leveraging data, tech and analytics to improve collections

TRANSCRIPT

Leveraging data, technology and next best action analytics to improve your collections

Speakers

Andy Beddoes

Consultant

Experian

Christine Pratt

Sr. Analyst

Aite Group

Paul Desaulniers

Sr. Director

Experian

3 © Experian

Christine Pratt

Sr. Credit Industry Analyst

Leveraging Data, Technology and Next Best Action Analytics to Improve Your Collections

4 © Experian

What we will discuss

1. Consumer credit portfolio trends

2. Sea change in debt collections

3. Is there appetite and funding?

4. Final thoughts

5 © Experian

Responses of 20 executives to an Aite Group 2016

survey of the top 50 U.S. retail lending institutions

with the largest consumer portfolio balances

Analysis based on a 2017 Aite Group online and

in-person survey of 41 executives at U.S.

community banks, credit unions, and finance

companies

Executives have extensive business or IT

responsibilities and titles that include president,

CEO, Director, CIO,CRO, and COO

Other information sources include estimates based

on government reports, industry knowledge,

discussions with and solution demonstrations from

vendors, company 10-Ks, and client references

Methodology

Source: Aite Group Survey of 20 credit executives from top 50 U.S. lenders, October 2015 to March 2016

Top 1 to 20 banks with largest

consumer and small-to-midsize

business portfolios

45%Top 21 to 40

banks with largest consumer and

small-to-midsize business portfolios

30%

Top 10 finance companies with

largest consumer credit portfolios

15%

Top 10 credit unions10%

Number of Executive Participants by U.S. Institution Type and Size of Credit Portfolio Balance (N=20)

6 © Experian

• Economy

• Consumer sentiment

• Regulations

• Interest rates

• Risk

• Returns

U.S. consumer credit market on the road to recovery

7 © Experian

No shortage of challenges for consumer lenders

8 © Experian

First signs of real consumer finance portfolio growth appear

Home mortgages70%

Helocs4.5%

Small business4.7%

Auto finance8.5%

Credit cards7.6%

Student loans2.7% Other

1.9%

U.S. Retail Loan Balances by Loan Type, January 2017(N=US$13.0 trillion)

Source: Aite Group analysis of data from Federal Reserve, Small Business Administration, and other industry sources

9 © Experian

Challenges in the numbers: too much work and not enough return

2016 portfolio’s composition very different from and much less profitable than 2005’s

Products 2016 2015 2013 2005

Credit cards 636 640 600 685Auto

finance 82 77 69 66

Mortgage 52 50 60 64

Student 26 28 52 55Home equity 15 16 33 37

Other 73 54 64 9

Total 885 865 878 915

Credit cards72%

Auto finance9%

Mortgage6%

Student3%

Home equity2%

Other8%

Total Number of Accounts in U.S. Retail Loan Portfolio, Year-End 2016 (N=e885 million accounts)

Source: Aite Group estimates

10 © Experian

Consumer loans see increasing delinquency levels

Source: Aite Group analysis of American Bankers Association and U.S. Federal Reserve data

2.9% 2.6% 1.8% 1.4% 1.2% 1.2%

6.3%

3.3%

2.4% 2.3% 2.4% 2.5%

3.3% 3.2%

1.7%1.6%

1.5%

1.8%

2009 2011 2013 2015 2016 2017*

Numbers of Delinquent U.S. Indirect Auto, Credit Card, and Heloc Accounts Shown as a Percentage of Accounts Managed by Regulated

Lenders in 2009, 2011, 2013, 2015, 2016, 2017(Q2)

Helocs Credit cards Indirect auto

11 © Experian

Charge-offs also continue to trend higher

0.120.47

1.79

3.06

2.14

1.461.13

0.50.25 0.2 0.07

3.734.33

6.44

10.5

7.97

4.72

3.913.39

3.03 2.913.46

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

U.S. Retail Loan Charge-Off Rates as of Q4 in Each Year, 2006 to 2016

Home mortgages All consumer Credit cards

Source: Aite Group depiction of U.S. Federal Reserve Data

12 © Experian

• Digitalization

• Personalization

• Self-serve

• Process revamps

• Cash flow

• Compliance

• Profits

Sea change in collections: Focus on customers, paring back costs

13 © Experian

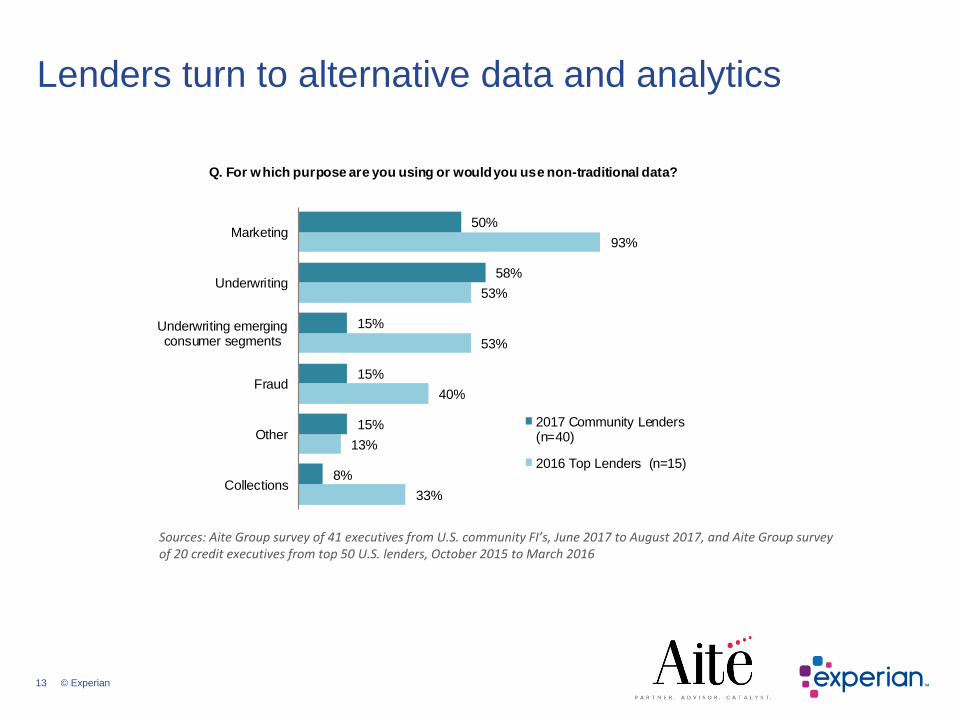

Lenders turn to alternative data and analytics

33%

13%

40%

53%

53%

93%

8%

15%

15%

15%

58%

50%

Collections

Other

Fraud

Underwriting emergingconsumer segments

Underwriting

Marketing

Q. For which purpose are you using or would you use non-traditional data?

2017 Community Lenders(n=40)

2016 Top Lenders (n=15)

Sources: Aite Group survey of 41 executives from U.S. community FI’s, June 2017 to August 2017, and Aite Group survey of 20 credit executives from top 50 U.S. lenders, October 2015 to March 2016

14 © Experian

10%

5%

25%

35%

17%

38%

40%

33%

15%

15%

28%

13%

5%

22%

2017 CL(N=41)

2016 TL(N=20)

2013 TL(n=18)

Approved or in the budget Very likely Likely Unlikely Very unlikely

Q. Please rate the likelihood that the following technologies would be approved by your institution: a new lending solution delivered in a hosted, SaaS, or hybrid environment.

Key driver: Growing acceptance of new IT delivery options

Sources: Aite Group survey of 41 executives from U.S. community FI’s, June 2017 to August 2017, Aite Group survey of 20 credit executives from top 50 U.S. lenders, October 2015 to March 2016, and Aite Group survey of 20 credit executives from top 50 U.S. lenders, February to June 2013

15 © Experian

IT budgets increasing for collections and for servicing

Sources: Aite Group survey of 20 credit executives from top 50 U.S. lenders, October 2015 to March 2016; Aite

Group survey of 20 credit executives from top 50 U.S. lenders, February to June 2013

10%

11%

15%

40%

28%

20%

37%

2016 (N=20)

2013 (n=18)

2016 (N=20)

2013 (n=19)

Colle

ctions

Se

rvic

ing

Q. What best describes your [2013 or 2016] consumer credit IT budget for each segment below?

Substantive increase from prior year(10% or more in enhancementsor new technology additions)

Modest increase from prior year(less than 10% in enhancementsor new technology additions)

16 © Experian

IT budget increases for data and analytics sought/received

17%

35%

22%

35%

24%

30%

27%

30%

2017 CL (N=41)

2016 TL (N=20)

2017 CL (N=41)

2016 TL (N=20)

Analy

tics

Data

managem

ent

Q. What best describes your [2016 or 2017] consumer credit IT budget for each segment below?

Substantive increase from prior year(10% or more in enhancementsor new technology additions)

Modest increase from prior year(less than 10% in enhancementsor new technology additions)

Sources: Aite Group survey of 41 executives from U.S. community FI’s, June 2017 to August 2017, and Aite Group survey of 20 credit executives from top 50 U.S. lenders, October 2015 to March 2016

17 © Experian

Final thoughts

New borrowers are scarce (and may stay that way),

improved communications’ support for collectors can

contribute to retention

Self-service whether for modifications or payments is a key

enabler of borrower satisfaction, lenders’ cost efficiencies,

and improved recoveries

Regulatory concerns need not overshadow profitability goals,

don’t let the true challenge—lack of demand for loans—get

lost in compliance fine print

Consider using credit risk and rising delinquency for IT budget

justifications: Vendor support is available for new platforms,

for overlays, for data and analytics

18 © Experian

Christine PrattSr. Analyst

[email protected]+1.617.338.6011www.aitegroup.com

Aite (pronounced “eye-tay”) Group is an independent research and advisory firm focused on business, technology, and regulatory issues and their impact on the financial services industry.

Visit us on the web and connect with us on Twitter and LinkedIn.

Improve Collection Performance

20 © Experian

Market ConditionsGreater Payment Stress across all products

• The top 20 card issuers grew portfolio

receivables YOY Q12017 by 6.6% while

growing delinquent receivables (60 days

past due) by 25.4%

• The cost effective management of

delinquent receivables is one of the top

challenges facing CRO’s

• New legislation (CECL, IFRS9) placing

further focus on collections

21 © Experian

Market ConditionsUS Auto Portfolio Dynamics are shifting: Delinquencies are rising

• Chart shows relative growth rates of

portfolios versus 60 DPD balances, YOY

• Combined Q12017 YOY portfolio growth

for top 20 lenders was 7.2%

• 60 day delinquencies grew by 25.4% in

the same period

• 10 of the top 20 US auto lenders 60DPD

receivables have grown at more than

twice the rate of their overall portfolios

• The challenge facing CRO’s is portfolio

growth without credit quality degradation

• Time to take a different approach? Source: Experian File One

Balanced Growth

EquilibriumAverage Top 20 Lenders

Lender’s Relative Portfolio

Size

Credit Quality

deterioration

22 © Experian

Collections professionals globally are concerned These external changes are driving a consistent set of challenges across the globe

Poor quality

contact

information

No effective

way to manage

restrictions on

customer

interactions

Lack of digital

capabilities to

enable

consumer self-

service

Painful

integration

makes it

difficult to

move past

legacy

constraints

Manual

processes

reduce

collector

efficiency

Limited ability

to execute

automated,

individualized

treatments

Experian Voice of Customer Research, March 2017

23 © Experian

Collections: Essential Premise

The essential premise of

collections is that if I can

contact my customer, I can

work with them to provide

debt resolution.

24 © Experian

Right Party Contact Rates in Decline

The essential premise of collections is that if I can

contact my customer, I can work with them to

provide debt resolution.

– Regulatory challenges

– 50% + no landline phone

– Single channel approach to collections

• Collections is overly dependent on single

channel outbound call strategy, with dated

analytics driving customer treatments.

CLIENT X, RIGHT PARTY CONTACT RATE

*Analytical project researching causes of delinquency increase at client X

25 © Experian

How do I improve collection performance in the age of declining RPC rates?

Drive the consumer

to the channel of

communication and

interaction that they

prefer

Consumers demand a frictionless and seamless customer experience

26 © Experian

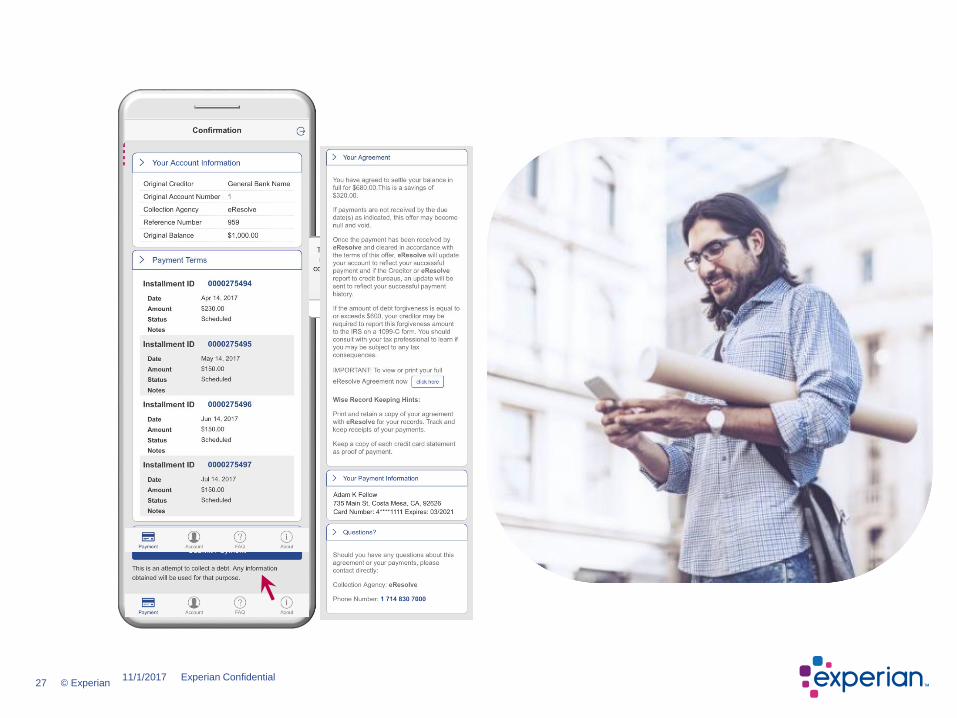

Elevate Collections into the Digital Age

Gives your clients

a digital communication channel

Manual

Collections Practices

Consumer in the

Digital World

#

No Caller ID

Frictionless Consumer Experience

eResolve™

• Digital (mobile and web)

• Non-threatening

• Resolution-driven

• At convenience of consumer’s place and

time

• Self serve / cost effective

3

27 © Experian11/1/2017 Experian Confidential

999

2017$75.00$300.00

4111111111111111

May

2020

Adam K Fellow

28 © Experian

To truly transform your collections

results you have to build your

strategies around the consumers

preferences.

But Digital is only the last mile ....

29 © Experian

Traditional (25 year old) approach to segmentation

1 Immediate high intensity outbound calling

2 Call day 1; medium / high intensity

3 Call day 1; medium intensity

4 Call day 1; low intensity

5 Leave to self-cure; call day 5, low intensity

6 Leave to self-cure; letter day 5, call day 10

7Leave to self-cure; letter day 10; call day

20

8 Leave to self-cure; letter day 20

Bala

nce

Risk score

30 © Experian

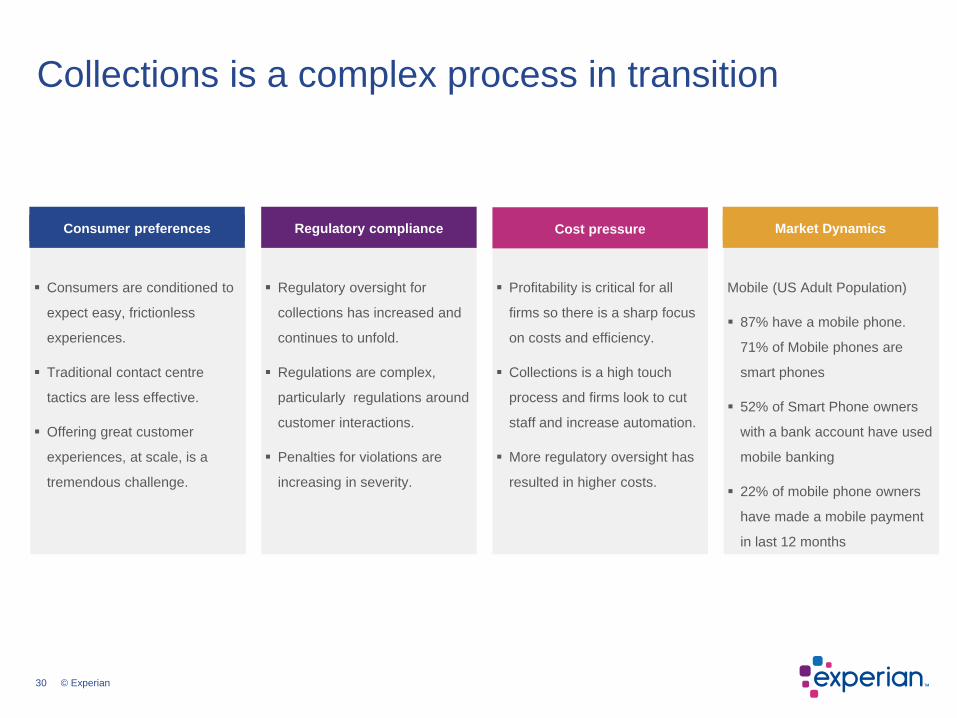

Collections is a complex process in transition

Consumers are conditioned to

expect easy, frictionless

experiences.

Traditional contact centre

tactics are less effective.

Offering great customer

experiences, at scale, is a

tremendous challenge.

Regulatory oversight for

collections has increased and

continues to unfold.

Regulations are complex,

particularly regulations around

customer interactions.

Penalties for violations are

increasing in severity.

Profitability is critical for all

firms so there is a sharp focus

on costs and efficiency.

Collections is a high touch

process and firms look to cut

staff and increase automation.

More regulatory oversight has

resulted in higher costs.

Consumer preferences Regulatory compliance Cost pressure

Mobile (US Adult Population)

87% have a mobile phone.

71% of Mobile phones are

smart phones

52% of Smart Phone owners

with a bank account have used

mobile banking

22% of mobile phone owners

have made a mobile payment

in last 12 months

Market Dynamics

31 © Experian

…by addressing key challenges facing collections teams we can make personalized collections a reality

Data

Analytics

Decisions

Execution

Blending customer information with credit,

behavioural, demographic and emerging data sets

enable a detailed customer view

Predictive models that inform decision making on the

basis of risk, behaviour, propensity, and overall

customer experience

Automated systems that use enriched data, analytics,

and collections policy rules to make decisions that

drive customer interactions or treatments

Systems and tools that support the collections

process by facilitating customer contact, negotiate,

and settlement

32 © Experian

Gain insights

Risk

Propensity

Behavior

Regulatory

..then build an effective, customer-centric process focused on an enhanced analytically driven experience

Collector

Enrich customer data

Contact

Credit

Demographic

Emerging

Collection agency Automated

workflow

Self-service

Decide

What’s the next

best action?

33 © Experian

..by using both batch and real-time decision management

11/1/2017 Experian Public

Expanding the scope of analytics through

the collections process

• Eligibility criteria for financial difficulties

programs

– Hardship

– Loan extensions

– Temporary reduced payments

• Settlement offers

• Agency placement optimization

34 © Experian

..which drive an efficient and automated collections workflow

• Focus collectors on key

tasks with a dynamic,

modern user interface.

• Provide collectors with

a granular view of a

customer’s relevant

information.

• Leverage capabilities

that improve contact,

response, and

commitment.

35 © Experian

Smarter CollectionsIntegrated ecosystem for collections and customer management

PowerCurve ® Collections

Batch Data• Triggers

• Premier Attributes

• Collections suite

Connectivity

eResolve™

PowerCurve ® Strategy

Management (batch and real

time analytics)

Behavior

history file

Real Time Data • Consumer credit

• Premier Attributes

On us

Off us

Systems

of record

Client

Machine Learning

36 © Experian

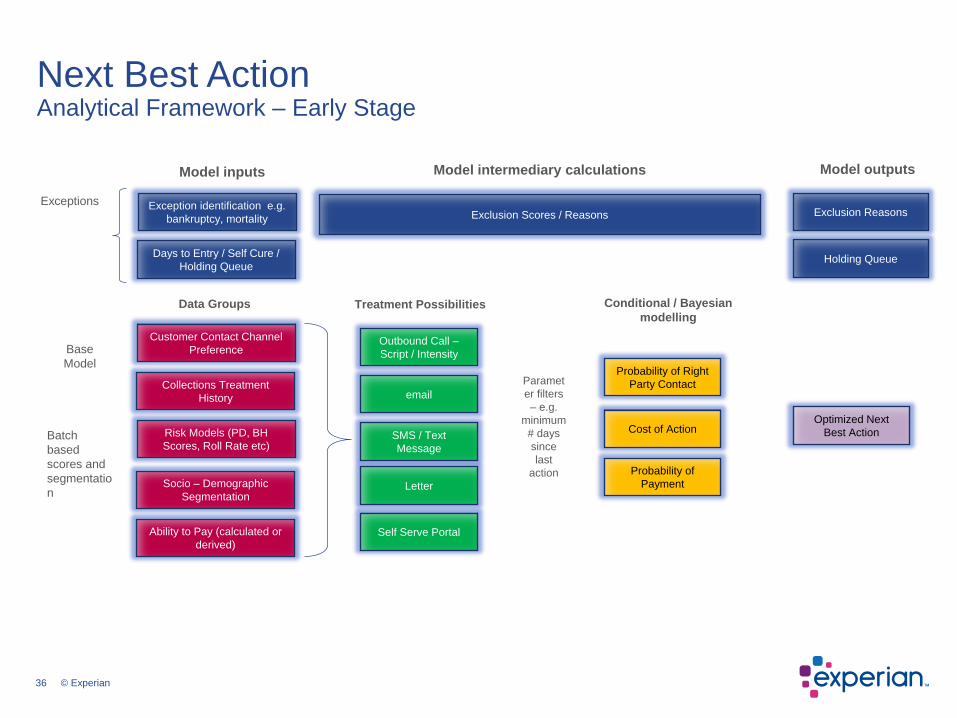

Model inputs Model outputsModel intermediary calculations

Conditional / Bayesian

modelling

Paramet

er filters

– e.g.

minimum

# days

since

last

action

Exception identification e.g.

bankruptcy, mortality

Base

Model

Batch

based

scores and

segmentatio

n

ExceptionsExclusion Scores / Reasons Exclusion Reasons

Customer Contact Channel

Preference

Days to Entry / Self Cure /

Holding QueueHolding Queue

Collections Treatment

History

Risk Models (PD, BH

Scores, Roll Rate etc)

Socio – Demographic

Segmentation

Ability to Pay (calculated or

derived)

Outbound Call –

Script / Intensity

SMS / Text

Message

Letter

Self Serve Portal

Probability of Right

Party Contact

Cost of Action

Probability of

Payment

Optimized Next

Best Action

Treatment PossibilitiesData Groups

Next Best ActionAnalytical Framework – Early Stage

37 © Experian

Customer FocusedOptimization in collections mathematically yields the highest value combination of actions

Data and Analytical

InsightCustomers

Thousands/Millions

Lifestyle needs

contact rules

competition

Customer-centric

marketing

ChannelsPreference

Offer/Treatment Timing(Any day/time)

Cross-channel strategy Product profitability

management

Resource efficiency

Maximum mail volume

Inbound capacity

contact history

Product portfolio

ROI hurdles

sales targets

Resource capacity

budgets events

Typical Constraints

Action A

Action B

Action C

Action D

Action E

Action F

1. Mon 5/5

2. Wed 5/7

3. Tue 5/13

4. Mon 6/2

5. Fri 6/6

Optimization Solutions

Data Lake

Customer contact

Channel preference

Collections

treatment history

Risk models (PD,

BH scores, roll rate

etc)

Socio –

demographic

segmentation

Ability to pay

(calculated or

derived)

Recommendations

• To enhance performance, a digital

strategy must be employed

• Better data, advanced analytics, and

automated decisions can now come

together to drive personalized

collections processes

• The customer experience will drive

improved results