payroll accounting section 11. overview accounting principles account classifications account...

TRANSCRIPT

Payroll Accounting

Section 11

Overview Accounting Principles Account Classifications Account Balances Journal Entries Recording Payroll Transactions Accounting Periods Accruals and Reversals Balancing and Reconciliations Financial Statements & Audits

Accounting Principles

FASB vs. GASB GAAP

Business Entity Concept Continuing Concern Concept Time Period Concept Cost Principle Objectivity Principle Matching Principle Realization Principle Consistency Principle

Account Classifications

Double Entry Accounting

*always need a debit and a credit

Equations:

ACRONYMSALE: Assets – Liabilities = Equity

REN: Revenue – Expenses = Net Income

NICE: Net Income – Income Distributed + Contributed Capital = Equity

[Contributed Capital + Net Income – Income Distributed = Equity]

Account Classifications

Asset AccountsCurrentTangible or Property,

Plant and EquipmentIntangible or Deferred

Account Classifications

Liability AccountsCurrent

Wages payableTaxes WithheldContributions to Benefit

PlansAccounts Payable

Long TermNotes Payable

Account Classifications

Equity Contributed Capital Retained Earnings Net Income

Revenue Amounts received for goods & services sold

Expense Cost of goods and services consumed

Account Balances

Type of Account Typical Balance

Debit Credit

Asset Debit Increase Decrease

Liability Credit Decrease Increase

Equity Credit Decrease Increase

Revenue Credit Decrease Increase

Expense Debit Increase Decrease

Contributed Capital Credit Decrease Increase

Income Distributed Debit Increase Decrease

T Accounts

Payroll Checking

Debits Credits

Wages Payable

Debits Credits

$100.00 $100.00

Chart of Accounts

Makes distinctions between Assets, Liabilities, Expenses, and Revenues

Makes distinctions between types of Assets, Liabilities, Expenses, and Revenues

Uses cost centers or department codes

Types of Journal Entries

Compound Entries General Ledger Subsidiary Ledger

Accounts Payable

Accounts Receivable

PPE (Fixed Assets)

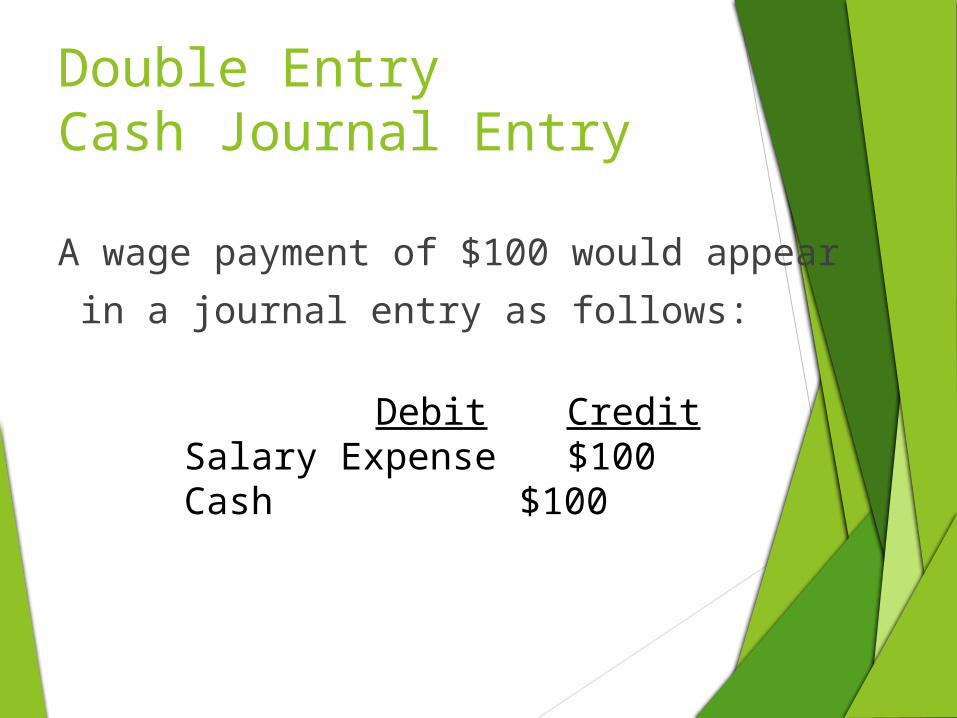

Double Entry Cash Journal Entry

A wage payment of $100 would appear

in a journal entry as follows:

Debit CreditSalary Expense $100Cash $100

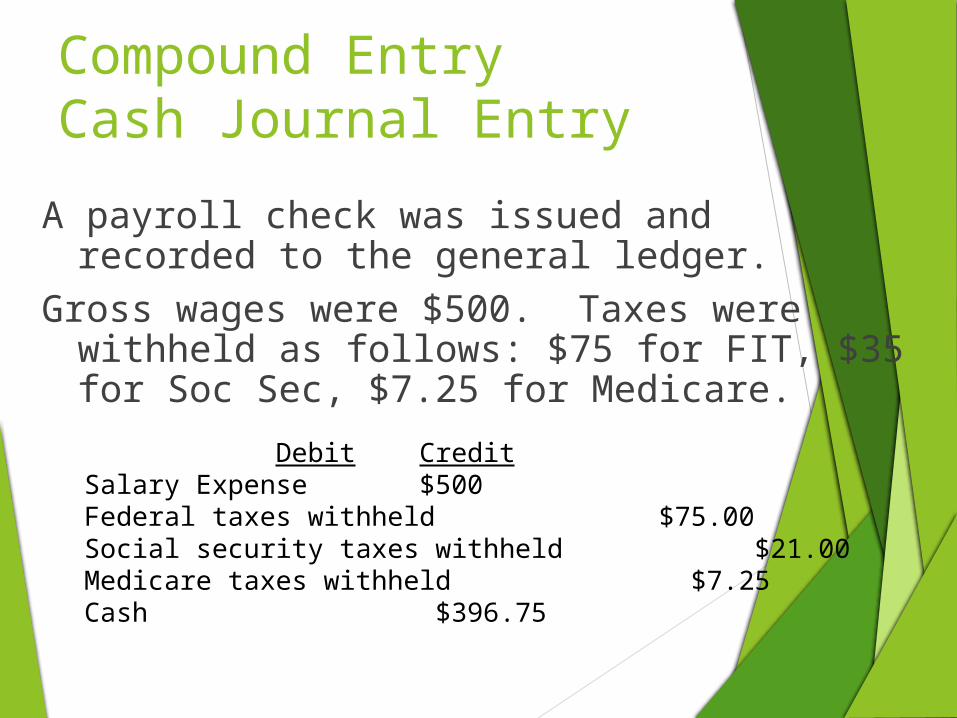

Compound EntryCash Journal Entry

A payroll check was issued and recorded to the general ledger.

Gross wages were $500. Taxes were withheld as follows: $75 for FIT, $35 for Soc Sec, $7.25 for Medicare.

Debit CreditSalary Expense $500 Federal taxes withheld $75.00Social security taxes withheld $21.00Medicare taxes withheld $7.25Cash $396.75

Accrual TransactionsSimple Journal Entry

Record Wages of $6340 due to employee

but not yet paid

Debit CreditWages Expense $6340Wages Payable $6340

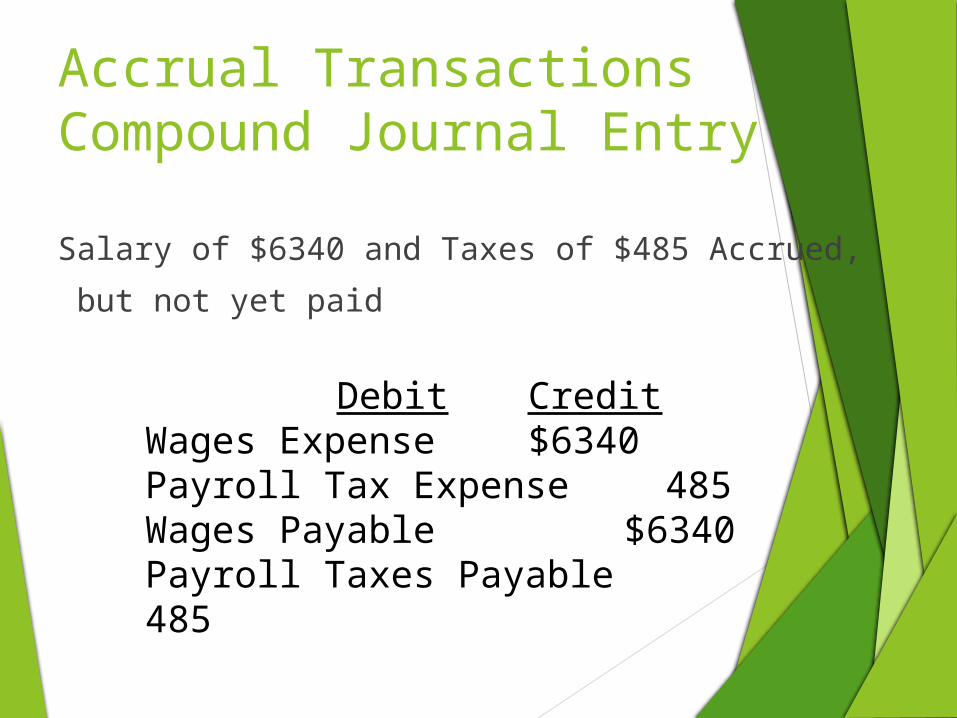

Accrual TransactionsCompound Journal Entry

Salary of $6340 and Taxes of $485 Accrued,

but not yet paid

Debit CreditWages Expense $6340Payroll Tax Expense 485Wages Payable $6340Payroll Taxes Payable 485

Accounting Periods Monthly, Quarterly or Yearly Fiscal Year vs. Calendar Year Employment Tax Returns / Employee

or Payee Information Statements

Accrual & Reversing Entries

Accruals at end of accounting period

Reversal of AccrualsReversal of Errors

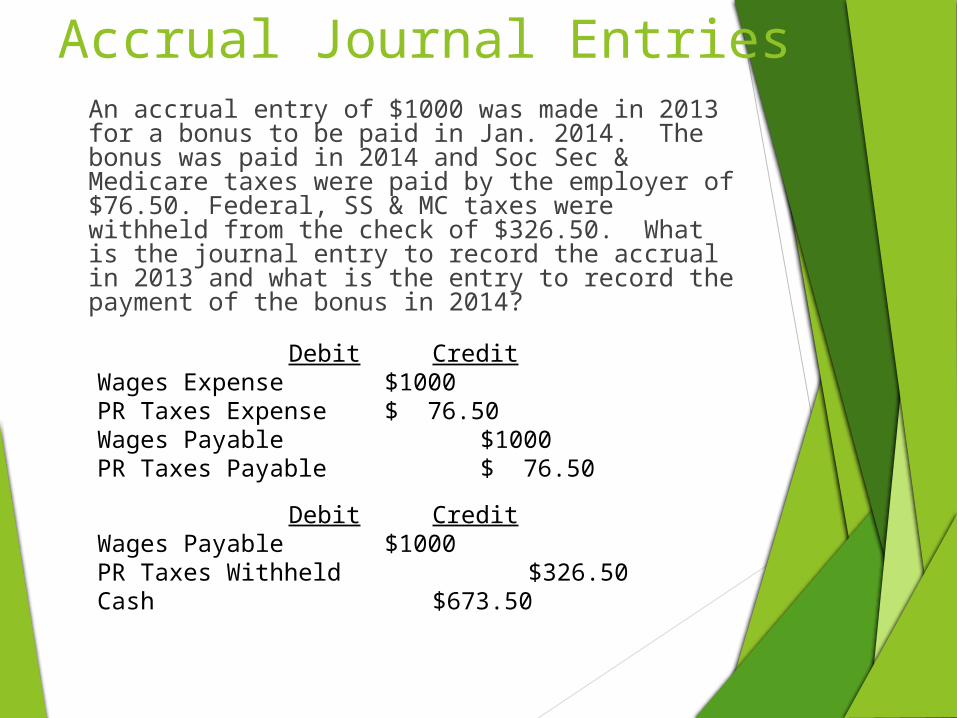

Accrual Journal EntriesAn accrual entry of $1000 was made in 2013 for a bonus to be paid in Jan. 2014. The bonus was paid in 2014 and Soc Sec & Medicare taxes were paid by the employer of $76.50. Federal, SS & MC taxes were withheld from the check of $326.50. What is the journal entry to record the accrual in 2013 and what is the entry to record the payment of the bonus in 2014?

Debit CreditWages Expense $1000PR Taxes Expense $ 76.50Wages Payable $1000PR Taxes Payable $ 76.50

Debit CreditWages Payable $1000PR Taxes Withheld $326.50Cash $673.50

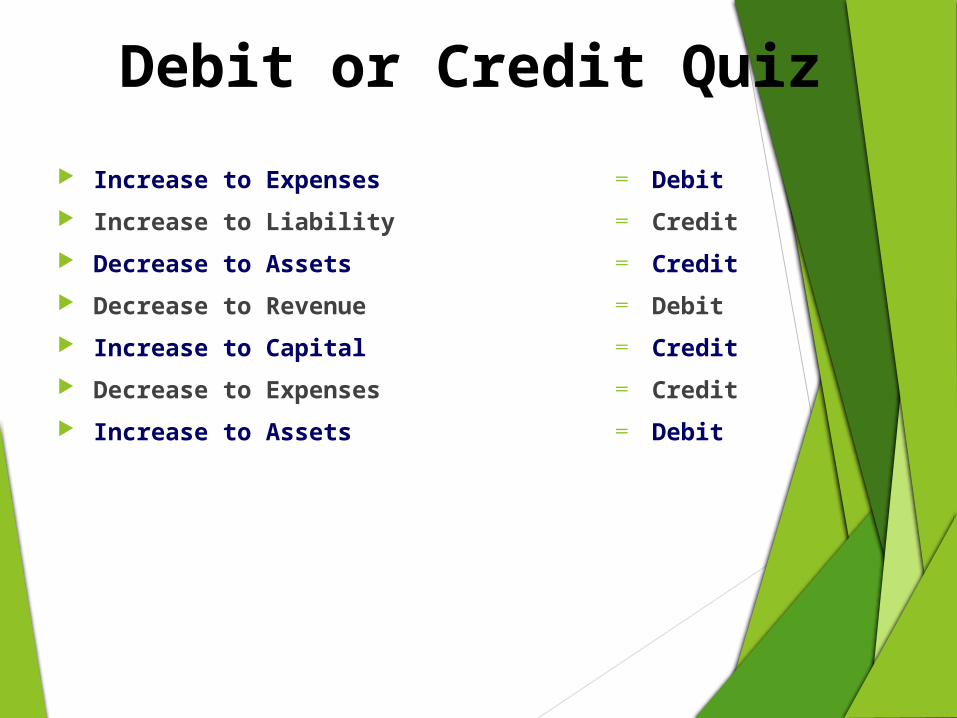

Debit or Credit Quiz

Increase to Expenses

Increase to Liability

Decrease to Assets

Decrease to Revenue

Increase to Capital

Decrease to Expenses

Increase to Assets

═ Debit

═ Credit

═ Credit

═ Debit

═ Credit

═ Credit

═ Debit

Balancing and Reconciliation

Periodic Balancing What?

Check against the payroll register Verify checks issued by A/P Verify the end of the month balance

When? Every payroll period Before filing tax returns Before sending out W-2’s or 1099’s

Bank Accounts – dual control

Financial Statements

Balance Sheet Income Statement Statement of Cash Flows Trial Balance Statement of Retained Earnings Notes to Financial Statements Audited Financial Statements

Budgets and Variances

Budget vs. Actual format Variances

Favorable Variance Unfavorable Variance

Budgets and Variances Quiz

Salary expense for the month of January was budgeted at $500. The actual expense incurred was $300. Is the variance favorable or unfavorable?

Answer: Favorable by $200

Questions ?

Overview

Internal Controls Sarbanes – Oxley Act Check Fraud Check 21 Accounting Interfaces with Payroll Terminology

Internal Controls

Blank Checks Computer

System Edits Internal

Auditor Negative Pay

deductions Payroll Bank

Account

Payroll Distribution

Phantom Employees

Rotation of job duties

Segregation of job duties

Time Reporting

Sarbanes-Oxley Act

Requires public companies to have a framework for identifying, documenting, and evaluating their internal controls over financial reporting.

Provides a logical way to analyze a company’s control system.

Prohibits a public accounting firm from providing both external auditing and most

non-auditing services to the same client and requires audit partners to rotate

every 5 years.

Check Fraud Group 1 security features Group 2 security features Group 3 security features

Check 21 Substitute checks used in clearing process

Impact on payroll

Questions ?