local economic assessments: our experience to date presentation by dr. nicholas j.o. miles, ghk...

TRANSCRIPT

Local Economic Assessments: Our Experience to Date

Presentation by

Dr. Nicholas J.O. Miles, GHK

Thursday the 29th of January

Newcastle University

Structure of the Presentation

Why we think that they are important

How we approached the task of completing an LEA

Outputs, Outcomes and Opportunities

(Possible ) Lessons from our Experience (Case Studies -Wolverhampton Local Economic Assessment December 2008; Tendring [Essex] and

Toronto, Canada).

“There is widespread recognition of the importance of regional, city and sub-regional specialisation to economic competitiveness. Comparative advantage is based on a number of factors including:

• place-specific increasing returns to scale;

• positive externalities generated by co-located activities; and

• increasing recognition of importance of region and city differentiation in production, and lifestyle factors.”

Source: Planning and Optimal Geographical Levels for Economic Decision Making – the Sub-Regional Role. UK Gov (BERA) March 2008

Local Economic Assessment:Releasing the Power of (local) Place?

The Power of Place

“Economic competencies are best built and integrated at the local level; Preferably at the lowest level of a viable functional economic area, be that a city-

region, a city or even a Local Authority. Which one is chosen is an empirical issue; evidence is required”

The Creative ‘Discovery’ District of Toronto – a key component of the Greater Toronto Area innovation ecosystem.

Discovery District Financial District Creative & Arts District

Gardiner Museum of Ceramic Art

Royal Ontario Museum

Women’s College

The MaRS CentreUHN Toronto GeneralHospital for Sick children

Entertainment District

Canadian Opera House

University of Toronto

UHN Princess MargaretMount Sinai

Art Gallery of Ontario

Royal Conservatory of Music

The Power of Place

LEAs.......are of increasing importance! (perhaps more so today than ever before)

For the Local Authority For its region

Fundamental to INTERVENTION – economic development

Important tool of engagement (and collaboration – creating a

‘communality of interests’)

Input to effective governance (‘institutional recomposition’)

A step towards / required for effective LAA – MAA – city-regions etc

Required for IRS etc

Needed in order to construct any form of EFFECTIVE ‘ask’ to RDA /

central government / PPPs – vital underpinning re funding strategy –

what is the most (cost) effective way to use (very) limited resources

.........and perhaps critical for:

UNDERSTANDING(Local Economic Assessment)

VISION / STRATEGY

IMPLEMENTATION

MONITOR / EVALUATE

•HOW - Structured? (sectors, clusters..etc)

•HOW - Works? (drivers; actors; reach...etc)

•HOW - Positioned*? (Benchmarking..etc)

•WHAT - Prospects? (SWOT/challenges/scenarios )

Engagement Partnership Leadership

* In regional, national and international markets / value networks

•Effective Support - LOCAL ECONOMY: Direct:

o Planning and regeneration (LDF...etc)o Procuremento Local lead markets

Indirect (support and nurture)o For profit sectoro Non for profit / social economy

•Effective - ‘GOVERNANCE’: Local partnerships (LPS - PPPs...etc) Cross LA working (LAA; MAA; City regions) Regional co-ordination (IRS etc) Cross national networking ‘Institutional re-composition’ (LAA; MAA; City regions; PPPs; [Triple Helix]..... ..etc)

BUT....Need a (Theoretical–Practical) Framework

Avoid ‘aimless’ collection of data – goes without saying (!?)

Search for drivers of change – and corresponding policy leverage

Need a way to ASSESS the local economy

Need a ‘yardstick’ – a common yardstick (issue of consistency within

e.g. IRS framework)

Start with an understanding of economic change

The logic of value creation + the character of competition HAS

CHANGED

Start with an Issues of (let’s take just three):– Globalisation: and the decomposition of production

Sunderland - Nissan Wolverhampton – Goodrich / United Technologies Tendring – Dormitory for the bankers! Farmers coping with CAP!

– Convergence: and the rise of new forms of wealth creation Emerging technologies are at the interface of trad disciplines + businesses. Distinction between manufacturing and services - blurred

– Commoditisation of activities: and the importance of HVA skills Corresponding heightening in importance of analytic skills and tacit

interactions Design - creativity – knowledge soaked economy Importance of innovation and building local innovation ecosystems

How does it stake up? Does if possess the competencies needed by today’s successful businesses (and social economy?)

Talent

Assets

Competencies

Governance

• Business leaders• Labour market skill sets

DYNAMIC:• Wealth producing• Knowledge producing(universities / colleges / innovation ‘ecosystem’)

STATIC:• Connectivity (transportation)• Built environment• Cultural ‘Objects’

A combination category - Places are the source of ‘competencies’ What is a place competent to do? Is the place noted for product creation? (e.g. Wolverhampton – Goodrich) Are its firms located in secure / defensible positions in global value networks? How could the area be branded?

• Role of: key actors PPPs LSPs Triple Helix

Useful categories to use in a LEA?• Successful businesses• Creative diversity

• Responsibility Assignment

Leveraging external collaborations

Business is changing – fast and furious – changing the way that wealth is generated – place is a variable – how can it respond?

One possible outcome of the local (joint) assessment

process - Tees Valley MAA / City Region

• A forward strategy for economic regeneration, with a clear programme of projects

• Supported by a detailed economic analysis of the City Region

• Included “asks” of Government “to help us achieve our ambitions”

• 3 main funding streams will implement the MAA Business Case:

Economic development / regeneration from One NorthEast

Transport from Regional Transport Board / DfT

Housing market renewal from Regional Housing Boards / CLG Leadership

• Global & NAFTA: Business not as usual; –understand changing context and role of city

• Off-shoring UP

• I nternational Competition UP

• Responses• Support selected Clusters

• Focus on ‘Creative City’ (exciting lives)

• Build compentencies and assets that HVA operations WANT. Attracting Talent

• New institutional arrangements for competitiveness (GTA, PPPs)– city facilitated, locally crafted - business driven• Toronto Financial Services Alliance

• Aerospace Action Partnership

• MaRS – creativity and innovation

• Playing on a bigger pitch: “In the research commercialisation arena, [MaRS] is the most exciting meeting place in the world”

The Greater Toronto RegionPositioning in the Global Economy-Building competencies

Also - Need to be (constructively) challenging:

Asking the hard and challenging questions

Getting people to think differently; highlighting hidden opportunities

‘Wood for trees – trees for wood’ issue

Combing external and internal viewpoints: “The core evidence base made a difference to how we think in Knowsley,

but the evidence has to be challenged. You have to have local knowledge input or it’s useless”

(Tim Dugdill, Chair of Knowsley Economic Partnership)

Co-develop the Assessment with the Local Authority

Use it as a mechanism to focus / tighten up interventions

WOLVERHAMPTON CITYWEST MIDLANDS

Public sector and Construction (Carillon)make up around 45%

of all the jobs in the City

De-industrialising

Business survival -poor

High level qualifications - lacking‘good quality local graduates.....’

Low earning society

Not producing enough jobs?

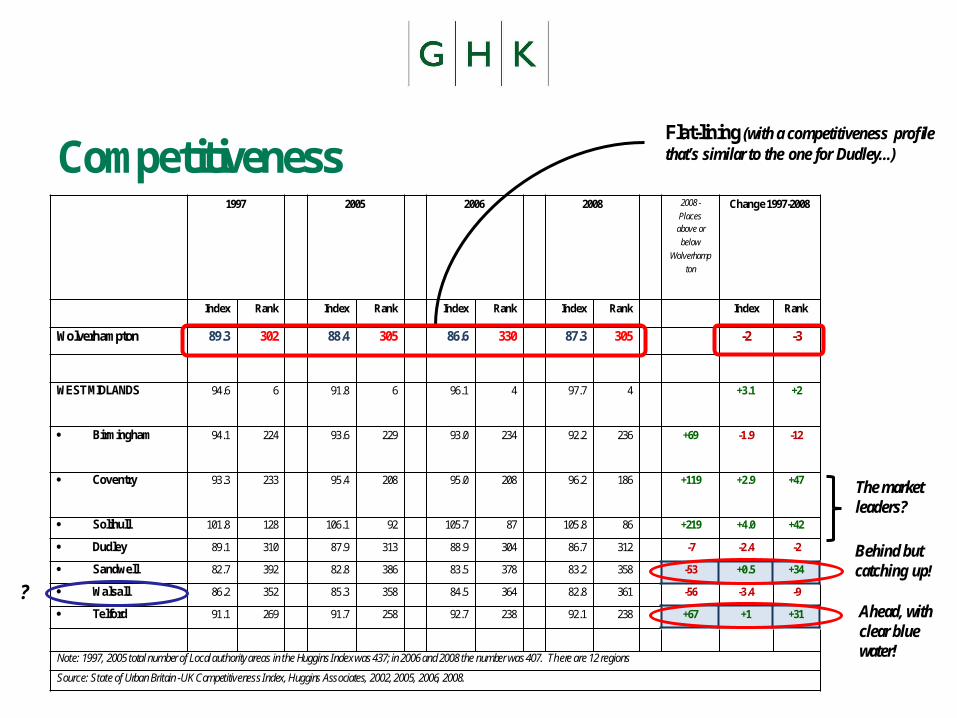

Scorecard

1997 2005 2006 2008 2008 -

Places above or

below

Wolverhamp

ton

Change 1997-2008

Index Rank Index Rank Index Rank Index Rank Index Rank

Wolverhampton 89.3 302 88.4 305 86.6 330 87.3 305 -2 -3

WEST MIDLANDS 94.6 6 91.8 6 96.1 4 97.7 4 +3.1 +2

Birmingham 94.1 224 93.6 229 93.0 234 92.2 236 +69 -1.9 -12

Coventry 93.3 233 95.4 208 95.0 208 96.2 186 +119 +2.9 +47

Solihull 101.8 128 106.1 92 105.7 87 105.8 86 +219 +4.0 +42

Dudley 89.1 310 87.9 313 88.9 304 86.7 312 -7 -2.4 -2

Sandwell 82.7 392 82.8 386 83.5 378 83.2 358 -53 +0.5 +34

Walsall 86.2 352 85.3 358 84.5 364 82.8 361 -56 -3.4 -9

Telford 91.1 269 91.7 258 92.7 238 92.1 238 +67 +1 +31

Note: 1997, 2005 total number of Local authority areas in the Huggins Index was 437; in 2006 and 2008 the number was 407. There are 12 regions

Source: State of Urban Britain -UK Competitiveness Index, Huggins Associates, 2002, 2005, 2006, 2008.

Flat-lining (with a competitiveness profile that’s similar to the one for Dudley...)

Behind but catching up!

Ahead, withclear blue water!

?

The market leaders?

Competitiveness

0.0 5.0 10.0 15.0 20.0 25.0

England and Wales

West Midlands

Birmingham

Coventry

Walsall

Wolverhampton

% of Working Age People in Employment with No Qualification

2007

2006

2005

What’s happening in WolverhamptonAnd why is it getting worse?

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0

England and Wales

West Midlands

Birmingham

Coventry

Walsall

Wolverhampton

% of Working Age in Employment with NVQ Level 4+

2007

2006

2005

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0

England and Wales

West Midlands

Birmingham

Coventry

Walsall

Wolverhampton

% of Working Age in Employment with NVQ Level 4+

2007

2006

2005

What’s happening in Wolverhampton

And why is it getting worse?

Pathways to employment (not clear at present):– Schools / University – building aspirations +skills + competencies (but slow at present)– A focus on attracting offices and building retail outlets– need1-2 high technology platforms?– Pathways to high end jobs as well as entry level jobs - required

Pathways to innovation (even more opaque):– University? The WT High Technology Corridor? Existing Firms? New Firms?– Environment does not encourage (sufficient) adoption and structural adaption?– Little collaboration with adjacent LAs – whither the Birmingham city region?– Aerospace – Centre of Excellence on I54 site (missed) opportunity? – Computer games and Creative industries – languishing (Californian GRAB!)?– Local lead markets / procurement – opportunity not exploited. Need a bold Move

Pathways to regeneration – sorted? But credit crunch MAY throttle plans! Pathways to effective governance – sorted? But Triple Helix in infancy!

Need push on all fronts – otherwise regeneration interventions underutilised /compromised without pathways to employment and innovation etc. Need to align core strategies and think about Plan B if physical regeneration focus compromised

Conclusions.......beyond the LEA?

A duty and a requirement - or an opportunity to look at matters afresh? – Surprise expressed at some of the figure and their interpretation– Stimulated discussion re e.g. ‘employability’ – Raised concerned about existing focus of development strategy– Thrown into high relief debate ‘regeneration v economic development’– Also debate about where to look for economic partners – the Black Country or to the

north and west (was Birmingham a blessing or a blight – what would make it a blessing? Should we work with Coventry – e.g. re aerospace centre of excellence?)

– Certainly provide ‘evidence’ – basis of strategy

Stand aside or get involved?– Secondary data tells an incomplete story (sometimes leads to misunderstanding)– Survey of / engagement with business vital– Brainstorming with key stakeholders crucial– Creating the ‘narrative’ (shared narrative for the LA and its place in the wider region)

Benchmark – Why against failure! Find the best? Debate!

Possible Lessons - Wolverhampton

TENDRING DISTRICT, ESSEX COUNTY

Percentage achieving 5 GSCE’s A-C (2004-05)

Only 49% gain 5 or more high-grade GSCE in 2006

Second lowest in Essex( Well below Regional and National Averages)

Challenges thrown into high relief - Are we in Trouble?

Flat-lining – economic underperformance– Lost sense of purpose – failed to find substitute to economy post-war…..?

– In general a low skilled low wage economy…(the skilled commute OUT)…?

– What is the narrative for Tendring…..?

– Need for a new Business Model….?

Difficult / divided politics – Working with adjacent Districts.....?

– Solid partnerships up and running....?

– Need for greater collaboration – within Haven Gateway sub-region....?

Need for a few Catalytic Projects.– Maximise benefits of Haven Port Development....?

– Use / Develop the Colchester fringe....?

– Focus on one up-market tourism ‘offer’ (note -TV Coastal Arc projects?)

– New healthy living retirement communities of the future?

– Make peace with London – best commuter-ville in the South East?

?

?

?

Need for a few Catalytic projects.– Best Marine Leisure offer in the East....?

– Focus on Gateway status – gateway to Europe and the World From the Mayflower

To: Ships built for the Napoleonic Wars

To: Transportation to the Trenches of WWI

To: Globalisation – represented by HUTCH!

Need for a Coherent Vision & Narrative to frame the projects.– The ingredients

Gateway Function

Tourism and Leisure

High Tech Development –Colchester

High Tech development – Renewables (wind power)

Land of the New ‘Creatives’

Retirement to die for

Commuter-Ville.

?

?What’s

achievable?Visionary and Inspiring YET

Practical?

Possible Lessons – Tendring

Generated discussion about:– the ‘role’ of the District

– working with big brother adjacent areas – Colchester / Ipswich – Possible MAA

(got Colchester involved at one stage!)

– (Physical) regeneration v economic development – input to their LDF

– The Future ( we ended up running a few scenarios – lifted horizons)

Became a narrative with which to frame a series of disparate projects

Helped the stakeholders think about and effectively construct their

‘ask’ to funders

Thank you for your AttentionLocal Economic Assessments Releasing the Power of Place