live-#3345829-v1-s&r - coffey powerpoint presentation · pdf filecairns rectangular pitch...

TRANSCRIPT

COFFEY PROJECTS INSERT HEADING HERE

Cairns Rectangular Pitch Stadium Needs Study Draft Report PresentationOctober 2011

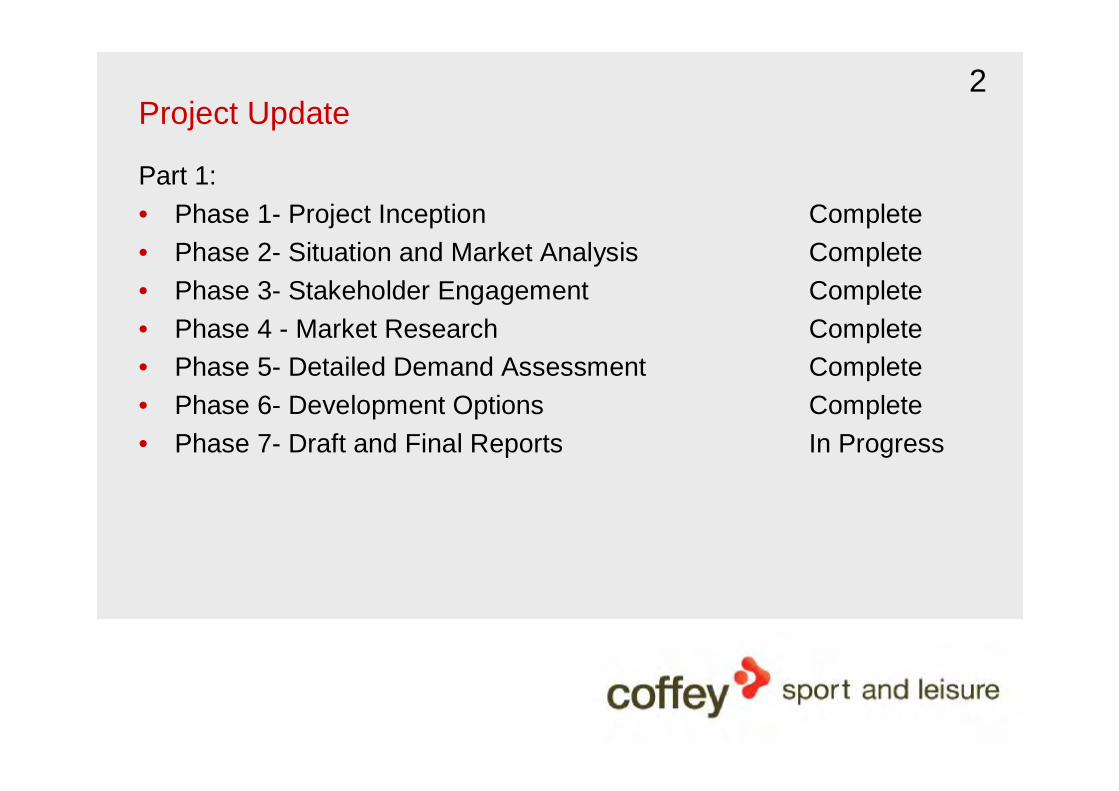

2Project Update

Part 1:• Phase 1- Project Inception Complete• Phase 2- Situation and Market Analysis Complete• Phase 3- Stakeholder Engagement Complete• Phase 4 - Market Research Complete• Phase 5- Detailed Demand Assessment Complete• Phase 6- Development Options Complete• Phase 7- Draft and Final Reports In Progress

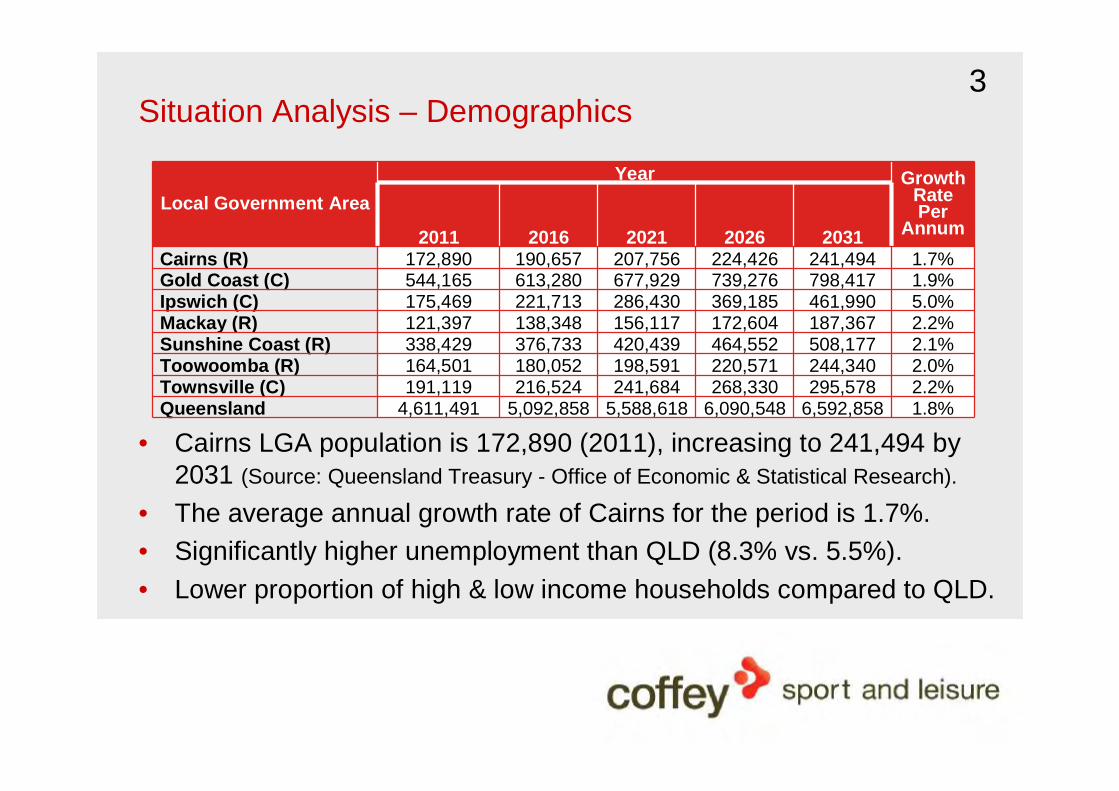

3Situation Analysis – Demographics

• Cairns LGA population is 172,890 (2011), increasing to 241,494 by 2031 (Source: Queensland Treasury - Office of Economic & Statistical Research).

• The average annual growth rate of Cairns for the period is 1.7%.• Significantly higher unemployment than QLD (8.3% vs. 5.5%).• Lower proportion of high & low income households compared to QLD.

Local Government Area Year Growth

Rate Per

Annum2011 2016 2021 2026 2031Cairns (R) 172,890 190,657 207,756 224,426 241,494 1.7%Gold Coast (C) 544,165 613,280 677,929 739,276 798,417 1.9%Ipswich (C) 175,469 221,713 286,430 369,185 461,990 5.0%Mackay (R) 121,397 138,348 156,117 172,604 187,367 2.2%Sunshine Coast (R) 338,429 376,733 420,439 464,552 508,177 2.1%Toowoomba (R) 164,501 180,052 198,591 220,571 244,340 2.0%Townsville (C) 191,119 216,524 241,684 268,330 295,578 2.2%Queensland 4,611,491 5,092,858 5,588,618 6,090,548 6,592,858 1.8%

4Situation Analysis – Literature Review• As part of the analysis the following documents were reviewed:

– Cairns Regional Council Corporate Plan 2009-2014.– Parks and Recreation Strategic Plan 2010-2015.– Tropical North Queensland Events Strategy 2010-2015.– Tourism Queensland - Tourism Action Plan to 2012.– Events Queensland Regional Development Program.– Toward Q2: Tomorrow’s Queensland.– Feasibility Study of the Barlow Park Master Plan (2003).

5Situation Analysis – Literature Review• Key outcomes include:

– Council’s Parks and Recreation Strategic Plan and Corporate Plan identify the requirement to undertake a study into a stadium.

– The TNQ Event Strategy indicates that a 20,000 seat stadium is currently not considered viable and a staged upgrade of Barlow Park is considered.

– Many of the documents do not specifically mention the development of a stadium, however a development would support many of the principles, goals and objects within these documents.

6Situation Analysis – Trends and Benchmarking

• Stadium design and the product offering is continuing to evolve, key areas include: – Spectators Experience: ‘Game is only part of experience’– Corporate Experience: ‘Not just a traditional function space’– Membership experience: ‘A different experience from the normal punter’– Design: ‘Must cater for multiple users’– Ancillary Services: ‘More than just a sporting venue’

• Queensland Stadia have unique design trends including:– Multiple levels of corporate hospitality.– Focus on outdoor entertainment.

7Situation Analysis – Competition

Venue Seats CapacityAnnual Core Tennant Use

(NRL, Super 15’s, A-League)

Skilled Park (Gold Coast) 27,400 27,400 25

Suncorp Stadium (Brisbane) 52,500 52,500 33

Dairy Farmers Stadium (Townsville) 26,500 26,500 12

Virgin Australia Stadium (Mackay) 2,000 12,000 0

Ausgrid Stadium (Newcastle) 17,000 23,000 25

Blue Tongue Stadium (Gosford) 20,000 20,000 19

Canberra Stadium (Canberra) 25,011 25,011 20

NIB Stadium (Perth) 20,000 20,000 21

Win Stadium (Wollongong) 11,000 20,000 6

8Situation Analysis – Competition

• There are a number of stadium developments in Queensland being considered including at Townsville, Rockhampton and Ipswich.

• When considering Townsville as the closest competition the following observations are made:– Dairy Farmers Stadium is owned/managed by Stadiums Qld (consulted as

part of study) with the State covering operating loss and capital works.– North Qld Cowboys team (only anchor tenant).– No new (or existing) national teams for (rectangular codes) currently

requiring a stadium in the region, therefore Cairns not competing with Townsville on this aspect.

– Some competition will exist for annual and/or one-off events in various codes, which is consistent with the current situation.

– The Cowboys new 30,000 seat stadium proposal is aspirational with development site still being used by QRN.

9Situation Analysis – Stadia Financial Performance

• Based on high level discussions with Stadium operators (including Queensland stadiums) the financial performance of stadiums are in general marginal (especially when factoring in significant maintenance, sinking fund/renewal funding and depreciation costs).

• Stadiums need 20+ plus significant events annually to breakeven operationally (excluding significant maintenance, sinking fund/renewal funding and depreciation costs).

10Situation Analysis – Stadia Financial Performance

• Stadiums Queensland currently manage the following stadiums:– Metricon Stadium (management outsourced to the Gold Coast Suns)

• Queensland Government $71.9m in funding;• Other funding parties Commonwealth Government $36m; Gold Coast

City Council $23m; and the AFL $13.3m.– The Gabba.

• $50 million Queensland Government funding for 2005 redevelopment.– Suncorp Stadium.

• $280 million Queensland Government funding.– Skilled Park.

• $160 million Queensland Government funding.– QSAC.– Dairy Farmers Stadium.

11Situation Analysis – Stadia Financial Performance

• The Queensland State Government was a significant capital funding partner in the above facilities.

• In 2008/2009 the Queensland Government contributed $70 million into the upkeep and development of sports infrastructure operated by Stadiums Queensland.

• Verbal advice from Stadiums Queensland is that these venues are managed around an objective of operational break-even, with the sinking fund and large capital works funded by the Queensland State Government on a case-by-case basis.

12Consultation – Overview

• Consultation/engagement included four main methods:– Workshop.– One on One Interviews.– Focus Group.– Market Research.

• Key groups consulted included:– National/State/Local Sporting organisations.– Government Departments.– Community and business groups.

13Consultation – Key Themes

• The key themes identified as part of the engagement process included:– Stadium Size.– Stadium Location.– Existing Facilities.– Stadium Content.– Elite Training Facilities.– Sports House.– Sports Development.– Economic Development.– Sustainability.– Multi-Purpose and Ancillary Facilities to activate the precinct.

14Consultation – Issues and Opportunities

Issues Opportunities

• Poor standard of current facilities.

• Mix of sports (athletics and

rectangular sports).

• Spectator experience.

• Attracting events and costs.

• On going viability.

• No core major tenant.

• Cost of use by sports.

• Location and access.

• Improved facilities and spectator

experience.

• National event attraction.

• Staged approach to delivery.

• Economic/tourism development.

• Development of facilities to support local

sport.

• Inclusion of other facilities to activate

the site.

• Possible consideration of integrating

showground and Barlow Park precinct.

15Market Research Findings – General• 75% rated current Barlow Park facilities poor to average. This value

is higher when compared to Council’s Community Satisfaction Survey where Barlow Park facilities which scored 3.5 out 5.

• 60% believe athletics track impacts spectator experience.• Strongest support is for NRL games then Super 15’s and A-League.• 75.6% would definitely/very likely attend national competition games.• 42.2% indicated they would attend 7-12 games.• 33% indicated extremely interested in stadium membership.• 20.7% would like a membership which included 1-7 games and

79.2% would like 8 plus games.• Other facilities identified for inclusion at a stadium include:– Elite training facilities.– Sports administration facilities.

16Market Research Findings – Business

• 42.2% of respondents spend under $5,000 annually on hospitality.• Current hospitality undertaken by companies include restaurants

(61.4%), Sporting events (54.3%) and functions (48.6%). • 52.9% of respondents believe there is a lack of hospitality options in

Cairns.• 42.9% of respondents were interested in a casual corporate

experience. • Of those that had undertaken corporate hospitality at rectangular

sporting events, 84.2% of respondents had attended rugby league.• Highest interest was to attending NRL games (34.4% definitely

interested) then Super 15’s (32.8%) and A-League (21.9%).

17Market Research Findings – Business

• 61.3% of respondents indicated they would likely use events at the stadium between 1-5 times per year with 35.9% bringing 5-8 guests.

• 46.9% were only ‘maybe interested’ or ‘Not interested at all’ at attending NRL games and 43% and 59.4% indicating the same response for Super 15’s and A-League.’

• 61.3% of respondents indicated that their company would likely use events at the stadium between 1-5 times per year with 35.9% bringing 5-8 guests.

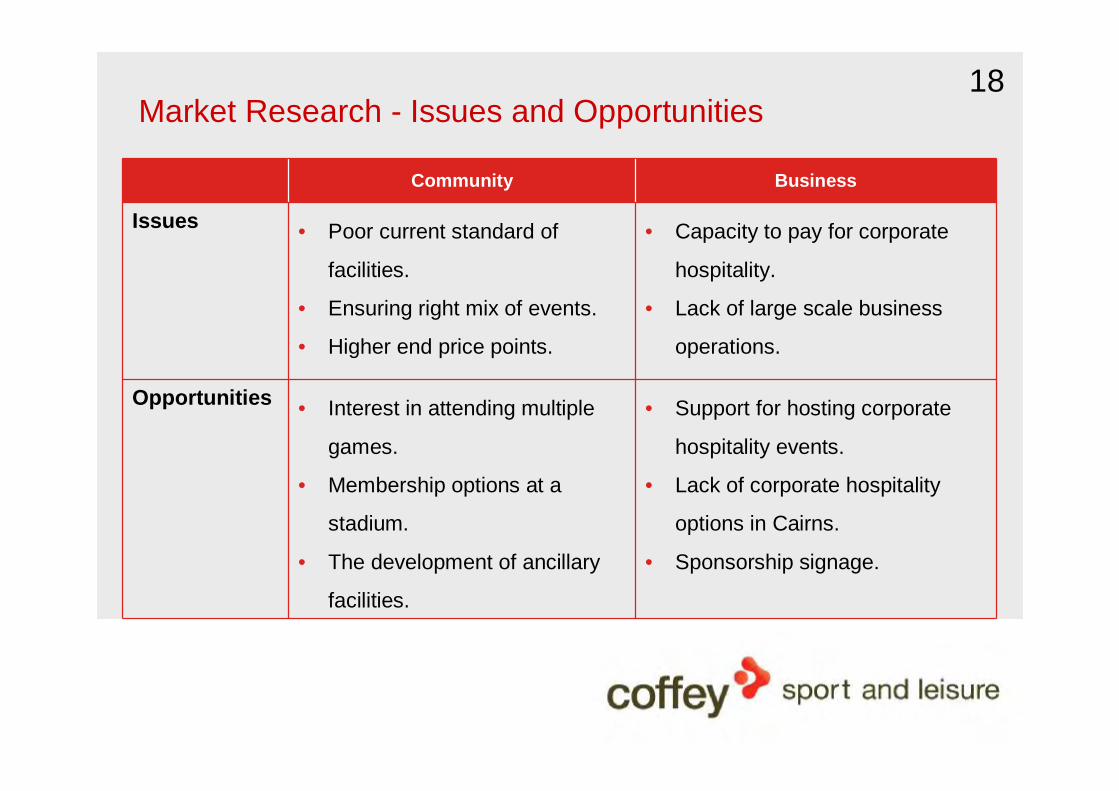

18Market Research - Issues and Opportunities

Community Business

Issues • Poor current standard of

facilities.

• Ensuring right mix of events.

• Higher end price points.

• Capacity to pay for corporate

hospitality.

• Lack of large scale business

operations.

Opportunities • Interest in attending multiple

games.

• Membership options at a

stadium.

• The development of ancillary

facilities.

• Support for hosting corporate

hospitality events.

• Lack of corporate hospitality

options in Cairns.

• Sponsorship signage.

19Demand Assessment - Overview• In considering likely demand for a stadium, CSL considered a range

of factors, including:– Consultation (including NRL, Cronulla Sharks, Sydney Roosters,

QRL/Queensland Red, A-League and Brisbane Roar).– Market research.– Trend data.– Competition.

• Demand analysis has considered likely:– Content– Spectator attendance– Competition. NB: Anecdotal information suggests that a stadium of size greater than

15,000-20,000 seats needs a population catchment of in the order of 300,000 plus people, which is the case of many of the stadium location included in the competitor analysis (Slide 7).

20Demand Assessment - Overview

• National Rectangular Sports (NRL, Super 15’s, A-League)– All codes/clubs indicated a level of interest in playing games in Cairns.– It is unlikely that a national Cairns team would form part of a national

competition in the short – medium term.– Currently no demand by any national code/club for a new stadium.– Number of games would need to be limited due to potential impacts on

membership at home venues.– Key decision making driver for codes/club was focused on the financial

deal/return. – Based on consultation an indicative annual national competition stadium

content base includes:A-League NRL Super 15’s

Trial/Preseason 1 1 1Home 1-2 1-2 1

21Demand Assessment – Expansion

• Expansion of National Code Sports is Generally Governed by:– Growth in TV Audience.– Growth of the Game linked to population growth.

• NRL Expansion Plans.• Verbal advice from the NRL is that growth in the NRL competition,

should it decide to expand, is likely to be in Brisbane, Perth and/or the Central Coast of NSW.

• Expansion is likely to be based around growing TV audiences and population growth allowing for growth of the game.

22Demand Assessment – Expansion

• A-League Expansion Plan• Verbal advice from the FFA is that growth in the A-League

competition is unlikely to happen in the short term.• When it does it is likely to focus on population growth areas such as

Western Sydney. • If the FNQ was to be a market then the FFA’s priority would likely be

re-establishment of a team in Townsville.• Expansion of National Code Sports :

– Super Rugby Expansion Plans.• Queensland Rugby indicated that it saw the Queensland Reds as

“Queensland's” team and therefore had no plans to add another Super Rugby team to the Queensland market.

• The ARU indicated that they had no intention at this stage to expand the Super Rugby Competition in Australia.

23Demand Assessment - Overview

• Attendance (National Rectangular Sports)– A review of national attendance figures (excluding finals) over the last

five years highlights the following:

– Consultation with national codes/clubs was that consideration tostadium size should be measured.

Year A-League NRL Super 15’s2006-07 12,898 15,474 21,241

2007-08 14,644 15,308 20,483

2008-09 12,116 15,523 19,2542009-10 9,719 15,896 19,3012010-11 8,429 16,576 19,2165 Year

Average 11,561 15,755 19,899

24Demand Assessment - Overview

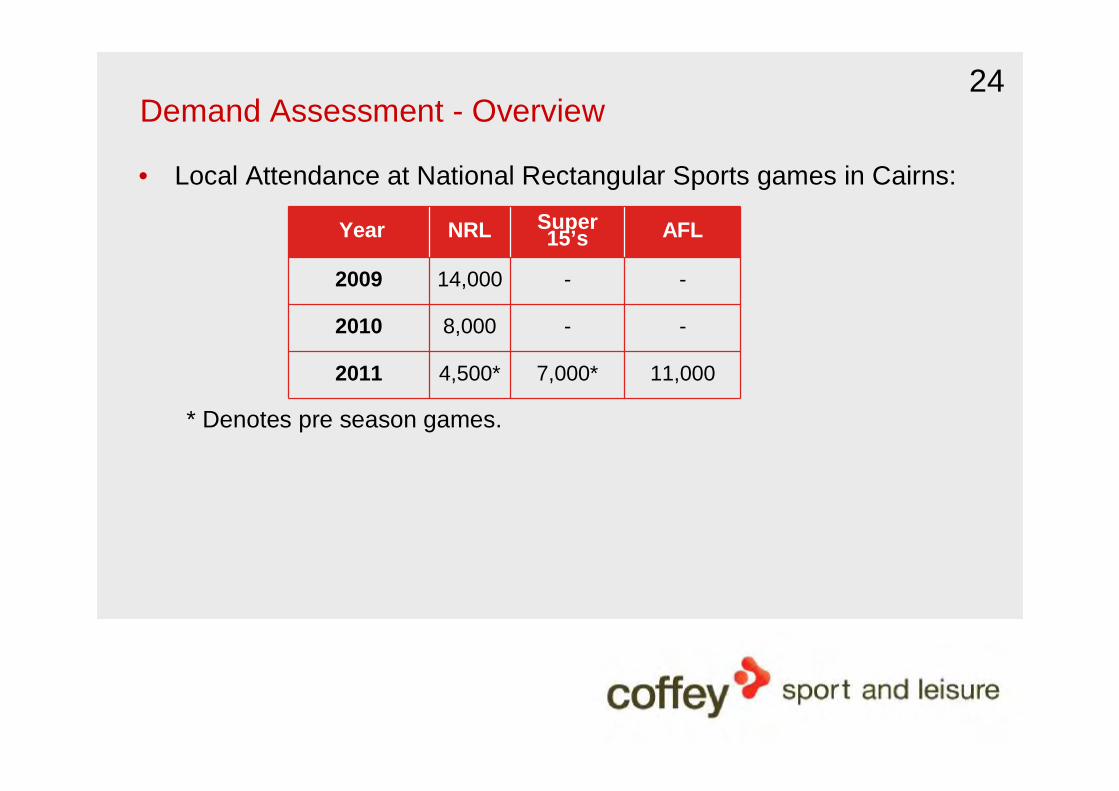

• Local Attendance at National Rectangular Sports games in Cairns:

* Denotes pre season games.

Year NRL Super 15’s AFL

2009 14,000 - -

2010 8,000 - -

2011 4,500* 7,000* 11,000

25Demand Assessment - Overview

• Market Research– Interest in attending national sporting games was strong.– Strong desire to attend multiple games and to purchase memberships.– Spectator experience is being impacted by current facilities at Barlow Park

including viewing due to the athletics track. • Competition

– Queensland has 5 existing rectangular stadiums ranging in standard and size.

– Queensland does not appear to have a strategic position on stadium development.

– There are a number of stadium proposals being considered in Queensland including 2 new stadiums and the possible upgrade of Townsville and Ballymore.

26Demand Assessment - Overview

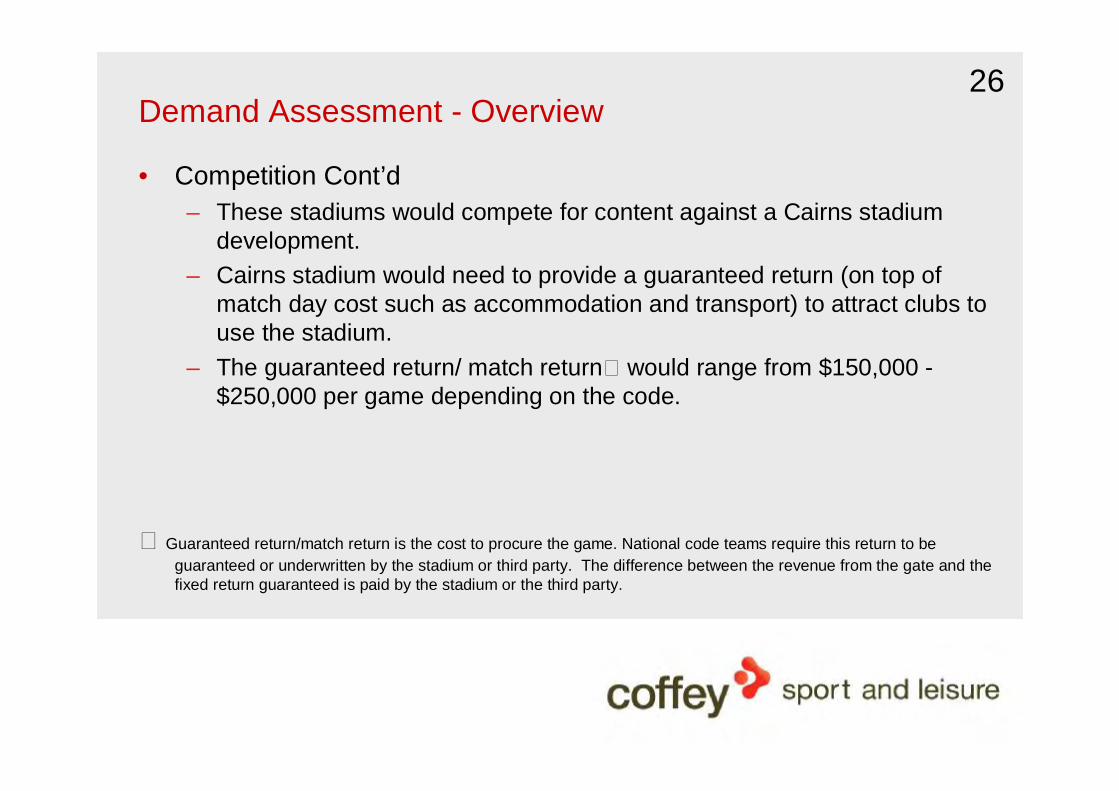

• Competition Cont’d– These stadiums would compete for content against a Cairns stadium

development.– Cairns stadium would need to provide a guaranteed return (on top of

match day cost such as accommodation and transport) to attract clubs to use the stadium.

– The guaranteed return/ match return would range from $150,000 -$250,000 per game depending on the code.

Guaranteed return/match return is the cost to procure the game. National code teams require this return to be guaranteed or underwritten by the stadium or third party. The difference between the revenue from the gate and the fixed return guaranteed is paid by the stadium or the third party.

27Demand Assessment - Summary• In assessing the demand the following key outcomes are identified:

– Content not likely to include Cairns based national team in the short to medium term.

– Current facilities at Barlow Park have been identified by spectators and sports as an issue for staging games in Cairns.

– While national codes/club have an interest in playing games in Cairns there is not direct demand for the development of a stadium to address a current market need.

– Codes/clubs will require significant financial returns.– Available stadium content is limited and competition for content will

continue to be high amongst stadiums in Queensland (and interstate). – Initial market research indicates strong local support to attend a stadium

staging national competition games.– Average attendance at NRL, Super 15’s and A-League all under 20,000

spectators.

28Demand Assessment – 10,000 seats/20,000 capacity• 10,000 seats/20,000 capacity was chosen as the optimum capacity on

the following basis:• Likely content;• Code expectation as to minimum seats and quality of seats;• Demand in the Cairns market:

– Average attendance at previous events in Cairns;– Direct market research in Cairns;

• Average sporting code attendance nationally; • Design considerations:

– Optimal design and spectator experience;– Seating on all four sides of venue;– Maximising amenity, player facilities, media facilities and

corporate facilities in the Western Grandstand.

29Demand Assessment – 10,000 seats/20,000 capacity• 10,000 seats/20,000 capacity was chosen as the optimum capacity on

the following basis:• Creating a point of differentiation in the Queensland stadia market

(there are at present no current of planned facilities of this size);• Allows for the master planned development of the facility up to 20,000

if supported by demand in the future;• Reasonable capital costs;• Reasonable operating costs to allow community sports to continue to

use the stadia.

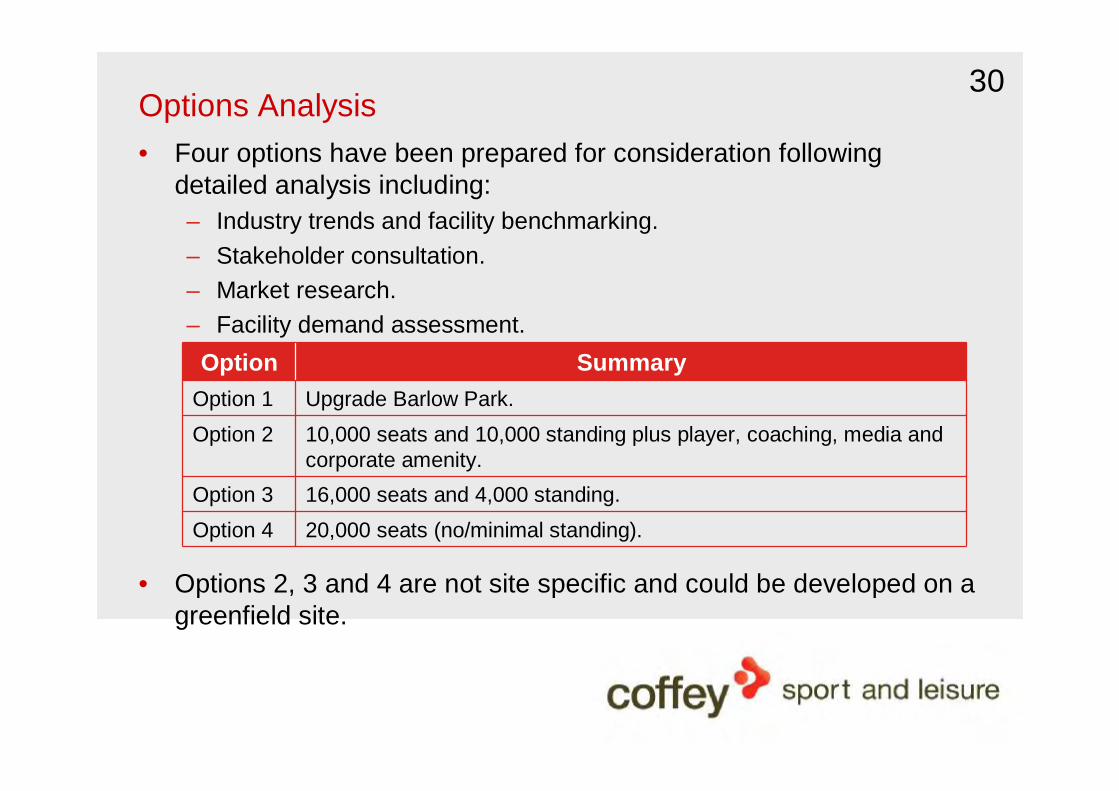

30Options Analysis• Four options have been prepared for consideration following

detailed analysis including:– Industry trends and facility benchmarking. – Stakeholder consultation.– Market research.– Facility demand assessment.

• Options 2, 3 and 4 are not site specific and could be developed on a greenfield site.

Option SummaryOption 1 Upgrade Barlow Park.Option 2 10,000 seats and 10,000 standing plus player, coaching, media and

corporate amenity.Option 3 16,000 seats and 4,000 standing.Option 4 20,000 seats (no/minimal standing).

31Option 1 – Summary

• Maintain existing facilities at Barlow Park.• Continue to upgrade in line with previous Master Plan.• Consider development options that improve venue for spectators,

player and officials, including:– Removal of the athletics track.– Improved corporate facilities.– Improved food and beverage facilities.– Upgrade lights.– Additional undercover seating.– Improved media facilities.

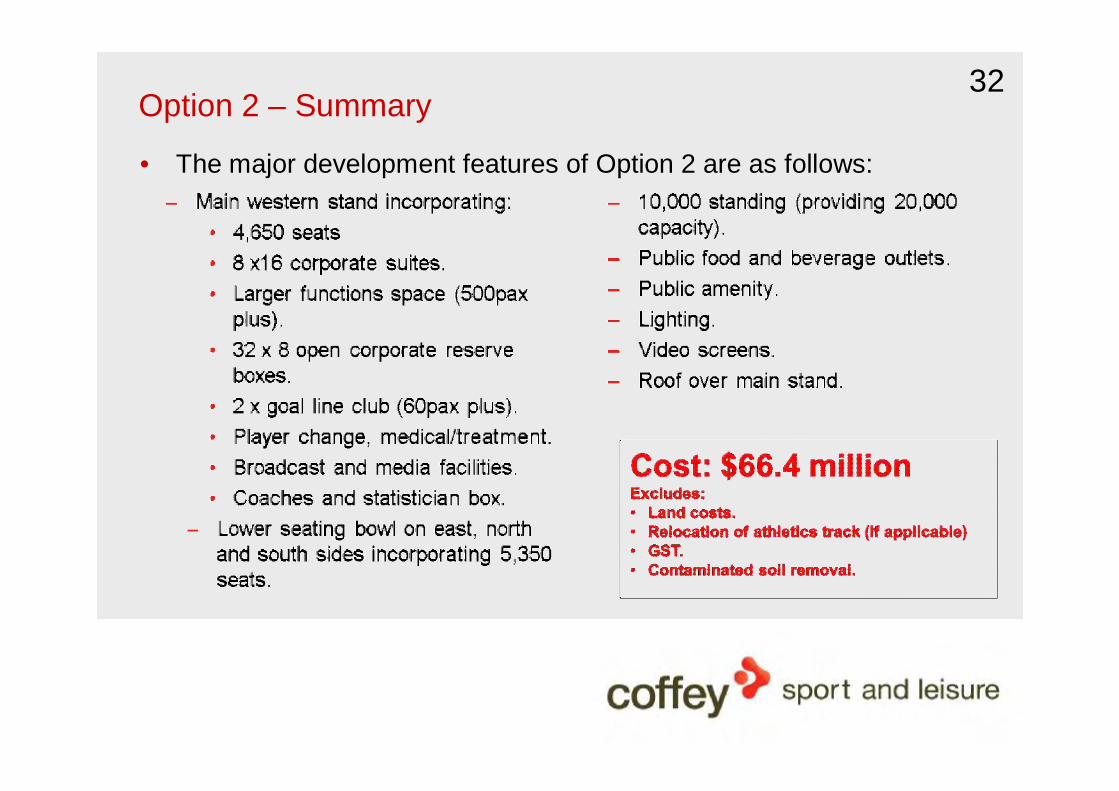

32Option 2 – Summary

• The major development features of Option 2 are as follows:

33Option 3 and 4 – Summary

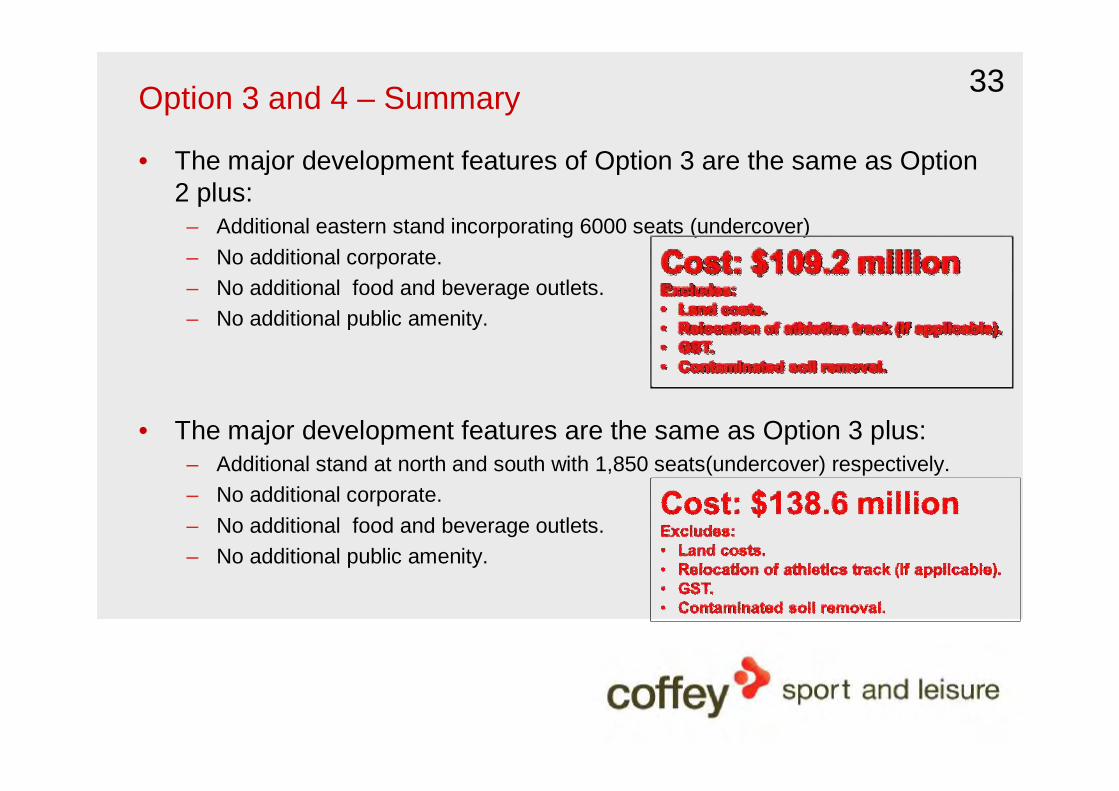

• The major development features of Option 3 are the same as Option 2 plus:– Additional eastern stand incorporating 6000 seats (undercover)– No additional corporate.– No additional food and beverage outlets.– No additional public amenity.

• The major development features are the same as Option 3 plus:– Additional stand at north and south with 1,850 seats(undercover) respectively.– No additional corporate.– No additional food and beverage outlets.– No additional public amenity.

34Options Analysis

Pluses Minuses

Option 1 – Provides affordable option for community sport.

– Maintains multi use focus as a community recreation facility.

– Potential for reduced capital cost option that may partly address sports issues.

– Spectator experience not addressed.– Does not address all sports issues. – Attracting and staging national games will be

impacted and compromised unless appropriate upgrades are made to address current issues.

– Conflict between user sports.

Option 2 – Larger capacity in terms of seating and more undercover seating.

– Creates atmosphere with seating around the ground.

– Improved corporate facilities.– Improved player/official amenity.– Improved broadcast and media amenity.– Possible improved non match day revenue

through functions business, concerts and entertainment events.

– Capacity/size point of difference in market.– Potential economic benefit to town/region

from staging larger events.

– Capital cost to deliver additional seating and corporate facilities.

– Ongoing operational costs of the stadium.– Ongoing cost of maintaining two stadiums if

Barlow Park is maintained.– Affordability of use by community level sport.– Costs associated with separating athletics

and field.– Risk of not attracting required level of content

on an annual basis.– Potential competition from other existing and

potential stadiums.

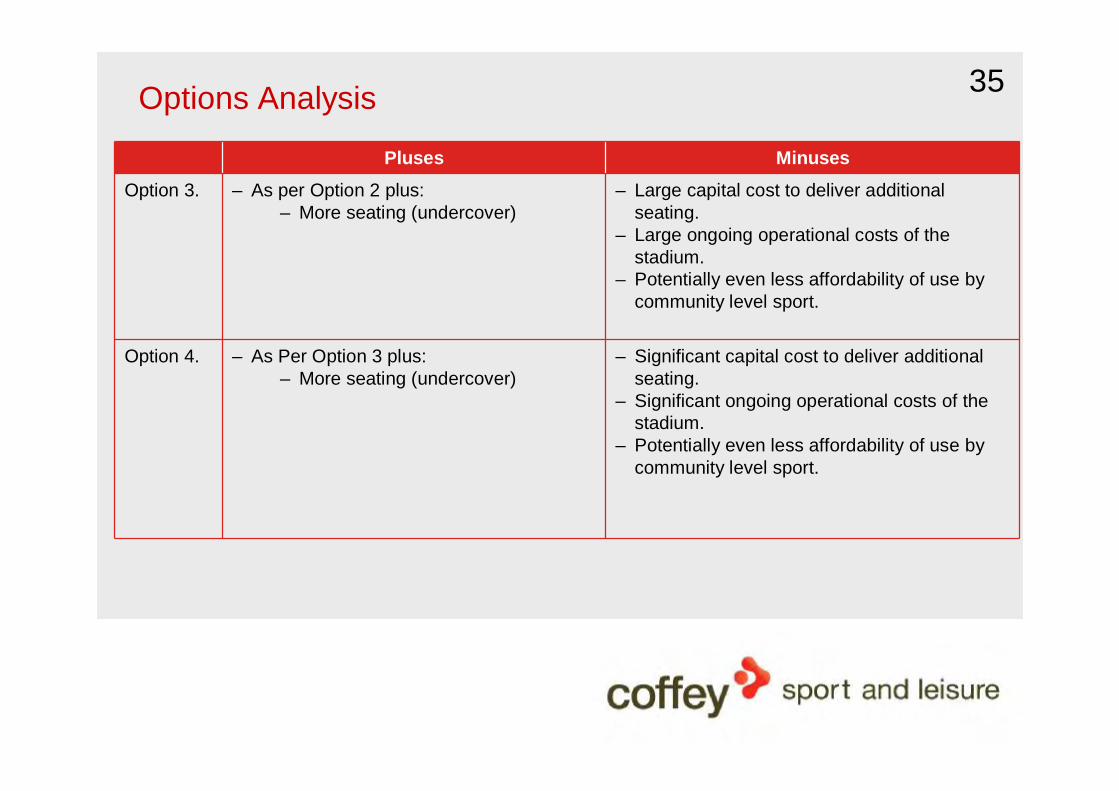

35Options Analysis

Pluses Minuses

Option 3. – As per Option 2 plus:– More seating (undercover)

– Large capital cost to deliver additional seating.

– Large ongoing operational costs of the stadium.

– Potentially even less affordability of use by community level sport.

Option 4. – As Per Option 3 plus:– More seating (undercover)

– Significant capital cost to deliver additional seating.

– Significant ongoing operational costs of the stadium.

– Potentially even less affordability of use by community level sport.

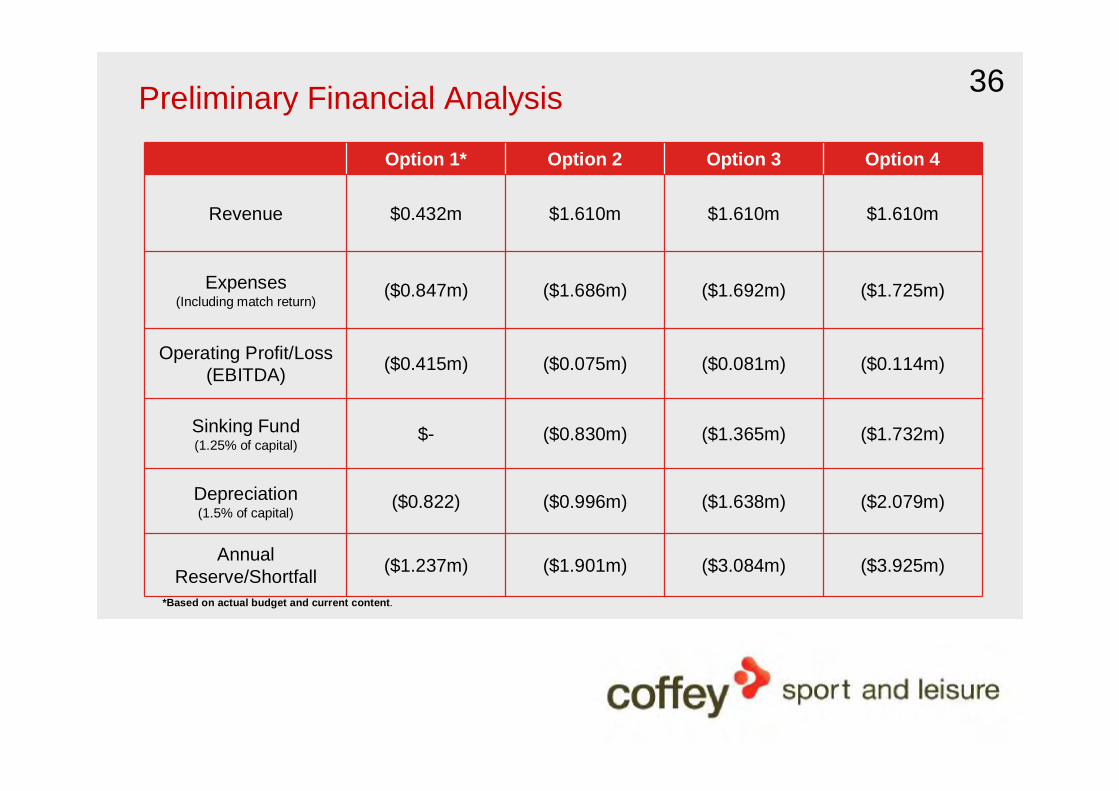

36Preliminary Financial Analysis

Option 1* Option 2 Option 3 Option 4

Revenue $0.432m $1.610m $1.610m $1.610m

Expenses(Including match return)

($0.847m) ($1.686m) ($1.692m) ($1.725m)

Operating Profit/Loss(EBITDA) ($0.415m) ($0.075m) ($0.081m) ($0.114m)

Sinking Fund(1.25% of capital)

$- ($0.830m) ($1.365m) ($1.732m)

Depreciation(1.5% of capital)

($0.822) ($0.996m) ($1.638m) ($2.079m)

Annual Reserve/Shortfall ($1.237m) ($1.901m) ($3.084m) ($3.925m)

*Based on actual budget and current content.

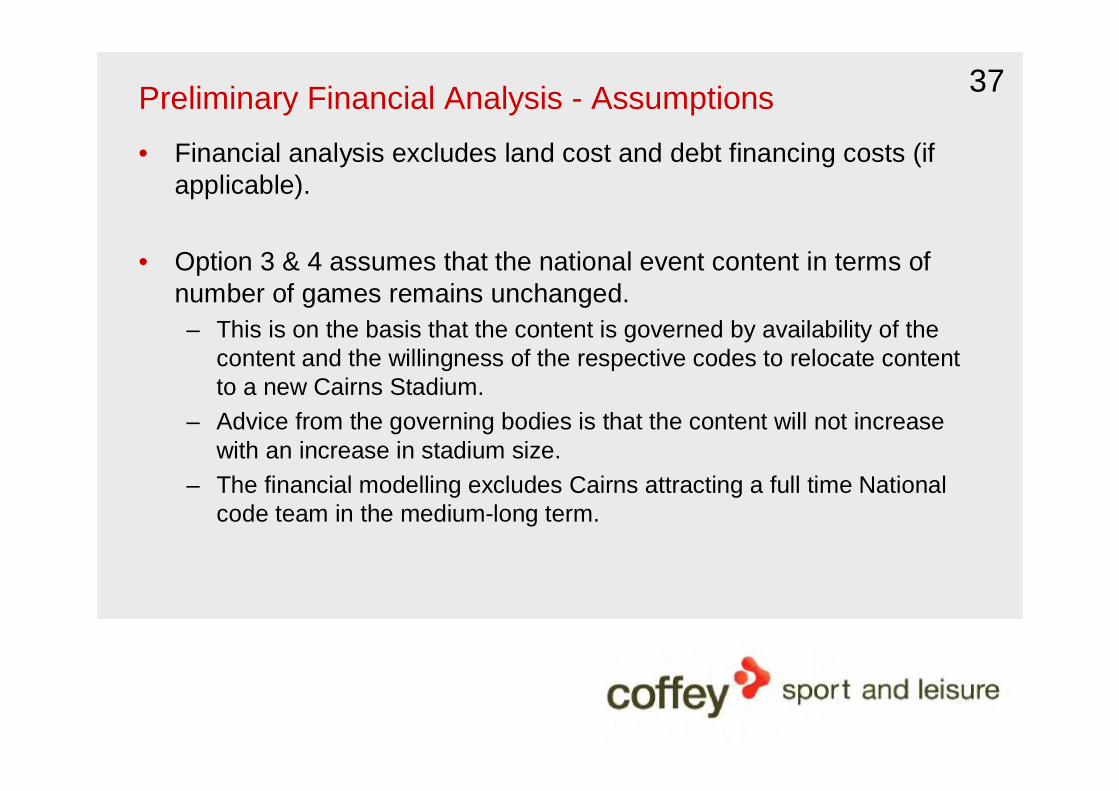

37Preliminary Financial Analysis - Assumptions• Financial analysis excludes land cost and debt financing costs (if

applicable).

• Option 3 & 4 assumes that the national event content in terms ofnumber of games remains unchanged.– This is on the basis that the content is governed by availability of the

content and the willingness of the respective codes to relocate content to a new Cairns Stadium.

– Advice from the governing bodies is that the content will not increase with an increase in stadium size.

– The financial modelling excludes Cairns attracting a full time National code team in the medium-long term.

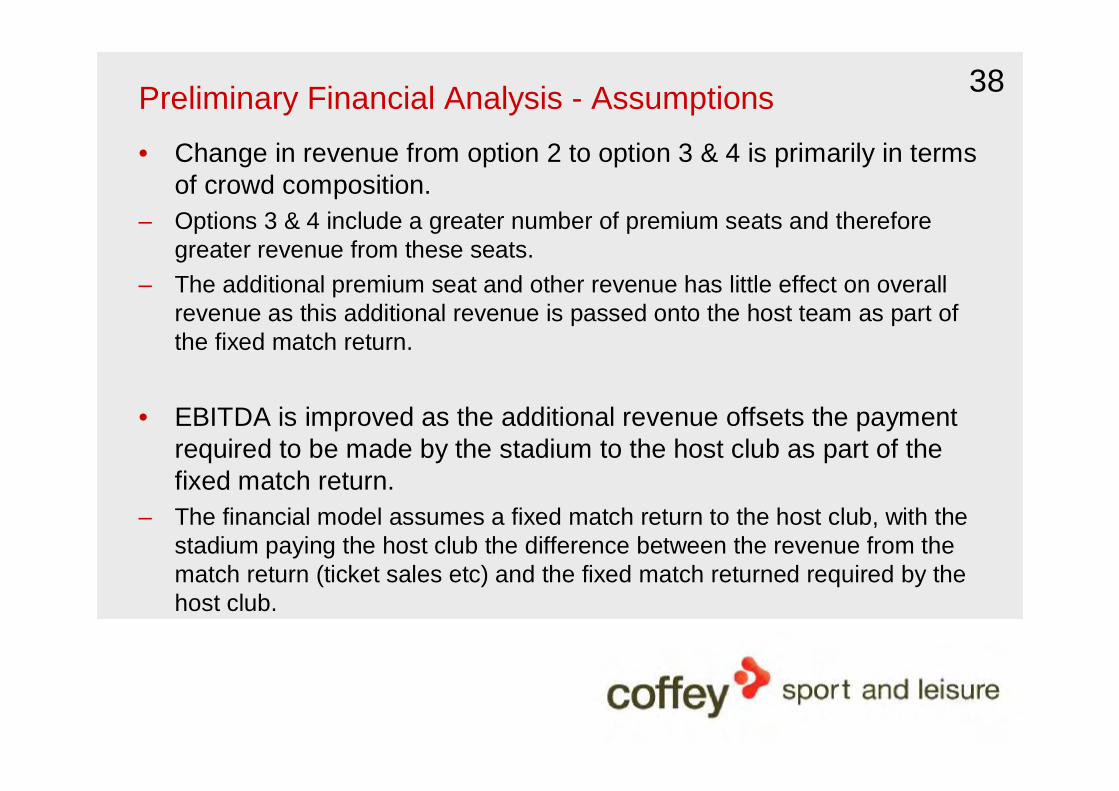

38Preliminary Financial Analysis - Assumptions• Change in revenue from option 2 to option 3 & 4 is primarily in terms

of crowd composition.– Options 3 & 4 include a greater number of premium seats and therefore

greater revenue from these seats.– The additional premium seat and other revenue has little effect on overall

revenue as this additional revenue is passed onto the host team as part of the fixed match return.

• EBITDA is improved as the additional revenue offsets the paymentrequired to be made by the stadium to the host club as part of the fixed match return.

– The financial model assumes a fixed match return to the host club, with the stadium paying the host club the difference between the revenue from the match return (ticket sales etc) and the fixed match returned required by the host club.

39Questions for Consideration• Is there a level of demand for a rectangular pitch stadium in Cairns

capable of hosting national code games and events?– Yes.• Is the demand sufficient to allow the venue to be sustainable in its

own right?– No.– Financial analysis indicates that, based on likely available content, local

demand, stadia operational costs, depreciation costs and sinking fund that no stadium development option will be financially sustainable in its own right.

– The current Barlow Park facility runs at an operational loss of $415K, or $1.237m after depreciation.

– Very few stadia across Queensland and Australia are operationally viable after depreciation and sinking fund.

40Questions for Consideration• Is there sufficient demand for a 20,000 seat stadium in Cairns that

can be sustainable in its own right?– No.– There is not sufficient demand, in terms of content, at present or likely in the

immediate future for a stadium with 20,000 seats that will enable the stadium to be sustainable in its own right.

• Is there national code content available for a stadium in Cairns?– Yes. – Approximately six games made up of practice/pre-season and home and

away matches across the NRL, A-League and Super Rugby.

41Questions for Consideration• Would the current facilities at Barlow Park allow Cairns to attract the

six games of national code content?– No.– The facilities at Barlow Park are currently insufficient in terms of:

• Seating numbers (including undercover seating);• Seating quality;• Spectator amenity;• Spectator experience (i.e. seating distance from field);• Media and TV facilities;• Lighting quality; and• Corporate facilities.

– The current facilities at Barlow Park would at a maximum allow Cairns to attract pre-season/practice games.

42Questions for Consideration• Would a new stadia in Cairns, with the right amenity and facilities,

allow Cairns to attract more national code content than what is currently achieved at Barlow Park?

– Yes.– Advice from the governing bodies is that a stadium of an adequate standard

in Cairns would allow them to allocate home and away and pre-season/practice games to Cairns on a regular basis.

– The amount of content is unlikely to be greater than 6-8 games per year across the codes.

• Will a new stadia in Cairns generate an economic impact greater than the operational costs/sinking fund costs of the stadia?

– The estimated one off value added benefit from the construction is $57.4m and a total of 576 jobs.

– The estimated ongoing annual benefit from stadium operations and induced visitations $9.6m and 132 jobs.

43Questions for Consideration• What is the optimum size of a stadia in Cairns?– A stadium capacity of no more than 20,000 is considered appropriate. – In the short to medium term a seating provision of 6,000-10,000 would be

appropriate, with 10,000 standing providing a total capacity 20,000.– In the long term seating numbers could be increased if the population base for

Cairns increases to in excess of 300,000 and/or national code tenant is based at the stadium.

– The optimum size is based on:• Likely content;• Catchment population under 300,000;• Demand in the Cairns market;• Creating a point of differentiation in the Queensland stadia market;• Allows for a master planned development of the facility up to 20,000 seats;• Reasonable capital costs;• Reasonable operating costs to allow community sports to continue to use the

stadia;

44Options For Consideration• In considering the options there was a need to determine what is an

appropriate capital cost and financial underwrite of a stadium and the planning timeline.

• Based on the projected content, capital cost, financial operations of the stadium and timelines, two options (Options 1 and 2) were considered for further analysis:– Option 1 – To cater for current demand:Will provide a reduced capital and operational financial underwrite,

however will not address all issues associated with the stadium and will impact potential content beyond current arrangements.

– Option 2 – Subject to Future Demand:Requires greater capital funding and the operational financial underwrite,

however addresses current issues with stadium and may position Cairns to attract additional events and is likely to improve attendance at events due to improved facilities.

45Strategic Considerations• In considering the options going forward Council need to consider

their Strategic position on whether they wish to:– Invest in a stadium on the basis of bringing event content and the

subsequent economic impact;– If yes what level of investment are they willing to make (in terms of the

stadium this will be in capital and operational funding).

• The answers to the above will dictate which option is to be pursued if any option at all.

46Options Going Forward• Subject to Council’s strategic position on its investment strategy

there are the two scenarios that could be considered:– Scenario A: Barlow Park.

That Council makes a decision that the investment in the stadia, both operationally and in capital, is too great in terms of the economic and social ROI and acknowledges that the investment in attracting events

to be an unacceptable risk, so determines the existing facility provision to be appropriate.

– Scenario B: Option 2 Development Option (as outlined in section 11).That Council makes the decision that the investment in the initial capital and ongoing operations is justified in principle based on the identified potential for broader economic and social benefits and seeks to investigate further how and when the outcomes of Option 2 can bedelivered.

47Next Steps

• Public exhibition.• Community feedback.• Prepare final report.