lesson 13-1 recording a payroll · lesson 13-1 recording a payroll. ... payroll taxes page 376...

TRANSCRIPT

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 13-1

Recording A Payroll

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

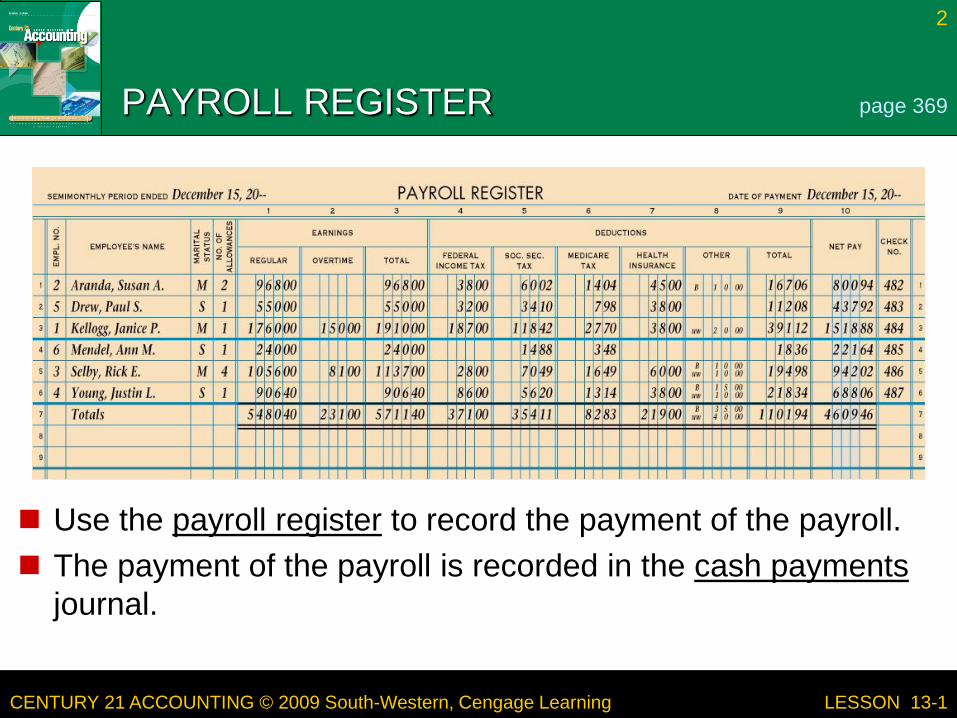

PAYROLL REGISTER

Use the payroll register to record the payment of the payroll. The payment of the payroll is recorded in the cash payments

journal.

2

LESSON 13-1

page 369

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

3

LESSON 13-1

ANALYZING PAYMENT OF A PAYROLL page 370

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

4

LESSON 13-1

6. Write the titles of accounts credited.

JOURNALIZING PAYMENT OF A PAYROLL

12

3 4 5

6

page 371

December 15. Paid cash for payroll, $4,609.46. Check No. 335.

71. Write the date.2. Write the title of the account

debited.3. Write the check number.4. Write the account debited. 7. Write the amounts credited.

5. Write the total amount paid to employees.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

JOURNALIZING PAYMENT OF A PAYROLL

The payroll is an Expense to the company The taxes and other deductions that were deducted from

the employees’ earnings and still owed to the government or other agencies are Liabilities.

Cash is also credited because money was paid out.

5

LESSON 13-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

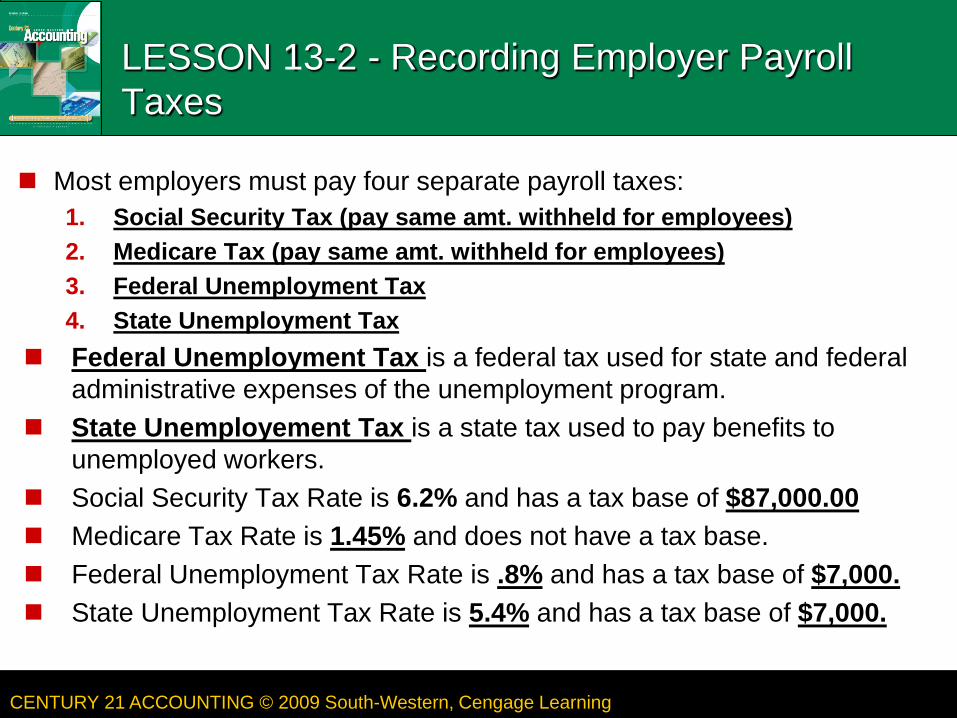

LESSON 13-2 - Recording Employer Payroll Taxes

Most employers must pay four separate payroll taxes:1. Social Security Tax (pay same amt. withheld for employees)2. Medicare Tax (pay same amt. withheld for employees)3. Federal Unemployment Tax4. State Unemployment Tax

Federal Unemployment Tax is a federal tax used for state and federal administrative expenses of the unemployment program.

State Unemployement Tax is a state tax used to pay benefits to unemployed workers.

Social Security Tax Rate is 6.2% and has a tax base of $87,000.00 Medicare Tax Rate is 1.45% and does not have a tax base. Federal Unemployment Tax Rate is .8% and has a tax base of $7,000. State Unemployment Tax Rate is 5.4% and has a tax base of $7,000.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

7

LESSON 13-2

UNEMPLOYMENT TAXABLE EARNINGS

2

3

page 374

11. Enter accumulated earnings and total earnings for each employee.2. Enter unemployment taxable earnings. 3. Total the Unemployment Taxable Earnings column.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

8

LESSON 13-2

UNEMPLOYMENT TAXES page 375

FederalUnemployment

Tax=

FederalUnemployment

Tax Rate×

UnemploymentTaxableEarnings

$6.32=0.8%×$790.00

StateUnemployment

Tax=

StateUnemployment

Tax Rate×

UnemploymentTaxableEarnings

$42.66=5.4%×$790.00

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

JOURNALIZING EMPLOYER PAYROLL TAXES

The employer’s taxes are Liabilities and are recorded in the General Journal until they are paid.

9

LESSON 13-2

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

10

LESSON 13-2

JOURNALIZING EMPLOYER PAYROLL TAXES page 376

December 15. Recorded employer payroll taxes expense, $485.92, for the semimonthly pay period ended December 15. Taxes owed are: social security tax, $354.11; Medicare tax, $82.83; federal unemployment tax, $6.32; state employment tax, $42.66. Memorandum No. 63.

(continued on next slide)

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

11

LESSON 13-2

JOURNALIZING EMPLOYER PAYROLL TAXES

12

3

5

4

6

page 376

4. Write the debit amount.1. Write the date.5. Write the titles of the liability

accounts credited.2. Write the title of the expense

account debited.6. Write the credit amounts.3. Write the memorandum number.

(continued from previous slide)

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

12

LESSON 13-2

TERMS REVIEW

federal unemployment tax state unemployment tax

page 377

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 13-3 - Reporting Withholding And Payroll Taxes

Employers are required to furnish Form W-2 to each employee by January 31 of the next year.

Employers must report the payroll taxes withheld from employee salaries and the employer payroll taxes due to the government by preparing the Employer’s Quarterly Federal Tax Return, Form 941.

Form W-3, Transmittal of Wage and Tax Statements, is sent to the Social Security Administration by February 28th each year to report the previous year’s earning and payroll taxes withheld for all employees. A copy of each employee’s W-2 must be attached to the W-3 form.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

14

LESSON 13-3

EMPLOYER ANNUAL REPORT TO EMPLOYEES OF TAXES WITHHELD page 378

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

15

LESSON 13-3

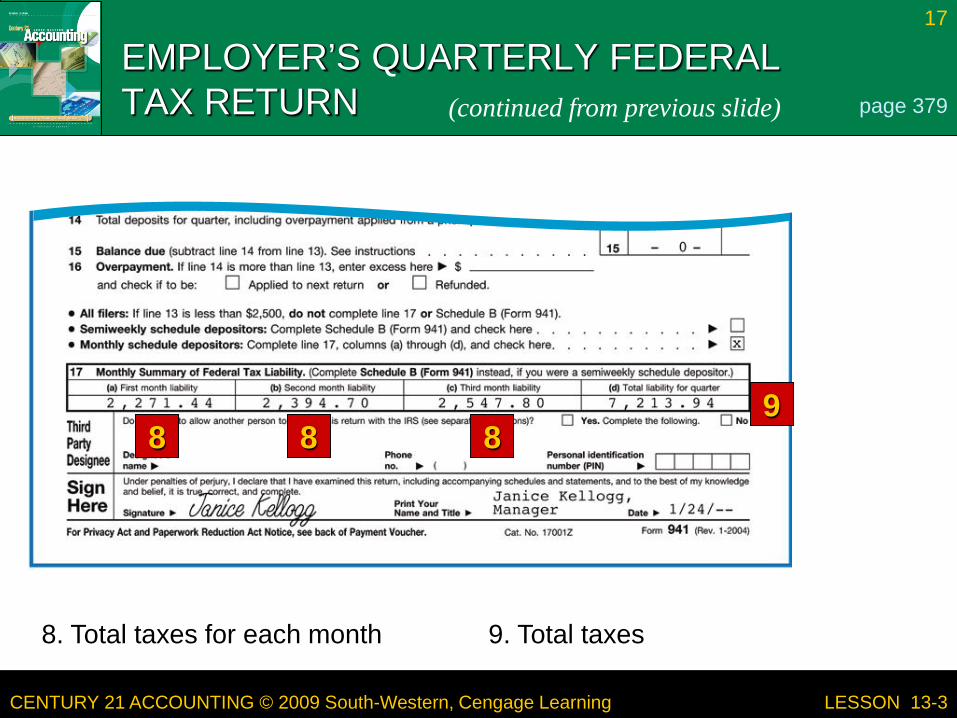

EMPLOYER’S QUARTERLY FEDERAL TAX RETURN page 379(continued on next slide)

1

2

1. Heading 2. Number of employees

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

16

LESSON 13-3

EMPLOYER’S QUARTERLY FEDERAL TAX RETURN page 379(continued on next slide)

3. Total quarterly earnings4. Income tax withheld5. Employee and employer social

security and Medicare taxes 7. Total taxes

6. Social security plus Medicare taxes

4

5

3

6

7

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

17

LESSON 13-3

EMPLOYER’S QUARTERLY FEDERAL TAX RETURN page 379(continued from previous slide)

8 8 89

8. Total taxes for each month 9. Total taxes

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

18

LESSON 13-3

EMPLOYER ANNUAL REPORTING OF PAYROLL TAXES page 381

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 13-4 - Paying Withholding and Payroll Taxes

The payment of payroll taxes to the government is referred to as a deposit.

How often the business has to make a deposit depends on how much taxes the business collected during the current deposit period and depends on the amount of payroll taxes owed during the prior 12-month period. The 12-month period that ends on June 30th of the prior year is called

the lookback period.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

20

LESSON 13-4

PAYING THE LIABILITY FOR EMPLOYEE INCOME TAX, SOCIAL SECURITY TAX, AND MEDICARE TAX page 383

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Form 8109, Federal Deposit Coupon

New employers are monthly schedule depositors for the first calendar year of business

IRS issues a monthly Form 8109 coupon book to new employers Employers will reevaluate when the deposit once a lookback period is

established Deposits can be made using the EFTPS (Electronic Federal

Tax Payment System) – businesses having deposits of more than $200,000 during the past calendar year must use this system

21

LESSON 13-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

22

LESSON 13-4

FORM 8109, FEDERAL DEPOSIT COUPON page 384

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

23

LESSON 13-4

JOURNALIZING PAYMENT OF LIABILITY FOR EMPLOYEE INCOME TAX, SOCIAL SECURITY TAX, AND MEDICARE TAX

1

23

45

page 385

January 15. Paid cash for liability for employee income tax, $757.00; social security tax, $1,451.38; and Medicare tax, $339.42; total, $2,547.80. Check No. 347.

1. Write the date.2. Write the titles of the three

accounts debited.

3. Write the check number.4. Write the debit amounts.5. Write the amount of the credit.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

PAYING THE LIABILITY FOR FEDERAL UNEMPLOYMENT TAX

Federal unemployment insurance is paid by the end of the month following each quarter if the liability amount is more than $100; anything outstanding is paid at year end.

24

LESSON 13-4

page 386

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

25

LESSON 13-4

JOURNALIZING PAYMENT OF LIABILITY FOR FEDERAL UNEMPLOYMENT TAX

1 2 3 4 5

page 387

January 31. Paid cash for federal unemployment tax liability for quarter ended December 31, $34.60. Check No. 367.

1. Write the date.

5. Write the amount of the credit to Cash.4. Write the debit amount.3. Write the check number.2. Write the title of the account debited.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

26

LESSON 13-4

JOURNALIZING PAYMENT OF LIABILITY FOR STATE UNEMPLOYMENT TAX page 387

January 31. Paid cash for state unemployment tax liability for quarter ended December 31, $233.55. Check No. 368.

1. Date

5. Credit amount4. Debit amount3. Check number2. Account debited

1 2 3 4 5

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

27

LESSON 13-4

TERMS REVIEW

lookback period

page 389