let’s bank on shared value - welcome to the bank of …€¦ · let’s bank on shared value is...

TRANSCRIPT

Let’s bank onshared value

2014 Sustainability Report

BANK OF THE PHILIPPINE ISLANDS2 3 2014 SUSTAINABILITY REPORT

Over the last 163 years, the Bank of the Philippine Islands (BPI) has built stakeholder trust on the foundation of expertise in advisory and relevant products and services that empower our clients financially. Moving forward, we aim to keep every Filipino’s trust by embedding economic, social, and environmental value in everything we do. G4-3

Through our commitment to shared value, we aspire to contribute to Filipino society beyond the scale of the financial services we provide.

We realize that our continuing success as a financial institution significantly depends on how well we work for every Filipino’s long-term financial welfare and how well we enable sustainable development in the Philippines. Leveraging on our shared value focus and our vital assets—prudent capital management, engaged workforce, efficient processes, and continued trust by stakeholders—places us in a strong position to become the Filipino banking champion.

To this end, we continually innovate to transform the way Filipinos bank, enhance livelihood and businesses, and encourage more sustainable investments, while delivering value for our clients and shareholders.

In this report, we share with you our success stories thus far, our stories of “Banking on Shared Value.”

5 2014 SUSTAINABILITY REPORT

We believe in our responsibility to our Shareholders. We treat capital as a most valuable asset and seek to generate superior returns while being prudent in risk-taking, spending, and investment.

BPI at a Glance04

Let’s Foster Financial Inclusion37

06

129

Let’s Invest in Sustainable Development49

10

xx

Joint Message from the Chairman and the President and CEO

71 Let’s Enhance Our CARE Systems

Our Report

83 Let’s Empower Our People and Society

Our Business

101

109

Let’s Use Resources Efficiently

23 Let’s Set Financial Wellness in Motion

Let’s Build Trust

AppendicesGRI Content IndexIndependent Assurance StatementAcknowledgment

14

The BPI CredoWe believe our first responsibility is to our Clients. If we understand and address our clients’ financial needs, we will be entrusted with their most important financial transactions, and we will build lasting relationships. We do well when our clients do well.

We believe in our responsibility to our People. We seek to hire the best people for each job, provide them with the means to perform at a high level and reward them fairly. We value integrity, professionalism, and loyalty. We promote a culture of mutual respect, meritocracy, performance, and teamwork. We strive to be the employer of choice among Philippine financial institutions.

We believe in our responsibility to our Country. Our prosperity is greatly dependent on the well-being of our nation. We aim to be inclusive and responsible in nation building. Through BPI Foundation, we are committed to the welfare and sustainability of the communities we serve.

BANK OF THE PHILIPPINE ISLANDS4 5 2014 SUSTAINABILITY REPORT

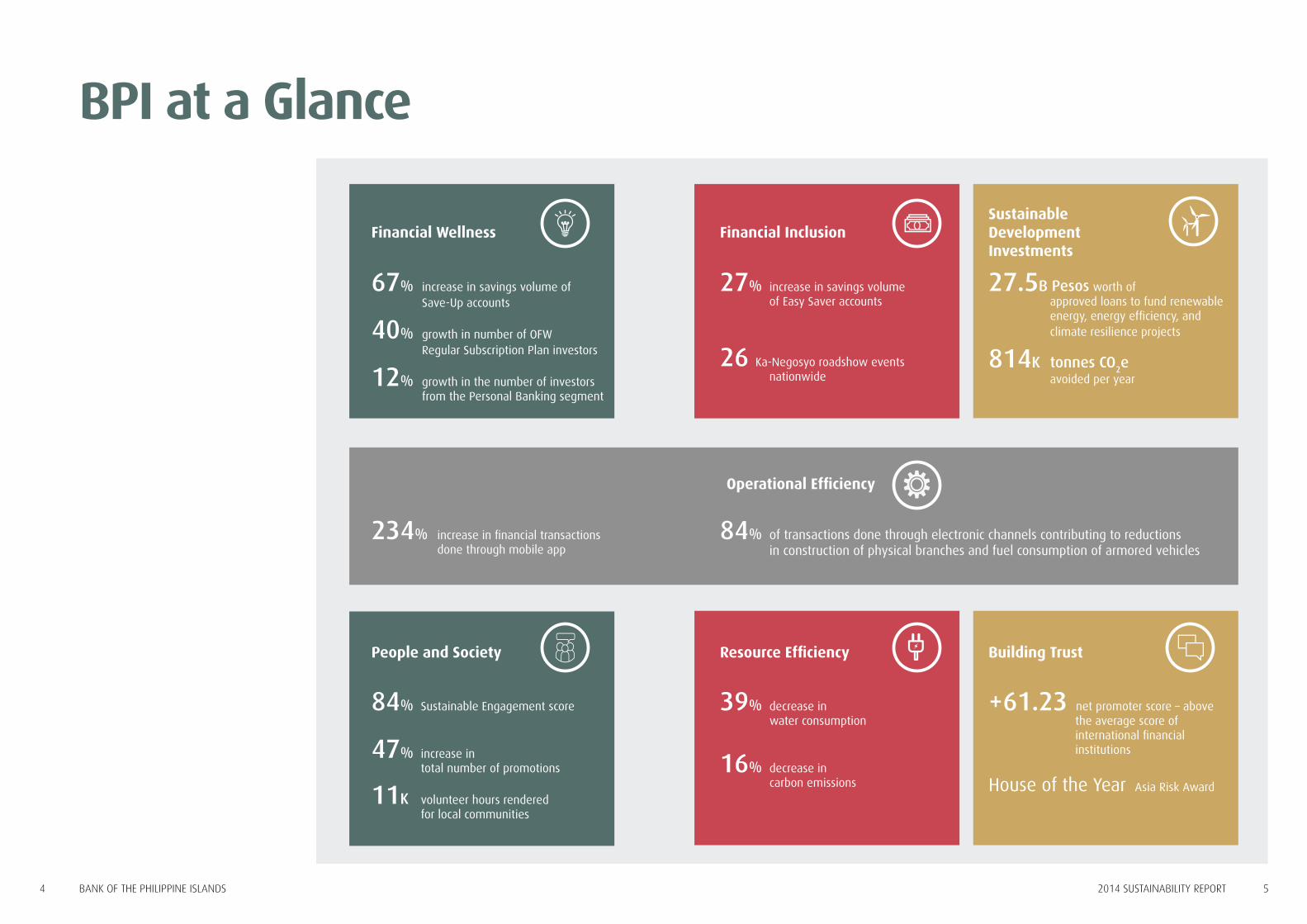

BPI at a Glance

84% Sustainable Engagement score

47% increase in total number of promotions

11K volunteer hours rendered for local communities

Financial InclusionFinancial Wellness

67% increase in savings volume of Save-Up accounts

40% growth in number of OFW Regular Subscription Plan investors

12% growth in the number of investors from the Personal Banking segment

27% increase in savings volume of Easy Saver accounts

26 Ka-Negosyo roadshow events nationwide

84% of transactions done through electronic channels contributing to reductions in construction of physical branches and fuel consumption of armored vehicles

234% increase in financial transactions done through mobile app

27.5B Pesos worth of approved loans to fund renewable energy, energy efficiency, and climate resilience projects

814K tonnes CO2e

avoided per year

+61.23 net promoter score – above the average score of international financial institutions

House of the Year Asia Risk Award

Building TrustPeople and Society Resource Efficiency

39% decrease in water consumption

16% decrease in carbon emissions

Operational Efficiency

Sustainable Development Investments

BANK OF THE PHILIPPINE ISLANDS6 7 2014 SUSTAINABILITY REPORT

Joint Message from the Chairman and the President and CEO G4-1

CHANGES ARE HAPPENING FOR YOU AT BPI

To all our stakeholders,

We have placed creating shared value as a cornerstone of our business. We continue to empower our people to innovate systems, products, and services that address our biggest sustainable development challenges – poverty, food security, climate change, ecosystems degradation, among others – while generating significant value for our business and our shareholders.

This year, we report on the progress we are making on three focus areas where we can deliver most impact – Financial Wellness, Financial Inclusion, and Sustainable Development Investments.

Financial Wellness

We aim to help every Filipino attain a strong financial foundation and build a healthy and productive financial future. We assist our clients by providing financial advice and offering a wide array of financial products and services suited for their needs. Our products are designed to foster a culture of saving, responsible borrowing, informed investing, and protection of asset value. We offer investment products with lower minimum amount requirement, as well as a regular subscription plan (RSP) that allows monthly contribution for investments.

BANK OF THE PHILIPPINE ISLANDS8 9 2014 SUSTAINABILITY REPORT

In 2014, we saw a 67% increase in Save-Up accounts, a 40% growth in OFW investors’ investments through RSP, an 8% increase in the number of mutual funds investors, and a 12% increase in the number of investors from the Personal Banking client segment.

Financial Inclusion

As a financial institution, we recognize our key role in addressing poverty. We continue to put special attention on the unbanked and low-income segments. We develop products that allow them entry into the formal banking sector.

Our Easy Saver product which does not require a maintaining balance helps low-income individuals start a relationship with the Bank. We help those who wish to start a business but do not have ready access to capital by offering affordable loans with extended payment terms.

In 2014, our total savings volume of Easy Saver accounts increased by 27% with a 14% increase in the number of account holders. We have also financed about 200 entrepreneurs who acquired franchise outlets.

Sustainable Development Investments

We focus on enabling investments that foster sustainable development, especially in the countryside. Of the total loans we provided in 2014, P94 billion went to investments in the countryside, boosting wholesale and retail trade, agriculture, manufacturing, and real estate, among others.

We are particularly proud to report that as of end of 2014, we approved P27.5 billion worth of loans to fund 174 projects in renewable energy, energy efficiency, and climate resilience. These investments generate over a thousand gigawatt hour (GWh) of renewable power, save 234 GWh of electricity from energy efficiency, and cut 814 thousand tonnes of greenhouse gas emissions.

Our Key Enablers

Our success thus far has been a product of efficient systems and channels, robust risk management, empowered employees, and customer trust.

Our electronic channels help reduce our transaction costs, thus enabling us to serve

Jaime Augusto Zobel de AyalaChairman

Cezar P. ConsingPresident & Chief Executive Officer

more low-income individuals. In 2014, 84% of total transactions were done through electronic channels, which reduced the need for many more physical branches.

We measure our performance as an employer using a sustainable engagement metric. In our latest survey, 84% of our employees consider themselves sustainably engaged, across various parameters such as involvement and empowerment, strategy and direction, as well as work tools and efficiency.

BPI’s proactive approach to enterprise and financial risk management allows us to effectively meet domestic and international market challenges. We have a strong top-down risk management culture, very experienced risk management leaders, well-defined risk appetite and metrics, and robust models and systems.

Our customers rated us 94.2% in overall customer satisfaction and 61.23 in net promoter score, which is well above the average score of international financial institutions. This is validated by the awards we received this year such as Best Payment Product Award, Diamond Award for Marketing and Best Retail Bank Award.

Our Business Bottomline

By serving our clients well, we achieve strong and sustainable financial performance. Our total revenue increased from P52.5 billion in 2013 to 55.8 billion in 2014. BPI recorded both net income and total comprehensive income of P18.0 billion, achieving a return on assets of 1.44 percent and a return on equity of 13.75 percent. For 2014, we received Bangko Sentral approval to pay P7.08 billion in total dividends, an annual payout ratio of 39.2 percent.

Looking Forward

We realize the extent of change we seek to create sustainable value for our clients, for the environment, for society and for our stakeholders via our various activities. What we achieved in 2014 inspires us to do more in the coming years. So, to all our stakeholders, “Let’s Bank on Shared Value.”

BANK OF THE PHILIPPINE ISLANDS10 11 2014 SUSTAINABILITY REPORT

Scope and Coverage G4-28, G4-29, G4-30

Let’s bank on shared value is BPI’s seventh annual Sustainability Report. It covers our business operations, inclusive of our subsidiaries and affiliates within the period of January 1 to December 31, 2014.

Purpose

This report presents the analysis of the economic, environmental and social performance of our business. Through this report, we update our stakeholders on the progress of the Bank’s shared value initiatives.

This report adheres to the Global Reporting Initiative (GRI) G4 Sustainability Reporting Guidelines and completed GRI’s Materiality Disclosures Service Check.

Data Sources

Sector performance data are sourced from the following documents or guidelines:

Economic Performance• Audited financial statements

conforming with Philippine Financial Reporting Standards

• Internally generated reports consolidated from the management information systems of the Bank’s various units

Environmental Performance• Consolidated data from our head

offices, Philippine branches, satellite offices, and subsidiaries

• Energy and water consumption from meter readings by utility companies

• Records of diesel consumption of vehicles and facilities

• Greenhouse gas (GHG) emissions calculations using the GHG Protocol Corporate Standards, Intergovernmental Panel on Climate Change (IPCC) emission factors for direct energy and National Grid Emission Factors of the country’s Department of Energy (DOE) for indirect energy

Social Performance• Internally generated reports

on our employee engagement, legal compliances and customer satisfaction

Assurance G4-33

The Bank enlisted TUV Rheinland, a global expert in Testing, Inspection, Certification & Training, for third-party verification. TUV conducted an Environmental, Social and Governance (ESG) on-site audit to ensure balance, accuracy, completeness, and comparability of the disclosures in this report. See pages 134 to 135 for the Independent Assurance Statement.

Our Report

Reporting Standards G4-32

This report is ‘In Accordance’ with the GRI G4 Guidelines - Core option for the non-financial performance. It is guided by peer performance comparison and benchmarking. The integrated macro and micro viewpoints enabled alignment with the 360° Sustainability Framework adopted by Ayala Corporation since 2013.

This report details 40 General Standard Disclosures, 20 Material Aspects and 25 Specific Standard Disclosures. See page 130 for the complete list of Material Aspects and its boundaries; pages 132 to 133 for the GRI Content Index.

Additional Reference

The Bank’s operational and financial performance is stated and filed at the Philippine’s Securities and Exchange Commission (SEC). It forms part of the Information Statement sent to stockholders. This is available for online access at www.bpiexpressonline.com.

Contact Information G4-31

For questions, comments, and suggestions, contact us:

Fidelina A. CorcueraChief Sustainability OfficerSustainability Office16th Floor BPI Building6768 Ayala AvenueMakati City 1226, Philippines Telephone: (632) 845-5202Email: [email protected]

BANK OF THE PHILIPPINE ISLANDS12 13 2014 SUSTAINABILITY REPORT

Sustainability Strategy FrameworkG4-2, G4-18, G4-19, G4-20, G4-21

Our Sustainability Strategy Framework guides our thrust to become every Filipino’s Banking Champion – in financial wellness, in financial inclusion and in sustainable development investments. To achieve this, we share in this report how we innovate for operational efficiency, empower our people and society, use resources efficiently, and continue to build stakeholder trust. This is aligned with our organizational philosophy as stated in our Credo.

OUR SUSTAINABILITY STRATEGY FRAMEWORK

FOCUS AREAS

ENABLERS

Enhancing Operational Efficiency

Setting Financial Wellness

in Motion

FosteringFinancialInclusion

Investing in Sustainable

Development

EmpoweringOur People and Society

Using ResourcesEfficiently

Building Trust

• Financial inclusion – We continually strive to widen our reach by developing products and services that address the needs and preferences of clients coming from low-income and underserved segments. We adhere to the ideals that true prosperity can only be achieved when everyone is involved.

• Sustainable development investments – We promote investments in industries that strengthen urban and countryside development. Advocating and advancing shared value financing, we also stimulate business innovation through cleaner, low-carbon, and resource efficient technologies. Our three main focus areas include:

• Financial wellness – We help individuals, communities and businesses grow their funds and build their wealth by facilitating financial

wellness opportunities, a range of innovative programs and more accessible investment options.

FOCUS AREAS G4-EC8

Culture of SavingResponsible BorrowingInvestment OptionsFinancial LiteracyWealth CreationAsset Insurance

Engaged EmployeesCareer DevelopmentEmployee SatisfactionEnvironmental SustainabilityEnterprise DevelopmentNation Building

G4-LA1, LA9, SO1

Convenient Banking | Electronic Channels | Cash Management Solutions | Retail ServicesReliable Remittances | International Network

Easy Saving OptionsPayment SolutionsAffordable LoansEnterprise AssistanceEmployee Stock OptionsMicro Insurance

FS7

Reduced Carbon FootprintConserved Fuel and EnergySaving on ElectricityDecreased Water ConsumptionSupply Chain Management100% Local Sourcing

Balanced DevelopmentWider AccessibilitySustainable FinancingLow-Carbon EconomyAgribusiness AssistanceCatalyzed Growth

FS6, FS8, G4-EN27

Customer SatisfactionHigh Quality ServiceMarketing BrillianceSound Risk ManagementBusiness Continuity ManagementLeadership Excellence

G4-EC1, PR5, PR7, PR8, HR3, HR4, HR5, HR6, SO5, SO8

G4-EN3, EN4, EN8, EN15, EN16, EN17, EC9

ENABLERS

15 2014 SUSTAINABILITY REPORT

Our Business G4-4, G4-5, G4-6, G4-8, G4-9

As one of the leading banks in the country for the last 163 years—our

business, products and services have contributed significantly to the national economic landscape and the day-to-day lives of Filipinos. Being the first bank established in the Philippines and in the Southeast Asian region, our history has been one of client trust, financial strength and innovation.

Our portfolio is strategically geared towards a sustainable and inclusive society. In our book, everyone is included. Individuals, enterprises and institutions alike benefit either directly or indirectly from the economic drivers generated by the Bank’s business. We will continue to deliver products and services efficiently, mindful of our corporate values of integrity, strength, innovation, and productivity.

With headquarters in the Makati Central Business District, BPI has ushered in

many firsts in the country’s banking and financial industry. This includes the automated teller machine (ATM), cash deposit machine (CDM), BPI Express Assist (BEA) machine, point-of-sale debit system, kiosk banking, phone banking, internet banking, and mobile banking. Our 825 branches and business centers and 2,575 ATMs and CDMs connect to form the largest combined network servicing seven million clients. Beyond nationwide coverage, our branch presence includes one in Hong Kong and four in Europe.

Acknowledged as a leading provider of financial services in the Philippines, together with our subsidiaries, we offer clients a wide range of financial products and services in corporate banking, consumer banking and lending, investment banking, asset management, insurance, securities distribution, foreign exchange, and leasing.

17%increase in total

economic value distributed(from 2013)

84% of revenue distributed

to key stakeholders

BANK OF THE PHILIPPINE ISLANDS16 17 2014 SUSTAINABILITY REPORT

Economic Value Distribution G4-EC1

Responsible contribution to nation building requires us to take on the challenge of fostering inclusive growth and wealth creation for every Filipino. This process begins in our internal systems and processes. Honest, accurate, and fair handling of information ensures that stakeholders who invest with the Bank are rewarded commensurately.

Fidelity to Ethical Corporate Citizenship

Our Unibank Central Accounting Division (UCAD) consolidates financial data, while Strategic and Corporate Planning Division (SCPD) assesses them for accuracy, in preparation for presentations to the Board of Directors and submission of reporting requirements to the SEC and Philippine Stock Exchange (PSE).

UCAD controls the Bank’s books of accounts to ensure accurate, fair and timely financial statements and other management reports. It also sees to it that all entities in the group compute and pay required taxes. It ensures compliances defined to UCAD with regulatory reporting to the Bangko Sentral (BSP), SEC, PSE, and Philippine Deposit

Insurance Corporation (PDIC). This ensures that all disbursements assigned to UCAD are processed within the prescribed authority limits.

SCPD is responsible for providing sound budget and variance analysis of the reports generated by UCAD. It guarantees that reporting requirements to the Bank’s Board of Directors and to government regulators are met.

The Board conducts check-and-balance practices as well as audits of the Bank’s financial performance and targets on a monthly basis. We also undergo quarterly and annual review checks by the SEC.

In million pesos

2014 Economic Figures

Economic value generated: Revenue 52,498

2013

47,385

2012

55,787

2014

Economic value distributed 48,041 40,120 47,125

Payments to suppliers

Payments to governments

Payments to employees

Payments to communities

Payments to providers of capital

Economic value retained

6,767

8,026

10,401

38

22,811

(656)

7,502

9,842

10,481

90

12,204

12,378

8,401

11,203

11,653

51

15,817

8,662

• Revenue / economic value generated: Our total revenue increased from ₧52.5 billion in 2013 to ₧55.8 billion in 2014, largely driven by the improvement in net interest income by ₧4.5 billion. For the same period, our ₧30.3 billion net interest income increased by 14.8% to ₧34.8 billion. This upsurge is due to expansion in our asset base of 24.6%, or ₧247.0-billion, tempered by a 28-basis point drop in net interest margin.

• Economic value distributed: Our total economic value distributed increased by 17%, from ₧40.1 billion in 2013 to ₧47.1 billion in 2014.

Payments to providers of capital: This refers to dividends paid and interest payments for deposits and borrowings. Amount totals from 2013 to 2014 show a 30% increase, from ₧12.2 billion to ₧15.8 billion.

Payments to employees: Disbursements due to salaries, wages and bonuses and staff benefits rose by 11%, from ₧10.5 billion in 2013 going up to ₧11.7 billion in 2014.

Payments to governments: These are tax payments made for corporate

revenue streams, i.e., interest income, foreign exchange, security trading, fees, commissions, and other income. These also include income and fringe benefit taxes for employees and taxes derived from properties and operational transactions. Taxes in 2014 amounted to ₧11.2 billion, a 14% increase over 2013’s ₧9.8 billion.

Payments to suppliers: This covers payments for trainings abroad and all suppliers and service providers. Procurement expenditures increased by 12% in 2014 reaching ₧8.4 billion, from ₧7.5 billion in 2013.

Payments to communities: This primarily pertains to donations and contributions to charities.

• Economic value retained: BPI posted a lower economic value retained from the previous year at ₧8.7 billion in 2014. This means we have increased our disbursements to key stakeholders. Our 2014 Annual Report, available online at www.bpiexpressonline.com, discusses our financial performance in detail.

Our indirect economic impact is discussed in detail in pages 21 to 81 of this report.

Economic Value Distributed in 2014

34%15,817

In million pesos %

18%

24%

8,401

11,203

25%

0.1%

11,653

51

a Payments to suppliers

b Payments to employees

c Payments to providers of capital

d Payments to governments

e Payments to communities

a

b

c

d

e

47,125M

BANK OF THE PHILIPPINE ISLANDS18 19 2014 SUSTAINABILITY REPORT

Defining What’s Material to UsG4-18

The Bank conducts periodic review of its materiality to identify key opportunities and risks relevant to emerging economic, social and environmental issues. We refer to key local and global sustainable development issues and define which issues we have the competencies to provide solutions to. We also value the perspectives of our four major stakeholders—Clients, People, Shareholders, and Country—that help us define our materiality, scope and boundaries.

Through this process, we are able to focus our efforts on areas where we are most competent on and where we are able to create the most positive impact.

This report defines management approaches for issues considered as material. We present our performance on these aspects using indicators that best capture our business context.

Guided by the GRI G4 Sustainability Reporting Guidelines, we conducted the materiality process, as outlined below.

Identification: Sustainability Context and Stakeholder InclusivenessWe referred to the 10 global megaforces identified by KPMG (Expect the Unexpected: Building Business Value in a Changing World, 2012)–climate change, energy and fuel, water scarcity, material resource scarcity, population growth, wealth, urbanization, ecosystem decline, food security, and deforestation–where any changes to which are likely to have the highest impacts to our business. We also looked at national trends and statistics, company reports, market and industry developments, and regulatory updates for localized sustainability context.

We collected information on stakeholder expectations as inputs to our process.

Prioritization: Materiality and Stakeholder InclusivenessWe engaged key officers and staff to identify which of the aspects are relevant to them and which fall under their competencies. Information were obtained through extensive series of meetings with various business units and through electronic communication exchanges.

In these discussions, we defined focus areas where the Bank can provide business solutions.

Stakeholder data including customer survey results, investor briefing materials and other information were used to validate identified material aspects.

We have consolidated these material aspects into our new BPI Sustainability Strategy Framework (see pages 12 to 13).

Validation: Completeness and Stakeholder InclusivenessOur management reviewed the BPI Sustainability Strategy Framework to ensure completeness and alignment to business strategy. Our various business units also confirmed that all important aspects and impacts of the business activities are considered.

Review: Sustainability Context and Stakeholder InclusivenessWe review our previous reports and continually find better indicators that provide a balanced picture of our impacts and sustainability performance. Moving forward, we will performs similar review process for the next reporting cycle.

BANK OF THE PHILIPPINE ISLANDS20 21 2014 SUSTAINABILITY REPORT

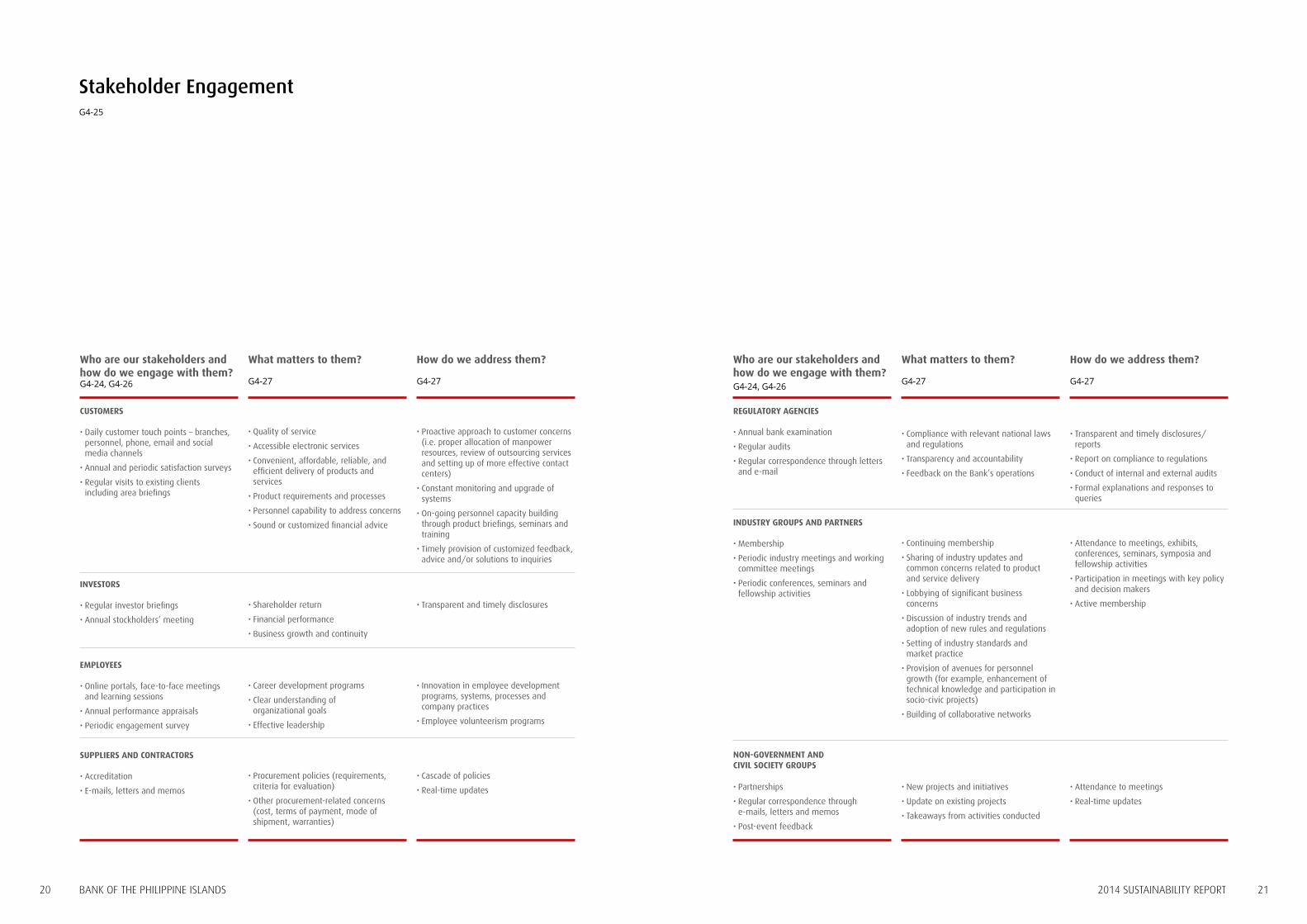

Stakeholder Engagement G4-25

Who are our stakeholders and how do we engage with them? G4-24, G4-26

What matters to them?

G4-27

How do we address them?

G4-27

CUSTOMERS

• Daily customer touch points – branches, personnel, phone, email and social media channels

• Annual and periodic satisfaction surveys

• Regular visits to existing clients including area briefings

INVESTORS

• Regular investor briefings

• Annual stockholders’ meeting

EMPLOYEES

• Online portals, face-to-face meetings and learning sessions

• Annual performance appraisals

• Periodic engagement survey

SUPPLIERS AND CONTRACTORS

• Accreditation

• E-mails, letters and memos

• Quality of service

• Accessible electronic services

• Convenient, affordable, reliable, and efficient delivery of products and services

• Product requirements and processes

• Personnel capability to address concerns

• Sound or customized financial advice

• Shareholder return

• Financial performance

• Business growth and continuity

• Career development programs

• Clear understanding of organizational goals

• Effective leadership

• Procurement policies (requirements, criteria for evaluation)

• Other procurement-related concerns (cost, terms of payment, mode of shipment, warranties)

• Cascade of policies

• Real-time updates

• Proactive approach to customer concerns (i.e. proper allocation of manpower resources, review of outsourcing services and setting up of more effective contact centers)

• Constant monitoring and upgrade of systems

• On-going personnel capacity building through product briefings, seminars and training

• Timely provision of customized feedback, advice and/or solutions to inquiries

• Transparent and timely disclosures

• Innovation in employee development programs, systems, processes and company practices

• Employee volunteerism programs

Who are our stakeholders and how do we engage with them?G4-24, G4-26

What matters to them?

G4-27

How do we address them?

G4-27

REGULATORY AGENCIES

• Annual bank examination

• Regular audits

• Regular correspondence through letters and e-mail

NON-GOVERNMENT AND CIVIL SOCIETY GROUPS

INDUSTRY GROUPS AND PARTNERS

• Membership

• Periodic industry meetings and working committee meetings

• Periodic conferences, seminars and fellowship activities

• Compliance with relevant national laws and regulations

• Transparency and accountability

• Feedback on the Bank’s operations

• New projects and initiatives

• Update on existing projects

• Takeaways from activities conducted

• Partnerships

• Regular correspondence through e-mails, letters and memos

• Post-event feedback

• Continuing membership

• Sharing of industry updates and common concerns related to product and service delivery

• Lobbying of significant business concerns

• Discussion of industry trends and adoption of new rules and regulations

• Setting of industry standards and market practice

• Provision of avenues for personnel growth (for example, enhancement of technical knowledge and participation in socio-civic projects)

• Building of collaborative networks

• Transparent and timely disclosures/reports

• Report on compliance to regulations

• Conduct of internal and external audits

• Formal explanations and responses to queries

• Attendance to meetings

• Real-time updates

• Attendance to meetings, exhibits, conferences, seminars, symposia and fellowship activities

• Participation in meetings with key policy and decision makers

• Active membership

BANK OF THE PHILIPPINE ISLANDS22 23 2014 SUSTAINABILITY REPORT

Let’s set financial wellness in motion

25 2014 SUSTAINABILITY REPORT

We aim to help every Filipino attain a strong financial foundation on which they can build a healthy and productive financial future. Our wide array of products

and services address our clients’ needs throughout their path towards financial freedom. In addition, our offerings are designed to help achieve long-term benefits for our clients, from fostering the value of saving, building healthy credit, to learning how to invest wisely and protecting assets. With this approach, BPI is well-positioned to be the Filipino’s banking champion, a champion that the Filipino public could trust to lead them to financial wellness, empowerment, and growth.

5,000individuals provided with stock market education

32% increase in number

of Jumpstart accounts

₧805.9Bsum insured

for earthquakes

₧824.8B sum insured for typhoons

₧824.8Bsum insured

for floods

8% increase in number of AMTG investors

BANK OF THE PHILIPPINE ISLANDS26 27 2014 SUSTAINABILITY REPORT

With only 43% of Filipino adults currently having savings (BSP National Baseline Survey on Financial Inclusion 2015), taking steps to improve this basic indicator of financial wellness is an imperative for us.

We offer a convenient means to help depositors regularly set aside a portion of their salary for future needs. The BPI Save-Up Account automatically transfers an amount specified by the depositor on a regular basis from an ATM source account such as Express Teller Savings, into a BPI Save-Up.

BPI Save-up also offers free insurance coverage through a tie-up with Philam Life Assurance Corporation. The insurance coverage–basic life insurance, accidental death, and accidental dismemberment–does not require medical clearance or premium payments. The coverage can equal to as much as ten times the account balance, with a maximum of ₧4 million.

Aside from scheduled automatic fund transfers, one may also transfer funds to his Save-up account any time. To further promote the habit of saving, the Save-Up account does not come with an ATM card and withdrawals cannot be made over the counter either. A Save-Up client may transfer and track his funds via our electronic banking portal, BPI Express Online (www.bpiexpressonline.com), the BPI Express Mobile app, or through our phone banking facility, BPI Express Phone (89-100). In 2014, total savings generated via Save-Up accounts grew by 26% from 2013, despite the 10% drop in the number of accounts. The average account size likewise increased significantly by 39%, showing that the average Save-Up account holder is able to save more over time.

Instilling a Culture of Saving

Year-on-Year Growth in Volume of Save-Up Accounts

2012 2013 2014

33%

Realizing that saving has more lasting impact when the habit is formed early on, we created a deposit product for the youth with the mentoring of their parents.

Branded as Jumpstart, it is BPI’s banner product in the BSP’s Build Up on Your Future (BOYF) Advocacy Program. Jumpstart’s product features enable parents to have a tool to teach their children practical money management and introductory banking, which are disciplines that hold value for life. These features are:

• Guaranteed Savings protects a portion of the child’s funds from unplanned withdrawals, to help attain a future goal.

• An allowance transfer facility ensures that the child’s allowance gets credited to his Jumpstart account on a timely basis.

• The Jumpstart ATM is as good as cash at over 40,000 BPI Express Teller Payment System-

accredited stores. It’s also the child’s Debit and Privilege Card when used at partner merchant outlets, where perks and privileges are offered.

• Cellphone reloading can be done at the nearest BPI Express Teller ATM, by calling BPI Express Phone at 89-100, by accessing BPI Express Mobile Menu on the cellphone, or on www.bpiexpressonline.com.

The continuing success of Jumpstart stems from targeted companies implemented by BPI’s Deposit Products Business Unit and Field Sales, together with the branches. Integral to these campaigns were the Financial Wellness Seminars for kids conducted in partner schools as well as product and advocacy awareness spread through Digital and Social Media Channels.

By 2014, the Jumpstart account holder base had grown by 32% from the previous year while volume has also increased by 14%.

Starting Them Young

Year-on-Year Growth in Average Savings per Account

2012 2013 2014

39%

Year-on-Year Growth in Number of Jumpstart^ Accounts

2012 2013 2014

38%

2012 2013 2014

19%

Year-on-Year Growth in Savings Volume of Jumpstart^

Accounts

26%

23%

14%

32%

BANK OF THE PHILIPPINE ISLANDS28 29 2014 SUSTAINABILITY REPORT

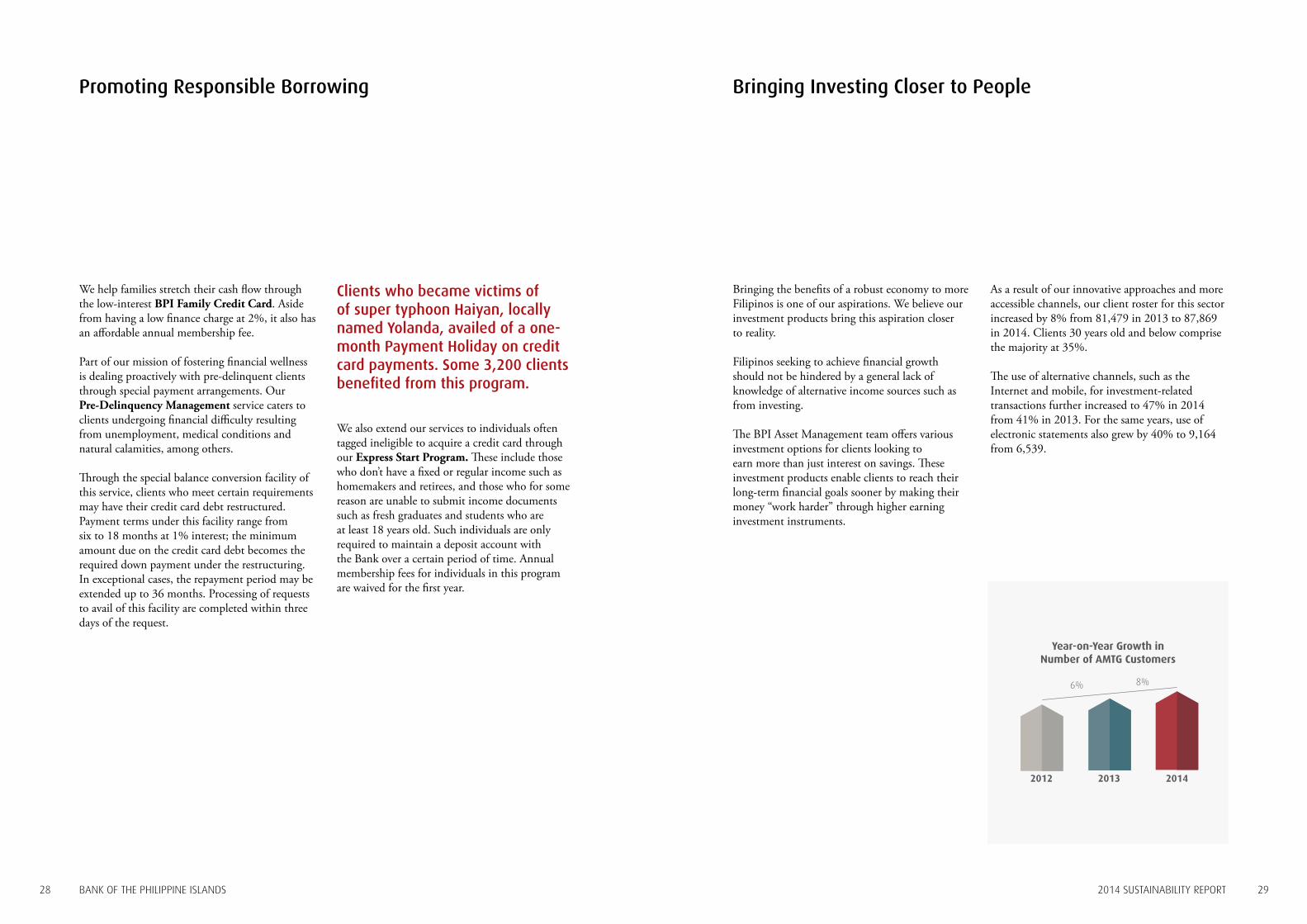

We help families stretch their cash flow through the low-interest BPI Family Credit Card. Aside from having a low finance charge at 2%, it also has an affordable annual membership fee.

Part of our mission of fostering financial wellness is dealing proactively with pre-delinquent clients through special payment arrangements. Our Pre-Delinquency Management service caters to clients undergoing financial difficulty resulting from unemployment, medical conditions and natural calamities, among others.

Through the special balance conversion facility of this service, clients who meet certain requirements may have their credit card debt restructured. Payment terms under this facility range from six to 18 months at 1% interest; the minimum amount due on the credit card debt becomes the required down payment under the restructuring. In exceptional cases, the repayment period may be extended up to 36 months. Processing of requests to avail of this facility are completed within three days of the request.

Clients who became victims of of super typhoon Haiyan, locally named Yolanda, availed of a one-month Payment Holiday on credit card payments. Some 3,200 clients benefited from this program.

We also extend our services to individuals often tagged ineligible to acquire a credit card through our Express Start Program. These include those who don’t have a fixed or regular income such as homemakers and retirees, and those who for some reason are unable to submit income documents such as fresh graduates and students who are at least 18 years old. Such individuals are only required to maintain a deposit account with the Bank over a certain period of time. Annual membership fees for individuals in this program are waived for the first year.

Promoting Responsible Borrowing

Bringing the benefits of a robust economy to more Filipinos is one of our aspirations. We believe our investment products bring this aspiration closer to reality.

Filipinos seeking to achieve financial growth should not be hindered by a general lack of knowledge of alternative income sources such as from investing.

The BPI Asset Management team offers various investment options for clients looking to earn more than just interest on savings. These investment products enable clients to reach their long-term financial goals sooner by making their money “work harder” through higher earning investment instruments.

As a result of our innovative approaches and more accessible channels, our client roster for this sector increased by 8% from 81,479 in 2013 to 87,869 in 2014. Clients 30 years old and below comprise the majority at 35%.

The use of alternative channels, such as the Internet and mobile, for investment-related transactions further increased to 47% in 2014 from 41% in 2013. For the same years, use of electronic statements also grew by 40% to 9,164 from 6,539.

Bringing Investing Closer to People

Year-on-Year Growth in Number of AMTG Customers

2012 2013 2014

6% 8%

BANK OF THE PHILIPPINE ISLANDS30 31 2014 SUSTAINABILITY REPORT

Advocating Financial Literacy

Promoting Investing as a Lifestyle

BPI consistently provides investor education programs. An important part of our efforts is an investment summit called Investment Roadmap which we conduct in various parts of the country. This summit highlights goal-setting and the means to achieve them through investing.

We also keep our clients informed on the state of economy and financial markets through financial advisories entitled BPI Asset Management WISE (Weekly Investment Series), Investment Insights and Investment Academy.

The world of investing is unfamiliar to most Filipinos. While people generally desire much bigger returns on their savings, their lack of knowledge and training in the many investment options keeps them from fulfilling their potential for financial growth.

We are adequately addressing this need through investment seminars and training. We educate our clients on the how-tos of investing based on their particular capacity, willingness, and risk appetite. Harnessing the power and reach of social media, we are gradually transforming public perception on investing, making it more accessible and attainable.

BANK OF THE PHILIPPINE ISLANDS32 33 2014 SUSTAINABILITY REPORT

Educating People on the Stock Market

Only 1% of Filipinos invest in the stock market, in contrast to Hong Kong’s 30% plus. We aimed to change this trend by democratizing access to financial markets and increase the stock market penetration rate in the country. To this end, BPI Securities established the Invest-in-You Trading Academy (I-TRAC) to educate potential retail investors on stock market investing.

This move propelled BPI Securities to be the 9th highest ranked broker in terms of market share among 184 Philippine trading participants. It also currently holds second place among all online brokers in the country. The program’s effectiveness is evident in the increased volume of trade transactions, which has multiplied five times over the past two years.

I-TRAC’s investor education programs promote stock market investing to ordinary citizens in schools, workplaces and various organizations in the country. Since 2013, the I-TRAC program has served more than 5,000 individuals. Stock market education seminars now run five to six times a month, where previously they were held twice a month in 2013.

One of the ways by which BPI Securities promotes investing as a lifestyle is through the Pinoy Millionaryo Club (PMC). We have virtually become the industry leader, being the only broker in the country with a successful track of hosting a “community” of investors. Through social events, seminars and social media campaigns, clients become passionate about investing and gamely interact with one another in a more deeply connected environment. Our goal is to help create as many Filipino millionaires as possible.

Having access to sound financial advice helps our client to properly navigate the market, make sound investment decisions and choose the right stock options. As members of PMC, they benefit from one-on-one sessions with our stock market coaches and are given priority in our investor education seminars. Moreover, they get access to exclusive research and special events.

Creating Filipino Millionaires

To determine the best investment option for a client, BPI Asset Management considers both investment capacity and risk tolerance. The client is given access to the best available investment information to build confidence and set realistic expectations from investments.

Our clients with limited financial know-how or start-up investment money are assisted through our Investment Funds. Unlike deposit accounts (savings and current accounts) that are generally for emergency and daily needs, our investment funds serve longer term financial goals, like tuition, retirement and home ownership. Our Investment Funds allow for greater flexibility and variety of investment choices:

These allow clients to start an investment account for as low as ₧10,000. Our UITFs are invested in the money market, bonds, and equities. Clients may choose particular funds to invest in, according to their preferred investment strategy. Withdrawal of earnings from UITFs can be made at any time.

These funds are managed by BPI Investment Management Inc. (BIMI), a wholly-owned BPI subsidiary. Our professionally managed mutual funds provide more diversification than most investors could achieve on their own. ALFM mutual fund offerings by BIMI only require a minimum investment of ₧5,000.

RSP allows clients to nominate a regular contribution amount for their investment account for purchase of units or shares, on a monthly or a quarterly basis, working like forced savings. Aside from delivering affordability, convenience and control, RSP results in higher returns for investors due to cost-averaging. There is no penalty for missing a scheduled contribution.

Since the lowering of minimum investment amount requirements in 2013, there has been a marked increase in our investor count. For the overseas Filipino segment, investors increased by 40% to 6,552 in 2014 from the previous year’s 4,668. Investors from the Personal Banking segment grew by 12%, from 36,836 in 2013 to 41,200 in 2014.

Offering a Wide Array of Investment Options

BPI Unit Investment Trust Funds (UITF)

ALFM Mutual Funds

Regular Subscription Plan (RSP)

BANK OF THE PHILIPPINE ISLANDS 35 2014 SUSTAINABILITY REPORT 34

Being in a country frequently visited by typhoons and other natural calamities, we are taking the lead in instilling the value of protecting one’s assets and managing risks.

BPI/MS Insurance Corporation (BPI/MS) issued a total of 236,791 insurance policies in 2014, serving 132,211 clients. Most clients availed of our motor insurance policy, with 118,840 policies; followed by fire insurance with 78,151; marine insurance with 13,349; and personal accident with 9,679 policies.

Meanwhile, total sums insured for natural catastrophe perils are ₧805.9 billion for earthquakes; ₧824.8 billion for typhoons; and ₧815 billion for floods.

BPI/MS relies on its 12 branches/satellite offices nationwide and the Unibank network to bring our products to the market. Our distribution channels include agencies, brokers, bancassurance, branches, and the Japanese Marketing Division.

Total premiums generated for 2014 amounted to ₧5.23 billion. Of this amount, 59% is attributed to fire insurance, 28% to motor insurance and 13% to the other products.

Across our major product lines, 236,791 insurance policies were availed of by policy holders in 2014. Collectively, motor, fire and marine insurance comprise 89 percent of this total.

Insurance Policy Type

118,840

9,679

78,151

50%

4%

33%

6%

2%

1%

4%

13,349

4,647

1,817

10,308

Motor

Fire

Marine

Personal accident

Other casualty

Engineering

Bonds and other insurance policies

%

Helping Prepare for the Unexpected

Jaime Mayoral

Testimonial

Insurance Agent BPI/MS Insurance

“There is ‘less stress’ in being an agent because you manage your own time, especially so, if you are in the right company with the right products.”

Jimmy is a veteran insurance agent. He is now just 2 years shy of his 25 year engagement withBPI/MS. If a life well-lived means being married for forty-three years, having four children and 13 grandchildren, then accountant Jaime O. Mayoral is living the high-life indeed. Add a winning attitude and great outlook to life; he is among the bank’s best success stories. “At 68, I am still an active BPI/MS Agent. Compared to other businesses, you need capital. You need space. But being an insurance Agent, what you need is knowledge. For us senior citizens, that’s what we have. Experience is the best teacher, and it made us sharp and credible.” There is, according to him “less stress” in being an agent because you manage your own time, especially so, if you are in the right company with the right products. Jimmy also appreciates the high regard that agents like him are given at BPI/MS. He says, “You can feel the warmth and respect that the staff is giving to agents here at BPI/MS, especially to us elderlies. Jimmy enjoys the freedom of not being limited to what his pension brings. He says, “having good products and the right clients, being an agent is more profitable. Ultimately, there are less financial worries. At my age, I am still able to help our relatives in the province of Pagudpud, Ilocos, Norte in their livelihood.” Beyond the endless financial opportunities, selling products that truly helps the clients gives meaning to his work. “I am still an active member of insurance clubs and associations. This helps me become an even more effective agent.” “I will continue being a BPI/MS agent for as long as I could.”

BANK OF THE PHILIPPINE ISLANDS36 37 2014 SUSTAINABILITY REPORT

Let’sfoster financial inclusion

39 2014 SUSTAINABILITY REPORT

Financial inclusion, or the delivery of financial services suited to low-income individuals and households, is a challenge that we at BPI try to address through

our various products, services, and channels.

By making banking more accessible, we help make financial well-being a reality for more Filipinos.

over 200franchise outlets

thriving

14%growth in number

of Easy Saver accounts

32cities covered by enterprise

development program

BANK OF THE PHILIPPINE ISLANDS40 41 2014 SUSTAINABILITY REPORT

Easy SaverAn Easy Saver account may be opened with only ₧200 and a ₧50 ATM card fee, with no maintaining balance required. Only a minimal fee of ₧5 per transaction is charged for BPI ATM withdrawals and debit transactions such as payments via the Express Payment System/POS, ATMs, mobile app, among others.

By 2014, the number of Easy Saver accounts increased by 14% from 2013. These accounts comprise a significant portion of BPI’s depositor base.

Total volume of savings from Easy Saver accounts also grew by 27% from 2013.

Average account size steadily increased by 12% annually from 2012 to 2014. This indicates that Easy Saver is able to serve account holder needs.

These numbers show that given access to affordable deposit products, Filipinos—from all walks of life—are able to gradually build savings through their deposit accounts.

Banking the UnbankedFS7

More than 21 million or 56% of the total employed persons in the country are minimum wage earners (2015 Philippines in Figures, Philippine Statistics Authority). This reality makes it difficult for a lot of Filipinos to save enough to open and maintain a regular bank account. Our Easy Saver deposit product was developed to change this.

Debit CardsAll ATM cards issued by our Bank are debit cards. These cards may be used for cash transactions in lieu of actual cash via Express Payment System (EPS). The amount of a purchase is deducted from the account’s available balance. In support of BSP’s thrust of reducing the circulation of cash and coins, the Bank provides incentives to its customers who use the EPS through a rebate or reward. This gives risk-averse and practical customers a seamless way to pay for everyday needs.

Prepaid CardsOur prepaid cards provide an efficient way for those without regular BPI savings accounts to manage their finances. They allow the cardholder to pay for purchases and services with a pre-deposited balance, which when

used up may be replenished as desired by the cardholder.

This is the entry-level product for individuals that may have specific needs or may not yet have the credit history like the young and underbanked individuals.

As prepaid card holders become more comfortable with cashless transactions, they eventually signed up for our other products. Over the last two years, about 30,000 prepaid card holders opened deposit accounts with us. Pantawid Pasada Prepaid Cards This prepaid card variant, launched for the Department of Energy, is aimed at helping drivers of public utility jeepneys (PUJ) cushion the impact of high fuel prices. PUJ drivers may present their Pantawid Pasada prepaid cards in retail gasoline stations in order to avail of government fuel subsidies.

When loaded with money through BPI’s ExpressLink real-time funds transfer system, the cards may be used at most of the retail gasoline stations nationwide.

The use of prepaid cards reduces operational cost and relevant carbon footprint of the Bank from the management of ATMs as well as the risk to theft at ATM centers.

Our debit and prepaid cards play significant roles in helping individuals previously unfamiliar with banking and financial transactions. These provide simple, convenient and secure payment options.

Providing Payment Solutions

Year-on-Year Growth in Savings Volume of Easy Saver

2012 2013 2014

69%

27%

Year-on-Year Growth in number of Easy Saver Accounts

2012 2013 2014

51%

14%

Year-on-Year Growth in Average Savings per Account

2012 2013 2014

12%12%

BANK OF THE PHILIPPINE ISLANDS42 43 2014 SUSTAINABILITY REPORT

Making Loans AccessibleFS7

Many Filipinos are hard-pressed to achieve financial stability and security for lack of funds and access to financial services. By providing easy access to loans, the Bank is making good progress in improving this situation.

BPI Housing Loans

We continually support events and gatherings that provide the public with information on property financing through various means.

We actively support the conduct of housing fairs, usually in consumer frequented areas like malls. By participating in these fairs, we reach prospective homebuyers. Aside from being able to educate the public we are able to receive and process loan applications on the spot. This way, we reach our market more efficiently. This resulted in increase in housing loan applications.

We hold investment talks to deepen relationships and nurture goodwill with our clients. In these talks, we share real estate trends and updates and enrich knowledge on housing loan products to improve understanding of market opportunities.

The Bank encourages community and individual growth of real estate brokers by widening the range of our accreditation and compensation programs for bona fide members of broker communities.

We also reward successful loan referrals by accredited brokers with corresponding incentives through our Brokers Circle Incentive Program. This scheme aims to inspire more brokers into our roster. This has resulted increases in loan referrals and actual real estate loan transactions.

BPI Ka-Negosyo

A good number of Filipinos who plan to start a business are unable to do so for lack of confidence or financial capability. We help them overcome these obstacles by providing financing assistance to both existing and start-up Filipino entrepreneurs through our BPI Family Ka-Negosyo loans. Short-term, long-term, or franchising loans serve to bridge capital requirements suited to different types of businesses.

We make investing in a business more interesting and appealing through social media posts and online community fora. Through these channels, we promote positive and educational conversations around business strategies, business growth and financial wellness, among others.

To educate would-be entrepreneurs, our Ka-Negosyo team regularly conducts investment seminars, training sessions, and solutions presentations.

Ka-Negosyo fosters partnerships with various business organizations such as the Philippine Franchise Association, Association of Filipino Franchisers Inc. and Go Negosyo who share our goal of helping entrepreneurs and business start-ups. We also conduct roadshows where we present our “Ka-Negosyo Best List,” a short list of franchise

brands vetted by BPI for business soundness. This allows for intelligent and less risky choices by our Ka-Negosyo loan clients.

We further alleviate overwhelming concerns of starting-up a business through extended payment terms.

We deliver this product through a 182-strong BPI Ka-Negosyo staff across 813 bank branches and 10 provincial centers nationwide.

In 2014, we conducted four major roadshow events in Metro Manila and six in the provinces, contributing to 14% growth in number of accounts.

BANK OF THE PHILIPPINE ISLANDS44 45 2014 SUSTAINABILITY REPORT

From Fruits to Franchise

Cheysserlyn Ting always had a passion for entrepreneurship. Her parents made a decent living from selling fruits and vegetables in Cauayan, Isabela. Now, at 26 years old, her passion compelled Cheysserlyn and her husband to set up their own business franchise of Daddy’s Toasted Siopao.

Through BPI Ka-Negosyo, managing the franchise became easier. “We didn’t have a hard time contacting them – the internet made them easy to reach via their website. They lent us our

start-up capital and once we started discussing terms and conditions, the Ka-Negosyo team was very helpful and encouraging.” she states.

It has only been two months but Cheysserlyn and her husband are enjoying their experiences in franchising. “I also believe we made the right decision in starting young. My family and I can enjoy our financial independence this early and create a self-sustaining means for our security as we grow older.”

Marlowe and Roselle Mendoza

Testimonials

Restaurant Success

Since getting married in 2006, Marlowe and Roselle Mendoza have dreamt of putting up their own restaurant. While both worked hard, capital was their main challenge.

The Mendozas found a reliable partner for their initial enterprise with BPI Family Savings Bank’s Ka-Negosyo Business Loans. “The Ka-Negosyo team really helped us a lot. They knew what we needed, allowed us to negotiate, and they were also motivated to help us succeed.”

Their first business funded by Ka-Negosyo was Red Engine Diner in Makati. Over the years, the Mendozas built other dining places such as Hermana, and The Recados - all possible through Ka-Negosyo.

“We are so grateful to have found one in BPI Family Ka-Negosyo. For middle-class people like us who were not born with a silver spoon, cashing in on an opportunity when it presents itself is priceless”, Roselle exclaimed.

“BPI knew what we needed, allowed us to negotiate, and they were also motivated to help us succeed.”

Cheysserlyn Ting

“We made the right decision in starting young.”

EntrepreneurDaddy’s Toasted Siopao

Restaurateurs Red Engine Diner, Hermana, The Recados

BANK OF THE PHILIPPINE ISLANDS46 47 2014 SUSTAINABILITY REPORT

Insuring Your Future

BPI/MS in cooperation with BPI Globe BanKO helps those in the lower income segment by providing innovative and affordable micro-insurance products and taking on the transfer of risks for their protection.

BPI/MS Bahay at Buhay product complements with microfinance loans which improve our clients’ social standing. We support and empower our clients’ financial independence by creating opportunities that allow them to continue to generate income.

PaniguroKO gives the account holder access to a non-life insurance policy that costs only ₧365 for a one-year coverage.

Educating Emerging Entrepreneurs

Sharing Financial Growth with Employees

Through the initial public offerings (IPOs) services of BPI Capital Corporation, we influence our clients to allocate stocks for their employees. This affords the employees the financial benefits gained as the company goes public.

In 2014, we have enabled around 300 employees to avail of the opportunity to invest in the company they work hard for. This allows companies to share their potential to create wealth with their employees.

BPI promotes entrepreneurship and empowers aspiring entrepreneurs as catalysts of positive change in communities.

Our Show Me, Teach Me, MSME program, in partnership with the Department of Trade and Industry’s Philippine Trade Training Center (PTTC), teaches emerging entrepreneurs basic skills that prepare them to develop better products matched to market needs.

Food packaging, labeling and product design enhancement, and assessment for the non-food sector were among the topics covered in 2014.

The program has covered 32 cities and has trained 1,526 MSMEs since 2010, making our local products more competitive.

Guiding Young Minds

The Bank believes in the Filipino youth and in the integrity of their ingenious ideas. We encourage idea innovation among our country’s brightest students who lack the groundwork for future business development.

The BPI-DOST Science Awards provides an avenue to present sound concepts having strong potential to be realized as actual science and technology-based businesses now or in future; or help advance current technologies for adoption to businesses thereby enhancing livelihood.

Counting among the most respected of local national student awards in the country, excellence in research and application in the fields of biology, chemistry, computer science, engineering, mathematics, and physics is duly recognized and rewarded. This annual program has been on-going for 25 years and is run with the Department of Science and Technology.

BANK OF THE PHILIPPINE ISLANDS48 49 2014 SUSTAINABILITY REPORT

Let’s invest in sustainable development

51 2014 SUSTAINABILITY REPORT

A big part of our success over the years may be attributed to a conscious effort to foster sustainable growth, anchored on countryside development and sustainable

energy. We are committed to financing projects that help build more vibrant, modern and low-carbon communities.

The co-dependence of the countryside and urban areas is important to achieving significant national economic growth. The 6.1% growth in Gross Domestic Product (GDP) in 2014 is mainly contributed by growth in the countryside–at 4% (2014 Gross Regional Domestic Product Highlights, National Statistical Coordination Board). Recognizing this, we strengthened our focus in enabling investments beyond the National Capital Region (NCR).

At BPI, we make sure that the growth we enable is sustainable and inclusive.

506Bpesos worth of loans for projects in Metro Manila

1,058 GWh RE generated

94Bpesos invested in

countryside development(Corporate Clients)

97Bpesos invested in various

development projects (BPI Capital)

257Bpesos raised for various development projects

(BPI Capital)

234 GWh saved from EE

projects

BANK OF THE PHILIPPINE ISLANDS 53 2014 SUSTAINABILITY REPORT 52

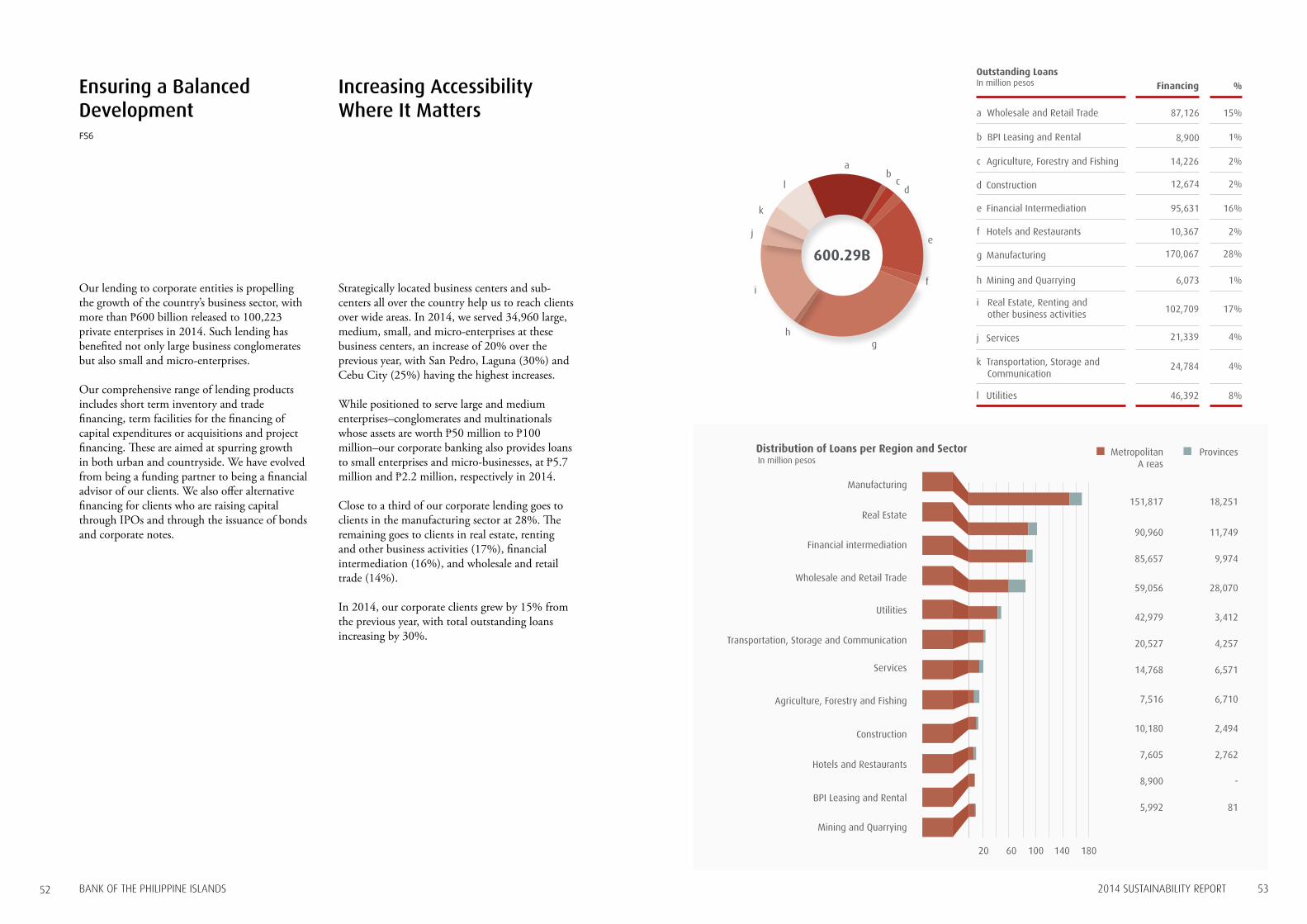

Our lending to corporate entities is propelling the growth of the country’s business sector, with more than ₧600 billion released to 100,223 private enterprises in 2014. Such lending has benefited not only large business conglomerates but also small and micro-enterprises.

Our comprehensive range of lending products includes short term inventory and trade financing, term facilities for the financing of capital expenditures or acquisitions and project financing. These are aimed at spurring growth in both urban and countryside. We have evolved from being a funding partner to being a financial advisor of our clients. We also offer alternative financing for clients who are raising capital through IPOs and through the issuance of bonds and corporate notes.

Strategically located business centers and sub-centers all over the country help us to reach clients over wide areas. In 2014, we served 34,960 large, medium, small, and micro-enterprises at these business centers, an increase of 20% over the previous year, with San Pedro, Laguna (30%) and Cebu City (25%) having the highest increases.

While positioned to serve large and medium enterprises–conglomerates and multinationals whose assets are worth ₧50 million to ₧100 million–our corporate banking also provides loans to small enterprises and micro-businesses, at ₧5.7 million and ₧2.2 million, respectively in 2014.

Close to a third of our corporate lending goes to clients in the manufacturing sector at 28%. The remaining goes to clients in real estate, renting and other business activities (17%), financial intermediation (16%), and wholesale and retail trade (14%).

In 2014, our corporate clients grew by 15% from the previous year, with total outstanding loans increasing by 30%.

Ensuring a Balanced DevelopmentFS6

Increasing Accessibility Where It Matters

Distribution of Loans per Region and SectorIn million pesos

20 14010060 180

Manufacturing

Real Estate

Financial intermediation

Hotels and Restaurants

Construction

Agriculture, Forestry and Fishing

Services

Transportation, Storage and Communication

Utilities

Wholesale and Retail Trade

Mining and Quarrying

BPI Leasing and Rental

Outstanding LoansIn million pesos

15%

2%

87,126

12,674

Financing %

1%

16%

1%

8,900

95,631

6,073

2%

2%

17%

28%

4%

4%

8%

14,226

10,367

102,709

170,067

21,339

24,784

46,392

a Wholesale and Retail Trade

b BPI Leasing and Rental

c Agriculture, Forestry and Fishing

d Construction

e Financial Intermediation

h Mining and Quarrying

f Hotels and Restaurants

i Real Estate, Renting and other business activities

g Manufacturing

j Services

k Transportation, Storage and Communication

l Utilities

ab

cd

e

f

gh

i

j

k

l

600.29B

ProvincesMetropolitan A reas

151,817 18,251

90,960 11,749

85,657 9,974

14,768

7,605

6,571

2,762

59,056 28,070

7,516

8,900

10,180

5,992

6,710

-

2,494

81

42,979 3,412

20,527 4,257

BANK OF THE PHILIPPINE ISLANDS54 55 2014 SUSTAINABILITY REPORT

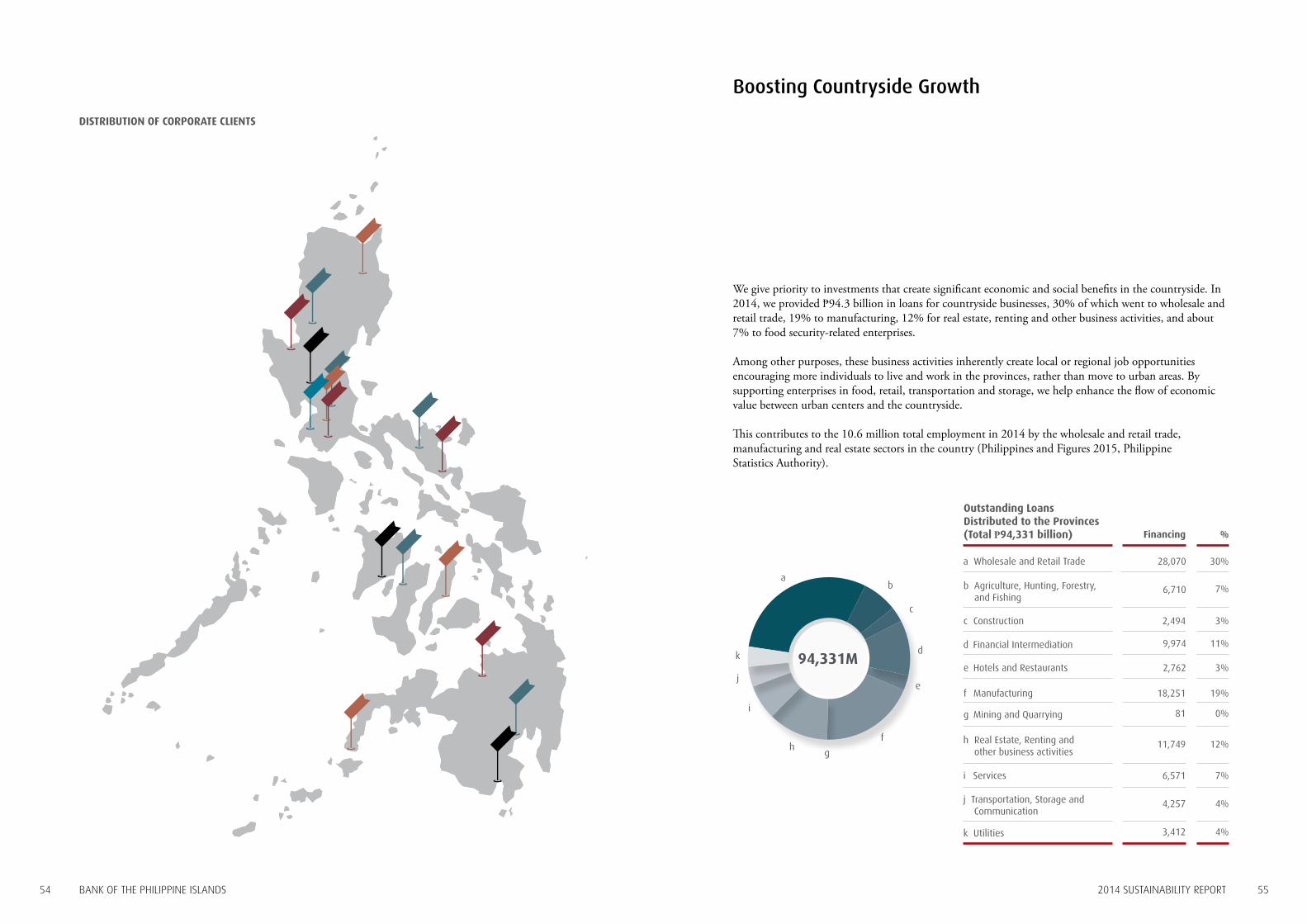

DISTRIBUTION OF CORPORATE CLIENTS

We give priority to investments that create significant economic and social benefits in the countryside. In 2014, we provided ₧94.3 billion in loans for countryside businesses, 30% of which went to wholesale and retail trade, 19% to manufacturing, 12% for real estate, renting and other business activities, and about 7% to food security-related enterprises.

Among other purposes, these business activities inherently create local or regional job opportunities encouraging more individuals to live and work in the provinces, rather than move to urban areas. By supporting enterprises in food, retail, transportation and storage, we help enhance the flow of economic value between urban centers and the countryside.

This contributes to the 10.6 million total employment in 2014 by the wholesale and retail trade, manufacturing and real estate sectors in the country (Philippines and Figures 2015, Philippine Statistics Authority).

Boosting Countryside Growth

Outstanding Loans Distributed to the Provinces (Total ₧94,331 billion)

30%

11%

28,070

9,974

Financing %

7%

3%

6,710

2,762

3%

19%

12%

0%

7%

4%

4%

2,494

18,251

11,749

81

6,571

4,257

3,412

a Wholesale and Retail Trade

b Agriculture, Hunting, Forestry, and Fishing

c Construction

d Financial Intermediation

e Hotels and Restaurants

f Manufacturing

h Real Estate, Renting and other business activities

g Mining and Quarrying

i Services

j Transportation, Storage and Communication

k Utilities

ab

c

d

e

f

gh

i

j

k 94,331M

BANK OF THE PHILIPPINE ISLANDS 57 2014 SUSTAINABILITY REPORT 56

BPI has been lending to the agribusiness sector for more than 30 years now. Recognizing our potential to create positive social and economic impact, we launched Agribusiness Solutions in March 2013, an enhanced lending program for the use of state-of-the-art technology in piggery and poultry sector operations. Other types of loan products include investments for agricultural crops and post-harvest operations such as rice mill, dressing plant, meat processing plant, slaughter house, cold storage, and feed mills, among others.

In 2014, the loans provided through these products help boost job creation and food production in the rural areas. A portion of these loans were channeled through rural banks with loan portfolios for agriculture and agrarian reform. Majority was released directly to individual borrowers and corporate clients. Two cooperatives, a federation of onion growers in Nueva Ecija and a sugar cooperative in Batangas, also availed of the lending facility.

The loan proceeds invested into piggery and poultry projects result in healthier animals, better productivity and better feed conversion ratio. Through these projects, piggery operators typically recover their investment in eight to nine years; poultry operators, five to six years. The proceeds were also invested in biodigesters for production of biogas fuel from animal wastes, saving for the farmers around 65% in electricity cost while significantly reducing their greenhouse gas (GHG) emissions.

The success of Agribusiness Solutions in 2014 was a result of aggressive marketing and promotional activities by a team of five product managers and three technical staff. Aside from undertaking advertising campaigns, Agribusiness Solutions participates in conventions and exhibits for this sector, like the National Hog Convention, Inahgen and Agrilink. It also holds technical fora and product briefings. In 2014, such briefings were conducted in 10 of our business centers namely Dagupan, San Fernando, Bulacan, Laguna, Batangas in Luzon; Bacolod, Iloilo and Cebu in the Visayas; and Davao and Cagayan de Oro in Mindanao.

Advancing the Agribusiness Sector

Financing Smallholder Farmers

Feature

BPI provided a loan to onion farmers’ cooperative, KASAMNE or Katipunan ng mga Samahang Magsisibuyas ng Nueva Ecija.

KASAMNE was organized and registered in 1989 at the Bureau of Agricultural Cooperative and confirmed by Cooperative Development Authority in 1991. It has a membership of about 450 onion producers and farmers from 17 cooperatives in the towns of Bongabon, Palayan, Laur, Gabaldon, Rizal, Gen. Natividad, Pantabangan and Palayan, and San Jose City of Nueva Ecija province.

The cooperative exists to help regulate onion prices year-round, protecting farmers from low prices during harvest season and local consumers from price hike during off seasons. It also helps farmers earn sufficient income throughout the year.

Extending the shelf life of the produce is key to keeping competitive prices. KASAMNE farmers turned to BPI to help them address this challenge.

With financing from BPI, onion growers were able to acquire and operate a cold storage facility. A portion of loan proceeds were also used as working capital of a farm input trading business. Now, the cooperative generates 95% of its revenues from storage fees and profits from sales of farm inputs.

KASAMNE produces 6,463 metric tons (or 235,000 50-kg bags) of onions a year, accounting for at least 5% of the country’s total onion production.

BANK OF THE PHILIPPINE ISLANDS58 59 2014 SUSTAINABILITY REPORT

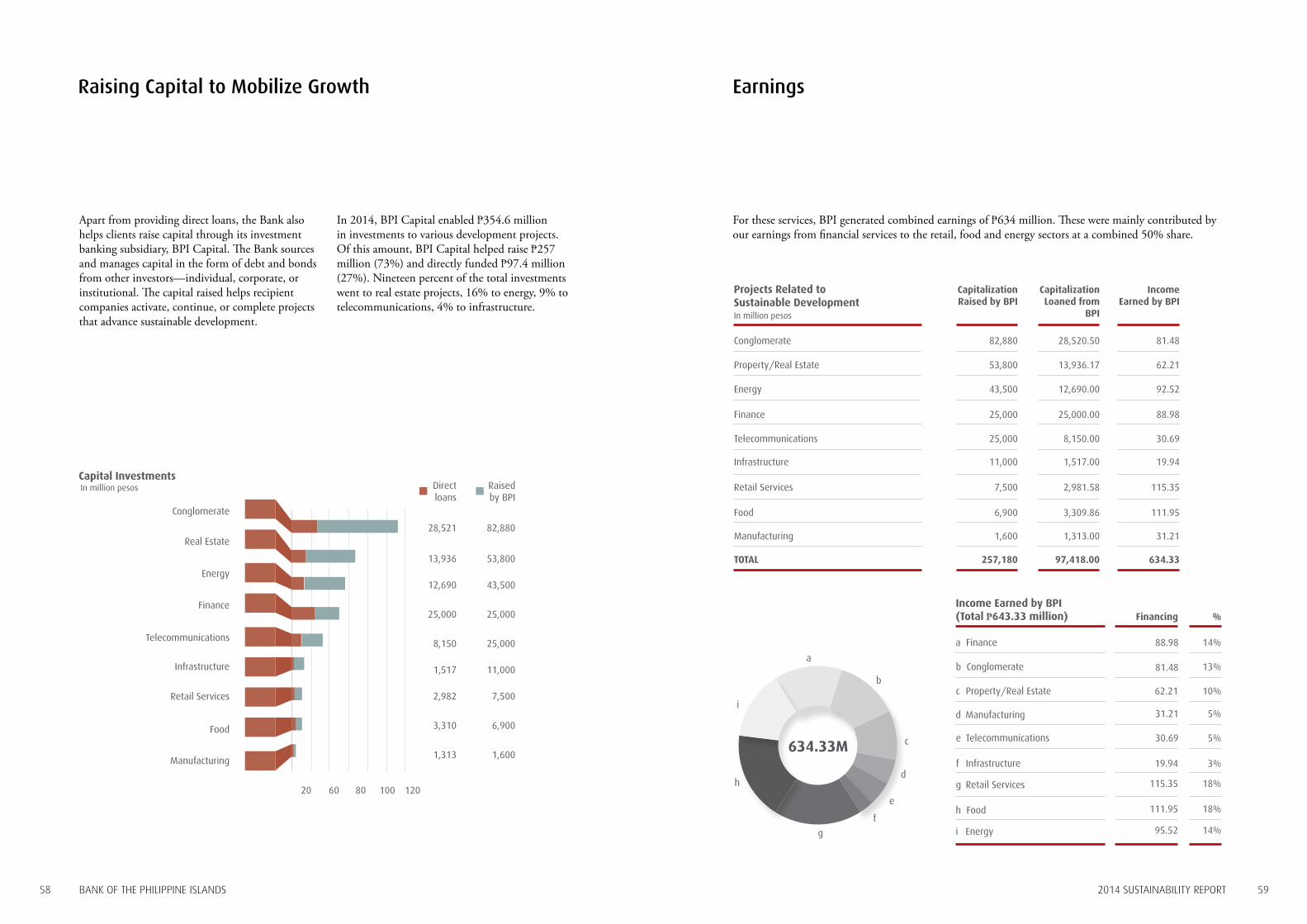

Apart from providing direct loans, the Bank also helps clients raise capital through its investment banking subsidiary, BPI Capital. The Bank sources and manages capital in the form of debt and bonds from other investors—individual, corporate, or institutional. The capital raised helps recipient companies activate, continue, or complete projects that advance sustainable development.

In 2014, BPI Capital enabled ₧354.6 million in investments to various development projects. Of this amount, BPI Capital helped raise ₧257 million (73%) and directly funded ₧97.4 million (27%). Nineteen percent of the total investments went to real estate projects, 16% to energy, 9% to telecommunications, 4% to infrastructure.

Raising Capital to Mobilize Growth

Capital InvestmentsIn million pesos Raised

by BPIDirect loans

20 10060

Conglomerate

Real Estate

Energy

Manufacturing

Food

Retail Services

Infrastructure

Telecommunications

Finance

28,521 82,880

13,936 53,800

12,690 43,500

2,982 7,500

25,000 25,000

3,310 6,900

8,150 25,000

1,313 1,600

1,517 11,000

12080

For these services, BPI generated combined earnings of ₧634 million. These were mainly contributed by our earnings from financial services to the retail, food and energy sectors at a combined 50% share.

Earnings

In million pesos

Projects Related to Sustainable Development

Conglomerate 28,520.50

Capitalization Loaned from

BPI

82,880

Capitalization Raised by BPI

81.48

Income Earned by BPI

Property/Real Estate 53,800 13,936.17 62.21

Energy

Infrastructure

Finance

Retail Services

Telecommunications

Food

Manufacturing

TOTAL

43,500

11,000

25,000

7,500

25,000

6,900

1,600

257,180

12,690.00

1,517.00

25,000.00

2,981.58

8,150.00

3,309.86

1,313.00

97,418.00

92.52

19.94

88.98

115.35

30.69

111.95

31.21

634.33

a

b

c

d

e

f

g

h

i

634.33M

Income Earned by BPI (Total ₧643.33 million)

14%

5%

88.98

31.21

Financing %

13%

5%

81.48

30.69

10%

3%

18%

18%

14%

62.21

19.94

111.95

115.35

95.52

a Finance

b Conglomerate

c Property/Real Estate

d Manufacturing

e Telecommunications

f Infrastructure

h Food

g Retail Services

i Energy

BANK OF THE PHILIPPINE ISLANDS60 61 2014 SUSTAINABILITY REPORT

Strengthening Business Resiliency

Since business resilience is vital to continuing countryside development, the Bank has partnered with the World Wildlife Fund for Nature-Philippines for conducting studies that measure the climate vulnerability of major cities in the Philippines outside of Metro Manila.

Entitled “Business Risk Assessment and the Management of Climate Change Impacts,” a total of sixteen cities to date have been assessed. The study ensures that climate change impacts

are correctly considered and industry players, including businesses, are able to make informed assessments of climate change impacts and realistically plan their sustainability strategies.

Research has so far covered Laoag, Baguio, Dagupan, Santiago, Angeles, Batangas, Naga, and Puerto Princesa in Luzon; Cebu, Iloilo and Tacloban in the Visayas; and Cagayan de Oro, Butuan, Davao, General Santos, and Zamboanga in Mindanao.

Raising Capital for a Food Manufacturer

BPI served as joint issue manager, lead underwriter and bookrunner for Century Pacific Food Inc. (CPFI), when it went public in May 2014. CPFI is the recognized market leader in canned fish, canned meat and milk products and the pioneer of the country’s tuna export business.

CPFI’s initial public offering (IPO) in May 2014 garnered an overwhelming response both from institutional and retail investors. It was more than 3.5 times oversubscribed. The initial offer was 229,654,404 shares for a total offer size of ₧3.16 billion. Following the strong investor demand, the IPO price settled at ₧13.75 per share, on the high end of the ₧12.50-14.50 per share price range. BPI successfully executed the transaction within four months.

On its first trading day, CPFI reached a peak of ₧16.04 and closed at ₧15.20, up 10.55% from the IPO price. Trading volume was at 60.8 million shares or about 26% of the outstanding shares issued.

The IPO’s proceeds will be used for CPFI’s capital expenditure, working capital, potential acquisitions, and debt repayment. The IPO is a prime example of how BPI’s support to the business sector stimulates growth in the economy, creates employment and eventually impacts the community. The partnership of CPFI and BPI Capital highlights their common values of management excellence, corporate social responsibility and openness to innovations.

Feature

62 63 2014 SUSTAINABILITY REPORT

In the Philippines, power generation is the biggest source of carbon emissions. Yet, according to the Department of Energy (DOE), our country has about 250,000 MW of untapped renewable energy (RE) capacity (National Renewable Energy Board Presentation on RA9513, Renewable Energy Management Bureau - DOE).

BPI contributes to tapping this RE potential capacity through the development of products and solutions that encourage investments in sustainable energy. BPI’s partnership with World Bank affiliate, International Finance Corporation (IFC) enabled the bank to get more deeply immersed in sustainable energy such as renewable energy, energy efficiency, and climate finance.

Through BPI’s Sustainable Energy Finance (SEF) Program, companies can invest in new technologies aimed at improving the efficiency of energy generation, distribution and use, and thereby cutting costs. SEF-financed projects have also significantly contributed to the bank’s finance portfolio.

We measure the impact of our various sustainable energy finance projects using three indicators:

• financial value - our business returns expressed in terms of loan amounts;

• socio-economic value - the value our clients generate as a result of the financial services we provide; and

• environmental value - the total reduction in carbon emissions as a result of these projects.

From 2010 to end-2014, BPI approved loans for 174 projects, amounting to ₧27.53 billion. Of this amount, 58% financed 110 energy efficiency projects, 34% funded 51 renewable energy projects, and the 8% funded 13 projects relating to building resilience in agriculture and water supply. By end-2014, a total of ₧22.8B SEF loans have been released. These projects are seen to generate 1,058 GWh of renewable power and save 234 GWh of electricity valued at ₧3.5 billion in annual financial benefit to our clients, preventing 813.5 thousand tonnes of carbon emissions from being emitted every year throughout the project life.

Making Headways into Low-Carbon Economy FS8

MAJOR SUSTAINABLE ENERGY FINANCING PROJECTS

₧2.9BWind

₧0.9B Geothermal

₧1.6BMini-hydro

₧2.3BConstruction of resilient poultry facilities

₧1.8BSolar

₧1.5BBiogas

₧0.7BBiomass

₧15.8BEnergy efficiency in buildings and in manufacturing

Climate Resilience

Renewable Energy

Energy Efficiency

Sustainable Energy Financing

₧9.3B34%

₧15.9B58%

₧2.3B8%

27.5B

Renewable Energy Produced and Power Saved (GWh)

1,058 82%

23418%

1,292 GWh

Annual Financial Savings

₧2.59B74%

₧0.90B26%

₧3.5B

GHG Avoidance (thousand tCO2e)

73791%

769%

813

* Total SEF loans released as of end-2014 reached P22.8B funding 174 projects.

BANK OF THE PHILIPPINE ISLANDS64 65 2014 SUSTAINABILITY REPORT

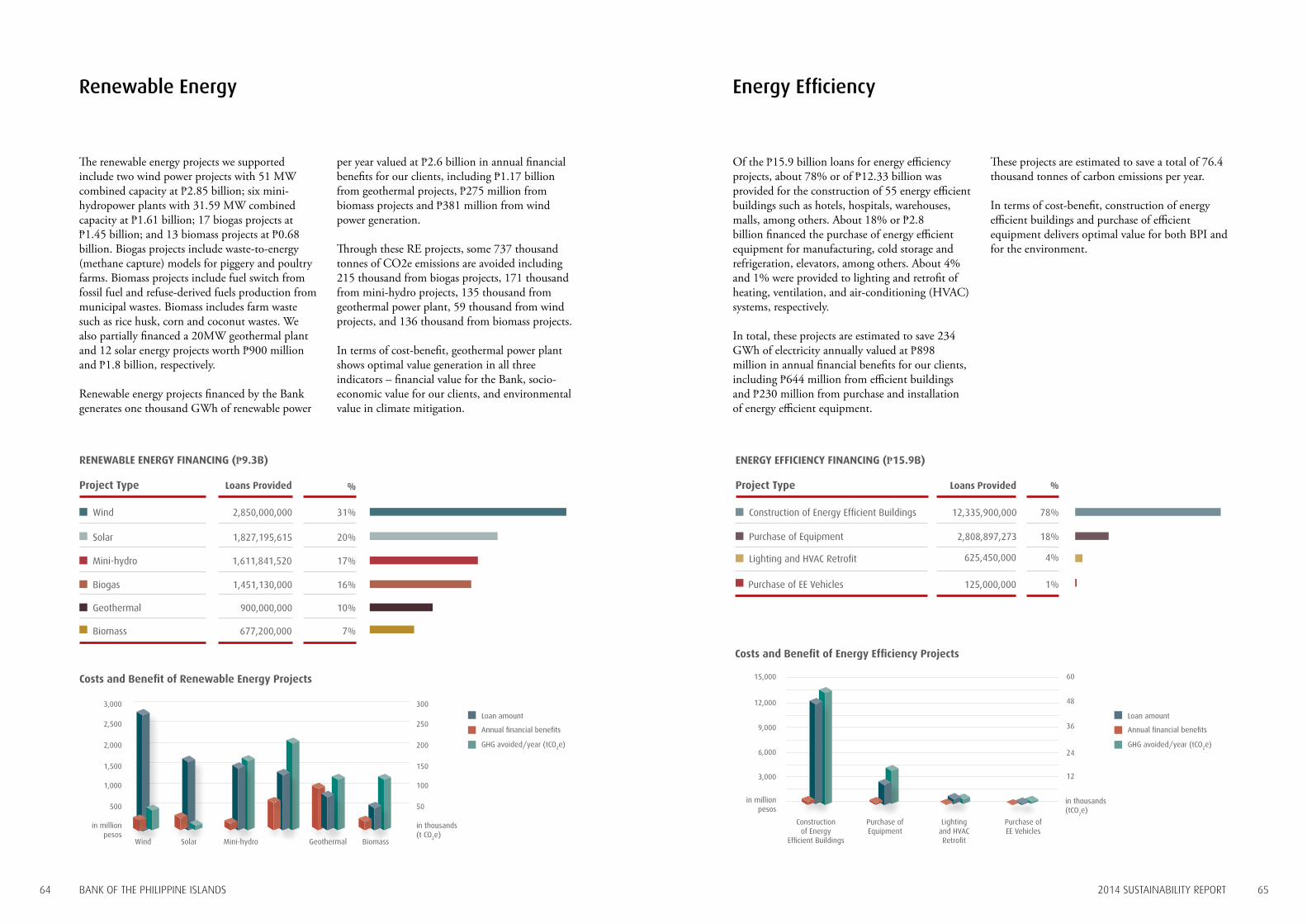

The renewable energy projects we supported include two wind power projects with 51 MW combined capacity at ₧2.85 billion; six mini-hydropower plants with 31.59 MW combined capacity at ₧1.61 billion; 17 biogas projects at ₧1.45 billion; and 13 biomass projects at ₧0.68 billion. Biogas projects include waste-to-energy (methane capture) models for piggery and poultry farms. Biomass projects include fuel switch from fossil fuel and refuse-derived fuels production from municipal wastes. Biomass includes farm waste such as rice husk, corn and coconut wastes. We also partially financed a 20MW geothermal plant and 12 solar energy projects worth ₧900 million and ₧1.8 billion, respectively.

Renewable energy projects financed by the Bank generates one thousand GWh of renewable power

per year valued at ₧2.6 billion in annual financial benefits for our clients, including ₧1.17 billion from geothermal projects, ₧275 million from biomass projects and ₧381 million from wind power generation.

Through these RE projects, some 737 thousand tonnes of CO2e emissions are avoided including 215 thousand from biogas projects, 171 thousand from mini-hydro projects, 135 thousand from geothermal power plant, 59 thousand from wind projects, and 136 thousand from biomass projects.

In terms of cost-benefit, geothermal power plant shows optimal value generation in all three indicators – financial value for the Bank, socio-economic value for our clients, and environmental value in climate mitigation.

Renewable Energy