macroeconomics monthly report - wirtualna polska filemonthly report february 2007 equity market the...

TRANSCRIPT

BRE Bank Securities

5 February 2007

Monthly Report BRE Bank Securities BRE Bank Securities

Periodic Report

Monthly Report February 2007

Equity market The macro-economic outlook for Poland is surprisingly positive. We do not see any threat of reversal in this uptrend in the next few months even given the inflated prices of Polish stocks. Company News Banks. The fourth-quarter earnings results will paint a rosy picture of the banking industry. High earnings expectations have been baked into the appreciating prices of bank stocks. That is why we are “retiring” our January ACCUMULATE ratings on Pekao, BPH, BZ WBK, and ING BSK. We will revise our forecasts after the fourth-quarter earnings reports. Telecommunications. TPSA’s stock price will probably be maintained at the current level by dividend payout and share buy-back. We recommend to use that strength to reduce holdings in TPSA before it starts to feel competi-tive pressure in Q1. Media. The excellent newspaper sales figures for December convinced us to stay bullish on Agora. Q4 results will probably confirm that the worst is already behind the company. IT. After a rally at the beginning of the year, most IT stocks have already exhausted their upside potential. We give REDUCE ratings on ComArch and Asseco Poland whose current prices more than price in the growth op-portunities that will present themselves in the years ahead. Smaller plays like Macrologic and Techmex still offer some upside. Metals We anticipate that the price of copper will stabilize at $5,000/T, and the downtrend will cease to impact KGHM. Now is a good time to take posi-tions in the stock. Construction. The fourth-quarter earnings of construction companies will disappoint despite favorable weather conditions due to growing costs. Moreover, given that market prices have exceeded our targets, we see a possibility of a correction in construction stocks in the coming month. Pharmaceuticals. According to IMS Health, drug sales in 2006 increased 4.2% relative to 2005. Based on this, we do not expect any surprises from the Q4 earnings results of pharmaceutical distributors, and predict that they will have a neutral impact on stock performance. Retail. Eurocash and Eldorado are set to release their Q4’06 earnings re-ports at the beginning of March. We expect good performance, especially from Eldorado. However, the current prices of both stocks already factor in the high expectations, and, since they have exceeded our price targets, we are downgrading our ratings on them. Ratings. We are downgrading our investment ratings for the following stocks at the time of this Monthly Report: BPH (Hold), Budimex (Reduce), BZ WBK (Reduce), ComArch (Reduce), ComputerLand (Hold), Eldorado (Reduce), Elektrobudowa (Hold), Eurocash (Sell), Hydrobudowa Śląsk (Reduce), ING BSK (Hold), Macrologic (Accumulate), Millennium (Reduce), Pekao (Hold), Polimex Mostostal (Reduce), Prokom Software (Hold), Tech-mex (Accumulate). We are suspending our rating on PGNiG.

BRE Bank Securities does not rule out offering brokerage services to an issuer of securities being the subject of a recommendation. Information concerning a conflict of interest arising in connection with issuing a recommendation (should such a conflict exist) is located on the final page of this report.

Analysts:

Marta Jeżewska (+48 22) 697 47 37 marta.jeż[email protected]

Michał Marczak (+48 22) 697 47 38 [email protected]

Andrzej Lis (+48 22) 697 47 42 [email protected]

Krzysztof Radojewski (+48 22) 697 47 01 [email protected]

Kamil Kliszcz (+48 22) 697 47 06 [email protected]

Macroeconomic Analyst Janusz Jankowiak

5 February 2007

WIG vs. indices in the region

BRE Bank Securities

Equity Market Macroeconomics

Avg daily trading volume (3M)

Average 2008 P/E

Average 2007 P/E

WIG 55 314 19.4

16.6

PLN 1462m

27000

32000

37000

42000

47000

52000

57000

06-01-30 06-05-28 06-09-23 07-01-19

pkt

WIG BUX PX50

BRE Bank Securities

5 February 2007 2

Monthly Report BRE Bank Securities

Table of Contents 1. Equity market ........................................................................................ 3 2. Fund flows ............................................................................................. 4 3. Current recommendations of BRE Bank Securities S.A. ....................... 6 4. Recommendation statistics ................................................................... 7 5. Macroeconomics ................................................................................... 8 6. Financial Sector ..................................................................................... 9

6.1. BPH ........................................................................................... 13 6.2. BZ WBK ..................................................................................... 15 6.3. Handlowy ................................................................................... 16 6.4. ING BSK .................................................................................... 17 6.5. Kredyt Bank ............................................................................... 18 6.6. Millennium ................................................................................. 19 6.7. Pekao SA .................................................................................. 21 6.8. PKO BP ..................................................................................... 22

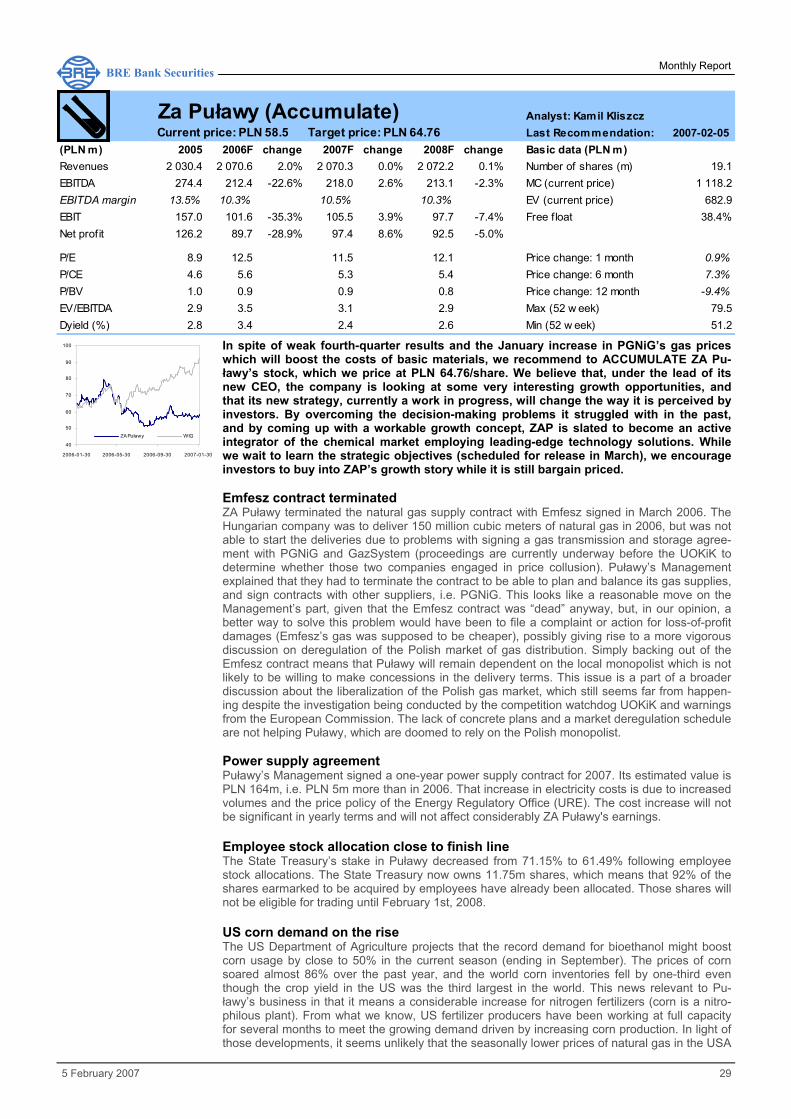

7. Gas & Oil, Chemicals ............................................................................. 24 7.1. Lotos .......................................................................................... 25 7.2. PGNiG ....................................................................................... 26 7.3. PKN Orlen ................................................................................. 27 7.4. ZA Puławy ................................................................................. 29

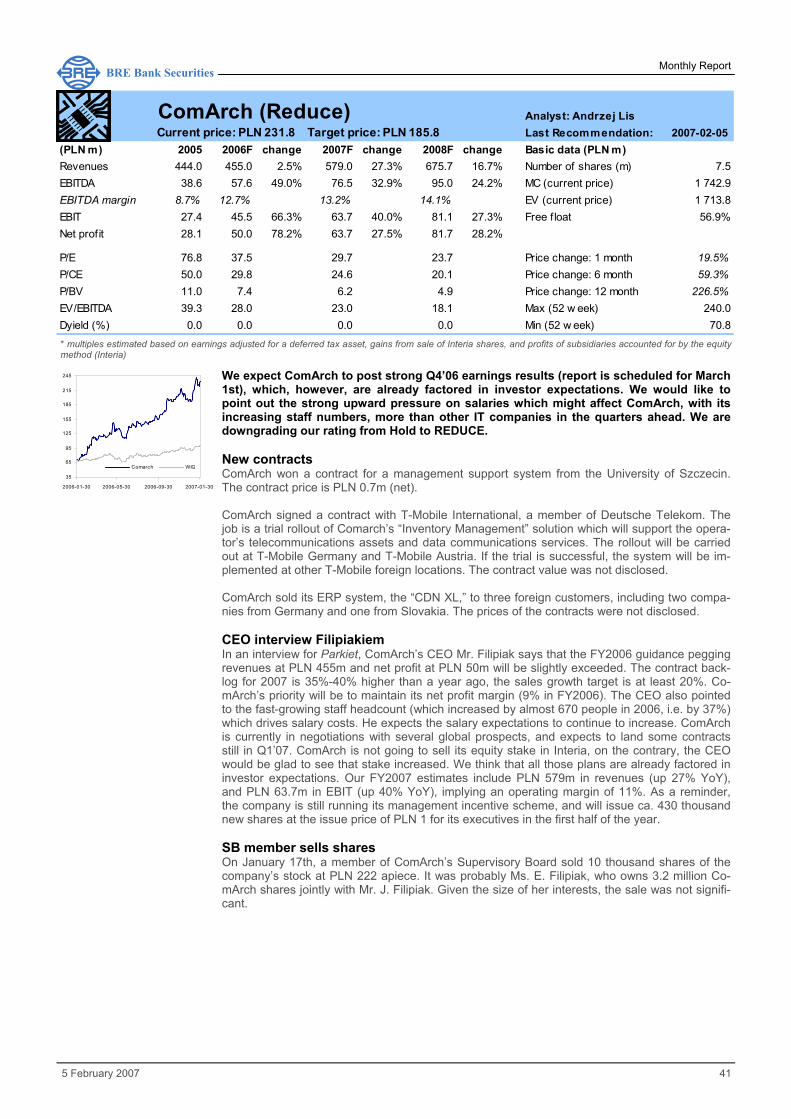

8. Telecommunications .............................................................................. 31 8.1. Netia .......................................................................................... 32 8.2. TP SA ........................................................................................ 34 9. Media ..................................................................................................... 36 9.1. Agora ......................................................................................... 37 10. IT Sector ................................................................................................ 38 10.1. ABG Ster-Projekt ...................................................................... 39 10.2. Asseco Poland........................................................................... 40 10.3. ComArch ................................................................................... 41 10.4. Computerland ............................................................................ 42 10.5. Macrologic ................................................................................ 44 10.6. Prokom Software ...................................................................... 45 10.7. Techmex ................................................................................... 47 11. Metals ..................................................................................................... 48 11.1. Kęty ........................................................................................... 49 11.2. KGHM ........................................................................................ 50 12.3. Koelner ...................................................................................... 51 12. Construction ........................................................................................... 52 12.1. Budimex ..................................................................................... 55 12.2. Elektrobudowa ........................................................................... 56 12.3. Hydrobudowa Śląsk ................................................................... 57 12.4. Polimex Mostostal ...................................................................... 58 12.5. Rafako ....................................................................................... 59 13. Pharmaceutical Manufacturers and Distributors ..................................... 60 13.1. Farmacol .................................................................................... 61 13.2. PGF ........................................................................................... 61 13.3. Prosper ...................................................................................... 62 13.4. Torfarm ...................................................................................... 63 14. Retail\Wholesale ..................................................................................... 64 14.1. Eldorado .................................................................................... 65 14.2. Eurocash ................................................................................... 66 15. Others ..................................................................................................... 67 15.1. Kogeneracja .............................................................................. 67 15.2. Mondi ......................................................................................... 68 15.3. Provimi-Rolimpex ....................................................................... 69

BRE Bank Securities

5 February 2007 3

Monthly Report BRE Bank Securities

Equity market January was a successful month for the equity market, corroborating our predictions offered in our Strategy 2007 report (Jan. 9th). Poland’s good macro-economic indicators, paired with sustained bullish sentiment to European and U.S. equity markets, produced gains for most of the world’s stock indexes. We do not see any threat of reversal in that uptrend in the next few months, even though Polish stocks are expensive. In the near term, a buildup of IPOs (March) could challenge, or even cause a reversal. However, TFI and OFE flow data indicate that both investment fund companies, and pension funds, accumulated enough free cash to absorb the IPOs. For now, current trends in the US economy show that the slowdown is milder than ex-pected, and the FED has inflation under control. The interest rate hikes expected from the ECB in March are already priced in. From a European standpoint, the information to look for-ward to is the impact of the increase in German VAT rates on GDP growth in January. Prelimi-nary estimations indicate that the impact was less than expected, prompting analysts to raise their GDP projections. As a result, concerns about a slowdown in Polish exports to Germany have been mitigated. The macro-economic outlook for Poland is surprisingly positive. The warm winter will probably bring the GDP growth data for the first quarter above analysts’ consensus. GDP growth predic-tions by macroeconomists are increasingly hovering around 5.5%. Neither the December ’06, or the January ’07 inflation data are expected to prompt the Monetary Policy Council (RPP) to raise rates. The average CPI inflation should not exceed 1.7%, and is expected to hit 2.2% max during the year. After the summer season, CPI inflation should decrease to 1%. Some macroeconomists predict a cooling down of the economy in the second half of the year (YoY GDP growth at 3.5-4%) relative to the high reference-year figures, potentially hurting the equity market. But, in our opinion, investors will not discount such a scenario until they see clear signs of a slowdown. Macroeconomic indicators seem to be confirming the predictions offered in our Strategy 2007 report. As expected, the US economy will return on the 3% GDP growth path in the first quar-ter, likely accelerating demand for basic materials, mainly copper and crude oil. In case of the copper market, the crucial demand propeller will be a rebound in the housing market which, despite decent GDP growth, lost 20% of its value in Q4’06. The short-term implication of this slump is reduced demand for and increasing inventories of copper (inventories are piling up mostly in the US and Europe, while demand in Asia is picking up). In a longer term, growing prices of basic materials will propel inflation, potentially causing turmoil in stock markets in the second half of the year. While basic materials markets continue to show weakness, the sentiment is still bearish on telecoms (defensive sector) and financial stocks. This trend will probably continue until a clear uptrend takes shape on crude and metals. We expect the sentiment on construction stocks to dwindle in the near term. Major industry players like Polimex and Budimex will show disappointing Q4 results. As labor and subcon-tractor costs increase while high-margin contracts remain scarce, the prices of construction stocks, which already reflect very sanguine scenarios, are in for a pullback. For the months ahead, we predict that investors will turn their attention to tile manufacturers. In our opinion, the large overproduction and slower-than-expected growth in demand are already priced in. The construction boom observed in 2006 is yet to trigger increased demand for fin-ishing products. This will not solve all of the industry’s problems, but the situation will slowly get better. Stocks like Polkolorit or Nowa Gala seem to us an attractive investment for the months ahead. Construction and IT stocks were growth leaders again in January, with indexes up 22.8% and 16.2% respectively. Food stocks displayed the weakest performance, as did telecoms, with TPSA gaining the most and Netia taking the biggest plunge. The WIG 20 securities rose by an average 6%. During the same time, the MidWIG gained over 13%.

Changes in WSE indexes WIG WIG20 MIDWIG Banks Constr Media Food Tel IT YTD 41.2% 21.3% 56.3% 58.8% 157.7% 13.0% 38.8% 13.4% 46.1% QTD 13.4% 10.2% 17.4% 27.4% 39.4% 18.9% 3.7% 12.1% 31.1% MTD 8.3% 6.0% 13.5% 11.1% 22.8% 7.7% 0.9% 3.5% 16.2% Source: WSE

BRE Bank Securities

5 February 2007 4

Monthly Report BRE Bank Securities

Fund Flows TFI December 2006 marked another month of robust inflows into investment fund companies (PLN 2.8 billion). In December 2005, inflows were stronger (PLN 3.4 billion), but the YoY decline recorded this year can be explained with clients moving their fund share purchase decisions up to November 2006, which was a record month for inflows at a whopping PLN 3.7 billion. Combined, inflows for the two final months of the year amounted to PLN 6.5 billion (25% more than in the corresponding period a year earlier). December also put a stop to outflows from debt funds. There was a shift in equity investments away from equity funds and into balanced funds. If this trend continues in the next few months, it might be an indication of greater market volatility.

TFI inflows/outflows by “equity component” funds and money market/debt funds

-2 000

-1 000

0

1 000

2 000

3 000

4 000

5 000

2005-11-01 2006-02-01 2006-05-01 2006-08-01 2006-11-01

mln PLN

Akcyjne, stabilnego w zrostu, mieszaneDłużne, pieniężne, pozostałe

Source: Analizy Online

OFE Open pension funds (OFEs) received PLN 1.2 billion from Social Insurance contributions in December. The share of equity securities in OFE portfolios was 34.1% at the end of December 2006 versus an average 34.9% in November. Allocations to equities increased by PLN 407m (1%), while the WIG index edged up under 0.5%, and the WIG 20 rose 2.1%. The equity com-ponent of OFE portfolios decreased as more assets were reallocated to debt and other securi-ties. The equity component is still at a level which could bring about a correction, enabling funds to dilute the capital invested in the stock market.

Equities in OFE portfolios vs. WIG20

16 000

21 000

26 000

31 000

36 000

41 000

46 000

51 000

56 000

gru-04 cze-05 gru-05 cze-06 gru-0620%

22%

24%

26%

28%

30%

32%

34%

36%

38%

40%

WIG Udział akcji w portfelach OFE

Source: BRE Bank Securities, Bankier.pl

PLN m

Equity, growth, balanced funds Debt, money-market, other

Equity component

Dec'04 Jun'05 Dec'05 Jun'06 Dec'06

BRE Bank Securities

5 February 2007 5

Monthly Report BRE Bank Securities

Emerging market funds Cash keeps flowing in to emerging market funds. Geographic allocations follow the same trends. Inflows are the largest for global market funds and funds dedicated to the Chinese market. Funds dedicated to Europe, the Middle East, and Africa (EMEA) recorded sustained outflow trends in January: they have lost close to US $300m since the beginning of the year, although they won back some $60m over the past two weeks. The sustained trends confirm that investor sentiment to emerging market funds is still bearish.

Weekly inflows/outflows for selected emerging market funds

GEM

-1 500

-1 000

-500

0

500

1 000

1 500

4-01

4-02

4-03

4-04

4-05

4-06

4-07

4-08

4-09

4-10

4-11

4-12

4-01

mln USD EMEA

-2 000

-1 500

-1 000

-500

0

500

1 000

4-01

4-02

4-03

4-04

4-05

4-06

4-07

4-08

4-09

4-10

4-11

4-12

4-01

mln USD

Source: EmergingPortfolio.com

$ millions $ millions

BRE Bank Securities

5 February 2007 6

Monthly Report BRE Bank Securities

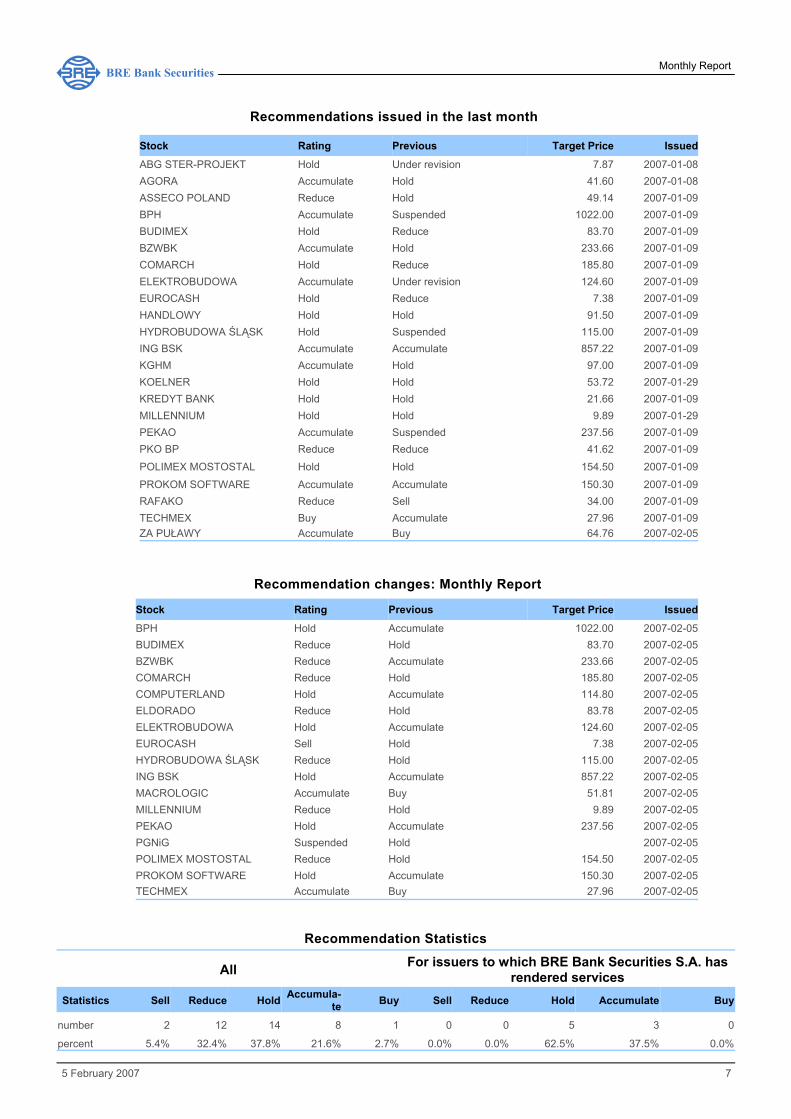

Current recommendations of BRE Bank Securities S.A.

Stock Rating Target Price Issued

ABG STER-PROJEKT Hold 7.87 2007-01-08 AGORA Accumulate 41.60 2007-01-08 ASSECO POLAND Reduce 49.14 2007-01-09 BPH Hold 1022.00 2007-02-05 BUDIMEX Reduce 83.70 2007-02-05 BZWBK Reduce 233.66 2007-02-05 COMARCH Reduce 185.80 2007-02-05 COMPUTERLAND Hold 114.80 2007-02-05 ELDORADO Reduce 83.78 2007-02-05 ELEKTROBUDOWA Hold 124.60 2007-02-05 EUROCASH Sell 7.38 2007-02-05 FARMACOL Accumulate 45.60 2006-11-07 HANDLOWY Hold 91.50 2007-01-09 HYDROBUDOWA ŚLĄSK Reduce 115.00 2007-02-05 ING BSK Hold 857.22 2007-02-05 KĘTY Hold 180.50 2006-09-27 KGHM Accumulate 97.00 2007-01-09 KOELNER Hold 53.72 2007-01-29 KOGENERACJA Hold 61.80 2006-11-07 KREDYT BANK Hold 21.66 2007-01-09 LOTOS Accumulate 59.30 2006-08-24 MACROLOGIC Accumulate 51.81 2007-02-05 MILLENNIUM Reduce 9.89 2007-02-05 MONDI Reduce 80.00 2006-12-05 NETIA Sell 3.80 2006-09-06 PEKAO Hold 237.56 2007-02-05 PGF Under revision 2006-12-05 PGNiG Suspended 2007-02-05 PKN ORLEN Buy 66.00 2006-08-24 PKO BP Reduce 41.62 2007-01-09 POLIMEX MOSTOSTAL Reduce 154.50 2007-02-05 PROKOM SOFTWARE Hold 150.30 2007-02-05 PROSPER Accumulate 20.90 2006-11-07 PROVIMI-ROLIMPEX Hold 21.81 2006-12-05 RAFAKO Reduce 34.00 2007-01-09 TECHMEX Accumulate 27.96 2007-02-05 TELEKOMUNIKACJA POLSKA Reduce 20.60 2006-10-27 TORFARM Hold 63.7 2006-08-25 ZA PUŁAWY Accumulate 64.76 2007-02-05

BRE Bank Securities

5 February 2007 7

Monthly Report BRE Bank Securities

Recommendations issued in the last month

Recommendation Statistics

All For issuers to which BRE Bank Securities S.A. has rendered services

Statistics Sell Reduce Hold Accumula-te Buy Sell Reduce Hold Accumulate Buy

number 2 12 14 8 1 0 0 5 3 0

percent 5.4% 32.4% 37.8% 21.6% 2.7% 0.0% 0.0% 62.5% 37.5% 0.0%

Recommendation changes: Monthly Report

Stock Rating Previous Target Price Issued

ABG STER-PROJEKT Hold Under revision 7.87 2007-01-08 AGORA Accumulate Hold 41.60 2007-01-08 ASSECO POLAND Reduce Hold 49.14 2007-01-09 BPH Accumulate Suspended 1022.00 2007-01-09 BUDIMEX Hold Reduce 83.70 2007-01-09 BZWBK Accumulate Hold 233.66 2007-01-09 COMARCH Hold Reduce 185.80 2007-01-09 ELEKTROBUDOWA Accumulate Under revision 124.60 2007-01-09 EUROCASH Hold Reduce 7.38 2007-01-09 HANDLOWY Hold Hold 91.50 2007-01-09 HYDROBUDOWA ŚLĄSK Hold Suspended 115.00 2007-01-09 ING BSK Accumulate Accumulate 857.22 2007-01-09 KGHM Accumulate Hold 97.00 2007-01-09 KOELNER Hold Hold 53.72 2007-01-29 KREDYT BANK Hold Hold 21.66 2007-01-09 MILLENNIUM Hold Hold 9.89 2007-01-29 PEKAO Accumulate Suspended 237.56 2007-01-09 PKO BP Reduce Reduce 41.62 2007-01-09 POLIMEX MOSTOSTAL Hold Hold 154.50 2007-01-09

PROKOM SOFTWARE Accumulate Accumulate 150.30 2007-01-09 RAFAKO Reduce Sell 34.00 2007-01-09 TECHMEX Buy Accumulate 27.96 2007-01-09 ZA PUŁAWY Accumulate Buy 64.76 2007-02-05

Stock Rating Previous Target Price Issued

BPH Hold Accumulate 1022.00 2007-02-05 BUDIMEX Reduce Hold 83.70 2007-02-05 BZWBK Reduce Accumulate 233.66 2007-02-05 COMARCH Reduce Hold 185.80 2007-02-05 COMPUTERLAND Hold Accumulate 114.80 2007-02-05 ELDORADO Reduce Hold 83.78 2007-02-05 ELEKTROBUDOWA Hold Accumulate 124.60 2007-02-05 EUROCASH Sell Hold 7.38 2007-02-05 HYDROBUDOWA ŚLĄSK Reduce Hold 115.00 2007-02-05 ING BSK Hold Accumulate 857.22 2007-02-05 MACROLOGIC Accumulate Buy 51.81 2007-02-05 MILLENNIUM Reduce Hold 9.89 2007-02-05 PEKAO Hold Accumulate 237.56 2007-02-05 PGNiG Suspended Hold 2007-02-05 POLIMEX MOSTOSTAL Reduce Hold 154.50 2007-02-05 PROKOM SOFTWARE Hold Accumulate 150.30 2007-02-05 TECHMEX Accumulate Buy 27.96 2007-02-05

BRE Bank Securities

5 February 2007 8

Monthly Report BRE Bank Securities

The zloty appreciated by over 1% against most major currencies in the second decade of January, on a combination of global and local factors. An appreciation trend manifested itself in the entire emerging markets segment following a steep fall in the prices of basic materials including crude oil. Locally, the zloty was driven by the December/January inflation surprise (according to official GUS estimates, the inflation rate was 1.38% at the end of 2006, and the max forecast for January is 1.6%), last year’s lower-than-expected budget deficit, effective absorption of EU funds at the end of 2006, and Fitch’s rating upgrade for Poland. The zloty should continue on its strengthening course in the first half of 2007. EU fund inflows in the first quarter of the year are estimated at PLN 5-6 billion. The zloty/euro exchange rate will stay within the range of 3.70-3.90 until mid year, and the zloty/dollar rate will remain below 3. A reversal might occur in the second half of the year, as EU fund inflows slow down, the economy cools, inflation goes slowly up, and the political/fiscal risk increases on approaching 2008 budget planning. The short end of the yield curve will be sustained at least until April/May on continuing expec-tations of interest rate hikes in Poland among some market stakeholders. Those expectations will disappear in the second half of the year as the current CPI falls to ca. 1%, and there is deflation in producer prices. It will be similar with expectations of interest rate hikes by the ECB in the euro zone, where, after the CPI falls to 1% in August and the growth rate slows down below potential, the refi rate will stop at 3.75%. As expectations grow that the FED will ease monetary policy in the USA, the short end of the yield curve in Poland seems to offer a considerable potential. The long end will be influenced by contrasting factors: on the one hand, the prevalent moderate mid-term inflation rate fore-casts will support prices; on the other hand, market rates will be affected by slower growth, increasing fiscal risk, anticipation of a steep surge in public debt service costs (PLN 5-6 billion in 2008-2010 relative to 2007), and uncertainty about convergence to the euro. Hence, while we expect the yield curve to be flat in the first half of the year, afterwards, it is probably going to steepen, with 10Y bond yields at 5.2% max. The past year was a favorable one for the state budget. Strong economic momentum drove revenues over PLN 2.5 billion above target. This was close to PLN 1.5bn more than forecasted in mid-2006. At the same time, the government’s firm grip on spending kept all through the year helped generate almost PLN 2.7 billion in savings. Last year’s deficit of PLN 25 billion (below target) could have been ca. PLN 2.5 billion lower if it had not been for the “permanent appropriations” moved forward to this year. Even as it was, the deficit better than the target PLN 30.5bn, and 0.5% of GDP below analysts’ expectations, at 2.5-2.6% of the GDP. Calculated using the EU approach which will start to apply in Poland as of March, the public sector deficit was 4.6-4.7% of the GDP. This is an alarming outcome. Despite near-6% eco-nomic growth, our public finance is still heavily unbalanced. Despite favorable stock market trends, privatization revenues did not even reach one-third of the (very humble) target. Hence, despite lower deficit, financing had to be larger that expected. Poland's enormous borrowing needs did not allow for a reversal in the uptrend in public debt which exceeded 48% of the GDP.

Macroeconomics

BRE Bank Securities

5 February 2007 9

Monthly Report BRE Bank Securities

Financial Sector Annual re-ranking of the WIG 20 index It seems like BRE will stay within the WIG 20 Index. Getin Holding was ranked higher, but BRE is still eligible to be included in the top 15 securities, and will therefore be retained in the index during the annual review. The re-ranking will not have any impact on the two stocks. BRE will be retained in the top-20 of WSE-listed securities, and Getin has been attracting large investor interest for some time. Getin will have another chance to make it into the WIG 20 after the BPH spin-off. The fight will be between Getin, Bank Handlowy, and Millennium. It is hard to tell which bank has the best chance of winning a place in the WIG-20 given that we do not know their future trading volumes or quotes. Intercharge dispute After five years of considerations, the Polish competition watchdog UOKiK wants to impose up to PLN 160m fines on the largest banks for “colluding” to charge overblown intercharge fees. UOKiK’s ruling has an “executable immediately” clause. The affected banks first appealed against the clause, and then against the ruling itself. Of the 19 banks fined, the following were hit hardest: PKO BP and Pekao (PLN 16.6m each), BPH (PLN 14.7m), ING BSK (PLN 14.1m), BZ WBK (PLN 14.1m), Millennium (PLN 12.2m), Kredyt Bank (PLN 12.1m), Bank Handlowy (PLN 10.2m), BRE (PLN 7.7m), and Getin Bank (PLN 4.8m). But this is not the end: once UOKiK’s ruling is validated, retail chains might sue the banks for the fees they charged earlier, possibly leading to the banks’ being forced to pay out compensa-tions in addition to reducing the intercharge fees. But the banks are not going to stand still. They claim that the intercharge fees are adequate to offset the maintenance costs of payment processing systems, and that the ruling will hamper further development of the payment processing network. Retailers, in turn, say that the inflated fees limit their capacity to handle payments. The dispute is not over yet. Some banks have rec-ognized provisions against the fine amounts, which might be shown in their Q4'06 financials. The fines themselves are not a big imposition on income; what is worse is the loss of inter-charge income and the possible future claims by retailers. In the worst-case scenario, banks will be able to offset the loss of income against account management or card fees. But the conse-quences are hard to assess at this stage. If the worst-case scenario pans out, the banks most hurt will be those with the broadest exposure to the retail banking market and those that issued the largest number of cards. 2007 another good year According to the Inspector General for Banking Supervision, bank profits in FY2007 might gain a further 15%–20%. Last year's aggregate net profit stood at PLN 10.7 billion. Banks are pre-pared to generate income growth, and will continue to improve efficiency. We agree. We predict a FY09/06 CAGR of 14%. Income will be driven by increasing volumes paired with a slowdown in costs. Even if some banks are going to incur expenses on enlarging their sales networks, economies of scale and new sales channels will more than offset the growing costs. Pengab down to 38pts The index gauging sentiment in the banking industry fell 1.5pts within a month. Bankers are becoming more and more critical about the market situation, and their projections for the future are becoming less and less optimistic. We stand by our belief that there is nothing wrong going on in the banking industry; historically, the Pengab index is still soaring. Also, it usually backs off in January as the market regains its balance after the Christmas season. Lending on an uptrend Loan sales in 2006 exceeded PLN 70bn, marking a 23.4% increase from the previous year. Financial intermediaries generated PLN 11 billion of that amount, which was a whopping 78.9% more than in 2005 (a little over PLN 6 billion). Leading the market is Expander (PLN 3.3bn), followed by Open Finance (PLN 2.9bn), Żagiel (PLN 1.95bn), and intermediaries with sales be-low PLN 1 billion: Notus, Dom Finansowy QS, Fiolet, PDK, Goldenegg, A-Z Finanse. Financial intermediaries will play an increasingly important role as financing providers. They can focus their sales efforts on a single product group, e.g. mortgage loans, and offer clients a range of solutions from different banks. Clients appreciate the wide choice of products and the possibility to handle all formalities at one place, with the help of a dedicated account manager. Another advantage of financial intermediaries are competitive prices, often more attractive than offered by banks, achieved through negotiations. Banks are more than willing to reduce their margins when an agent offers to sell its millions of zlotys-worth of its products. This is good news for Getin Holding (three of its subsidiaries: Open Finance, Fiolet, and PDK were included in the

BRE Bank Securities

5 February 2007 10

Monthly Report BRE Bank Securities

ranking), and Kredyt Bank (Żagiel). Note that Żagiel is the undisputed leader in selling cash loans (the value of an average cash loan is much lower than an average mortgage loan). Record sales of mortgage loans According to data compiled by Rzeczpospolita, banks sold PLN 43.4bn-worth of mortgage loans (vs. PLN 24.3bn in 2005). The Polish Banks’ Association (ZBP) arrived at a similar figure (PLN 41bn). PKO BP is still the leader in mortgage loans, with sales at PLN 10.1bn. Millennium came in second (PLN 4.7bn) after BPH decided to discontinue selling foreign-currency mortgage loans. BPH was third even in spite of its diminishing market share (PLN 4.5bn). Lower in the ranking are GE Money (PLN 3.4bn), Pekao (PLN 2.7bn), mBank (PLN 2.3bn). Everybody knew that 2006 would be a record year for mortgage loan sales, and predictions hovered around PLN 40m. Also the record sales generated by ranking leaders came as no surprise. In our opinion, the market has already discounted the impressive performance in the mortgage loan market in 2006. ZBP: mortgage loan portfolio to reach PLN 350-400 billion by the end of 2015 According to the Polish Banks’ Association (ZBP), the value of mortgage loans might reach PLN 350-400 billion in 2015. 2007 sales are forecasted at PLN 55 billion versus over PLN 41 billion in 2006. The ZBP forecast covers retail clients and real-estate developers. At the end of 2006, ca. 40% of home loans were written in zlotys versus 20% at the beginning of the year. No new consumer lending regulations are expected to be introduced in the next few months (FCY lend-ing restrictions). Summing up, the ZBP expects that sales will surge ca. 34% YoY in 2007 (this applies to volumes, which include refinancing). Like in 2006, the increase in the net mortgage loan portfolios of banks across the board will be lower than sales volumes due to old debt re-payments and refinancing. If the mortgage loan portfolio is to increase from PLN 90bn to PLN 350-400bn at the end of 2015, the ‘15/06 CAGR would be 16% - 18%. This is in line with our expectations. At the end of November 2006, the YoY increase in home loans was over 50%. This means that the growth rate figures will decrease, but it will be an effect of the growing YoY comparable base, not of nominally weaker volumes. Good times are ahead of the Polish bank-ing industry, but this scenario is inline with our outlook, and has been already largely discounted by the market. Home loan subsidies In January, PKO BP pioneered sales of home loans with government-subsidized interest pay-ments based on an agreement with Bank Gospodarstwa Krajowego. The subsidies are an effect of the new law providing for governmental support for families who want to buy homes. Eligible loans are for 50 sqm of apartment space (the apartments themselves cannot be more than 75 sqm), and 70 sqm of house space (for houses up to 140 sqm). The subsidies are granted only to families and single parents who are not home owners. Pekao is also going to sign agreement enabling it to offer subsidized home loans. Other banks are sure to follow suit. PKO BP might be the first, but competition is just around the corner. Since the interest payments are subsidies only up to a certain point, and the eligible borrowers often have to take out long-term loans (25-30 years) to meet creditworthiness requirements, the subsidies will not change much in their borrowing capacity. In short, people who could not afford to take out loans before, will not be able to do so now. Another barrier for potential subsidized-loan borrowers is the cap put on the per-sqm price of the financed homes. However, the price-per-sqm criterion will be updated. We do not think that the loan interest subsidies will change much in the lending business landscape. Extended loan repayment terms According to Gazeta Wyborcza, UK’s Abbey National Bank extended the repayment periods on its mortgage loans to even 57 years. This is a result of an interest rate hike by the UK Central Bank, paired with the growing prices of homes. If the payment period had not been extended, the creditworthiness of Britons would decrease dramatically. We are seeing a similar trend in Poland, with durations reaching 45 years in some cases. Looking at what is happening in the UK, we can conclude that loan durations will increase. In our opinion, this will lead to prolonged home loan portfolio durations, and a steadying of the income earned on those products. 6.3 million credit cards Approximately 700,000 new cards were issued in the fourth quarter of last year (vs. 400,000 in Q3’06). Like every year, banks experienced an upswing during the Christmas shopping season. However, many clients received cards as add-ons to other products (cash loans, mortgage loans, installment plans), and most of them will never use them. Simpler procedures and adding cards to each product drove PKO BP’s sales to a whopping 239,000 cards in Q4’06 alone. At the end of the year, the number of cards issued amounted to 908,000, placing the bank in pole position in credit card accounts. Runners up include Lukas Bank (807,000), GE Money Bank (750,000), Bank Handlowy (662,900), BPH (487,000), and Millennium (257,000). ING BSK also recorded decent sales, the bulk of which were generated in the last quarter of 2006. But the number of card issuances has nothing to do with actual card transaction volumes. Credit cards become profitable for banks only if clients pay for their issuance. For now, both the share of

BRE Bank Securities

5 February 2007 11

Monthly Report BRE Bank Securities

credit cards in total cards issued (ca. 25%), and the number of credit card transactions (11% of all transactions), show that their usage is still infrequent. And, after all, banks do not start to profit on cards until clients go into debt. Factoring gains popularity Banks and specialized factoring companies purchased PLN 20 billion-worth of invoices in 2006, which was one-third more than in 2005. Businesses are increasingly turning to factoring provid-ers. The biggest gainers included Factor in Bank, Fortis Commercial Finance, and Bank BGŻ. Banks performed better than factoring companies, increasing the level of purchased debt by 63% YoY, versus 22%. Raiffeisen Bank and Pekao Facotring bought the largest number of ac-counts receivable, followed by ING Commercial Finance, Polfacotr, and GMAC Commercial Finance. The factoring market has great growth potential. Last year, Getin Bank spun off a “Factor in Bank” from its organization last year, which is currently recording the highest growth rates (compared to a small YoY base). As more and more businesses turn to banks for factoring services, bank income will grow. Record year for leasing 2006 was a record year for the leasing business in Poland. The value of leased assets amounted to PLN 21.5 billion, which was 32% more than in 2005. Last year’s leasing business was driven by vehicle leases, and, as a new development, machine and equipment leases. In EU countries, leasing has a 17% share in total investment financing (25% max). Poland is slowly catching up, with a 10% share. According to lease experts, the outlook on 2007 is good, and the market is expected to grow by up to 25%. This is another news confirming that busi-nesses are starting to become more active in using banking services. Aside from loans and leases, corporations are also increasingly looking for services like financial products and cash management. This is good news for banks that have leasing subsidiaries. And, once again, BZ WBK sets an example as a well-organized group which, by developing several business arms at the same time, has positioned itself to take advantage of the momentums in different markets. Its lease subsidiaries have a 6.1% market share. The lease market momentum is also good news for Pekao Leasing (3.5%), BPH Leasing (5.0%) (or, rather, the post-merger Pekao which will take it over), Millennium Leasing (6.2%), BRE Leasing (9.8%). These trends will also indi-rectly benefit banks with large exposure to the corporate segment, i.e., in addition to those listed above, also ING BSK and Bank Handlowy. Car loans Rzeczpospolita published a list of top car loan sellers. In pole position is still Santander Con-sumer Bank, with PLN 1117.2m car loan sales in FY2006. Below are Getin Bank (PLN 862.9m), GE Money (PLN 601.9m), Volkswagen Bank (PLN 557.8m). Further down the line are banks that sold less than PLN 400m (BPH is ninth with PLN 204m, ING BSK is fifteenth with PLN 63.5m). The best performers were banks that do not limit themselves to selling via their own branches, but that also struck partnerships with retail chains and other distributors. Banks that did not make it to the top spots in the ranking cannot be criticized: some of them do not sell car loans at all (PKO BP, Pekao, BZ WBK). This is good news for Getin Bank. We should remem-ber, however, that buyers often finance cars with cash loans (to avoid the formalities), or other forms of consumer financing. Banks spent almost PLN 590m on promotion in 2006 Promotional expenses in 2005 stood at PLN 365m, which means that they soared a whopping 60% in 2006. The YoY increase in 2005 was close to 18%. By stepping up promotional activi-ties, banks increased their share in the advertising market from 3.3% in 2005 to 4.5% in 2006. The biggest spenders included BPH (PLN 4.56m), Eurobank (PLN 45.2m), ING BSK (PLN 39m), Millennium (PLN 36.8m), Lukas Bank (PLN 33.8m), PKO BP (PLN 29.8m), Polbank EFG (over PLN 29m). Each of them had its own reasons to step up advertising: for some, it was re-branding, and for others, it was launch advertising (Polbank EFG). The underlying motivation, however, was to reach consumers in a period of prosperity in the retail banking market. We expect equally intense advertising efforts from banks this year. Bank accounts on the rise The number of personal accounts increased by 1.3m in 2006, driven mainly by lending and im-proving Internet access. At the end of 2006, the number of zloty accounts reached 17.4 million. The leader in account volumes is PKO BP (6.07m accounts), followed by Pekao (2.3m), and BPH (1.4m). The numbers grow both thanks to new as well as existing clients who own more than one account. The ratio of unbanked population is decreasing, and market saturation with banking products is increasing. But banks still have a lot of uncharted territory to cover. With time, however, as the territory shrinks, they will have to start competing with each other. But this is such a long-term perspective that it is not being taken into account in bank valuations. Bank Pocztowy’s FY2006 performance Bank Pocztowy’s FY2006 net profit was slightly higher than in FY2005 (FY’05: PLN 23.9m). BP

BRE Bank Securities

5 February 2007 12

Monthly Report BRE Bank Securities

currently operates 20 of its stands at post offices. According to the CEO, a list has already been drafted of 1.2 thousand more post offices that will host bank teller windows this year. BP launched the sales of its “post office express loan” (a cash loan) at the end of last year. Accord-ing to plans, the bank was to sell PLN 100m-worth of loans from September to January. The exact figure was not disclosed, but it was lower than expected due to post office worker strikes. Looking at Bank Pocztowy’s performance so far, it does not look like it should threaten the mar-ket share of listed commercial banks in the near term. PKO BP, which owns 25% of BP’s equity, wants to develop sales of its products via the post-office channels. But BP will not become a significant component of the volume-building strategy at least for another year. Santander Consumer Bank moves into retail The bank is currently the market leader in car loan sales. This year, it is going to launch a com-plete retail offer. It has been offering mortgage and cash loans for some time, but will extend the mix to include other products, such as credit cards, deposits, and personal accounts. To date, Santander has financed its lending business via interbank operations, where guarantees issued by its strategic investor with a high investment rating made it easier to acquire financing. The bank will receive a capital injection of PLN 120m to PLN 520m, as its lending activity (64% YTD portfolio growth after Q3’06) has led to a decline in its CAR to around 8%. More competition for listed banks. Polbank EFG will enlarge sales network in 2007 Polbank EFG is going to enlarge its sales network, and launch an investment fund share offer in the first half of the year. New branches are expected to reach BEP after 2.5-3.5 years. Also in the first half of the year, Polbank EFG will introduce new products for consumers and small businesses. There are no plans to launch an insurance offering for now. Polbank EFG’s current product mix includes personal accounts, savings accounts, cards, cash loans, mortgage loans, and investment and working-capital loans for small businesses. Kazimierz Stańczak confirmed that the bank’s FY2006 targets were met. Plans for the first six months of the year further in-clude an enhancement of the e-banking service functionality. It looks like Polbank EFG is here to stay and we can expect to see more of its in our streets. For now, it operates through 67 of its own branches and 61 partner outlets, but wants to expand the sales network. Polbank EFG is a new player which, for now, poses no threat to volumes generated by listed banks. The strong market momentum and the fact that the bank is just starting out means that other banks have nothing too fear in the short term, but should watch out in the longer term.

BRE Bank Securities

5 February 2007 13

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska19 Last Recommendation: 2007-02-05(PLN m) 2005 2006F change 2007F change 2008F change Basic data (PLN m)Net interest income 1 981.4 2 185.0 10.3% 2 375.0 8.7% 2 516.0 5.9% Number of shares (m) 28.7Interest margin 3.6% 3.5% 3.5% 3.6% MC (current price) 31 013.5Revenue f/banking oper. 3 083.9 3 530.4 14.5% 3 829.2 8.5% 4 072.8 6.4% Free float 25.3%Operating profit 1 560.9 1 973.6 26.4% 2 335.7 18.3% 2 346.2 0.5%Gross profit 1 294.4 1 706.0 31.8% 2 031.9 19.1% 2 018.5 -0.7%Net prof it 1 027.4 1 333.6 29.8% 1 601.0 20.1% 1 584.6 -1.0%

ROE 16.8% 20.2% 22.8% 21.7% Price change: 1 month 15.0%P/E 30.2 23.3 19.4 19.6 Price change: 6 month 35.5%P/BV 4.9 4.5 4.3 4.2 Price change: 12 month 36.4%D/PS 22.1 30.0 41.8 50.2 Max (52 w eek) 1 088.0Dyield (%) 2.0 2.8 3.9 4.6 Min (52 w eek) 610.0

Current price: PLN 1080 Target price: PLN 1022BPH (Hold)

500

600

700

800

900

1000

1100

2006-01-30 2006-05-30 2006-09-30 2007-01-30

BPH WIG

BPH’s stock has risen over 17% since our last rating, therefore, we are downgrading from Accumulate to BUY. Our price target on the stock is a blend of four factors: 3.3x Pekao’s stock price, dividends from the FY2006 profit, BPH TFI’s price, and Mini-BPH’s price estimates. Pekao’s stock has also rallied recently. If we take such an increased valuation and leave all other factors unchanged, the implied price of BPH is PLN 1096/share. This estimate includes the Mini-BPH price estimate of four times its equity. Even if the actual selling price is higher, it will still account for a mere 18% of our price target on BPH. The main factor determining BPH’s stock performance at the moment is Pekao’s stock. And, since the latter shows no upside potential, the former does not either. Near-30% profit boost The bank proudly announced that its Q4’06 profit will boost the full-year bottom line by several dozen percent. The gross C/I ratio and ROE will be higher than the strategic targets of 47% and 24.3% respectively. This is in line with our expectations. We estimate that BPH will report a net profit of PLN 1.334bn for FY2006. The Q4’06 bottom line will be PLN 416m, including an estimated PLN 81m from the sale of PLN 1bn worth of non-performing loans (PLN 100m before taxes). Those numbers imply that the year-over-year increase in profit will be close to 30%, in-cluding almost 22% in recurring profit (excluding the NPL sale). More details on BPH division UniCredit reported the start of a due diligence audit at the Mini-BPH by the short-listed prospec-tive buyers. Once the audit is complete, the bidders will submit binding offers. According to un-official sources quoted by Parkiet, the list is composed of five investors (General Electric, Raif-feisen International, BNP Paribas, KBC, and an unknown organization). The shareholders of BPH and Pekao will meet in late March to approve the merger processes (most importantly the division of BPH, incorporation of assets into Pekao, and sale of the Mini-BPH). All those proc-esses will be subject to approval by relevant supervision bodies. UniCredit wants to finish the spin-off and incorporation of the remaining BPH into Pekao in the second quarter of 2007, and sell the Mini-BPH in the second half of the year. The good news is that the processes scheduled for 2007 were accelerated. The stock merger consideration will be issued earlier than we ex-pected, as will be the case with the incorporation of BPH’s assets into Pekao; similarly, the Ex-traordinary General Assemblies that we though would take place in April were moved back to March. UniCredit also officially confirmed the Mini-BPH’s status. We expect to learn its selling price in late Q1/earlyQ2. „Mini – BPH” valuation According to January speculations, the “mini-BPH” might be worth even EUR 1-1.5bn. Accord-ing to press releases, the due dilligence audit was scheduled for late January/early February, and short-listed investors were supposed to submit binding offers in mid-February. For the time being the schedule of due dilligence matches the assumptions. Unicredito said that the short-listed investors had already started the due dilligence procedure, and afterwards are expected to submit binding offers. In the context of the fact that the shareholders of BPH and Pekao will meet in late March to approve the merger processes, we believe that the investors interested in mini-BPH will submit binding offers before. As Unicredit must have some time to examine the offers, most probably they will be submitted in mid-February. While presenting “mini-BPH” valuation, the investors will give the price of BPH TFI, which will be the part of “mini-BPH” group after its sale. Therefore, we have not much time left to speculate about “mini-BPH” valuation. In the course of time the discount applied to “mini-BPH” valuation should decrease. According to the press, the

BRE Bank Securities

5 February 2007 14

Monthly Report BRE Bank Securities

price range of "mini-BPH” is between 2.8 and 4.3x the equity as of 1 September 2006. We maintain our view that the Mini-BPH will be sold for 4xBV.

BRE Bank Securities

5 February 2007 15

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska44 Last Recommendation: 2007-02-05(PLN m) 2005 2006F change 2007F change 2008F change Basic data (PLN m)Net interest income 909.3 1 021.2 12.3% 1 164.0 14.0% 1 301.4 11.8% Number of shares (m) 73.0Interest margin 3.2% 3.3% 3.5% 3.6% MC (current price) 19 443.9Revenue f/banking oper. 1 895.8 2 346.9 23.8% 2 621.8 11.7% 2 917.9 11.3% Free float 29.5%Operating profit 750.6 1 130.6 50.6% 1 327.4 17.4% 1 544.0 16.3%Gross profit 689.5 1 087.5 57.7% 1 234.8 13.5% 1 436.9 16.4%Net prof it 516.3 780.5 51.2% 899.8 15.3% 1 058.9 17.7%

ROE 16.1% 22.0% 23.1% 24.9% Price change: 1 month 13.4%P/E 37.7 24.9 21.6 18.4 Price change: 6 month 41.0%P/BV 5.8 5.2 4.8 4.4 Price change: 12 month 70.8%D/PS 2.4 6.0 7.5 8.6 Max (52 w eek) 267.5Dyield (%) 0.9 2.3 2.8 3.2 Min (52 w eek) 146.0

BZ WBK (Reduce)Current price: PLN 266.5 Target price: PLN 233.7

120

140

160

180

200

220

240

260

2006-01-30 2006-05-30 2006-09-30 2007-01-30

BZ WBK WIG

BZ WBK’s stock appreciated ca. 20% since our last rating (January 9th), therefore, we are downgrading our rating from Accumulate to REDUCE. The market has probably already factored in investor expectations of higher-then-expected Q4’06 earnings. The Q4’06 re-port is scheduled for February 22nd. If it is good, we might revise our rating. At the mo-ment, BZ WNK trades on an ‘07P/E multiple of 21, assuming that the FY2007 net income improves by over 15%. Incentive plan On motion from the Supervisory Board, steps were taken to launch Management Stock Option Plan II for the top management of BZ WBK and its subsidiaries. Under the plan, the managers will be vested senior bonds entitling them to subscribe to BZ WBK’s shares in the future. The Board formulated and approved the basic Plan guidelines and proposed that shareholders vote to adopt them at the nearest GA. The Plan will be carried out through an issue of senior bonds entitling their holders, subject to fulfillment of certain financial criteria, to acquire the bank's shares issued within the framework of a conditional equity increase (up to 150 thousand shares between 2007 and 2010). The bank informed about its plans earlier, therefore it should come as no surprise for the market. Supervisory Board member resigns Mr. Declan McSweeney resigned as Member of BZ WBK’s Supervisory Board. The reason was not disclosed, however, we believe that this news has no impact on our view on the bank.

BRE Bank Securities

5 February 2007 16

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska12 Last Recommendation: 2007-01-09(PLN m) 2005 2006F change 2007F change 2008F change Basic data (PLN m)Net interest income 1 025.9 1 046.3 2.0% 1 170.7 11.9% 1 271.4 8.6% Number of shares (m) 130.7Interest margin 3.1% 3.0% 3.1% 3.3% MC (current price) 11 857.4Revenue f/banking oper. 2 232.2 2 055.8 -7.9% 2 276.8 10.7% 2 484.5 9.1% Free float 24.4%Operating profit 765.3 764.0 -0.2% 823.3 7.8% 975.0 18.4%Gross profit 793.4 803.7 1.3% 765.5 -4.8% 908.5 18.7%Net prof it 616.4 630.7 2.3% 620.0 -1.7% 735.9 18.7%

ROE 10.7% 11.8% 11.4% 13.2% Price change: 1 month 3.5%P/E 19.2 18.8 19.1 16.1 Price change: 6 month 31.5%P/BV 2.3 2.2 2.2 2.1 Price change: 12 month 28.2%D/PS 12.0 3.6 4.3 4.3 Max (52 w eek) 91.2Dyield (%) 13.2 4.0 4.8 4.7 Min (52 w eek) 64.0

Current price: PLN 90.8 Target price: PLN 91.5Handlowy (Hold)

55

65

75

85

95

2006-01-30 2006-05-30 2006-09-30 2007-01-30

Bank Handlowy WIG

We are reiterating our HOLD rating on Bank Handlowy’s stock, which edged up a little under 2% since our last Research. We do not see any upside in the stock. We believe that our valuation reflects investor expectations about the benefits of the bank’s new Retail Strategy and a rally in the corporate banking market. We do not expect to hear any details of how the Strategy implementation is going until the Q4’06 earnings release on March 1st. Our net income estimate for Q4’06 is PLN 140m, which, although flat relative to Q3 (PLN 142m), was built on growing income rather than provision reversals. We do not expect a breakthrough in the Retail segment yet. The new Retail Strategy will start to influence earnings this year.

BRE Bank Securities

5 February 2007 17

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska017 Last Recommendation: 2007-02-05

(PLN m) 2005 2006F change 2007F change 2008F change Basic data (PLN m)Net interest income 721.2 944.2 30.9% 1 077.9 14.2% 1 183.1 9.8% Number of shares (m) 13.0Interest margin 1.9% 2.1% 2.2% 2.2% MC (current price) 10 694.2Revenue f/banking oper. 1 641.2 1 759.5 7.2% 1 978.9 12.5% 2 179.7 10.1% Free float 18.5%Operating profit 561.2 578.2 3.0% 746.7 29.1% 883.7 18.3%Gross profit 705.8 805.0 14.0% 748.5 -7.0% 855.4 14.3%Net prof it 549.5 651.7 18.6% 596.0 -8.5% 681.6 14.4%

ROE 16.4% 17.6% 15.2% 16.4% Price change: 1 month 6.8%P/E 19.5 16.4 17.9 15.7 Price change: 6 month 35.0%P/BV 3.0 2.8 2.7 2.5 Price change: 12 month 39.4%D/PS 20.5 27.5 32.6 29.8 Max (52 w eek) 835.0Dyield (%) 2.5 3.3 4.0 3.6 Min (52 w eek) 540.0

ING BSK (Hold)Current price: PLN 822 Target price: PLN 857.2

500

550

600

650

700

750

800

850

2006-01-30 2006-05-30 2006-09-30 2007-01-30

ING BSK WIG

We are downgrading our rating on ING BSK to account for the appreciation in market price. The bank will release its Q4’06 earnings results on February 15th, and we will re-vise our valuation accordingly. ING BSK has broad exposure to the corporate banking market, and is therefore well-positioned to leverage the upcoming upswing in corporate borrowing (corporate debt in the banking sector was up 13% YoY at FY2006 year-end). FY2007 performance will be driven by the interest rate cut on ING BSK’s most popular savings account product, the Otwarte Konto Oszczędnościowe (since January 15th), which will boost the bank’s net interest margin and income. The product has a large share in total liabilities (ca. 1/3 of interest-bearing liabilities), it might have a positive long-term effect on ING BSK's financial performance. Deposit interest rate cut On 15th January 2007 ING BSK reduced its deposit interest rates. The cuts mainly regard the most popular savings accounts: the “OKO” for retail clients and “Zysk” for SMEs. They are not very deep, and account for 0.25 ppt. At the end of Q3’06, ING BSK managed 820,000 OKO accounts. The value of all retail savings accounts was PLN 14104 billion, including PLN 12.53bn generated by OKO. The value of ING BSK’s interest-bearing liabilities at the end of Q3’06 was PLN 42.054bn, of which almost 83% came from deposits. The share of retail savings accounts in total deposits was a little over 40%. Retail savings accounts make for one-third of ING BSK’s total interest-bearing liabilities. If the interest expense incurred on the savings ac-count portfolio is cut by 25bps, the interest expense on the total portfolio of interest-bearing li-abilities will fall by a little over 8bps. There are a few explanations for the interest rate cut: either ING BSK wants to expand and sustain its margins, or, the cut is a temporary measure designed to help finance another promotional campaign with raised interest rates on term deposits. This impact of this news for the full-year performance will be positive to neutral, but will boost the Q1’07 profit. The deposit interest rate cut is not so deep as to cause clients to leave, but, given the large volume, will drive ING BSK’s interest margin. 146,000 new accounts ING BSK managed to acquire 146,0000 new savings accounts thanks to its promotional cam-paign. The campaign was conducted on two levels: existing clients received cash rewards for bringing in new accounts, while the bank was running a parallel advertising campaign. The latter proved more effective than the clients. The bank admitted that its main objective for Retail was to acquire new accounts. This approach, paired with the lack of a major success in retail lend-ing, led to a below-market average growth in the loan portfolio. Now, as the bank steps up its corporate financing offer, there is a chance for improvement. Rating upgrade Fitch Ratings upgraded the rating for ING BSK to AA- from A+. This is a result of the recent upgrade for Poland on its foreign-currency issuer default rating.

BRE Bank Securities

5 February 2007 18

Monthly Report BRE Bank Securities

10

13

16

19

22

25

2006-01-30 2006-05-30 2006-09-30 2007-01-30

Kredyt Bank WIG

Analyst: Marta Jeżewska011 Last Recommendation: 2007-01-09(PLN m) 2005 2006F change 2007F change 2008F change Basic data (PLN m)Net interest income 753.4 772.8 2.6% 887.9 14.9% 1 002.5 12.9% Number of shares (m) 271.7Interest margin 3.6% 3.5% 3.8% 4.0% MC (current price) 5 704.8Revenue f/banking oper. 1 208.9 1 176.3 -2.7% 1 347.0 14.5% 1 499.8 11.3% Free float 14.5%Operating profit 329.3 435.7 32.3% 423.9 -2.7% 538.2 27.0%Gross profit 321.4 457.6 42.4% 362.2 -20.8% 464.6 28.3%Net prof it 415.9 440.1 5.8% 293.3 -33.4% 376.3 28.3%

ROE 26.0% 23.5% 13.6% 15.8% Price change: 1 month -4.8%P/E 13.7 13.0 19.4 15.2 Price change: 6 month 35.0%P/BV 3.4 2.8 2.5 2.3 Price change: 12 month 47.9%D/PS 0.0 0.2 0.4 0.4 Max (52 w eek) 24.2Dyield (%) 0.0 1.0 1.9 1.8 Min (52 w eek) 14.0

Kredyt Bank (Hold)Current price: PLN 21 Target price: PLN 21.7

We are reiterating our HOLD rating on Kredyt Bank’s stock, which has not moved since our last Research. The Q4’06 earnings report, scheduled for release on February 16th, might give an upward push to the market price. Our Q4 net income estimate of PLN 54m does not factor in one-offs such as provision reversals or deferred tax asset recognitions which add to the reported earnings figures. The sales successes achieved in FY2006 will continue this year, and commitment to fulfilling the FY2007 earnings guidance will drive valuation. 2007 will also be another year of market share rebuilding for Kredyt Bank. Af-ter a period of restructuring and start of network enlargement in 2006, income will in-crease on the back of improved volumes. Retail still the main source of income Kredyt Bank’s market share is ca. 4%. KBC has set an ambitious target of 9%, which will be difficult to achieve through organic growth. One way to advance those efforts would be to ac-quire the Mini-BPH,” but KBC stays silent on any speculations to that effect. The plan is to in-crease market share by strengthening positioning in selected segments of Retail Banking. The priorities include mortgage loans, investment funds, and credit cards. The partnership with Warta will also help in expanding market share. Kredyt Ban’s VP Bohdan Mierzwiński confirms that Retail will remain the main source of income for the bank even as other business segments are developed. He hopes to achieve an improvement in FY2007 in sales of mortgage loans (over PLN 2 billion) and investment funds (assets now exceed PLN 3bn, including PLN 1.24bn generates last year). FY2006 showed that, after a period of restructuring and rebranding, Kredyt Bank started to acquire new accounts and increase sales volumes. FY2007 will bring the first effects of those efforts. We expect a considerable improvement in recurring operating income before provisions, achieved on the bank of robust income growth and thanks to the fact that the sales network enlargement is financed from savings on the old cost base (ensuring moderate increase in expenses). This is in line with our predictions.

BRE Bank Securities

5 February 2007 19

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska16 Last Recommendation: 2007-02-05(PLN m) 2005 2006F change 2007F change 2008F change Basic data (PLN m)Net interest income 480.1 650.5 35.5% 762.5 17.2% 922.2 20.9% Number of shares (m) 849.2Interest margin 2.3% 2.8% 2.9% 3.0% MC (current price) 9 850.5Revenue f/banking oper. 1 465.3 1 253.1 -14.5% 1 534.7 22.5% 1 866.3 21.6% Free float 34.5%Operating profit 704.8 409.4 -41.9% 546.2 33.4% 738.1 35.2%Gross profit 709.7 370.8 -47.8% 458.5 23.7% 623.9 36.1%Net prof it 567.1 300.8 -47.0% 371.4 23.5% 505.3 36.1%

ROE 25.9% 13.1% 15.9% 19.4% Price change: 1 month 39.9%P/E 17.4 32.7 26.5 19.5 Price change: 6 month 93.3%P/BV 4.1 4.4 4.0 3.6 Price change: 12 month 96.6%D/PS 0.3 0.5 0.2 0.2 Max (52 w eek) 11.6Dyield (%) 2.4 4.7 1.5 1.8 Min (52 w eek) 5.3

Millennium (Reduce)Current price: PLN 11.6 Target price: PLN 9.9

4

6

8

10

12

2006-01-30 2006-05-30 2006-09-30 2007-01-30

MILLENNIUM WIG

Investor reaction to Millennium’s Q4’06 earnings report more than factored in the strong performance. We believe that the stock already prices in the high net-income expecta-tions for the years ahead (‘09/06 CAGR at 31%), even despite the inevitable increase in costs related to network expansion. The ’06 P/E is 32.2, and the FY2007 estimate is 26.1 (in spite of expected 23.5% in FY2007 net income). The Q1’07 earnings will reflect sea-sonal weakness in the banking industry relative to Q4’06 (the Christmas shopping sea-son is always the best time for banks), the bank’s growing network expenses, and weaker performance by the brokerage business (no handling of transactions related to reduction by BCP of its interests in Millennium). We are downgrading our rating on Mil-lennium from Hold to REDUCE. We expect to see an improvement in the coming quarters which, however, has already been discounted in the stock price. 4Q 2006 results – above consensus Millennium’s Q4’06 bottom line of PLN 89m beat both our expectations (PLN 76m) and the ana-lysts’ consensus (PAP: PLN 74m; Parkiet PLN 71m). The net profit figure was generated based on the group’s recurring income streams. The highlight of the Q4 earnings figures was fee in-come at PLN 114m, beyond our expectations and the consensus (between PLN 93m and 97m). The robust increase in recurring banking income more than offset the additional expansion costs. Total costs were higher than expected (PLN 257m vs. our est. PLN 216m and PAP con-sensus of PLN 225m). We were very impressed with Millennium’s fourth-quarter performance, especially the stellar fee income figure and revised upward our financial projections for the bank for the years ahead. For more information, refer to our analytical research on Millennium of 29 February 2007. Brain drain PR News portal said that a large group of transaction banking experts from BPH are soon going to transfer to Millennium. Millennium will set up a Transaction Banking Department within its Corporate Banking Division. This is good news for Millennium, neutral to the sale of the “mini-BPH,” and not so good for the “Enlarged Pekao.” The mini-BPH would not be able to retain those experts anyway, and, after all, all corporate centers are being transferred to Pekao. The Enlarged Pekao could have problems integrating the corporate segment, especially considering that it has been one of BPH’s main strengths. Unfortunately, that strength was largely derived from the human capital. There had been talk before that Millennium took advantage of the un-certain situation of BPH’s employees and solicited their mortgage loan consultants aside from the mortgage loan-driven retail segment. Development of corporate banking which, so far, has not been wildly successful, could bring Millennium stability and mitigation of the risks entailed in relying on just one product. Aiming to beat the market Millennium’s factoring sales in FY2006 increased by 123% (YoY). The bank purchased debt worth over PLN 1.4bn. Its representatives estimate that the factoring market will grow 30% an-nually and Millennium wants to go faster than that. Millennium’s market share is currently 7%. Its factoring business accelerated after the incorporation of the subsidiary Forin which boosted cross sell. The sales network has been enlarged, and the number of account managers has increased by 70%. If Millennium manages to expand the segment of its business targeted to corporate accounts (mainly SMEs), its income stream will be steadier . We believe that the sec-ond pillar like corporate services would be a good move on the bank’s part. Mortgage loan sales go hand in hand with market growth Millennium wants to up its FY2006 mortgage loan sales figure in FY2007. Its goal is to achieve

BRE Bank Securities

5 February 2007 20

Monthly Report BRE Bank Securities

growth in line with the markets. The bank hopes to generate PLN 1 billion on average per quar-ter, and scale up the overall mortgage loan portfolio to PLN 10bn by the end of the year. Millen-nium will therefore focus on retaining its position. According to estimates, sales of mortgage loans across the banking sector will increase by 30%-40%. The share of zloty mortgage loans in total sales is on the rise while, in January, it was eight percent, by December, it surged to 35%. Millennium’s representatives believe that the sales structure will be retained in 2007, with an over-30% share of zloty loans. The bank’s sales estimates are close to what has recently been announced by the Polish Banks’ Association (it was determined that banks extended PLN 41bn-worth of mortgage loans in 2006, and, in 2007, that number is expected to reach PLN 55bn, which means that sales will rise 34%). Millennium’s plans are in line with our estimates for its mortgage lending business. We assume that the loan portfolio at the end of 2007 will be worth PLN 10.5bn. Sale of NPLs As promised, Millennium signed an agreement to sell its past-due receivables to the securitiza-tion fund “Bison Niestandaryzowany Sekurytyzacyjny Fundusz Inwestycyjny Zamknięty” man-aged by BPH TFI. The total value of the NPLs is PLN 541.6bn. The price was not disclosed. Its estimated impact on net profit will be PLN 6.9m. The bank had announced earlier that it was going to sell approximately PLN 500m-worth of bad loans by the end of Q1 2007. We did not include that sale in our FY2007 projections, which include a net profit estimate of PLN 371m. If we factor in the NPL sale in bottom line estimates, the implied net profit is PLN 378m, and PLN 6.9m accounts for 1.8% of that amount. Assuming that the bank pays out 48% of its consoli-dated profit as dividends to shareholders, PLN 6.9m added to net profit makes for less than PLN 0.01 per dividend. Accordingly, the sale will not have a big impact on the bank’s FY2007 earnings. This is in line with our expectations. that Millennium would sell its bad loans for the purposes of reorganizing its bad debt, not for profit. For more information on our valuation of Millennium, refer to our October 26th, 2006 Research.

BRE Bank Securities

5 February 2007 21

Monthly Report BRE Bank Securities

130

160

190

220

250

280

2006-01-30 2006-05-30 2006-09-30 2007-01-30

Pekao WIG

Analyst: Marta Jeżewska016 Last Recommendation: 2007-02-05(PLN m) 2005 2006F change 2007F change 2008F change Basic data (PLN m)Net interest income 2 350.4 2 344.5 -0.3% 2 612.8 11.4% 2 816.7 7.8% Number of shares (m) 166.8Interest margin 3.9% 3.5% 3.6% 3.7% MC (current price) 43 370.1Revenue f/banking oper. 4 342.3 4 567.1 5.2% 5 011.9 9.7% 5 440.1 8.5% Free float 43.1%Operating profit 2 066.9 2 330.3 12.7% 2 694.5 15.6% 3 042.4 12.9%Gross profit 1 873.6 2 205.5 17.7% 2 550.0 15.6% 2 876.2 12.8%Net prof it 1 537.7 1 794.5 16.7% 2 065.5 15.1% 2 329.7 12.8%

ROE 18.7% 20.7% 22.2% 23.4% Price change: 1 month 10.6%P/E 28.1 24.2 21.0 18.6 Price change: 6 month 34.4%P/BV 5.1 4.8 4.5 4.2 Price change: 12 month 52.9%D/PS 7.4 8.6 9.9 11.2 Max (52 w eek) 260.0Dyield (%) 2.8 3.3 3.8 4.3 Min (52 w eek) 159.5

Current price: PLN 260 Target price: PLN 237.6Pekao (Hold)

It seems like our postulate that Pekao is a more attractive investment than PKO BP is proving correct. Because Pekao’s market price has appreciated over 16% since January 9th, we are downgrading our rating from Accumulate to HOLD. We believe that the stock already prices in the expected benefits of the upcoming merger with BPH. We expect the merger factor to continue to reflect positively in Pekao as the bank fills us in on further merger details (possibly on he occasion of the Q4’06 report release on February 21st). We might revise our valuation on a good news flow. Looking at the current price, we rec-ommend to hold positions in Pekao’s securities.

BRE Bank Securities

5 February 2007 22

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska016 Last Recommendation: 2007-01-09

(PLN m) 2005 2006F change 2007F change 2008F change Basic data (PLN m)Net interest income 3 544.5 3 791.7 7.0% 4 285.7 13.0% 4 801.5 12.0% Number of shares (m) 1 000.0Interest margin 4.0% 3.9% 4.1% 4.3% MC (current price) 48 080.0Revenue f/banking oper. 5 699.1 6 050.2 6.2% 6 854.2 13.3% 7 687.1 12.2% Free float 43.1%Operating profit 2 304.6 2 725.0 18.2% 3 297.0 21.0% 3 844.2 16.6%Gross profit 2 167.0 2 678.2 23.6% 2 986.0 11.5% 3 473.5 16.3%Net prof it 1 734.8 2 101.7 21.2% 2 337.6 11.2% 2 716.2 16.2%

ROE 19.7% 22.3% 21.7% 22.3% Price change: 1 month 1.0%P/E 27.7 22.9 20.6 17.7 Price change: 6 month 25.2%P/BV 5.5 4.8 4.2 4.0 Price change: 12 month 48.4%D/PS 1.0 0.8 1.0 1.1 Max (52 w eek) 49.5Dyield (%) 2.1 1.7 2.0 2.2 Min (52 w eek) 31.3

PKO BP (Reduce)Current price: PLN 48.1 Target price: PLN 41.6

25

30

35

40

45

50

2006-01-30 2006-05-30 2006-09-30 2007-01-30

PKO BP WIG

In light of the continuing lack of decisions regarding the incomplete Management Board lineup, we are reiterating our REDUCE rating on PKO BP’s stock. The strong momentum in the Retail segment will drive income in the quarters ahead, but the persisting decision-making and innovation deadlock causes the bank to lose its edge over competition. We see the biggest threat to PKO BP’s business not in the enlargement of Pekao, but rather in the increasingly aggressive and dynamic growth of its smaller rivals. Resignation by VP Jacek Obłękowski, who was in charge of Retail, PKO BP’s main strength, added fur-ther to the general indecision. The fact that the Management Board only has three mem-bers (+acting CEO Marek Głuchowski, Chairman of PKO BP's Supervisory Board), the unfilled CEO spot, the incomplete Supervisory Board lineup, and the postponement of new Strategy announcement from Q1’07 to Q2’07 all make for a bad news flow. That is why, even if the bank posts better-than-expected Q4’06 earnings results, investing in PKO BP as a mid-term investment is very risky. Supervisory Board fails to nominate CEO and VPs PKO BP’s Supervisory Board did not manage to elect a new CEO and two vice-presidents, and suspended the recruitment process until further notice. The reason was resignation by Jacek Osiatyński from his function as Supervisory Board member, after which the Board had no quo-rum to vote. Now, PKO BP has to call an Extraordinary General Meeting to complete the Super-visory Board lineup to give it power to elect the CEO and VPs. It was announced that the proce-dures will last until the beginning of May. This means that the bank will remain without leader-ship at least for another month. Jacek Obłękowski resigns as VP Mr. Obłękowski was responsible for Retail, PKO BP’s key line of business. He did not anoint a replacement. Him stepping down is a threat to PKO BP’s business. Because a new CEO and VPs cannot be nominated before the Supervisory Board once again works in its statutory lineup, the persistent indecision might affect the bank’s performance in the medium term. The Manage-ment Board is left with three members: Wojciech Kwiatkowski, Rafał Juszczak, and Zbigniew Sokal. Marek Głuchowski, Chairman of PKO BP’s Supervisory Board, will work as acting CEO until April 10th. Request to the KNB to approve Mr. Juszczak as MB member As expected, after the last Management Board member who had approval of the Commission for Banking Supervision (KNB) left the bank on January 1st, the Supervisory Board filed a re-quest with the KNB to issue a similar approval for Rafał Juszczak. New Strategy announcement A while ago, PKO BP announced that it was preparing a new strategy plan spanning a longer horizon than the strategy currently in force. The full Strategy was supposed to be revealed in late first quarter, preceded by an unveiling of the general strategic outline at the beginning of the year. But no such announcements have taken place so far, although acting CEO Marek Głu-chowski promised that the Strategy work is a priority task for the bank, and that the new CEO would reveal the details in Q2’07. This is only a small delay relative to the original promises, but we would not be surprised if the Strategy announcement was postponed further due to the pro-longed management instability. Mortgage loans – sales up at least 20% PKO BP is hoping to step up sales by at least 20% in 2007. Last year’s sales amounted to PLN 11 billion. The mortgage loan portfolio is supposed to grow at a two-digit rate. One competitive

BRE Bank Securities

5 February 2007 23

Monthly Report BRE Bank Securities

advantage will be the agreement that PKO BP signed with Bank Gospodarstwa Krajowego con-cerning government-subsidized interest payments on mortgage loans provided for in the new laws on supporting families in buying homes. PKO BP hopes to underwrite at least PLN 1.5bn in such loans. Last year, sales were up 45%, and the portfolio rose by over 20%. At the end of Q3’06, the gross value of the bank’s mortgage loan portfolio stood at PLN 21.1bn, compared with PLN 16.8bn at the end of FY2005 (a 25.6% increase in nine months, PLN 4.3bn change). At that time, PKO BP declared loan sales growth at a rate twice as high as portfolio growth. The reasons included early repayments of the mortgage loans (meaning the new portfolio), the cli-ents switching to other banks, and the regular loan payments (the older the loan, the more in-clined the borrowers were to choose shorter payment terms). This year, PKO BP’s target is to sell at least PLN 13 billion in loans. The two-digit growth rate will be sustained on the portfolio, but the increasing reference figures will lead to slower growth. We believe, however, that PKO BP will achieve this goal due to its market position, which will be strong until the good economic situation continues (not very likely to change). Therefore, it is hard to be pessimistic about it. FY2006 profit distribution Paweł Szałamacha, Vice-Treasury Minister, announced that the payout ratio from the FY2006 income will be close to last year’s, when PKO BP paid out 47.71% of its standalone net profit (a little over 46% of consolidated profit) to its shareholders. The dividend announcement is in line with our expectations. If we assume that net profit will be reported at PLN 2.1bn, this means PLN 0.97/share. As profit is expected to have gained over 21% YoY, dividends will be equally higher. Since the statement by the Vice-Treasury Minister was in line with our expectations, there is no need for us to revise our projections. PKO TFI PKO TFI recorded PLN 3.3bn inflows last year. An acceleration came in the fourth quarter when funds collected PLN 1.56bn vs. PLN 1.78bn in the first nine months 2006. The transfer of PKO BP’s deposits to investment funds might have been partly responsible for that success. At the end of September, PKO BP’s deposit accounts were worth PLN 82bn, including PLN 55.4bn in retail accounts. To advance sales, the new CEO decided to start a campaign to persuade more clients to transfer their deposits to investment funds, and to enlarge the network of fund distribu-tors. PKO BP’s deposit base is indeed a right source of inflows for investment funds. However, we still do not know who will become the new CEO. We believe that PKO BP will be increasing investment fund share sales this year. Deposit transfers to funds may boost the fee income.

BRE Bank Securities

5 February 2007 24

Monthly Report BRE Bank Securities