lecture capbud risk

TRANSCRIPT

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 1/29

Chapter 7

Risk and Real

Options inCapitalBudgeting

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 2/29

Project Analysis &

Evaluation• Evaluating NPV Estiates – !o" relia#le is our NPV estiate$ –

%orecasting Risk Bad decisions'ro errors in projected cash (o"s)• *e ight accept a “#ad” project)• *e ight reject a “good” project)

– Projected vs) Actual cash (o"s – +,+O -gar#age in gar#age out. – Capital #udgeting is NO/ an entirely

echanical process)

2

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 3/29

WACC & Project RiskExpected

Ret

urn (%)

Beta

SML

WACC

= !%

= "%#ncorrect

acceptance

#ncorrect

rejection

B

A$!

R f=

A = '$

ir* = '

B = '+

If a firm uses its WACC to make accept/reject decisions for all types ofprojects, it will hae a tendency toward incorrectly acceptin! riskyprojects and incorrectly rejectin! less risky projects"

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 4/29

/ypes o' Risk

• 0tand alone risk1 0tand alone risk iseasured #y the varia#ility o' the project#se2pected return)

• Corporate or "ithin34r risk1 Corporate riskis easured #y the project#s ipact onuncertainty a#out the 4r#s 'utureearnings)

• 5arket6 or #eta6 risk1 5arket risk iseasured #y the project#s eect on the4r#s #eta)

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 5/29

8uanti'ying Risk and itsAppraisal

• Risk is the varia#ility o' possi#le outcoes• Assuption o' independence

– No causative relationship #et"een cash (o"s 'ro periodto period

– Risk3'ree rate 'or discounting• ,solate the tie value o' oney

– 0tandard deviation o' the pro#a#ility distri#ution o' NPVs

• 9:

( )∑= +

=n

t t

f

t

R

A NPV

0 1

( )∑= +

n

t t

f

t

R

σ

02

2

1

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 6/29

0tandardi;ing the<ispersion

• Assess the pro#a#ility o' adversity

• <eterining pro#a#ilities o' adverseevents

– Consult the noral pro#a#ility distri#utionta#le

– E2press dierences 'ro the ean inters o' standard deviations to deterine

the pro#a#ility

• %undaental 'or a realistic assessent

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 7/29

,n'oration +enerated

• Pro#a#ility distri#ution o' ,RR – Copute the ean and standard deviation

• Nonnoral distri#ution

• Biases in o#taining in'oration – Adjustent 'or #iases

• Pro#les – Over3adjustent

– Accounta#ility – Results depends on #ehavioral considerations

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 8/29

<ependence o' Cash %lo"s-C%s. over /ie

• Conse=uence o' C%s #eing correlated overtie – Per'ect correlation

• C%s deviate in e2actly the sae relative anner• >inear 'unction

– 5oderate correlation• ?se a series o' conditional pro#a#ility distri#utions

• /ake account o' the correlation o' C%s over tie

σ = σ

t

1+Rf ( ) t

t =0

n

∑

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 9/29

/otal Risk 'or 5ultiple,nvestents

• /otal risk

– /he su o' systeatic and unsysteatic

risk

• 0tandard deviation -0<.

• Correlation #et"een projects

• %easi#le co#inations and doinance

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 10/29

0tandard <eviation

• <epends on – <egree o' correlation #et"een various

projects

• !igher the degree o' positive correlation thegreater the 0< o' the port'olio

– 0< o' possi#le NPVs o' each project

• +reater the 0< o' individual projects the

greater the 0< o' the port'olio

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 11/29

Correlation Bet"eenProjects

• Range o' correlation

– Bet"een @ and )@@

– >ack o' negatively correlated projects

• ?nrelated lines o' #usiness tend tohave lo" degrees o' correlation

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 12/29

%easi#le Co#ination and<oinance

• Evaluating 'easi#le co#inations

– <eterine "hich co#inationsdoinate in NPV andor 0<

– <eterines the ecient 'rontier

• Relation to e2isting port'olio

– ,nvestent proposals can #eeliinated #ecause they are doinated

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 13/29

Real Options in Capital,nvestents

• Valuation in general

• /ypes o' option – Option to vary output

– Option to a#andon

– Option to postpone

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 14/29

Valuation in +eneral• Real options

– Enhance the "orth o' a project – <icult to value

• <ecision trees• 0iulations• Ad hoc approaches

• Project "orth NPV D option value• As the nu#er o' options increases – ?ncertainty increases – Option value increases – Project#s "orth increases

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 15/29

/he Option to E2pand

• ?sing a decision tree – E2pected NPVs 'or the various #ranches

– 0e=uence o' decisions and chance events

– Optial set o' decisions• Rolling #ack the tree

• Back"ard induction

– Coparing NPVs• Optial decision at the 4rst decision point

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 16/29

/he Option to A#andon

• Provides a sa'ety net

• Consists o' – 0elling the asset

or

– Eploying the asset in another area

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 17/29

Econoic Rationale 'orA#andonent

• 0ae as capital #udgeting

• Project "orth NPV "ithout a#andonent D Value o' a#andonent option

• A#andon a project – ,' the PV o' possi#le 'uture #ene4ts

current a#andonent value – Appears #etter no" than in the 'uture

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 18/29

• Abandonment Option MakesSituation Better

– A signi4cant iproveent occurs• A portion o' the do"nside is eliinated

"hen events turn un'avora#le

– A#andonent is ore valua#le

• /he greater the volatility o' C%s – A#andonent itigates the eects o'

#ad outcoes

• Ongoing Abandonment

Evaluations – Optial tie to a#andon

– Continual assessent o' projects

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 19/29

/he Option to Postpone or /ie

• O#tain ne" in'oration – 5arket – Prices

– Cost• +ive up

– ,nteri C%s – %irst over advantage

• Coodity situation• Noncoodity situation

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 20/29

%inal O#servations on RealOptions

• Real options are dierent 'ro 4nancialoptions – Cannot use risk neutrality

–E2ercise price can change over tie – Volatility is dicult to easure

– ,precise opportunity cost

– 5ore dicult to value

• Recognition o' anageent (e2i#ility

• 5ore uncertainty is a positive "ith real options

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 21/29

/echni=ues 'or easuringstand alone risk

1. Sensitivity Analysis

2. Scenario Analysis

3. Monte Carlo Simulation Analysis

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 22/29

“*hat ,' ”1 0ensitivityAnalysis

• 0ho"s ho" changes in one input varia#le aect NPV or ,RR)

• All varia#les6 e2cept the one o' interest6 are 42ed) Change onevaria#le to see eect on NPV or ,RR)

• Ans"ers “"hat i' ” =uestions6 e)g)6 “"hat i' sales decline #y :FG$”

• Advantages

– Provides rough easure o' stand3alone risk)

– ,denti4es “dangerous” varia#les)

• <isadvantages

– <oes not re(ect diversi4cation)

– 0ays nothing a#out the likelihood o' the change in the

varia#le) – ,gnores relationships aong varia#les)

22

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 23/29

“*hat ,' ”1 0cenario

Analysis• E2aines several discrete scenarios6 usually a"orst case6 #est case6 and ost likely case)

• Brackets the range o' likely outcoes)

• Advantages – Provides use'ul in'oration on a project#s stand alone

risk #y sho"ing the range o' likely outcoes)

• <isadvantages

– Only a 'e" discrete outcoes are considered)

– Assues input varia#les are per'ectly correlated -e)g)6all the #est or "orst things "ill happen at the saetie.) /his leads to overstateent o' the e2trees)

23

“*hat ,'”1 0iulation

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 24/29

“*hat ,' ”1 0iulationAnalysis

• /echni=ue in "hich pro#a#le 'uture events are siulated on a

coputer)• 5odel the project that sho"s the relationship #et"een NPV

and paraeters and e2ogenous varia#le)

• 0peci'y the values o' the paraeter and the pro#a#ilitydistri#ution o' the e2ogenous varia#le)

• Pro#a#ility distri#utions are selected 'or the input varia#les) /he coputer dra"s rando nu#ers 'ro the speci4eddistri#utions to siulate 'uture levels o' sales6 e2penses6 etc)

• /he process is repeated a large nu#er o' ties -6@@@D. andthe average NPV and standard deviation are deterined)

• Advantages

– Re(ects pro#a#ilities o' 'uture inputs) – Provides e2pected NPV and standard deviation #ased on

input pro#a#ilities and relationships aong inputs)

• <isadvantages1Pro#a#ility distri#utions are su#jective)No true decision rule)

5ay look ore accurate than it really is)24

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 25/29

<ecision /ree Analysis• ?se'ul in evaluating projects "ith capital outlays ade

over several years)

– At t@H Conduct a Rs)F@6@@@ 'easi#ility study on theuse o' ne" underground natural gas storage technology)

– At tH 0pend Rs))F illion 'or a pilot projectdeonstrating the ne" technology)

– At tIH ,nvest Rs)7F illion in a 'ull scale undergroundstorage 'acility)

– At t7H 0pend Rs)I@ illion to e2pand the e2isting'acility)

25

,easi-i.it/

Stud/

(! 0)

Pi.otProject

('! M)

,u..1Sca.e

,aci.it/

(! M)

Expansion

( M)

Stop

Stop

Stop

s n ap a

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 26/29

s n ap aBudgeting

• *hat does “risk” ean in capital #udgeting$ – ?ncertainty a#out a project#s 'uture

pro4ta#ility) – 5ay #e easured #y σNPV6 σ,RR6 or the

project#s #eta) – *ill the project increase the 4r#s and

shareholder#s risk$ – Risk analysis ay soeties

incorporate historical data #ut're=uently is #ased on su#jective

judgeents)• /ypes o' risk

– 0tand3alone risk – Corporate risk – 5arket risk

26

,ncorporat ng R s nto

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 27/29

,ncorporat ng R s ntoCapital Budgeting

• /he Certainty E=uivalent 5ethod – Estiate the certainty e=uivalent cash

(o"s 'or each period) – <iscount at the risk3'ree rate to get NPV)

• /he Risk3Adjusted <iscount Rate5ethod -RA<R. – Estiate a discount rate that re(ects the

riskiness o' the project#s cash (o"s)

– <iscount the estiated cash (o"s at therisk3adjusted rate to get NPV) – <eterining risk3adjusted rates1

• . /he “pure play” ethod• :. 0u#jective approach• J. <ivisional cost o' capital

27

ore on e ure ay

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 28/29

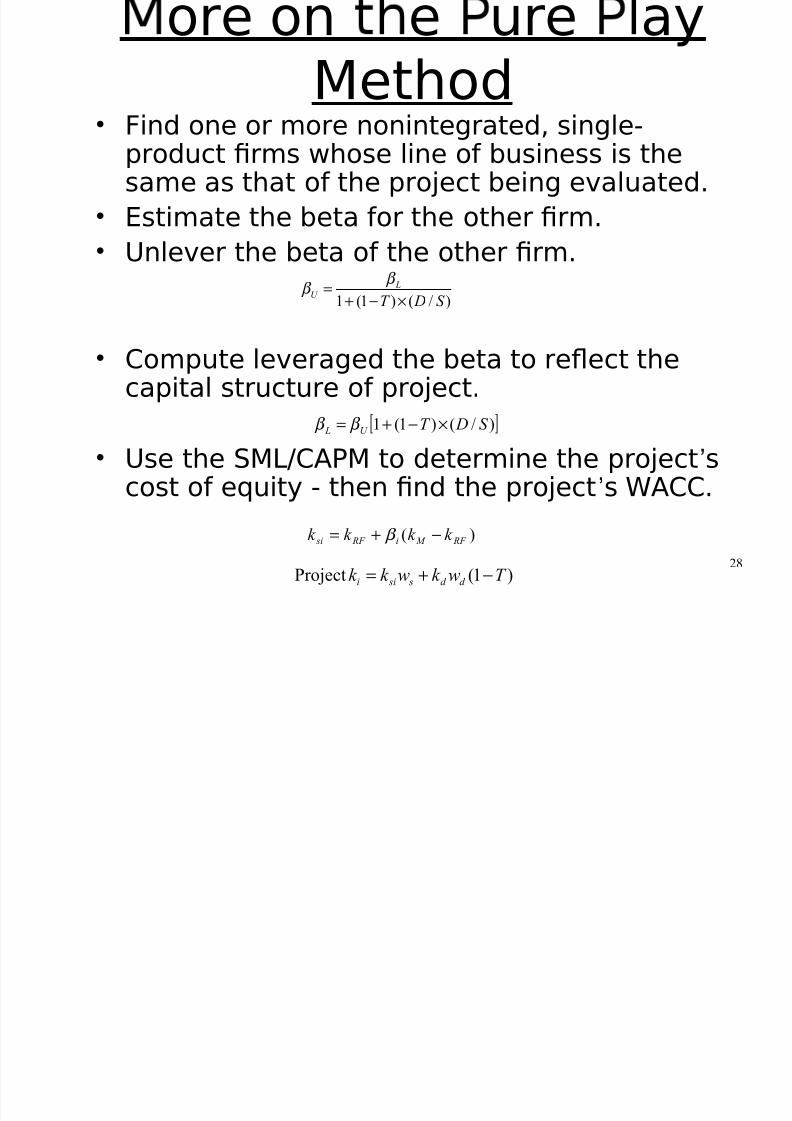

ore on e ure ay5ethod

• %ind one or ore nonintegrated6 single3product 4rs "hose line o' #usiness is thesae as that o' the project #eing evaluated)

• Estiate the #eta 'or the other 4r)

• ?nlever the #eta o' the other 4r)

• Copute leveraged the #eta to re(ect thecapital structure o' project)

• ?se the 05>CAP5 to deterine the project#scost o' e=uity 3 then 4nd the project#s *ACC)

28

)/()1(1 S DT

LU

×−+

= β β

[ ])/()1(1 S DT U L ×−+= β β

)( RF M i RF si k k k k −+= β

)1(Project T wk wk k d d s sii −+=

/he !oe <epot1 A 0ensitivity Analysis

7/24/2019 Lecture Capbud Risk

http://slidepdf.com/reader/full/lecture-capbud-risk 29/29

/he !oe <epot1 A 0ensitivity Analysis

/he 'ollo"ing is an analysis o' ane" store #eingconsidered #y the !oe <epot6 "ith the 'ollo"ing

assuption governing the #ase case1• ,nitial ,nvestent in the store Rs) :)F illion

• E2pected li'e o' the store @ years

• 0alvage Value o' the store preises at the end o' @years Rs) F)F illion

• E2pected Revenues s=uare 'oot in the 4rst year Rs)J@@ s=uare 'ootH +ro"th rate FGH

• Pre ta2 operating argin -EB,/0ales. @G

• *orking capital as a percentage o' Revenue @GH

investent is at the #eginning o' each period andcopletely salvagea#le at the end o' the project li'e)

• /he depreciation each year is coputed using 5ARC0depreciation rates)

•/he corporate ta2 rate is JKGH the cost o' capital is: FG