level of awareness of non-bsba hed students on banking industry: basis for decision making

TRANSCRIPT

1

CHAPTER I

THE PROBLEM AND ITS BACKGROUND

INTRODUCTION

Banks have a major role in the economy of any nation. Most people know that

investing in a bank is a good institution to place our money to secure for the future. They

are engaged in the investment to have a bright future for their families and for themselves .

Today, we can see that in banking industry there’s a big competition. Banks come up

with several products that give them many choices in choosing the best for their clients.

Investment banking has played in generating economic growth, creating employment and

reducing poverty levels all over the world. It has a major role to play as the global economy

returns to reasonable growth.

As we all know, banking industry encouraged financial relationships with customers

of all sizes to supply financial products and services that arouse economic growth.

Mejorada (2009) stated that there are increasing number of people who work to achieve

financial security and stability by means of either putting up business or engaging in other

income generating activities aside from their current employment.

Banking industry provides products such as saving accounts, time deposit, checking

accounts and real estate/ mortgage loans that help the clients to provide what they need in

the future. As the banking industry becomes globalized and liberalized, clients anywhere

in the world will soon expect the same world class service from any bank or financ ia l

institution offering the same products.

Many of young people are not fully aware or informed in the said products particular ly

2

non-business students. They are not well-informed about the features and different benefits

of banking products. The researchers came up with the idea on testing the awareness of

students about them.

Sacred Heart College, Lucena City is one of the academic institutions in Quezon that

provides knowledge toward banking opportunities particularly in the business course.

Surely, the business students are capable in answering questions related to banking industry.

But this time, the researchers will be focusing on other students to test their awareness and

knowledge in investing at the banks.

In the light of these realities and with the aim of contributing valuable information, the

researchers found it essential to determine the level of awareness of selectednon-BSBA

HED students on banking products.

This study will be able to make the selected college students value the importance of

saving money and what kind of banking products would truly benefit them. Also for them

to realize that even they are not business students, they should be aware in invest ing

activities.

STATEMENT OF THE PROBLEM

The study would like to determine the level of awareness of selected non-BSBA HED

students on banking products: basis for decision making. Specifically, the researchers

sought to answer the following questions:

1. What is the demographic profile of the respondents in terms of:

A. Age

3

B. Gender

C. Course

D. Year Level

2. What is the level of awareness of selected non-BSBA HED students on banking

products in terms of:

A. Savings Account

B. Time Deposit

C. Checking Account

D. Real Estate/Mortgage Loans

3. How may the level of agreement of selected non-BSBA HED students on banking

products affect their decision making?

4. Is there a significant difference between the level of awareness of selected non-

BSBA HED students on banking products when they are classified according to

their demographic profile?

HYPOTHESIS

There is no significant difference between the level of awareness of selected non-

BSBA HED students on banking products when they are grouped according to their

demographic profile.

4

CONCEPTUAL FRAMEWORK

Input Process

Output

The paradigm shows the framework that guided the researchers in conducting the study.

The study made use of the input-process-output method wherein the input includes age,

gender, course, year level, level of awareness of selected non-BSBA HED students on

Demographic profile of the

responded in level of:

Age

Gender

Course

Year Level

Level of Awareness and

Agreement of Selected Non-

BSBA HED Students on

Banking Products in terms

of:

A. Savings Account

B. Time Deposit C. Checking Accounts

D. Real Estate / Mortgage Loan

Seminar containing information about

banking products and basis on decision

making

Analysis of level of

Awareness of Selected Non-

BSBA HED Students on

Banking Products

Analysis of level of

agreement of selected non-

BSBA HED students on

banking products affect their

decision making

Analysis of Significant

Difference between the

level of Awareness when

they are group according to

their Demographic profile

Figure 1. Level of Awareness of Selected Non-BSBA HED Students on Banking Products: Basis

for Decision Making

5

banking products and their decision making. The process is the analysis of level of

awareness and agreement of selected Non-BSBA HED Students on banking products and

the significant difference between the level of awareness when they are classified according

to their demographic profile. The output is seminar containing information about banking

products and basis for decision making. The respondents will have a knowledgeable and

wise decision making in the choice of banking products.

SCOPE AND LIMITATIONS

This study focused on “Level of Awareness of Selected Non-BSBA HED Students on

Banking Products: Basis for Decision Making”. Among non-BSBA HED students, we

included Accountancy students due to the reason that they are focusing more on keeping

the records rather than engaging with different banking products. Primary data were

gathered from the answers of the respondents who provided responses to the questionnaires

distributed by the researchers. Secondary data were gathered from books, journals,

newspapers and electronic resources. The study covered the second semester and summer

term of school year 2014-2015.

SIGNIFICANCE OF THE STUDY

The researchers wanted to share the importance of their study to other people, to whom

they feel would also benefit from this study such as:

School Administrators

It will help them to know the point of view of the college students from different terms

of banking products and how they manage their financial resources.

6

Business Administration Faculty

It will provide them information about different products provided by bank that will

serve as reliable source throughout their lessons and may enhance the lessons.

College Students

It will provide them the knowledge and understanding towards by banking products

particularly, non-business administration students. It may help them in choosing the suited

banking products for them.

Present Researchers

This will serve as a reliable source of information that may use in enlightening topics

related to their study. This can serve as a resource material on what the banks can provide.

This can also serve as a venue in applying the knowledge in Business subjects.

Future Researchers

This can serve as a guide for them to learn and broaden their knowledge in the field of

managing money effectively.

DEFINITION OF TERMS

The following terms were operationally defined for the purpose of easy understand ing

by the readers.

Banking industry- is a dynamic and significant component to individuals, corporates,

small and medium businesses, national and global, economic, socio and financial well-

being.

Banking products- a deposit account, savings account, certificated of deposit or other

deposit instrument issued by a bank.

7

Checking Account-is a bank account that allows easy access to the funds. It is the account

that you will use to pay your bills and make most of your financial transactions.

Decision Making – is the thought process of selecting a logical choice from the

available options.

Expected return- is a tool used to determine whether or not an investment has a positive

or negative average net outcome - it is not a hard and fast figure of profit or loss.

Interest rate – The amount charged, expressed as a percentage of principal, by a lender to

a borrower for the use of assets.

Investing- expend money with the expectation of achieving a profit or material result by

putting it into financial schemes, shares, or property, or by using it to develop a commercia l

venture.

Investment return – it is a performance measure used to evaluate the efficiency of an

investment or to compare the efficiency of a number of different investments.

Real Estate/ Mortgage Loan- Land plus anything permanently fixed to it, includ ing

buildings, sheds and other items attached to the structure.

Savings account- a bank account on which interest is paid, traditionally one for which a

bankbook is used to record deposits, withdrawals, and interest payments.

Time Deposit- A savings account or certificate of deposit (CD) held for a fixed-term, with

the understanding that the depositor can make a withdrawal only by giving notice.

8

CHAPTER II

REVIEW OF RELATED LITERATE AND STUDIES

This chapter presents the foreign and local literature and studies related to current

research. The researchers refer to all possible sources of information relevant to the present

undertaking substantial to this presentation.

The first part is discussion of related literature lifted from various sources like books,

internet, periodicals and other materials that are related to the present study. The second

part presents the findings of studies already taken which have direct bearing on the study.

The last part is the evaluation of the quality and findings of the research.

Related Literature

Mejorada (2009) stated that there are an increasing number of people who work

to achieve financial security and stability by means of either putting up business or

engaging in other income generating activities aside from their current employment.

Levitt (2012) cited that banking has played in generating economic growth, creating

employment and reducing poverty levels all over the world. Banking still has a major role

to play as the global economy returns to reasonable growth in the next two to three years.

Bunye (2011) stated that bank savings accounts have traditionally been one of the

simplest and most convenient ways to save. These accounts typically have the lowest

minimum deposit requirements and the fewest withdrawal restrictions. But they often pay

the lowest interest rates of any of the savings alternatives. However, when banks are

9

competing for your deposits, they may offer substantially higher interest or other benefits

for opening a savings account. Houston (2013) stated that time deposit is an interest-

bearing bank deposit that has a specified date of maturity. Checking account is very liquid,

and can be withdrawn using checks, automated cash machines and electronic debits, among

other methods. It include business accounts, student accounts and joint accounts along with

many other types of accounts which offer similar features. Checking accounts are offered

by most banking institutions for a minimal fee or no fee at all. Real estate is a special

instance of real property, which is real estate – land and buildings – plus the rights of use

and enjoyment that come with the land and its improvements.

Reilly et.al (2012) said that when current income exceeds current consumption desires,

people tend to save the excess. They can give up the immediate possession of these savings

for a future larger amount of money that will be available for future consumption. This

trade off of present consumption for a higher level of future consumption is the reason for

saving. And to make savings increase over time is to engage on investment.

Mejorada (2009) discussed that investment decisions should not be based on

emotions or sentiments. In some cases an investor buys a particular item of investment just

because everybody is buying the same. Then, there are also investors who “fall in love”

with their investments so that they are unable to sell to take advantage of the rise in prices.

Investment based on emotions or sentiments provide greater opportunities for the other

investors who make rational investors.

According to Caldwell (2013) to her article entitled ‘‘Money in your 20s Expert’’

if you have that much money, you are likely better off to put the majority into a savings

account or another type of investment tool. Your checking account should really only hold

10

the money that you need for your daily transactions during the month. Though some banks

do offer interest bearing checking accounts, the rates are usually lower than a savings

account.

Banzon (2010) said that real estate is and has always been the greatest wealth

builder in history that has been proven many times, and is presented in a number of

international bestsellers on the subject of investments. Unlike usual “paper” investments,

real estate is not subject to fluctuations common to stock or bond markets. “Real estate

investments are considered the ultimate security and a solid base for increasing wealth

because property values appreciate over time.”

Tan (2013) entitled “2 Things You Need to Know about Time Deposit” said that Time

deposits also earn higher interest rates compared to savings and checking accounts,

depending on the amount placed and term. The higher they are, the higher are interest rates.

Cornwell (2011) clarified that banking industry is a dynamic and significant

component to individuals, corporates, small and medium businesses, national and global,

economic, socio and financial well-being. This industry cultivates financial relationships

with customers of all sizes to supply financial products and services that stimula te

economic growth, and act as a catalyst to national and global economics. The industry

players produce a variety of services from savings accounts to home and business loans

and mortgages, and from fund mobilization to handling global mergers and acquisitions.

Abercombie explained that decision making is the thought process of selecting

a logical choice from the available options. When trying to make a good decision,

a person must weigh the positives and negatives of each option, and consider all the

alternatives. For effective personal decision making in terms on investment, a person must

11

be knowledgeable about investment world so you could determine which investment tool

is profited for you.

Colayco (2010) explained that earning and saving money is prerequisites, not a

guarantee, to achieving financial comfort. It is prudent and correct investing that will

ensure your financial independence. Investors however should not be obsessed only on the

kind of returns they can generate from the investment, but also be aware of the risks that

go with it. “Almost 90% of investors focus on returns and not on risks, not knowing that

risks are by and large controllable and returns are not.

Brown, et al. (2012) said that we must understand the risk factors that affect the

required rates of return and include them in your assessment of investment opportunities.

Because the required returns on all investments change over time and because large

differences separate individual investment, you need to be aware of the several components

that determine the required rate of return, starting with the risk-free rate.

Related Studies

Kumar(2013) entitled “A Study on Investment Pattern and Awareness of Salaried

Class Investors in Coimbatore District”, claimed that the sense of awareness of an investor

towards savings is created modified and shaped up by various external sources. The print

and electronic media such as the dailies, weeklies, television, radio etc., and personal

contact with friends, relatives, investment consultants etc, contribute a lot in creating

awareness among investors. As the awareness of investors is considered to be indispensab le

while studying one’s savings pattern, an attempt was made to measure the awareness level

of investors. Awareness is an abstract concept and hence it cannot be measured directly in

12

quantifiable terms. Moreover, there is no fixed or readymade method available to measure

it but the awareness can be indirectly measured.

Madhukarrao(2011) entitled “A study of Investment Awareness Among the

College Teachers in Latur District” said that Financial Management is not about earning a

lot of money but it point outs that we should be very careful while spending, saving or

investing it for the future.

According to Chua et.al (2009) entitled “Level of Awareness of the Major Students

on the Financial Investment Instrument Offered by Banks and the Degree of Risk Involved”

claimed that there are different types of financial investment includes shares, other equity

investment and bonds are the financial assets that are expected to provide income or

positive future cash flows and may increase in value giving the investor capital gains.

Espiritu, et al(2011) entitled “The Level of Awareness of Selected Sacred Heart

College Personnel on Investment Portfolio: Basis for Strengthening Financial Leverage”,

confirmed that investing is one way to make our life stable and reach or income goal. If we

don’t recognize the benefits of investment, we will miss a chance to have a life that is

wealth lifted and financially stable. In addition, we should instill awareness of the different

opportunities available even with meager resources.

Synthesis of the Review of Related Literature and Studies

The related literature shows the reasons why it is good to engage in banking products.

It also discussed why it is good to save in a bank and their respective products and how

investors come up with the idea of saving and their decision about it.

13

Investors found that it is convenient to save in different institutions that will generate

their income and to secure money for future use. When it comes to saving that includes

decision-making. Whether investor are going to save or not. What kind of banking products

are they going to engage with? In deciding, future investors must be knowledgeable in the

banking world so that they could choose the best product for them. It should not be based

on emotions. Every investors must be rational in saving.

Banking industry is a major choice in lending your money. Although interest rates are

low it is much better. It cultivates financial relationships with customers of all sizes to

supply financial products.

The related studies came from different foreign and local research studies that tackle

the importance of having enough awareness to different kinds of products offered by banks.

It also said that banking awareness is not just about earning a lot of money but it point outs

that we should be very careful while spending, saving or investing it for the future. Being

aware knows the existence and characteristics of a risky asset and have the same

information on the probability distribution of the return. The print and electronic media

such as the dailies, weeklies, television, radio etc., and personal contact with friends,

relatives, investment consultants etc, contribute a lot in creating awareness among

investors.

There are different types of financial investment includes shares, other equity

investment, banking products and bonds are the financial assets that are expected to provide

income or positive future cash flows and may increase in value giving the investor capital

gains. That made investing as one way to make our life stable and reach our income goal.

If we don’t recognize the benefits of different tools, we will miss a chance to have a life

14

that is wealth lifted and financially stable. And so, we really do need to have awareness

towards the different kinds of banking products, so that we will be easy for us to choose

for what is best for us to deal with.

15

CHAPTER III

RESEARCH METHODOLOGY

This chapter presents the technique and the procedures that were used to gather

relevant information regarding the problem that manifested by the researchers. The

contents of this chapter are research design, research locale, research population and

samples, research instrumentation, data gathering procedure and statistical treatment of

data.

Research Design

The researchers used descriptive method of research. This study is used to distinguish

the demographic profile of students about their age, sex and course, to recognize the

students’ level of awareness regarding investment opportunities offered by bank in terms

of investment tools, their level of agreement on it that affects their decision making and to

know the significant difference between the levels of awareness of respondents according

to their profile.

Research Locale

The research was conducted in Sacred Heart College Lucena City wherein various

courses are offered such as BSBA, BSCS, BSA, BSED, BEED, BSN, BSSW,

BSPHARMA, BSP and ABCOMM. The researchers have chosen SHC students to be their

respondents for them to assess the level of their awareness regarding banking products. The

respondents are college students particularly non-BSBA. SHC is the oldest catholic

16

institution in Quezon Province. It is accredited by the Philippine Accrediting Association

of School and University (PAASCU), located at 1 Merchan Street, Lucena City. It offers

quality education to students and provides knowledge toward investment opportunit ies

particularly in the business course. Also, the researchers believe that the students in SHC

are capable in engaging in banking activity at their young age.

Research Population and Sample

Selected college students of SHC particularly non-BSBA students served as the

respondents of the study to determine their level of awareness on investment opportunit ies

offered by banking industry. The researcher used Stratified Random Sampling Technique

in considering the total number of non-BSBA HED students of 919 for the second semester,

AY 2014-2015.

In determining the sample size, the following Slovin’s formula was used:

𝑛 = 𝑁

1 + 𝑁𝑒2

𝑛 =919

1 + 919(.052)

𝑛 =919

3.2975

𝑛 = 279

Where:

n is the sample size

N is the total population

e is the margin of error

17

Table 1

Distribution of respondents according to course and year level

There were a total of 279 respondents who met the set criteria for the stratified

random sampling. There were 15 respondents from Pharmacy, 20 from AB

Communication, 20 from Nursing, 30 from Elementary Education, 34 from Computer

Science, 35 from Social Work, 37 from Psychology, 41 from Accountancy and 47 from

Secondary Education.

Course Number of

Respondents

Number of respondents

per year level (n÷4)

Pharmacy (49/919*279) 15 15

AB Communication (65/919*279)

20 5

Nursing (67/919*279) 20 5

Elementary Education (99/919*279)

30 7.5 or 8

Computer Science

(113/919*279)

34 8.5 or 9

Social Work (115/919*279) 35 8.75 or 9

Psychology (122/919*279) 37 9.25 or 9

Accountancy (135/919*279) 41 10.25 or 10

Secondary Education (154/919*279)

47 11.75 or 12

Total 279

18

Research Instrumentation

The researchers prepared a questionnaire as the data gathering tools. The survey served

as the source of the data for the relevant information. The questionnaire was done in

consultation with the thesis adviser prior to its approval. The items in the questionna ire

were formulated based on the related literature and studies gathered from the reading of

various resources such as books, undergraduate thesis, internet and pamphlets.

The questionnaire was composed of three parts. The first part includes the

demographic profile of respondents in terms of age, gender, course, and year level.

The second part composed of different products offered by the banks and the

respondents’ awareness towards it.

The last part is about the level of agreement of selected non-BSBA HED students on

banking products that affects their decision making.

Data Gathering Procedure

After determining the sample size of respondents in which 279 as the total. The

researchers consulted their thesis adviser and some professor prior to its approval. They

sought permission from the Dean of College of Nursing and Pharmacy, Dean of College of

Accountancy and Computer Science, Dean of College of Education, Psychology and

Liberal Arts, and Dean of College of Social Work, by way of letter informing that this

study will be conducted before and during final exams until signing of clearance. The

copies of questionnaires will be distributed personally by the researchers to the

respondents.

19

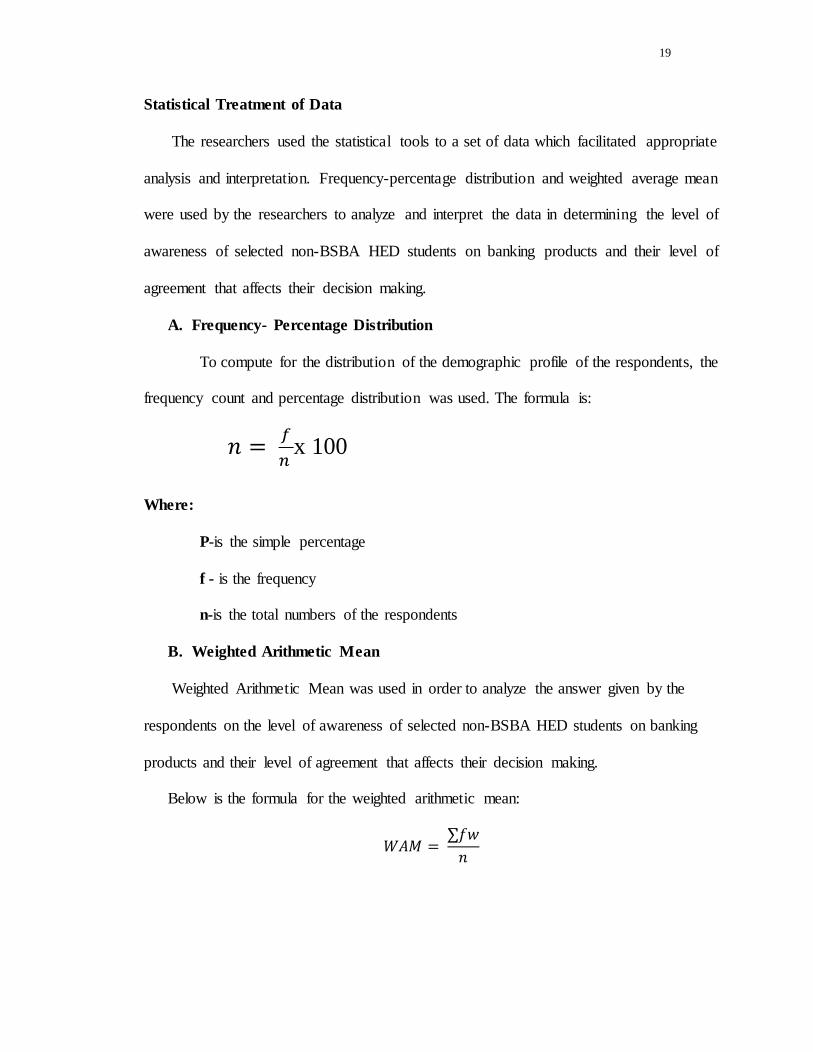

Statistical Treatment of Data

The researchers used the statistical tools to a set of data which facilitated appropriate

analysis and interpretation. Frequency-percentage distribution and weighted average mean

were used by the researchers to analyze and interpret the data in determining the level of

awareness of selected non-BSBA HED students on banking products and their level of

agreement that affects their decision making.

A. Frequency- Percentage Distribution

To compute for the distribution of the demographic profile of the respondents, the

frequency count and percentage distribution was used. The formula is:

𝑛 = 𝑓

𝑛 x 100

Where:

P-is the simple percentage

f - is the frequency

n-is the total numbers of the respondents

B. Weighted Arithmetic Mean

Weighted Arithmetic Mean was used in order to analyze the answer given by the

respondents on the level of awareness of selected non-BSBA HED students on banking

products and their level of agreement that affects their decision making.

Below is the formula for the weighted arithmetic mean:

𝑊𝐴𝑀 = ∑𝑓𝑤

𝑛

20

Where:

WAM - is weighted arithmetic mean

∑fw- is the sum of the product of the frequency and weight

n - is the total number of responses per item

Range:

Problem 2. Level of awareness of selected non-BSBA HED students on banking

products.

Descriptive scale with continuum Rating Verbal Description

4 3.26-4.00 Highly aware

3 2.51-3.25 Aware

2 1.76-2.50 Less aware `

1 1.00-1.75 Unaware

Problem 3. Level of agreement of selected non-BSBA HED students on banking

products that affect their personal decision making.

Descriptive scale with continuum Rating Verbal Description

4 3.26-4.00 Strongly agree

3 2.51-3.25 Agree

2 1.76-2.50 Disagree

1 1.00-1.75 Strongly Disagree

Problem 4. C. T-Test and ANOVA FORMULA

The T-Test and ANOVA Formula was used to determine the difference on the level of

awareness of the respondents on banking products when they are classified according to

their profile.

21

T-Test was used for the Gender:

𝒕 = 𝒙𝟏 − 𝒙𝟐

√[ ∑(𝒙𝟏− 𝒙𝟏)𝟐+ ∑(𝒙𝟐− 𝒙𝟐 )𝟐

𝒏𝟏+𝒏𝟐−𝟐][

𝟏

𝒏𝟏 +

𝟏

𝒏𝟐]

Where:

X1is mean of the first sample

X2is mean of the second map

S1is standard deviation of first sample

S2is standard deviation of second sample

n1 is number of items in first sample

n2 is number of items in second sample

ANOVA Formula was used for the age, course and year level:

SS bet = ∑(∑𝐱𝐀𝐢)𝟐

𝑵𝑨𝑰 -

(∑𝐱𝐢)𝟐

𝑵

SS tot = ∑x𝟏𝟐 - (∑𝐱𝐢)𝟐𝐬

𝑵

SS wit= SStot–SS bet

Where:

SS= sum of squares

SS bet = bet group’s sum of squares

SS wit = within group’s sum of squares

SS tot = total sum of the squares

22

CHAPTER IV

PRESENTATION, ANALYSIS AND INTERPRETATION OF DATA

This chapter presents the analysis and interpretation of data gathered to make this

chapter more scientific, the researchers followed the sequence of the questionnaire used in

this study. The data were gathered from the respondents of selected HED non-BSBA

students of Sacred Heart College in school year 2014-2015.

Part I – Demographic profile of the respondents

Part II – Level of awareness of selected HED non-BSBA students on banking products

Part III - Level of Agreement of the respondents on banking products as basis for their

decision making

Part IV –Significant difference between the levels of awareness of respondents when they

are classified according to their profile.

23

Part I – Demographic profile of the respondents:

Table 2

Frequency – Percentage Distribution of the Respondents

According to Age

Age Frequency Percentage (%)

15-17 61 21.86

18-20 206 73.84

21-23 12 4.3

Total 279 100

Figure 2

Frequency – Percentage Distribution of the Respondents

According to Age

The figure 2 shows the distribution of the respondents when they are classified

according to their age. The graph revealed that 73.84% of the respondents were belongs to

18-20 years old, followed by 21.86% which belongs to 15-17 years old and 4.3% which

belongs to 21-23 years old. It could be interpreted that the responses given by the

respondents were came from middle age.

24

Most college students are between 18 – 20 years old because 2nd and 3rd year

students fall in this age. While some 1st and 4th year are still on this age.

According to Becker, if you are young, it is not very important to put in a lot of

money for investment if you have very long term goal such as retirement. On the other

extreme, if you are middle aged and thinking about retirement, but you are just starting to

save for retirement, you should invest the maximum amount you can afford so you can live

comfortably when you retire. You should also put your money in a relatively safe

investment, so there is very little risk of losing much of it by the time you retire.

Table 3

Frequency – Percentage Distribution of Respondents

According to Gender

Sex Frequency Percentage (%)

Female 224 80.29

Male 55 19.71

Total 279 100

Figure 3

Frequency – Percentage Distribution of Respondents

According to Gender

The figure 3 shows the distribution of respondents when they are classified according

to their sex. The graph revealed that 229 or 80.29% of the respondents were female and 55

25

or 19.71% were male. It could be intepreted that majority of the responses to the

questionnaire were came from female respondents.

Most of the respondents are dominated by female because based on the statistics of the

school and even here in Quezon Province, women have greater population than men.

Another reason is the courses that being offered in school are somehow related to the

woman’s skill and capability these are Nursing, Pharmacy and Education. Also the men are

commonly taking criminology, marine, and engineering in which are not offered by this

institution.

One of the bases in identifying the capabilities of a person is gender. Problems were

unavoidable part of the investment, be it a man or woman owned investment. It is only the

type of problem that differs. According to Liebeman, Simma (2009), understanding of

different strength and styles that different genders bring to the work table could create more

equality for men and women. Man and women use different process in decision making.

Table 4

Frequency-Percentage Distribution of the Respondents

According to Year Level

Year Level Frequency Percentage (%)

First Year 79 28.32

Second Year 67 24.01

Third Year 66 24.01

Fourth Year 67 23.66

Total 279 100

26

Figure 4

Frequency-Percentage Distribution of the Respondents

According to Year Level

The figure 4 shows the distribution of the respondents when they are classified

according to their year level. The graph revealed that 66 or 23.66% of the respondents were

third year, 67 or 24.01% of the respondents were second year the same with fourth year,

and 79 or 28.32% were first year. It could be interpreted that the responses given by the

respondents were came from newly college students.

Most of the respondents are 1st year students due to the fact that during opening of

the semester there are a lot of freshmen students in school but due to the unnecessary events

like transferring to another school, population tend to decrease upon reaching next level.

27

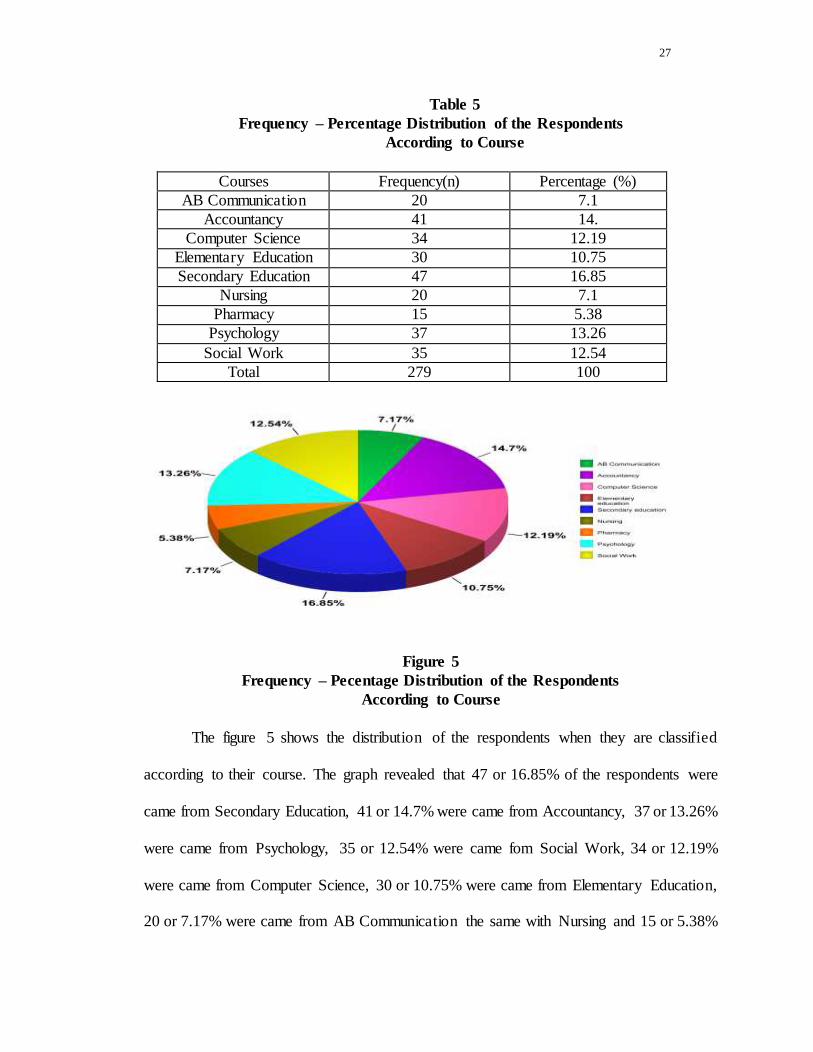

Table 5

Frequency – Percentage Distribution of the Respondents

According to Course

Courses Frequency(n) Percentage (%)

AB Communication 20 7.1

Accountancy 41 14.

Computer Science 34 12.19

Elementary Education 30 10.75

Secondary Education 47 16.85

Nursing 20 7.1

Pharmacy 15 5.38

Psychology 37 13.26

Social Work 35 12.54

Total 279 100

Figure 5

Frequency – Pecentage Distribution of the Respondents

According to Course

The figure 5 shows the distribution of the respondents when they are classified

according to their course. The graph revealed that 47 or 16.85% of the respondents were

came from Secondary Education, 41 or 14.7% were came from Accountancy, 37 or 13.26%

were came from Psychology, 35 or 12.54% were came fom Social Work, 34 or 12.19%

were came from Computer Science, 30 or 10.75% were came from Elementary Education,

20 or 7.17% were came from AB Communication the same with Nursing and 15 or 5.38%

28

were came from Pharmacy. It could be interpreted that the majority of the responses given

by the respondents were from Secondary Education students.

Pharmacy course has the least population due to the reason that it is a new course.

While Secondary Education has the highest respondents due to the fact that teaching is still

in-demand throughout the years and due to the new program called K-12 and so the students

prefer this course. But according to the professors of the school, nursing had the highest

population before due to the reason that it was in-demand.

29

Part II

Table 6

Level of Awareness of the Respondents on Banking Products

4 3 2 1 WAM VD

Saving Deposit

I know that Savings account is a bank account on which interest is paid, traditionally one for which a bankbook is used to record deposits, withdrawals, and interest payments.

138 104 20 17 3.30 Aware

I know that the minimum initial deposit is 500. 83 101 78 17 2.90 Aware I know that the interest rate is 0.25 %. 50 84 105 40 2.52 Aware

Total WAM 2.91 Aware

Time Deposit

I know that Time Deposit is a savings account or certificate of deposit (CD) held for a fixed-term, with the understanding that the depositor can make a withdrawal only by giving notice.

86 122 57 14 3.00 Aware

I know that the minimum initial deposit is 1, 000.

42 102 105 30 2.56 Aware

I know that the interest rate is .250% per 30 days.

25 74 117 63 2.22 Least Aware

Total WAM 2.59 Aware

Checking Account

I know that Checking Account is a bank account in which you can use in paying your bills and make most of your financial transactions that allow easy access to the funds.

105 100 65 9 3.08 Aware

I know that the minimum initial deposit is Php. 5000.00.

37 95 104 43 2.45 Least Aware

I know that there is no interest rate. 32 85 106 56 2.33 Least Aware

Total WAM 2.62 Aware

Real Estate/Mortgage Loan

I know that Real Estate or Mortgage Loan is a loan acquired from a financial institution to purchase a home or land.

75 74 86 44 2.65 Aware

I know that in investing Housing loan there are fixed periods with fixed interest rates.

66 93 93 27 2.71 Aware

I know that there’s repayment penalty on this loan.

74 80 94 31 2.69 Aware

Total WAM 2.71 Aware

TOTAL GWAM 2.72 Aware

30

Legend:

Table indicates the level of awareness of all selected Non-BSBA HED students on

banking products. The weighted arithmetic mean of 2.72 with a qualitative description of

AWARE reveals that non-BSBA HED students were knowledgeable on Savings

Account(2.91), Time Deposit(3.05), Checking Account(2.50), Real Estate/Mortgage

Loan(2.51) which offered by banks. They were AWARE on what Savings Account (3.30),

Time Deposit (3.00) and Checking Account (3.08) mean, and Real Estate / Mortgage Loan

with a weighted mean of 2.65. They were AWARE on the initial deposit of Savings Account

with a weighted mean of 2.90 and its interest rate with a weighted mean of 2.52. The

respondents were AWARE on initial deposit of Time Deposit with a weighted mean of 2.56

but LEAST AWARE on its interest rate with a weighted mean of 2.22. They were LEAST

AWARE on the initial deposit of Checking Account with a weighted mean of 2.33 and they

were also LEAST AWARE that it has no interest rate with a weighted mean of 2.17. The

non-BSBA HED students were LEAST AWARE that Real estate has fixed periods with

fixed interest rates with a weighted mean of 2.42. But they were AWARE that there’s

repayment penalty on this loan with a weighted mean of 2.70.

According to Caldwell(2013) to her article entitled ‘‘Money in your 20s Expert’’ if

you have that much money, you are likely better off to put the majority into a savings

account or another type of investment tool. Your checking account should really only hold

3.26 - 4.00 Highly Aware

2.51 – 3.25

Aware

1.76 - 2.50

Least Aware

1.00 - 1.75

Unaware

31

the money that you need for your daily transactions during the month. Though some banks

do offer interest bearing checking accounts, the rates are usually lower than a savings

account.

Banzon (2010) said that real estate is and has always been the greatest wealth

builder in history that has been proven many times, and is presented in a number of

international bestsellers on the subject of investments. Unlike usual “paper” investments,

real estate is not subject to fluctuations common to stock or bond markets. “Real estate

investments are considered the ultimate security and a solid base for increasing wealth

because property values appreciate over time.”

Tan (2013) entitled “2 Things You Need to Know about Time Deposit” said that

Time deposits also earn higher interest rates compared to savings and checking accounts,

depending on the amount placed and term. The higher they are, the higher are interest rates.

32

Part III

Table 7

Level of agreement of the respondents on investment tools offered by banking

industry that affects their personal decision making

Savings Account 4 3 2 1 WAM VD

I will look on the performance of the bank when I am about to invest.

157 100 22 0 3.48 Strongly Agree

I will not rely on banker’s recommendations because I will use my own research report to study, verify its assumptions and make my own decisions.

91 132 52 4 3.11 Agree

I will put my money in the bank for me to lessen my spending habits.

108 99 59 13 3.08 Agree

Total WAM 3.22 Agree

Time Deposit I will look on the interest rate when investing in a bank.

135 98 44 2 3.31 Strongly Agree

I will make sure that the money I’ll invest in a bank is the money that I can afford to lose.

98 87 75 19 2.95 Agree

I will focus more on the return than the risks involved.

72 110 67 30 2.8 Agree

Total WAM 3.02 Agree

Checking Account I will choose to have a bank account for me to have a convenient way in paying my bills.

111 131 25 12 3.22 Agree

I will choose to have an account for me to have an easy access funds.

108 105 59 7 3.13 Agree

I will avoid risks when investing. 79 124 53 23 2.93 Agree

Total WAM 3.09 Agree

Real Estate/ Mortgage Loan I will make sure that I understand the terms and condition before investing on it.

139 101 35 4 3.34 Strongly Agree

I will check on the longevity and integrity of the building management or association.

115 101 48 15 3.13 Agree

I will look into the design and construction guidelines as these will determine whether my selection will actually accommodate my needs.

116 103 43 17 3.14 Agree

Total WAM 3.20 Agree

Total GWAM 3.14 Agree

33

Legend:

Table indicates the level of agreement of all selected Non-BSBA HED students on

investment tools offered by banks. The weighted arithmetic mean of 3.14 with a qualitat ive

description of AGREE reveals that non-BSBA HED students were agree based on their

personal decision making. The respondents are AGREE on Savings Account (3.22), Time

Deposit (3.02), Checking Account (3.09), and Real Estate / Mortgage Loan (3.20) mean.

In Savings account, they were STRONGLY AGREE on “I will look on the

performance of the bank when I am about to invest” with the mean of 3.48 while they were

AGREE in “I will not rely on banker’s recommendation because I will use my own research

report to study, verify its assumptions and make my own decisions” with the mean of 3.11

and “I will put my money in the bank for me to lessen my spending habits” with the mean

of 3.08. In Time Deposit, they were STRONGLY AGREE in “I will look on the interest

rate before investing in a bank” with the mean of 3.31 while in “I will make sure that the

money I’ll invest in a bank is the money that I can afford to lose” and “I will focus more

on the return that the risks involved” they were AGREE with the mean of 2.95 and 2.80.

In Checking Account, they were all AGREE with the means of 3.22, 3.13 and 2.93. In Real

Estate/ Mortgage Loan, they were STRONGLY AGREE in “I will make sure that I

understand the terms and condition before investing on it” with the mean of 3.34 while in

3.26 - 4.00 Strongly Agree

2.51 – 3.25

Agree

1.76 - 2.50

Disagree

1.00 - 1.75

Strongly Disagree

34

“I will check on the longevity and integrity of the building management or association”

and “I will look into the design and construction guidelines as these will determine whether

my selection will actually accommodate my needs” with the means of 3.13 and 3.14 they

were AGREE.

Colayco (2010) explained that earning and saving money is prerequisites, not a

guarantee, to achieving financial comfort. It is prudent and correct investing that will

ensure your financial independence. Investors however should not be obsessed only on

the kind of returns they can generate from the investment, but also be aware of the risks

that go with it. “Almost 90% of investors focus on returns and not on risks, not knowing

that risks are by and large controllable and returns are not.

Kumar(2013) entitled “A Study on Investment Pattern and Awareness of Salaried

Class Investors in Coimbatore District”, claimed that the sense of awareness of an

investor towards savings is created modified and shaped up by various external sources.

The print and electronic media such as the dailies, weeklies, television, radio etc., and

personal contact with friends, relatives, investment consultants etc, contribute a lot in

creating awareness among investors.

35

Part IV. Significant Difference of the level of awareness of the respondents when they are

grouped according to their demographic profile

Table 8

F-test Results in Finding the Significant Difference between the levels of awareness

of respondents according to their age.

Variable

Compared df Means Computed

F-value Critical F-

value Decision Impression

@ 0.05 level

15 – 17 18 – 20 21 – 23

dfb = 2 dfw = 33 dft = 35

X1 = 2.90 X2 = 2.78 X3 = 2.63

1.868 3.28 Accept Ho Not significant

Table shows the F-test result in finding significant difference between the levels of

awareness of respondents when grouped according to their age. With the absolute

computed F-value of 1.868 and a critical F-value of 3.28, the researchers accept the null

hypothesis which is not significant at 0.05 level. This means that the level of awareness of

the respondents when grouped according to their age (15 – 17, 18 – 20, and 21 – 23) does

not vary significantly.

Table 9

T-test Results in Finding the Significant Difference between the levels of awareness

of respondents according to their gender.

Variable Compared

df Means Computed T-value

Critical T-value

Decision Impression @ 0.05

level

Male and Female

22 X1 =

2.79 X2 =

2.71

0.56 2.074 Accept Ho Not Significant

36

Table shows the T-test result in finding significant difference between the levels of

awareness of respondents when grouped according to their sex. With the absolute

computed value T-value of 0.56 and a critical T-value of 2.074, the researchers accept the

null hypothesis which is not significant at 0.05 level. This means that the level of awareness

of respondents when grouped according to their sex (male and female) does not vary

significantly.

Table 10

F-Test Results in Finding the Significant Difference between the levels of awareness

of respondents according to their year level.

Variable

Compared df Means Computed

F-value Critical F-

value Decision Impression

@ 0.05 level

1st Year 2nd Year 3rd Year 4th Year

dfb = 3 dfw = 44 dft = 47

2.77 2.99 2.65 2.55

3.671 2.83 Reject Ho Significant

Table shows the F-test result in finding significant difference between the levels of

awareness of respondents when grouped according to their year level. With the absolute

computed F-value of 3.671 and a critical F-value of 2.83, the researchers reject the null

hypothesis which is significant at 0.05 level. This means that the level of awareness of the

respondents when grouped according to their year level (1st, 2nd, 3rd and 4th year) vary

significantly.

37

Table 11

F-test Results in Finding the Significant Difference between the levels of awareness

of respondents according to their course.

Variable Compared

df Means Computed F-value

Critical F-value

Decision

Impression @ 0.05 level

Accountancy AB Communication Computer Science Elementary Education Secondary Education Nursing Pharmacy Psychology Social Work

dfb = 8 dfw = 99 dft = 107

2.98 3.02 2.86 2.48 2.50 2.82 2.69 2.24

4.771 2.03 Reject Ho

Significant

Table shows the F-test result in finding significant difference between the levels of

awareness of respondents when grouped according to their course. With the absolute

computed F-value of 4.771 and a critical F-value of 2.03, the researchers reject the null

hypothesis which is significant at 0.05 level. This means that the level of awareness of the

respondents when grouped according to their courses vary significantly.

38

CHAPTER V

SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATION

This chapter presents the summary of findings, conclusion and recommendation

derived from the data about the study entitled “Level of Awareness of Selected Non-BSBA

HED Students on Banking Products: Basis for Decision Making”.

Summary

The study entitled “Level of Awareness of Selected Non-BSBA HED Students on

Banking Products: Basis for Decision Making” was designed to determine the demographic

profile of selected non-BSBA HED students in terms of age, gender, course and year level.

Second is to determine the level of awareness of students on banking products. Third is

their level of agreement on the factors that will affect their decision making before dealing

on banking products. Lastly if there is a significant difference between the level of

awareness of selected non-BSBA HED students on banking products when they are

classified according to their demographic profile.

The study utilized the descriptive method. The study is conducted in Sacred Heart

College and the respondents are college students particularly non-BSBA with the total

average of 279. Stratified Random Sampling was used to facilitate the study. The

researcher used simple percentage method, weighted arithmetic method, T-test and F-test

for analysis and interpretation of data gathered and were presented in graphs and tables.

39

Findings

After analyzing the data gathered from the respondents, the researcher got the following

findings.

1. On the average of respondents there are 279 non-BSBA students, 20 comes from

AB communication, 41 comes from Accountancy, 34 comes from Computer

Science, 30 comes from Elementary Education, 47 comes from Secondary

Education, 20 comes from Nursing, 15 comes from Pharmacy, 37 comes from

Psychology, and 35 comes from Social Work with the total average of 279. When

it comes to Age only 61 respondents who are in between 15-17, 206 who are in the

age of 18-20, and the remaining 12 are in the ages between 21– 23 with the total of

279. Were male is 55 while female is 224 with the total of 279. And lastly when it

comes to year level the total of first year is 79, second year is 67, third year is 66

and fourth year is 67.

2. The total weighted arithmetic mean of 2.72 revealed that most of non-BSBA HED

students were knowledgeable on banking products with a qualitative description of

Aware. Among all the banking products, savings account got the highest WAM,

next is Real Estate/Mortgage Loan, followed by Checking Account and lastly is

Time Deposit.

3. As to the level of agreement of the respondents to the factors that will affect their

decision making before saving on bank, the responses resulted that they are all agree

with a total weighted mean of 3.14. It indicates that they will follow first the factors

before deciding on what banking product they will engage in.

40

4. That there is no significant difference in the level of awareness according to age

and gender but in the level of awareness when grouped according to year level and

course, there is significant differences.

Conclusion

Based on the result of the study the following conclusion were drawn.

1. Majority of Non-BSBA HED Students are come from Secondary Education. Most

of them are female. Majority of them are belong to 18-20 years old. First year

students got the highest number of respondents among all year level.

2. The course of Elementary Education, Nursing, Pharmacy, and Social Work are not

knowledgeable enough about banking products. While, college students that came

from Secondary Education, AB Communication, Computer Science, Accountancy,

and Psychology shows that they are aware about banking products

3. The respondents have differences when it comes to the level of awareness due to

the different fields that they are taking.

4. Non-BSBA HED Students’ awareness on banking products varies when they are

classified according to their course because they were encountering banking

products, specifically those students who came from Accountancy and Computer

Science. Some students who are already aware about banking products because they

already have bank accounts.

Implication Derived From the Study

The researcher identified the different kind of banking products, to help the Non-

BSBA HED Students to determine it before engaging so that they are knowledgeab le

41

before dealing with it. The Non- BSBA students were able to express their level of

awareness and their on banking products and it will be served as their basis on making

decisions in terms of saving in bank.

Recommendation:

In the light of the findings and conclusion, the researchers posed these

recommendation:

The student should learn about the different types of banking products, its features, terms

and conditions and other essential facts that they must know. It will be served as their basis

for selection.

That they should look for the factors that will affect their decision making in choosing the

best banking product to deal with.

That even this earlier time, they must know to save, specifically in the safest and most

convenient institution like bank, by prioritizing what they need or want.

For the future researchers they must gather more information and improve this research

study as well. They should have patience in conducting a survey and be more responsible

in accomplishing their tasks. To have a better understanding when it comes in investing.

42

Bibliography

A. Books

Brown, K., & Reilly, F. (2012). Understanding Investment Analysis and Portfolio

Management. C. Engage Learning Asia Pte. Ltd.

Bunye, I. (2011). Central Banking for Every Juan & Maria. Tomir Books.

Colayco, F. (2010). Pisobilities Gabay sa Buhay Pinansyal Pera mo, Palaguin mo!

Colayco Foundation for Education Inc.

Houston, F. (2013). Fundamentals of Financial Management. FINEX Research &

Development Foundation, Inc.

Jones, C. (2011). Investment Analysis and Management. John Wiley and Sun Inc.,.

Mejorada, N. (2009). Investment Management. FINEX Research & Development

Foundation, Inc. .

Pagoso, C. (2010). Money, Credit & Banking. Rex Book Store.

Reilly, F., & Norton, E. (2011). Investments, Fourth Edition. Elm Street Publishing

Services Inc.,.

B. Journals

Invest Now. (2009, May 4). Business World, p. Vol. 22 #1192.

How to invest in the Philippine Stock Market. (2011, February 6). Manila Bulletin, p.

Vol. 458 No. 97.

Banzon, J. (2010, October 28). Federal Land exec cites tips on Smart Property

Investment. Manila Bulletin, pp. Vol. 454 #28 B-8.

Buffet, W. (2009, October 13). Locked and Loaded: Protect your Investment. Manila

43

Bulletin, p. Vol. 23 #78.

So, M. (2011, February 6). Investment Watch: Why It's All About Timing. Manila

Bulletin, pp. Vol. 490 #20, P.C/D6.

Somera, D. (2010, October 5). Investment Risk Formula. Philippine Daily Inquirer, p.

Vol. 25 #299 pB3.

Tiongso, R. (2013, January 24). Where Do I Put My Money. Philippine Daily Inquirer, p.

Vol. 15 # 47 p133.

C. Unpublished Thesis

Kumar (2013, April) “A Study on Investment Pattern and Awareness of Salaried Class

Investors in Coimbatore District”

Madhukarrao(2011, April)“A study of Investment Awareness among the College Teachers

in Latur District”

Nabeta, et al(2012, April)“Investor awareness, perceived risk attitudes, and stock market

Investor behavior”

Chua et.al (2009, March) “Level of Awareness of the Major Students on the Financial

Investment Instrument Offered by Banks and the Degree of Risk Involved”

Espiritu, et al (2011, March “The Level of Awareness of Selected Sacred Heart College

Personnel on Investment Portfolio: Basis for Strengthening Financial Leverage”

D. Electronic Publications

Banking Industry www.investopedia.com

44

Tan Angelina Helen. Imoney. (2013 March 5) 2 Things You Need to know About Time

Deposit.http://www.imoney.ph/articles/what-you-need-to-know-about-time-deposit/

Kennon Joshua, (2012)Investing for Beginners Expert. http://beginnersinvest.about.com/od/Trust-

Funds/a/What-Is-A-Trust-Fund.htm

Caldwell Mirriam(2013) Money in Your 20s Expert

http://moneyfor20s.about.com/od/managingyouraccounts/a/checking.htm