london market review 2015 - health | aon 2012 2013 usd 108bn usd 81bn usd 44b 2014 usd n 39bn usd...

TRANSCRIPT

Aon Risk SolutionsAon Broking

Risk. Reinsurance. Human Resources.

London Market Review 2015Property and Casualty

Property & Casualty 3

Executive summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

International property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Metals industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 Pulp and paper industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Mining industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

U.S. property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

International casualty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

U.S. casualty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Product recall and contamination . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Hospital professional liability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Appendices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Natural disaster events

IUA London member markets

Lloyd’s syndicates

Contributors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

We categorise the London market for the purposes of this report as Lloyd’s of London (Lloyd’s) and the company market represented by the International Underwriting Association (IUA) .

For each of the sectors we have included supporting insurance market statistics and insight from a wide selection of industries and territories that have seen new developments or where London markets set lead terms. (This excludes UK retail risks.)

The objective of the report is to share market data and trend information that help insurance buyers accessing the London market make informed risk transfer and risk management decisions.

Contents

4 London Market Review 2015

Executive summary

2014–warmer, with light winds

The London property and casualty market enjoyed a second consecutive year where below average natural

catastrophe losses allowed most carriers to report strong financial results for 2014, even

in the context of often brutal competition in the property insurance sector.

Insured natural catastrophe losses during 2014 were USD 39 billion, set against a ten-year average of USD

63 billion. Globally 2014 was the warmest year since records began in 1880, a timely reminder of the longer

term trend of increased natural catastrophe events linked to climate change.

Total insured natural catastrope losses

Source: Aon Benfield

When natural catastrophe losses are below the median, the London market–Lloyd’s syndicates in particular–tend

to post better than global peer group loss ratios. 2014 was a case in point.

This helped London underwriters successfully compete and retain market share, when rates for many territories

and industrial risk classes are near or heading towards those seen at the end of the soft market of 1999–2001.

Reinsurer capital globally grew to USD 575 billion, including USD 62 billion of deployed alternative capacity–both

record highs. The size of natural catastrophe losses required to burn off enough capital to change the soft market

trend is therefore much greater.

Change in global reinsurer capital

2015 outlook–changeable

With market conditions event-dependent, it is difficult to accurately forecast the speed and direction of future

market trends. The most likely outcome for 2015 is Scenario 1– a soft market (with occasional short term rate

spikes and regional differences). However, many market commentators argue that Scenario 2 is becoming

more likely: a hard market due to climate change, and an uptick in geopolitical risk and a concern over a major

cyber terrorism event or health pandemic.

0

25

50

75

100

125

20122011 2013

USD 108bn USD

81bn USD 44b

2014

USD 39bnn

USD

$410B $340B $400B $470B

$455B

$505B

$540B

$575B

-17% 18%

18% -3% 11%

7% 6%

2007 2008 2009 2010 2011 2012 2013 Q3 2014

Property & Casualty 5

Global insurance market future scenarios

Broader policy terms A growing trend observed in 2014 and we expect to develop further in 2015, is the broadening of policy

coverage. Exclusions are being gradually loosened, and additional coverage extensions are often added

without charge. Rewording of cyber coverage buyback clauses is also occurring.

Increased appetite Emboldened by three good underwriting years, we have observed an increase in the London market’s

appetite for some of the higher risk sectors such as mining, metals, and pulp and paper. Specific

industry coverage is included in the report to analyse this trend.

Musical chairs

In the London casualty market a number of new carrier start–ups in the sector requiring underwriter talent

kicked off a round of musical chairs that is still playing. When all the underwriters are in their new seats

buyers can expect an increase in competition for their business.

Market consolidation

At the time of writing a new wave of carrier consolidation had commenced with the announcements of

XL’s purchase of Catlin, where scale is quoted as the principal reason for the deal, followed by news of

Fairfax’s offer for Brit. Further consolidation is expected as global players look to secure a larger London

market presence from limited options.

Luigi Sturani Head of Property, Casualty and Crisis Management

Mark Parker Chief Commercial Officer, Property, Casualty and Crisis Management

*Note major industry-specific loss experience changes would still move market terms for that specific industry sector

Scenario 1 Soft market (with occasional short-term rate spikes and regional differences) due to:

Annual natural catastrophe losses between USD 40 billion to USD 80 billion, with all these events:

1. Geopolitical risk level unchanged

2. World economy continues to grow at 3–4% annually

3. No significant change in average world wide risk loss levels*

Scenario 2 Hard market due to:

Natural catastrophe losses over USD 100 billion in an annual period, with one or more of the following events:

1. Major cyber terrorism event

2. Increased global conflict / religious war

3. Financial crisis (Greek euro exit / China property bubble)

4. Health pandemic / black swan

6 London Market Review 2015

2014 trends The international (non U.S.) sector of the London market provides insurance and reinsurance protection for companies located in over 200 countries. Consequently, high-level market trends should be applied to local factors, such as natural catastrophe events or regional industry cluster trends, for example hotels in the Caribbean or manufacturing in Asia.

There was increased competition for all classes of property risk during 2014, with over-capacity and the signing down of carrier participation stoking a softening market trend. Some countries and industry sector rates dropped to levels not seen since 1999–2001.

Even buyers with claims activity often secured small rate reductions, if a special case was made relating to the loss cause.

The London market has a heavy weighting towards natural catastrophe-exposed countries and the more complex industrial risks that often require large policy limits. This means the sector is more volatile than a general basket of property risks and the rate movements detailed in the table should be considered in this context.

Theoretical total London per risk capacity increased to USD 1. 9 billion, part of the global theoretical capacity of USD 4.8 billion per risk. The big difference, and a continuation of the trend kicked off in Spring 2013, is that both London and global carriers are being much more aggressive in using their per risk stamp capacity to protect and / or pursue market share.

International property

2014 and Q1 2015 premium rate changes

Country Loss free Loss active

Australia -10% to -25% flat to +5%

Brazil -5% to -15% +0% to +10%

Chile -10% to -20% +0% to +10%

China -5% to -10% +0% to +10%

Colombia 0% to -10% +10% to +15%

Europe (ex UK) -5% to -15% 0% to +15%

India -5% to -25% +5% to +10%

Indonesia -5% to -10% +5% to +15%

Israel -5% -20% +5% to +10%

Japan -5%to -15% +5 to +15%

Middle East 0% to -10% +5 to +25%

New Zealand -10% to -20% 0% +15%

Russia / CIS -5% to -10% +5% to +20%

South Africa -5%to -15% 0% to +5%

Taiwan -5%to -15% +10% to +15%

Turkey -5% to -20% +5% to +10%

Global programmes -5% to -25% -5% to +20%

Even buyers with claims activity often secured small rate reductions, if a special case was made relating to the cause of loss.

Property & Casualty 7

2015 outlook Asia Pacific Australian and New Zealand-domiciled companies with London market placements again secured some of the largest improvement in terms, tracking local market rate movements.

Despite thinner rates, the sector remained profitable for London due to the below average level of major risk and natural catastrophe losses.

Slower ecomomic growth and lower commodity prices for the many mining companies headquartered in Australia who use the London market, will mean lower ingoing business interruption values and consequently smaller base premiums in 2015.

Australian and New Zealand risk managers have historically blended local, regional and London / European market shares to manage their organisation’s interests over the market cycle. We expect this competitive dynamic to intensify unless the soft market trend changes.

The London market wrote new or increased shares on a number of Indonesian, Indian and Japanese risks in 2014 and we expect this trend to continue in 2015.

Europe, Middle East and Africa As premium volume for London’s traditional heavy industrial risks and global programmes with significant natural catastrophe exposure has shrunk, London underwriters and brokers have cast their eyes more widely to compete aggressively on EMEA-located business they had not prioritised in the past. We expect this to continue in 2015. The sector was profitable in 2014, with only two large natural catastrophe losses: flooding in Southeastern Europe in May 2014 which caused insured losses of USD 250.

million and storms during June 2014 across France and Germany which accounted for USD 3 billion of losses.

Economic sanctions imposed on Russia in Spring 2014, created uncertainty for brokers and underwriters with March and April inception dates. Once the new laws were understood there was a small reduction in the level of business transacted on Russian industrial property risks, with oil and gas companies most affected.

Africa and the Middle East are two regions with strong economic growth trajectories, and Aon observed double digit percentage premium growth to London in 2014. However, the region remains a challenge for London to grow market share because local markets compete aggressively where price is the principal differentiator. Where more holistic risk engineering and risk management packaged service are offered, deals involving London and European marketed are regularly closed.

Latin America Other than losses connected to the year-long drought in Brazil–estimated at USD 450 million–Latin America was free of major natural catastrophe losses in 2014, delivering a profitable year for both local and London markets.

Rates in Chile, Columbia and Peru showed the largest declines due to the link to natural catastrophe rates, which were already tracking lower in both the insurance and reinsurance markets. We expect this trend to continue in 2015.

The economies of Brazil and Argentina are slowing and will place pressure on buyers seeking to balance their total cost of risk strategy with local market and international security choices.

Sophisticated Latin American buyers with long-term London and European carrier relationships have targeted lower policy deductibles and long-term policy deals as well as rate reductions, to improve their total cost of risk positions with some success.

Year USD billion

Global 4.8

London 1.9

2015 theoretical international property market capacity (per risk)

8 London Market Review 2015

Many metals companies insure their mining (including refining if integrated) and smelting risks separately, because they secure better terms from the market due to the larger capacity and greater competition for standalone smelting risks, compared to combined mining and smelter placement options.

Hybrid Hybrid placements, where the smelter and mining risk are insured together but the below ground mining risk is reinsured separately into 1) a specialist market or 2) a captive insurance vehicle or 3) a standalone local market placement, are common. Some companies use a mix of all three strategies.

This section of the report covers refining and smelting risk on a standalone basis, or the parts of a hybrid placement left by carving out elements of mining risk. The mining section of this report covers stand-alone miners and integrated miners with combined placements.

2014 trends At the global metals industry level the sector enjoyed a year of below-average loss activity, under-pinned by below-median global natural catastrophe losses.

Within this trend there were some significant differences. In EMEA, risk loss claims for the steel industry were above average. The Middle East aluminium smelter industry also continued to be loss active. There were large individual losses in Latin America and the U.S., but they did not exceed the metal industry rolling average for these regions.

The diagram below outlines the average rate reduction for metals risks. (Made up from 95% steel / aluminium / copper / zinc producers / and 5% other metals).

While rates continue to trend downwards we have noted growing resistance to chase rates lower. Many of the traditional metal industry lead underwriters are now participating excess of the primary USD 10–50 million layers, as they believe rates are too cheap but wish to maintain client relationships, allowing specialist primary underwriters to compete for the first loss layer.

Metals industry

Metals industry combined PD / BI rate evolution

30%

Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

Q1 15

Pulp & paper All sectors

30%

Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

Q1 15

Metals All sectors

Source: Aon

Property & Casualty 9

2015 outlook The metals industry is quite difficult to forecast because unlike the mining sector where rates were ramped up by major losses in prior years and are still relatively high, rates for the metals sectors are at or near previous market cycle lows, but remain profitable at this level due to recent levels of loss activity. The question is how low will they go?

Competition We anticipate that competition in the sector will continue, but carriers will become much more selective regarding how they utilise their capacity. Some carriers will cut back participation or increasingly move to excess layer positions on loss active placements or those with below average risk management profiles. For the best, well-managed risks we expect market competition to increase.

Interwoven with the rating trend is a push by brokers to broaden policy coverage for their clients at minimal or zero cost, by loosening policy exclusions and / or adding or widening policy coverage extensions. This trend will continue and has historically been the forerunner to the end of the soft market cycle.

For further details on the steel and aluminium industries, please refer to the Aon 2015 report dedicated to the sector.

Rates for the metals sectors are at or near previous market cycle

lows, but remain profitable at this level due to recent levels of loss activity. The question is how low

will they go?

Interwoven with the rating trend is a push

by brokers to broaden policy coverage

for their clients at minimal or zero cost.

10 London Market Review 2015

2014 trends The pulp and paper sector sector is well served by London carriers due to the specialist underwriting knowledge required to write these complex property damage and business interruption risks. Black Liquor Recovery Boilers have a significant explosion potential and many plants are located in natural catastrophe zones.

Improving loss ratios Based on Aon data the loss experience for the pulp and paper industry in 2014 was below average, with no stand-out differences between the main producing countries in the northern hemisphere–Canada, the U.S. and Scandinavia–and their peers in Indonesia, China and Chile. Aon’s claim statistics indicate an improving trend in loss frequency and severity in the sector.

This can be partly explained by a lower level of natural catastrophe claims in the past three years, however, the underlying risk loss experience is also showing a down-ward trend, which suggests an improvement in risk man-agement and loss control within the industry.

The graph opposite outlines the market trend for pulp and paper rates. They reduced at a slightly faster rate than the property sector average and we saw this trend continue through 2014 into the first quarter of 2015.

2015 outlook Compared to other commodity sectors, the prices for pulp and paper products have been less volatile and ingoing values are forecast to be stable.

Many integrated paper and packaging companies have posted growth in volumes and revenues for 2014, which contrasts with most metals and mining companies.

This is significant because it indicates maintenance and capital expenditure budgets will not be reduced or possibly grow, which is a positive for the sector’s insurers and reinsurers.

We also expect to see pulp and paper companies from Canada, the U.S. and Scandinavia, to continue to use the London market for deductible buyback and captive protection placements as they attempt to manage their total cost of risk downwards through the market cycle.

Pulp and paper industry

Based on Aon data, the loss experience for the pulp and paper industry in 2014 was below average, with no stand-out differences between the main producing countries in the northern hemisphere—Canada, the U.S. and Scandinavia—and their peers in Indonesia, China and Chile.

Property & Casualty 11

Pulp and paper industry combined PD / BI rate evolution

30%

Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

Q1 15

Pulp & paper All sectors

30%

Q1 08 Q1 09 Q1 10 Q1 11 Q1 12 Q1 13 Q1 14

25%

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

Q1 15

Metals All sectors

Strong long-term relationships between clients and their lead insurer(s) are prevalent in the sector, and we expect London carriers with existing leading positions to maintain or attempt to grow market share.

Good relations Mutually beneficial business relationships between carriers and pulp and paper companies are the foundation for competitive terms in this sector due to the high hazard risk and the requirement for specialist sector underwriting and a focus on risk engineering. Strong long-term relationships between clients and their lead insurer(s) are prevalent in the sector, and we expect London carriers with existing leading positions to maintain or attempt to grow market share.

Source: Aon

12 London Market Review 2015

2014: fortune favoured the brave The big news from 2014 was the low level of mining industry claims, across all size mining risks, which based on Aon’s analysis, ran at a levels between 40–50% of the ten-year average. This is in contrast to the 2008–2012 period when the sector, delivered loss ratios of over 300%, resulting in withdrawals from the sector an associated reduction of capacity and tightening of policy coverage. Those brave carriers that stayed with the mining sector have seen their fortunes turn around, and enjoyed a bumper year.

In the 2014 mining section of this report we split out market commentary for 1) major global miners and 2) medium and junior miners, because high levels of loss activity in the first group and much lower loss ratios and capacity requirements from the second, have created two markedly different market dynamics to review.

We again review the two sectors separately as major differences in placement dynamics are at play. Carriers remain cautious towards the major miner sector, but are attracted by the premium pool and deductibles that are available. Some are seeking to grow market share, and a number of carriers have written mining risks in 2014 that they had declined in prior years.

Major global mining companies For the small group of major global mining companies that have large multi-territory operations and were also the source of the 2008–2012 claims, rates fell and available market capacity increased.

These companies have complex and often unique risk profiles and held differing objectives for their 2014 renewals. Some traded the rate reductions available for increased natural catastrophe limits, while others used premium savings to protect their captive insurers from elements of risks they had been forced to retain during the mining sectors’ recent hard market.

Despite the softening trend, lead mining carriers in London and Europe continued to maintain a disciplined approach to underwriting the sector, even in the face of increased competition.

2015 outlook The price of iron ore and copper has reduced significantly during the past 12 months, so ingoing business interruption values declared in 2015 are forecast to be lower than 2014. This will mean that total premium for the sector starts from a lower base and we anticipate that carriers will be resistant to rate reductions that further compounds this situation. If loss levels remain below average however, we expect the current rate reduction trend and the availability of wider policy coverage to continue.

The chart below shows global mining market capacity for different types of mining. This is very much a guide because natural catastrophe limits, and individual company risk profiles drive market capacity. This capacity is also qualified by the term “usable”–in other words capacity at a price that buyers are prepared to pay and providing the cover they require.

Mining industry

Global mining market capacity

“Usable” global per risk marketcapacity 2014 2015

Above ground / opencast mining USD 1.4 billion to USD 1.7 billion USD 1.8 billion to USD 2 billion

Below ground hard rock USD 300 million to USD 450 million USD 300 million to USD 550 million

Below ground soft rock / coal USD 100 million to USD 230 million USD 120 million to USD 250 million

Property & Casualty 13

Medium and junior miners While classified as medium and junior for underwriting purposes, companies in this category include many world-class mining companies that insure assets in access of USD 10 billion. For these organisations assets are often, but not exclusively, in a single country and as a group have not delivered to the insurance market the run of large losses that the global major companies have. Both insureds and insurers in this group have benefited from below average natural catastrophe losses and risk losses, with underwriters recording low loss ratios and buyers enjoying reduced insurance costs. 2014 was also a period when brokers sought to widen coverage and the following table includes some of the areas that experienced revised terms from prior renewals.

Policy coverage improvements

Areas of coverage improvement or sub-limit increases

Tailing dams Port blockage sub-limits

Interdependency Contingent business interruption

Flood definitions / exclusions Underground sub-limits

Civil unrest Cyber risks

U.S. and Canadian miners have enjoyed improved terms helped by soft market conditions in the general property market, where some carriers have looked to write mining risks to make up for lost premium volume in other industries.

For the mining hubs of Australia, South Africa and Latin America rate reductions and broader policy coverage was the norm for 2014 and for Q1–Q2 2015 renewal discussions this trend is continuing.

Saudi Arabia, as a growth country for the mining industry, was also popular. The absence of significant natural catastrophe exposures and well-managed risks attracted carriers looking to diversify and grow their portfolios.

Underground The underground coal mining sector has experienced a small uptick in usable capacity, but still requires participation from a large number of carriers to build a block of capacity over USD 100 million.

It is our expectation that this trend will gather pace, and significantly more underground risk capacity will become available from a blend of new and existing sources.

Gold While the sample pool is relatively small, it appears gold miners have been targeted as a preferred class by certain insurers and reinsurers. Significantly lower rates and wider policy coverage is available to those that exhibit high-quality risk management and a professional risk transfer approach.

Ebola For Europe, the Middle East and Africa terms and issues have often been country-specific. Miners in West African countries have had to manage Ebola outbreaks, and in most instances without insurance coverage for lost production. A range of new products arrived in the market after the event.

14 London Market Review 2015

2014 trends 2014 saw a rapid softening of the U.S. property market that had seen rates sustained in 2013 following Superstorm Sandy in late 2012.

A number of high-profile markets looked to hold ratings in the first quarter of 2014. However, it was apparent that the continued low interest rate environment, lack of catastrophe losses, and influx of new capital will inevitably lead to significant rate reductions. In fact, the largest U.S. catastrophe losses recorded in 2014 were 2.9 billion from severe weather events and associated flooding in the central U.S. and a cumulative drought effect of USD 1.5 billion across the U.S. as referenced in appendix 1, suggesting that there will be little downward pressure on ratings.

The London market not only matched the U.S. rate trend but recognised the importance of being even more competitive and the larger players frequently flexed their muscles in an attempt to squeeze the smaller market participants off placements and / or secure preferential signings. The table below details the average rate movement range per quarter, demonstrating the quickening pace of market softening as the year progressed.

2015 outlook Catastrophe treaties renewed on 1 January with significant double digit reductions; the outlook for 2015 sees little sign of a let-up in the downward rating cycle. The final months of 2014 certainly saw an increased drive for premium income to fill year-end budgets.

Barring a major earthquake, we see no immediate sign of any break in the sustained trend of further market softening. The majority of U.S. business renews in advance of the 2015 windstorm season and we predict double digit rate reductions. In the longer term we see perhaps only the occasional pauses in rate softening for large natural catastrophes similar to Sandy. However, it will probably take a mega catastrophe or series of events exceeding USD 100 billion to change the direction of the market. The total per risk capacity for U.S. natural perils is forecast to be slightly up in 2015 as noted in the table below.

U.S. property

Quarter and year Claims free Loss active

Q1 2014 0% to -5% +0% to +12.5%

Q2 2014 -5% to -10% 0% to +10%

Q3 2014 0% to -5% +0% to +12.5%

Q4 2014 -5% to -10% 0% to +10%

Q1 2015 -5% to -15% 0% to -5%

Q2 2015 -5% to -15% 0% to -5%

2014 / 2015 average quarterly rate changes

Catastrophe treaties renewed on 1 January with significant double digit reductions; the outlook for 2015 sees little sign of a let-up in the downward rating cycle.

Peril Total capacity per risk

London market capacity per risk

California Earthquake USD 600 million USD 225 million

Windstorm USD 1 billion USD 350 million

U.S. large risk sector capacity

Property & Casualty 15

London market edge Against a background of softening rating trends, the challenge for the London market is to remain “relevant” but to continue to be pro active to market changes.

Fortunately, London and European underwriters have also benefited from the lack of catastrophe events and enjoyed excellent results on their U.S. portfolios in 2014. Therefore, in addition to continually providing a high quality of service and security, London carriers are offering dedicated SPS (facility) solutions through Aon for the following industries:

• Real estate • Hospitality• Entertainment

These industry solutions stand alongside London carrier expertise in financial institutions, retail, railroads, and technology industries, all of which enjoy access to broad policy wordings, and the London market’s experienced claims service.

It is a unique feature of the London carrier and U.S. insured relationships that both enjoy a deep mutual understanding, built up over decades of trading together. This business empathy is built on annual dialogue, roadshow, or indeed at the unique Aon Miami Symposium.

Structured portfolio solutions and facilities The London market is offering a number of new Aon Structured Portfolio Solution options in 2015, one of the most in demand products has been a new homeowners Aon Flood Facility developed between our London team and Aon Affinity.

Also available from the London market are a wide range of dedicated U.S. facilities including mortgage impairment products and a number of creative and competitively priced deductible buyback products.

During the soft market U.S. buyers are challenging London to create compelling reasons to continue placing business there, and to date the market has risen to the call with a larger and more tailored range of risk transfer products and solutions.

16 London Market Review 2015

2014 trends There were interesting developments and outcomes for the 2014 year within the international casualty market. Throughout the period we heard commentary from carriers about the squeeze on margin associated with increased overheads and claims cost and low investment returns.

There was further talk of changes to reinsurance treaties putting further pressure on direct writers. But international casualty market results remained positive to the extent that the sector looked an attractive zone to enter or expand into as part of a wider portfolio.

We observed new carriers coming in and an expansion of long-standing writers of other segments spreading across the liability market.

This led to an unprecedented need for experienced talent to staff up the new portfolio opportunities and there followed a flurry of underwriters moving from one organisation to another.

Clearly the new participants arriving with fresh ideas, new concepts and exciting business plans needed to be fed and driven forward. For the established carriers losing their talent, it became a time to rebuild teams with new people and to maintain current portfolios, while seeking to develop new business.

This was all very good news for clients and a very new situation to that observed in this market segment over the preceding years.

Competition increased not only between the London markets, but also with local market expansions and competitive drive. Premium reductions and positioning varied according to risk type, quality and the usual factors, but on average rate on line reductions in the order of 5% to 10% were noted.

Long-term agreements were offered and innovation on coverage, scope and product offering climbed high on both buyers’ and underwriters’ agendas.

International casualty

Country Loss free Loss active

Global programmes -5% to -10% +5 to +20%

Australia -5% to -10% +10 to +20%

Canada -5% to -10% +5 to +25%

EMEA -5% to -10% +10 to +30%

Rest of the world -5% to -10% +5 to +15%

2014 rate change range

Property & Casualty 17

2015 outlook At the time of writing we see a continuation of the trend that opened 2015. Senior underwriters who have moved have not yet arrived at their new offices and plans are therefore yet to be executed. Further underwriter moves are ongoing and more to come likely.

Capacity continues to expand, as does the challenge presented by new and expanding markets to the current writers. The reinsurance market overall has been favourable to the direct liability market and we see and hear of greater flexibility in coverage on offer for reinsurance treaties, offering benefits to our direct clients.

We see an additional USD 75 million of capacity entering the market contributing to what was probably USD 75 million to 100 million of new and expansionist capacity in 2014.

This additional capacity has also come to the fore with the movement of experienced underwriters and a notable expansion of lead markets in the segment. There is greater flexibility towards offering global capacity, including U.S. domestic risk, and more markets offering combined onshore and offshore energy liability coverage. Construction capacity will remain strong and competitive. We have seen good continued growth in this sector and expect this trend to continue.

Our premium rate expectations are for a reduction of 5–10%. We believe 2015 will be an exciting year in the international casualty sector. Major buyers in Australia, Canada and Latin America can expect to see some improvement in coverage even in more challenging industries such as oil and gas, and mining and power, where the potential for sizeable casualty claims exists.

Year Capacity

2014 USD 2 billion

2015 USD 2.2 billion

International casualty total London market capacity

18 London Market Review 2015

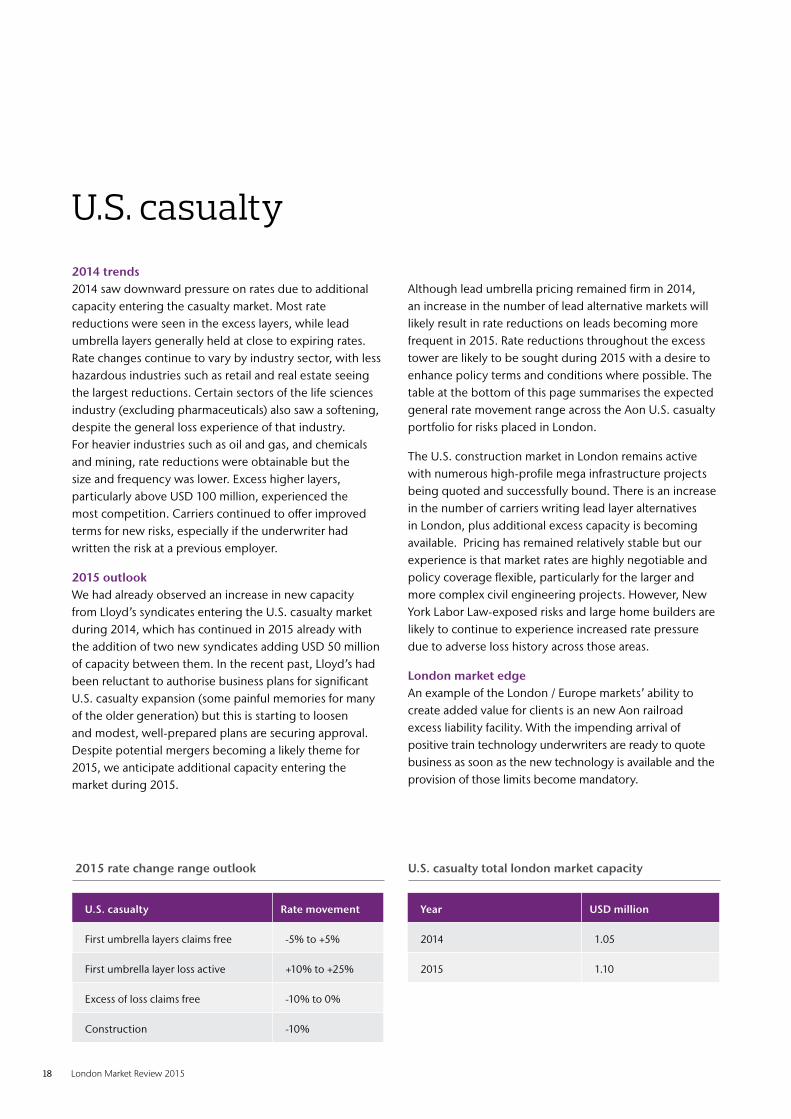

2014 trends 2014 saw downward pressure on rates due to additional capacity entering the casualty market. Most rate reductions were seen in the excess layers, while lead umbrella layers generally held at close to expiring rates. Rate changes continue to vary by industry sector, with less hazardous industries such as retail and real estate seeing the largest reductions. Certain sectors of the life sciences industry (excluding pharmaceuticals) also saw a softening, despite the general loss experience of that industry. For heavier industries such as oil and gas, and chemicals and mining, rate reductions were obtainable but the size and frequency was lower. Excess higher layers, particularly above USD 100 million, experienced the most competition. Carriers continued to offer improved terms for new risks, especially if the underwriter had written the risk at a previous employer.

2015 outlook We had already observed an increase in new capacity from Lloyd’s syndicates entering the U.S. casualty market during 2014, which has continued in 2015 already with the addition of two new syndicates adding USD 50 million of capacity between them. In the recent past, Lloyd’s had been reluctant to authorise business plans for significant U.S. casualty expansion (some painful memories for many of the older generation) but this is starting to loosen and modest, well-prepared plans are securing approval. Despite potential mergers becoming a likely theme for 2015, we anticipate additional capacity entering the market during 2015.

Although lead umbrella pricing remained firm in 2014, an increase in the number of lead alternative markets will likely result in rate reductions on leads becoming more frequent in 2015. Rate reductions throughout the excess tower are likely to be sought during 2015 with a desire to enhance policy terms and conditions where possible. The table at the bottom of this page summarises the expected general rate movement range across the Aon U.S. casualty portfolio for risks placed in London.

The U.S. construction market in London remains active with numerous high-profile mega infrastructure projects being quoted and successfully bound. There is an increase in the number of carriers writing lead layer alternatives in London, plus additional excess capacity is becoming available. Pricing has remained relatively stable but our experience is that market rates are highly negotiable and policy coverage flexible, particularly for the larger and more complex civil engineering projects. However, New York Labor Law-exposed risks and large home builders are likely to continue to experience increased rate pressure due to adverse loss history across those areas.

London market edge An example of the London / Europe markets’ ability to create added value for clients is an new Aon railroad excess liability facility. With the impending arrival of positive train technology underwriters are ready to quote business as soon as the new technology is available and the provision of those limits become mandatory.

U.S. casualty

U.S. casualty Rate movement

First umbrella layers claims free -5% to +5%

First umbrella layer loss active +10% to +25%

Excess of loss claims free -10% to 0%

Construction -10%

Year USD million

2014 1.05

2015 1.10

2015 rate change range outlook U.S. casualty total london market capacity

Property & Casualty 19

2014 trends Product recalls are on the increase and are becoming more costly across all industries and geographic regions.

The reasons behind this are tighter regulation, increased media attention and more stringent contractual obligations passing down the supply chain, as well as larger volume recalls.

Regulators are increasing random testing in an attempt to discover economically motivated adulteration of food and U.S. regulators have stepped up their inspections of food manufacturing facilities outside of the U.S. in respect of foreign companies exporting into the country.

New in 2014 is the enforcement of criminal prosecutions in the U.S. by the FDA and there are currently some very high profile cases going through the courts, including the Peanut Corporation of America and Wright Brothers.

London continues to be the leading market for product recall and contamination insurance, with a wide range of carriers and policy coverage options.

The table below shows the average rate change range per industry sector observed during 2014.

2015 outlook Capacity in the product recall market continues to grow with more innovation and solutions being developed by various London carriers each year.

Most companies involved in manufacturing a product will have a supply chain and attention will be required regarding their suppliers. Companies need to understand where their ingredients or components are coming from in order to protect their brand to avoid a costly recall.

As of 1 January, 2015, we saw new capacity entering the market on the non-food side of the business from two Lloyd’s syndicates.

A leading European reinsurers is developing a product tailored for food and drink manufacturing companies that will offer business interruption coverage but will not have the bodily injury or property damage requirement. This product is still in its infancy and the carrier is currently working with 3 or 4 clients as live test cases.

London market edge The London market leads the way in offering full product guarantee, financial loss and recall cover on both automotive components and other industry sectors.

With a number of claims and adverse publicity from food and drink product recalls due to contamination, the London market has continued to offer coverage. Smaller regional or country specific markets have reduced or withdrawn from the sector as they do not have the spread of risk to avoid local events delivering losses out of balance with the premiums written.

Product recall and contamination

Industry Capacity

Food and drink USD 300 million

Automotive components USD 100 million

Pharmaceutical contamination USD 25 million

Restaurant contamination USD 50 million

Water contamination USD 25 million

Consumer finished good products (varies by specific product) USD 100 million

London market product recall and contamination capacity

Industry Rate change range

Food and drink -10 to +10%

Automotive components -10 to 0%

Pharmaceutical contamination +10% to +20%

Restaurant contamination -5 to 0%

Water contamination 0 to -5%

Consumer finished good products (varies by specific product) +5 to 0%

London market 2014 and 2015 rate changes

20 London Market Review 2015

2014 trends There are now more markets with worldwide underwriting capabilities rather than simply a focus on either U.S. or non-U.S. business. However, there remains a significant group of carriers who have maintained this division.

The market remained soft with premiums reducing by between 5% and 20% year-on-year. Greater reductions on rate could be negotiated on accounts which demonstrated significant improvements in clinical and patient safety.

Meanwhile, the quality dashboard took a more influential weighting in the underwriting decision and has become a key part of discussions with clients during meetings or hospital tours.

The abundance of capacity has also influenced pricing, although many clients have remained loyal to carriers, keeping in mind the long-tail nature of hospital professional liability cases, and the general increase in claim severity and healthcare industry change.

Away from rating pressures, there has also been a softening of policy terms and conditions with attractive long-term agreement contracts of up to three years available. Such agreements provide companies with long-term coverage and pricing stability and also provide a hedge against future market hardening.

2015 outlook The outlook for 2015 is for the market to continue to soften. New carriers are looking to gain market share, while existing carriers are protecting their positions, helping to create increased competition.

As healthcare strategy evolves in each territory, London markets will continue to align hospital professional liability solutions to wider corporate objectives, such as premium that is correlated with quality improvements.

There are areas of emerging exposures in the hospital environment and it is likely there will be a push for greater integration of such coverages.

The value of the quality and patient safety clinical dashboard, which has become a key part of underwriting submissions, will grow in the eyes of insurers because if gives a prospective view for insurers and allows them the opportunity to negotiate more bespoke added value coverage and products for hospitals.

London markets are looking to diversify their portfolios by balancing large hospitals with allied groups, such as dentistry, primary care and mental health institutions. Additionally, markets are looking at developing portfolios in areas of high growth, particularly in Latin America and Asia.

Hospital professional liability

Year Rate movement

2014 -5% to 20%

2015 -5% to 20%

Year USD Million

2012 USD 200 Million

2013 USD 230 Million

2014 USD 250 Million

2015 USD 260 Million

2015 range rate change outlook London market capacity

Property & Casualty 21

London market edge The London market, in partnership with Aon, has developed a UK medical malpractice product which incorporates a range of coverage enhancements, preferential pricing and dedicated claims expertise targeted at small and medium-sized healthcare providers. The product is supported by two Lloyd’s syndicates offering diversification and the benefit of Lloyd’s security and general underwriting agreements.

London underwriters also offer a specialist product for the fertility and mental health segments of healthcare in the UK, both with a unique set of risk features. The market and Aon have crafted a broad policy form to provide coverage for supported by a specialist claims handling capability.

Healthcare Advantage is a London market product developed by Aon for allied healthcare professionals and providers in Canada. The solution provides a range of coverage lines, including medical malpractice, errors and omissions and general and cyber liability. This one-stop policy reduces the chances of coverage gaps and delivers cost synergies.

Greater reductions on rate could be negotiated

on accounts which demonstrated significant improvements in clinical

and patient safety.

There are areas of emerging exposures in

the hospital environment and it is likely there will

be a push for greater integration of such

coverages.

5% and 20%

The market remained soft with premiums

reducing by between

year on year.

22 London Market Review 2015

Appendices

Property & Casualty 23

Appendix 1–Natural disaster events

Date(s) Event Location Deaths Structures / claims Economic loss1 (USD)

Insured loss1 (USD)

September Flooding India, Pakistan 648 375,000 18 billion 700 million

October 12-14 Cyclone Hudhud India 68 200,000 11 billion 650 million

July 15-20 Typhoon Rammasun

China, Philippines, Vietnam 206 1,000,000 7.2 billion 300 million

Summer Drought China N/A N/A 5.2 billion 750 million

February 8-16 Winter weather Japan 95 288,000 5.0 billion 2.5 billion

May 13-21 Flooding Southeast Europe 86 150,000 4.5 billion 250 million

Year-long Drought Brazil N/A N/A 4.3 billion 450 million

June 18-20 Severe weather France, Germany 6 750,000 4.0 billion 3.0 billion

May 18-23 Severe weather United States 0 425,000 4.0 billion 2.9 billion

Year-long Drought United States N/A N/A 4.0 billion 1.5 billion

All Other Events 65 billion 26 billion

Totals 132 billion 39 billion

Date(s) Event Location Insured loss actual (USD)

Insured loss2 (2014 USD)

August 2005 Hurricane Katrina United States 66.9 billion 80.7 billion

March 11, 2011 EQ / tsunami Japan 35 billion 37.1 billion

October 2012 Hurricane Sandy U.S., Caribbean, Bahamas, Canada 30.2 billion 30.9 billion

August 1992 Hurricane Andrew U.S., Bahamas 15.7 billion 26.4 billion

January 17, 1994 Earthquake United States 15.3 billion 24.8 billion

Yearlong 2012 Drought United States 18 billion 18.8 billion

September 2008 Hurricane Ike United States 15.2 billion 16.5 billion

June–December 2011 Flooding Thailand 15.5 billion 16.3 billion

October 2005 Hurricane Wilma United States 12.5 billion 14.8 billion

February 22, 2011 Earthquake New Zealand 13.5 billion 14.5 billion

2014 Top 10 global economic and insured loss events

Top 10 costliest global insured loss events (1950–2014)1 Subject to change as loss estimates develop

2 Adjusted using U .S . Consumer Price Index (CPI)

24 London Market Review 2015

Appendix 2

Ace European Group Limited

AIG Europe Limited

Allianz Global Corporate Specialty AG

Allied World Assurance Company (Europe) Ltd

Arch Insurance Company (Europe) Ltd

Aspen Insurance UK Limited

Assicurazioni Generali S.p.A. (UK Branch)

AXA Corporate Solutions SA

Aviva Insurance Limited

Axis Specialty Europe Plc

Catlin Insurance Company (UK) Ltd

Chubb Insurance Company of Europe SE

CNA Insurance Company Limited

Endurance Worldwide Insurance Limited

Everest Reinsurance (Bermuda) Ltd

FARADAY Reinsurance Company Limited

General Reinsurance Company

Global Aerospace Underwriting Managers (GAUM)

Great Lakes Reinsurance (UK) Plc

Hannover Re SE

Houston Casualty Company London

International Insurance Company of Hannover SE

Lancashire Insurance Company (UK) Limited

Liberty Mutual Insurance Europe Limited

Markel International Insurance Company Limited

Munich Reinsurance Company

New India Assurance Company Limited

QBE Insurance (Europe) Ltd

Royal & Sun Alliance Insurance plc

SCOR UK Company Limited

Sirius International Insurance Corporation

Swiss Re Europe S.A, UK Branch

Swiss Re International SE, UK Branch

Tokio Marine Kiln Insurance Limited

Tokio Millennium Re (UK) Limited

Torus Insurance (UK) Ltd

Transatlantic Re

Trans Re London

Travelers Insurance Company

W R Berkley Insurance Europe Ltd

XL Re Ltd

XL Insurance Company

Zurich Insurance Plc

IUA London member markets

Property & Casualty 25

Appendix 3

Managing agent Syndicate

ACE Underwriting Agencies Limited 2488

Advent Underwriting Limited 0780

AEGIS Managing Agency Limited 1225

Allied World Managing Agency Limited 2232

Amlin Underwriting Limited 2001

Amlin Underwriting Limited 6106

AmTrust at Lloyd's Limited 0044

AmTrust at Lloyd's Limited 1206

Antares Managing Agency Limited 1274

ANV Syndicates Limited 0779

ANV Syndicates Limited 1861

ANV Syndicates Limited 1969

ANV Syndicates Limited 5820

Arch Underwriting at Lloyd's Ltd 2012

Argenta Syndicate Management Limited 1110

Argenta Syndicate Management Limited 2121

Argo Managing Agency Limited 1200

Ark Syndicate Management Limited 4020

Ark Syndicate Management Limited 6105

Ascot Underwriting Limited 1414

Aspen Managing Agency Limited 4711

Asta Managing Agency Limited 1897

Asta Managing Agency Limited 1910

Asta Managing Agency Limited 1945

Managing agent Syndicate

Asta Managing Agency Limited 2357

Asta Managing Agency Limited 2525

Asta Managing Agency Limited 2526

Asta Managing Agency Limited 4242

Atrium Underwriters Limited 0609

Barbican Managing Agency Limited 1955

Barbican Managing Agency Limited 6113

Beaufort Underwriting Agency Limited 0318

Beazley Furlonge Limited 0623

Beazley Furlonge Limited 2623

Beazley Furlonge Limited 3622

Beazley Furlonge Limited 3623

Beazley Furlonge Limited 6107

Brit Syndicates Limited 2987

Canopius Managing Agents Limited 0260

Canopius Managing Agents Limited 0958

Canopius Managing Agents Limited 4444

Canopius Managing Agents Limited 6115

Capita Managing Agency Limited 2255

Cathedral Underwriting Limited 2010

Cathedral Underwriting Limited 3010

Catlin Underwriting Agencies Limited 2003

Catlin Underwriting Agencies Limited 2088

Catlin Underwriting Agencies Limited 3002

Lloyd’s syndicates

26 London Market Review 2015

Managing agent Syndicate

Catlin Underwriting Agencies Limited 6111

Catlin Underwriting Agencies Limited 6112

Chaucer Syndicates Limited 1084

Chaucer Syndicates Limited 1176

Chubb Managing Agent Ltd 1882

ERS Syndicate Management Limited 0218

Faraday Underwriting Limited 0435

Hardy (Underwriting Agencies) Limited 0382

HCC Underwriting Agency Ltd 4141

Hiscox Syndicates Limited 0033

Hiscox Syndicates Limited 3624

Hiscox Syndicates Limited 6104

Liberty Syndicate Management Limited 4472

Managing Agency Partners Limited 2791

Managing Agency Partners Limited 6103

Markel Syndicate Management Limited 1400

Markel Syndicate Management Limited 3000

Marketform Managing Agency Limited 2468

Mitsui Sumitomo Insurance Underwriting at Lloyd's 3210

Montpelier at Lloyd's Limited 5151

Munich Re Underwriting Limited 0457

Navigators Underwriting Agency Limited 1221

Managing agent Syndicate

Newline Underwriting Management Limited 1218

Novae Syndicates Limited 2007

Pembroke Managing Agency Limited 4000

Pembroke Managing Agency Limited 6110

QBE Underwriting Limited 0386

QBE Underwriting Limited 2999

RenaissanceRe Syndicate Management Limited 1458

RJ Kiln & Co. Limited 0308

RJ Kiln & Co. Limited 0510

RJ Kiln & Co. Limited 0557

RJ Kiln & Co. Limited 1880

R&Q Managing Agency Limited 1991

S.A. Meacock & Company Limited 0727

Shelbourne Syndicate Services Limited 2008

Sportscover Underwriting Limited 3334

Starr Managing Agents Limited 1919

Talbot Underwriting Ltd 1183

The Channel Managing Agency Limited 2015

Torus Underwriting Management Limited 1301

Travelers Syndicate Management Limited 5000

W R Berkley Syndicate Management Limited 1967

XL London Market Ltd 1209

Lloyd’s syndicates (continued)

ContributorsU.S. property

Simon Methven+44 (0)20 7086 [email protected]

Paul Foreman+44 (0)20 7216 [email protected]

International property

Massimiliano Roveda+44 (0)20 7086 [email protected]

Jorge Artunduaga+44 (0)20 7086 [email protected]

Jamie Topping+44 (0)20 7086 [email protected]

U.S. casualty

Simon Good+44 (0)20 7086 [email protected]

U.S. casualty construction

Galen Brislane+1 441 595 [email protected]

International casualty

Richard Payne+44 (0)20 7216 [email protected]

Product recall & contamination

Kary Yates+44 (0)20 7086 [email protected]

Hospital professional risks

Will Barber+44 (0)20 7086 [email protected]

Mining & metals

Mark Parker+44 (0)20 7216 [email protected]

Mark Kettle+44 (0)20 7216 [email protected]

David Williams+44 (0)20 7086 [email protected]

Bruce Dettling+44 (0)20 7086 [email protected]

Craig Dowell+44 (0)20 7086 [email protected]

Pulp & paper

Julian Catmull+44 (0)20 7086 [email protected]

James Pash +44 (0)20 7086 2028 [email protected]

Please contact your local Aon office or any of the above for further copies of this report.

Risk. Reinsurance. Human Resources.

About Aon Aon plc (NYSE:AON) is a leading global provider

of risk management, insurance and reinsurance

brokerage, and human resources solutions and

outsourcing services . Through its more than

66,000 colleagues worldwide, Aon unites to

empower results for clients in over 120 countries

via innovative and effective risk and people

solutions and through industry-leading global

resources and technical expertise . Aon has been

named repeatedly as the world’s best broker, best

insurance intermediary, reinsurance intermediary,

captives manager and best employee benefits

consulting firm by multiple industry sources . Visit

www .aon .com for more information on Aon and

www .aon .com/manchesterunited to learn about

Aon’s global partnership with Manchester United .

© Aon plc 2015. All rights reserved.The information contained herein and the statements expressed

are of a general nature and are not intended to address the

circumstances of any particular individual or entity . Although

we endeavor to provide accurate and timely information and

use sources we consider reliable, there can be no guarantee that

such information is accurate as of the date it is received or that it

will continue to be accurate in the future .

No one should act on such information without appropriate

professional advice after a thorough examination of the

particular situation .

Aon UK Limited is authorised and regulated by the Financial

Conduct Authority .

FP 8831

www.aon.com