learning area 5 chapter 8 financial statements. explain the purpose of and be able to prepare a...

TRANSCRIPT

Learning Area 5Chapter 8 Financial Statements

Explain the purpose of and be able to prepare a simple: Income statement Balance sheet Statement of changes in equity Cash flow statement (understand & interpret)

Understand how to apply the accounting concepts (page 2)

Objectives

Two parts Assets (everything owned by business) How these assets were financed (Equity and

liabilities) “Snapshot” of events at a point in time Balance sheet equation:

Assets = Equity + Liabilities Balance sheet per p4 (know format!!!)

1. Statement of financial position p3

Asset is a resource or inflow of economic benefits Non-current asset = fixed assets (property) Current assets = debtors / cash / inventory Non-current asset usually long economic lives (>= 12 months)

Tangible assets: Touch Examples: Vehicles, Machinery, Property Measured: Cost – accumulated depreciation Revaluation of property…, still depreciated Not all depreciate in value i.e. land has infinite life (revalue)

1.1 Non-current assets p5

Intangible assets: Assets that cannot be touched Example: Goodwill = Sale price of company A – Net book value of company A (net book value: total assets – total liabilities = equity)

Research and development cost Concessions, patents – right over product or discovery Trade marks, brand names – MacDonald's However IAS 38 claims …. “internally generated not an

asset”

1.1 Non-current assets p6

Investments Interest in other companies: shares, loans,

debentures etc. Measured: Market value, (refer cost concept

chapter 7 – see why we did the accounting concepts??!!! )

1.1 Non-current assets p7

Cash and items convertible into cash in the normal course of business (< 12 months)

Inventories Stock: Raw materials, Work-in-progress,

consumables, finished goods Measured: Lower of cost and net realisable

value

1.2 Current assets p7

Trade receivables (Debtors) Amounts owed by customers Measured: ‘Cost’ – Provision for doubtful

debts…Take into account possible losses

due non-payment Other current assets

E.g. Short term investments in money market fund or fixed deposit (less than 1 year)

1.2 Current assets p8

Amount contributed by the shareholders (Share capital and share premium) and earned by the shareholders (Retained earnings / reserves)

Assets – liabilities = Equity Comprises:

Share capital Reserves:

Share premium Revaluation reserve (example property revalued)

Retained earnings

1.3 Equity p8

Liability = Finance by third parties, therefore amounts payable / owed to third party

Net current assets (working capital) = CA – CL Indicate the liquidity of the business

1.4 Liabilities p9

Current liabilities (< 12 months) Trade payables (creditors)

Measured: face value (cost) Short-term borrowings (overdraft)

Measured: amount actually overdrawn Current portion of long-term borrowings

Portion repayable within one year (< 12 months)

Current tax payable

1.4 Liabilities p9

Non current liabilities Due >12 months Long-term borrowings

Medium-term loans, hire purchase liability and finance leases

Long-term provisions Estimated liabilities Provision for claims incurred but not yet reported (IBNR)

Contingent liabilities Potential liability, not likely: Disclose per Notes

1.4 Liabilities p10

Question 8.4 Solution Blank.docxQuestion 8.4 Solution.docx

Question 8.4 p11

Income statement – part of statement of comprehensive income… revenue until profit after tax

Other comprehensive income – only “gains on revaluation” part is examinable

Income statement: Insight into activities and profits Over a period of time (12 months) P13 (know format by hard!!!)

2. Statement of comprehensive income p12

Revenue can be sales / income from services rendered

Also called turnover or sales Recognised when earned in accordance with

realisation concept

2.1 Revenue p13

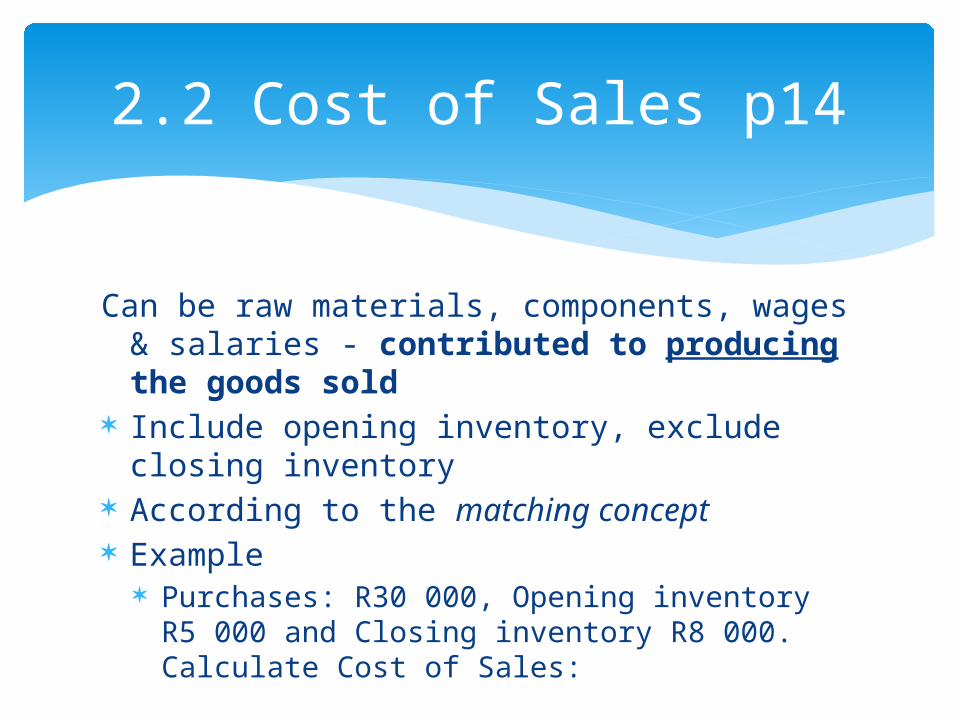

Can be raw materials, components, wages & salaries - contributed to producing the goods sold

Include opening inventory, exclude closing inventory

According to the matching concept Example

Purchases: R30 000, Opening inventory R5 000 and Closing inventory R8 000. Calculate Cost of Sales:

2.2 Cost of Sales p14

Distribution costsCosts associated with sales, distribution and

advertising Example: Delivery vehicle

Administrative expensesWages & salaries, directors’ remuneration

Not strictly related to production…Indirect costs (“overheads”)

Distribution costs & Administrative expenses

Finance income Income from Investments e.g. rent from

property, interest, dividends

Finance Costs Interest payments on loans Why disclose?

Finance income & Finance cost

As calculated per tax notes (do later in May) Why not Profit x 28%?

Depreciation vs Capital allowances Provision for doubtful debts Prohibited expenses and losses Assessed losses from previous years

Tax expense p15

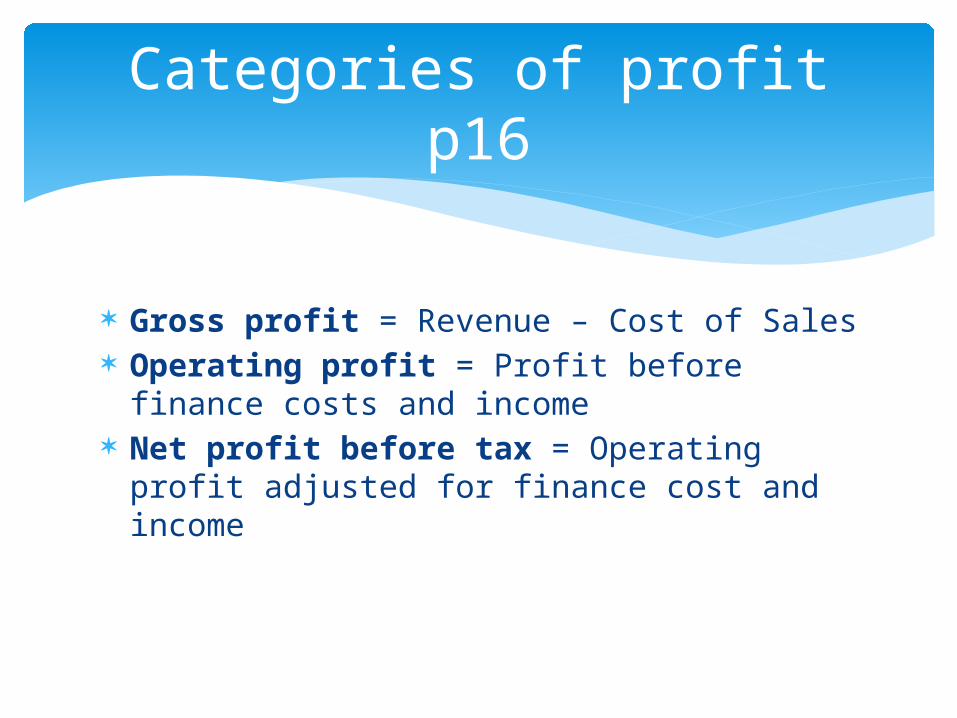

Gross profit = Revenue – Cost of Sales Operating profit = Profit before finance

costs and income Net profit before tax = Operating profit

adjusted for finance cost and income

Categories of profit p16

EPS = Earnings attributable to ordinary shareholders / number of ordinary shares

Earnings attributable to ordinary shareholders: If no preference shares: Profit after tax If pref shares: Profit after tax – dividends

payable to pref shareholders

Earnings per share p16

Revaluation of non-current assets – Effect: Non-current asset Increase Revaluation reserve increase

Increase reflect as ‘gain on revaluation’ in the other comprehensive income

Example: Land: Cost = R560 000, Revalued to R780 000.

Revaluation of assets held as an investment “gains from investments” per other comprehensive

income

Other comprehensive income – Revaluation (p17)

Downward revaluation: Expense in the income statement unless it

reverse a previous upward revaluation surplus Asset sold:

Realised gain/loss: Income statement

Other comprehensive income – Revaluation (p19)

Solution 8.6.docx

Question 8.6

Question 8.1 p6 Intangible assets Question 8.3 p11 Classification: Balance

sheet Work through Question 8.5 p14 Cost of Sales

and Question 8.6 p19 Income Statement again

Homework

The purpose of the cash flow statement is to show cash movements and liquidity of company

Gives insight to the following: Why did bank balance not increase

/decrease in correlation with profitability? Can company generate sufficient cash? What did company do with loan taken out

during the year?

3. Cash Flow Statement (p20)

Cash vs Profit

Income statement recognises depreciation and credit sales which is not a flow of funds

Cash flow statement ignores the accruals concept

3. Cash Flow Statement (p21)

Profit Cash

Purchase non-current asset for cash

- Decrease

Increase depreciation charge

Decrease -

Revaluation of inventory (upward)

Increase -

Paying tax - Decrease

Paying dividends - Decrease

Question 8.8 (p22)

Profit Cash

Selling goods on credit (above cost price)

Increase -

Purchase of raw material on credit

Lower -

Issue of loan capital or new shares for cash

- Increase

Selling an investment (zero capital gain)

- Increase

Question 8.8 (p22)

3 Sections: CF from operating activities – reconciles

profit before tax to cash from operating activities

CF from investing activities – disposal and acquisition of long term assets and investment income

CF from financing activities – changes in size of equity and loans (share issues, repayment of loans etc.)

Cash flow statement: Structure (p24)

Net cash generated from operating activities (p25)

Operating profitAdjustments for:

- Depreciation - Decrease/(Increase) in inventory level- Decrease/(Increase) in trade and other receivables- Increase/(decrease) in trade and other payables

Cash generated from operations

Tax and interest to be deducted for ‘Net cash generated from operations’

33 000

18 000(7 000)

(1 500)(9 400)33 100

Investing & Financing Activities

Investing activities Buy or sell fixed

assets (property and plant)

Interest or dividends from investments

“Liquid assets” such as short-term investments in securities

Financing Activities Dividends to

shareholders Cashflows arising:

o repayment of loans o new borrowing o issue of shares

Solution Q8.10.docx

Question 8.10HOMEWORK

Reconciles all equity accounts’ opening balances to closing balances

Example p28 Example - Statement of changes in equity.docx

Dividends What is dividends? Proposed by directors on annual general

meeting

Statement of changes in equity p28

Notes will cover: Detailed disclosures and explanatory

information Accounting policies Post balance sheet events …true and fair view of the position of the

company

Notes to the accounts p30

Be able to: Explain the importance of each statement,

and explain the different elements on the statements

Compile the various statements Explain the difference between profit and

cash

What to expect in a test/exam…

Question 8.7 & 8.9 & 8.10Cash flow statement

Question 8.11Statement of changes in equity

Solution 8.11 Changes in equity.docx

HOMEWORK

My consultation hours:Wednesdays: 9h3o till 12hooThursdays: 14h30 till 16h15

PLEASE NOTE!!

Date: Friday 7 March 2014 Time : 16:00 Total : 40 marks Duration: 1 hour Venue: Centenary 1 & 2 Scope: Chapters 1; 2; 7; 8 and 9

(Learning areas: 1; 2; 4; 5 and 6)

Semester test 1