lng yearbook 2015 - the definitive reference guide to the liquefied natural gas infrastructure...

TRANSCRIPT

©noticeThis material is copyright by visiongain. It is against the law to reproduce any of this material without the prior written agreement of visiongain. You cannot photocopy, fax, download to database or duplicate in any other way any of the material contained in this report. Each purchase and single copy is for personal use only.

LNG Yearbook 2015: The Definitive reference Guide to the Liquefied Natural

Gas Infrastructure Market 2015-2025Capex on Large-Scale Onshore Liquefaction & Regasification,

Floating LNG (FLNG), Small-Scale LNG and LNG Carriers

www.visiongain.com

Contents 1. Report Overview 1.1 LNG Yearbook 2015: The Definitive Reference Guide to Liquefied Natural Gas (LNG): Infrastructure and Market

Forecast 2015-2025: Capex on Large-Scale Onshore Liquefaction & Regasification, LNG Carriers, Small-Scale and

Floating LNG (FLNG) Vessels

1.2 Why You Should Read This Report

1.3 Benefits of This Report

1.4 Structure of This Report

1.5 Key Questions Answered by This Analytical Report Include:

1.6 Who is This Report For?

1.7 Market Definition

1.8 Methodology

1.9 Frequently Asked Questions (FAQ)

1.10 Associated Visiongain Reports

1.11 About Visiongain

2. Introduction to the LNG Infrastructure Market 2.1 The Role and Function of LNG Infrastructure

2.1.1 The LNG Supply Chain

2.1.2 What is Natural Gas Liquefaction?

2.1.3 What is LNG Regasification?

2.1.4 Brief History of LNG Infrastructure

2.2 The Role of LNG Carriers

2.2.1 Global LNG Carrier Market Segmentation

2.2.2 History of LNG Carriers

2.2.3 LNG Carrier Technologies

2.2.4 The LNG Carrier Market Structure

2.3 The Role of FLNG

2.3.1 FLNG Market Structure Overview

2.3.2 FLNG Vessels

2.3.2.1 Regasification Vessels

2.3.2.2 Liquefaction Vessels

2.3.3 FLNG Technology

2.3.3.1 Brief History of FLNG

2.3.3.2 Offshore Regasification

2.3.3.3 Offshore Liquefaction

www.visiongain.com

Contents 2.3.3.4 Conversions and New Builds

2.3.4 FLNG’s Increasing Preferability

2.4 The Role of Small-Scale LNG

2.4.1 Global Small Scale LNG Market Overview

2.4.2 Global Small Scale LNG Market Segmentation

2.4.3 Small Scale LNG Submarket Categories

2.5 Introduction to LNG Market Dynamics

3. The Global LNG Market 3.1 The Global LNG Submarket Forecasts

3.2 The Global LNG Market Analysis

3.2.1 What is Shaping the Expansion of the Global LNG Trade?

3.2.1.1 Demand Side Factors

3.2.1.2 Supply-Side Drivers

3.2.1.3 Global LNG Market: Where Are We Now; Where Will We Be in 5 Years; Where Will We

Be in 10 Years?

3.2.2 Increasing Demand for Natural Gas

3.2.3 The Economics of the LNG Trade versus Movement of Natural Gas via Pipelines

3.2.4 Arbitrage Opportunity

3.2.5 Desire to Increase Energy Security

3.2.6 Unconventional Gas Reserves

3.2.7 Environmental and Climate Dimensions

3.2.8 Impact of Travel Distances

3.2.9 Key Uncertainties in the Global LNG Market

3.2.10 Oil Price Collapse Analysis and Forecast

3.2.10.1 Supply- Side Factors: Tight Oil

3.2.10.2 Supply-Side Factors: Libya

3.2.10.3 Supply-Side Factors: OPEC

3.2.10.4 Demand-Side Factors: Chinese and Indian Growth

3.2.10.5 Known Unknowns and Major Variables that Impact the Oil Price

3.2.10.6 Visiongain’s Oil Price Assumptions and Forecast

3.2.11 Oil Price and LNG Price Relationship

3.2.12 No Universal Gas Pricing Index

3.2.13 Can a Global LNG Spot Market Emerge?

3.2.14 Japan’s Fukushima Crisis and Future Energy Mix

www.visiongain.com

Contents 3.2.14.1 Tsunami and History

3.2.14.2 Capital Expenditure Analysis

3.2.14.3 Will Nuclear Power Generation Restart?

3.2.14.4 The Future of Coal Power Generation

3.2.14.5 How Has, and Will, the Japanese Economy Affect LNG Infrastructure Spending?

3.2.14.6 Liquefaction Equity Investment Indicative of Future Imports

3.2.14.7 Future Electricity Demand

3.2.14.8 Japan’s Role in the Global FLNG Market

3.2.15 Towards an Oversupplied LNG Market

4. The Global Large-Scale Onshore LNG Market 4.1 Global Large-Scale Onshore LNG Liquefaction & Regasification Market

4.2 Global Large-Scale Onshore LNG Liquefaction & Regasification Analysis

4.2.1 What Challenge Does Floating Liquefied Natural Gas Pose Onshore LNG Liquefaction Terminals?

4.2.1.1 The Economics

4.2.1.2 Regulatory/Tax Benefits and Development Timeframes

4.2.1.3 Flexibility

4.2.1.4 Overall Assessment

4.3 The Global LNG Liquefaction Market (Large-Scale Onshore) 2015-2025

4.3.1 Large-Scale Onshore LNG Liquefaction Facilities in Operation, Under Construction or Planned

4.4 The Global LNG Regasification Market (Large-Scale Onshore) 2015-2025

4.4.1 Large-Scale Regasification Terminals in Operation, Under Construction and Planned

5. The Global LNG Carrier Market 5.1 The Global LNG Carrier Market Forecast 2015-2025

5.2 Dynamics of the LNG Carrier Market

5.3 Current LNG Carrier Fleet

5.4 The LNG Carrier Market Analysis

5.4.1 LNG Carrier Market Drivers & Restraints

5.4.2 Arbitrage Opportunities and the LNG Carrier Market

5.4.3 LNG Carriers Fleet and Historical Data.

5.4.4 Charter Rates, the LNG Spot Market and LNG Carrier Demand

5.4.5 No LNG Construction Capacity Constraint

5.4.6 The Dominant Role of Liquefaction Capacity in Determining the Global LNG Carrier Market

5.4.7 The Impact of Australian Liquefaction Uncertainty on the Global LNG Carrier Market

www.visiongain.com

Contents 5.4.8 East African LNG Exports and the LNG Carrier Market

5.4.9 The Impact of North American LNG Exports on the LNG Carrier Market

5.4.10 West African Natural Gas Supply, LNG Carrier Mileage and LNG Carrier Demand

5.4.11 Norway, Russia and Ice-Class LNG Carriers

5.4.12 LNG Carrier Mileage, Routes and Future Outlook

5.4.13 How an Increase in Interregional Activity Will Affect LNG Carrier Demand

5.4.14 LNG Demand Patterns, Regasification Terminals and the Triangulation of the LNG Carrier Fleet

5.4.15 How the Replacement of LNG Vessels Will Influence the LNG Carrier Market

5.4.16 The Impact on the LNG Carrier Market of Using LNG as a Transportation Fuel

5.4.17 Environmental Factors and the LNG Carrier Market

5.4.18 LNG versus Pipeline Economics and the LNG Carrier Market

5.4.19 LNG Carrier Market Restraints

5.4.20 Geographical Limitations on Liquefaction Capacity

5.4.21 Demand Uncertainty & Volatile Gas Spot Prices

5.4.22 Liquefaction Capacity Supply Constraint

5.4.23 Qatar North Field Moratorium

5.4.24 European and Asian LNG Demand Concerns

5.4.25 Concern Regarding Sustainability of Long Term Charter Rates

5.4.26 Current LNG Carrier Order Book

5.4.27 Expansion to LNG Carrier Fleet

5.4.28 Small-Scale LNG Carriers

5.5 Mark III (T-Mark III, Mark III Flex) Containment System Market Forecast 2015-2025

5.5.1 Mark III Containment System Drivers & Restraints

5.5.2 Mark III Containment System Drivers & Restraints

5.5.3 T-Mark III LNG Carrier Orders

5.6 GTT No. 96 Containment System Market Forecast 2015-2025

5.6.1 GTT No. 96 Drivers & Restraints

5.6.2 GTT No. 96 LNG Carrier Orders

5.7 Moss Rosenberg Containment System Market Forecast 2015-2025

5.7.1 Moss Rosenberg Containment System Drivers & Restraints

5.7.2 Moss Rosenberg LNG Carrier Orders

5.8 SPB Containment System Market Forecast 2015-2025

5.8.1 SPB Rosenberg LNG Carrier Orders

5.9 The Small-Scale LNG Carrier Market Forecast 2015-2025

5.9.1 Small-Scale LNG Carriers Represent a Logical Expansion of LNG Supply Chain

5.9.2 Expanding Use of Satellite Stations

www.visiongain.com

Contents 5.9.3 Development of River-Based LNG Carriers

5.9.4 Use of Small-Scale LNG for Island Distribution

5.9.5 Expansion of LNG Bunkering

5.9.6 Small-Scale LNG Containment Technology Advantage

5.9.7 Japanese Small-Scale LNG Prospects

5.9.8 Ship-to-Ship Transfers of LNG

5.9.9 Environmental Benefits and Small-Scale LNG Carriers

5.9.10 Small-Scale LNG Carrier Market Drivers & Restraints

6. The Global FLNG Market

6.1 Global FLNG Market Forecast

6.1.1 Regional FLNG Market Forecasts

6.2 Leading National FLNG Markets 2015-2025

6.2.1 Top 10 Countries in FLNG 2015-2025

6.2.2 FLNG Market Barriers to Entry Analysis

6.3 Summary of Global FLNG Market Determinants

6.3.1 Drivers in the FLNG Market

6.3.1.1 Favourable Economics Compared to Onshore

6.3.1.2Tax/ Regulatory Benefits and Development Timeframes

6.3.1.3 Avoid Security Challenges

6.3.1.4 Monetisation of Stranded and Unused Gas

6.3.1.5 LNG versus Pipeline Economics

6.3.1.6 Economic Flexibility of LNG

6.3.1.7 Mobility of FLNG

6.3.1.8 FLNG Deployment Speed and Cost

6.3.1.9 Improvements in Subsea Technologies

6.3.1.10 Deeper Water

6.3.2 Restraints in the FLNG Market

6.3.2.1 Securing Contracts, Insurance and Project Finance

6.3.2.2 High Capital Expenditure

6.3.2.3 Shipyard Capacity

6.3.2.4 FLNG Complexity

6.3.2.5 Logistics and Extreme Weather

6.3.3 Overall FLNG Market Drivers and Restraints

6.4 FLNG Submarket Comparison and Analysis

www.visiongain.com

Contents 6.4.1 LNG FPSO Submarket Forecast 2015-2025

6.4.1.1 Market Barriers

6.4.1.2 2015 Oil Price Update

6.4.1.3 LNG FPSO Market Drivers & Restraints

6.4.1.4 LNG FPSO Projects

6.4.1.5 LNG FPSO Production Capacity Forecast 2015-2020

6.4.2 FSRU Submarket Forecast 2015-2025

6.4.2.1 FSRU Market Drivers & Restraints

6.4.2.2 FSRU Projects – Operational and Potential

6.4.2.3 FSRU Regasification Capacity Forecast 2015-2020

7. The Global Small-Scale LNG Market 7.1 Global Small Scale LNG Market Forecast 2015-2025

7.2 Global Small Scale LNG Market Analysis

7.2.1 LNG Demand Forecasts

7.2.2 Small-Scale LNG Carriers as Part of the LNG Supply Chain

7.2.3 Oil Prices and the Small Scale LNG Market

7.2.4 Global Small Scale LNG Market Drivers & Restraints

7.3 Small Scale LNG Submarkets Forecast 2015-2025

7.3.1 Small Scale Regasification Market Forecast 2015-2025

7.3.1.1 Small Scale Regasification Analysis

7.3.2 Small Scale Liquefaction Market Forecast 2015-2025

7.3.2.1 Small Scale Liquefaction Analysis

7.3.3 LNG Satellite Stations 2015-2025

7.3.3.1 Small Scale LNG Satellite Stations Analysis

7.3.4 LNG Bunkering Facilities for Vessels 2015-2025

7.3.4.1 LNG Bunkering Facilities for Vessels Analysis

7.3.5 LNG Fuelling Stations for Road Vehicles 2015-2025

7.3.5.1 LNG Fuelling Stations for Road Vehicles Analysis

8. The Australasian LNG Market 2015-2025

8.1 The Australian LNG Market 2015-2025

8.1.1 Australian Large-Scale Onshore LNG Liquefaction Market 2015-2025

8.1.1.1 Overall Drivers & Restraints on Australian LNG Liquefaction Investment

8.1.1.2 Capital Expenditure Analysis

www.visiongain.com

Contents 8.1.1.3 What Are the Prospects for Brownfield Terminal Development?

8.1.1.4 Future Outlook for Australian LNG Infrastructure

8.1.1.5 Australian LNG Liquefaction Infrastructure in Operation, Under Construction and Planned

8.1.2 The Australian FLNG Market Forecast 2015-2025

8.1.2.1 Australian FLNG Market Analysis

8.1.2.2 Prelude and Australian LNG FPSO Project Analysis

8.1.2.3 Analysis of Australia-Timor Leste Offshore Gas Dispute

8.1.2.4 Australian FLNG Political Considerations

8.1.2.5 Australian FLNG Market Drivers & Restraints

8.1.2.6 Australian FLNG Projects

8.1.3 The Australian Small Scale LNG Market Outlook

8.1.3.1 Small Scale Liquefaction Plants in Australia

8.1.3.2 LNG Fuelling Stations in Australia

8.1.3.3 LNG Bunkering Facilities in Australia

8.2 The Papua New Guinea LNG Market 2015-2025

8.2.1 Papua New Guinea LNG Liquefaction Outlook

8.2.2 Papua New Guinea FLNG Market Forecast 2015-2025

8.2.2.1 Papua New Guinea FLNG Market Analysis

8.3 The New Zealand LNG Market

8.3.1 New Zealand FLNG Market

9. The North American and Caribbean LNG Market 2015-2025 9.1 The US LNG Market 2015-2025

9.1.1 US Large-Scale Onshore LNG Liquefaction Market 2015-2025

9.1.1.1 Overall Drivers & Restraints on US LNG Liquefaction Investment

9.1.1.2 Drivers for Capital Expenditure

9.1.1.3 Restraints on Capital Expenditure

9.1.1.4 US Large-Scale Onshore LNG Liquefaction Terminal Locations

9.1.1.5 US LNG Liquefaction Infrastructure in Operation, Under Construction and Planned

9.1.2 United States FLNG Market 2015-2025 Forecast

9.1.2.1 United States FLNG Market Analysis

9.1.2.2 US LNG FPSO Project Analysis

9.1.2.3 United States FLNG Projects

9.1.2.4 United States FLNG Market Drivers and Restraints

9.1.3 US Small Scale LNG Market Forecast 2015-2025

www.visiongain.com

Contents 9.1.3.1 US Small Scale LNG Submarkets Analysis

9.1.3.2 Small Scale LNG Regasification Terminals in US

9.1.3.3 Small Scale Liquefaction Plants in US

9.1.3.4 LNG Fuelling Stations in US

9.1.3.5 LNG Satellite Stations in US

9.1.3.6 LNG Bunkering facilities in US

9.1.3.7 How Does the US Shale Gas Market affect Small-Scale LNG?

9.2 Canadian LNG Market 2015-2025

9.2.1 Canadian Large-Scale Onshore LNG Liquefaction Market 2015-2025

9.2.1.1 Overall Drivers & Restraints on Canadian LNG Liquefaction Investment

9.2.1.2 Capital Expenditure Analysis

9.2.1.3 Canadian Onshore LNG Liquefaction Projects

9.2.1.4 Upstream Reserves

9.2.1.5 Pipeline Construction Costs

9.2.1.6 Greenfield Terminal Costs and Economics

9.2.1.7 Threats to LNG Liquefaction Terminal Investment

9.2.1.8 Canadian LNG Liquefaction Infrastructure in Operation, Under Construction and Planned

9.2.2 Canadian FLNG Market Outlook

9.3 Trinidad and Tobago FLNG Market Outlook

9.3.1 Trinidad & Tobago Onshore LNG Prospects

9.4 Guadeloupe and Martinique LNG Market Outlook

9.4.1 Guadeloupe and Martinique FLNG Market Outlook

9.5 Jamaican LNG Market Outlook

9.5.1 Jamaican FLNG Market Outlook

9.6 Puerto Rican LNG Market Outlook

9.6.1 Puerto Rican FLNG Market Outlook

9.7 Other North American LNG

9.7.1 Other North American and Caribbean FLNG Market

9.7.1.1 Other North American and Caribbean FLNG Market Drivers & Restraints

9.7.1.2 Other North American and Caribbean FLNG Projects

9.8 North American FLNG

9.8.1 The North American and Caribbean FLNG Market Forecast 2015-2025

9.8.1.1 The North American and Caribbean FLNG Market Analysis

9.8.2 North American LNG FPSO Production Capacity Forecast 2015-2025

www.visiongain.com

Contents 10. The Asian LNG Market 2015-2025

10.1 Asian FLNG Market

10.1.2 The Asian FLNG Market Forecast 2015-2025

10.1.3 Asian FLNG Market Analysis

10.1.4 Asian FLNG Market Drivers & Restraints

10.1.5 Asian FLNG Projects

10.1.6 East Asian FSRU Regasification Capacity Forecast

10.2 Small Scale LNG Regasification Terminals in Asia

10.3 The Chinese LNG Market 2015-2025

10.3.1 Chinese Large-Scale Onshore LNG Regasification Market 2015-2025

10.3.1.1 Overall Drivers and Restraints on the Chinese Onshore LNG Regasification Market

10.3.1.2 Drivers

10.3.1.3 Restraints

10.3.1.4 Chinese Onshore LNG Regasification Infrastructure in Operation, Under Construction

and Planned

10.3.2 The Chinese LNG Carrier Market Forecast 2015-2025

10.3.2.1 Chinese Demand for LNG Carriers

10.3.2.2 Are Expanding Natural Gas Pipeline Supplies to China a Threat to the Chinese LNG

Carrier Market?

10.3.2.3 Increasing Numbers of Chinese Shipyards Capable of Building LNG Carriers

10.3.2.4 LNG Carrier Construction and the Chinese Yuan

10.3.2.5 Labour Costs, Foreign Orders and Attractive Financing

10.3.2.6 Small Scale LNG Carrier Construction in China

10.3.2.7 Limitations on LNG Carrier Market in China

10.3.2.8 Chinese LNG Carrier Market Drivers & Restraints

10.3.2.9 Chinese LNG Carrier Orders

10.3.3 Chinese FLNG Market Forecast 2015-2025

10.3.3.1 Chinese FLNG Market Analysis

10.3.3.2 Chinese LNG, FLNG, and Gas Consumption

10.3.4 China Small Scale LNG Market Forecast 2015-2025

10.3.4.1 China Small Scale LNG Submarkets Analysis

10.3.4.2 Small Scale LNG Regasification Terminals in China

10.3.4.3 Small Scale Liquefaction Plants in China

10.3.4.4 LNG Fuelling Stations in China

10.3.4.5 LNG Bunkering Facilities in China

10.3.4.6 LNG Satellite Stations in China

www.visiongain.com

Contents 10.3.4.7 China’s Natural Gas Pipelines and the Small Scale LNG Market

10.3.4.8 The Effects of Shale Gas Development on Small-Scale LNG in China

10.3.4.9 The Effects of Coalbed Methane Development on Small-Scale

10.3.4.10 The Effects of Tight Gas Development on Small-Scale LNG in China

10.4 The Japanese LNG Market 2015-2025

10.4.1 Japanese Large-Scale Onshore LNG Regasification Market 2015-2025

10.4.1.1 Overall Drivers and Restraints on the Japanese Onshore LNG Regasification

Market

10.4.1.2 Capital Expenditure Analysis

10.4.1.3 Will Nuclear Power Generation Restart (and if so when)?

10.4.1.4 The Future of Coal Power Generation

10.4.1.5 How Has, and Will, the Japanese Economy Affect LNG Infrastructure Spending?

10.4.1.6 Future Investment

10.4.1.7 Future Electricity Demand

10.4.1.8 Japanese LNG Regasification Infrastructure in Operation, Under Construction and

Planned

10.4.2 The Japanese LNG Carrier Market Forecast 2015-2025

10.4.2.1 The Japanese Yen and LNG Carrier Orders

10.4.2.2 Are Wage Levels Affecting Japanese LNG Carrier Orders?

10.4.2.3 The Competitive Advantage of Japanese LNG Carriers

10.4.2.4 Shift Away From Long-Term Contracts Hurting Japanese LNG Carrier Construction

Industry

10.4.2.5 The Potential for More LNG Carrier Construction in Japan

10.4.2.6 The Challenge of China to Japanese LNG Carrier Builders

10.4.2.7 The Advantage of Moss Spherical Containment Systems (Only Used by Japanese

Shipbuilders)

10.4.2.8 The Small-Scale LNG Carrier Market in Japan

10.4.2.9 The Challenge to Japanese LNG Carrier Builders of South Korean Shipbuilders

10.4.2.10 Japanese LNG Carrier Market Drivers & Restraints

10.4.2.11 Japanese LNG Carrier Orders

10.4.3 Japan FLNG Outlook

10.4.4 Japan Small Scale LNG Market Forecast 2015-2025

10.4.4.1 Japan Small Scale LNG Submarkets Analysis

10.4.4.2 Small Scale LNG Regasification Terminals in Japan

10.4.4.3 Small Scale Liquefaction Plants in Japan

10.4.4.4 LNG Fuelling Stations in Japan

www.visiongain.com

Contents 10.4.4.5 LNG Satellite Stations in Japan

10.4.4.6 LNG Bunkering facilities in Japan

10.5 The South Korean LNG Market 2015-2025

10.5.1 South Korean Large-Scale Onshore LNG Regasification Market 2015-2025

10.5.1.1 Overall Drivers and Restraints on the South Korean Onshore LNG Regasification Market

10.5.1.2 Current LNG Demand Situation

10.5.1.3 What is the Future of Nuclear Power Generation in South Korea?

10.5.1.4 South Korean LNG Regasification Infrastructure in Operation, Under Construction and

Planned

10.5.2 The South Korean LNG Carrier Market Forecast 2015-2025

10.5.2.1 Bulk Orders Potential Provides Competitive Advantage

10.5.2.3 Q-Max and Q-Flex Vessel History

10.5.2.4 The Challenge to South Korea of Chinese Shipbuilders

10.5.2.5 South Korean LNG Carrier Propulsion Systems Provide Competitive Advantage

10.5.2.6 South Korean Shipbuilding Expertise Depth

10.5.2.7 South Korean LNG Carrier Market Drivers & Restraints

10.5.2.8 South Korean LNG Carrier Orders

10.5.3 South Korea FLNG Outlook

10.5.4 South Korean Small Scale LNG

10.5.4.1Small Scale LNG Regasification Terminals in South Korea

10.5.4.2 LNG Bunkering Facilities in South Korea

10.6 The Indian LNG Market 2015-2025

10.6.1 Indian LNG Infrastructure Outlook

10.6.1.1 Indian LNG Regasification Terminals in Operation and Under Construction

10.6.2 The Indian LNG Carrier Market Forecast 2015-2025

10.6.3 Indian FLNG Market Forecast 2015-2025

10.6.3.1 Indian FLNG Market Analysis

10.6.3.2 Planned Indian FLNG Projects

10.6.4 Small Scale LNG Regasification Terminals in India

10.7 Bangladesh LNG Outlook

10.7.1 Bangladesh FLNG Outlook

10.8 Pakistani LNG Outlook

10.8.1 Pakistani FLNG Outlook

10.9 Sri Lankan LNG Outlook

10.9.1 Sri Lankan FLNG Outlook

www.visiongain.com

Contents 11. The South East Asian LNG Market 2015-2025

11.1 South East Asian Large-Scale Onshore LNG Infrastructure

11.1.1 South East Asian Large-Scale Onshore LNG Liquefaction Market 2015-2025

11.1.1.1 Overall Drivers & Restraints on South East Asian LNG Liquefaction Investment

11.1.2 South East Asian Large-Scale Onshore LNG Gasification

11.1.3 South East Asian LNG Liquefaction Infrastructure in Operation, Under Construction and Planned

11.2 The Southeast Asian FLNG Market Forecast 2015-2025

11.2.1 Southeast Asian FLNG Market Analysis

11.2.2 Other Southeast Asian FLNG Projects

11.3 The Indonesian LNG Market 2015-2025

11.3.1 Indonesian LNG Liquefaction Outlook

11.3.1.1 A Domestic LNG Trade and the Shift Toward Natural Gas Consumption

11.3.1.2 The Indonesian Domestic Gas Trade

11.3.1.3 Coalbed Methane in Indonesia

11.3.2 The Indonesian FLNG Market Forecast 2015-2025

11.3.2.1 Indonesian FLNG Market Analysis

11.3.2.2 Future Indonesian Liquefaction

11.3.2.3 Indonesian FLNG Market Drivers & Restraints

11.3.2.4 Indonesian FLNG Projects

11.3.3 Indonesia Small Scale LNG Market & Submarket Forecasts 2015-2025

11.3.3.1 Indonesia Small Scale LNG Submarkets Analysis

11.3.3.2 Small Scale LNG Regasification Terminals in Indonesia

11.3.3.3 Small Scale Liquefaction Plants in Indonesia

11.3.3.4 LNG Fuelling Stations in Indonesia

11.3.3.5 LNG Satellite Stations in Indonesia

11.3.3.6 LNG Bunkering facilities in Indonesia

11.4 Malaysian LNG Market 2015-2025

11.4.1 Malaysian LNG Liquefaction Outlook

11.4.2 The Malaysian FLNG Outlook

11.5 Thai LNG Market 2015-2025

11.5.1 Thai FLNG Outlook

11.6 Vietnam LNG Market 2015-2025

11.6.1 Vietnamese FLNG Outlook

11.7 Philippines LNG Market 2015-2025

11.7.1 Filipino FLNG Outlook

11.8 Singapore LNG Outlook

www.visiongain.com

Contents 11.9 Brunei LNG Outlook

11.9.1 Brunei LNG Liquefaction Outlook

11.10 Timor Leste LNG Outlook

11.10.1 Timor Leste FLNG Outlook

12. The European LNG Market 2015-2025

12.1 European Large-Scale Onshore LNG Regasification Market 2015-2025

12.1.1 How Does the Ukraine Crisis Impact Future European LNG Demand?

12.1.2 The Impact of Gas Pipeline Developments on LNG Infrastructure Investment

12.1.3 The Economics of LNG Imports vs. Russian Gas

12.1.4 The FSRU Option – A Threat to Onshore Regasification in Europe?

12.1.5 What Will the Effect of UK North Sea Gas Declines be on Regasification Infrastructure?

12.1.6 Shale Gas Development Issues and their Relation to LNG Infrastructure Development

12.1.6.1 Shale Gas in Poland

12.1.6.2 Shale Gas in the UK

12.1.6.3 Shale Gas in Germany

12.1.7 Energy Security & Geo-Politics as a Driver of Regasification Infrastructure Development

12.1.8 A Shift to Natural Gas Power Generation?

12.1.9 Baltic States LNG Regasification Outlook

12.1.10 Overall Drivers and Restraints on the European Onshore LNG Regasification Market

12.1.11 European LNG Regasification Infrastructure in Operation, Under Construction and Planned

12.2 European FLNG Market Forecast 2015-2025

12.2.1 European FLNG Market Analysis

12.2.2 European FLNG Market Drivers & Restraints

12.2.3 European FLNG Projects

12.2.4 European FSRU Regasification Capacity Forecast 2015-2020

12.3 Europe Small Scale LNG Market Forecast 2015-2025

12.3.1 Europe Small Scale LNG Submarkets Analysis

12.3.2 Small Scale LNG Regasification Terminals in Europe

12.3.3 Small Scale Liquefaction Plants in Europe

12.3.4 LNG Fuelling Stations in Europe

12.3.5 LNG Satellite Stations in Europe

12.3.6 LNG Bunkering Facilities in Europe

12.3.6.1 Break Bulk Facilities in Europe

12.4 The Cypriot LNG Market 2015-2025

12.4.1 Cypriot FLNG Market Outlook

www.visiongain.com

Contents 12.5 The Greek LNG Market 2015-2025

12.5.1 Greek FLNG Outlook

12.6 The Italian LNG Market 2015-2025

12.6.1 Italian LNG Regasification Terminal Outlook

12.6.2 Italian FLNG Market Outlook

12.7 The Lithuanian LNG Market 2015-2025

12.7.1 Lithuanian FLNG Market Outlook

12.8 The Turkish LNG Market 2015-2025

12.8.1 Turkish FLNG Market Outlook

12.9 The UK LNG Market 2015-2025

12.9.1 UK FLNG Market Outlook

12.10 The Ukraine LNG Market 2015-2025

12.10.1 Ukraine FLNG Market Outlook

12.11 The Malta LNG Market 2015-2025

12.11.1 Malta FLNG Market Outlook

12.12 The Russian LNG Market 2015-2025

12.12.1 Russian Large-Scale Onshore LNG Liquefaction Market 2015-2025

12.12.1.1 Russia Onshore Liquefaction Facilities and Prospects

12.12.1.2 Overall Drivers & Restraints on Russian LNG Liquefaction Investment

12.12.1.3 Russian LNG Liquefaction Infrastructure in Operation, Under Construction and Planned

12.12.2 Prospects for the Russian FLNG Market

12.12.2.1 Golar and Rosneft

13. Middle Eastern LNG Market 2015-2025

13.1 The Middle Eastern FLNG Market Forecast 2015-2025

13.1.1 Middle East FLNG Market Analysis

13.1.2 Middle Eastern FLNG Market Drivers & Restraints

13.1.3 Other Middle Eastern FLNG Projects

13.1.4 Middle Eastern FSRU Regasification Capacity Forecast 2015-2020

13.1.5 Middle Eastern LNG FPSO Production Capacity Forecast 2015-2025

13.2 The Egyptian LNG Market 2015-2025

13.2.1 Egyptian Onshore LNG Liquefaction Prospects

13.2.2 Egyptian FLNG Market Outlook

13.3 The Israeli LNG Market 2015-2025

13.3.1 Israeli LNG Infrastructure Outlook

www.visiongain.com

Contents 13.3.2 Israeli FLNG Market Forecast 2015-2025

13.3.2.1 Israeli FLNG Market Analysis

13.3.2.2 Israeli FLNG Projects

13.4 The Jordanian LNG Market 2015-2025

13.4.1 Jordanian FLNG Market Outlook

13.5 The Kuwaiti LNG Market 2015-2025

13.5.1 Kuwaiti FLNG Market Outlook

13.6 The Lebanese LNG Market 2015-2025

13.6.1 Lebanese FLNG Market Outlook

13.7 The UAE LNG Market 2015-2025

13.7.1 UAE FLNG Market Outlook

13.8 The Qatari LNG Market 2015-2025

13.8.1 Qatari Onshore LNG Liquefaction Prospects

14. The African LNG Market 2015-2025

14.1 The African Large-Scale Onshore LNG Infrastructure

14.1.1 East Africa Large-Scale Onshore LNG Liquefaction Market 2015-2025

14.1.1.1 Overall Drivers & Restraints on East African LNG Liquefaction Investment

14.1.1.2 East African LNG Liquefaction Infrastructure in Operation, Under Construction and

Planned

14.2 The African LNG Carrier Market

14.2.1 East African LNG Exports and the LNG Carrier Market

14.3 The African FLNG Market Forecast 2015-2025

14.3.1 African FLNG Market Analysis

14.3.2 African FLNG Market Drivers & Restraints

14.3.3 African FLNG Projects

14.3.4 African LNG FPSO Production Capacity Forecast 2015-2025

14.3.5 West Africa FLNG Outlook

14.4 The Equatorial Guinea LNG Market 2015-2025

14.4.1 Equatorial Guinea Large-Scale LNG Infrastructure Outlook

14.4.2 Equatorial Guinean FLNG Market Forecast 2015-2025

14.4.2.1 Equatorial Guinean FLNG Market Analysis

14.5 The Mozambique LNG Market 2015-2025

14.5.1 Mozambique Large-Scale LNG Infrastructure Outlook

14.5.1.1 Mozambique LNG Liquefaction Outlook

www.visiongain.com

Contents 14.5.1.2 Anadarko’s LNG Plan: The Onshore Option

14.5.1.3 ENI’s FLNG Option

14.5.1.4 Overall Drivers & Restraints on Mozambique LNG Liquefaction Investment

14.5.1.5 Mozambique Development Context & Tax Regime

14.5.1.6 Most Likely Scenario for Mozambique LNG Development

14.5.2 Mozambique FLNG Market Forecast 2015-2025

14.5.2.1 Mozambique FLNG Market Analysis

14.6 The Tanzanian LNG Market 2015-2025

14.6.1 Tanzanian LNG Liquefaction Outlook

14.6.2 Tanzanian FLNG Outlook

14.7 The South African LNG Market 2015-2025

14.7.1 South African FLNG Outlook

14.8 The Algerian LNG Market 2015-2025

14.8.1 Algerian Liquefaction Outlook

14.9 The Angolan LNG Market 2015-2025

14.9.1 Angola Liquefaction Outlook

14.9.2 Angolan FLNG Outlook

14.10 The Nigerian LNG Market 2015-2025

14.10.1 Nigeria Liquefaction Outlook

15. The South American LNG Market 2015-2025

15.1 South American LNG Infrastructure Outlook

15.2 The South American FLNG Market Forecast 2015-2025

15.2.1 The South American FLNG Market Analysis

15.2.2 Other South American FLNG Market Drivers & Restraints

15.2.3 Other South American FLNG Market Projects

15.2.4 South American FSRU Regasification Capacity Forecast 2015-2025

15.3 The Brazilian LNG Market 2015-2025

15.3.1 Brazilian LNG Infrastructure Outlook

15.3.2 The Brazilian FLNG Market Forecast 2015-2025

15.3.2.1 Brazilian FLNG Market Analysis

15.3.2.2 Outlook for Brazilian FLNG Units

15.3.2.3 Brazilian FLNG Market Drivers & Restraints

15.3.2.4 Brazilian FLNG Projects

15.3.3 Brazilian Small-Scale LNG Market Outlook

www.visiongain.com

Contents 15.3.3.1 LNG Fuelling Stations in Brazil

15.4 The Argentine LNG Market 2015-2025

15.4.1 Argentine LNG Infrastructure Outlook

15.4.2 Argentine FLNG Market Outlook

15.5 The Chilean LNG Market 2015-2025

15.5.1 Chilean LNG Infrastructure Outlook

15.6 The Ecuadorian LNG Market 2015-2025

15.6.1 Ecuadorian FLNG Market Outlook

15.7 The Colombian LNG Market 2015-2025

15.7.1 Colombian FLNG Market Outlook

15.8 The Uruguay LNG Market 2015-2025

15.8.1 Uruguay FLNG Market Outlook

16. PEST Analyses of the LNG Infrastructure Market 16.1 PEST Analysis of the Large-Scale Onshore LNG Infrastructure Market

16.2 PEST Analysis of the LNG Carrier Market 2015-2025

16.3 PEST Analysis of the FLNG Market 2015-2025

16.4 PEST Analysis of the Small Scale LNG Market 2015-2025

17. Expert Opinion 17.1 Cheniere Energy

17.1.1 Cheniere Energy, Sabine Pass & Corpus Christi

17.1.2 Why US LNG Exports Make Sense

17.1.3 Who is Buying Future US LNG?

17.1.4 The Impact on US LNG Competitiveness of ~$80/bbl Oil

17.1.5 Cheniere LNG Competitive Advantage

17.1.6 Future US LNG Export Volumes & the FERC Approval Process

17.1.7 Panama Canal Risk?

17.1.8 The Future of the LNG Trade and East Asian Demand

17.1.9 US Floating Barge Proposals

17.2 Stena Bulk

17.2.1 Stena Bulk Position

17.2.2 LNG Carrier Market Drivers

17.2.3 The Yamal LNG Project

www.visiongain.com

Contents 17.2.4 Long-term Contracts and the Spot Market

17.2.5 LNG Carrier Market Restraints

17.2.6 LNG Carrier Capacity

17.2.7 The Widening of the Panama Canal

17.2.8 LNG Carrier Charter Rates

17.3 Matthew Blycha, HFW LLP Interview

17.3.1 About HFW LLP

17.3.2 Impact of Oil and LNG Price Fall

17.3.3 Impact of a Functioning LNG FPSO

17.3.4 Impact of Oil Price on Financing FLNG Projects

17.3.5 Australian Public Response to FLNG

17.3.6 Australian FLNG Regulatory Issues

17.4 Robert Shivers, Lonestar FLNG (Houston Tx) Interview

17.4.1 About Lonestar FLNG

17.4.2 Issues in LNG FPSO Design and Alternatives

17.4.3 Shipyard Size and Availability of LNG Carriers for Conversion

17.4.4 Impact of the Oil Price on the FLNG Market

17.4.5 Future of FLNG in the United States

17.4.6 Competition and Rising Fees in the Panama Canal

17.4.7 Competing New Designs for LNG FPSOs

17.4.8 Final Thoughts

17.5 Swedegas

17.5.1 Swedegas Operations

17.5.2 Port of Gothenburg LNG Facility

17.5.3 LNG Ship Bunkering

17.5.4 LNG Fuel for Road Vehicles

17.5.5 Northern Europe and Project Opportunities

17.6 GasEner SRL

17.6.1 GasEner SLR Operations

17.6.2 Small Scale Liquefaction and Regasification

17.6.3 The LNG Supply Chain

17.6.4 LNG Ship Bunkering

17.6.5 The Small and Large Scale LNG Markets Relationship

17.6.6 LNG Satellite Stations

17.6.7 Regions for Small-Scale LNG

www.visiongain.com

Contents 18. Leading Companies in the LNG Infrastructure Market 18.1 Leading Companies in Large-Scale LNG Infrastructure Market

18.1.1 Leading LNG Liquefaction Operators

18.1.1.1 BP

18.1.1.2 BG Group

18.1.1.3 Cheniere Energy

18.1.1.4 Chevron

18.1.1.5 ConocoPhillips

18.1.1.6 ExxonMobil

18.1.1.7 Petronas

18.1.1.8 Royal Dutch Shell

18.1.1.9 Total S.A.

18.1.2 Other Players of Importance within the Global LNG Infrastructure Industry (Operators, Investors,

Engineering Companies)

18.2 Leading Operators in the LNG Carrier Market

18.2.1 Royal Dutch Shell plc, (Shell) Overview

18.2.1.1 Analysis of Shell

18.2.1.2 Future Outlook for Shell in the LNG Carrier Market

18.2.2 Nippon Yusen Kabushiki Kaisha (NYK) Overview

18.2.2.1 Analysis of NYK

18.2.2.2 Future Outlook for NYK in the LNG Carrier Market

18.2.3 Mitsui O.S.K. Lines, Ltd. (MOL) Overview

18.2.3.1 Analysis of MOL

18.2.3.2 Future Outlook for MOL in the LNG Carrier Market

18.2.4 Misc Berhad (Misc) Overview

18.2.4.1 Analysis of Misc

18.2.4.2 Future Outlook for Misc in the LNG Carrier Market

18.2.5 Teekay Corporation Analysis

18.2.5.1 Analysis of Teekay

18.2.5.2 Future Outlook for Teekay in the LNG Carrier Market

18.2.6 Maran Gas Maritime Inc. (MGM) Overview

18.2.6.1 Analysis of MGM

18.2.6.2 Future Outlook for MGM in the LNG Carrier Market

18.2.7 Golar LNG Limited (Golar) Overview

18.2.7.1 Analysis of Golar

18.2.7.2 Future Outlook for Golar in the LNG Carrier Market

www.visiongain.com

Contents 18.2.8 BW Group Overview

18.2.8.1 Analysis of BW Group

18.2.8.2 Future Outlook for BW Group in the LNG Carrier Market

18.2.9 GasLog Ltd Overview

18.2.9.1 Analysis of GasLog

18.2.9.2 Future Outlook for GasLog in the LNG Carrier Market

18.2.10 Kawasaki Kisen Kaisha (K Line) Ltd Overview

18.2.10.1 Analysis of K Line

18.2.10.2 Future Outlook for K Line in the LNG Carrier Market

18.3 Leading Companies in the FLNG Market

18.3.1 Leading Companies in the FSRU Market

18.3.2 Excelerate Energy

18.3.2.1 Excelerate Products and Services

18.3.2.2 Analysis of Excelerate Energy within the FLNG Market

18.3.2.3 Excelerate M&A Activity

18.3.2.4 Future Outlook for Excelerate Energy

18.3.2.5 Excelerate LNG FPSO Projects

18.3.3 Golar LNG

18.3.3.1 Golar Products and Services

18.3.3.2 Analysis of Golar LNG within the FLNG Market

18.3.3.3 Future Outlook for Golar LNG

18.3.3.4 Golar and Rosneft

18.3.3.5 Golar Projects

18.3.4 Höegh LNG

18.3.4.1 Höegh Products and Services

18.3.4.2 Analysis of Höegh LNG within the FLNG Market

18.3.4.3 Höegh M&A Activity

18.3.4.4 Future Outlook for Höegh

18.3.4.5 Höegh Projects

18.3.5 Leading Companies in the LNG FPSO Market

18.3.6 Shell and Associates

18.3.6.1 Analysis of Shell and Associates in the FLNG Market

18.3.6.2 Future Outlook of Shell and Associates

18.3.6.3 Shell and Associates Projects

18.3.7 Petronas

18.3.7.1 Analysis of Petronas in the FLNG Market

www.visiongain.com

Contents 18.3.7.2 Future Outlook of Petronas

18.3.7.3 Petronas LNG FPSO Projects

18.3.8.1 Exmar

18.3.8.2 Noble Energy

18.3.8.3 Woodside Petroleum

18.3.9 Leading FLNG Constructors

18.3.10 DSME and Associates

18.3.10.1 Analysis of DSME in the FLNG Market

18.3.10.2 DSME and Associates Future Outlook

18.3.10.3 DSME and Associates Projects

18.3.11 Samsung Heavy Industries (SHI)

18.3.11.1 Samsung Heavy Industries Future Outlook

18.3.11.2 Samsung Heavy Industries Projects

18.3.12 Hyundai Heavy Industries (HHI)

18.3.12.1 Hyundai Heavy Industries Future Outlook

18.3.12.2 Hyundai Heavy Industries Projects

18.3.13 Leading Service Providers in the FLNG Market

18.3.14 Black & Veatch

18.3.15 JGC Corporation

18.3.16 KBR

18.3.17 Saipem

18.3.18 Technip

18.3.19 Wison Offshore & Marine

18.3.20 Other Companies in the FLNG Market

18.4 Leading Companies in the Small-Scale LNG Market

18.4.1 Small-Scale LNG Technology Providers

18.4.1.1 Air Products & Chemicals Inc, (APCI)

18.4.1.2 Black & Veatch

18.4.1.3 Chart Industries, Inc. (Chart)

18.4.1.4 Cryostar Group

18.4.1.5 Wartsila Hamworthy

18.4.2 Small Scale LNG Companies

18.4.3 Gasnor Shell Overview

18.4.3.1 Gasnor Shell Analysis

18.4.3.2 Gasnor Shell Future Outlook

18.4.4 Skangass AS Overview

www.visiongain.com

Contents 18.4.4.1 Skangass AS Analysis

18.4.4.2 Skangass AS Future Outlook

18.4.5 Gazprom Overview

18.4.5.1 Gazprom Analysis

18.4.5.2 Gazprom Future Outlook

18.4.6 Energy Holdings Limited (ENN) Overview

18.4.6.1 ENN Analysis

18.4.6.2 ENN Future Outlook

18.4.7 Kunlun Energy Limited Overview

18.4.7.1 Kunlun Energy Analysis

18.4.7.2 Kunlun Energy Future Outlook

18.4.8 Other Notable Companies in the Small Scale LNG Market

19. Conclusions & Recommendations

19.1 Large-Scale Onshore LNG Infrastructure Conclusions

19.1.2 Key Findings

19.2 The LNG Carrier Market Conclusions

19.2.1 The LNG Carrier Market Outlook

19.2.2 Key Findings in the LNG Carrier Market

19.2.3 Recommendations for the LNG Carrier Market

19.3 Global FLNG Market Conclusions

19.3.1 Global FLNG Market Outlook

19.3.2 Key Findings

19.3.2.1 LNG FPSO Submarket

19.3.2.2 FSRU Submarket

19.3.2.3 Regional and Leading National FLNG Markets

19.3.3 Recommendations

19.4 Small-Scale Onshore LNG Infrastructure Conclusions

19.4.1 Market Outlook

19.4.2 Key Findings

19.4.3 Recommendations

www.visiongain.com Page 490

LNG Yearbook 2015: The Definitive Reference Guide to the Liquefied Natural Gas Infrastructure Market 2015-2025: Capex on Large-Scale Onshore Liquefaction & Regasification, Floating LNG (FLNG), Small-Scale LNG and LNG Carriers

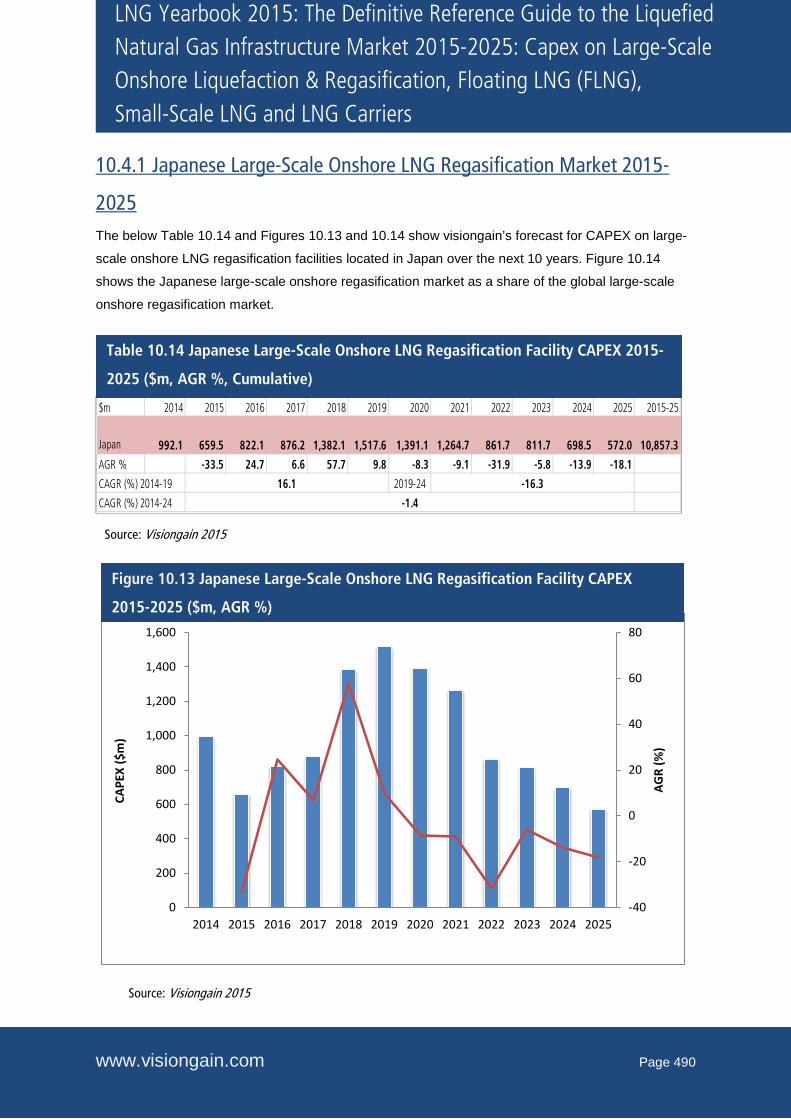

10.4.1 Japanese Large-Scale Onshore LNG Regasification Market 2015-

2025 The below Table 10.14 and Figures 10.13 and 10.14 show visiongain’s forecast for CAPEX on large-

scale onshore LNG regasification facilities located in Japan over the next 10 years. Figure 10.14

shows the Japanese large-scale onshore regasification market as a share of the global large-scale

onshore regasification market.

$m 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2015-25

Japan 992.1 659.5 822.1 876.2 1,382.1 1,517.6 1,391.1 1,264.7 861.7 811.7 698.5 572.0 10,857.3

AGR % -33.5 24.7 6.6 57.7 9.8 -8.3 -9.1 -31.9 -5.8 -13.9 -18.1

2019-24 -16.3

-1.4

16.1CAGR (%) 2014-19

CAGR (%) 2014-24

-40

-20

0

20

40

60

80

0

200

400

600

800

1,000

1,200

1,400

1,600

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

AGR

(%)

CAPE

X ($

m)

Source: Visiongain 2015

Table 10.14 Japanese Large-Scale Onshore LNG Regasification Facility CAPEX 2015-

2025 ($m, AGR %, Cumulative)

Figure 10.13 Japanese Large-Scale Onshore LNG Regasification Facility CAPEX

2015-2025 ($m, AGR %)

Source: Visiongain 2015

www.visiongain.com Page 499

LNG Yearbook 2015: The Definitive Reference Guide to the Liquefied Natural Gas Infrastructure Market 2015-2025: Capex on Large-Scale Onshore Liquefaction & Regasification, Floating LNG (FLNG), Small-Scale LNG and LNG Carriers

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2015-2025

CAPEX $m 408.3 751.1 670.1 715.8 687.0 648.8 513.2 572.6 483.9 478.0 558.0 478.0 6556.5

AGR (%) 10.3% 15.4% 8.8% -5.1% -7.8% -27.4% -4.9% -5.2% -1.8% 0.0% 0.0%

CAGR (%) 2015-20 2020-25-7.3% -1.4%

CAGR (%) 2015-25 -4.4%

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

0

100

200

300

400

500

600

700

800

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

AGR

(%)

CAPE

X $m

Year

Source: Visiongain 2015

Table 10.16 Japanese LNG Carrier Market Forecast 2015-2025 ($m, AGR %, CAGR %,

Cumulative)

Source: Visiongain 2015

Figure 10.17 Japanese LNG Carrier Forecast 2015-2025 ($m, AGR%)

www.visiongain.com Page 676

LNG Yearbook 2015: The Definitive Reference Guide to the Liquefied Natural Gas Infrastructure Market 2015-2025: Capex on Large-Scale Onshore Liquefaction & Regasification, Floating LNG (FLNG), Small-Scale LNG and LNG Carriers

17. Expert Opinion

17.1 Cheniere Energy Katie Pipkin is Senior VP of Business Development and Communications at Cheniere Energy.

She has held this position since March 2014, and prior to that was the VP of Finance, during which

time she helped secure the financing for the Sabine Pass LNG liquefaction project. Her extensive

experience within the energy industry spans finance, business development and investor relations

functions. Between 2004 and 2007, she worked at Lehman Brothers as a sell-side analyst for the

natural gas sector. Prior to this she spent six years at Dynegy within their accounting/finance and

investor relations departments. Ms. Pipkin earned a B.B.A in Finance from the University of Texas.

Visiongain interviewed Ms. Pipkin in October 2014 and would like to thank her for her astute insights.

Cheniere Energy is a Houston-based energy company primarily engaged in LNG-related

businesses. Cheniere is developing nine liquefaction trains overall for 40.5 mmtpa- six LNG trains as

part of a liquefaction project adjacent to its existing Sabine Pass LNG regasification terminal in

Cameron Parish, Louisiana, with aggregate capacity of approximately 27 mmtpa, and another three

LNG trains at a soon to be developed LNG export terminal near Corpus Christi, Texas, with aggregate

capacity of up to 13.5 mmtpa.

17.1.1 Cheniere Energy, Sabine Pass & Corpus Christi Visiongain: Please describe the work of Cheniere Energy and your involvement in the LNG industry. Katie Pipkin: We are currently developing two liquefaction projects – the Sabine Pass Liquefaction

facility and the Corpus Christi liquefaction facility.

The Sabine Pass Liquefaction facility will be the first LNG export terminal to be built in over 40 years

in North America. Construction is well underway on the first four liquefaction trains and we expect first

LNG production by late 2015. An expansion with trains 5 & 6 is in the final stages of the regulatory

process and we expect to reach a final investment decision in 2015. When complete, the Sabine Pass

liquefaction facility will be capable of exporting approximately 27 mmtpa of LNG, equivalent to

approximately 3.8 bcf/d.

The Sabine Pass liquefaction project is a brownfield development and several of the existing assets at

the Sabine Pass regasification terminal will be used for exporting LNG, including the storage tanks

and marine berths. We are adding liquefaction trains at the site that have been designed using the

ConocoPhillips Optimized Cascade Process technology, a proven technology that has been used in

www.visiongain.com Page 703

LNG Yearbook 2015: The Definitive Reference Guide to the Liquefied Natural Gas Infrastructure Market 2015-2025: Capex on Large-Scale Onshore Liquefaction & Regasification, Floating LNG (FLNG), Small-Scale LNG and LNG Carriers

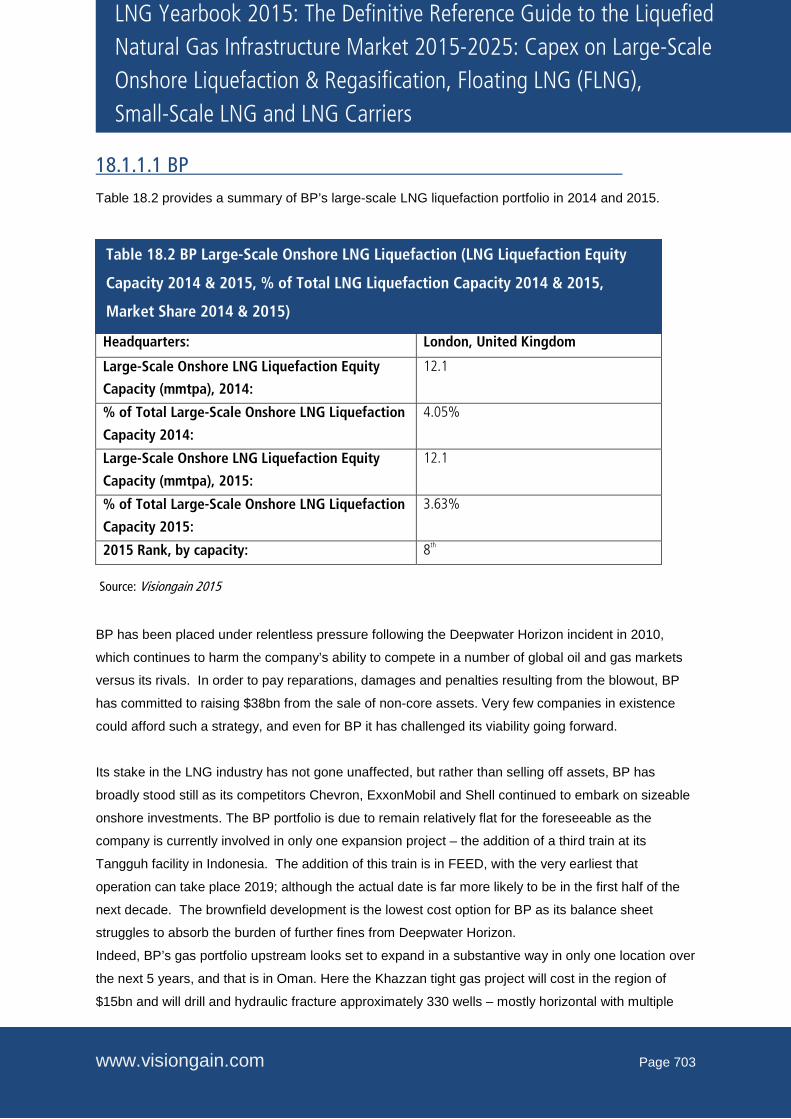

18.1.1.1 BP Table 18.2 provides a summary of BP’s large-scale LNG liquefaction portfolio in 2014 and 2015.

Headquarters: London, United Kingdom

Large-Scale Onshore LNG Liquefaction Equity

Capacity (mmtpa), 2014:

12.1

% of Total Large-Scale Onshore LNG Liquefaction

Capacity 2014:

4.05%

Large-Scale Onshore LNG Liquefaction Equity

Capacity (mmtpa), 2015:

12.1

% of Total Large-Scale Onshore LNG Liquefaction

Capacity 2015:

3.63%

2015 Rank, by capacity: 8th

BP has been placed under relentless pressure following the Deepwater Horizon incident in 2010,

which continues to harm the company’s ability to compete in a number of global oil and gas markets

versus its rivals. In order to pay reparations, damages and penalties resulting from the blowout, BP

has committed to raising $38bn from the sale of non-core assets. Very few companies in existence

could afford such a strategy, and even for BP it has challenged its viability going forward.

Its stake in the LNG industry has not gone unaffected, but rather than selling off assets, BP has

broadly stood still as its competitors Chevron, ExxonMobil and Shell continued to embark on sizeable

onshore investments. The BP portfolio is due to remain relatively flat for the foreseeable as the

company is currently involved in only one expansion project – the addition of a third train at its

Tangguh facility in Indonesia. The addition of this train is in FEED, with the very earliest that

operation can take place 2019; although the actual date is far more likely to be in the first half of the

next decade. The brownfield development is the lowest cost option for BP as its balance sheet

struggles to absorb the burden of further fines from Deepwater Horizon.

Indeed, BP’s gas portfolio upstream looks set to expand in a substantive way in only one location over

the next 5 years, and that is in Oman. Here the Khazzan tight gas project will cost in the region of

$15bn and will drill and hydraulic fracture approximately 330 wells – mostly horizontal with multiple

Table 18.2 BP Large-Scale Onshore LNG Liquefaction (LNG Liquefaction Equity

Capacity 2014 & 2015, % of Total LNG Liquefaction Capacity 2014 & 2015,

Market Share 2014 & 2015)

Source: Visiongain 2015