lecture notes banking regulation program mm banking stie perbanas

TRANSCRIPT

Lecture Notes

Banking Regulation

Program MM BankingSTIE Perbanas

Topics

• Topics include:

- Asymmetric Information and Bank Regulation

- International Banking Regulation

- Banking Crisis Throughout the World

Asymmetric Information and Bank Regulation

• Analysis of asymmetric information, moral hazard, and adverse selection provide an excellent backdrop for understanding the current regulatory environment in banking.

• Asymetric information – different parties in a financial contract do not have the same information.

• Adverse selection – problem that occurs before transaction - potential bad credit risks are the ones who most actively seek out loans – big risk takers might be the most eager to to take out a loan because they know that they are unlikely to pay it back.

Asymmetric Information and Bank Regulation

• Moral hazard – arises after transaction occurs – once borrowers have obtained a loan, they may take on big risks because they are playing with someone else’s money – lowers the probability that the loan wil be repaid.

• Asymetric information leads to adverse selection and moral hazard problems

• There are seven basic categories of bank regulation, which we will examine from an asymmetric information perspective.

Asymmetric Information and Bank Regulation

1. Government Safety Net: Deposit Insurance and the FDIC (in USA), LPS (in Indonesia)

• Prior to FDIC or LPS insurance, bank failures meant depositors lost money, and had to wait until the bank was liquidated to receive anything. This meant that “good” banks needed to separate themselves from “bad” banks, which was difficult for banks to accomplish.

• The inability of depositors to assess the quality of a bank’s assets can lead to panics. If depositors fear that some banks may fail, their best policy is to withdraw all deposits, leading to a bank run, even for “good” banks.

Asymmetric Information and Bank Regulation

• Bank panics did occur prior to the FDIC, with major panics in 1819, 1837, 1857, 1873, 1884, 1907, and 1930-1933, and even after FDIC bank panics still occurred in 1980s, 2008.

• In Indonesia, bank panics did occur during financial crisis in 1997/98 prior to LPS and previously government deposit guarantee program (safety net).

• The deposit insurance agency handles failed banks in one of two ways: the payoff method, where the banks is permitted to fail, and the purchase and assumption method, where the bank is folded into another banking organization.

Asymmetric Information and Bank Regulation

• Implicit insurance is available in some countries where no explicit insurance organization exists.

• The FDIC and LPS or any kind of implicit deposit insurance creates moral hazard incentives for banks to take on greater risk than they otherwise would because of the lack of “market discipline” on the part of depositors.

• The deposit insurance creates adverse selection. Those who can take advantage of (abuse) the insurance are mostly likely to find banks attractive.

Asymmetric Information and Bank Regulation

• Regulators are reluctant to let the largest banks fail because of the potential impact on the entire system (systemic risk). This is known as the “Too Big to Fail” doctrine. This increases the moral hazard problem for big banks and reduces the incentive for large depositors to monitor the bank.

2. Restrictions on Asset Holdings and Bank Capital Requirements – minimizing moral hazard

• Regulations limit the type of assets banks may hold as assets, e.g. banks may not hold common stock (risky).

Asymmetric Information and Bank Regulation

• Banks are also subject to capital requirements. Banks are required to hold a certain level of capital (book equity) that depends on the type of assets that the bank holds.

• Details of bank capital requirements:

• Capital must exceed 8% of the banks risk-weighted assets and off-balance sheet activities

• Basle Accord – capital requirements - set up by Basel Committee on Banking Supervision in

1988, an agreement among banking officials (originally by 10 countries but today adopted by more than 100 countries) on capital requirements.

Asymmetric Information and Bank Regulation

- Basle II accord (2004) – adopted by Bank Indonesia since 2008• a reform of the original Basle accord 1988 – risk-based capital requirement• banks are required to have at least 8% of their risk-weighted assets• 4 categories of assets and off-balance sheet activities:

- Zero weight (items that have little default risk)- 20% weight (claims on bank )- 50% weight (municipal bonds and residential mortgages )- 100% weight (loans to consumers and corporations)

• The framework of Basel II is based on three pillars:- Minimum capital requirements- Strengthening the supervisory process- Improving market dicipline

How Asymmetric Information Explains Banking Regulation

3. Bank Supervision: Chartering and Examination• Reduces the adverse selection problem of risk-takers or

crooks owning banks to engage in highly speculative activities. Charters (license) may simply not be granted.

• Examinations assign a CAMELS rating to a bank, which can be used to justify cease and desist orders for risky activities.

• Period reporting (call reports) and frequent (sometimes unannounced) examinations allow regulators to address risky / questionable practices in a prompt fashion.

How Asymmetric Information Explains Banking Regulation

4. Assessment of Risk Management

• Past examinations focused primarily on the quality of assets. A new trend has been to focus on whether the bank may take excessive risk in the near future.

• Four elements of risk management and control:

1. Quality of board and senior management oversight

2. Adequacy of policies limiting risk activity

3. Quality of risk measurement and monitoring

4. Adequacy of internal controls to prevent fraud

How Asymmetric Information Explains Banking Regulation

5. Disclosure Requirements• Better information reduces both moral hazard and adverse selection

problems

6. Consumer Protection• Standardized interest rates (APR)

• Prevent discrimination (e.g., CRA)

7. Restrictions on Competition• Branching restrictions, which reduced competition between banks

• Separation of banking and securities industries: Glass-Steagall. i.e., preventing nonbanks from competing with banks.

• In Indonesia, separation of banking and securities industries are clearly defined under different law and separate regulators (BI, BAPEPAM).

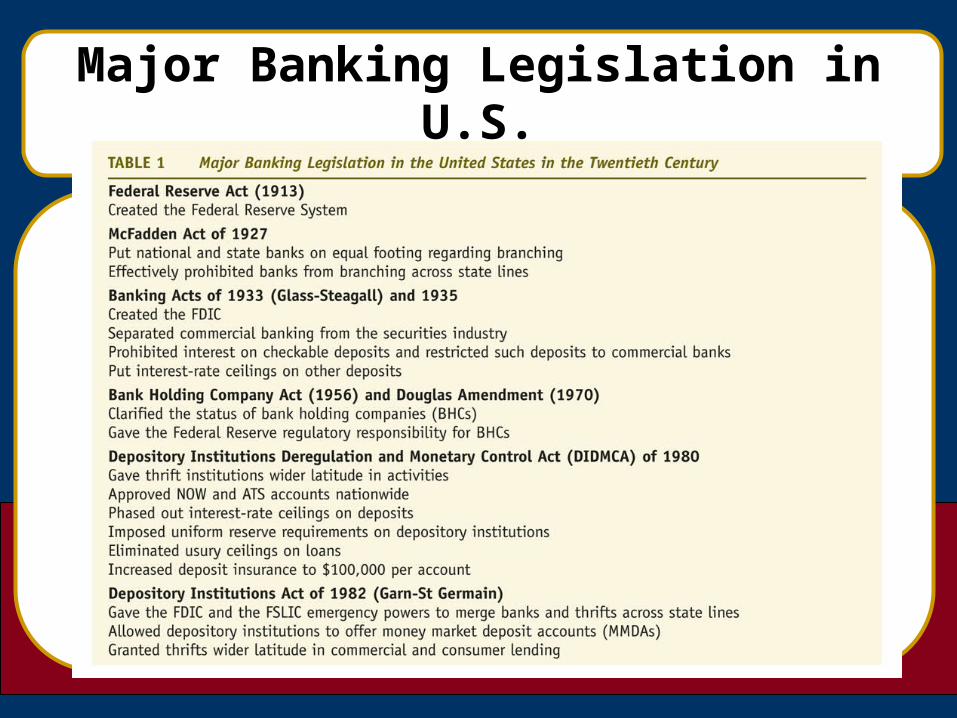

Major Banking Legislation in U.S.

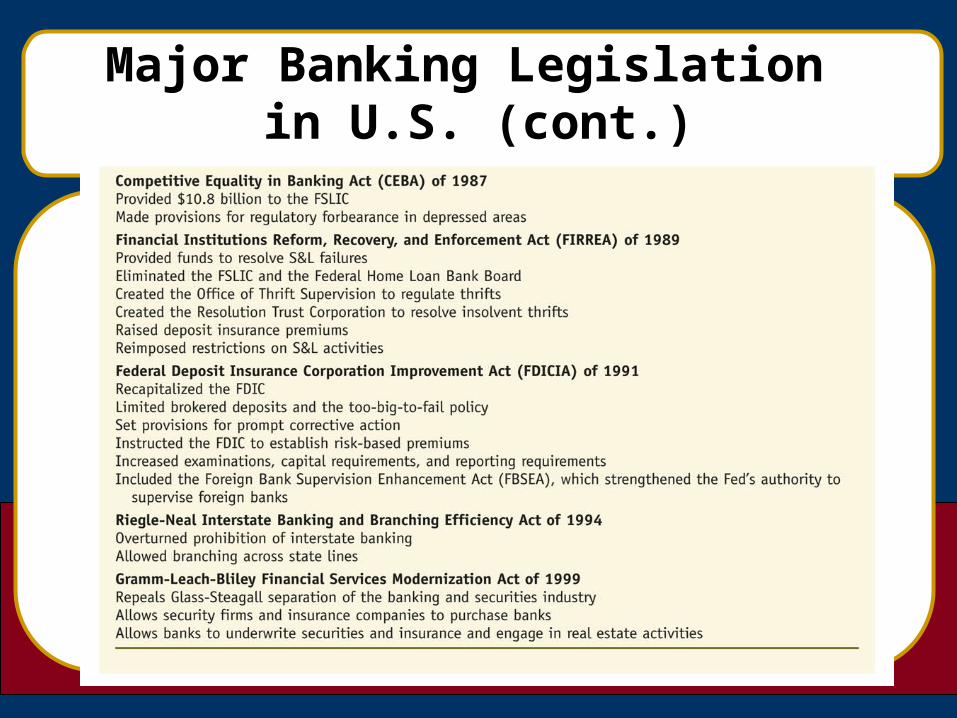

Major Banking Legislation in U.S. (cont.)

International Banking Regulation

• Bank regulation in many countries are being harmonized.

• Bank capital requirements are in the process of being standardized across countries with agreements like the Basel Accord .

• There is a particular problem of regulating international banking and can readily shift business from one country to another and requires coordination of regulators in different countries (a difficult task).

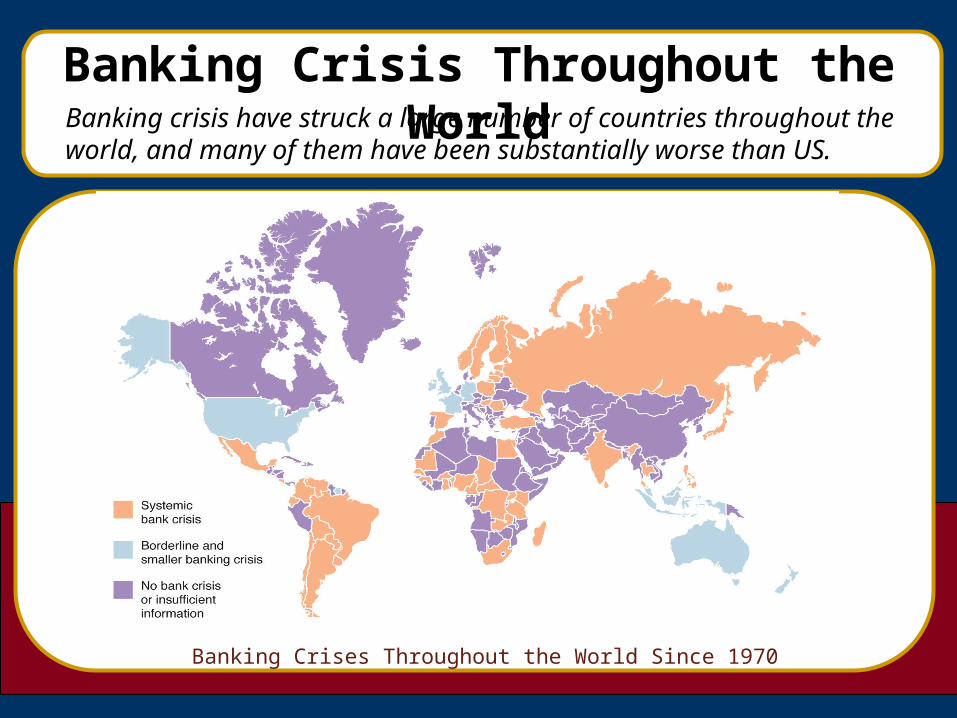

Banking Crises Throughout the World Since 1970

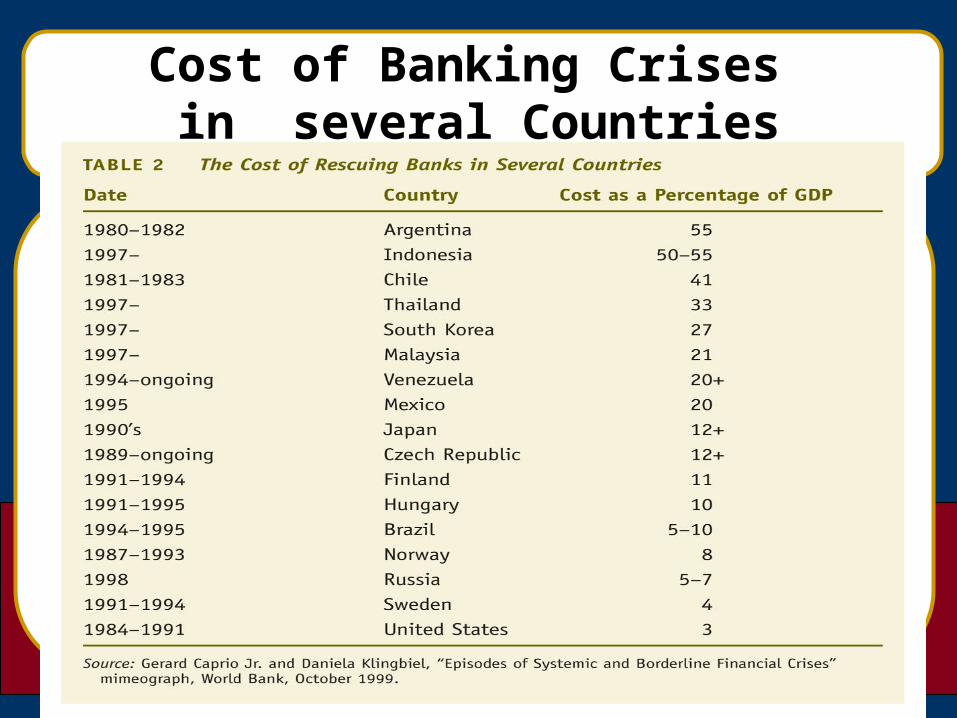

Banking Crisis Throughout the WorldBanking crisis have struck a large number of countries throughout the world, and many of them have been substantially worse than US.

20-18

Cost of Banking Crises in several Countries

Banking Crisis Throughout the World

• Latin America- Many banks were government owned with interest rate

restrictions similar to Regulation Q.- Similar loan losses and bailout experience as the U.S. in the

late 1980s.- Argentina ran into government confidence problem, causing

required rates on government debt to exceed 25%, which caused severe problems for the banking industry.

- Losses and bailouts as a percent of GDP are high (20% +) relative to that in the U.S. (around 3%).

Banking Crisis Throughout the World

• Russia and Eastern Europe- Many banks were government owned prior to the downfall of

communism.

- Private banks had little experience screening and monitoring loans.

- Substantial loan losses ensued.

- The bailout in Russia alone may exceed $15 billion

• Japan

- Prior to the 1980s, Japan’s financial markets were heavily regulated. Deregulation led to excessive risk taking and high loan losses, particularly in real estate loans.

Banking Crisis Throughout the World

• Japan (cont.)

- Several large bank failures were announced in 1995. Several failures followed in 1996 and 1997.

- Japan is experiencing similar regulator forbearance policies (linient) as the U.S. in the early 1980s.

- Even with positive steps, bad loans throughout the banking system had reaches over $1 trillion in 2001.

- System is still a long way from being healthy.

Banking Crisis Throughout the World

• China

- Many banks were government owned.

- Investments in many state-owned enterprises, which are notoriously inefficient.

- Current attempt at a bailout calls for partial privatization of the biggest banks.

Banking Crisis Throughout the World

• East Asia (Thailand, Indonesia, Malaysia, Philippines, South Korea)

- These countries suffered from financial crises in 1997/1998

- Lending boom in the aftermath of liberalization led to substantial loan losses.

- Nonperforming loans and bailout costs exceeding 20% of GDP are common place.

- Indonesian crises cost around Rp 650 trillion (50% of GDP)