leading the way - av.sc.com

TRANSCRIPT

in Asia, Africa and the Middle East

Leading the way in A

sia, Africa and the M

iddle East

Annual Report and Accounts 2009-2010

Annual R

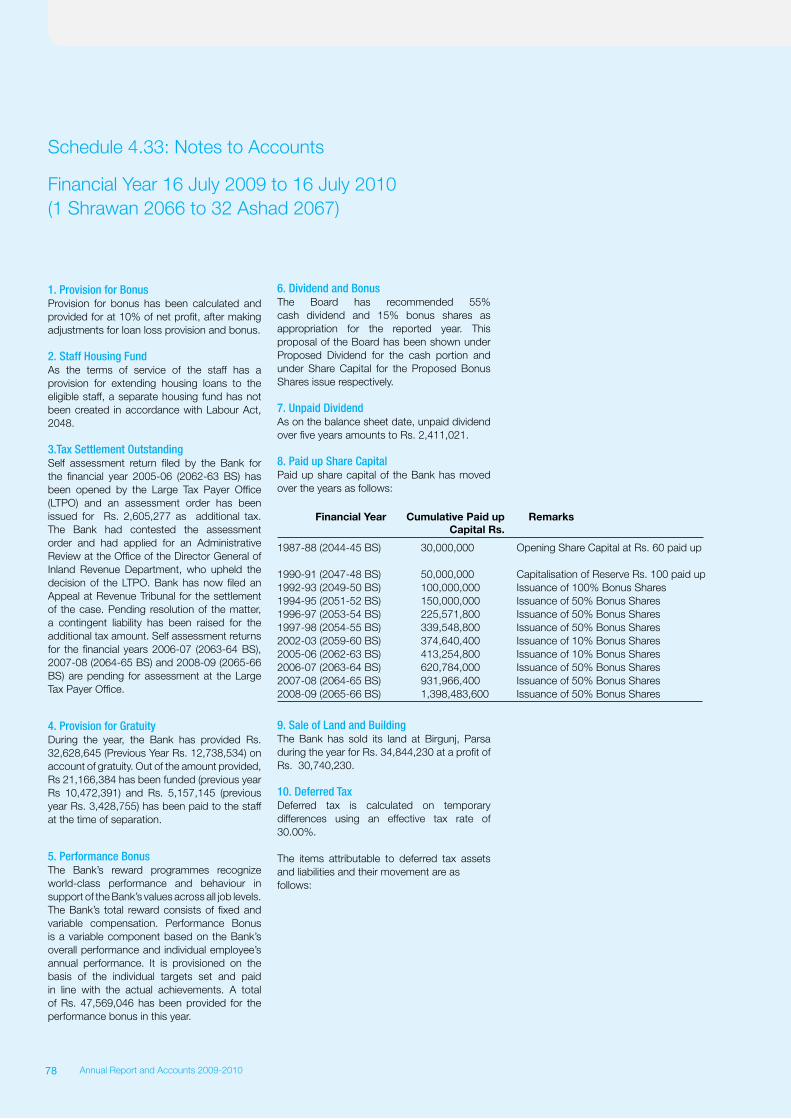

eport and Accounts 2009-2010

Leading the way

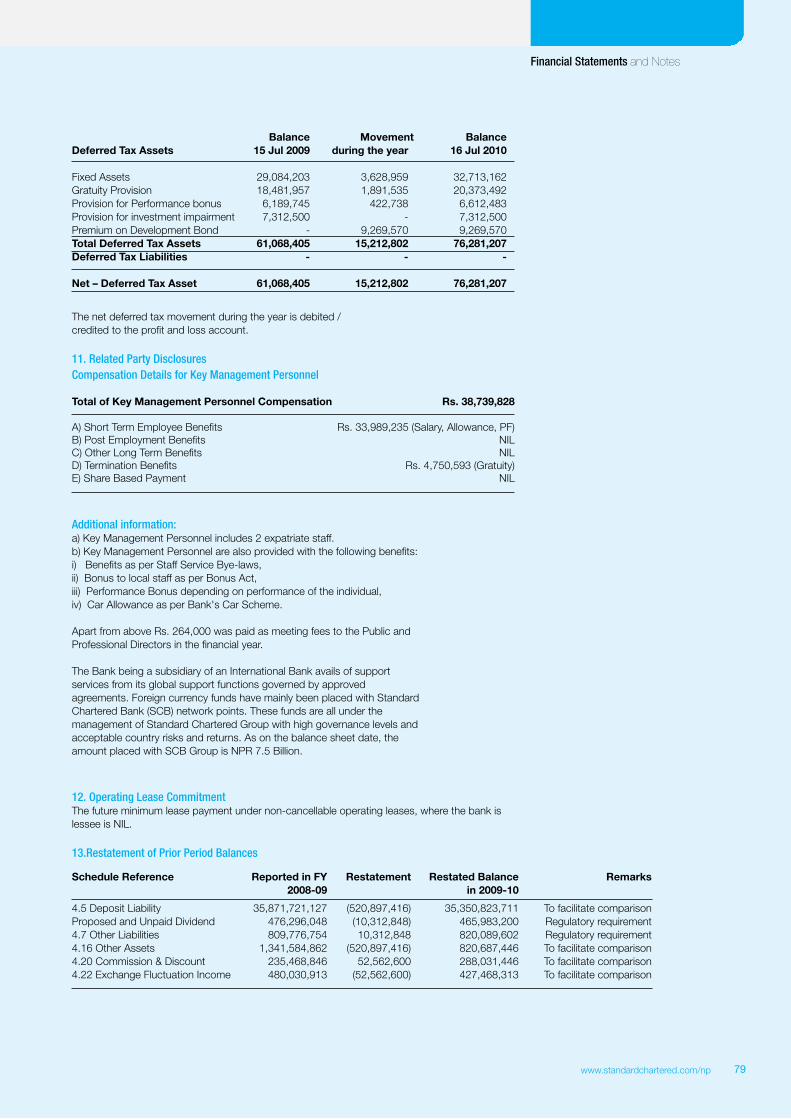

Our performance

Financial highlights

FYE 2009/10

Non-fi nancial highlights

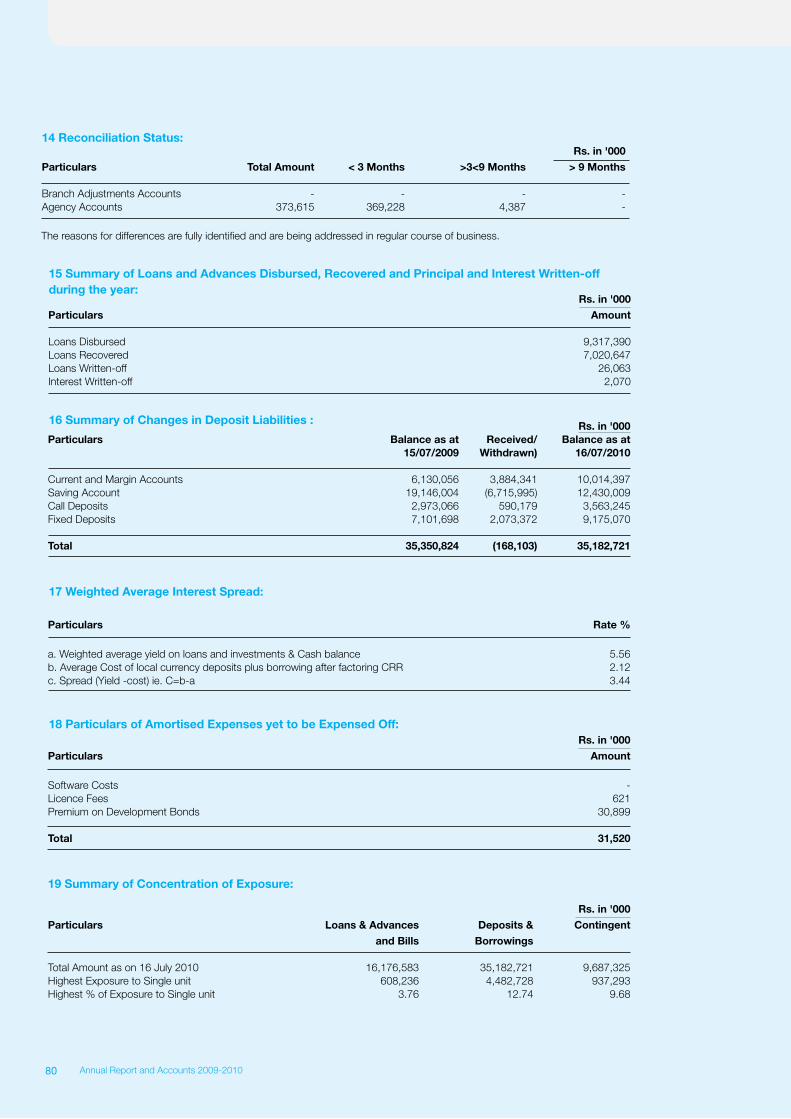

Operational highlights

2298m

14.60%

1612m

42918

32.22%

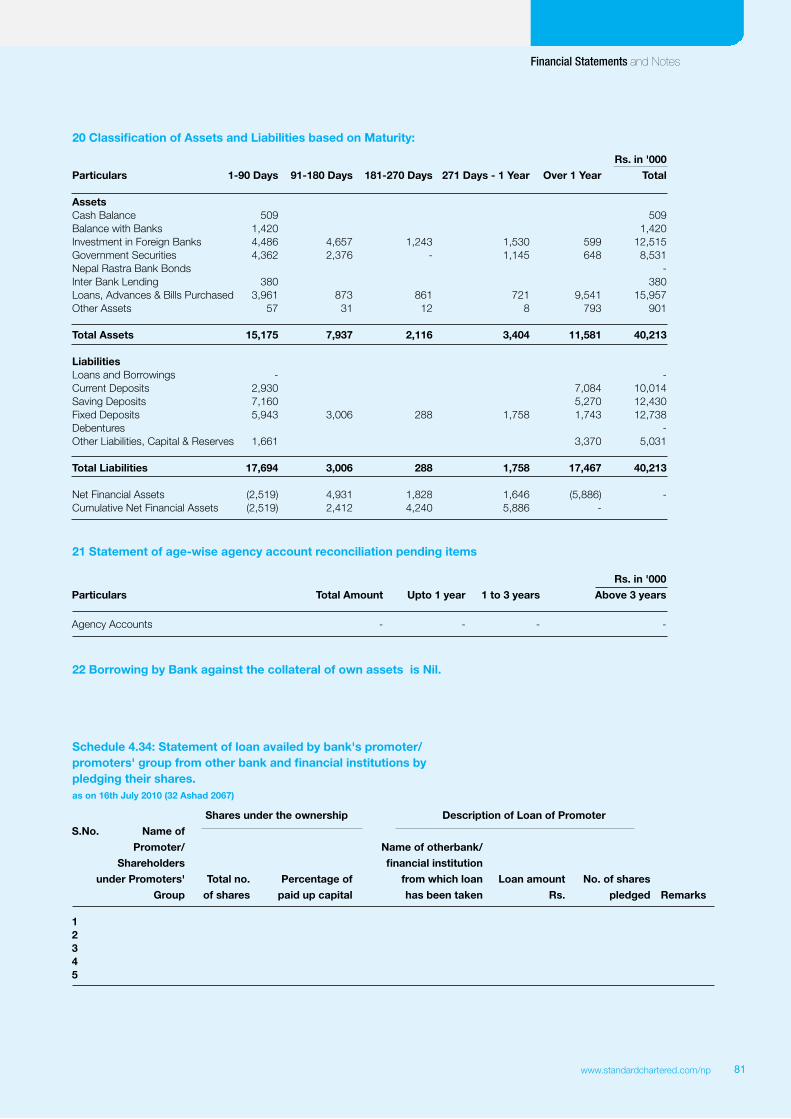

40,213m

70%

Operating Income

(in NPR where applicable)

Points of representation

Capital Adequacy

Operating Profi t

Employees

Return on equity

Total Assets

Dividend

Stable Income Growth

Stable Profi t Growth

Robust balance sheet

Sound capital base

Sound risk management

Sustainable business

(IncludingBonus Shares)

Disclaimer

Standard Chartered Bank Nepal Limited is an Equal Employment Opportunity/ Affi rmative Action employers. Standard Chartered Bank Nepal Limited is committed to providing equal employment opportunities to every employee and every applicant for employment, regardless of, but not limited to, such factors as race, color, religion, sex, age, familial or marital status, ancestry, sexual orientation, veteran status or being a qualifi ed individual with a disability; within the legal framework of the country.

Standard Chartered Bank Nepal Limited undertakes no obligation to update any statement in this Annual Report 2009-2010 to refl ect events or circumstances after the date on which such statement is made. Information in this Annual Report is as of July 16, 2010.

Designed & Processed by: PowerComm, 5552987, Printed in Nepal

1www.standardchartered.com/np

About UsStandard Chartered Bank Nepal Limited has been in operation in Nepal since 1987 when it was initially

registered as a joint-venture operation. Today the Bank is an integral part of Standard Chartered Group

having an ownership of 75% in the company with 25% shares owned by the Nepalese public. The

Bank enjoys the status of the largest international bank currently operating in Nepal.

Standard Chartered Bank Nepal Limited has been in operation in Nepal since 1987 when it was initially registered as a joint-venture operation. Today the Bank is an integral part of Standard Chartered Group having an ownership of 75% in the company with 25% shares owned by the Nepalese public. The Bank enjoys the status of the largest international bank currently operating in Nepal.

Standard Chartered PLC is a leading international bank, listed on the London, Hong Kong and Mumbai stock exchanges. It has operated for over 150 years in some of the world’s most dynamic markets and earns more than 90 per cent of its income and profits in Asia, Africa and the Middle East. This geographic focus and commitment to developing deep relationships with clients and customers has driven the Bank’s growth in recent years.

With 1,700 offices in 70 markets, Standard Chartered offers exciting and challenging international career opportunities for more than 80,000 staff. It is committed to building

a sustainable business over the long term and is trusted worldwide for upholding high standards of corporate governance, social responsibility, environmental protection and employee diversity. The Bank’s heritage and values are expressed in its brand promise, ‘Here for good’.

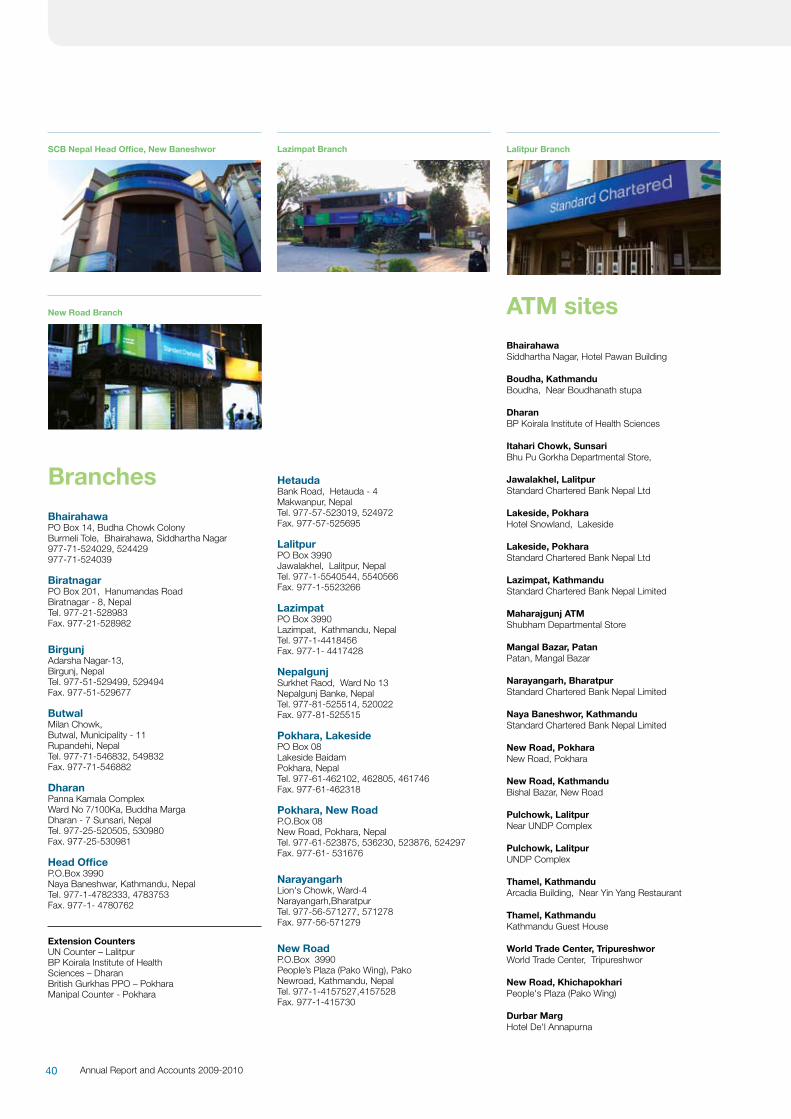

With 18 points of representation, 23 ATMs across the country and with more than 400 staff, Standard Chartered Bank Nepal Ltd. is in a position to serve its customers through an extensive domestic network. In addition, the global network of Standard Chartered Group gives the Bank a unique opportunity to provide truly international banking services in Nepal.

Standard Chartered Bank Nepal Limited offers a full range of banking products and services in Wholesale and Consumer banking, catering to a wide range of customers encompassing individuals, mid-market local corporates, multinationals, large public sector companies, government corporations, airlines, hotels, SME’s as well as the DO segment comprising of embassies, aid agencies, NGOs and INGOs.

The Bank has been the pioneer in introducing ‘customer focused’ products and services in the country and aspires to continue to be a leader in introducing new products in delivering superior services. It is the first Bank in Nepal that has implemented the Anti-Money Laundering policy and applied the ‘Know Your Customer’ procedure on all the customer accounts.

Corporate Social Responsibility is an integral part of Standard Chartered’s ambition to become the world’s best international bank and is the mainstay of the Bank’s Values. Standard Chartered throughout its long history has played an active role in supporting those communities in which its customers and staff live. It concentrates on projects that assist children, particularly in the areas of health and education. Environmental projects are also occasionally considered. It supports non-governmental organisations involving charitable community activities The Group launched two major initiatives in 2003 under its ‘Believing in Life’ campaign- ‘Living with HIV/AIDS’ and ‘Seeing is Believing’.

2 Chairman’s Statement8 CEO & Director’s Report14 Our Approach to Corporate

Responsibility20 Here for people, Here for good People Strength:

Business review overview Corporate Governance Financial Statements and Notes

41 Auditor’s Report42 Balance Sheet43 Profit & Loss Account44 Profit & Loss Appropriation Account45 Statement of Changes in Equity46 Cash Flow Statement47 Schedules76 Significant Accounting Policies78 Notes to Accounts83 Disclosure as per Bank’s disclosure

policy under the Basel –II Capital Accord of Nepal Rastra Bank

86 Nepal Rastra Bank’s Approval and Directions

87 Five Years Financial Summary

26 Our Approach to Corporate Governance32 Additional Information36 Board of Directors38 Management Team40 Branches and ATM’s

Annual Report and Accounts 2009-20102

Chairman’s Statement

“ Our in-depth understanding of this market, ability to quickly adapt to the changing landscape and the flair of our management to execute Bank’s strategy has played a crucial role in achieving a sustained growth. ”

– Neeraj Swaroop, Chairman

It is with great pleasure I report that Standard Chartered Bank Nepal Limited has once again maintained its track record of consistent performance and has registered an impressive result for the fiscal year ended 16 July 2010. Delivering record results in this challenging economic and socio-political environment is indeed a commendable accomplishment. The foundation of success has been built mainly on our ability to follow a consistent strategy and focus of business in the areas of our strength.

During the year under review, the Bank gave continuity to its projects involving footprint expansion. A Branch as well as three new ATMs were added during the year. We also launched various innovative products both under Consumer and Wholesale Banking. These steps have had a positive bearing on our overall performance.

During our presence in Nepal for over twenty three years, we have been able to consolidate our position by effectively blending our global capability, deep local knowledge and creativity to outperform our competitors. This ability has helped us to serve our customers well, it also makes us part of their community. Our in-depth understanding of this market, ability to quickly adapt to the changing landscape and the flair of our management to execute Bank’s strategy has played a crucial role in achieving a sustained growth.

Against the back-drop of a rapidly changing world, we have been working very closely with our people, customers, regulators, industry and the community. This has provided us with enormous strength to successfully handle the changing business & economic environment encompassing the country.

3www.standardchartered.com/np

Business review overview

I would like to reiterate that our brand is the most valuable asset which is at the heart of our strategic intent i.e, to be the world’s best international Bank, leading the way in Asia, Africa and the Middle East. Recent launch of our new brand promise `Here for good’ has given our brand a new dimension. While the Bank now has a new brand promise, `Here for good’ is, in reality, its oldest belief. It is what we have been doing for the past 150 years, and its aims for the next. It complements the Bank’s strategy, and also its values – Trustworthy, International, Responsive, Courageous and Creative. This renewed thrust and commitment will ensure Standard Chartered to continue to remain the best brand in this market.

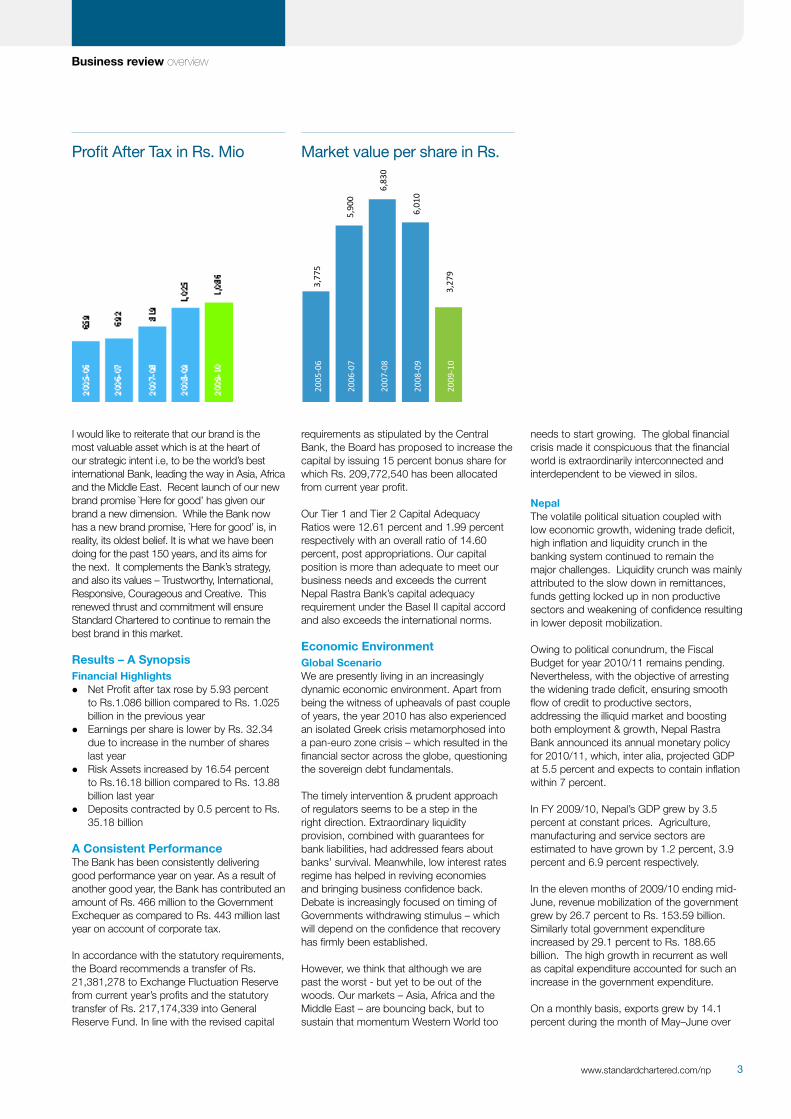

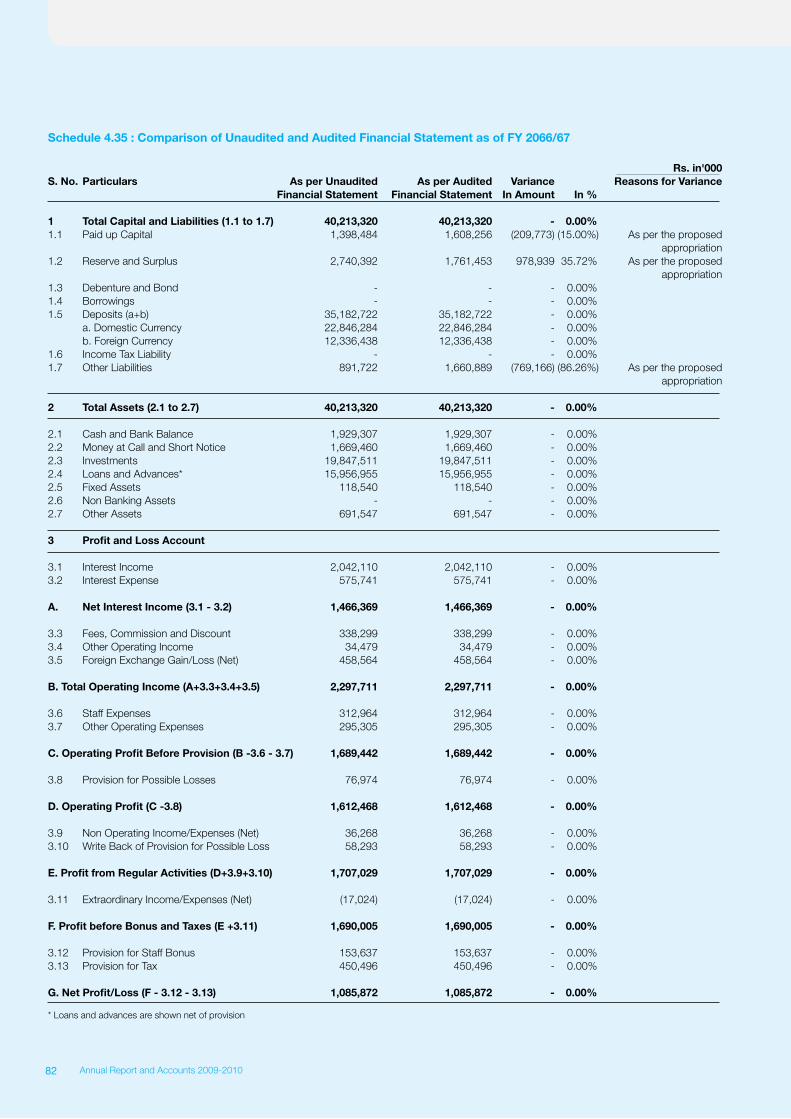

Results – A Synopsis Financial Highlights Net Profit after tax rose by 5.93 percent

to Rs.1.086 billion compared to Rs. 1.025 billion in the previous year

Earnings per share is lower by Rs. 32.34 due to increase in the number of shares last year

Risk Assets increased by 16.54 percent to Rs.16.18 billion compared to Rs. 13.88 billion last year

Deposits contracted by 0.5 percent to Rs. 35.18 billion

A Consistent PerformanceThe Bank has been consistently delivering good performance year on year. As a result of another good year, the Bank has contributed an amount of Rs. 466 million to the Government Exchequer as compared to Rs. 443 million last year on account of corporate tax.

In accordance with the statutory requirements, the Board recommends a transfer of Rs. 21,381,278 to Exchange Fluctuation Reserve from current year’s profits and the statutory transfer of Rs. 217,174,339 into General Reserve Fund. In line with the revised capital

requirements as stipulated by the Central Bank, the Board has proposed to increase the capital by issuing 15 percent bonus share for which Rs. 209,772,540 has been allocated from current year profit.

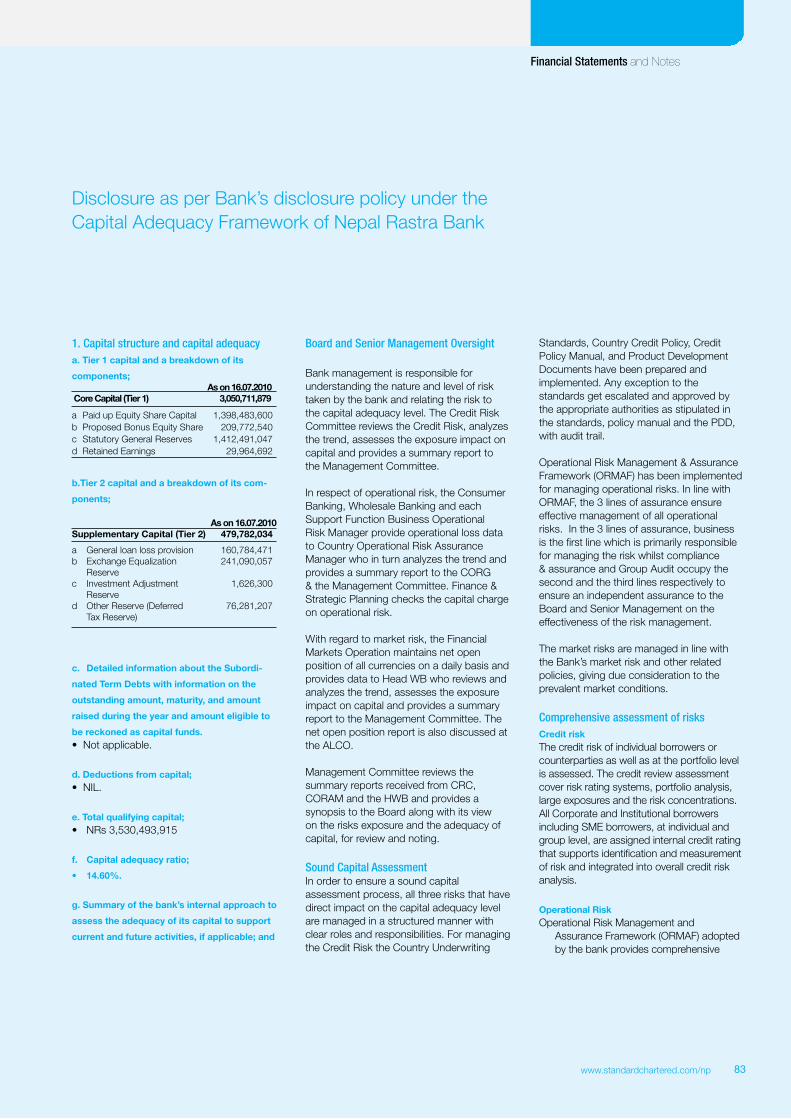

Our Tier 1 and Tier 2 Capital Adequacy Ratios were 12.61 percent and 1.99 percent respectively with an overall ratio of 14.60 percent, post appropriations. Our capital position is more than adequate to meet our business needs and exceeds the current Nepal Rastra Bank’s capital adequacy requirement under the Basel II capital accord and also exceeds the international norms.

Economic EnvironmentGlobal ScenarioWe are presently living in an increasingly dynamic economic environment. Apart from being the witness of upheavals of past couple of years, the year 2010 has also experienced an isolated Greek crisis metamorphosed into a pan-euro zone crisis – which resulted in the financial sector across the globe, questioning the sovereign debt fundamentals.

The timely intervention & prudent approach of regulators seems to be a step in the right direction. Extraordinary liquidity provision, combined with guarantees for bank liabilities, had addressed fears about banks’ survival. Meanwhile, low interest rates regime has helped in reviving economies and bringing business confidence back. Debate is increasingly focused on timing of Governments withdrawing stimulus – which will depend on the confidence that recovery has firmly been established.

However, we think that although we are past the worst - but yet to be out of the woods. Our markets – Asia, Africa and the Middle East – are bouncing back, but to sustain that momentum Western World too

needs to start growing. The global financial crisis made it conspicuous that the financial world is extraordinarily interconnected and interdependent to be viewed in silos.

NepalThe volatile political situation coupled with low economic growth, widening trade deficit, high inflation and liquidity crunch in the banking system continued to remain the major challenges. Liquidity crunch was mainly attributed to the slow down in remittances, funds getting locked up in non productive sectors and weakening of confidence resulting in lower deposit mobilization.

Owing to political conundrum, the Fiscal Budget for year 2010/11 remains pending. Nevertheless, with the objective of arresting the widening trade deficit, ensuring smooth flow of credit to productive sectors, addressing the illiquid market and boosting both employment & growth, Nepal Rastra Bank announced its annual monetary policy for 2010/11, which, inter alia, projected GDP at 5.5 percent and expects to contain inflation within 7 percent.

In FY 2009/10, Nepal’s GDP grew by 3.5 percent at constant prices. Agriculture, manufacturing and service sectors are estimated to have grown by 1.2 percent, 3.9 percent and 6.9 percent respectively.

In the eleven months of 2009/10 ending mid-June, revenue mobilization of the government grew by 26.7 percent to Rs. 153.59 billion. Similarly total government expenditure increased by 29.1 percent to Rs. 188.65 billion. The high growth in recurrent as well as capital expenditure accounted for such an increase in the government expenditure.

On a monthly basis, exports grew by 14.1 percent during the month of May–June over

Profit After Tax in Rs. Mio Market value per share in Rs.

3,77

5

5,90

0

6,83

0

6,01

0

3,27

9

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

Annual Report and Accounts 2009-20104

the previous month. However, compared to the corresponding period of previous year, the exports have declined by 9.8 percent to Rs. 55.37 billion. The merchandise imports, on the other hand, grew by 35.2 percent to Rs. 342.99 billion.

Despite the rise in trade deficit, the Balance of Payment (BOP) improved gradually from a record high deficit of Rs. 23.53 billion in mid-March to Rs. 15.07 billion by mid-June. This is attributed to a surplus generated in the transfer account that includes grants, pension receipts and remittance. As a result, the level of gross foreign exchange reserve improved to Rs. 247.42 billion in mid-June which is sufficient for financing merchandise imports of 8.1 months and service imports of 6.8 months.

The year on year (y-o-y) inflation as measured by the consumer price index moderated to 9.6 percent in mid-June 2010 compared to 12.3 percent in the corresponding period last year.

In line with the appreciation of the Indian Rupees against the US dollar, the Nepalese currency vis-à-vis the US dollar appreciated by 4.62 percent in mid-June 2010 compared to mid-July 2009. Nepalese rupee has a fixed parity of 1:1.6 with the Indian Rupee. The exchange rate of one US dollar stood at Rs. 74.60 in mid-June 2010 compared to Rs. 78.05 in mid-July 2009.

The Year AheadSCB Nepal‘s prudent funding, liquidity and high asset quality policies have stood it in good stead during the difficult times. During this period, the bank remained adequately liquid to support the credit needs of the clients from both the businesses viz. Wholesale and Retail. We will continue to manage our balance sheet in a conservative manner, maintaining high liquidity and strong capital ratios.

We believe that great opportunities lie ahead as the government is committed to attain accelerated growth rate in the economy and contain inflation. Needless to mention, it will largely depend upon the political stability and the security environment. We have a firm belief that the financial services sector, in which we are a player, will continue to grow and develop into a major pillar of the Nepalese economy.

The agriculture sector, which is largely dependent upon the weather conditions, is likely to experience a setback because of the late arrival of monsoon this year. However, this is likely to be mostly compensated by the ongoing expansion of cultivation area and enhancement in distribution of inputs and services in the rural areas owing to improving security situation. The industrial sector is estimated to grow at an average pace in the coming year. For the fact that the government has reiterated its commitment to increase infrastructural expenditure and improvement in the operating environment, some stability in the economy can be envisaged.

The year 2011 is being celebrated as `Visit Nepal Year.’ This is expected to provide some momentum in the tourism related activities.

Corporate GovernanceGovernance across the Bank is robust. As you may all appreciate, banking is a relationship business. We highly value the relationships that we have with our people, regulators, clients and the other stakeholders; all efforts will be made to further deepen this relationship.

We are committed to ensuring the integrity of governance. In addition to the established committees, we have committees on Diversity and Inclusion, Health and Safety, the Environment, Outserve Plus and

Community Partnership. The initiatives taken by these committees have added value to our stakeholders and delighted them. We believe good governance provides clear accountabilities, ensures strong controls, instills the right behaviors and reinforces good performance.

Mr. Anurag Adlakha, Mr. Sushen Jhingan and Mr. Sujit Mundul nominated by the Standard Chartered Grindlays Australia and Mr. Ram Bd. Aryal as Professional/Independent Director continue to be in the Board of SCB Nepal Limited. I, Neeraj Swaroop, continue to represent the Standard Chartered Group on the Board of Standard Chartered Bank Nepal Limited.

As on the date of this report, the Board is made up of the Non-Executive Chairman, one Executive Director and four Non-Executive Directors of which one is professional /independent Director appointed as per the regulatory requirement. Director, Mr. Arjun Bandhu Regmi, representing the public shareholders, has submitted his resignation from the post of Public Director citing personal reasons and the same has been accepted in the 264th Board meeting of the Bank held on 5th July 2010. The Board is currently in the process of fulfilling the vacant post as per the provisions of the Companies Act. I would like to thank Mr. Arjun Bandhu Regmi for his contribution during his tenure as Public Director of the Bank.

In Conclusion The global economy in 2010 started looking better than it did a year ago. Our markets – and particularly Asia – are better placed than most parts of the world to weather the risks, but they are not immune; so we cannot remain complacent. We must appreciate that the policymakers in most part of Asia have been effective in responding to the twists and turns of the crisis. Whilst the economic

Earning Per Share in Rs. Return on Total Assets

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

175.

85

167.

37

131.

92

109.

99

77.6

5

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2.56

2.42 2.

46

2.56

2.70

5www.standardchartered.com/np

Business review overview

uncertainties continue, we start the year with a blend of caution and confidence.

Based on the data recently released by the government, economic indicators were just seen to be satisfactory during the review period. Key obstacles in resuscitating the weakening economy were seen to be the issues such as taming of inflation, creating investor-friendly environment and pushing the exports up to bridge the widening trade deficit. Despite the challenging situation, the Bank was able to record a satisfactory outcome due mainly to the commitment and focus exhibited by the management team in creating shareholders value.

Our top priority is to maintain our track record of delivering superior financial performance. To do this we need to sustain the momentum in both Wholesale and Consumer Banking. We are staying focused on the basics of banking; on the way we manage liquidity, capital, risks and costs. We are deepening our relationships by getting closer to our clients. We are also expanding the product capabilities and solutions we provide to them. For both the businesses, the depth and quality of our customer relationships are critical to our strategy and success.

We are cautious in expanding our risk assets portfolio and are satisfied the way we are growing in Wholesale and Consumer Banking. Under both the businesses, we have been following risk management techniques that minimize the likelihood of “any surprises”. Costs are well controlled. We are committed to stick to our strategy and will continue to focus on deepening our relationships with our clients.

Our brand is all about commitment. We are Here for good, to create value for our

shareholders, to support and partner our clients and to make a positive contribution to the broader community. We are here for the long term. Building a sustainable business is an integral part of our long-term strategy to enhance shareholder value. Many of our employees chose to get involved in community activities, and this further underpins our standing as being amongst the most customer and community caring institutions in Nepal.

Continued support and trust endowed upon us by our valuable customers, shareholders and other stakeholders has enabled us to remain the best Bank in Nepal. I sincerely appreciate their efforts to bestow us with their encouragement, trust and loyalty. SCB Nepal was the recipient of `Bank of the Year’ award for 2009 from the Financial Times; it is a testimony of this fact.

Our intention is to make meaningful contribution in accelerating the economic activities of the country to attain a higher growth rate. We are looking at the year ahead with cautious optimism. We have to remain vigilant, prudent and focused on the sound management of our balance sheet – this will remain key areas of focus.

Ministry of Finance and the Central Bank have been playing key roles in driving the financial sector reforms in Nepal. We welcome and appreciate the initiatives that are aimed at strengthening the overall financial system in the country. Support and guidance received from our Regulators and the high level of governance of the Standard Chartered Group have been the cornerstones for us in consistently delivering good results, in maintaining exemplary governance standards and in providing superior products and services.

“ We are Here for good, to create value for our shareholders, to support and partner our clients and to make a positive contribution to the broader community. ”

Being the only international Bank in the country with strong performance and values culture, SCB Nepal clearly edges past rest of the competition for being the `Employer of Choice’. The Bank aims at retaining this coveted position. We have been placing continuous focus on staff’s learning & development and in building their leadership capabilities. In an endeavor to address the diverse need of our people and to create a conducive work environment, we have been embracing work-life balance.

The Diversity and Inclusion Council, which is playing a key role in taking forward our D & I agenda, continued to address the different strands of diversity including women, and the differently-abled.

On behalf of SCB Nepal’s Board of Directors, I take this opportunity to thank all the stakeholders for their patronage. Let me take this opportunity to express my sincere appreciation towards our valued customers and shareholders for standing by us in our journey. I would also like to thank all our employees for their untiring efforts and loyalty towards the organization. They were instrumental in enabling us to deliver these good results.

What we achieved during this year will soon be history. There are good reasons for us to be thrilled about our past laurels but we now need to look forward and concentrate in delivering another good year. Whilst I do not underestimate the challenges and uncertainties before us, I am excited by the opportunities. We are equipped and are in a better position to deal with the emerging challenges.

Neeraj Swaroop Chairman

Total Shareholder Equity

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

1,75

4 2,11

6

2,49

3

3,05

2 3,37

0

Annual Report and Accounts 2009-20106

Leading the way in helping realize local dreams

7www.standardchartered.com/np

Krishna Textiles Udhyog

Annual Report and Accounts 2009-20108

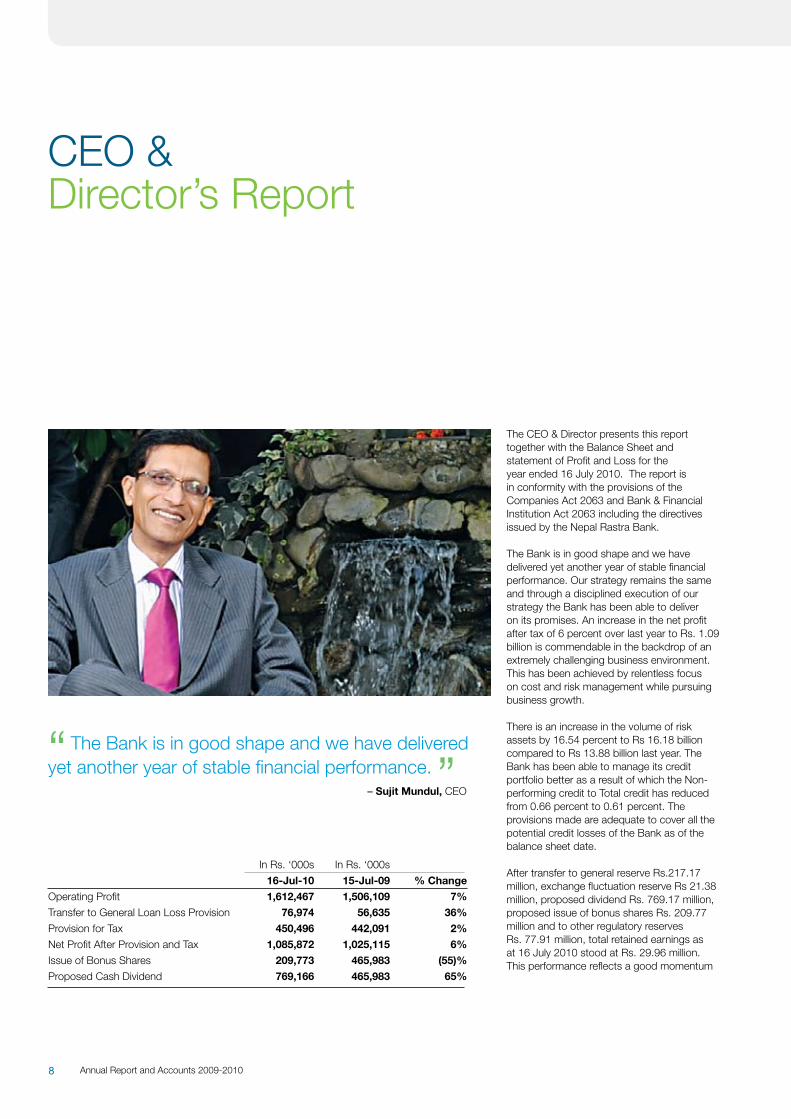

In Rs. ‘000s In Rs. ‘000s

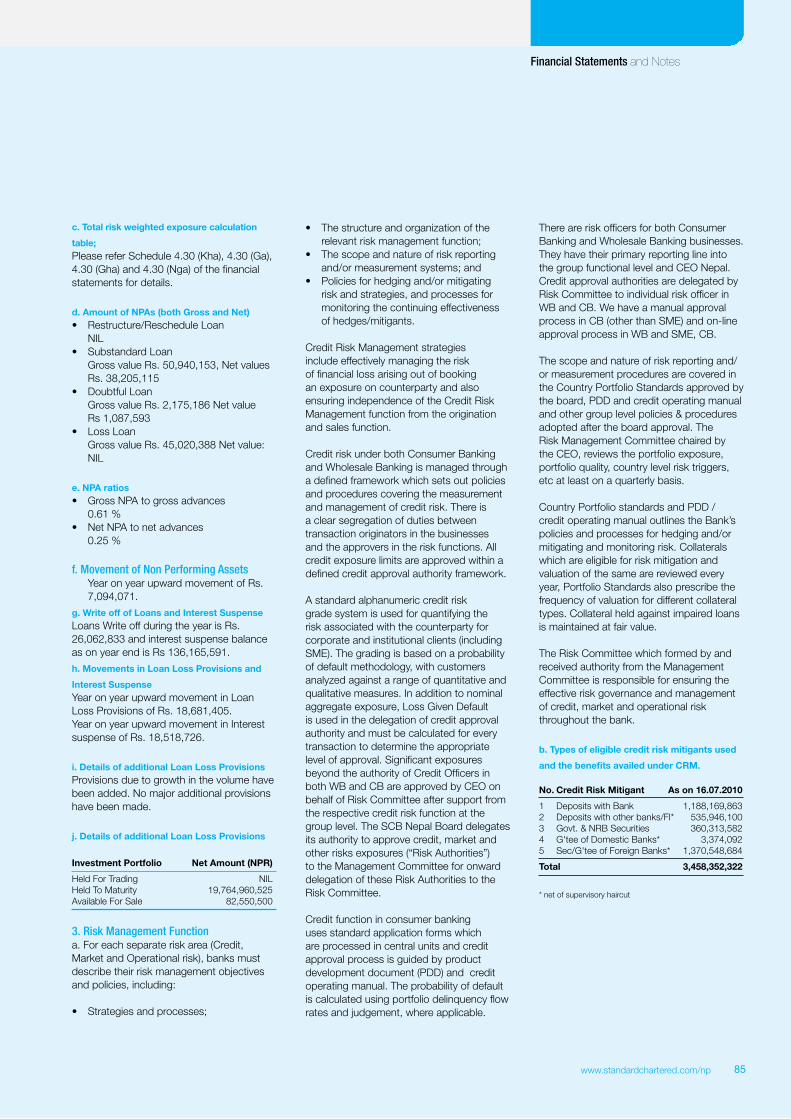

16-Jul-10 15-Jul-09 % Change

Operating Profit 1,612,467 1,506,109 7%

Transfer to General Loan Loss Provision 76,974 56,635 36%

Provision for Tax 450,496 442,091 2%

Net Profit After Provision and Tax 1,085,872 1,025,115 6%

Issue of Bonus Shares 209,773 465,983 (55)%

Proposed Cash Dividend 769,166 465,983 65%

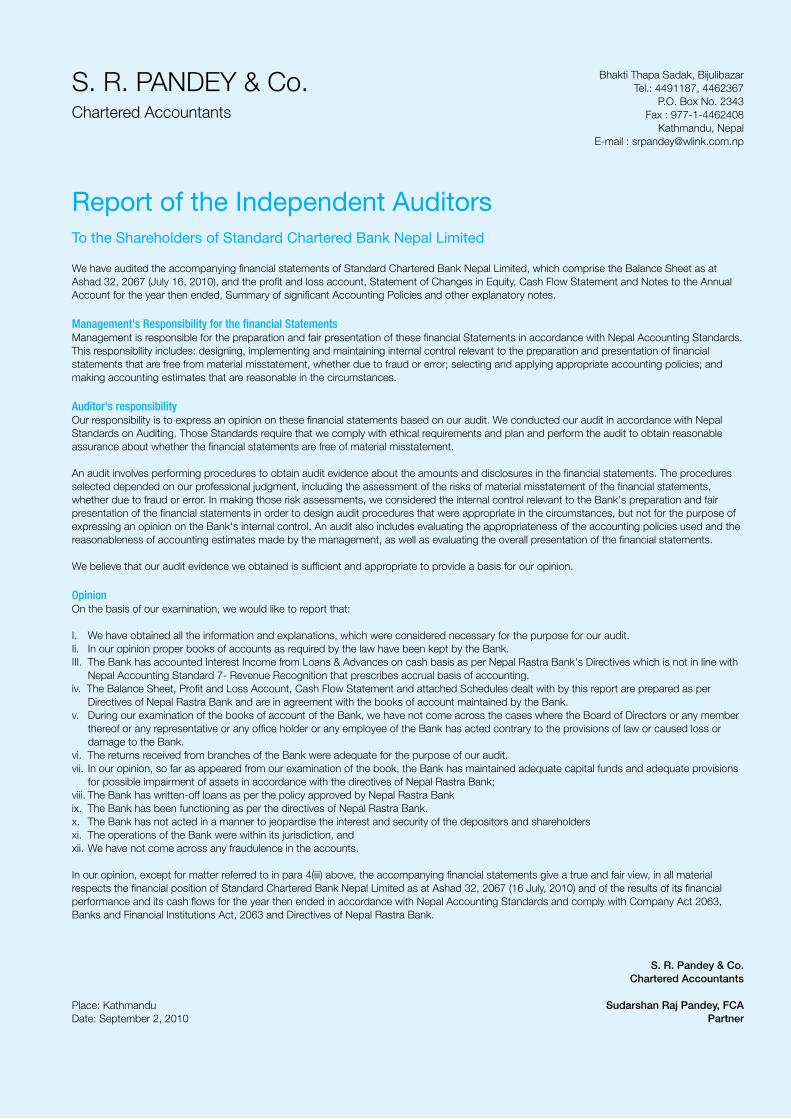

The CEO & Director presents this report together with the Balance Sheet and statement of Profit and Loss for the year ended 16 July 2010. The report is in conformity with the provisions of the Companies Act 2063 and Bank & Financial Institution Act 2063 including the directives issued by the Nepal Rastra Bank.

The Bank is in good shape and we have delivered yet another year of stable financial performance. Our strategy remains the same and through a disciplined execution of our strategy the Bank has been able to deliver on its promises. An increase in the net profit after tax of 6 percent over last year to Rs. 1.09 billion is commendable in the backdrop of an extremely challenging business environment. This has been achieved by relentless focus on cost and risk management while pursuing business growth.

There is an increase in the volume of risk assets by 16.54 percent to Rs 16.18 billion compared to Rs 13.88 billion last year. The Bank has been able to manage its credit portfolio better as a result of which the Non-performing credit to Total credit has reduced from 0.66 percent to 0.61 percent. The provisions made are adequate to cover all the potential credit losses of the Bank as of the balance sheet date.

After transfer to general reserve Rs.217.17 million, exchange fluctuation reserve Rs 21.38 million, proposed dividend Rs. 769.17 million, proposed issue of bonus shares Rs. 209.77 million and to other regulatory reserves Rs. 77.91 million, total retained earnings as at 16 July 2010 stood at Rs. 29.96 million. This performance reflects a good momentum

“ The Bank is in good shape and we have delivered yet another year of stable financial performance. ” – Sujit Mundul, CEO

CEO &Director’s Report

9www.standardchartered.com/np

Business review overview

in the underlying businesses and disciplined management of risks and costs.

RepresentationAs at 16 July 2010, the Bank maintained eighteen points of representation which included fourteen branches and four extension counters. In addition to this, services were also extended to our customers through twenty three ATMs located at different parts of the country.

Wholesale BankingWB delivered another year of strong performance. What was achieved in the last one year is of significance because of the difficult operating environment, characterized by low economic growth, widening trade deficits, tight liquidity coupled with volatile political situation.

Opportunities that met our lending criteria were limited. WB was extremely careful in booking new exposures. At the same time we focused on select clients by actively providing enhanced level of facilities and the more sophisticated products viz. FX options, structured deposits, cross currency swaps, supranational trade finance, etc. This enabled our clients to hedge their FX and interest rate risks and undertake business that they would not have been able to close, had such product offerings not been available to them. It would be apposite to mention that we remained open for business “as usual” even during the most testing situation of liquidity crisis.

While it would be challenging to operate successfully in an environment which is expected to remain difficult– we are confident of maintaining the upward trajectory and at the same time will ensure that all risks be it credit, market, operational, etc. are well managed. We will continue to review our strategy so

that we remain ahead of competition and can respond to the changing dynamics of the market faster than anyone else.

Consumer BankingConsumer Banking continues to adopt customer and segment focused approach, balancing the banking solutions with appropriate risk control measures. Product and service innovation, sales through service excellence, appropriate risk based pricing and investment for the future are the essential ingredients of our operating business model.

During FY 2009/2010, the business continued to encounter numerous challenges stemming from the political conundrum and lackluster economic environment ranging from policy changes to load shedding, impacting adversely the overall operating environment. Whilst these challenges have been there for quite sometime, Liquidity crisis took the center stage decelerating the growth in deposits with further compression in margins.

To remain competitive, the Bank had to raise interest rates on its Structured Call and Fixed Deposits.

However, given our well managed balance sheet and Credit Deposit Ratio, the business continued to lend despite the liquidity challenges facing the market. SME, Auto, Mortgage, Personal Loans and Credit Cards showed steady growth. Auto and Mortgage loans contributed significantly to the Consumer Banking Lending Portfolio.

During the period under review, the Bank opened a branch in New Road and added three more ATMs.

Customer Charter Workshop in progress Launch of Priority Banking card

In line with the Consumer Bank’s transformation agenda, Customer Charter defining customer focus was rolled out to the entire Consumer Banking staff. The Customer Charter primarily focuses on Customers based on the following three principles:

Friendly, Fast and Accurate Service Solution to our Customers’ financial needs Recognition of overall banking relationship

with our Customers

As a testimony of our commitment towards Customer Charter, the Bank, inter alia, has launched the following:

Amulya Bachat Khata - A special Savings Scheme whereby higher interest rate up to the maximum of 6.5 percent p.a is given on the daily balances.

Added two more branches under the 365 days banking service - Naya Baneshwar Branch and New Road branch (former opens on all holidays and latter closes only on Saturdays).

Extended banking hours by one hour across the branch network between Sunday and Thursday and half an hour on Friday.

In order to gauge the satisfaction level of our customers and to continuously improve the way we work, regular feedback and surveys are undertaken. These feedback and surveys provide us with valuable insights about our products, services and people. This also enables us to improvise and introduce various policies, procedures, products and value added services that meet our customers’ needs whilst addressing the encompassing risk issues.

Annual Report and Accounts 2009-201010

Our commitment to Treating Customers Fairly and our policies on Mis-selling and Mis- representation remain core to our values.

We will continue to invest in footprint expansion and our chosen segments. However, given the fluidity in the operating environment we will continue to remain cautiously optimistic in our approach.

As in the past we will strike a careful balance between risk and reward for a sustainable growth.

Outserve Plus - Continuously Improving the Way We WorkContinuously improving the way we work is one of the Bank’s five strategic priorities. The Bank has an Outserve Plus programme which works as the vehicle for continuously improving the way we work. Through Outserve Plus, we have made great progress in creating a culture of continuous improvement.

We have an Outserve Council which over the years, has acted as a catalyst for continuous improvement. Outserve Plus allows us to place greater focus on the underlying infrastructure and processes of the Bank that underpin customer service, productivity and control environment. The ambition for everyone in the Bank therefore is to work Simpler, Faster and Better.

Through Outserve Plus we will continue to look for the ways to be more efficient and effective in what we do, ensuring that we are “Here for good” and “Here for customers”.

Future PlansWe will continue to make appropriate investments in our franchise based on the operating environment. For the year 2010/2011, our key focus will be on Customer Service and SME. Bancassurance is another area where we will be making significant investment for generating fee income. Lending products like Auto, Mortgage, Credit Cards and Personal Loan will continue to be offered to our target segments and improvements in the turn-around time will receive our prime attention. Similarly we will continue to accelerate our deposit drive in order to maintain a better semblance in our balance sheet. We are also committed to providing easy banking solutions to our Visually Challenged customers within the existing framework and constraints.

We also intend to enhance our Online banking capabilities by adding additional features thereby obviating the need for customers to visit the bank for their basic banking requirements. Along with this, we will also be driving our e-statement agenda in order to ensure that customers receive their statements in a more efficient manner.

Inward remittances, an importance source of foreign currency earning, will continue to play a key role in the expansion of our consumer base.

On the WB side, we will continue to offer “total solutions” to our clientele with new products and seamless services. Our endeavor will be to further deepen our relationships

SCB Nepal was the recipient of ‘Bank of the Year’ award for 2009 by The Financial Times, London

CEO addressing a town hall to mark the launch of Bank’s refreshed brand promise - Here for good.

11www.standardchartered.com/np

Business review overview

and achieve core banking status for all the corporate customers.

Nepal holds a huge potential to become a popular tourist destination. The year 2011, which is being celebrated as `Visit Nepal Year’, is expected to provide momentum to the tourism related activities. The steady economic growth of the two neighboring countries i.e. India and China is likely to offer opportunities for Nepal to act as a trade corridor. Suitable policy decisions to capitalize on these opportunities will help our agenda of achieving higher business growth. We will closely follow the opportunities for investment in infrastructural areas viz. hydropower, agriculture and other service sector industries.

In line with our revised brand promise, `Here for good’ we have full commitment to investing in our people, processes and systems with a view to improve the quality of our service for delighting our customers. As we have been doing in the past, we will continue to make a real difference to our communities. We will consciously drive and maintain our high level of governance. For our shareholders we shall strive to continue providing them with superior returns.

Credit EnvironmentThe risk management remained extremely challenging in the last fiscal year. The instability and uncertainty in the global economy brought about by the Western financial crisis persisted till recently. Though Nepal was believed to be relatively insulated from the

global financial crisis, its lagging effects were seen in the last FY in terms of deceleration in workers remittance, a key component in Nepal’s GDP, and decline in exports. During the past FY, Nepalese Economy witnessed low economic growth, widening trade deficit and liquidity shortage in the banking system. The continued security concerns and political uncertainty, double-digit inflation, growing energy crisis and nation-wide long strikes were some other key factors that affected the country’s credit environment. Decline in foreign exchange reserves, slowdown in deposit mobilization and reportedly aggressive flow of credit to unproductive sectors led to liquidity crisis, affecting the productive sectors in terms of inadequate credit support and high cost of borrowing.

Against the backdrop of a difficult political and economic environment, the Bank has been able to maintain its credit quality owing to its proactive risk management approach. The Bank continues to stick to the fundamentals of good banking. Clear strategy and discipline, strong relationship with the clients, rigors around the quality and debate on risk-return dynamics, etc are the few key elements that contributed to the success in the risk management. We are well disciplined in our liquidity management which is corroborated by our conservative C/D ratio and high capital adequacy.

AuditorM/S S. R. Pandey & Co., Chartered Accountants, were appointed as Statutory Auditors for FY 2009/10 by the 23rd Annual General Meeting of the Bank held on 4th

November 2009. We would like to thank them for their contribution made during their tenure as Auditors of the Bank. As per the recommendation of the Audit Committee, this meeting will decide on the appointment of the auditor for next year.

Proposed Dividend and Bonus SharesThe 266th meeting of the Board of Directors of the Bank has proposed dividend to the shareholders of the Bank for the year ended 16 July 2010 at the rate of 55 percent in cash and issue of bonus shares at the rate of 15 percent.

Sujit MundulDirector and CEO

The Bank has introduced extended banking hours across the branch network.

The Bank expanded its footprint by adding an ATM at the UN premises in Harihar Bhawan

Annual Report and Accounts 2009-201012

Leading the way by touching lives

13www.standardchartered.com/np

Annual Report and Accounts 2009-201014

“ Talking sustainability is no longer optional for a bank due to the crisis that the banks have just been through. We have to prove that our business model is sustainable. We have to demonstrate that we make a positive contribution to sustainable growth and development. ”

We maintained our commitment to building a sustainable business as a bank, simultaneously creating value for our shareholders, supporting our customers and contributing to the communities in which we live and work. This has underpinned our strategy and success for over 150 years across Asia, Africa and the Middle East; and it will be the foundation for our future.

Talking sustainability is no longer optional for a bank due to the crisis that the banks have just been through. We have to prove that our business model is sustainable. We have to demonstrate that we make a positive contribution to sustainable growth and development.

We believe that through building a sustainable business we can deliver, broadly, three positive outcomes: contributing to the real economy; promoting sustainable finance; and leading the way in our communities. Our commitment, to our clients, investors, regulators, in our markets and to our staff, is to be Here for good.

Contributing to the real economyThe greatest impact we can make as an international financial institution to the societies in which we operate, is through our direct contribution to the real economy. By offering products and services that serve the needs of our customers we can assist individuals, corporates and other financial institutions to act as agents of economic activity.

Access to finance Many live within communities and their inability to raise finance has a direct impact on economic activity. The Bank is committed to improve access to financial services to such population of Nepal by helping them bring in the realm of financial services.

Our Approach toCorporate Responsibility

The Bank is the promoter of few rural development banks and Rural Microfinance Development Centre (RMDC) which underlines the Bank’s association with this business since long time. The Bank is represented in the Board of RMDC, an eminent wholesale lending micro finance entity. The Bank has also been lending to rural development banks and NGOs to facilitate onward lending to the rural population for the development of microfinance in Nepal.

Responsible selling and marketing Treating customers fairly has moved to the top of the agenda for many financial regulators around the globe. We welcome this development and will monitor and adopt new rules and regulations as they come into force in the markets in which we operate.

Clarity around the segmentation of customers has been increased and we have developed products and services based on clearly identified needs in Consumer Banking. In Wholesale Banking, we place much emphasis on treating our clients fairly and ensuring that they are sold appropriate products for their needs. It is also central to our strategy to become the ‘core’ bank for more clients.

Tackling financial crime We tackle financial crime in three ways: we minimize the risk that our products and services can be used by money launderers; we deny suspect terrorists access to our banking systems; and we build robust controls against fraud and corruption.

Great place to work We are truly a diverse organization with 125 nationalities represented among over 80,000 employees. We have on the ground presence in 70 markets and use our in-depth local knowledge and understanding of cultures to

15www.standardchartered.com/np

Business review overview

Bank is the sponsor of prestigious ‘ProAm Surya Nepal Masters 2010’ golf tournament

Joining hands with Tilganga Eye Centre to provide eye care services to the poor & under priveleged

provide a unique service to our clients and customers.

Our culture and values are a source of competitive advantage which is hard to replicate. They are a key ingredient in what we believe is a unique emotional connection between the Bank and our employees, and between employees and our customers. In short, they encourage customers and employees to join us and stay with us.

Community InvestmentAs an international financial institution, the greatest contribution we can make to the societies in which we operate is through our direct contribution to the real economy. We believe in promoting sustainable finance to contribute to the challenges and opportunities presented by social and environmental risk.

SCB Nepal has constituted Standard Chartered Nepal Community Partnership Forum (SCNCPF) to undertake various community initiatives in Nepal. It is registered with District Administration Office and has received affiliation from Social Welfare Council.

The two major initiatives of the Bank launched in 2003 under its ‘Believing in Life’ campaign are ‘Seeing is Believing’ and ‘Living with HIV’.

Seeing is Believing Seeing is Believing is a public-private partnership that addresses avoidable blindness. Launched in 2003, the programme has gone from a simple staff –led initiative to raise enough money to carry out 28,000 cataract operations to $37 million global funding initiative. In 2008, we launched A New Vision, our latest commitment to Seeing is Believing. We will invest a further $20 million to provide sustainable eye-care services for 20 million people in deprived communities in 20 cities.

The Vitamin A Capsule (VAC) distribution program for 2010 in Kathmandu valley concluded successfully on 2-3 November 2009 and 19-20 April in April 2010. In line with our ‘Seeing is Believing’ initiative, our staff members from different branches joined the teams from Helen Keller International/Nepal (HKI/N) to raise awareness and provide support to community health volunteers during the distribution days after undergoing half a day training at HKI/N. Since 2007, Standard Chartered Bank’s ‘Seeing is Believing’ program has worked with HKI/N, the Ministry of Health and Population, and the Nepal Technical Assistance Group to strengthen Vitamin A awareness and distribution systems in the Kathmandu Valley. VAC distribution program in Kathmandu valley is being partially funded by the SCB Group.

World Sight Day was celebrated on 8th of October 2009. An agreement was signed between the Bank and Tilganga Eye Centre (TEC) to conduct 700 cataract surgeries to the poor and underprivileged people in different parts of the country in between October 2009- July 2010. In addition, an exhibition cum sale of handicraft goods produced by visually impaired people was held at the Bank’s Head office. The Bank has been instrumental in supporting restoration of sight to ~4,900 people till date, by sponsoring eye camps and intraocular lenses for cataract surgeries in partnership with Tilganga Eye Centre (TEC) and other local hospitals.

International Agency for the Prevention of Blindness (IAPB), a working partner of SCB Group under the Seeing is Believing program, signed an agreement on behalf of the Bank with Christian Blind Mission UK (CBM UK) in order for Eastern Regional Eye Care Programme (EREC–P), Biratnagar to receive USD 1 million worth of financial assistance

At a program organised to celebrate World Environment Day 2010

Annual Report and Accounts 2009-201016

from the SCB Group. The assistance will be utilized towards construction, establishment of Eye Care Centres, Outreach Dept and Capacity building for local implementing partners. The project is progressing and SCB Nepal is closely monitoring developments of the project.

Standard Chartered Bank Nepal Walkathon is an annual fund raising event through which the Bank provides a platform to engage cross sections of our community to raise funds. We have been conducting this event since 2003 and it continues to remain a signature event of the Bank.

As a part of Wholesale Bank initiative, the Bank raised funds worth USD 3,400 through the sale of raffle tickets. The funds raised from the sale of raffle tickets will go to support the Bank’s ‘Seeing is Believing’ initiative.

Lazimpat Branch organized ‘Football for Hope & Vision’, a fund raising event for our ‘Seeing is Believing’ initiative targeted at raising funds from our staff members by screening World Cup football match live .

Living with HIVAIDS remains a global killer with no cure or vaccine. Over 33 million people are infected

by HIV and AIDS, with 6,800 new infections each day; 15-24-year-olds count for 45% of all new HIV infections. This pandemic has a devastating impact on many communities where we do business. Education is a key component of prevention strategies.

We have been running a workplace HIV education programme, called Living with HIV since 1999, which currently involves a network of more than 1,150 HIV Champions in 50 countries globally. In Nepal, we have 30 HIV Champions who work to raise awareness of HIV and AIDS in the Bank and with external organizations.

The Bank, in partnership with Nepal Banker’s Association, rolled out its Living with HIV program to the senior officials of various Banks. The program was successfully conducted by our Bank’s HIV Champions.

All our HIV Champions have been receiving refresher training through ‘Train the Trainer’ refresher sessions held at different intervals.

Like previous year, the Bank continued to support the under privileged women/ girls living with HIV /AIDs residing at Karuna Bhawan by sponsoring the cost of skill training program. The skill training program was

SCB staff volunteering during the Vitamin A Capsule distribution program

Patients after undergoing eye surgery at an eye camp held in Putali bazar, Syangja

Celebrating the festival of ‘Teej’ with our friends at Karuna Bhawan

17www.standardchartered.com/np

Business review overview

The Bank supported Mahendra Shanti School, Balkot, Bhaktapur with 20 computers for computer education

Walking together for a noble cause-Walkathon 2009

imparted to these needy women/children so as to make them self reliant and to be capable of earning their livelihood.

The Bank also continued to sponsor education and living expenses of two LwHIV children at Maiti Nepal for three years.

Focus on Youth, Health, Education and Environment In line with our commitment to reiterate that the Bank is Here for good, we have undertaken various initiatives viz.:

The Bank continues to support to the deserving students of Shree Mahendra Shanti High School, Balkot by providing incentives/scholarships through VISCOSS – Nepal for the ninth consecutive year. The Bank also supported the school with 20 sets of computers to help them providing computer education to their students.

To mark the World Environment Day, Tree Plantation Campaign was organized by the Bank on 5 June to mark the World Environment Day. The staff planted altogether ~500 tree saplings at the Institute of Engineering, Pulchowk Campus.

The Bank was actively engaged in the International Cricket Council World Cup-

Staff displaying placards on environmental awareness at the Head Office

Div 5 matches held during 20th -27th February. The Bank is the co-sponsor of Nepal Cricket Team with branding rights.

Successful conclusion of the ‘Surya Nepal Masters Golf Tournament 2010’ which was held from 21-24 April. The event is considered to be one of the biggest professional golf tournaments organized in Nepal and generated good level of visibility for the Brand like in the past. The Bank was the ProAm sponsor of this tournament.

The Bank sponsored ‘Vow 6th Top College Women Competition 2009’ – an event that highlights the achievements of young, talented and versatile women students of Nepal and imparts them a platform to excel in their career. This was done mainly with a view to drive our D & I agenda and to strengthen the Brand amongst the young and college going students in Nepal – the Bank has been supporting the event for the last two years.

As a part of CB Credit initiative, the Bank raised funds worth USD 6,178 through the sale of raffle tickets. The funds raised from the sale of raffle tickets are intended to be utilized towards the support of under privileged children.

Annual Report and Accounts 2009-201018

Leading with our sustainable business strategy

19www.standardchartered.com/np

Bhotekoshi Power Company Pvt. Ltd.

Annual Report and Accounts 2009-201020

Here for people, Here for goodPeople Strength:

New business initiatives supported by transformation created opportunities for new people with diverse background to take up challenging and exciting roles in the Bank. There were a total of 81 new hires to start their career in the Bank, majority inducted through job advertisements posted in our SCB Career Webpage.

Our people strength has increased by 7% making a total of 429 staff as of 16 July, 2010 as compared to 392 in 15 July, 2009. The current mix of male and female staff is 63:37.

During the year under review 14 of our employees completed 20 years, 4 completed 15 years, 3 completed 10 years and 24 employees completed 5 years of dedicated services to the Bank. The staff members completing their long service periods were felicitated on different occasions by the CEO with certificates and awards.

Right Start and Engagement programs for our 59 new joiners were conducted by the Bank at different dates. This was done with a view to motivate our new entrants to welcome them to work in a great place, live our culture and values and provide opportunity to build their career.

Our people strategy and priorities have remained consistent over the last few years.

Engagement:Recognizing the fact that an important part of sustaining business performance and driving productivity comes from engaging and motivating our employees, the Bank focused on employee engagement and proved successful in maintaining the engagement level in spite of a challenging market environment.

This high participation rate in Gallup Q12 Survey, which we use to measure engagement, reflects a strong commitment from employees to voice their opinions and demonstrates their trust in the process. Our overall score remained strong. We ensure that teams create `action plans’ and `follow through’ on their commitments. This involves regular conversations with managers with an objective to clarify what the expectations are thereby addressing the concerns and difficult questions, if any.

Learning Week:Learning Week was successfully organized in conjunction with the SCB Regional Organization Learning Team targeting all levels of employees in August. Various learning interventions, such as video sessions on “Even Eagles need a Push” were attended by 191 staff members. 28 of our employees attended a session on “Power of Vision”.

SCB Drama Mania A pan Bank drama competition ‘SCB Drama Mania’ was organized by the Bank during the year under review. A total of eleven teams with staff representation from all Branches and Units of the Bank participated in this popular event. The event created a very high level of engagement, excitement and unravelled enormous amount of hidden talents within the Bank. Preliminary rounds were held during the months of July and August with the finals of the event held in Kathmandu on 7th of August. All performances received great appreciation of the eminent external judges and a house full of audience on both the occasions. This event was followed by the annual staff party.

“ Recognizing the fact that an important part of sustaining business performance and driving productivity comes from engaging and motivating our employees, the Bank focused on employee engagement and proved successful in maintaining the engagement level in spite of a challenging market environment. ”

21www.standardchartered.com/np

Business review overview

Honoring one of the women Gold medalists of 11th South Asian Games

External Extra Curricular Activities: Nine staff members representing various

departments and functions of the Bank participated in the coveted “Soaltee Crowne Plaza Super Sixes Cricket Tournament – 2009”.

Health and Safety Campaign week was celebrated in October with an objective to raise awareness and importance of these areas in order to provide our people with awareness, materials and basic tips and training.

Ten staff members representing various departments participated in the Inter Bank Volleyball Tournament 2010 organized by the Nepal Rastra Bank (NRB) on the occasion of its 55th Anniversary.

Employee Volunteering:It is crucial for the Bank to have our employees a deep understanding of the local markets and community where we operate. Our people have been playing a key role in appreciating the challenges and demonstrating the required commitment while working in partnership with the communities to overcome these challenges. As ambassadors of our brand, we have been empowering our employees by providing them opportunities to participate in various community programs through Employee Volunteering (EV) and champion networks. This activity is at the heart of our unique culture and is the reason why many of our people choose to work for us.

Employee Volunteering program is an internal initiative of the Bank whereby our staff members are encouraged to participate in community activities. As per the program, the staff are entitled for three days leave in addition to their annual leave to volunteer in the community related activities.

“Standard Chartered Nepal Walkathon 2009 – A Walk for a brighter tomorrow” is the Bank’s annual fund raising event conducted with an objective to raise funds for our various community initiatives, engage our staff and raise awareness around avoidable blindness, HIV/AIDS and environment. This event was organized successfully on 21st Nov 09 in which 90% of our staff in Kathmandu walked about 5 kms for this noble cause.

Seeing is Believing: About 20 staff volunteered 2 days each in

October ’09 and in April ’10 to distribute Vitamin A capsules in conjunction with Helen Keller Int’l and Nepal Technical Assistance Group. This is a SCB Group funded project in Nepal.

In partnership with Tilganga Eye Centre (TEC) our staff members in Kathmandu volunteered at eye camps held on 5th and 12th of June at Bhaktapur and Sindhupalchowk. Further our staff in branches outside Kathmandu have also volunteered in various eye camps in their areas.

Living with HIVOur HIV Champions have been constantly volunteering their time to conduct awareness and education sessions on HIV/AIDS on a bi-monthly basis to all new joiners in the Bank and also conducted similar sessions for other external organizations such as schools, colleges, Rotary Clubs, Rotaracts and manpower agencies.

World AIDS Day World AIDS Day was celebrated with a focus on awareness and educational activities

Induction Programs are designed for the new joiners to help them gain better understanding about the Bank.

Volunteers on a blissful note during ‘Clean Rani Pokhari Campaign’ under Employee Volunteering initiative

Annual Report and Accounts 2009-201022

through engagement of our staff. Awareness and education workshops were conducted by our staff HIV Champions for our trainees/new-joiners. Similarly in association with Nepal Banker’s Association (NBA), this workshop was rolled-out to the representatives of 15 local banks. Voluntary Counseling and Testing (VCT) was organized for our staff members in the Bank premises. Staff creatively decorated their branches/departments with symbols, posters raising awareness on HIV/AIDS and displayed placards with messages on HIV awareness.

World Environment DayVarious programs were organized to mark the World Environment Day (WED) in June. Our employees made a difference by volunteering to plant 400 saplings at the premises of Pulchowk Engineering College, Pulchowk. Other activities included display of placards at the Bank entrance, Car Pooling and several internal broadcasts on environment to build awareness around the theme.

Building leadership capabilitiesStrong leadership is critical to our success. It is through our leaders that we motivate employees, drive performance and impart our unique culture.

We offer emerging leaders a series of programs and workshops to support their personal development, through one-on-one coaching; through our flagship Leadership Development Programs and our Great Managers workshops. An interactive session on “KFCI (Know, Focus, Care and Inspire) Awareness” was conducted for 42 managers and 19 of our Managers have completed a course on Leadership Essentials.

In order to build leadership from within, we have a number of specific programmes targeted at our high potential employees at each level, which help us to grow and develop them into our future leaders by providing mentors, networking opportunities, career discussions and specific learning opportunities. We provide support and skills to the Managers to help manage their talent pools. “Managing Talent in a Changing World” - a full day program was conducted for 12 People Managers. Senior Managers participated in the Country Leadership Team meetings conducted in the year under review. Nine of our employees were given opportunities outside Nepal for short term assignments. During the year under review, two employees took up roles in SCB Group points in other countries. Our talents were given opportunities to interact with Senior visitors from the Group to learn about the Group’s focus, priorities and leadership skills.

Training And Development OpportunitiesWe strongly believe in the need to “Keep Learning, Keep Growing” and with this belief Bank has been encouraging staff to actively involve in enhancing their knowledge and skills through various types of learning program be it through classroom programs, web based learning, on the job, self reading, assessments, attachment programs, sharing knowledge amidst each other. Number of learning opportunities - In-house trainings, Local programs by external trainers/ organizations, Global trainings, Short term attachment programs in the Group, On the job learning inside and outside the country were organized during this fiscal year through which our staff were able to develop their personal,

Roll out of ‘Know Focus Care & Inspire’(KFCI) workshop to staff

‘SCB Drama Mania’: The employees showcased their hidden talent through this event.

“ Strong leadership is critical to our success. It is through our leaders that we motivate employees, drive performance and impart our unique culture. ”

23www.standardchartered.com/np

Business review overview

professional and leadership skills. A total of 995 mandays were spent in learning and development programs during the year under review.

Similarly, an impactful session on “Team Effectiveness” was conducted for the Bank’s management team.

Strengthening performance cultureTo reinforce our performance culture, we have launched a new global online system for managing performance which allows all employees to set their annual objectives online. This reinforces the basics of good people management and ongoing performance coaching by ensuring that all employees have stretching job objectives in place and are clear of what is expected of them.

The system captures all employee performance and values objectives online so that managers and employees can agree and review them at the click of a button throughout the year. It also provides a structured method to capture progress and feedback from colleagues and managers. This is a key factor in high employee engagement and helps reinforce our culture.

Diversity and inclusionOur focus on diversity and inclusion provides us with a unique competitive advantage and we work hard to maintain this. We constantly strive to improve the way we work so that employees can balance their work and personal commitments, maximize their potential and perform to their best. Keeping this in mind, maternity leave period for our female staff members has been revised to 90

from 45 days so that they can spend quality time with their newborn babies.

Festival of women folks, ‘Teej’ was celebrated by our female staff by celebrating it in-house and also by visiting the HIV affected women shelter homes and providing them with clothes and sweets. ‘Bhai Tika’ was celebrated by women colleagues presenting a muffler as a token of friendship and appreciation to all male colleagues in the Bank.

International Women’s Day 2010International Women’s Day was celebrated by organizing various activities at the behest of D&I Council.

Throughout this day, women wore beautiful scarves presented to them by their male colleagues.

To make that special woman in their lives feel valued, staff expressed/dedicated their messages in poetry, quotes etc.

An exhibition cum sale was organized in the Bank’s premises of products made by trafficked children and women rescued by an NGO- The Esther Benjamins Trust.

HR Team visited one of the girls college and conducted an hour long interactive session sharing the importance of banking for women.

3 women who won medals at the SAF games were invited and felicitated at a Town Hall.

We believe that our strong focus on engaging our people around our brand, further embedding our unique culture and values will continue to provide us competitive advantage.

Senior Management in action during the ‘Team Effectiveness’ session

‘Going Green’: The Bank planted 5,000 trees at Bisankhunarayan in Lalitpur

“ We believe that our strong focus on engaging our people around our brand, further embedding our unique culture and values will continue to provide us competitive advantage. ”

Annual Report and Accounts 2009-201024

Leading the way in nurturing the economy

25www.standardchartered.com/np

Rolpa Carpet Industries

Annual Report and Accounts 2009-201026

Our approach to corporate governance

A SynopsisFollowing are the steps taken by the management for strengthening Corporate Governance in the organization.

The Board of Standard Chartered Bank Nepal Limited is responsible and accountable to the shareholders and ensures that proper corporate governance standards are maintained.

The Audit Committee meets quarterly to review the internal and external inspection reports, control and compliance issues and provides feedback to the Board as appropriate.

The Manco (Management Committee) represented by all Business and Function Heads is the apex body managing the day to day operations of the Bank. Chaired by the CEO, it meets at least once a month for formulating strategic decisions.

The Annual General Meeting is used as an opportunity to communicate with all shareholders.

To ensure compliance with applicable laws, enhance resilience to external events and avoid reputational risk, the Board has adopted SCB Group policies and procedures.

Ultimate responsibility of effective Risk Management rests with the Board supported by Audit Committee, Manco, Country Operational Risk Group (CORG), Asset and Liability Committee (ALCO) and Risk Management Committee (RMC)

Embracing exemplary standards of governance and ethics wherever we operate is an integral part of our Strategic Intent. The Group Code of Conduct is adopted to help us meet this objective by setting out the standards of behavior we must follow with each other and with our customers, communities, investors and regulators.

AnalysisThe Board of Standard Chartered Bank Nepal Limited is responsible for the overall management of the Company and for ensuring that proper corporate governance standards are maintained. The Board is also responsible & accountable to shareholders.

The report describes how the Board has applied the principles and provisions of the Nepal Rastra Bank directives on Corporate Governance and the provisions of Companies Act, 2063 and Bank and Financial Institution Act, 2063 (the “Corporate Governance Code”). The directors confirm that:

Throughout FY 2066/067, the Company complied with all the provisions of the Corporate Governance Code. The Company complied with the listing rules of Nepal Stock Exchange Limited.

Throughout FY 2066/067, the Company was in compliance with the Securities Registration and Issuance Regulation, 2065

The Company has adopted a Code of Conduct regarding securities transactions by directors on further terms no less than required by the Nepal Rastra Bank Directives and the Companies Act and that all the Directors of the Bank complied with the Code of Conduct throughout FY 2066/067.

The BoardAs at the date of this report, the Board is made up of the Non-Executive Chairman, one Executive Director and four Non-Executive Directors of which one is professional /independent Director appointed as per the regulatory requirement. Director, Mr. Arjun Bandhu Regmi, representing the public shareholders, had submitted his resignation from the post of Public Director citing personal reasons and the same was accepted by the Board at 264th Board meeting of the Bank

“ The Group Code of Conduct is adopted to help us meet this objective by setting out the standards of behavior we must follow with each other and with our customers, communities, investors and regulators. ”

Corporate governance

Corporate Governance

27www.standardchartered.com/np

Sharing a presentation with NRB on ‘Risk Management Strategies & Investment Products’

23rd AGM of the Bank in progress

held on 5th July 2010. The Board is currently in the process of fulfilling the vacant post as per the provisions of the Companies Act.

The Board composition complied with the regulatory requirements. Four Directors including the Non-Executive Chairman are nominated by the SCB Group to represent it in the Board in proportion to its shareholding. The Board meets regularly and has a formal schedule of matters specifically reserved for its decision. These matters include determining and reviewing the strategy of the Company, annual budget, overseeing statutory and regulatory compliance and issues related to the Company’s capital. The Board is collectively responsible for the success of the Bank.

During the year under review, the Board held 14 board meetings of which 1 was held by circulation. The Directors are given accurate, timely and clear information so that they can maintain full and effective control over strategic, financial, operational, compliance and governance issues.

The following table illustrates the number of Board and Audit Committee meetings held during the year under review:

Audit Board Committee Number of meetings 14 4 in FY 2066/067 Neeraj Swaroop 12* - Anurag Adlakha 4* 1 Sushen Jhingan* 9* 1 Sujit Mundul 14 - Ram Bahadur Aryal 14 4 Arjun Bandhu Regmi 10 -

* Chairman Mr. Neeraj Swaroop attended Six Board meetings through his alternate Director Mr. Aniruddha Bose and Mr. Sushen Jhingan attended two Board meeting through his alternate Director Mr. Peter Warbanoff.

Audit Committee As required by the local regulations, the Board has formed an Audit Committee with clear terms of reference. The Audit Committee meeting is normally held on a quarterly basis. The Committee reviews internal audit reports, Nepal Rastra Bank Inspection reports, Statutory Audit reports, Bank’s financial condition, internal audit/controls issues, compliance issues, etc. The Committee provides feedback to the Management through the Board of Directors as appropriate.

The Independent/Professional Director chairs the Committee for ensuring complete independence. The composition of the Audit Committee as on 16th July 2010 was as below:

Ram Bahadur Aryal - Non Executive Director- Chairman Anurag Adlakha - Director - Member Sushen Jhingan, Director - Member Gopi Krishna Bhandari - Member Pradip Shrestha - Member Secretary

All members of the Audit Committee are either non-executive directors or independent of business. The responsibilities of the Committee are in congruence with the framework defined by the NRB Directives and the Companies Act.

Management Committee (Manco)The Management Committee (Manco) represented by all Business and Function Heads of the Bank is the apex body that manages the Bank’s operation on a day to day basis. Manco meets formally at least once a month and informally as and when required. The strategies for the Bank are decided and monitored on a regular basis and decisions are taken jointly by this Committee. The CEO Chairs the Manco.

As at the date of this report, the composition of the Manco was as follows: Mr. Sujit Mundul, Chief Executive Officer Mr. Anurag Mishra, Head Wholesale Banking Ms. Anju Sharma, Head Consumer Banking Ms. Rakhi Singh, Chief Financial Officer Mr. Sudesh Khaling, Chief Information Officer Mr. Shobha Bd. Rana, Head, Legal and Compliance & Assurance Mr. Diwakar Poudel, Head, Corporate Affairs Ms. Bina Rana, Head, Human Resources Mr. Gopi Bhandari, Senior Manager Credit

Relations with Shareholders The Board recognizes the importance of good communications with all the shareholders. There is regular information, both financial as well as non-financial, published by the Company for the shareholder’s information. The AGM is used as an opportunity to communicate with all the shareholders.

The notice of the AGM, as required by the Companies Act, was sent to shareholders at least 21 days before the date of the meeting at their mailing addresses available in the Company’s records. In addition to that the notice and agenda of the AGM were also published twice in the national level daily newspaper for the shareholders information.

Internal ControlThe Board is committed to managing risks and in controlling its business and financial activities in a manner which enables it to maximize profitable business opportunities, avoid or reduce risks which can cause loss or reputational damage, ensure compliance with applicable laws and regulations and enhance resilience to external events. To achieve this, the Board has adopted the SCB Group policies and procedures of risk identification, risk evaluation, risk mitigation and control/monitoring.

Annual Report and Accounts 2009-201028

functional level. Information is communicated through the functional, business committees to the Board which seeks to ensure that key risk issues are addressed at the appropriate levels and to provide assurance that standards and policies are being followed.

Credit Risk Credit risk is the risk that counterparty to a financial instrument will cause a financial loss to the Company by failing to discharge an obligation. Credit exposure includes individual borrowers and connected groups of counterparties and portfolios, in the banking and trading books. Standards are approved by the Board and the delegation of credit authorities are overseen by the CEO. Procedures for managing credit risk are determined at the business level with specific policies and procedures being adapted to different risk environment and business goals. Business risk officers are in place to maximize the efficiency on decision making. The Credit Risk is managed by Risk Management Committee, chaired by the CEO. This Committee, inter alia, reviews and monitors the Bank’s Assets Portfolio.

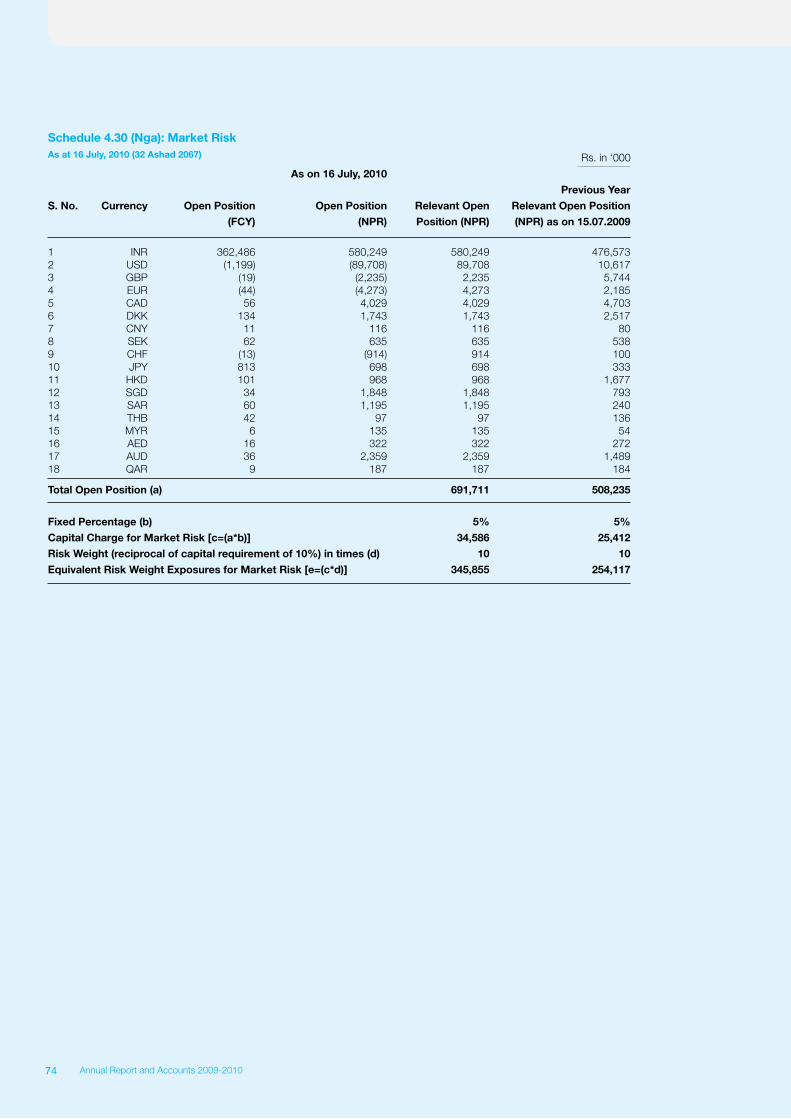

Market Risk Market risk is the exposure created by potential changes/volatility in market prices and rates. The Bank is exposed to market risk arising principally from customer driven transactions. The objective of the Bank’s market risk policies and processes is to obtain the best balance of risk and return while meeting our customers’ requirements. Market risk is managed by Asset and Liability Committee (ALCO) which agrees policies and levels of risk appetite.

Liquidity Risk Liquidity risk is defined as the risk that the Bank either does not have sufficient financial resources available to meet all its obligations and commitments as they fall due, or can access them only at excessive costs. It is the policy of the Bank to maintain adequate liquidity at all times and for all relevant currencies, and hence, to be in a position to meet all obligations as they fall due. The liquidity risk is managed both on a short term and a medium terms basis. In the short term, the focus is on ensuring that the cash flow demands can be met through asset maturities supported by customer deposits and wholesale borrowings where required. The Asset/Liability Management Committee (ALCO) under the chairmanship of CEO

meets at regular intervals to review the Deposit/Investment strategy of the Company and regulatory compliance. The ALCO is responsible for both statutory and prudential liquidity.

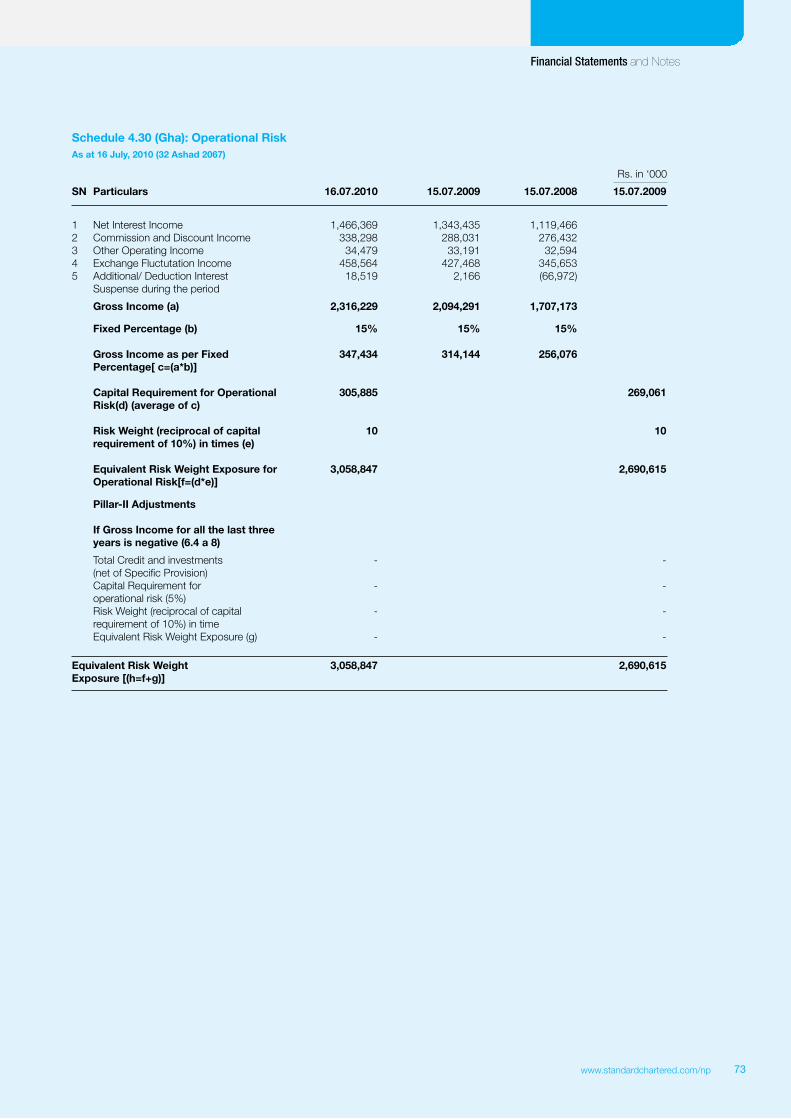

Operational RiskOperational Risk is the risk of direct or indirect loss due to an event or action resulting from the failure of internal processes, people and systems, or from external events. To ensure that the key operational risks are managed in a timely and effective manner, a framework of policies, procedures and tools has been established within the Bank to identify, assess, monitor, control and report such risks.

A robust Operational Risk Management and Assurance Framework (ORMAF) has been established as per SCB Group guidelines to supervise and manage the operational risk in the Bank. A Country Operational Risk Group (CORG) under the chairmanship of CEO is in place to supervise and direct the management of operational risk at country level whilst Business and Functional Operational Risk Groups are responsible for managing business and functional level operational risks in the Bank. Similarly, each unit in the Bank has a Unit Operational Risk Manager responsible for managing the operational risk at the unit level.

Bank’s existing operational risk management system has been further strengthened by creating a new role titled ‘Country Operational Risk Officer’ with responsibility to ensure end to end operational risk management across businesses and functions in the country and to drive the governance process.

Regulatory Risk Regulatory risk includes the risk of non-compliance with the regulatory requirements. The Bank has implemented appropriate compliance framework, policies and procedures and has effectively managed the regulatory risk. While compliance team is responsible for establishing and maintaining the compliance risk, compliance of such policies and procedures is the responsibility of each employee.

Legal Risk Legal risk is the risk of unexpected loss, including reputational loss arising from defective transactions or contracts, claims being made or some other event resulting in liabilities or other loss for the Bank, failure to protect the title to and ability to control

The effectiveness of the Company’s internal control system is reviewed regularly by the Board, its Committees, Management and Internal Audit. The Audit Committee has reviewed the effectiveness of the Bank’s system of internal control during the year and provided feedback to the Board as appropriate.

The Internal Audit monitors compliance with policies/standards and the effectiveness of internal control structures across the Company through its program of business/unit audits. The Internal Audit function is focused on the areas of greatest risk as determined by a risk-based assessment methodology. Internal Audit reports are periodically forwarded to the Audit Committee. The findings of all audits are reported to the Chief Executive Officer and Business Heads for initiating immediate corrective measures.

Risk Governance Through its risk management framework the Bank seeks to efficiently manage credit, market and liquidity risks which arise directly through the Bank’s commercial activities as well as operational, regulatory and reputational risks which arise as a normal consequence of any business undertaking.

As part of this framework, the Bank uses a set of principles that describe its risk management culture. The principles of risk management followed include:

Balancing risk and reward. Disciplined and focused risk taking to

generate a return. Taking risk with appropriate authorities and

where there is appropriate infrastructure and resource to manage them.

Anticipating future risks and ensuring awareness of all risks.

Efficient and effective risk management and control to gain competitive advantage.

Ultimate responsibility of the effective management of risks rests with the Board. The Audit Committee, within an authority delegated by the Board, reviews risk areas and monitors the activities of Management Committee (Manco), Country Operational Risk Group (CORG), Asset and Liability Committee (ALCO), and Risk Management Committee (RMC).