maponya mall shopper profilepage 5 shopper media consumption lifestyle statements: shopping sa...

TRANSCRIPT

Shopper profile

Page 1

Contents

The value of the data 1Mall demographic profile 2Shopper media consumption 4

The following data has been collected and verified by Ask Afrika Group, the copyright license holder for Target Group Index (TGI).

Ask Afrika Group is the largest independent South African market research company with fieldwork capabilities in 95% of Sub-Saharan Africa. They are backed by the power of TGI Research, the only SA population database with psychographics that cover over 600 lifestyle and attitude statements.

TGI is South Africa’s broadest consumer/shopper profiling tool in sampling 24 000 nationally representative respondents aged 15+, living in communities 8 000+. Insights are tailor-suited for malls, which link demographic, psychographic, brand and media insights. TGI supports strategic and informed decision making.

The value of the data

Sample size: 620 Weighted to SA shopper: 438 000

RET

AIL

Page 2

65+

45-64

35-44

25-34

15-24

Motivated Experiencers Independents Utopians Virtuous Materialists IndifferentTraditionalists Comfort zone dwellers

Black

White

Coloured

Indian/ Asian

SA shopper

Mall demographic profile

Age Race

Most important media used*

Life values

6.8%7.1%

90%

31.1% 4%

20.3% 4.8%

24.6% 1.2%

17.3%

73.1%

23.2% 10.6%

12.2%22.5%

29.1% 4.2%

18%

Gender

48.9%

49.8%

51.1%

50.2%

LSM

4 5 6 7 8 9 10

3.1%

7% 41.5

%

24.7

% 6.9%

13% 3.

7%

2.3%

10.2

%13

.3%

9%

7.6%

13.4

%

36.4

%

9.3%

8.8%

25.6

%

9.9%

8.4%

10.2

%

20.8

%14

.6%

12.7

%8.

7%

8.5%

11.3

%

12.6

%

14.1

%12

.7%

3.9%

7% 8.9%

SA shopper vs Maponya Mall shopper

1.3%

3.6%

MagazinesInternet(Desktop)

Internet(Mobile)

Outdoor (Billboards and posters)

In-store

46.6%

42.8%

TVNewspapers

5.6%

7.9%

15.9%

14.4%

Radio

3.3%

3.7%

21.5%

20.6%

Cinema

0.6%

0.6%

*Based on those that have visited a mall in the past three months/*2018C TGI Data.

3%

5.2%

3.5%

2.3%

RET

AIL

Page 3

Marital status Life stages Income

5.6%6.6%

5%5.9%

3%3.4%3.6%4.9%

35.9%29%

1.3%2.4%

3.1%2.4%

32.4%35%

English Afrikaans Any Sotho Language

Sepedi Sesotho Xitsonga Setswana Tshivenda Any Nguni Language

Siswati IsiZuluIsindebele IsiXhosa Hindi/ Urdu

Language

8.7% 15

.7%

5.9% 14

.3%

7.3%

6.1%

38%

28% 4.

9%3.

1%

14.2

%11

.1%

0.4%

1%

7.8% 14

%

0.2% 1.7%

43.2

%40

.3%

0% 0.2%

34.8

%23

.8%

3.3%

1.1%

11.7

%7.

6%

9.4%

12.5%

0%

5%

11.3%

5.7%

13.8%

0%

5%

37.4%

5.1%

9.1%

3.1%

1.7%

9.6%

5.1%

2.7%

2%

5.9%

33.6%

37.3%42.3%27.7%31.3%

9.6%11%

8.6%5.7%

49.1%47%

4.3%2.7%

5%5.1%

4.3%3.01%

Married/ living together

as partners

Married

Living together as partners

Single - divorced/

separated

Single - divorced

Single - separated

Single - never married

Single - widowed

Dependent singles

Breaking out

Settled singles

Nest builders

Play school/ pre-teen/

teen parents

Single parents

Empty nesters

All alone

SA shopper vs Maponya Mall shopper

Up to R999

R1 000 - R1 999

R2 000 - R2 499

R2 500 - R2 999

R3 000 - R5 999

R6 000 - R9 999

R10 000 - R13 999

R14 000 - R17 999

R18 000 +

Refused to share

SA shopper

Mall demographic profile RET

AIL

Page 4

Most important factors when shopping Do they look out for sales promotions?

Shopper media consumption

SA shopper vs Maponya Mall shopper

Yes, always

Yes, sometimes

42.4%

39%

33%

36.5%

Yes, occasionally

Never

11.4%

10.8%

13.3%

12.9%

Type of in-store advertising noticed

On-shelf

Aisle-end advertising

Floor advertising

Trolley advertising

Poster advertising

60.5%

51.8%

36.4%

34.3%

37.3%

36.1%

33.9%

35.6%

37.1%

26.8%

Do they ever notice in-store advertising?

81%

82.1%

19%

17.9%

Maponya Mall (%) SA shopper (%)

01 Advertising 4.4 4.4

02 Availability 6.3 6.4

03 Comfort 6.5 9.1

04 Consumer or user reviews 2.7 1.2

05 Durability 4.9 3.8

06 Ease of care/ease to care for 1.2 1.7

07 Fashion 5.2 3.7

08 Friends/family recommendations 1.1 1.9

09 Material/fabric 0.9 1.9

10 Origin (ethically produced, country of manufacturer) 1.4 0.8

11 Price 23.2 27.4

12 Professional recommendations 1.2 1

13 Promotions 5.3 3.9

14 Quality 28.1 22.8

15 Store layout 1.5 1.2

16 The item is on sale 2.9 2.3

17 The manufacturer’s brand 2.1 1

18 Versatility 0.8 1.1

SA shopper

RET

AIL

Page 5

Shopper media consumption

Lifestyle statements: shopping

SA shopper vs Maponya Mall shopper

01. When I see a new brand I often buy it to see what it’s like

02. When doing household shopping I budget for every cent

03. I always look out for special offers

04. I always buy brands my domestic prefers

05. It’s worth paying more for organic food

06. I really enjoy any kind of shopping

07. Once I find a brand I like, I tend to stick to it

08. I only shop at supermarkets that sell good quality fresh food

09. I’m tempted to buy products I’ve seen advertised

10. When buying toiletries the brand I choose is very important to me

11. I tend to buy the cheapest household cleaning products

12. I often try new household cleaning products

13. I feel reassured using products recommended by an expert

14. I ask people’s advice before buying new things

15. Store ambience is important in my selection of a fast food/quick service restaurant or outlet

16. I am prepared to pay a higher price for a meal offering when eating out/ordering a take-away meal, as long as the quality is good

17. Home/office delivery is important to me in deciding which fast food/ quick service outlet to use

18. My children decide where to go for take away food

19. People come to me for advice before buying new things

20. I expect quick and efficient service when going out for a quick meal

21. I always buy brands my children prefer

22. I usually only go shopping when I have something I really need

23. I tend to hold out on buying things I want until they go on sale

24. I generally do my bulk and top-up shopping at different food retailers

25. The location of stores will determine whether or not I shop there

26. I am open to using a smartphone application to scan and pay for items I am purchasing in-store/online

27. Celebrities influence my purchase decisions

28. Even though I have a favourite brand, if another brand is on special offer I buy it instead

29. I prefer to buy local brands when I can

01 05 0902 06 1003 07 1104 08 12 13 14 15

16

28.9

%32

.4%

13.1

%7.

3%

22

21.5

% 11.4

%

13.4

%9.

2%

18

8.4%

8.4%

18.2

%10

.7%

24

15.8

%9.

5%

14.7

%12

.1%

16%

20%

20

30.1

%22

.7%

15.9

%14

.3%

26

11.2

%19

.4%

24%

22.6

%

17

27.3

%20

.4%

12.5

%10

.2%

23

13.7

%8.

5%

22.7

% 11.5

%

29

21% 11

%

9.3%

8.2%

19

10%

7%

22%

16.6

%

25

18% 10

.3%

34.2

%26

.6%

2131

.8%

22.7

%

12.3

%8.

3%27

10.5

%11

.1%

22.2

%21

.4%

28

30%

26.6

%

17%

19.4

%

SA shopper

RET

AIL

Page 6

SA shopper vs Maponya Mall shopper

Newspapers

Magazines

TV

Internet

Outdoor

Cinema

Radio

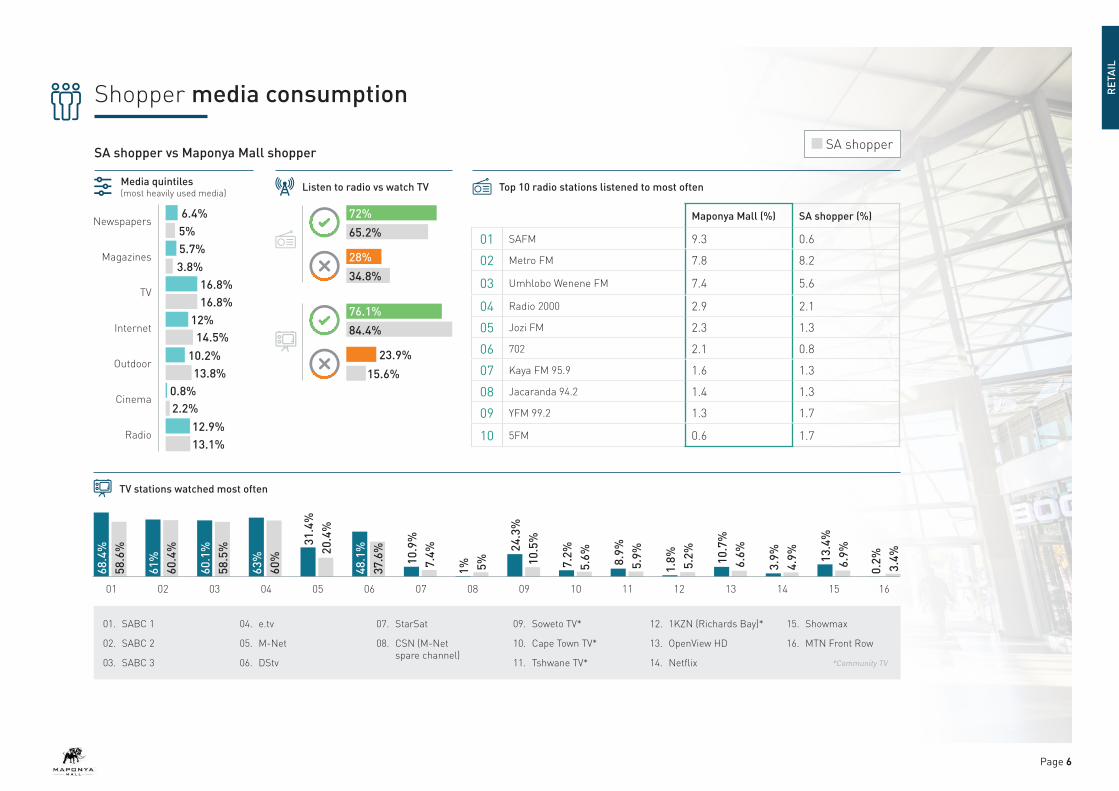

Media quintiles (most heavily used media)

TV stations watched most often

6.4%

5.7%

16.8%

12%

0.8%

10.2%

12.9%

5%

3.8%

16.8%

14.5%

2.2%

13.8%

13.1%

Top 10 radio stations listened to most oftenListen to radio vs watch TV

72%

76.1%

65.2%

84.4%

28%

23.9%

34.8%

15.6%

68.4

%58

.6%

60.1

%58

.5% 31

.4%

20.4

%

61%

60.4

%

63%

60%

48.1

%37

.6%

10.9

%7.

4%

1% 5%

24.3

%10

.5%

8.9%

5.9% 10

.7%

6.6%

7.2%

5.6%

1.8% 5.2%

3.9%

4.9% 13

.4%

6.9%

0.2%

3.4%

01. SABC 1

02. SABC 2

03. SABC 3

04. e.tv

05. M-Net

06. DStv

07. StarSat

08. CSN (M-Net spare channel)

09. Soweto TV*

10. Cape Town TV*

11. Tshwane TV*

12. 1KZN (Richards Bay)*

13. OpenView HD

14. Netflix

15. Showmax

16. MTN Front Row

*Community TV

01 05 0902 06 1003 07 1104 08 12 13 14 15 16

Shopper media consumption

SA shopper

Maponya Mall (%) SA shopper (%)

01 SAFM 9.3 0.6

02 Metro FM 7.8 8.2

03 Umhlobo Wenene FM 7.4 5.6

04 Radio 2000 2.9 2.1

05 Jozi FM 2.3 1.3

06 702 2.1 0.8

07 Kaya FM 95.9 1.6 1.3

08 Jacaranda 94.2 1.4 1.3

09 YFM 99.2 1.3 1.7

10 5FM 0.6 1.7

RET

AIL

Page 7

SA shopper vs Maponya Mall shopper

Internet frequency: desktop (%)

Internet usage: desktop (%)

Internet frequency: mobile (%)

Internet usage: mobile (%)

Maponya Mall (%) SA shopper (%)

Several times a day 4.9 5.7

Once a day 6.4 5.9

Three to five times a week 4.6 4.6

Once or twice a week 2.7 2.6

Two or three times a month 0.2 1.6

Once a month 0.5 0.7

Less often 4.8 4.2

Maponya Mall (%) SA shopper (%)

Communication 22.9 26.4

Information 7.3 10

Shopping, retail and finance 4.6 3.8

Entertainment 7.7 6.3

Downloads 7.3 5.8

Apps 0.1 0.2

Other activities 5.9 5.2

Maponya Mall (%) SA shopper (%)

Several times a day 6.9 13.4

Once a day 7.4 7.5

Three to five times a week 5.2 6

Once or twice a week 5.6 3.9

Two or three times a month 1.9 1.5

Once a month 0 0.4

Less often 3.5 3.8

Maponya Mall (%) SA shopper (%)

Communication 26.4 33.9

Information 9.8 12.5

Shopping, retail and finance 5.9 4.5

Entertainment 7.6 8

Downloads 6.7 6.8

Apps 1.1 0.3

Other activities 5.9 5.3

Shopper media consumption

SA shopper

RET

AIL