r sE m p l o y e e sC u s t o m e r s S u p p l i e r s

SLIDE 7

2015 A BREAKTHROUGH YEAR – OPERATING

New SYNC milestone: more than 15 million vehicles with SYNC

Investing $4.5 billion in electrified vehicles by 2020

Announced Ford Smart Mobility Plan

Achieved four-year agreement with UAW

Ford Credit recognized as No. 1 in J.D. Power customer satisfaction

#1Successfully launched 16 global products

Opened last of 10 new plants to support growth in Asia Pacific

10 New Plants

Record Sales in China, More Than 1.1 Million Vehicles Sold

$4.5Billion

Quality and customer satisfaction to best-ever levels in all regions

SLIDE 8

+

� One Ford

� Product Excellence

� Innovation

Delivered with Passion

Acceleration

LOOKING AHEAD TO 2016 – OUR FOCUS

In Every Part of Our Business

AsiaPacific

Americas

Europe,

Middle East

& Africa

SmallMedium

Large

=

THE PLAN

+Profits

& Cash

PROFITABLE GROWTH

FOR ALL

SLIDE 9

ONE FOOT IN TODAY, ONE FOOT IN TOMORROW

Strengthening Today’s Business; Preparing For New Opportunities

RISK REWARDS

GROWTH RETURNS

�!

�

SLIDE 10

KEEPING OUR CORE AUTOMOTIVE BUSINESS STRONG

Building Our Future On A Strong Foundation

SLIDE 11

DisruptiveImpact OnBusiness

DisruptiveTechnology Change

New Mobility

Start-Up OEMs

Connectivity

AutomatedDriving

New Retail

Non-TraditionalEntrants

Shift To Asia

Digital Experience

Low-Cost Brands

Alternative Fuels

Electrification

Light-Weighting

Driver Assist

Source: Roland Berger Strategy Consultants

Big Data / Analytics

AUTOMOTIVE INDUSTRY TRENDS

Our Industry Is Rapidly Evolving –We Plan To Be A Leader

SLIDE 12

$2.3Trillion

$5.4Trillion

FROM MAKING VEHICLESTO PROVIDING TRANSPORTATION

Transportation As A Service Represents A Significant Opportunity

Traditional Auto Revenue

Other Transportation Services Revenue

Ford Share 6% Ford Share 0%

SLIDE 13

FORD SMART MOBILITY

Changing The Way The World Moves To Make People’s Lives Better

SLIDE 14

MAKING PEOPLE’S LIVES BETTER

Working Both Our Core Business And Emerging Opportunities To Build An Even Stronger Future

SLIDE 15

FORD SMART MOBILITY INITIATIVES

Bringing New, Emerging Opportunities To Life

� Tripling Autonomous fleet

� Added testing (M-City, CA)

� Velodynecollaboration

� Snow testing

� SYNC Connect

� Apple Car Play, Android Auto

� AppLink expansion

� SmartDeviceLinkpartners

• Ford Credit Link

• GoDrive car sharing

• Multi-modal mobility solutions

• Techstars Mobility challenge

� FordPass

� Amazon Echo

� Lincoln Miles

� IBM partnership

� Pivotal partnership

SLIDE 16

2016 BUSINESS ENVIRONMENT

External Conditions Broadly Supportive Of Continued Growth In Global Industry Sales

U.S. 17.8 17.5 – 18.5 2.5% 2.3 – 2.8%

Europe 19.2 19.0 – 20.0 1.0% 1.2 – 1.7%

Brazil 2.6 2.0 – 2.5 (3.6)% (2.0) – (3.0)%

China 23.3 23.5 – 25.5 6.9% 6.5 - 7.0%

Global 88.8 88.0 – 92.0 2.4% 2.3 – 2.8%

GDP (Pct)Industry (Mils)

2015* 2016 2015* 2016

* 2015 data estimated; China reflects retail

SLIDE 17

2016 PRODUCT LAUNCHES

Global ProductLaunches in 2016

E s c ape Supe r D u t y

F u s i o n / Mondeo4 - d o o r | H y b r i d | E n e r g i

L i n c o l n MKZg a s | H y b r i d

L i n c o l n Con t i n e n t a l

Rap t o r

GT

Fo c u s RS Fo c u s E l e c t r i c12

SLIDE 18

2016 COMPANY KEY METRICS

Sustaining Strong Financial Results In 2016

* Excludes special items

2016 FY Plan

Automotive

– Revenue Equal To or Higher Than 2015

– Operating Margin* Equal To or Higher Than 2015

– Operating-Related Cash Flow* Strong, but Lower Than 2015

Total Company Pre-Tax Profit* Equal To or Higher Than 2015

Tax Rate (Pct) Low 30s

Operating EPS* Equal To or Higher Than 2015

SLIDE 19

DRIVERS OF 2016 AUTOMOTIVE OPERATING MARGIN

Growing LeanFavorable Market Factors And Continued Investment For Profitable Growth

Margin Impact

Volume And Mix

Pricing

Cost

Parts And Service

Overall Assessment Equal To or Higher Than 2015

SLIDE 20

2016 BUSINESS UNIT PRE-TAX RESULTS

All Regions Profitable, Except South America; Sustaining Strong Performance In North America

2016 FY Plan

Automotive– North America About Equal To 2015

» Operating Margin (Pct) 9.5% or Higher

– South America Greater Loss Than 2015

– Europe Higher Than 2015

– Middle East & Africa Equal To or Higher Than 2015

– Asia Pacific Higher Than 2015

– Other Automotive Loss of About $800 Million

Ford Credit Equal To or Higher Than 2015

SLIDE 21

FORD RETURN ON INVESTED CAPITAL

ROIC Healthy And Higher Than Cost Of Capital In Majority Of Last Twenty Years

2003 2010 20141995 2004 20122005 2006 2007 2008 2009 2011 20131996 1997 1998 1999 2000 2001 2002

Five-Year Average ROIC* (Pct.)

* Based on Ford ROIC methodology

11%

16%

25%

(6)%

0%

SLIDE 22

FORD AND COMPETITORS RETURN ON INVESTED CAPITAL

Ford ROIC Compares Favorably To Industry Peers, Reflecting Relative Capital Efficiency

20142010 20122011 2013

Five-Year Average ROIC* (Pct.)

* Based on Ford ROIC methodology. For Fiat Group and GM, cumulative ROIC since 2009 reflecting post-bankruptcy results; for Fiat Group, consolidated Chrysler results effective June 2011.

FordVWBMW

GM

Fiat Group / FCA

Toyota9%

4%

(1)%

(5)%

16%

SLIDE 23

2016 FORD RISK PROFILE

Continuing To Improve Ford Risk Profile In 2016

C A S H A N D L I Q U I D I T Y

At or h igher than target levels

B A L A N C E S H E E T

Leverage – Consistent with Single-A ratingGlobal funded pensions – Ful ly funded

B R E A K E V E N

Automotive – HealthyNorth America – At target

R E G I O N A L P R O F I T A B I L I T Y

All regions prof itable except South America; Europe prof itabil i ty to improve

F O R D C R E D I T

Robust asset performance and l iquidity;ROE and managed leverage at target

F O R D S M A R T M O B I L I T Y

Concrete and meaningful progress

SLIDE 24

� Support Sale of Ford Vehicles Globally

� Target Return on Equity

� Optimize Capital Deployment

� Cash and Liquidity

� Leverage Framework

� Fund andDe-Risk Pensions

� Renew Products

� Profitable Growth

� Smart Mobility

� Restructuring

� Infrastructure

� Sustainable Regular Dividend

� Eliminate Ongoing Dilution

� Supplemental Dividend

FundThe Plan

Strong Ford Credit

ShareholderDistributionStrategy

InvestmentGradeBalanceSheet

CAPITAL ALLOCATION FRAMEWORK

Framework To Deploy Capital Successfully Implemented; Now Moving To Next Stage Of Shareholder Distribution Strategy

SLIDE 25

� Regular dividend

‒ Sustainable through a business cycle

‒ Target top quartile auto yield

� Supplemental cash dividend

Provides cash beyond regular dividend

May vary by year

Equal benefit to all shareholders; recognizes large retail ownership

$4.3

$2.4 $2.4

$9.1

$2.3

$2.5

$1.0

$1.0

Supplemental Dividend

Anti-Dilutive Share Repurchases

Regular Dividends

$6.6

$2.5

$3.5

$12.6

Shareholder Distributions (Bils.)Dividends

* Assumes 2016 regular dividend of $0.15 per share per quarter

SHAREHOLDER DISTRIBUTIONS

Declaring First Quarter Regular And $1 Billion Supplemental Cash Dividends; Plan 2016 Shareholder Distributions Of $3.5 Billion, Up About 40% From 2015

2012 - 2016*2012 - 2014 2015 2016*

SLIDE 26

WRAP-UP

Driving Toward Automotive And Mobility Leadership

� Delivered six consecutive years of strong performance, including a breakthrough year in 2015, transforming Ford

� For 2016, continuing our journey with another outstanding year as we work toward automotive and mobility leadership in the years ahead

DEUTSCHE BANK GLOBAL AUTOMOTIVE CONFERENCE

SLIDE 28

RISK FACTORS

Statements included or incorporated by reference herein may constitute "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are based on

expectations, forecasts, and assumptions by our management and involve a number of risks, uncertainties, and other factors that could cause actual results to differ materially from those stated, including, without limitation:

• Decline in industry sales volume, particularly in the United States, Europe, or China due to financial crisis, recession, geopolitical events, or other factors;

• Decline in Ford's market share or failure to achieve growth;

• Lower-than-anticipated market acceptance of Ford's new or existing products;

• Market shift away from sales of larger, more profitable vehicles beyond Ford's current planning assumption, particularly in the United States;

• An increase in or continued volatility of fuel prices, or reduced availability of fuel;

• Continued or increased price competition resulting from industry excess capacity, currency fluctuations, or other factors;

• Fluctuations in foreign currency exchange rates, commodity prices, and interest rates;

• Adverse effects resulting from economic, geopolitical, or other events;

• Economic distress of suppliers that may require Ford to provide substantial financial support or take other measures to ensure supplies of components or materials and could increase costs, affect liquidity, or cause production

constraints or disruptions;

• Work stoppages at Ford or supplier facilities or other limitations on production (whether as a result of labor disputes, natural or man-made disasters, tight credit markets or other financial distress, production constraints or

difficulties, or other factors);

• Single-source supply of components or materials;

• Labor or other constraints on Ford's ability to maintain competitive cost structure;

• Substantial pension and postretirement health care and life insurance liabilities impairing our liquidity or financial condition;

• Worse-than-assumed economic and demographic experience for postretirement benefit plans (e.g., discount rates or investment returns);

• Restriction on use of tax attributes from tax law "ownership change”;

• The discovery of defects in vehicles resulting in delays in new model launches, recall campaigns, or increased warranty costs;

• Increased safety, emissions, fuel economy, or other regulations resulting in higher costs, cash expenditures, and / or sales restrictions;

• Unusual or significant litigation, governmental investigations, or adverse publicity arising out of alleged defects in products, perceived environmental impacts, or otherwise;

• A change in requirements under long-term supply arrangements committing Ford to purchase minimum or fixed quantities of certain parts, or to pay a minimum amount to the seller ("take-or-pay" contracts);

• Adverse effects on results from a decrease in or cessation or clawback of government incentives related to investments;

• Inherent limitations of internal controls impacting financial statements and safeguarding of assets;

• Cybersecurity risks to operational systems, security systems, or infrastructure owned by Ford, Ford Credit, or a third-party vendor or supplier;

• Failure of financial institutions to fulfill commitments under committed credit and liquidity facilities;

• Inability of Ford Credit to access debt, securitization, or derivative markets around the world at competitive rates or in sufficient amounts, due to credit rating downgrades, market volatility, market disruption, regulatory

requirements, or other factors;

• Higher-than-expected credit losses, lower-than-anticipated residual values, or higher-than-expected return volumes for leased vehicles;

• Increased competition from banks, financial institutions, or other third parties seeking to increase their share of financing Ford vehicles; and

• New or increased credit, consumer, or data protection or other regulations resulting in higher costs and / or additional financing restrictions.

We cannot be certain that any expectation, forecast, or assumption made in preparing forward-looking statements will prove accurate, or that any projection will be realized. It is to be expected that there may be differences between

projected and actual results. Our forward-looking statements speak only as of the date of their initial issuance, and we do not undertake any obligation to update or revise publicly any forward-looking statement, whether as a result

of new information, future events, or otherwise. For additional discussion, see "Item 1A. Risk Factors" in our Annual Report on Form 10-K for the year ended December 31, 2014, as updated by subsequent Quarterly Reports on

Form 10-Q and Current Reports on Form 8-K.

APPENDIX

Item Appendix

2015 Planning Assumptions and Key Metrics 1

Return on Invested Capital Methodology 2

Return on Invested Capital Calculations (Ford and Competitors) 3 - 8

PENSION AND OPEB UPDATE

APPENDIX INDEX

2015 PLANNING ASSUMPTIONS AND KEY METRICS

* After Pension / OPEB revision announced on January 7, 2016; see materials on Ford’s Investor Relations website for details** Compared with 2014

*** Excludes special items

2014 FYResults* Prior Updated*

Planning Assumptions (Mils)

Industry Volume

- U.S. 16.8 About 17.7

- Europe 20 14.6 About 16.0

- China 24.0 About 24.0

Key Metrics

Automotive:

- Revenue (Bils) 135.8$ Higher**

- Operating Margin*** 4.6 Higher**

- Operating-Related Cash Flow (Bils)*** 3.6$ Higher**

Ford Credit (Compared with 2014):

- Pre-Tax Profit (Bils) 1.9$ Equal To Or Higher**

Total Company:

- Pre-Tax Profit (Bils)*** 7.3$ $8.5 - $9.5 $10.0 - $11.0

2015 FY Outlook

%

APPENDIX 1

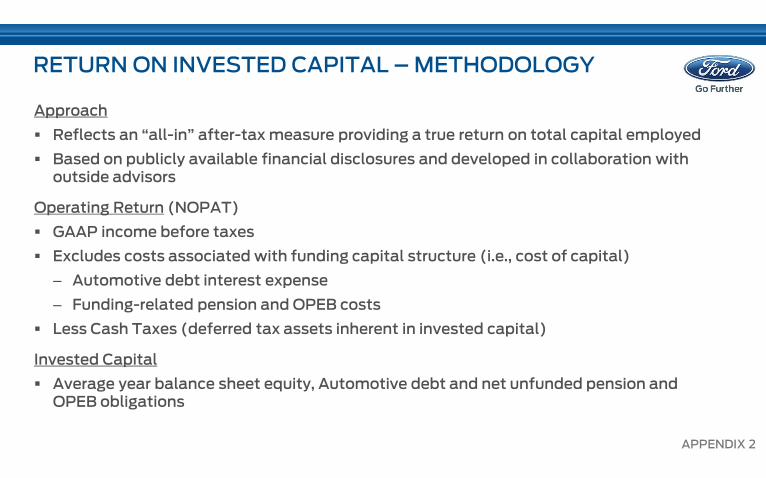

RETURN ON INVESTED CAPITAL – METHODOLOGY

APPENDIX 2

Approach

� Reflects an “all-in” after-tax measure providing a true return on total capital employed

� Based on publicly available financial disclosures and developed in collaboration with outside advisors

Operating Return (NOPAT)

� GAAP income before taxes

� Excludes costs associated with funding capital structure (i.e., cost of capital)

– Automotive debt interest expense

– Funding-related pension and OPEB costs

� Less Cash Taxes (deferred tax assets inherent in invested capital)

Invested Capital

� Average year balance sheet equity, Automotive debt and net unfunded pension and OPEB obligations

FORD – RETURN ON INVESTED CAPITAL CALCULATION

APPENDIX 3

2010 2011 2012 2013 2014

Net Operating Profit After Tax (NOPAT) (Bils.) (Bils.) (Bils.) (Bils.) (Bils.)

Pre-Tax Profit (Incl. Special Items) 7.1$ 3.7$ 2.0$ 14.4$ 1.2$

Add Back: Costs Related to Invested Capital

Automotive Interest Expense 1.8 0.8 0.7 0.8 0.8

Funding-Related Pension and OPEB Costs* (0.2) 5.2 6.2 (6.1) 3.4

Less: Cash Taxes (0.1) (0.3) (0.3) (0.5) (0.5)

Net Operating Profit After Tax 8.6$ 9.4$ 8.6$ 8.6$ 5.0$

Invested Capital

Equity (1.0)$ 14.9$ 15.9$ 26.2$ 24.5$

Redeemable Non-Controlling Interest - - 0.3 0.3 0.3

Automotive Debt 19.1 13.1 14.3 15.7 13.8

Net Pension and OPEB Liability 17.9 22.0 25.5 14.9 16.2

Invested Capital (End of Year) 36.0$ 50.0$ 56.0$ 57.0$ 54.8$

Average Year Invested Capital 40.1$ 43.2$ 53.1$ 56.5$ 55.7$

Annual ROIC 21.5% 21.7% 16.2% 15.2% 8.9%

Five-Year Average ROIC** (5.0)% 3.0% 7.3% 17.4% 16.2%

* Reflects total pension & OPEB (income) / expense except service cost

** Calculated as five-year average NOPAT divided by five-year average invested capital

Note: Totals may not foot due to rounding

BMW – RETURN ON INVESTED CAPITAL CALCULATION

APPENDIX 4Source: BMW Group Annual Reports

2010 2011 2012 2013 2014

Net Operating Profit After Tax (NOPAT) (Bils.) (Bils.) (Bils.) (Bils.) (Bils.)

Pre-Tax Profit (Incl. Special Items) 4.9€ 7.4€ 7.8€ 7.9€ 8.7€

Add Back: Costs Related to Invested Capital

Interest Expense 0.3 0.2 0.2 0.3 0.3

Funding-Related Pension and OPEB Costs* 0.1 0.1 0.1 0.1 0.1

Less: Cash Taxes (1.3) (2.7) (2.5) (2.8) (4.3)

Expense in Lieu of Amortization of Development Costs** 0.3 0.2 0.0 (0.7) (0.4)

Net Operating Profit After Tax 4.2€ 5.3€ 5.7€ 4.8€ 4.4€

Invested Capital

Equity 23.9€ 27.1€ 30.6€ 35.6€ 37.4€

Less: Capitalized Development Assets** (4.6) (4.4) (4.3) (5.0) (5.5)

Automotive Financial Liabilities 2.1 3.3 3.1 2.3 5.2

Net Pension and OPEB Liability 1.6 2.2 3.8 2.3 4.6

Invested Capital (End of Year) 23.0€ 28.2€ 33.1€ 35.2€ 41.8€

Average Year Invested Capital 23.0€ 25.6€ 30.7€ 34.2€ 38.5€

Annual ROIC 18.2% 20.6% 18.5% 14.2% 11.5%

Five-Year Average ROIC*** 10.1% 11.4% 12.7% 15.1% 16.1%

* Reflects total pension & OPEB (income) / expense except service cost

** Elimination of development cost capitalization effects from IFRS reporting

*** Calculated as five-year average NOPAT divided by five-year average invested capital

Note: Totals may not foot due to rounding

2010 2011 2012 2013 2014

Net Operating Profit After Tax (NOPAT) (Bils.) (Bils.) (Bils.) (Bils.) (Bils.)

Pre-Tax Profit (Incl. Special Items) 0.7€ 1.9€ 1.5€ 1.0€ 1.2€

Add Back: Costs Related to Invested Capital

Interest Expense 1.0 1.6 2.0 1.9 1.9

Funding-Related Pension and OPEB Costs** 0.0 (0.1) 0.4 0.2 0.4

Less: Cash Taxes (0.7) (0.5) (0.5) (0.4) (0.5)

Expense in Lieu of Amortization of Development Costs*** (0.5) (0.8) (1.5) (1.2) (1.2)

Net Operating Profit After Tax 0.5€ 2.1€ 1.9€ 1.6€ 1.7€

Invested Capital

Equity 12.5€ 9.7€ 8.4€ 12.6€ 13.7€

Less: Capitalized Development Assets*** (2.9) (3.5) (4.9) (5.7) (7.1)

Automotive Debt 19.8 24.8 25.9 28.3 31.7

Net Pension and OPEB Liability 1.1 8.2 10.2 7.1 8.4

Invested Capital (End of Year) 30.5€ 39.2€ 39.6€ 42.3€ 46.8€

Average Year Invested Capital 30.9€ 34.9€ 39.4€ 40.9€ 44.5€

Annual ROIC 1.7% 6.0% 4.9% 3.9% 3.9%

Cumulative Average ROIC (since 2009)**** 1.7% 4.0% 4.3% 4.2% 4.1%

* Fiat Group consolidated Chrysler results effective June 2011

** Reflects total pension & OPEB (income) / expense except service cost

*** Elimination of development cost capitalization effects from IFRS reporting

**** Calculated as average NOPAT since 2009 divided by average invested capital since 2009

Note: Totals may not foot due to rounding

FCA – RETURN ON INVESTED CAPITAL CALCULATION*

APPENDIX 5Source: Fiat Group / FCA Annual Reports

GM – RETURN ON INVESTED CAPITAL CALCULATION

APPENDIX 6Source: GM 10-K Filings

2010 2011 2012 2013 2014

Net Operating Profit After Tax (NOPAT) (Bils.) (Bils.) (Bils.) (Bils.) (Bils.)

Pre-Tax Profit (Incl. Special Items) 7.2$ 9.2$ (28.7)$ 7.5$ 4.2$

Add Back: Costs Related to Invested Capital

Automotive Interest Expense 1.1 0.5 0.5 0.3 0.4

Funding-Related Pension and OPEB Costs* (0.6) (1.9) 2.2 (0.2) (0.4)

Less: Cash Taxes (0.4) (0.6) (0.6) (0.7) (0.9)

Net Operating Profit After Tax 7.3$ 7.3$ (26.6)$ 6.8$ 3.3$

Invested Capital

Equity 37.2$ 39.0$ 37.0$ 43.2$ 36.0$

Automotive Debt 4.6 5.3 5.2 7.1 9.4

Net Pension and OPEB Liability 32.2 32.7 35.6 26.2 30.8

Invested Capital (End of Year) 74.0$ 77.0$ 77.8$ 76.5$ 76.2$

Average Year Invested Capital 77.8$ 75.5$ 77.4$ 77.1$ 76.4$

Annual ROIC 9.4% 9.7% (34.4)% 8.9% 4.4%

Cumulative Average ROIC (since 2009)** 9.4% 9.5% (5.2)% (1.7)% (0.5)%

* Reflects total pension & OPEB (income) / expense except service cost

** Calculated as average NOPAT since 2009 divided by average invested capital since 2009

Note: Totals may not foot due to rounding

TOYOTA – RETURN ON INVESTED CAPITAL CALCULATION*

APPENDIX 7Source: Toyota 20-F Filings

2010 2011 2012 2013 2014

Net Operating Profit After Tax (NOPAT) (Bils.) (Bils.) (Bils.) (Bils.) (Bils.)

Pre-Tax Profit** (Incl. Special Items) 778¥ 631¥ 1,635¥ 2,759¥ 3,201¥

Add Back: Costs Related to Invested Capital

Interest Expense 29 23 23 20 23

Funding-Related Pension and OPEB Costs*** 4 24 18 8 (6)

Less: Cash Taxes (211) (282) (331) (411) (1,146)

Net Operating Profit After Tax 600¥ 395¥ 1,346¥ 2,376¥ 2,072¥

Invested Capital

Equity 10,920¥ 11,066¥ 12,773¥ 15,219¥ 17,647¥

Automotive Debt 1,562 1,558 1,284 1,246 1,249

Net Pension and OPEB Liability 546 677 658 538 537

Invested Capital (End of Year) 13,028¥ 13,301¥ 14,715¥ 17,002¥ 19,433¥

Average Year Invested Capital 13,233¥ 13,164¥ 14,008¥ 15,858¥ 18,218¥

Annual ROIC 4.5% 3.0% 9.6% 15.0% 11.4%

Five-Year Average ROIC**** 5.7% 3.6% 2.8% 7.7% 9.1%

* Reflects fiscal year (April 1 of noted year through March 31 of following year)

** Includes equity earnings reported after income before income taxes

*** Reflects total pension & OPEB (income) / expense except service cost

**** Calculated as five-year average NOPAT divided by five-year average invested capital

Note: Totals may not foot due to rounding

VW – RETURN ON INVESTED CAPITAL CALCULATION

APPENDIX 8Source: VW Group Annual Reports

2010 2011 2012 2013 2014

Net Operating Profit After Tax (NOPAT) (Bils.) (Bils.) (Bils.) (Bils.) (Bils.)

Pre-Tax Profit (Incl. Special Items) 9.0€ 18.9€ 25.5€ 12.4€ 14.8€

Add Back: Costs Related to Invested Capital

Interest Expense 1.2 1.1 1.4 1.5 1.5

Funding-Related Pension and OPEB Costs* 0.7 0.7 0.8 0.8 0.8

Less: Cash Taxes (1.6) (3.3) (5.1) (3.1) (4.0)

Expense in Lieu of Amortization of Development Costs** (0.1) (0.2) (0.7) (1.6) (1.7)

Net Operating Profit After Tax 9.2€ 17.3€ 21.9€ 9.9€ 11.4€

Invested Capital

Equity 48.7€ 63.4€ 82.0€ 90.0€ 90.2€

Less: Capitalized Development Assets** (7.7) (9.9) (12.9) (14.2) (15.7)

Automotive Financial Liabilities 5.8 4.7 12.5 11.9 9.8

Net Pension and OPEB Liability 15.4 16.7 23.9 21.7 29.7

Invested Capital (End of Year) 62.2€ 74.9€ 105.6€ 109.5€ 114.0€

Average Year Invested Capital 58.4€ 68.5€ 90.2€ 107.5€ 111.7€

Annual ROIC 15.8% 25.3% 24.3% 9.3% 10.2%

Five-Year Average ROIC*** 11.0% 15.5% 17.9% 16.1% 16.0%

* Reflects total pension & OPEB (income) / expense except service cost

** Elimination of development cost capitalization effects from IFRS reporting

*** Calculated as five-year average NOPAT divided by five-year average invested capital

Note: Totals may not foot due to rounding