legal ability planning presented by: janna dutton, jd attorney and founder dutton & casey, pc...

TRANSCRIPT

LEGAL ABILITY PLANNING

PRESENTED BY:

JANNA DUTTON, JDATTORNEY AND FOUNDER

DUTTON & CASEY, PCESTATE PLANNING – PROBATE – ELDER LAW

PHONE: 312-899-0950PHONE: 847-261-4708

www.duttonelderlaw.com

Dutton & Casey, PCAttorneys at Law

Dutton & Casey, PC, Attorneys at law

2

▪Financial Decision-Making and Management

▪Health Care Decision-Making and Management

▪Care Planning

▪Long-Term Care Costs

Issues Involved in Planning and Caring

Dutton & Casey, PC, Attorneys at law

3

The Power of Attorney for Property allows an individual, referred to as the "principal" in the document, to designate another person, known as the "agent" to act for the principal as described in the document for purposes of financial and other property transactions. The agent stands in the shoes of the principal and is then legally authorized to act.

A principal must have mental capacity to execute a power of attorney: ability to comprehend the document and the effect of signing the document.

A. Advantages1. Durable -effective beyond mental incapacity

2. Revocable if competent

3. Amendable

4. Low cost to set up

Power of Attorney for Property

Dutton & Casey, PC, Attorneys at law

4

B. Disadvantages

1. Easily abused - no accountability

2. Difficult to remove a “bad” agent if principal incapacitated

3. Often difficult to use with out of state institutions

4. Allows principal to continue to contract despite incapacity, potentially making bad decisions and jeopardizing assets

5. Agent has no duty to act

C. Special Powers which must be added

1. Gifting - for Medicaid planning or other purposes

2. Transferring assets to a Trust (for self or others)

3.3. Establishing OBRA Trusts

4.4. Representation in legal separations\domestic relations actions

Power of Attorney for Property

Dutton & Casey, PC, Attorneys at law

5

D. Duties of an Agent

1. Accounting - documentation of receipts, disbursements, significant actions

2. Loyalty, acting for the welfare of the principal

3. No self-dealing, comingling of assets

Power of Attorney for Property

Dutton & Casey, PC, Attorneys at law

6

Allows for property to be owned in trust, with a designated trustee in control of the assets, and requires that the trustee manage the property according to the terms of the trust document.

A.AdvantagesB. 1. Avoids probate at the death of the Grantor.

2. Provides for effective management of property during the incapacity of the Grantor.

3. Allows the Grantor to remain in control; easy to change the trust document. However, also may not prevent financial exploitation.

2. Living Trusts

Dutton & Casey, PC, Attorneys at law

7

B. Disadvantages1.1. More expensive to create (legal fees).

2.2. Assets must be transferred to trust - time consuming effort.

3.3. Assets must be held in trust - requires lifetime administration.

4.4. Trustee has authority only over Trust assets and is limited by the terms of the trust document

C. Duties of Trustee

1. Prudently invest and administer trust assets.

2. Loyalty to trust beneficiaries; no self-dealing

3.Accounting to trust beneficiaries

4.Compliance with terms of trust document

Living Trusts

Dutton & Casey, PC, Attorneys at law

8

A form of joint ownership whereby each owner owns one hundred percent of the property; at the death of one of the joint owners, the surviving owners own the entire property.

Advantages1. No cost to set up.

2. Effective way to avoid probate.

3. Effective way to arrange estate so that others will be able to manage during incapacity.

Joint Tenancy

Dutton & Casey, PC, Attorneys at law

9

Disadvantages1. Risky - joint tenancy has an ownership interest in the property and the

property is available to the creditors of the joint tenant, as well as may become subject to the marital disputes, disabilities, and other problems of the joint tenant.

2. Does not allow for contingent beneficiaries if the joint tenancy predeceases.

3. Surviving joint tenant is entitled to the entire property at death of a joint tenant - where there are several persons who are the beneficiaries of the owner’s estate, difficult to name all as joint tenants, and more risky.

4. For Medicaid purposes, Medicaid applicant presumed to be 100% owner of a all personal joint property

Joint Tenancy

Dutton & Casey, PC, Attorneys at law

10

Convenience Accounts

As of January 1, 2010, Illinois law allows bank account holders to name another person on their account for the sake of convenience. Previously, your sole option in naming another person on your account was as joint tenants with rights of survivorship, meaning the joint tenant is entitled to inherit the account upon your death. It also meant that you were making an inter vivos gift, or in other words, giving the joint tenant the right to legally take all of your money for himself. Furthermore, it meant that you could not remove the joint tenant without his consent– even if this person was withdrawing money from the account for himself without your permission. The new law allows you to name a person on your account without making an inter vivos gift and without entitling that person to inherit your account upon your death. Most importantly, the new law allows you to remove the person from your account at any time without his permission.

Note: Your joint accounts will not be converted automatically to convenience accounts under this law and you still have the option of holding joint accounts. In order for this new law to apply, you will need to go to your bank and open a new convenience account.

Dutton & Casey, PC, Attorneys at law

11

The Power of Attorney for Health Care allows an individual, referred to as the "principal" in the document, to designate another person, known as the "agent" to act for the principal as described in the document to make health care decisions for the principal. The agent stands in the shoes of the principal and is then legally authorized to act, including acting to withhold or withdraw life support as well as make any other type of health care decisions.

The principal must have mental capacity to execute a power of attorney for health care.

A. Advantages 1. Decisions are legally enforceable

2. Amendable

3. Revocable regardless of mental status

B. Disadvantages 1. Revocable regardless of the mental condition of the principal.

2. If designate a person who is unaware of principal’s values, they may make a health care decision contrary to principal’s wishes.

3. Power of Attorney for Health Care

Dutton & Casey, PC, Attorneys at law

12

A Living Will is a document that expresses your preferences to forgo life support in the circumstances that it would only prolong the dying process. It does not authorize another person to make a decision, but is a form of communication to a health care provider.

A. Advantages

1.Allows a method of communicating values to health care providers that death-delaying life support is not wanted.

B. Disadvantages

1.On a practical level, is not legally enforceable by person signing it.

2.May be ignored.

Living Will

Dutton & Casey, PC, Attorneys at law

13

The cost of long term care-meaning either in-home care or nursing home care for individuals requiring assistance with activities of daily living- is largely an uninsured healthcare cost for most individuals. Planning for possible exposure to these costs is necessary for effective retirement planning.

A. Medicare Coverage1. Covers 100 days of skilled nursing care provided in a Medicare certified nursing facility following a hospitalization per spell of illness. Medicare pays the full cost of the first 20 days. There is a coinsurance payment of $144.50 per day for days 21 through 100 which most Medicare supplemental policies cover.

2. Medicare provides home care to those individuals needing intermittent skilled care, usually post hospitalization only, although long term part time skilled home care services are covered. Skilled care does not include custodial care, which is the type of long term care most individuals impaired by dementia require

II. Planning for Long-Term Care Costs

Dutton & Casey, PC, Attorneys at law

14

Long Term Care Insurance is the only health insurance that pays for custodial long term care, either at home, or in a nursing home.

B. Long-Term Care Insurance

Dutton & Casey, PC, Attorneys at law

15

Medicaid

Federal – State Program Federal Law and Monitoring State Law – Regulations and Policy State “Medicaid Agency” – Illinois

Department of Healthcare and Family Services

State Eligibility Determinations – Illinois Department of Human Services

16

Dutton & Casey, PC, Attorneys at law

Illinois Medicaid Covered Long Term Care Nursing homes Supportive living- “Waivered” Community care program (over 60) –

“Waivered” In-home services (under 60) –

“Waivered”

17

Dutton & Casey, PC, Attorneys at law

Medicaid Eligibility

Residency and Citizenship

Categorical eligibility

Need

18

Dutton & Casey, PC, Attorneys at law

Residency

Only residents of Illinois are eligible for Illinois Medicaid. Voluntarily living in Illinois No durational requirement Intention to remain in Illinois

If an individual maintains a home in another state, Illinois residency may not be established.

19

Dutton & Casey, PC, Attorneys at law

Citizenship

Only U.S. Citizens or lawful aliens are eligible for Medicaid. Lawfully admitted for permanent residency;

or Permanently residing in the United States

under color of law Documentation of U.S. Citizenship and

identity is required of all applicants except for Medicare, SSI, and RSDI recipients.

20

Dutton & Casey, PC, Attorneys at law

Categorical Eligibility

Under current law, for an individual to be eligible for Medicaid, must be categorically eligible: Aged, blind or disabled; Child; Caretaker of eligible child.

Additionally, the individual must meet strict financial requirements.

21

Dutton & Casey, PC, Attorneys at law

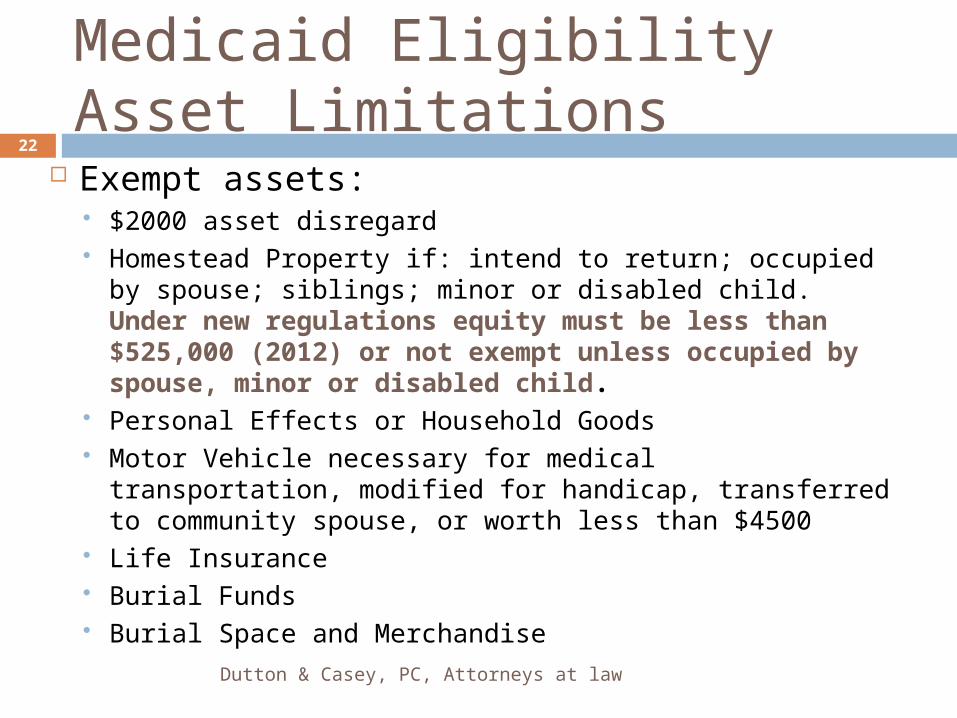

Medicaid Eligibility Asset Limitations

Exempt assets: $2000 asset disregard Homestead Property if: intend to return; occupied by

spouse; siblings; minor or disabled child. Under new regulations equity must be less than $525,000 (2012) or not exempt unless occupied by spouse, minor or disabled child.

Personal Effects or Household Goods Motor Vehicle necessary for medical transportation,

modified for handicap, transferred to community spouse, or worth less than $4500

Life Insurance Burial Funds Burial Space and Merchandise

22

Dutton & Casey, PC, Attorneys at law

Exempt Homestead

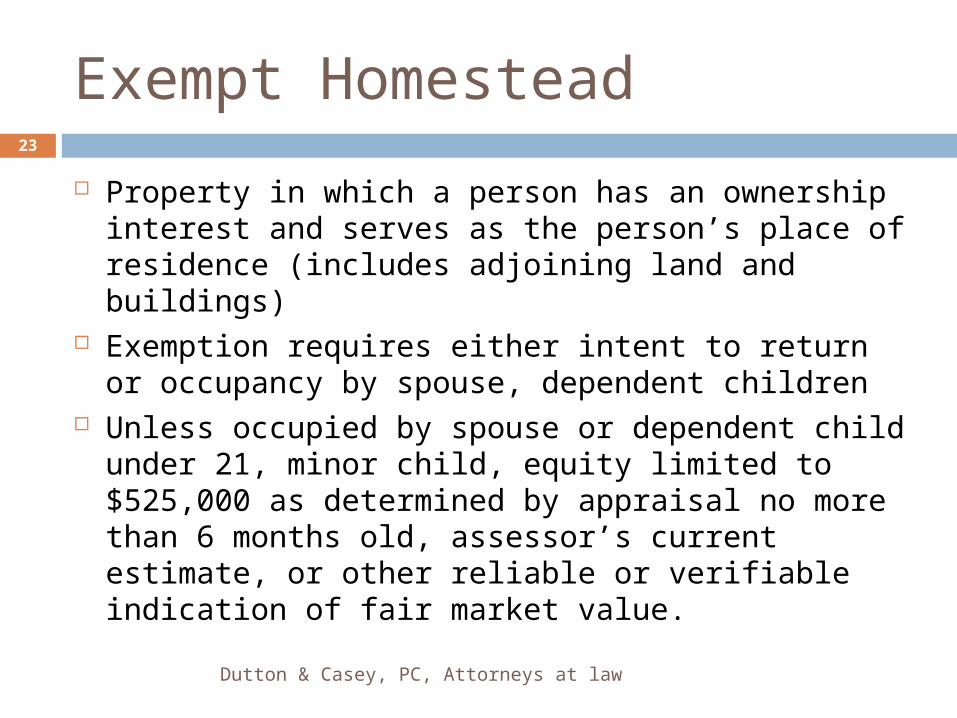

Property in which a person has an ownership interest and serves as the person’s place of residence (includes adjoining land and buildings)

Exemption requires either intent to return or occupancy by spouse, dependent children

Unless occupied by spouse or dependent child under 21, minor child, equity limited to $525,000 as determined by appraisal no more than 6 months old, assessor’s current estimate, or other reliable or verifiable indication of fair market value.

23

Dutton & Casey, PC, Attorneys at law

Personal Property

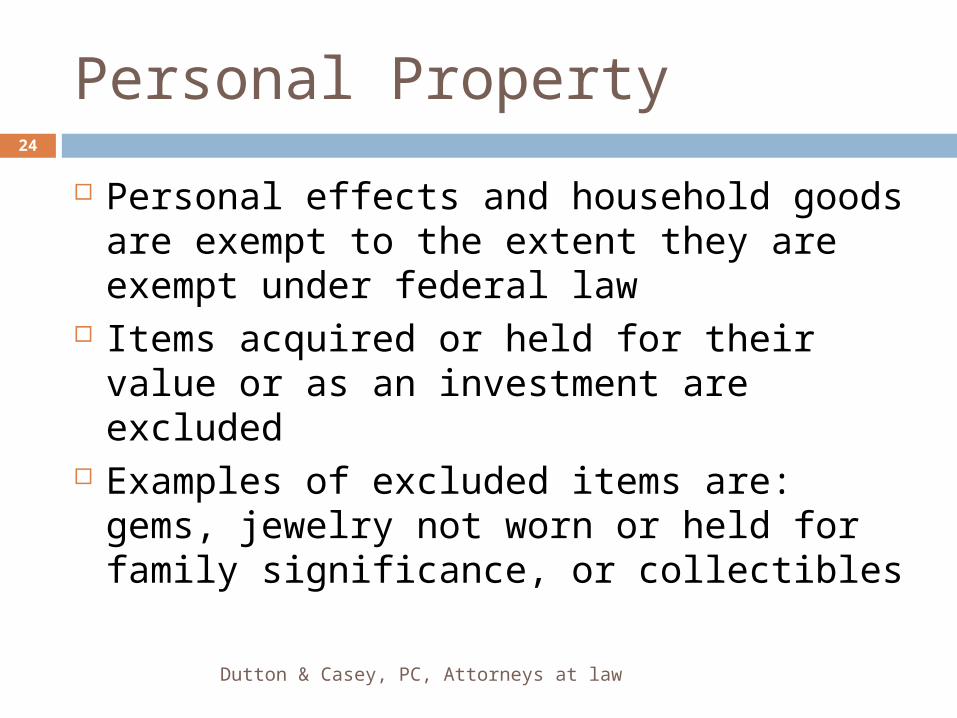

Personal effects and household goods are exempt to the extent they are exempt under federal law

Items acquired or held for their value or as an investment are excluded

Examples of excluded items are: gems, jewelry not worn or held for family significance, or collectibles

24

Dutton & Casey, PC, Attorneys at law

Burial Space Exemptions

For use by applicant, spouse or any immediate family members

Includes gravesites, crypts, mausoleums, urns, caskets, vaults, plots, niches, etc.

Also- headstones, markers, plaques, burial containers and arrangements for opening and closing gravesites

25

Dutton & Casey, PC, Attorneys at law

Joint Assets

Joint accounts and personal property Presumption is 100% belongs to applicant

Joint real estate Life estate

Life estate may be subject to lien Change: funds used to purchase life estate

will be considered to be non-allowable transfer of assets unless the purchaser resides in the home for a period of at least one year after date of purchase

26

Dutton & Casey, PC, Attorneys at law

Burial Funds

Up to $1,500 in a revocable burial fund contract; Funds in an irrevocable prepaid burial contract up

to $5,874, including both goods and services but not including burial spaces; or

A prepaid burial contract funded by an irrevocable assignment of a person’s life insurance policy irrevocably assigned to a trust which includes a statement that, upon the death of the person, the State will receive all amounts remaining in the trust.

27

Dutton & Casey, PC, Attorneys at law

Entrance Fees

A person’s entrance fee in a continuing care community will be considered as part of a person’s available assets if: Person has ability to use resource for care Person is eligible for a refund of any

remaining fee or Entrance fee does not confer ownership

interest

28

Dutton & Casey, PC, Attorneys at law

Non-Homestead Real Estate

Considered available unless: Farmland property; Small fractional interest; Listed for sale, will not be counted for six

months as long as good faith effort to sell continues; or

Property was homestead property that is no longer exempt and that is producing income in an amount equal to six percent or greater of person’s equity.

29

Dutton & Casey, PC, Attorneys at law

Annuities

Ownership or purchase of any annuity must be disclosed;

Revocable and assignable annuities are available;

Payments considered available income; and

Failure to name State as remainder beneficiary after spouse, disabled or minor child will result in denial of eligibility for long term care services.

30

Dutton & Casey, PC, Attorneys at law

Annuities

In addition to above, purchase of an annuity by an institutionalized person will be considered a penalized transfer unless: Purchased with retirement funds; or Purchased from a commercial financial

institution, is actuarially sound based on the social security life expectancy ; payout is equal to or less than life expectancy, is irrevocable and nonassignable, and benefits are paid in approximately equal periodic payments.

31

Dutton & Casey, PC, Attorneys at law

Income Eligibility

To qualify for Medicaid coverage, the nursing home or supportive living resident’s countable monthly income must be less than the nursing home’s monthly private pay rate. Different income rules apply to the Community

Care Program Income in the community spouse’s name is

not considered available to the nursing home spouse from the first full month in which the nursing home spouse is institutionalized.

“Name on the instrument” rule

32

Dutton & Casey, PC, Attorneys at law

Allowable Deductions from Income of Nursing Home Medicaid Recipient

Personal needs allowance ($30 for Nursing Home residents/$90 for Veterans) Community Spouse Income Allowance Family Maintenance Needs Allowance Maintenance for Dependent Children under 21 not residing with community

spouse Amounts to cover Medicare and other health insurance premiums Amounts to cover over the counter drugs or other medically necessary items

ordered by a physician but not paid for by Medicaid and amounts to cover incurred expenses for medical or remedial care for the institutionalized spouse not paid for by Medicaid limited to those incurred within the 6 months prior to the month of an application if a current liability. Medical expenses incurred during a penalty period not allowable.

Amounts to maintain a home in the community if a person who has no spouse or dependent children at home is admitted to a facility for what is expected to be six months or less, provided that a physician has certified that the individual is expected to return home within six months. Amount of the deduction is based upon the AABD MAG standard.

33

Dutton & Casey, PC, Attorneys at law

Community Spouse Maintenance Needs Allowance The community spouse is able to receive a contribution from the

nursing home spouse's income to bring his or her total monthly income up to the amount of a predetermined monthly needs allowance, $2,739. There are provisions for annual adjustments of this figure like the asset figure that is tied to the consumer price index of the previous year.

Community spouse or nursing home spouse may request a fair hearing to establish a greater amount of maintenance allowance. For instance, if regular heath care costs exceeding $2,739 per month can be proven at a fair hearing to increase the needs standard, the allowance from the nursing home spouse's income may be increased.

Under new regulations, the Community Spouse must prove exceptional circumstances resulting in significant financial distress.

Additionally, if the community spouse has a court order for support or maintenance which, in combination with the community spouse's income, exceeds the $2,739 standard, IDHS must abide by the court order.

34

Dutton & Casey, PC, Attorneys at law

Community Spouse Assets

Under new regulations, all assets of the institutionalized spouse and community spouse count as available in determining eligibility.

Community Spouse Asset Allowance – the standard allowance is $109,560. All other nonexempt assets considered available to pay for case.

Court Orders – the State must allow assets awarded to the community spouse by court order

35

Dutton & Casey, PC, Attorneys at law

Community Spouse Asset Allowance

Increased Asset Allowance by Appeal Hearing Based upon community spouse’s separate

income; Increase in Asset Allowance measured by the

cost of an actuarially sound single premium life annuity that, when added to the combined income of the institutionalized spouse and community spouse will be sufficient to raise the CS’s total income, including the income of the nursing home spouse, to the standard ($2739).

36

Dutton & Casey, PC, Attorneys at law

Community Spouse Rules

Under the new regulations, the nursing home spouse’s application for Medicaid will not be denied based upon the assets of the community spouse if the nursing home spouse “assigns” to the State his or her support rights; the nursing home spouse is incapable of signing an Assignment; or undue hardship will result.

The State may seek Responsible Relative income payments from the spouse or take other legal action.

37

Dutton & Casey, PC, Attorneys at law

Major Differences Between Old and New Spousal Impoverishment Rules

CS assets count towards NH spouse Medicaid eligibility: Prenuptial Agreements irrelevant - all assets count

CS refusal - NH spouse may be determined eligible provided he/she “Assigns” right to spousal support to the State. State allowed to legally pursue CS for support both for income contribution under current rules and by other legal actions.

Income First Rule for increased asset allowance

38

Dutton & Casey, PC, Attorneys at law

Nonallowable Transfers

Non-allowable transfers are those made for less than fair market value which are presumed to be made for the purpose of qualifying for Medicaid and do not fall within one of the exceptions.

39

Dutton & Casey, PC, Attorneys at law

Transfer of Assets Rules

For applications filed on or after 1/1/2012, a 60-month “look back”

New rules applicable to all transfers occurring on or after January 1, 2007, except hardship exceptions apply

Penalty period calculated for each month in which nonallowable transfer occurred by dividing amount transferred by average cost of nursing home care

Penalty period measured in months and partial months/days

40

Dutton & Casey, PC, Attorneys at law

Transfer of Assets Rules

Penalty period starts the month that the applicant is receiving a long term care level of care and is eligible for Medicaid based upon an application but for the application of the penalty period; multiple penalty periods run consecutively. BUT SEE HARDSHIP EXCEPTIONS

No“partial” cures for transfers occurring after November 1, 2008 – penalty reduced only if the entire amount transferred is returned to applicant. Partial cures allowed for transfers made prior to November 1, 2008.

41

Dutton & Casey, PC, Attorneys at law

Hardship Waivers of Penalties

For Transfers occurring prior to November 1, 2011:

Hardship waiver of penalty period shall be granted if applicant signs an attestation form stating that the penalized transfer was made in reliance on the administrative rules in effect at the time of the transfer and that, without a waiver, the applicant faces deprivation of medical care, food, clothing, shelter, or other necessities

42

Dutton & Casey, PC, Attorneys at law

Hardship Waivers of Penalties

A facility in which an institutionalized person is residing may request a hardship waiver on behalf of that person provided written consent has been obtained from the person who is legally competent or from the person’s personal representative, which may include the person who signed the application for medical assistance on behalf of the resident.

43

Dutton & Casey, PC, Attorneys at law

Notice of Hardship Waivers

The Department shall issue a notice to any person who is subject to a penalty period not less than 10 days prior to imposition of the penalty. The notice shall inform the person of the period of ineligibility for long term care services and include a statement that the person may request a hardship waiver by submitting evidence. Upon review, the Department shall issue a notice of decision on a request for a hardship waiver that includes a statement that the person may appeal the decision.

44

Dutton & Casey, PC, Attorneys at law

Allowable Transfer of Assets

Allowable Transfers of Assets Transfers of exempt homestead property to: a spouse, minor child,

disabled adult child, sibling with an equity interest residing on the property, or child who lived with applicant and provided care or support for years prior to nursing home admission

Transfers to or for the benefit of the Community Spouse Transfers to a blind or disabled child of any age or to a trust created solely

for the benefit of the disabled child Transfers by a disabled person under age 65 to an OBRA Pay Back Trust

or OBRA Pooled Trust Subaccount. Note: transfers by disabled persons over the age of 65 to an OBRA Pay Back Trust or OBRA Pooled Trust Subaccount are penalized transfers.

Transfers where it is determined that a denial of eligibility would create an undue hardship

Transfers made exclusively for a reason other than to qualify for benefits Transfers to a Community Spouse that were result of a court order Transfers that are returned to the person prior to a determination of

eligibility. If returned after eligibility determination, must be returned in full.

45

Dutton & Casey, PC, Attorneys at law

Allowable Transfers of Assets – Proposed Rules Changes to allowable transfers under new

rules Transfers of homestead to 2-year, live-in

caregiver child: Need evidence (physician’s statement) to

support that the term would have otherwise required institutional level of care ;

Need evidence to show the child resided with the person;

Need evidence to show the child provided care that prevented institutionalization, such as affidavits.

46

Dutton & Casey, PC, Attorneys at law

Medicaid Rules and Payments to Caregivers Personal Care Contracts must be established

prior to the receipt of services; Services must be clearly identified and

reimbursed consistent with the prevailing cost in the service area;

Contemporaneous receipts, logs or other credible documentation showing actual delivery of services;

Presumption that services provided by friends or family are “gratis” unless there is contemporaneous written agreement.

47

Dutton & Casey, PC, Attorneys at law

Promissory Notes

The purchase of a promissory note, loan or mortgage by an applicant is considered a transfer of assets unless: A written instrument recording the transaction is executed,

signed and dated on the effective date of the transaction; Repayment term is actuarially sound; Instrument provides for payments to be made in equal

installments with no deferral or balloon payments; Instrument prohibits cancellation; and There is a verifiable record of consistent, timely payments

of amounts due under the Note. (Delinquency of 3 months or more results in the loan being considered nonallowable.)

Assignment of remainder to State up to amount Medicaid paid.

48

Dutton & Casey, PC, Attorneys at law

Hardship Waiver for transfers after November 1, 2011

The Department shall waive a penalty period or portion of a penalty period if it determines the penalty causes undue hardship defined as: Deprivation of medical care endangering person’s

health or life, food, clothing, shelter; Person requesting waiver has burden of proof of

actual hardship. Person must provide written evidence to

substantiate the circumstances of the transfer, attempts to recover the uncompensated value of the transfer, reasons for the transfer and the impact of the penalty period of ineligibility

49

Dutton & Casey, PC, Attorneys at law

Hardship Waivers for transfers after 11/1/2011

Person must present credible and convincing evidence that the person has, in good faith and to the best of their ability, taken all equitable and legal means available to recover an asset that has been transferred. In cases involving alleged theft, fraud, elder abuse or other misappropriation of assets, evidence of referrals to law enforcement is required.

50

Dutton & Casey, PC, Attorneys at law

Miscellaneous Changes

Retroactive eligibility – must prove eligibility in each of three months of retroactive eligibility. Currently presumed except may use funds for legal fees, prepaid burial.

Asset transfer rules will apply to persons living in Community Integrated Living Arrangements.

Assets considered available when the person has the lawful power to cause the resource to be available (although not actually easily available, i.e. requires lawsuit to be filed).

51

Dutton & Casey, PC, Attorneys at law

Medicaid Treatment of Trusts Self Settled (or by spouse) Revocable Trusts -

commonly known as “Living Trusts” Count as an asset

Self Settled (or by spouse) Irrevocable Trusts Whatever amounts that the trustee may use for the

benefit of the Medicaid applicant is presumed available; it can use any principal, all available

Third -Party Trusts Do not count if “discretionary”; count if can be used for

support, health and maintenance OBRA Payback Trusts

Do not count if meet all requirements

52

Dutton & Casey, PC, Attorneys at law

OBRA Individual Payback Trust Requirements Irrevocable Established by parent, grandparent, court or

guardian Beneficiary disabled. Transfer allowable only if

beneficiary under age 65. Any state which paid out Medicaid benefits on

behalf of beneficiary is paid back at the death of the beneficiary before any other payment except taxes and reasonable expenses of administration.

If proceeds of trust are from personal injury action, the Department lien must be paid off before transferring the proceeds to the trust.

53

Dutton & Casey, PC, Attorneys at law

OBRA Pooled Trust Subaccount Requirements Irrevocable Established by parent, grandparent, court or

guardian or the beneficiary him or herself Beneficiary disabled. Transfer allowable only if

beneficiary under age 65. Payback to any State providing Medicaid unless

retained by the Trust If States are paid back at the death of the

beneficiary must be before any other payment except taxes and reasonable expenses of administration.

54

Dutton & Casey, PC, Attorneys at law

DUTTON & CASEY, P.C.ESTATE PLANNING – PROBATE – ELDER LAW

www.duttonelderlaw.com

Attorneys:Janna Dutton, Kathryn C. Casey, Helen Mesoloras, and Hanny Pei

Client Care Coordinator:Erin C. Vogt, LCSW, ACSW, CMC

Appointments Available In:Arlington Heights, Chicago, Skokie, and Vernon Hills, Illinois

Phone: 312-899-0950 or 847-261-4706Email: [email protected]