liberia: issues and options in the energy sector

TRANSCRIPT

Report No. 5279-LBR

Liberia: Issues and Optionsin the Energy Sector

December 1984

Report of the Joint UNDP/World Bank Energy Sector Assessment ProamThis document has a restricted distribution. Its contents may not be disclosedwithout authonzation from the Govemment, the UNDP or the Worid Bank.

...

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

JOINT UNDP/WORLD BANK ENERGY SECTOR ASSESSMENT PROGRAMREPORTS ALREADY ISSUED

Country Date Number

Indonesia November 1981 3543-INDMauritius December 1981 3510-MASKenya May 1982 3800-KESri Lanka May 1982 3792-CEZimbabwe June 1982 3765-ZIMHaiti June 1982 3672-HAPapua New Guinea June 1982 3882-PNGBurundi June 1982 3778-BURwanda June 1982 3779-RW.Malawi August 1982 3903-MALBangladesh October 1982 3873-BDZambia January 1983 4110-ZATurkey February 1983 3877-TUBolivia April 1983 4213-BOFiji June 1983 4462-FliSolomon islands June 1983 4404-SOLSenegal July 1983 4182-SESudan July 1983 4511-SUUganda July 1983 4453-UG

Nigeria August 1983 4440-UNINepal August 1983 4474-NEPGambia November 1983 4743-GMPeru January 1984 4677-PECosta Rica January 1984 4655-CRL esothc Tanuary 1984 4676-LSOSeychelles january 1984 4693-SE'YMorocco March 194 4157-MORPortugal Acri; i984 4824-PONiger May 1984 4642-NIRE;thiopia Ju`v 1984 4741-ETC.ape Verde Auzust 1984 5073-CVGuinea Bissau Auzaust 1984 5033-CUBBotswana Seotember 1984 4'998-BTSt. Vincen: and

the Grenadcnes September 1984 5103-STVSt. Lucia Sep1e r 984 5111-SLUParaguay Oc' h.er 1984 51'5-PATanzania Ncv e.-nber 1984 '959-TA

FOR OFFICIAL USE ONLY

REPORT NO. 5279-1BR

LIBERIA

ISSUES AND OPTIONS IN THE ENERGY SECTOR

DECEMBER 1984

This is one of a series of reports of th- Joint UNDP/World Bank EnergySector Assessment Program. Finance for thie work has been provided, inpart, by the UNDP Energy Account, and the work has been carried out bythe World Bank. This report has a restricted distribution. Its contentsmay not be disclosed without authorization from the Government, the UNDPor the World Bank.

ABSTRACT

The economy of Liberia has been in decline since 1979 and theprospects for future economic growth are uncertain. Between 1979 and1983, the modern sector GDP was estimated to have declined at a rate of5.6Z per year. The impact of the lessened demand for Liberia's exportproducts, especially iron ore, has been magnified by poor management ofthe economy and of the major state-owned enterprises. The two mainenergy parastataLs - the Liberian Electricity Corporation (LEC) and theLiberian Petroleum Refining Company (LPRC) -- are now threatened withsevere liquidity problems. Three main themes have been pursued in thisreport to address the severe issues facing the Liberian energy sector:restoring financiaL viability to LEC and LPRC; maximizing the service-ability and productivity of installed energy production, storage, andhandling capacity in the petroleum and power sectors; and optimizing theexploitation and replenishment of presently abundant woody fuelresources. An energy sector investment program of US$60 million is putforth between 1984 and 1993, and technical assistance projects are recom-mended to assist in the implementation of the investment program.

ABBREVIATIONS AND ACRONYMS

Abbreviations

bbl barrelbd bone dryGJ gigajouleGDP gross domestic productGWh gigawatt hourha hectarekg kilogramKVA kilovolt amperekW kilowattkWh kilowatt hour1 literLPG Liquified Petroleum Gasm mcwb moisture content, moisture content wet basis* cubic meterM,M thousandMM millionMVA megavolt ampereKW megawattKWh megawatt hourOD oven drysv,s solid volume, solidtonne,te metric tonnetoe tonnes of oiL equivalenttpa,tpy tonnes per annum, tonnes per year

Acronyms

AfDB African Development BankEFMC Econonic and Financial Management CommitteeLEC Liberia ELectricity CorporationLPRC Liberia Petroleum Refinery CorporaticnGOL Government of LiberiaDOE Department of EnergyMLME Ministry of Lands, Mines and EnergyFDA Forestry Development AuthorityNEC National Energy CommitteeORNL Oak Ridge National Laboratory

This report is based on the findings of an energy assessment mission whichvisited Liberia in February, 1984. The mission assignments were, K. Newcombe,Mission Leader, Power Sector Management and Household Energy; H. Ansari,Deputy Mission Leader, Petroleum Sector Co-ordination and InstitutionalArrangements; G. Alibaruho, Economist, Macroeconomic Linkages; G. Herrmann,(Cons) Power Systems Planning and Engineering; R. Chronowski, (Cons) Wood-fired Power Systems and Industrial Energy; G. Duxbury, (Cons) PetroleumEconomist; J. Russel, (Cons) Petroleum Procurement and Transportation Issues;J. Shillingford, (Cons) Refinery and Depot Engineering and Economics. KenNewcombe was the principal author of the report.

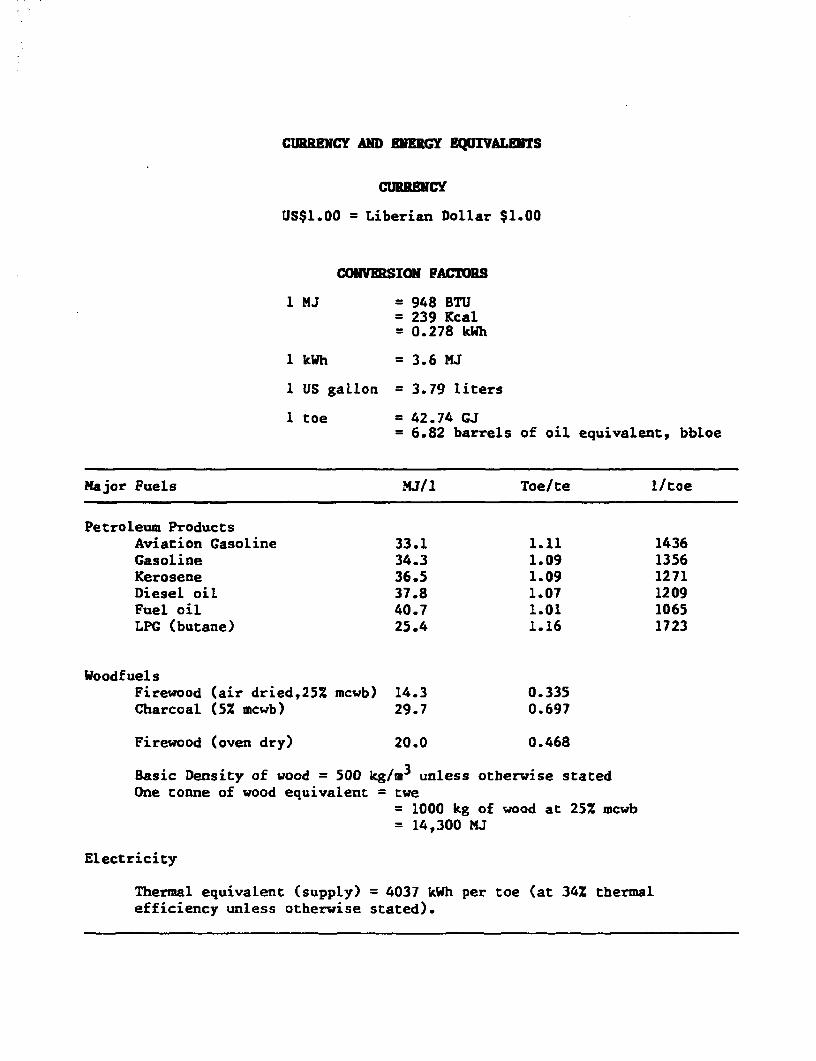

CUB ENY ND EEGY ZQUIVALENTS

cUrRC

US$1.00 = Liberian Dollar $1.00

CONVERSION FACTORS

1 MJ = 948 BTU= 239 Kcal= 0.278 kWh

1 kWh = 3.6 MJ

1 US gaLlon = 3.79 liters

1 toe = 42.74 GJ= 6.82 barrels of oil equivalent, bbloe

Major Fuels MJ/i Toe/te 1/toe

Petroleum ProductsAviation Gasoline 33.1 1.11 1436Gasoline 34.3 1.09 1356Kerosene 36.5 1.09 1271Diesel oil 37.8 1.07 1209Fuel oil 40.7 1.01 1065LPG (butane) 25.4 1.16 1723

WoodfuelsFirewood (air dried,25% mcwb) 14.3 0.335Charcoal (52 mcwb) 29.7 0.697

Firewood (oven dry) 20.0 0.468

Basic Density of wood = 500 kg/m3 unless otherwise statedOne tonne of wood equivalent = twe

= 1000 kg of wood at 25Z mcwb= 14,300 MJ

Electricity

Thermal equivalent (supply) = 4037 kWh per toe (at 34X thermalefficiency unless otherwise stated).

TABLE OF CONrENTSPage

SUMMARY AND RECOMMENDATIONS ................... ......... .... i

I. ENERGY AND THE ECONOMY OF LIBERIA .......................... 1Country Background ............ ....... .........-. 1Trends in Economic Performance ........................... 1Energy and the Economy........ ........................... 2Indices of Change in the Energy Economy ................ 3

The Present Pattern of Energy Consumption** ............. 3Recent Trends in Power and Petroleum Consumption ....... 6

Future Energy Demand ................................... . 8Changing Fuel Mix.......... ........................... 10

Energy Pricing .................... .............................. 11

II. PETROLEUM ..................................... ............. 14Background ......... .. ........... ............ 14Petroleum Resources ...................................... 14Petroleum Product Demand ........................................ . 14Supply of Petroleum ......................... ......... 16Port Facilities ............. ................................. 17

Procurement Arrangements ...... ................... 18Product Purchasing Performance......................... 19Other Components of the Landed Price ................... 20Final Cost of Petroleum Supply at the Depot*& ........a 21Short Term Measures. ........... ....... ....... 23

Financing of Petroleum Imports ........................... 23Distribution Costs.....6-0-060 ........ ....... 24

Private Sector RoLe in Product Supply . . 25Options for Private Sector Involvement ......ol em....en.t. 26

Product Storage Capacity ................................. 26Parcel Size Limitations ................................ 28

Prospects for Oil Refining in Li b e r i a ................. 28Institutional Issues and Options . . 29Petroleum Investment and TechnicalAssistance Requirements..................... 30

III. ELECTRICITY ................. e-sov.......... e.e........ 31Introduction .......................................... 31Institutional Arrangements ............................... 31The Power System .... 00 ........... . 32

Short Term Problems .... .. ............................ 36Current Financial Status ............................... 36Liquidity ................. 0......................... 36Non-Technical Losses ................................... 37

Reducing Non-Technical Losses...... ....... .... 37Privatization ...................................... 39

Reducing Technical L o s s e s ................. 39rmplementation ...................................... 40Efficient Use of ELectricity ........................... 41

Page

Electricity Demand Projections............................ 42Financial Projections....... ...... 43

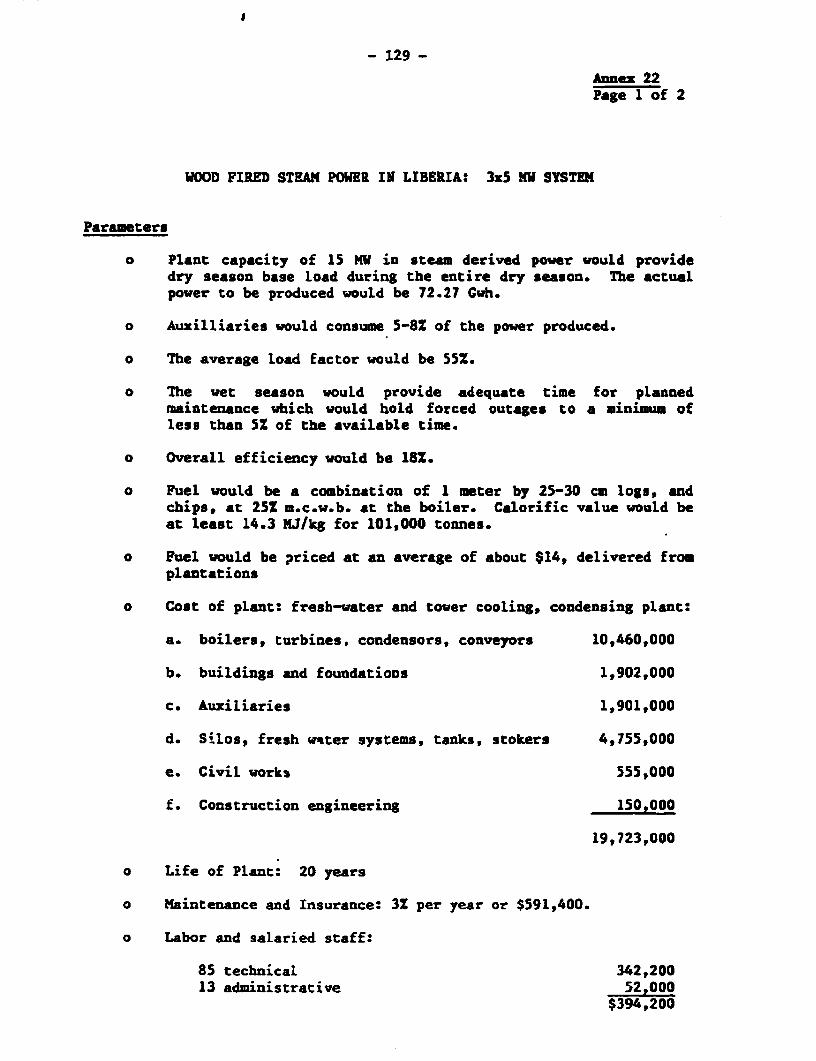

Generation Needs and Options............................. 43Immediate Supply .......................... ............ 44Long Term Supply Agreement with BMC.................... 45Fuel Oil Fired Dieselse....................... 46Wood-fired Steam Power Generation..................... 46Coal as a Power Source ................... 47Hydropower ............................................ 48Upgrading the Mt. Coffee Hydropower Station............ 49Conclusions and Recommendations onGeneration Expansion ................................ 50

Generation and Transmission Planning Studies........... 51HydroLogy ............................................... S1Transmission Expansion...6.06606606-see ............... . 52

Isolated Supply Systems........................ .......... 52Alternative Energy Supply for IsolatedPower Generation ..................................... 55

Electricity Pricinge.e.e........................... 56Short Run Marginal Cost of Hydropower ........ 0........ 56Long Run Marginal Costs................................ 56Tarif fs. . . . . . . . . . . . . . 0. 0. . . . . . . .4. 000. a6. . ... . . 56M-anagement Isus.......................58

Subsector Investment and TechnicalAssistance Requirements................. e............. 59

IV. HOUSEHOLD AND INDUSTRIAL ENERGY ............................* 62Introduction................................................ 62Household Energy....................................... 62The Pattern of Household Energy Use .................... 62Comparative Economy of HousehoLd Fuels ................. 63

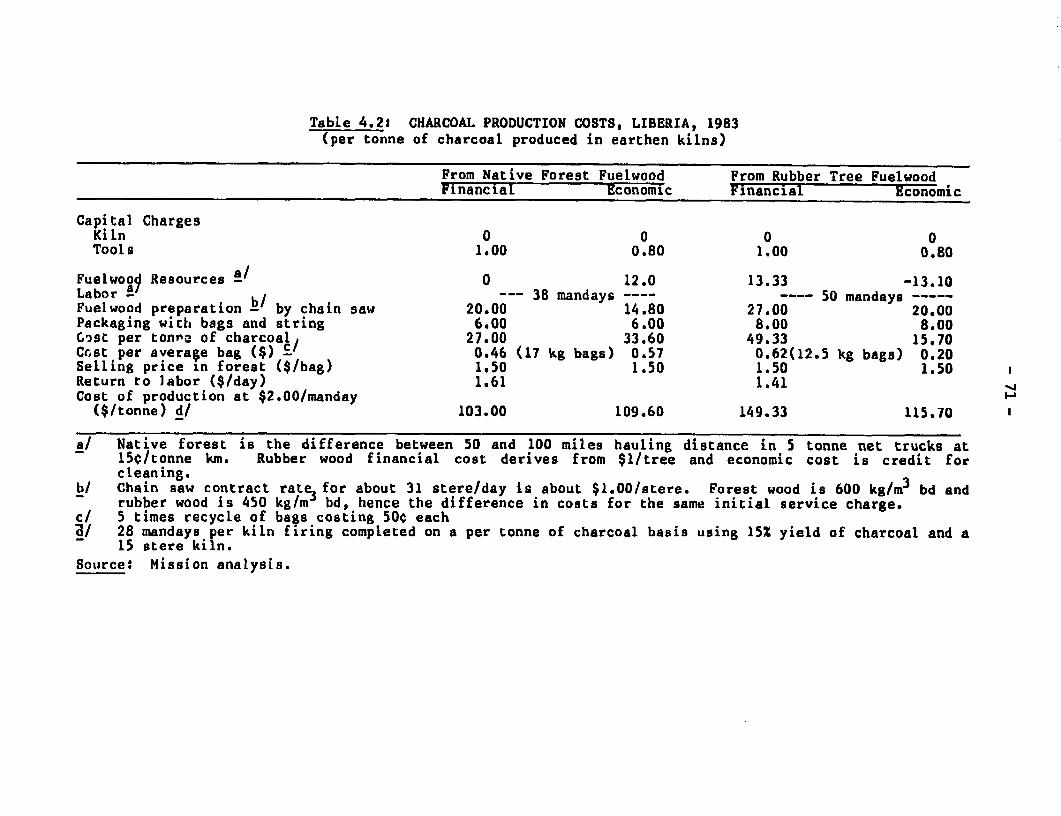

Woodfuel Supply and Demand............................... 66Present Woodfuel Resources ............................. 66National Woodfuel Demandt.. .. . . . . . . e.. .. ... .. e.e..... . 67Supply and Demand of Woodfuels to Monroviao.s............ 67Rubber as an Energy Crop............... ............. ... 68The Economics of Rubbertree Wood Charcoal Production... 70Policy Implications and Recommendations ................ 72Other Woodfuel Resource Management Optionse............. 72

The Charcoal Industry...& .............. o ........ .... 74Improved Charcoaling Efficiency ........................ 74The Prospect for Exporting Charcoal.................. O.. 75Modifying Demand for Household Cooking Fuels....e..... 78Kerosene and LPG Supplies................. .............. 80

Solar Water Heating.... ... * . ........ & 80Industry ........es........ 0.00........ ........................ 81Energy Efficiency in Manufacturing ..................... 81Interfuel Substitution in the Manufacturing Sector..... 82Risks and Logistics ........ ......... .... ... 84

Page

V. INVESTMENT, INSTITUTIONAL ARRANGEMENTS AND MPOW...ER........ 85Energy Sector Investment... .6..... .0.....e.g...... .... 85Revised Energy Sector Investment Program .............. 86Investment Priorities....... .............. 87Source of Funds ...... ............................0 89

Energy Planning, Institutions and Manpower Needs ......... 89Institutional Arrangements ...... .... ....060000000 89Energy Planning ...................... 90Role of an Energy Policy and Planning Division 0. o...... 91Prerequisites for Effectiveness ........... 000......... 92Policies and ............................ ..... 92Manpower Needs ......................................... * 92Technical Assistance.........e.............e............ 93

ANNEXES

1. Energy Balance, 1983 ................... 952. Energy Balance, 1993.... ... . .. .g..... ... **** 963. Border Price Build-up for Liberia, First Quarter 1984 .... 974. Ex-Depot Price Build-up. ....... . 985. 1983 Purchase/Sales Pattern............................. 996. Estimated Oil Product Consumption, 1983................ 1007. Product Prices Paid by LPRC Compared to International

Spot Market Levels, 1983 ........... ............. 1028 Main LPRC Tankage ................ ........ 1049. Economics of Refining in Liberia, 1988 and 1993 .......... 10510. Refining Options ................ l................. 11111. LPRC Staff Distribution and Numbers...................... 11412. Schedule of Installed and Available Generating Plant..... 11513. Statistics on the Nature and Performance of

Government Isolated Power Systems, 1982/83............. 11614. Historical Trends in Sales and Generation................ 11715. LEC Actual & Projected Income & Expenditure

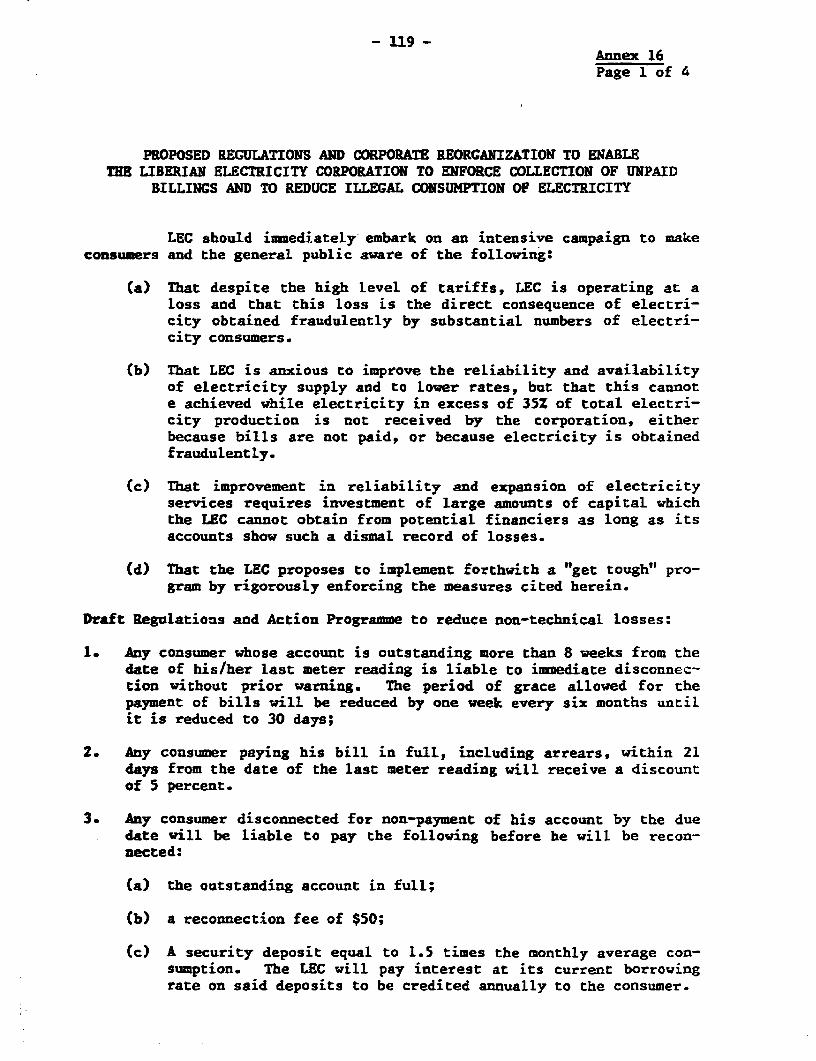

Statements ............................. .00..................... 11816. Proposed Regulations and Corporate Reorganization

of LEC .... .6 *** 0*........... 11917. Assumptions for Energy and Power Sector Demand

Forecast ..... ...... ......* 12318. LEC Historical and Projected Sales ...... 12519. LEC Historical and Projected Generation

Mix and Fuel Consumptione. .. .........e.e.o... 12620. Parallel Operation of BMC and LEC Systems .. 0 ............. 12721. Cost of Production from Modern Slow Speed Diesels........ 12822. Wood Fired Steam Power ............ ...... ... ....... *0 12923. Operations Cost of Coal Fired Steam Generating Plant..... 13124. Generation Equipment for Government

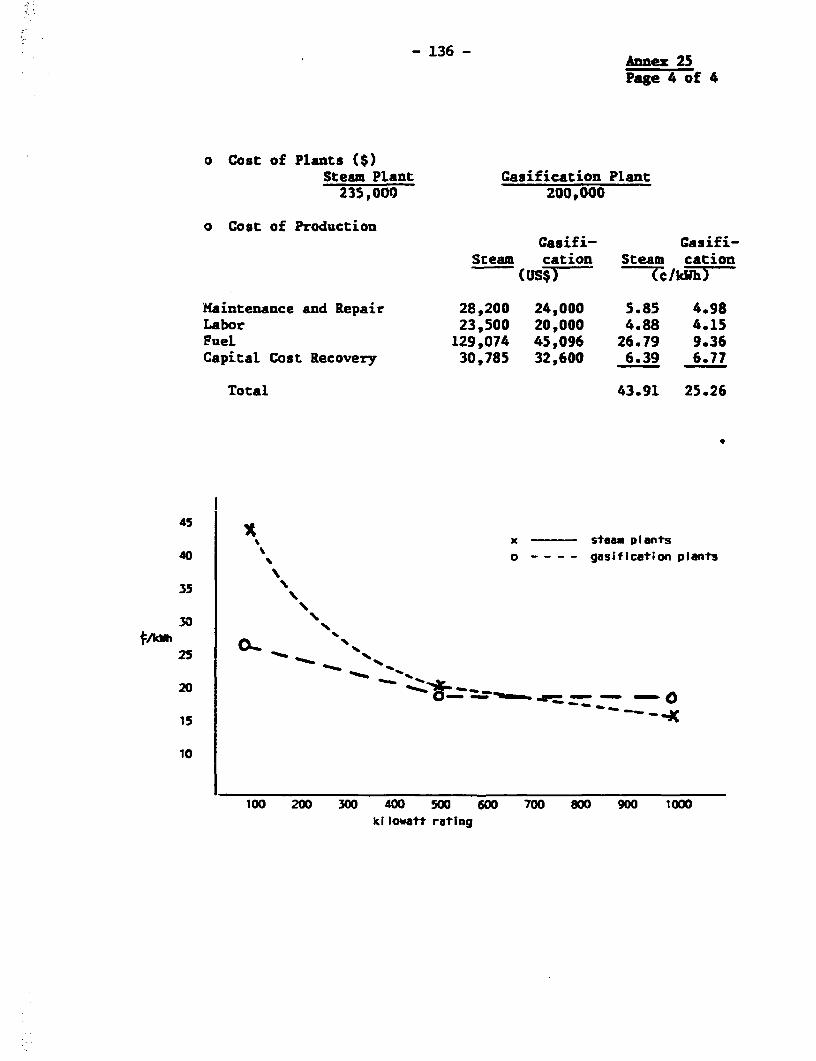

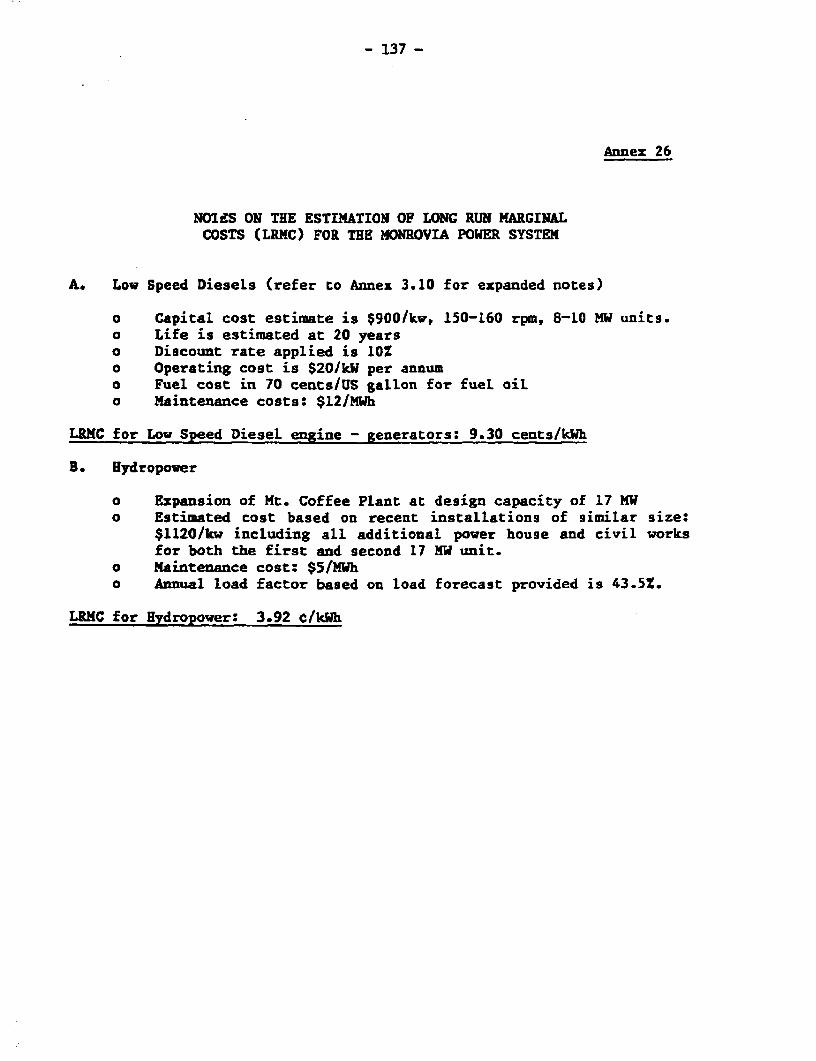

Isolated Power Systems, 1983 .......................... 13225. Wood Steam vs. Wood Gasification Power Pl ant ........... 13326. Estimation of Long Run Marginal Costs For Monrovia ....... 13727. Firewood Prices, 1984 . ............. o ..................... 13828. Charcoal Prices, 1984 .................................... 139

Page

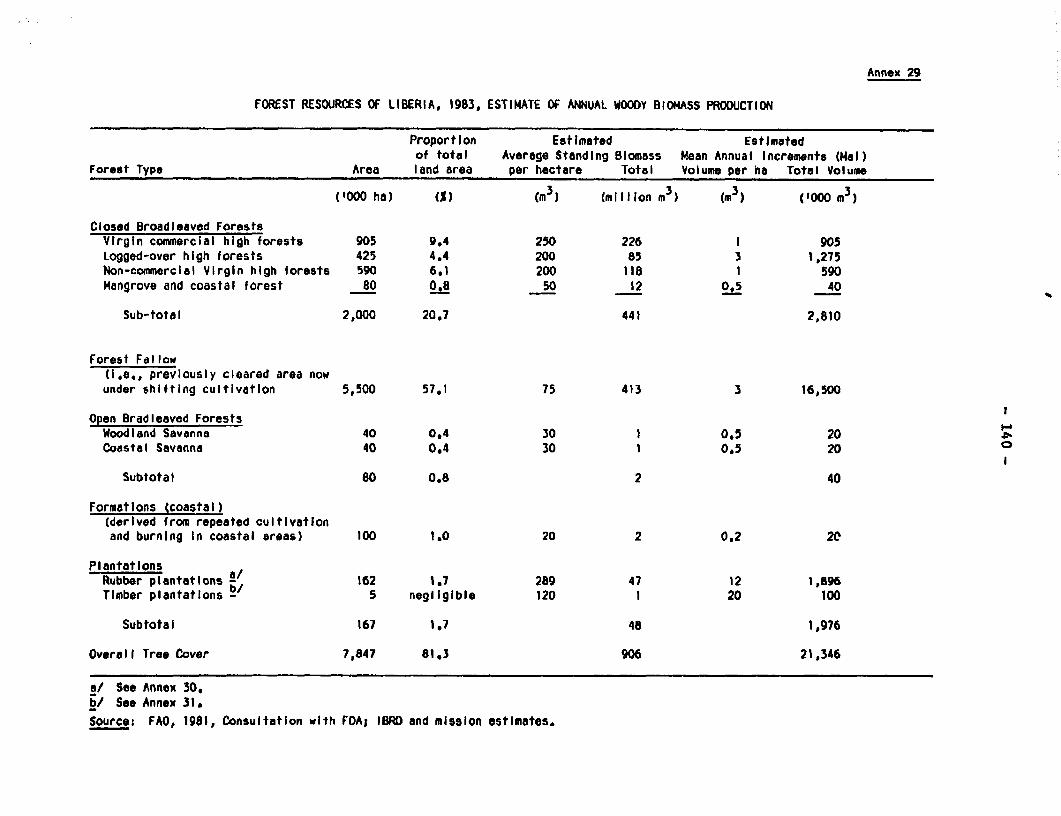

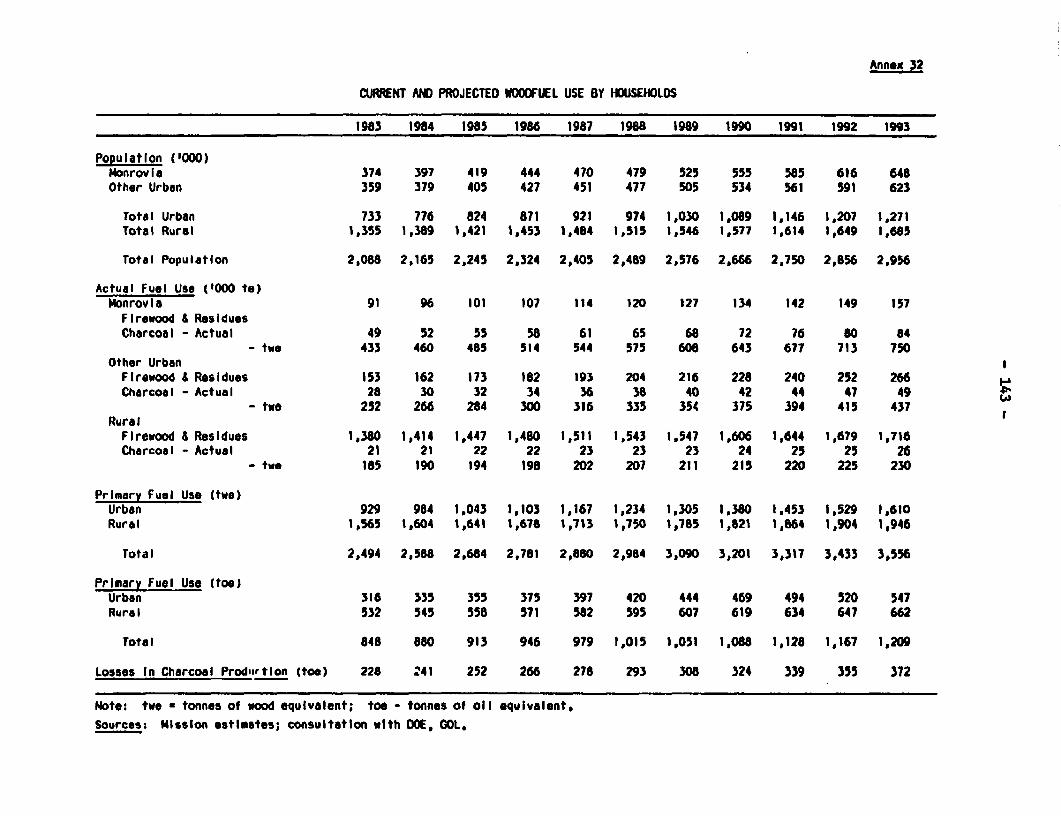

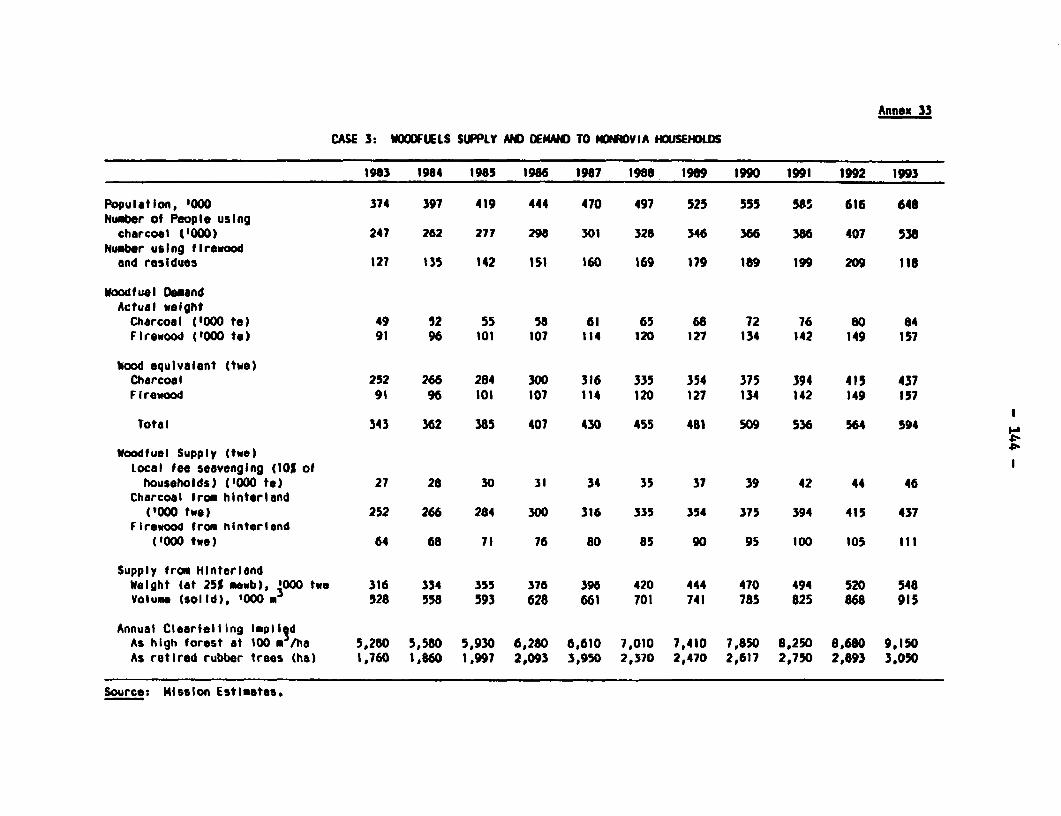

29. Forest Resources, 1983 ........... . 14030. Estimated Rubber Tree Stand, 1983 ........................ 14131. Plantation Timber Resources, 1983........................ 14232. Current and Projected Woodfuel Use by Households ......... 14333. Woodfuels Supply and Demand to Monrovia Households ....... 14434. Price Build-up for Charcoal in Liberia, 1984 ............. 14535. Energy Sector Investment Program, 1984-93...........0..... 146

TABLES1. Final Energy Consumption1.1 Trends in GDP and Modern Energy Consumption1.2 Petroleum Imports, Re-exportes, and Total Merchandise Trade, 1976-821.3 Final Energy Consumption, 19831.4 Energy Intensities of Selected Regional Countries, 1981-821.5 Recent Consumption Trends for Petroleum and Power1.6 Final Consumption of Petroleum Products by Sector, 19821.7 Significant Future Trends in Energy Supply and Consumption1.8 Petroleum Prices and Costs, Monrovia, Liberia, First Quarter, 19842.1 Development of Petroleum Products Consumpti3n, 1979-832.2 Mining Sector Fuel Requirements2.3 Countrywide Petroleum Demand Forecast2.4 Premia Paid by LPRC on 1983 Imports2.5 LPRC's Other Purchasing Costs2.6 Simplified Comparison of Costs of Petroleum Products Import2.7 LPRC Refined Petroleum Product Storage Capacity, 19842.8 Petroleum Sector Investment Program3.1 Installed Capacity of Electrical Generating Plant in Liberia, 19833.2 Estimated Power Generation in Lib-ria, 19833.3 Generation and Sales for the Monrovia Power System, 1979-833.4 Generation and Sales Projection for the Monrovia Power System3.5 Short Run Marginal Costs of Thermal Generation, 19843.6 Hydropower Resources of Liberia3.7 Characteristics of IsoLated Generating Systems, Liberia, 1982-833.8 Load Projection for Isolated Generating Stations, Liberia, 1984-933.9 Long Run Marginal Cost Estimates, Monrovia Power System3.10 Power Sector Investment Program, 1984-934.0 HousehoLd Energy Consumption, 19834.1 Comparative Cost of Household Energy Forms in Monrovia,

First Quarter, 19844.2 CharcoaL Production Costs, 19834.3 CharcoaL Production Costs Using Improved Metal Kilns4.4 Possible Charcoal Export Price Structure4.5 Cost of Cooking in Liberia with Present and Improved Stoves5.1 Overview of Energy Investment in the Public Sector, 1976-875.2 Average Annual Component of Public Investment Program

by Sector, 1981-875.3 Major New Investments by Priority Class5.4 Energy Sector Investment Program: 1984-93

MAPSIBRD 12867R: Country MapIBRD 18368: Offshore PetroLeum ExplorationIBRD 18383: Generation and Transmission Network

MAIN FINDINGS AND COECLUSIG0S

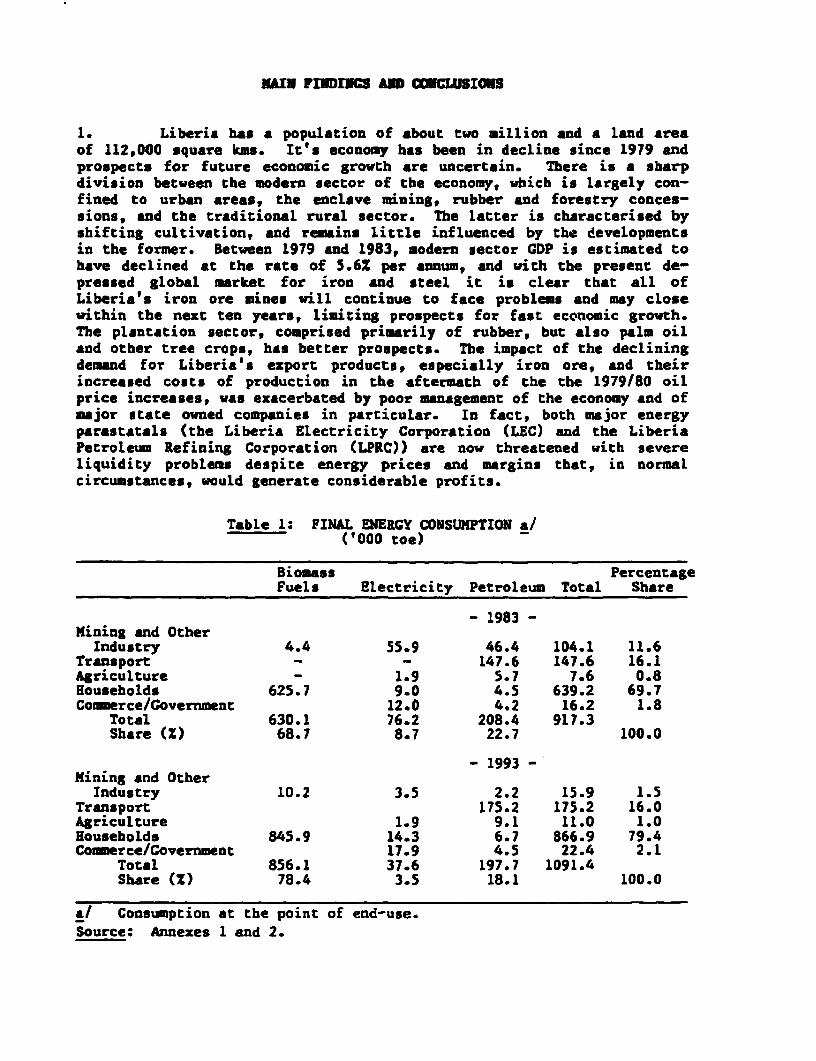

1. Liberia has a population of about two million and a land areaof 112,000 square kms. It's economy has been in decline since 1979 andprospects for future economic growth are uncertain. There is a sharpdivision between the modern sector of the economy, which is largely con-fined to urban areas, the enclave mining, rubber and forestry conces-sions, and the traditional rural sector. The latter is characterised byshifting cultivation, and remains little influenced by the developmentsin the former. Between 1979 and 1983, modern sector CDP is estimated tohave declined at the rate of 5.62 per annum, and with the present de-pressed global market for iron and steel it is clear that all ofLiberia's iron ore mines will continue to face problems and may closewithin the nezt ten years, limiting prospects for fast economic growth.The plantation sector, comprised primarily of rubber, but also palm oiland other tree crops, has better prospects. The impact of the decliningdemand for Liberia's export products, especially iron ore, and theirincreased costs of production in the aftermath of the the 1979/80 oilprice increases, was exacerbated by poor management of the economy and ofmajor state owned companies in particular. In fact, both major energyparastatals (the Liberia Electricity Corporation (LEC) and the LiberiaPetroleum Refining Corporation (LPRC)) are now threatened with severeliquidity problems despite energy prices and margins that, in normalcircumstances, would generate considerable profits.

Table 1: FINAL ENERGY CONSUMPTION a/('000 toe)

Biomass PercentageFuels Electricity Petroleum Total Share

- 1983 -Mining and OtherIndustry 4.4 55.9 46.4 104.1 11.6

Transport - - 147.6 147.6 16.1Agriculture - 1.9 5.7 7.6 0.8Bouseholds 625.7 9.0 4.5 639.2 69.7Coouerce/Government 12.0 4.2 16.2 1.8

Total 630.1 76.2 208.4 917.3Share (Z) 68.7 8.7 22.7 100.0

- 1993 -Mining and OtherIndustry 10.2 3.5 2.2 15.9 1.5

Transport 175.2 175.2 16.0Agriculture 1.9 9.1 11.0 1.0Households 845.9 14.3 6.7 866.9 79.4Coerce/Government 17.9 4.5 22.4 2.1

Total 856.1 37.6 197.7 1091.4Share (X) 78.4 3.5 18.1 100.0

a/ Consumption at the point of end-use.Source: Annexes 1 and 2.

- ii -

The pattern of final energy consumption is summarized in Table 1.1. From1980 to 1984, Liberia's consumption of petroleum and electricity declinedin line with economic activity and is projected to decline further, bothin absolute terms, and relative to the consumption of traditional biomassfuels, particularly during the early 1990s as the Bong mine closes. Con-versely, over the same period the share of firewood and charcoal is pro-jected to increase from about 70% to 80%. While Libe-ia's present percapita energy consumption of 438 kgoe per year is well above that of itsneighbours, the likelihood is that this distinction will be shortlived.In effect, the Liberian energy economy is in a transition just the oppo-site of most developing economies where the share of modern fuels of thetotal energy mix increases as urbanization and industrialization pro-ceeds. In Liberia, the overall growth in energy supply over the 1984-1993 period is expected to be 3.6% p.a., or marginally higher than popu-lation growth, and its source will be almost exclusively woodfuels. Thedeclining demand for modern fuels has far-reaching implications for powerand petroleum subsector management and planning, and the growing demandfor woodfuels raises important questions regarding the optimal exploita-tion of the country's forests.

Overall Energy Strategy

2. Three main themes of a comprehensive energy strategy emergefrom this energy assessment:

(a) Restore financial viability to the main public sector energysupply and production agencies - the Liberian Electricity Cor-poration (LEC) and the Liberian Petroleum Refining Corporation(LPRC). So long as these parastatals are unable to generatesufficient surpluses for adequate maintenance and for capitalinvestment there is little prospect of reliable and reasonablypriced energy supply. The achievement of this objective willrequire upgraded management and strict enforcement of paymentof energy accounts supported by new legislation, regulationsand consumer billing practices and a determined political willto succeed.

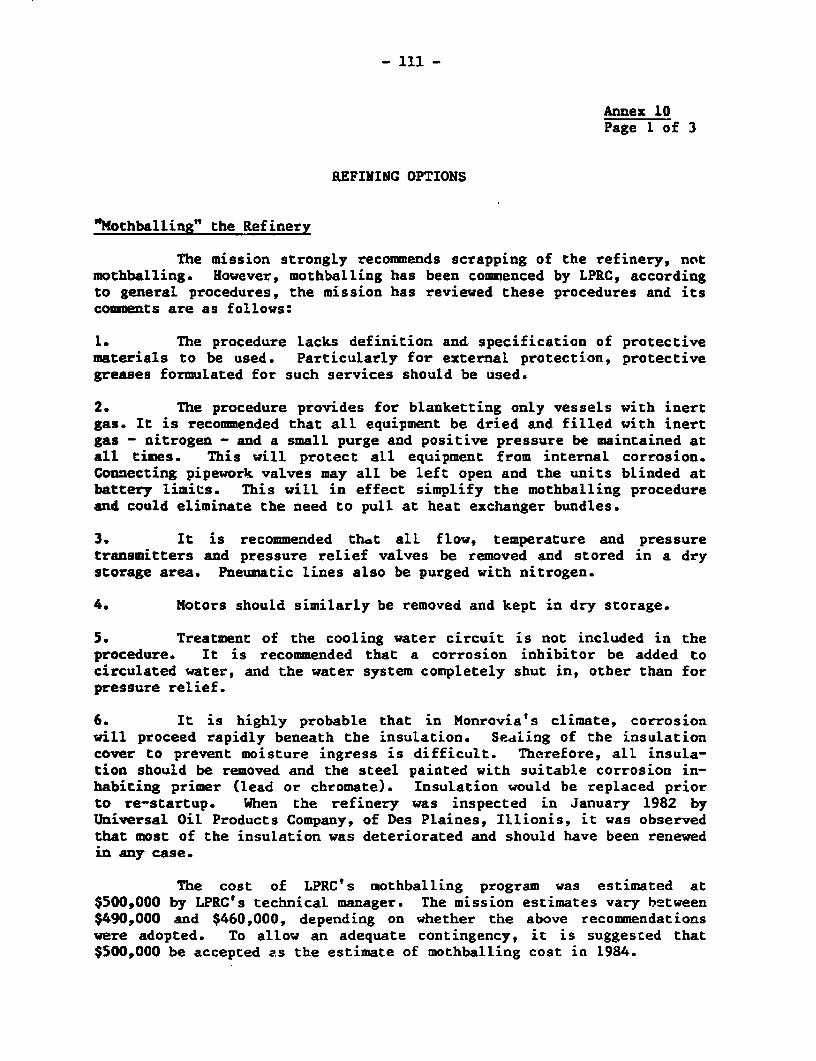

(b) Maximize the serviceability and productivity of installedenergy production, storage and handling capacity in the petro-leum and power sectors. While there is either declining oralmost stagnant markets for modern energy forms, maximum bene-fit will be derived from the rehabilitation of existing faci-lities in each subsector, with the exception of the refinerywhich should be dismantled forthwith. Crash programs to re-meter consumers, redesign and refurbish electrical distributionand to rehabilitate economically serviceable ceieration plantare required. Similarly, maximum use is to be made of under-utilized generating plant within the enclave mining sector inpreference to purchase of new generating equipment. In the

- iii -

petroleum subsector, storage facilities should be revamped andport handling equipment upgraded to facilitate efficientoperation of a petroleum depot relocated at the Water Frontarea instead of at the old refinery site.

(c) Optimize the exploitation of presently abundant woody fuelresources in order to reduce the destruction of accessible highforest and to increase the benefit to the economy of the con-sumption of woodfueLs by using wood from retired rubber treeplantations. Resource inventories, systematic incentives forprivate sector exploitation of the least cost forest resourcesand the demonstration of modern efficient production and end-use equipment will be required.

Key Issues and Options

Petroleum Subsector

3. Until 1982, petroleum products were produced at the Govern-ment's refinery in Monrovia under the management of its wholly-ownedLiberian Petroleum Refining Corporation (LPRC). The refinery was closedat the beginning of 1983 due to the LPRC's inability to meet a majorpayment for crude oil. Subsequently the GOL decided not to re-open therefinery because further evaluation indicated that it was cheaper toimport petroleum products than to refine them locally. However, LPRCstaff had little experience in product procurement and frequently boughttoo late and paid above market rates. In addition, not only were mostrefinery cost centers kept active but new equipment was purchased andinstalled after the Government's decision that the refinery was not to bere-opened. Unauthorized extraction of petroleum products added furtherto the costs of petroleum supply. The LPRC management is also burdenedby serious litigation following the collapse of crude oil supply arrange-ments, and by confused debtor-creditor obligations and, as a resutlt, isunable to devote sufficient attention to day-to-day problems of opera-tional inefficiency. The net result of these problems in 1983 was anadditional and avoidable cost burden of at least US$13 million, or aboutUS$77 per tonne of product imported by the LPRC. The key issues in thesector are, then, how best to improve the efficiency of petroleum pro-curement and supply to the wholesale market, and whether to completelydismantle or to mothball the refinery. Of even more immediate concern isthe need to secure for the LPRC sufficient liquidity to procure productwhen required and in the desired quantities. By February 1984 the com-pany's effective reserves had fallen so low that it had to reduce cargosizes to make ends meet against rising costs. LPRC's solvency isthreatened both by the ongoing inability of the Liberian ElectricityCorporation to fully pay for products suppLied, and by its own ineffi-ciency. The most important of the measures nroposed by the mission toresolve these problems are as follows:

iv -

(a) dissolve the LPRC and form a Liberian Petroleum Supply Companywith the sole objective of importing and wholesaling petroleumproducts. As part of this re-arrangement all present refinerycost centers should be closed, staff retrenched, salable assetsreaLised, and a clear determination made of the current finan-ciaL and legal obligations of the LPRC.

(b) procure the services of an experienced oil industry company tomanage under contract the new supply company, to train Liberianstaff to operate the company within three years, and to expe-dite the liquidation of LPRC assets and the re-employment ofstaff qualified and suitable to serve the new company. Staffemployed in petroleum supply should be reduced from 480 to amaximum of 85 in the process.

(c) dismantle the refinery to the extent of its saLable components,rent or sell office facilities, and move the site of the petro-leum depot to the Water Front area in the port of Monrovia.

(d) Upgrade the storage at the Water Front area as well as off-loading and other handling facilities to promote efficient andcost-effective operations in the new location. This willrequire an investment of about US$7.5 million which must beprepared by an immediate engineering design and costing study.

Power Subsector

4. Power supply to the Monrovia power system (MPS) fell at almost22 per annum between 1980 and 1984. Throughout this period losses havebeen about 35% of generation (20% unbilled consumption and 15X technicallosses). Since only about 70X of electricity officially sold is paidfor, this means that payment is received for less than half of the elec-tricity generated. Tariffs are at least 50X higher than the presentcosts of production and the long run marginal costs of supply. Untilrecently the LEC was able to remain solvent because of the large differ-ence between the cost of supply and tariffs, which were raised as re-quired. Now the LEC is faced with stricter te-ms of credit, higher costsof production due to the growing use of gas turbines, and a furthertariff increase is unlikely to be acceptable to the Government. Duringthe 1984 dry season a major fuel oil fired engine generator set failedand, as with the previous dry season, supply was at best intermittent.LEC chose to meet supply with gas turbines which have direct costs ofproduction well above the tariff level, instead of negotiating additionalsupply from the Bong Mine (see para 3.3) of low cost fuel oil firedgeneration, or rehabilitating its lower cost diesel generators. Demandis forecast to grow at about 0.2% per annum over the next decade andsubsequently the need for major new generating capacity is limited tosecuring supply at the present level, although an excellent opportunityexists for the suppLy of additional hydropower to the Bong Mine in returnfor thermal generation in the dry season and for sale on commercialterms. The most pressing problems are the theft of power and the failure

-v-

to enforce payment for all electricity consumption billed. Indeed if LECis unable to pay the LPRC for petroleum fuels because it cannot enforcepayment from its own consumers it may eventually be responsible both forits own and the LPRC's insolvency. On system planning and development,the mission believes that a combination of generation and distributionrehabilitation, additional low speed diesels fired with fuel oil, andwood-fired steam power using Bomi Hills forest resources are part of aleast cost solution. However, the precise conf_guration and timing ofthe Least cost options for power suppLy must be determined by the recom-mended planning studies. There is no economic justification for LargescaLe hydropower development on the St. Paul and Mano rivers for at leasta decade, and even implementing the projects recommended by the missionwill pose serious fiscal constraints. In this context, major transmis-sion construction now appears to have a lower priority in the face ofurgent short to medium term generation and distribution rehabilitationrequirements. In the mission's view, it would be useful to review withthe AfDB the project recently negotiated with a view to possibly resche-duling it and emphasizing the valuable metering component it contains.Similarly, in the isolated supply systems funded directLy by the GOL andmanaged by the LEC, costs exceed revenue by almost US$6 million per yearcompared with a budgeted subsidy of US$750,000, and plans are afoot toexpand supply of both diesel, wood and hydropower to these systems.Under present circumstances this can only greatly increase the annualloss. The key issues center first on the means by which unpaid consump-tion can be cut, bills can be paid and the financial viability of theinstitution restored and, secondly, on the least cost means of supplyover the remainder of the decade. In order for any program of reform tobe successful, however, existing management practices will have to bechanged and administration improved markedly, including better staff dis-cipLine and wholly revised accounting, planning, decision making andoperational procedures.

5. Urgent measures include:

(a) introduction of regulations and procedures designed to ensurepayment for electricity supplied and sharp curtailment of un-paid consumption. These regulations would have to be supportedby new legislation to enable the LEC to quickLy apply strongpenalties for non-compliance. Essential to the success of anysuch approach however, is the full and public support ofgovernment.

(b) rehabilitation and redesign of distribution facilities andmetering all consumers not served by an operational meter, andpossibly the introduction of tamper-proof load limiters forconsumers with very low level power consumption. These stepsare to be undertaken in parallel with the enforcement of newreguLations, and revision of consumer billing and accountingprocedures. A comprehensive power system efficiency audit isrequired to identify the highest priority measures and toprepare for a larger program of generation and distributionrehabilitation.

- vi. -

(c) management of the LEC for a period of three years under an ex-ternal management contract on a "fee plus" performance relatedbasis. The contractor concerned would be specifically chargedwith implementing the reforms outlined herein, training staffto replace them in their management role in the near term, andreducing costs, including those for staff. The contractorwould also assume respbnsibility for revising consumer billingand accounting procedures, and implementing metering and con-sumer level distribution rehabilitation programs.

(d) negotiation of an extended contract with the Bong Mining Com-pany for the supply of thermal power during the 1985 dry seasonto reduce reliance on high cost LEC thermal generation.

On the cost and source of power supply to rural towns:

(e) The average variable cost of production is 27C/kWh and thereceipts average 4centslkWh, which led to a loss of US$5.3million in the last financial year. This loss will growrapidly to US$8 million per year if planned diesel installa-tions proceed. Consequently, no additional capacity of anykind should be installed until the tariff is set at 15e/kWh inthe first instance, and metering and billing arrangements aresuch that all consumers pay for supply at this level. In thelonger term tariffs need to be raised to at least cover vari-able costs. If demand persists under these revised tariffs, awood-fired steam plant appears justified in some supply centresand the interconnection of Gbarnga with the Monrovia PowerSystem should be evaluated.

Household Energy

Woodfuel Resources

6. Liberia has forest cover of some kind over more than 80% of itslandscape and in gross terms the annual production of fuel quality bio-mass substantially exceeds demand. However, woodfuel demand is localisedand concentrated particularly in Monrovia, the largest urban center,which is now growing at 5-6% per year. In Monrovia, charcoal now domi-nates the household energy market and hence, with the low efficiency ofconversion from wood to charcoal, the demand for fuelwood in the hinter-land has grown rapidly in the past decade at the expense of nearbyforests. By 1993, the demand for fuelwood is expected to be one-thirdhigher than at present, suggesting that the pace of deforestation willquicken and that the price of woodfuels may rise in real terms as fire-wood and charcoal is transported from further and further afield. Thus,in contrast to the superficial impression that woodfuels are abundant,localized shortages may appear and it is now important to take stock ofexisting and accessible forest resources and to devise a strategy for

- vii -

least cost supply to the household and commercial/industrial woodfuelmarket in the longer term. Perhaps the most important and economicallyattractive source of woodfuels for Monrovia and other urban areas isrubber plantations. Although rubber wood already supplies a portion ofthe Monrovia market for charcoal and firewood, the sustainable yield ofrubber wood from retired rubber trees exceeds the annual demand for wood-fuels into the 1990's and the cash received by smallholders from sellingtheir senile rubber trees can contribute substantially to replanting.

Charcoal Production

7. Firewood and charcoal production and supply is generally man-aged by a large number of smalLholders and entrepreneurs and, despite theconstraints of traditional technology and poor transport infrastructure,the market is supplied adequately and efficiently. The role of govern-ment in woodfuels supply shouLd therefore be in support of the privatesector by providing incentives to use the most economic woodfuel re-sources and to upgrade the efficiency of conversion from wood to char-coal. For example, the carbonisation of retired rubber trees should bepromoted as an integral part of the rehabilitation of the smallholderrubber industry. Similarly, more efficient metal kilns and charcoalstoves offer some prospect of reducing pressure on the remaining closedcanopy native forests within reach of the major urban areas. Finally,with the economic prospects for pulpwood production fading, a case can bemade for evaluating the managed exploitation of the designated Stateforest areas for the production of charcoal for export to countries inthe West African region such as Mauritania, now suffering from defores-tation and desertification.

8. Specific measures arising from the above include:

(a) a resource inventory of smallholder and concession plantationsidentifying the location and quantity of rubber tree woodavailable now and each year over the next decade at least.

(b) expansion of the demonstration project for low cost metal kilnsand the establishment of a credit facility for their supply tosmallholders prepared to exploit retired rubber trees, residuesfrom organised forest clearing and other wastes for charcoalproduction.

(c) mounting a trial shipment of charcoal to Senegal or Mauritaniaas part of a feasibility study to identify logistical problemsand the costs and benefits of the prospective trade.

(d) production and demonstration of improved charcoal stoves fromelsewhere in Africa (for example, Kenya).

9. Other household energy options which appear attractive includethe use of solar water heating and the introduction of a range of moreefficient kerosene stoves. Although both technological improvements

- viii -

offer considerable financial benefits to the indir' lual consumer eventheir widespread adoption would only generate small economic benefit tothe economy in comparison with other options identified here for reformin energy production and supply. Hence, for the time being, Governmentassistance should be limited to modest promotion.

Industrial Energy

10. The manufacturing sector in Liberia is small and unlikely toexpand significantly in the foreseeable future. Individual factoriesappear to have adjusted their energy consumption well to high prices anduncertain supplies. There are no outstanding cases for substitution ofoil by fuelwood as residual fuel oil is already widely used for heat andsteam raising. The enclave sector managers have also implemented manyimportant fuel economy measures in recent years. The two biggest rubberproducers have installed wood-fired boilers and the Bong Mine has fine-tuned process heat and thermal power production. There is, however, anexceLlent economic prospect of substituting fuel oil with fueLwood iniron ore drying at the Bong Mine. The Bong Mine initiated this proposalin 1983 but was unable to attract acceptable tenders for fuelwood supply.The mission was able to define the costs and logistics of fuelwood supplyto the mine and found that annual fuel oil import costs can be reduced byabout US$1.3 million and the BMC can save US$1 million per year usingalready existing but unutilized plantation timber resources. The keyconstraint to the implementation of this fuel substitution option is thatthe Bong Mining Company, faced with the present depressed market for itsore, is unwilling to offer a purchase contract of longer than one year ata time. Avenues should be investigated by which this investment barriermay be overcome including:

(a) a precise definition of the investment required by an entre-preneur supplying fuelwood and by Bong Mining Company, and

(b) the provision by the GOL of risk capital of the order ofUS$500,000 providing a one-year sales contract can be securedwith Bong Mine by the local fuelvood supplier concerned.

Energy Pricing

11. Energy prices in Liberia are characterised by being, cn thewhole, cons,derably higher than the economic costs of production orsupply. For electricity supplied to the MPS, if consumer billing andutility management reforms proposed by the mission are implemented, itshould be possible to reduce tariffs in real terms in the 1986 wetseason. Petroleum products are retailed at 2-3.5 times their borderprices, hence the main pricing consideration is the extent to which gaso-line and diesel taxes are used to generate government revenue. Govern-ment and concession prices for diesel and fuel oil are very close toborder prices and there is a case for slightly increasing the price whichLPRC charges LEC for these products. The matter of serious underpricingof the electricity produced in the isolated power systems supplyingsmaller towns has been taken up earLier in para 5.

- ix -

Institutional Arrangements

12. Energy policy and planning is weak in Liberia, partly as a re-sult of a shortage of staff and experience in the Department of Energy(DOE), and partly because of the isolation of its parent ministry - theMinistry of Lands, Mines and Energy - from the mainstream of decision-making in the Government. No energy sector investment program is pro-duced and hence there is no policy framework for the development of thesector. The existing vehicle for policy dialogue in the sector is theNational Energy Committee (NEC). This body has advisory powers only, andalthough it has served a useful role initially in raising awareness inGovernment of the gravity of the energy problem, and later as a forum forthe ORNL/GOL energy assessment, it is now time to make a transition to awell staffed and equipped full-time energy policy and planning agencyclosely associated with the highest levels of Government decision making.The major energy parastatals - the Liberian Electricity Authority and theLiberian Petroleum Refining Company - make their plans without meaningfulconsultation with each other or the DOE, and promote them to theMinistries of Finance, of Economic Affairs and Planning, and the Head ofState, limiting critical review. Similarly, the Government is unable toadequately monitor the performance of its energy companies because itsdirectors lack both management experience and familiarity with energysector business. The main recommendations here include:

(a) the formation of an energy policy and planning division withinthe DOE separate from any functions of the former Bureau ofHydrocarbons and dissolution of the NEC.

(b) the formulation of administrative procedures which would estab-lish for this division a close advisory reLationship with theEconomic and Financial Management Committee of the GOL.

(c) representation of the head of the energy planning division orthe Director of Energy on the boards of the LEC and the LPRC orits successor.

(d) the provision of at least three full-time high level profes-sionals for the energy planning division plus support staff andtrainees and finance for at least four man-years of trainingper year.

Energy Sector Investment

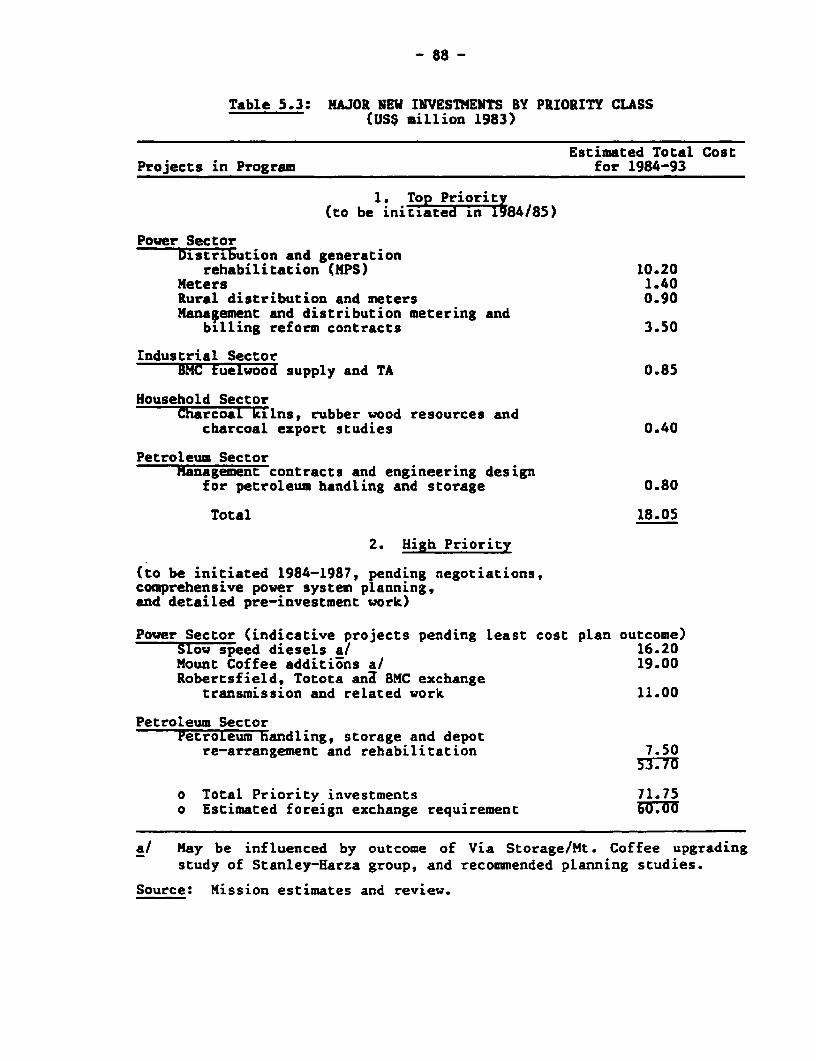

13. Investment projects totalling US$122 million (Table 5.4), whichinclude about US$80 million in foreign costs, are regarded as economi-cally justified by the mission for the 1984/1993 period. However, thereare such serious short- to medium-term fiscal constraints on public sec-tor investment that this will almost certainly mean that a smallerprogram of high priority investments will have to be adopted. A list ofthe higher priority inwestments is provided in Table 5.3 amounting toUS$72 million. Those in this priority category are urgent and need to be

implemented without deLay. Those in the higher priority category areindicative projects still to be precisely defined by engineering designand costing studies and Least cost planning studies. About 80Z of thisinvestment is required in the power subsector. This reduced programavwerages US$7 million per year compared with a maximum resource availa-bility for public sector investment in the next few years of US$100million p.a., although major investment is believed to be required earlyin the program. The major constraints on public sector investment gener-ally appear to be the provision of the local funds component of majorprojects. Both the LEC and the LPRC could generate sufficient localfunds and a substantial proportion of the foreign funds required tofinance their investment programs provided proposed reforms are made intheir operations. Yet it seems unlikely that significant new donor fundswill flow to the energy sector unless the energy parastatals demonstratea capability to reform, and to restore their own financial viability.

Priority Actions

14. The following are the highest priority activities proposedwithin each subsector, with the likely cost and duration in brackets:

Petroleum

(a) Design, costing and priority ranking in terms of benefit tooperational cost and efficiency of investments required totransfer the petroleum depot from the refinery to the WaterFront area, and to rehabilitate and reconfigure storage andhandling facilities ($200,000, three months).

(b) Procurement of management services to establish and operate theproposed new Petroleum Supply Company for three years and toliquidate the assets of the LPRC ($600,000 per year, six monthsto establish).

Power

(a) Power system efficiency audit to define the investments econo-mically justified in distribution and generation rehabilitationand to review the serviceability of all thermal generatingplant ($75,000, four months).

(b) Procurement of management services to manage and implementreforms in the LEC, including supervision of remetering, dis-tribution rehabilitation, re-organisation of accounting, estab-lishment of effective management information and decision-making systems and high-level management training and develop-ment ($500,000 per year, six months to establish).

(c) Bong Mine-LEC power exchange capacity review to determine thepresent level at which power can be sent in both directions,and the transformer capacity, protection gear and other

xi -

facilities required to facilitate transfer up to 40MW ($30,000,two months).

HaLsehold Energy

(a) Rubberwood and other forest energy resource inventory withinreach of Monrovia and other urban centers (US$100,000, sixmonths).

(b) Expansion of demonstration project for extensive field trialsof simplified metal charcoal kilns (US$80,000, six months).

(c) Charcoal export feasibility study which would also define theprospect of managing the Cape Mount State forests as a sustain-able charcoal resource (US$100,000, six months).

Industry

(a) BMC fuelwood supply and conversion pre-investment analysis(US$50,000, three months).

I. ERGY AND THE ECONY OF LIBERIA

Country Background

1.1 The area of Liberia is 112,000 square kilometers, more thanhalf of which is covered by natural forest. At the end of 1982 thepopulation was estimated to be about two million, with 35% classified asurban. However, the first census since 1974 was completed recentLy andmay reveal a somewhat different demography. The economy is divided intotwo significant and quite discrete sectors, an enclave sector consistingof mining, forestry and rubber concessions dominated by multinationalcompanies, and a subsistence agriculture sector. The latter supportsmore than 60% of the population, and all agricultural activities employclose to 80% of the work force. Industry and the service sector employ7Z and 14% of the work force, respectively. Unemployment is estimated tobe about 15Z of the potential work force and perhaps as high as 301 inthe urban areas. The enclave sectors are the main source of foreignexchange hence the global demand for iron ore, and to a lesser extentrubber and timber, largely determines the economic performance of themodern sector. Iron ore mining alone accounts for about one-third ofCDP, yet the links between this and other sectors are weak, resulting inuneven distribution of the benefits of their produ=tion, and localizedinfrastructure deveLopment. The estimated average per capita GNP in 1981was US$520, whereas the enclave sector produced a per capita CDP ofUS$1,620, and the entire modern sector, US$780. These are in contrastwith a per capita GDP of US$160 per year for the traditional sector.

Trends in Economic Performance

1.2 During the 1960s and early 1970s, the Liberian economy recordedhigh growth rates in CDP, 6% and 4Z per annum, respectiveLy. Thisimpressive performance was due to increasing output and unit value fromiron ore and rubber concessions and indirectly to an improvement in theterms of trade. This period came to an end in the mid-1970s as the priceof oil rose, the demand for iron ore and rabber declined precipitously,and the cost of mining operations escalated. The impact of these adverseglobal trends was exacerbated by poor management of the public sectorwhere the number of unprofitable parastatal entities mushroomed. Between1974 and 1979, GDP growth fell to an average of only 1Z per annum. Signsof economic recovery in 1978 and 1979 turned out to be illusory; growthwas partially the result of only a brief upturn in iron ore, rubber andtimber prices. Also, economic activity was temporarily stimulated by alarge injection of capital for construction of OAU conference facilitieswhich yielded little more in the medium term than an enduring debt ser-vice problem. On top of a declining external demand for enclave product,a revolution occurred in 1980 causing social disruption and ushering in aperiod of inappropriate policies, especially in fiscal management; a

- 2 -

trend that persisted until recently. GDP in the modern sector declinedby an average of 5.6% per annum between 1980 and 1982, compared with 1.1%per annum since 1976, 1/ as indicated in Table 1.1. In contrast to theearly 1970s, the terms of trade also deteriorated, falling by 24.5Zbetween 1978 and 1982. Finally, the balance of payments has deterioratedduring recent years due largely to the ongoing flight of capital. Thecapital account surplus, which was over US$135 million in 1978 (20X ofmonetary GDP), fell to US$6.1 million by 1981 and has been negativesince, illustrating the devastating nature of capital flight folLowingthe rice riots of 1979 and the coup of 1980. On the other hand, thecurrent account deficit narrowed from US$158 million (23.6% of CDP) toUS$44.6 million (6.2% of GDP) between 1978 and 1982.

Energy and the Economy

1.3 Trends in economic performance and the consumption of modernenergy forms over the last 8 years are shown in Table 1.1, and the costof imported petroleum is compared with total imports and exports inTable 1.2. For the most part, the direction of change in these indicesis parallel, with petroleum consumption falling more sharply than CDP,which reflects the relative petroleum intensity of the volatile enclaveeconomy. There is also a close relationship between trends in electric-ity consumption and GDP - a matter discussed again when reviewing thepower subsector in detail (see Chapter III).

1.4 It is evident that, like most other developing countries,Tiberia felt the impact of the oil price rises of 1979-80. The propor-tion of total export earnings spent on petroleum imports rose from alittle over 102 in the mid-1970s to about 25% in the early 1980s. NotonLy is the impact of oil imports on the balance of payments every bit assevere in Liberia as in many other African economies, but because theforeign exchange for the procurement of petroleum products had to comefrom the public sector, the impact of oil procurement on Governmentfiscal and external balance of payments was disastrous. Indeed,financing petroleum imports, together with debt service, have been themost important elements in the Government's external payments problems.Until 1982, cr-de oil was imported by the government and processed at thegovernment-owned petroleum refinery. The prima facie reason for theclosure of this refinery in January of 1983 was the Government's inabi-lity to service the oil facility financed by a consortium of foreignbanks for crude oil procurement. Since that time the country's refinedproduct needs have been satisfied by imports arranged through the former

1/ No accurate estimates of traditional sector GDP have been availablesince 1979. However, assuming that this subsector has been growingat about the same rate as the population, the cumulative decline intotal GDP becween 1980 and 1982 would be about 3.3% per annum.

refinery company and various enclave sector mulcinationals. Oil importsthrough the Government-owned LPRC are still constrained by a shortage ofdomestic revenue and foreign exchange. Indeed, in general, the importcapacity of the public sector is determined by domestic revenue genera-tion, foreign exchange availability or foreign credit established withoverseas banks. As foreign exchange and foreign credit have been con-strained over the past four years, there has been extreme difficulty inmeeting scheduled oil payments. The deterioration in the public sectordomestic financial resources and balance of payments have seriouslyundermined fiscal viability and overall confidence in the economy.

Indices of Change in the Energy Economy

1.5 The Liberian energy economy has been devolving since th late1970s if development in this context is defined as an increasing percapita consumption of modern fuels, i.e., petroleum and electricity.Petroleum consumption declined at more than ten times and electricityconsumption fourfold the rate of decline in modern sector CDP since theend of the 1970s; in per capita terms the rate of decline is evensharper. However, it is likely that the bulk of the population, thesubsistence sector, is relatively little affected by the vicissitudes ofthe enclave sector and its repercussions for urban-industrial produc-tivity and petroleum supply. There is practically no rural villageelectrification and the only petroleum consumption for most households isthe occasional use of kerosene lamps. In the macroeconomic context, de-clining petroleum consumption is now being reinforced by declining over-all imports and, together with real decreases in unit costs for petroleumproducts, should ensure that the burden of petroleum import costs on thebalance of payments is not further increased.

The Present Pattern of Energy Consumption

1.6 An energy balance for Liberia for 1983 is presented in Annex 1.The gross supply of energy to the economy is estimated at 1.3 milliontoe, and final consumption after conversion losses at 0.9 million toe.The pattern of final energy consumption is summarized in Table 1.3 below.Biomass fuels comprise 69% of final consumption, compared with 23% forpetroleum and 8Z for electricity. Almost 8% of final supply is met withcharcoal within the biomass fuel component, and directed almost exclu-siveLy to the urban household market. On a sectoral basis, householdsdominate consumption albeit comprised largely of woodfuels. Mining andtransport consume 10% and 162 of total final energy supply, accountingfor the great majority of petroleum consumption outside of electricitygeneration for public supply, whereas the government, conmercial andestate agriculture sectors consume less than 3% between them.

Table 1,1: TREN0S IN GOP AND MOOERN ENERGYCONSL'PTION, 1976-83

AverageAnnualGrowth

1976 1977 1978 1979 1980 1981 1982 1983 Rate (W)

GOP at factor costUSS million (1971 prices) 357.2 354.2 368.2 384.4 366.2 350.1 328.5 307.1 -2.18

Traditional GDP econ. 73.5 77.2 77.2 78 S. 80 82.4 / 84.9 / 87.7 a/ 2.56Total GOP f.c. (1971 prices) 430,7 431,4 445.4 462.4 446,2 432,5 413.4 394.8 -1.25GOP at Current Market Prices 761.8 872.9 943.7 1067.6 1116.8 1055.4 1063.6 1046,9 4.65Popeilatlon (1000) 1,632 1,690 1,743 1,810 1,873 1,941 2,012 2,088 3.55Petroleum Consumption ('000) n.a. n,a. n,a. 602 609 472 438 422 -9,3Electricity (GWh) b/ 329 339 344 367 364 341 323 308 -0.9 C

Per CapitaGOP f.c. (1971 USS prices) 263,9 255.3 254.7 255.5 238,2 222.8 205.5 189.1 -4.90Petroleum Consumption(Kgoe/year) n.a. n.a. n,a. 333 325 243 218 202 -13.31

Electricity Consumption(kWh/year) 202 201 197 203 194 176 161 148 -4.50

a/ Estimates,;/ Public or LEC Supply only: Generation minus 15S allowance for non-technical losses.

Source: Bank staff and mission estimates and GOL.

Table 1.2: PETROLEUI IMPORTS, RE-EXPORTS,AND TOTAL MERCJWNDISE TRAME, 1976-82

(million S)

1976 1977 1978 1979 1980 1981 1982

Refined Petroelum

Products Crude Oil 53.1 68.7 84.6 103.2 152.1 129,6 94.1

Petroleum Re-exports - - - - - - -

Not Petroleum Imports 53.1 68,7 84.6 103.2 152.1 129.6 115.1

Total Merchandise Imports

CIF 399.2 463.5 480.8 506.5 533.9 477.4 428.4

Non-petroleum merchandise

Exports FOB 457.1 447.4 486.4 536.6 600.4 529.4 477.4

Net petroleum imports/

Total lmorts 13.3 14,7 17.6 20.4 28.4 27.1 26.9

Net petroleum Imports/

Total Exports 11.6 15.4 17.4 19.2 25.3 24.5 24.1

a/ Not considering aviation and marine bunkers as re-imports.

Source: Economic Survey, 1982, pp. 15,20. Annual Report, National Bank of

Liberia, 1982.

Table 1.3: FINAL ENERGY CONSUMPTION, 1983

('000 toe)

Fuelwood Charcoal Electricity Petroleum Total Share

Mining - - 53.1 44.8 95.3 10.7

Other Industry 4.4 _ 2.8 1.6 8.8 0.9Transport _ - - 147.6 147.6 16.1

Agriculture - - 1.9 5.7 7.6 0.8Households 556.2 69.5 9.0 4.5 639.2 69.7

Commerce/Government 12.0 4.2 16,2 1.8

Total 560.6 69,5 78.8 208.4 917.3 -Share (1) 61.1 7.6 8.6 22.7 100.0

Source: Annex 1.

-6-

1.7 In a regional context Liberia has one of the most energy inten-sive economies. Two very crude indices of energy intensity are providedin Table 1.4 for countries in the West African region for which eitherenergy sector assessments have been completed or are underway. Theseindices compare only the use ot modern fuels with total population andeconomic production, and they illustrate well the impact of the miningsector on Liberia's energy economy for it is this activity which distin-guishes Liberia from the other countries for which this comparison ismade. With resource constraints looming and demand projections showingpoor iron and steel prospects, iron ore production in Liberia is certainto decline steadily during the remainder of the century. Therefore, bythe mid to late 1990s, the energy intensity of economic production inLiberia will more closely resemble that of the other regionaL economies.

Table 1.4: ENERGY INTENSITIES OF SELECTEDREGIONAL COUNTRIES, 1981-82

Consumption of modern Consumption of modernGOP per Energy forms per Energy formsCapita capita per unit GOP

(USS) (toe/1,000 people (toe/million USS)per year)

Liberia 520 352 677Ivory Coast 1,200 155 123Mali 150 22 153Upper Volta 250 26 104Benin 380 33 88Togo 320 92 288Senegal 450 66 147

Source: World Bank and mission estimates.

Recent Trends in Power and Petroleum Consumption

1.8 In the first instance, electricity production in the miningsector is about two-thirds of all power generation in Liberia but hasbeen declining rapidly in the past three years. There is an exchangeagreement between the public sector supply and the mines which has aminimal net balance but which effectively reduces the mining sectorspetroleum-based power consumption during the wet season and reduces thecost of the public system's petroleum supply during the dry season (seeChapter III for details). However, excluding mining sales, demand by thepublic at large has been declining since 1980 (see Table 1.1 and Annex14). Within the public supply system almost half of the consumption is bygovernment and commerce and about 40% by households. The contribution ofparastatals to commercial demand for el.ectricity is not identified,

-7-

though it is undoubtedly significant since air-conditioning is the majorload, and these quasi-governmental institutions are numerous and havetheir offices largely within the Monrovia Power System supply zone.Despite the overall decline in sales, it is likely that government con-sumption of electricity, directly or indirectly, has grown substantiallyin line with the growth in Government and parastatal employees since therevolution in 1980. It is also noteworthy that only about half the powergenerated is paid for, implying that roughly 40Z of power actuallydelivered is regarded as being free. When taken together, these observa-tions make the progressive decline in electricity generation and salessince 1980 all the more remarkable. The trends in petroleum product con-sumption year by year over this same period are also indicated in Table1.5. These data show that the most uniform and sharp decline in consump-tion occurred in 1981, the year during which fuel oil consumption felldramatically, reflecting a decline in mining activity. By 1983 thedownward trend for fuels commonly used by the general public and businesscommunity - gasoline, diesel and kerosene - had bottomed out and a smallamount of growth in demand was occurring over a greatly reduced consump-tion base. This recent positive trend in petroleum fuel consumption maybe related to a small resurgence in rubber production in 1983.

Table '.5: RECENT CONSUMPTION TRENDS FOR PETROLEUM AND POWER

Average1980 1981 1982 1983 1979-83- Percentage

Power Sales by LEC -0.9 -6.3 -5.3 -4.2 -4.5

Petroleum Product SupplyLPG -4*9 -10.3 17.1 -2.4 0.6Gasol ine -7.0 -14.4 -2.5 -5.3 -8.0Avgas 0 6.0 -22.6 -2.4 -5.7Jet fuel -28.9 -11.1 0.9 3.6 -10.9Kerosene -8.5 -16.1 -31.7 3.6 -16.5Diesel Oi l -13.3 -21.9 -13.5 5.3 -12.8Fuel Oil 24.3 -26.4 -5.0 -16.9 -8.5

Source: Mission estimates, LPRC, LEC.

1.9 Petroleum end-use in 1983 is provided in Table 1.6. From asectoral perspective the majority of the petroleum fuels used directlyare consumed in transport. Excluding the aviation fuels, 60% of theinternal transport fuel consumption is in the form of gasoline for taxis,light utility vehicles and other forms of public transport centered onMonrovia. Mining is responsible for more than 20% of direct petroleumconsumption divided equally between diesel and fuel oil. Diesel use in

- 8 -

mining is mostly for ore extraction and transport, whereas fuel oil isused for drying ore for pelLetisation. However, when petroleum-fueledpower production is included, the mines become the dominant end-usesector for petroleum. Almost all the power supply to LANCO, the onlyother large iron ore mine, comes from this source. Petroleum fuel usedin mining has, nevertheless, been declining during the 1980s and isexpected to decline further, eventually ceasing in the early to mid-1990sas high grade accessible ore is exhausted. Petroleum is used to generateone-third of the public power supply, and combined with mines and otherindustry generation, is responsible for consumption of over half of totalpetroleum imports. During the next decade there is the opportunity tomarginally increase the share of indigenous hydropower but there will beno significant displacement of oil-fired power generation by hydropowerwithin the next ten years. The consumption of petroleum fuels in thehousehold, manufacturing and agriculture sectors is less than 6% of thetotal used directLy. In industry fuel oil, diesel, and some kerosene areused for heat and steam raising. The manufacturing sector does generateelectricity with diesel to support its operations during outages on thepublic power supply grid, and the lost profits and displaced investmentcapital in ensuring this back-up is sizeable. Upper income householdsused LPG as a back-up to electricity for cooking. However, since therefinery closed, all LPG has had to be imported at a much higher cost.The sharp increase in price and only intermittent supply has caused con-sumption to drop. If public power supply becomes reliable the latentdemand for LPG will also decline and future imports are likely to benegligible in the context of overall petroleum supply. Kerosene is animportant lighting source and is supplied from the Ivory Coast throughunrecorded channels as well as through the port of Monrovia. The demandfor kerosene lighting is largely outside of the urban economy and appearslittle influenced by more global economic trends. Petroleum consumptionin agriculture is mostly in rubber production, with much smaller quan-tities in rice, palm oil, cocoa and other cash crops. Rubber prices haveimproved and the industry is being rapidly revived and expanded inLiberia though with the major rubber factories converting to wood-firedsteam plant, there will be little increase in the direct use of petroleumproducts in the industry outside of transport and power production.

Future Energy Demand

1.10 The prospects for economic growth in Liberia are uncertain,indeed the demand forecasts made by the mission assume that the miningsector will continue to decline and that possibly mining could cease by1993 unless large investments are undertaken to develop new ore bodies;such investments are unlikely to materialize due to the secularly weakdemand for iron ore. Such a prospect would greatly reduce the base andlevel of economic activity and modify the pattern of energy consumptionin future. The energy balance projected for 1993 (Annex 2) is based onthe most likely evolution of iron ore production and the respective minesas best forecast by the Bank's industry Department during the course of

-9-

the energy assessment mission. The key assumptions are outlined in Annex17 and are the best estimates that can be made on the basis of avaiLableinformation on the global steel market. This forecast bears strongly onthe demand forecast for electricity and for petroleum products generally,and consequently bears strongly on the scale and nature of energy sectorinvestment during the next ten years. However, because the major con-sumer in the iron ore sector, BMC, is assumed to remain in productionthrough 1992, assumptions of better prospects for the mining sector donot alter the conclusions materially (BMC's energy demand is five timesthat of LAMCO; see Table 2.2). It is, therefore, quite important to em-phasize that even with a more optimistic view of enclave sector produc-tivity, little change is implied during the 1980s in the overall energydemand and hence in the sector investment program the mission hasdevised. Moreover, no account has been taken in the forecast provided,of the potential savings in fuel oil in the Bong Mine through the use offuelwood (see para. 4.29), which are greater than che entire consumptionfor the NIOC. Similarly, any success in having consumers pay for elec-tricity consumed will tend to depress demand further and this effect hasnot been strongly built into the power demand forecast as projected (only25% of unpaid demand is assumed lost if it must be paid for: Annex 17),and the full impact of this, too, would tend to offset any new demandthrough better-than-forecast performance in the enclave sector. However,as a result of the changes in the forecast of economic prospects and thesectoral composition of production, major shifts are likely to occur inthe fuel mix and the sectoral pattern of consumption over the 1983-84period, rather than in the aggregate level of energy consumption. Themore significant of these are presented in Table 1.7, which is a summaryof selected components of the energy balances for 1983 and 1993 providedin Annex 2.

Table 1.6: FINAL CONSLMPTION OF PETROLEUMPRODUCrS BY SECTOR, 1982

(toe per day)

Gaso- Diesel Fuel PercentageLPG line Avgas Jetfuel Kerosene Oil Oil Total Share

Mining - - - - - 23.0 21.8 44.8 21.5Other Industry - 1.2 - - 0.2 0.6 0.8 1.6 0.8Agriculture 1.2 4,5 - 5.7 2.7Households 0.3 - - - 4.2 - - 4.5 2.2Transport - 70.2 0.6 30.4 - 46.4 - 147.6 70.8Comnercial/Government 0.3 - - - 1.0 2.9 - 4.2 2.0

Total 0.6 71.4 0.6 30.4 5.4 77.4 22.6 208.4 -Share (S) 0.3 34.3 0.3 14.6 2.6 37.1 10.8 - 100.0

Power Production - - - - - 54.4 156.1 203.9 50.3

Total 0.6 71.4 0.6 30.4 5,4 131.8 178.7 418.9 -Share (W) 0.1 17.0 0.1 7.3 1.3 31.5 42.7 - 100.0

Note: Excludes Petroleum DeDot Use.

Source: Mission estimates, LPRC, LEC.

- 10 -

Changing Fuel Mix

1.11 For reasons aLready elaborated above, fuel oil consumption de-clines sharply over the next decade. The decline would be even greaterif an increase in fuel oil fired power generation for public power supplywere not projected. For the foreseeable future fuel oil is perhaps thecheapest source of power generation to meet dry season demand, and tomeet the heat and steam requirements of the manufacturing sector. Thedemand for diesel oil is projected to decline not only through the reduc-tion in mining activity, but because of the more extensive use of fueloil displacing it for power generation as the least cost generation op-tions are implemented. However, diesel oil is the prime fuel for thetransport of manufactured goods, agriculture and forest products, and thereduction in its demand for ore handling is somewhat tempered by thegrowing demand for transport generated by recovery in these activities.A slight expansion in hydropower is anticipated which will displaceprimarily fuel oil, but also diesel oil fired power generation. Thegreatest expansion in supply of any fuel is that anticipated for char-coal, for which demand is seen to be linked with urbanization, and whichwill remain cheaper than its competitors - LPG and kerosene - throughoutthe period. The market for kerosene is small and relatively insensitiveto fluctuations in modern sector performance, as kerosene is predomin-antly used for lighting in rural areas. On balance, the demand for bio-mass fuels will grow slightly faster than the rate of population growth,and their share of final energy consumption will move from 70% to 80%over the period: a most atypical transition that can be likened to adevolution of the energy economy which in most other developing countriesis undergoing a slow but certain transition away from biomass fuels withurbanization and industrialization. The fact that fuelwood resources cansustain this transition, with reasonable management, is in part why thetransition is likely to occur but can be regarded, nevertheless, a for-tuitous characteristic of Liberia's natural resource endowment. Thedecline in consumption forecast for the major petroleum fuels is largelythe result of the projected possible closure of some of the iron oremines. The forecast increase in public power supply of 0.2% p.a. is verylow in comparison with aLmost any other developing country, and againreflects the relatively unique circumstance anticipated of losing a majorsource of wage and salary income in the period. This strong negative im-pact, and the impact on demand of having more and more consumers experi-ence the true cost of their consumption by being forced to pay theirelectricity bills, is only counteracted by growing urbanization and theaccumulation of minimum need for electricity for Lighting, some cookingand other services.

1.12 Sectoral consumption patterns change with the possible loss ofmining and this counteracts any relative growth in transport energy usestimulated by the expansion of economic activity in commercial agricul-ture and forestry. The share of household energy use increases as dis-cussed above, though also as an outcome of the decLine in energy use inother sectors. The net effect of these sectoral and fuel mix changes isthat final energy use per capita shrinks and overall energy use expands

- II -

at less than the rate of population growth through 1993. How decliningoil imports will affect the balance of payments depends, obviously, onthe level of export earnings outside of mining, the price of oil, andmany other factors that cannot be predicted with any accuracy. However,it is clear that the pressure on forests is going to increase dramatic-ally with the annual consumption of wood fuels growing by over one-thirdwithin the decade, and with this demand increasingly concentrated aroundcities and towns. The consequent need for improved forest and fuelwoodresource management is elaborated later in this report.

Table 1.7: SIGNIFICANT FUTURE TRENDS INENERGY SUPPLY AND CONSUMPTION

PercentageChange

1983 1993 Per Year

Major Energ yFormsor Sources CGross Supply)Puel Oil COrO toe) 185.9 38.9 -16.6Diesel Oil ('000 toe) 131.9 76.5 -5.6Firewood ('000 tonnes) 1636.3 2168.7 2.9Charcoal ('000 tonnes) 97.7 158.9 5.0Hydropower (GCh) 283.4 305.9 0.8

Fuel Class (Gross Supgly)Electricity (GWh) -'(public supply) 307.7 302.6 -0.2

Petroleum ('000 toe) 407.2 256.8 -4.7Biomass ('000 twe) 2,488.1 3,558.7 3.6

End-Use Sectors (Final use)Mining 000 toe) 95.3 0.0 n.a.Transport ('000 toe) 147.6 175.2 1.7Households ('000 toe) 639.4 866.9 3.1Agriculture ('000 toe) 7.6 11.0 3.8

Overall Energy Consumption (final use)Per caplta per yearAll Energy forms (kgoe) 438.1 367.9 -1.8Electricity (LEC Supply; kWh) 147.4 102.4 -3.7Petroleum (Kgoe) 99.8 66.6 -4.1

Total Energy ('000 toe) 914.7 1091.4 1.8

a/ Generation less 15% for non-technical losses.Source: Annexes 1 and 2.

Energy Pricing

1.13 The prices of petroleum fuels and electricity on the fonroviaPower System (MPS) are for the most part above the economic costs of

- 12 -

supply. Electricity pricing issues are discussed in detail in ChapterIII (paras. 3.28-3.33) though, briefly, the current tariff for the HPS isa uniform 15 cents/kWh, and the estimated LRMC is a little more than 9cents/kWh for low voltage consumers. Early in 1984 the SRMC for some ofthe thermal generation was above this tariff level, though measures havebeen proposed by the mission which would avoid this in the forthcomingdry seasons when thermal power is required at the margin. The maintariff issues for the MPS are financie.1 rather than economic and have todo with the rate of retirement of the LEC's short term debt, the size ofwhich depends, in turn, on the extent to which present outstandings haveto be regarded as bad debts. The mission has projected LEC's financialperformance under certain assumptions and shown that there is adequatescope for quite steep debt service over the next few years providingmetering, billing and other reforms are implemented (see para 3.19, andAnnex 15). In the GOL's isolated supply systems, revenues provide forless than one-sixth of the SRMC and urgent tariff reform is requiredprior to any further investment in power supply to these areas. A seriesof steps towards levying a more realistic cost-based tariff are providedby the mission in Chapter III (para. 3.33). The issues in petroleumpricing are more akin to those in respect of power on the MPS.

1.14 Petroleum prices and costs for supply to Monrovia are providedin Table 1.8. Border prices to bulk and retail consumers are estimatedin Annex 3, and the build-up of ex-depot prices from the Liberian Petro-leum Refining Corporation (LPRC) is provided in Annex 4. At the retaillevel, prices for gasoline and diesel oil are between 2.6 and 3.3 timesthe economic cost of supply, whereas fuel oil supplied to the manufactur-ing sector in Monrovia is about 2.3 times economic costs. Prices to con-cessions, on the other hand, range from being slightly below the borderprice in the case of fuel oil, to double this level in the case of gaso-line. Concession supply includes that to the Liberian Electricity Corpo-ration (LEC) which, in 1984, was evenly balanced between fueL oil anddiesel such that, on average, the economic price was being paid. In thefuture, as fuel oil becomes the dominant source of thermal power supplyto the public grid, the transfer price between the LPRC and the LECshould reflect full economic costs. Currently this is a rather academicconsideration as the LEC does not pay for the greater part of the oilsupplied by the LPRC. Similarly, concession holders, or the multina-tional companies operating the iron ore, timber and rubber enclaves, areincreasingly supplying their own product, especially fuel oil, hence theonly concern need be the level of cost recovery by the LPRC for the useof its product handling and storage facilities. The mission examined thecharge now levied on the Bong Mine for this purpose ($0.65/bbl) and foundit to be a fair reflection of economic costs incurred. A substantialpart of the ex-depot price for petroleum products is excise duty and,additionally for gasoLine only, a contribution to a "stabilization fund"established by the GOL to finance the debt built up in the Public Sectorthrough delinquency in payment between government departments and para-statals. The Level of excise tax and the stabilisation fund tax is amatter of fiscal policy about which there is ongoing dialogue between theCOL, the IMF and the World Bank. The mission's only observation is that,

- 13 -

unless the LEC greatly reduces unpaid power consumption, and both it andthe LPRC reduce their own excessive operating costs, these fiscalmeasures will not in themselves be adequate to resolve the cycling publicdebt problem. Therefore, the mission urges the COL to enforce the mea-sures outlined in the following chapters which are designed to radicallycut costs, improve operating efficiency, and increase cash flow to bothparastatals.

Table 1.8: PETROLEUM PRICES AND COSTS, MONROVIA, LIBERIA,FIRST QUARTER, 1984

(US dollars)

Ex-depot Retail Concession EstimatePrice Price Price Economic Cost-------- per US gallon -B- Bulk - Retail

Gasoline (Premium) 2.81 3.00 1.89 0.84 0.90Kerosene (Power) 2.33 2.55 1.4' 0.85 0.90Oiesel Oil 2.16 2.35 0.87 0.84 0.90Fuel Oi1 1.67 n.a. 0.68 0,72 n.a.Liquified Petroleum 1.75 2.00 n.a. n,a, n.a.Gas (per kg) (per kg)

Source: Oil Companies, LPRC and mission estimates, Annexes 3 and 4.n.a. = not available/applicable.

1.15 The firewood, fuelwood and charcoal markets are in privatehands and there is fair price competition. Some apparent anomalies inwoodfuels pricing are discussed in Chapter IV whereby prices for firewoodvary considerably across the Monrovia urban area and between Monrovia andits immediate hinterland. However, by and large, the market is operatingwell and supply of these fuels is efficient. Prospects have also beenidentified by the mission for reducing the economic cost of woodfuel pro-duction and exploitation of the natural forest resource by increasing theinformation available to entrepreneurs regarding opportunities to gainaccess to suitable fuelwood, and through offering incentives of creditand other facilities for the use of the least cost resources.

- 14 -

II. PETROLEUN

Background

2.1 The main issues in the petroleum sector are concerned with op-tions for the efficient procurement of refined petroleum products and thefate of the now dormant Liberian refinery. These issues embrace, inturn, the need to resolve serious financial problems threatening the con-tinuity of petroleum supply and the need to greatly streamline adminis-trative arrangements for importing and wholesaling petroleum as part of awider cost reduction program. In order to define a least cost practicalsolution to these problems the mission reviewed in detail the operationsof the Liberian Petroleum Refining Company (LPRC) and examined the physi-cal condition of the refinery and petroleum handling and storage faci-lities. Similarly, in order to better understand Liberia's petroleumprocurement options the mission examined relevant international petroleumproduct markets in the context of projected local demand. This chapterpresents the integration of these analyses of short and longer termissues and options in an attempt to define a strategy to reduce the con-straint imposed by high petroleum costs on Liberia's economic develop-ment.

Petroleum Resources

2.2 There are no known hydrocarbon reserves in Liberia. Potentialpetroleum resources have been identified in small sedentary basins on-shore and in the extension of thiLs sedimentary sequence offshore. In1971, four offshore wells were sunk, all of which proved to be dry,though there were hydrocarbon shows in many of the geological sequencesdrilled. Nevertheless, in line with the interests of the oil companiesconcerned in the global oil market -' che day, these concessions wereabandoned. In 1980, the Bank extended a US$5 million loan to Liberia forpetroleum exploration promotion, including a 2,500 km seismic program inthe offshore prospective zone. The outcome of this project has so farbeen an exploration production agreement between the GOL and Amoco Inter-national which is currently undertaking additional seismic work and pre-paring to drill the first of the four exploratory wells to which it iscommitted. It is obvious that the profile of Liberian energy policy willchange dramatically if economic reserves are established, though even ifthey were discovered this year there is unlikely to be an effect on thecountry's energy supply prior to the 1990s.

Petroleum Product Demand