managing cash flow

DESCRIPTION

CHAPTER 12. Managing Cash Flow. The Importance of Cash. “Everything is about cash – raising it, conserving it, collecting it.” Guy Kawasaki. Common cause of business failure: Cash crisis!. Cash Management. - PowerPoint PPT PresentationTRANSCRIPT

Copyright © 2011 Pearson Education

CHAPTER CHAPTER 1212

Copyright © 2011 Pearson Education

“Everything is about cash – raising it, conserving it, collecting it.”

Guy Kawasaki

Ch. 12: Managing Cash Flow12 - 2

Common cause of business failure: Common cause of business failure:

Cash crisis!Cash crisis!

Copyright © 2011 Pearson Education

A business can be earning a profit and be forced to close because it runs out of cash!

American Express OPEN Small Business Monitor study: ◦ 59% of small business owners

experience problems with cash flow.

◦ Their biggest cash flow concern is the ability to pay bills on time.

Ch. 12: Managing Cash Flow12 - 3

Copyright © 2011 Pearson Education

Ch. 6: Franchising and the Entrepreneur

6 - 4

FIGURE 12.1 Small Business Owners’ Strategies for Improving Cash Flow Source: American Express OPEN Small Business Monitor, 2008.

Copyright © 2011 Pearson Education

Cash management – forecasting, collecting, disbursing, investing, and planning for the cash a company needs to operate smoothly.

Young and growing companies are “cash sponges.”

Know your company’s cash flow cycle.

Ch. 12: Managing Cash Flow12 - 5

Copyright © 2011 Pearson Education

12 - 6Ch. 12: Managing Cash Flow

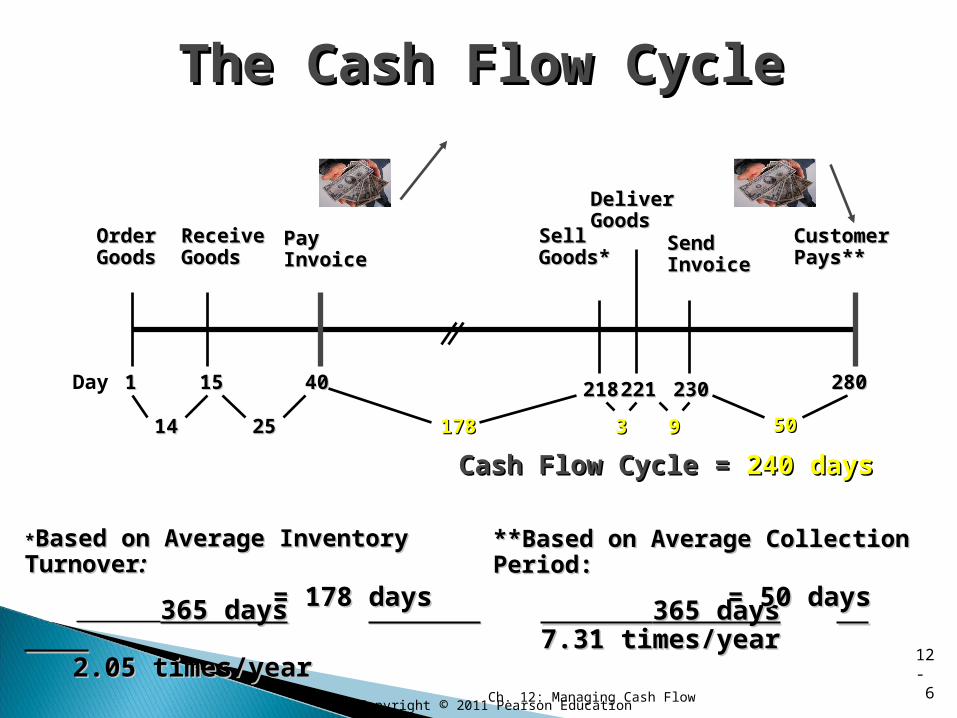

The Cash Flow CycleThe Cash Flow Cycle

OrderOrderGoodsGoods

Day 11

ReceiveReceiveGoodsGoods

1515

PayPayInvoiceInvoice

4040

1414 2525

218218

178178

SellSellGoods*Goods*

DeliverDeliverGoodsGoods

221221

33

CustomerCustomerPays**Pays**

SendSendInvoiceInvoice

230230

99

280280

5050

Cash Flow Cycle = Cash Flow Cycle = 240 days240 days

**Based on Average Inventory TurnoverBased on Average Inventory Turnover::

365 days365 days 2.05 times/year2.05 times/year

**Based on Average Collection Period:**Based on Average Collection Period:

365 days365 days 7.31 times/year7.31 times/year

= 178 days= 178 days

FIGURE 12.2

= 50 days= 50 days

Copyright © 2011 Pearson Education

1. Cash Finder

2. Cash Planner

3. Cash Distributor

4. Cash Collector

5. Cash Conserver

12 - 7Ch. 12: Managing Cash Flow

Copyright © 2011 Pearson Education

Cash ≠ profits.Cash ≠ profits. Profit is the difference between a Profit is the difference between a

company’s total revenue and total company’s total revenue and total expenses.expenses.

Cash is the money that is free and readily Cash is the money that is free and readily available to use.available to use.

Cash flow measure a company’s liquidity Cash flow measure a company’s liquidity and its ability to pay it bills.and its ability to pay it bills.

Ch. 12: Managing Cash Flow12 - 8

Copyright © 2011 Pearson EducationCh. 12: Managing Cash Flow

12 - 9

Cash

Accounts Payable

Decrease in CashDecrease in Cash

Production/Cash Purchases

Inventory

Accounts Receivable

Cash Sales

Increase in CashIncrease in Cash

LeakageLeakage

LeakageLeakageFIGURE 12.3

Copyright © 2011 Pearson Education

A “cash map” that shows the amount and the timing of a firm's cash receipts and cash disbursements over time.

Predicts the amount of cash a company will need to operate smoothly.

Helps to visualize a company’s cash receipts and cash disbursements and the resulting cash balance.

Ch. 12: Managing Cash Flow

12 -

10

Copyright © 2011 Pearson Education

Remember Goldilocks, the Three Bears, and the porridge:

◦Not too much...◦Not too little...◦But a cash balance that's just right ... for you!

Ch. 12: Managing Cash Flow

12 -

11

Determine a Determine a Minimum Cash BalanceMinimum Cash Balance

Copyright © 2011 Pearson Education

1. Determine a Minimum Cash Balance

2. Forecast Sales

Ch. 12: Managing Cash Flow

12 -

12

(continued)

Copyright © 2011 Pearson Education

The heart of the cash budget.

Sales are ultimately transformed into cash receipts and cash disbursements.

Cash forecast is only as accurate as the sales forecast from which it is derived.

Ch. 12: Managing Cash Flow

12 -

13

Copyright © 2011 Pearson Education

“Lumpy” or seasonal sales patterns are common.

◦ 15% to 18% of wine and spirits shops’ annual sales occur between December 15 and 31.

◦ 40% of toy sales take place in last 6 weeks of the year.

Ch. 12: Managing Cash Flow

12 -

14

(continued)

Copyright © 2011 Pearson Education

Prepare three sales forecasts:

Pessimistic

Optimistic

Most Likely

Ch. 12: Managing Cash Flow

12 -

15

Copyright © 2011 Pearson Education

Example:

Number of cars in trading zone 84,000 x Percent of imports x 24% = Number of imported cars in trading zone 20,160

Number of imports in trading zone 20,160 x Average expenditure on repairs x $485 = Total import repair sales potential $9,777,600

Total import repair sales potential $9,777,600 x Estimated market share x 9.9% = Sales estimate $967,982

Ch. 12: Managing Cash Flow

12 -

16

Copyright © 2011 Pearson Education

1. Determine a Minimum Cash Balance

2. Forecast Sales

3. Forecast Cash Receipts

Ch. 12: Managing Cash Flow

12 -

17

(continued)

Copyright © 2011 Pearson Education

Record all cash receipts when the cash is actually received (i.e. the cash method of accounting).

Determine the collection pattern for credit sales; then add cash sales.

Monitor closely: Slow and non-payers.

Ch. 12: Managing Cash Flow

12 -

18

Copyright © 2011 Pearson EducationCh. 12: Managing Cash Flow

12 -

19

13.60%

23.60%

42.80%

57.80%

73.60%

85.20%

93.80%

0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

24

12

9

6

3

2

1

Probability of Collection

Nu

mb

er o

f Mo

nth

s D

elin

qu

ent

Collecting Delinquent Collecting Delinquent AccountsAccounts

Copyright © 2011 Pearson Education

1. Determine a Minimum Cash Balance

2. Forecast Sales

3. Forecast Cash Receipts

4. Forecast Cash Disbursements

Ch. 12: Managing Cash Flow

12 -

20

(continued)

Copyright © 2011 Pearson Education

Record disbursements when you expect to make them.

Start with those disbursements that are fixed amounts due on certain dates.

Review the business checkbook to ensure accurate estimates.

Add a cushion to the estimate to account for “Murphy’s Law.”

Don’t know where to begin? Try making a daily list of the items that generate cash and those that consume it.

Ch. 12: Managing Cash Flow

12 -

21

Copyright © 2011 Pearson Education

1. Determine a Minimum Cash Balance

2. Forecast Sales

3. Forecast Cash Receipts

4. Forecast Cash Disbursements

5. Estimate End-of-Month Cash Balance

Ch. 12: Managing Cash Flow

12 -

22

(continued)

Copyright © 2011 Pearson Education

Take Beginning Cash Balance ... Add Cash Receipts ... Subtract Cash Disbursements Result is Cash Surplus

or Cash Shortage (Repay or Borrow?)

Ch. 12: Managing Cash Flow

12 -

23

Copyright © 2011 Pearson Education

Increase amount and speed of cash flowing into the company

Reduce the amount and speed of cash flowing out

Make the most efficient use of available cash

Take advantage of money-saving opportunities such as cash discounts

Finance seasonal business needs

Ch. 12: Managing Cash Flow

12 -

24

Copyright © 2011 Pearson Education

Develop a sound borrowing and repayment program

Impress lenders and investors Provide funds for expansion Plan for investing surplus cash

Ch. 12: Managing Cash Flow

12 -

25

(continued)

Copyright © 2011 Pearson Education

1. Accounts Receivable

2. Accounts Payable

3. Inventory

Ch. 12: Managing Cash Flow

12 -

26

Copyright © 2011 Pearson Education

About 90% of industrial and wholesale sales are on credit, and 40% of retail sales are on account.

Survey of small companies across a variety of industries found that 77% extend credit to their customers.

Remember: “A sale is not a sale until you collect the money.”

Accounts receivable goal: Collect your company’s cash as fast as you can.

Ch. 12: Managing Cash Flow

12 -

27

Copyright © 2011 Pearson EducationCh. 12: Managing Cash Flow

FIGURE 12.5 Cash Flow Concerns Source: Based on American Express Corporation, 2005.

12 -

28

Copyright © 2011 Pearson Education

Establish a firm credit-granting policy.◦ Screen credit customers carefully.

◦ Develop a system of collecting accounts.

◦ Send invoices promptly.

◦ When an account becomes overdue, take action immediately.

◦ Add finance charges to overdue accounts (check the law first!).

Ch. 12: Managing Cash Flow

12 -

29

Accounts ReceivableAccounts Receivable

Copyright © 2011 Pearson Education

Ensure that invoices are accurate and timely.

Include a description of the goods or services purchased.

Ensure that invoices match purchase orders or contracts.

Highlight the balance dues and due date.

Include contact information in case customers have questions.

Ch. 12: Managing Cash Flow

12 -

30

Copyright © 2011 Pearson Education

Stretch out payment times as long as possible without damaging your credit rating.

Verify all invoices before paying them. Take advantage of cash discounts.

Ch. 12: Managing Cash Flow

12 -

31

Accounts PayableAccounts Payable

Copyright © 2011 Pearson EducationCh. 12: Managing Cash Flow

12 -

32

DayDay

AmountAmount

00 1010 3030

$1,000$1,000$980$980

2020 daysdays

$20$20

R = R = IIP x TP x T

= $20$20$980 x 20/365$980 x 20/365

= 37.25%= 37.25%

FIGURE 12.6

Copyright © 2011 Pearson Education

Negotiate the best possible terms with your suppliers.

Be honest with creditors; avoid the “the check is in the mail” syndrome.

Schedule controllable cash disbursements to come due at different times.

Use credit cards wisely.

Ch. 12: Managing Cash Flow

12 -

33

Accounts PayableAccounts Payable

Copyright © 2011 Pearson Education

Monitor it closely; inventory can drain a company’s cash.

Avoid inventory “overbuying.” It ties up valuable cash at a zero rate of return.

Arrange for inventory deliveries at the latest possible date.

Negotiate quantity discounts with suppliers when possible.

Ch. 12: Managing Cash Flow

12 -

34

InventoryInventory

Copyright © 2011 Pearson Education

Consider bartering, exchanging goods and services for other goods and services, to conserve cash.

Trim overhead costs: ◦Ask for discounts and “freebies” ◦Periodically evaluate expenses◦Lease rather than buy◦Avoid nonessential cash outlays◦Negotiate fixed loan payments

to coincide with your company’s cash flow

Ch. 12: Managing Cash Flow

12 -

35

Copyright © 2011 Pearson Education

Trim overhead costs:◦Buy used equipment◦Hire part-time employees and freelancers◦Outsource nonessential activities◦Control employee advances and loans◦Establish an internal security and control

system◦Develop a system to battle check fraud◦Change shipping terms

Ch. 12: Managing Cash Flow

12 -

36

(continued)(continued)

Copyright © 2011 Pearson Education

Start selling gift cards Switch to zero-based budgeting Be on the lookout for employee theft Keep your business plan current Invest surplus cash

Ch. 12: Managing Cash Flow

12 -

37

(continued)(continued)

Copyright © 2011 Pearson Education

““Cash is King”Cash is King” Cash and profits are not the same.Cash and profits are not the same. Entrepreneurial success means Entrepreneurial success means

operating a company “lean and operating a company “lean and mean.”mean.”◦ Trim wasteful expenditures.Trim wasteful expenditures.◦ Invest surplus funds.Invest surplus funds.◦ Plan and manage cash flow.Plan and manage cash flow.

Ch. 12: Managing Cash Flow

12 -

38