lawley seminar | acsi retirement planning

TRANSCRIPT

Lawley-Courier 2015 Seminar Series

April 16, 2015

Presented by Mark E. Brand, Esq.Actuarial Consulting Services, Inc.

There are many plan design options available for tax-qualified defined contribution and defined benefit retirement plans.

Considerations include:differences in the nature and size of the workforceemployee turnover characteristicsage and length of service disparities between

owners/executives and “rank-and-file” employeesthe willingness of employees to make their own

contributionsamount available each year for contributions by the

employerability of the employer to commit to making specific

levels of contributions from year to year Internal Revenue Code and IRS nondiscrimination

requirements

Examples of plan designs to consider:safe harbor 401(k) plan“integrated” profit sharing contributionsnew comparability profit sharing contributionscash balance defined benefit plan

SAFE HARBOR 401(k)Ordinarily, pre-tax contributions (401k deferrals)

made by a “highly compensated employee” (HCE) from his W-2 pay or his self-employment income (i.e., his “earnings”) are subject to deferral limit nondiscrimination testing.Although the IRS 401k deferral limit is $18,000 in

2015 ($17,500 in 2014), the limit may be reduced if the non-HCE employees do not contribute enough to allow the plan to pass the deferral limit nondiscrimination testing.

In addition to the $18,000 deferral limit, if at least age 50, an additional $6,000 in 2015 ($5,500 in 2014) can be deferred without being subjected to nondiscrimination testing.

A safe harbor 401(k) plan is exempt from the deferral limit nondiscrimination testing, i.e., no “cutback”.

Two alternative types of safe harbors:Safe harbor non-elective contribution

The employer contributes 3% of pay for each employee who is eligible to make a 401k deferral.

Safe harbor matching contribution If an employee contributes 5% of pay, the employer

must make a matching contribution of 4% of pay. This generally is 100% of the first 3%, plus 50% of the

next 2%.

There are special rules that should be considered as part of the planning process, for example:Should the safe harbor contributions only be

made for employees who have completed a “year of service”, i.e., are there part-time employees who do not work at least 1,000 hours per year, who may be permitted to contribute their own money but may be excluded from the safe harbor contributions?

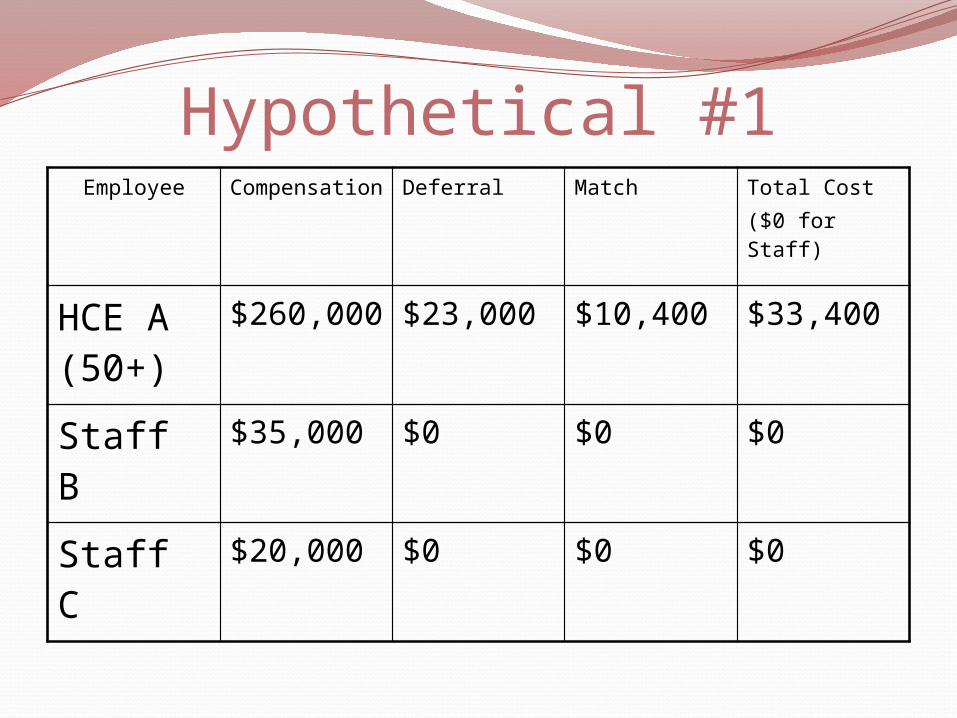

Hypothetical #1Employee Compensation Deferral Match Total Cost

($0 for Staff)

HCE A (50+)

$260,000 $23,000 $10,400 $33,400

Staff B $35,000 $0 $0 $0

Staff C $20,000 $0 $0 $0

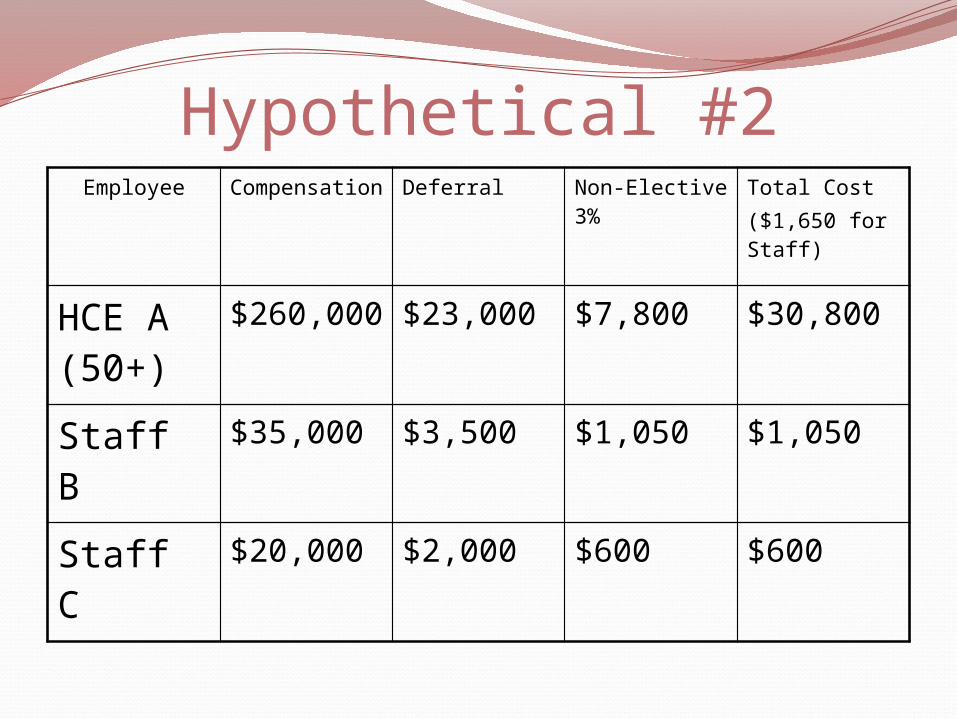

Hypothetical #2Employee Compensation Deferral Non-Elective

3%Total Cost($1,650 for Staff)

HCE A (50+)

$260,000 $23,000 $7,800 $30,800

Staff B $35,000 $3,500 $1,050 $1,050

Staff C $20,000 $2,000 $600 $600

“INTEGRATED” PROFIT SHARING CONTRIBUTIONS

Employer “profit sharing” contributions can be made to a 401(k) plan, including a safe harbor 401(k) plan.

The aggregate plan contributions for a HCE can be $53,000 in 2015 ($52,000 in 2014) plus any additional age 50 deferrals ($6,000 in 2015 or $5,500 in 2014). If the HCE’s pay or earnings are at least $265,000 in

2015 ($260,000 in 2014) and he maximizes his deferral contributions plus safe harbor contributions, that may leave as much as $24,400 (if safe harbor match) or $27,050 (if safe harbor non-elective) available as a profit sharing contribution.

A traditional plan design allocates profit sharing contributions pro rata based on each “eligible” employee’s pay.

An “integrated” plan design recognizes that the employer is contributing to Social Security on pay up to the FICA taxable wage base (“TWB”) ($118,500 in 2015; $117,000 in 2014).

How does integration work?The contribution is allocated at the rate of X%

of pay to the integration level (i.e., the “breakpoint”) and at the rate of Y% of pay (greater than X) on pay in excess of the integration level.

IRS regulations set the maximum contribution/allocation rates based on the breakpoint which is chosen.

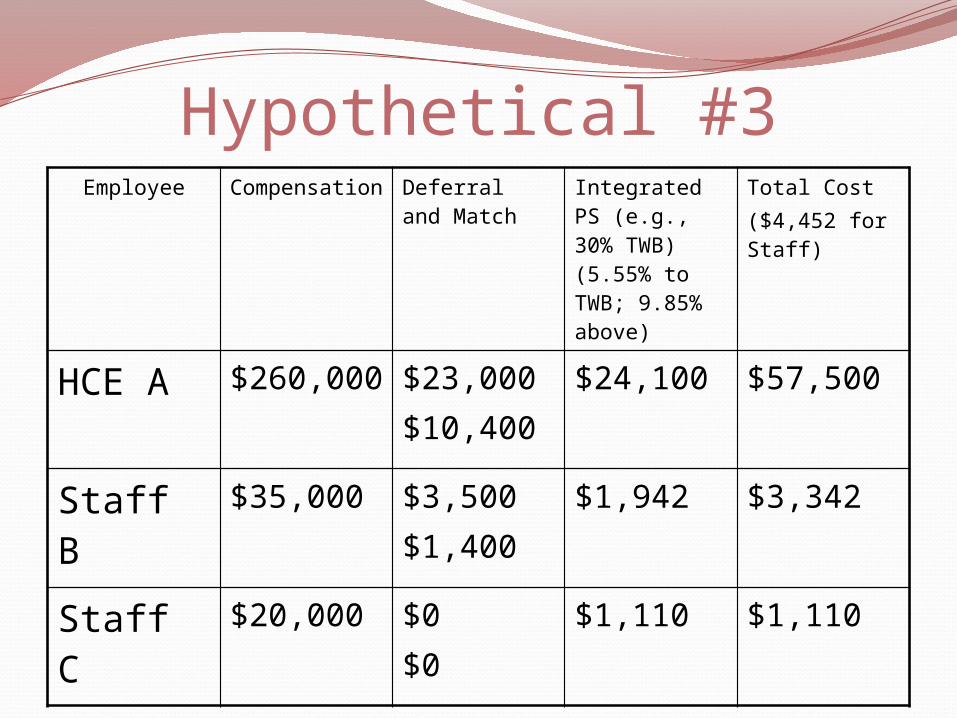

Hypothetical #3Employee Compensation Deferral and

MatchIntegrated PS (e.g., 30% TWB) (5.55% to TWB; 9.85% above)

Total Cost($4,452 for Staff)

HCE A $260,000 $23,000$10,400

$24,100 $57,500

Staff B $35,000 $3,500$1,400

$1,942 $3,342

Staff C $20,000 $0$0

$1,110 $1,110

NEW COMPARABILITY PROFIT SHARING CONTRIBUTIONS

An alternative to traditional pro rata or integrated profit sharing contribution allocations.

Provides an opportunity to maximize contributions if the HCEs are older, while minimizing allocations to younger staff.

Provides flexibility, for example:All HCEs do not have to receive maximum

contributions.Some rank-and-file employees can receive higher

percentage contributions than others.

What is the theory behind allowing higher contribution rates for older HCEs?For an older plan participant, the contributions will be

held and invested for a shorter time until retirement, therefore, more is needed for the contribution to be equivalent to that which is made for a younger plan participant.

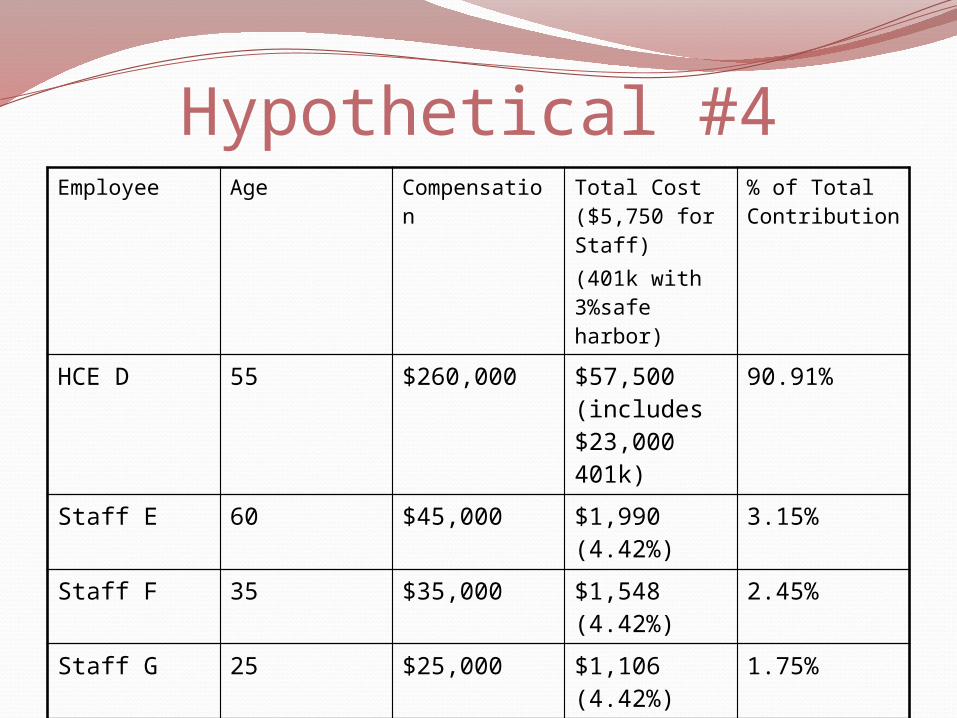

Hypothetical #4Employee Age Compensation Total Cost

($5,750 for Staff)(401k with 3%safe harbor)

% of Total Contribution

HCE D 55 $260,000 $57,500 (includes $23,000 401k)

90.91%

Staff E 60 $45,000 $1,990 (4.42%)

3.15%

Staff F 35 $35,000 $1,548 (4.42%)

2.45%

Staff G 25 $25,000 $1,106 (4.42%)

1.75%

Staff H 25 $25,000 $1,106 (4.42%)

1.75%

CASH BALANCE DEFINED BENEFIT PLANGreat opportunity for professionals (and others).Depending on the demographics of the group,

includingages,compensation levels, andnumbers of

owners/professionals, other HCEs, and other staff,

it may be possible to design a cash balance plan that provides for very high levels of "contributions" to the owners’/professionals’ cash balance accounts.

A cash balance plan may be designed so that the annual funding "cost" – the contributions – for an owner’s/professional’s benefits earned under the plan far exceeds the $53,000 (or $59,000) annual contribution limit for a defined contribution plan.

In some cases, it is possible to participate in a defined contribution plan up to the maximum $53,000 (or $59,000) level and participate in a cash balance plan at the maximum benefit level.

Like the new comparability plan design, it may be possible to have different levels of "contributions" for different participants, including:Older professionals receiving much greater

contributions than younger staff; orSelected professionals benefitting much more

significantly than the other professionals and the rank-and-file employees.

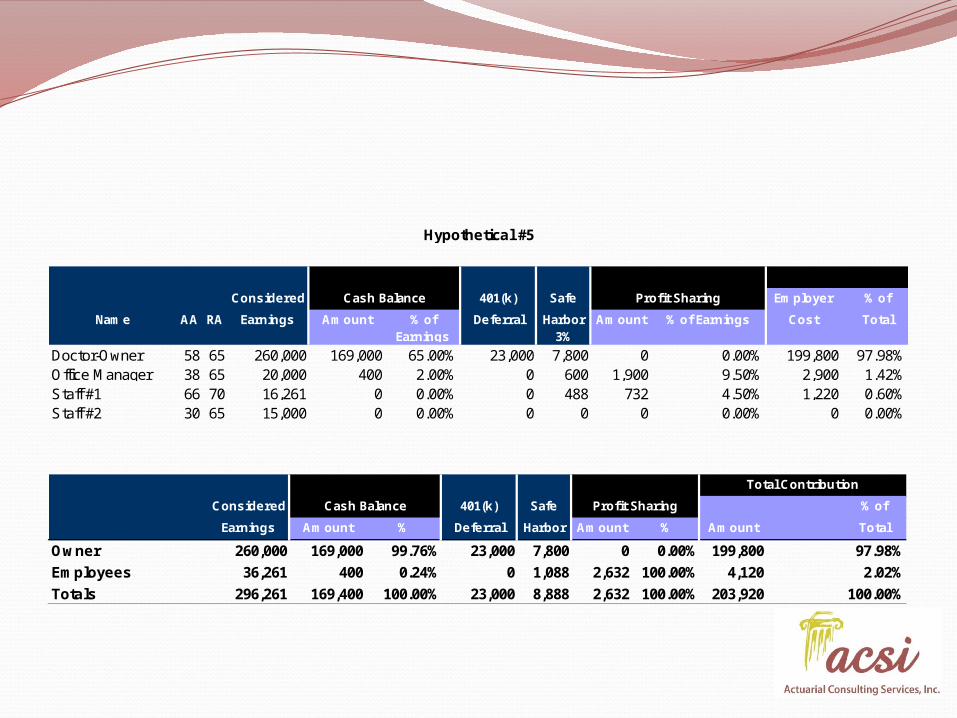

Hypothetical #5A One-Owner Business with 3 employees plus

the Owner.The Owner maintains both a Cash Balance

DB Plan and a 401(k) New Comparability Profit Sharing Plan.

One of the employees works less than 1,000 hours each year.

AA

58386630

Amount

199,800

4,120

203,920

Hypothetical #5

Considered Cash Balance 401(k) Safe Profit Sharing Employer % of

Name RA Earnings Amount % of Earnings

Deferral

65.00% 23,000 7,800 0

Harbor 3%

Amount

0.00% 199,800 97.98%

Total% of Earnings Cost

1,900 9.50% 2,900Office Manager 65 20,000 400 2.00% 0 1.42%

65 15,000 0 0.00% 0 0 0

600

Total Contribution

0.00% 0 0.00%

Considered Cash Balance 401(k) Safe Profit Sharing % of

Earnings Amount % Deferral

23,000 7,800 0 0.00%

Harbor Amount %

Employees 36,261 400 0.24% 0

Owner 260,000 169,000 99.76%

1,088 2,632 100.00%

0.60%

97.98%

Total

2.02%

Totals 296,261 169,400 100.00% 23,000 8,888 2,632 100.00% 100.00%

Staff #20.00% 0 488 732 4.50% 1,220

Doctor-Owner

Staff #1 70 16,261 0

65 260,000 169,000

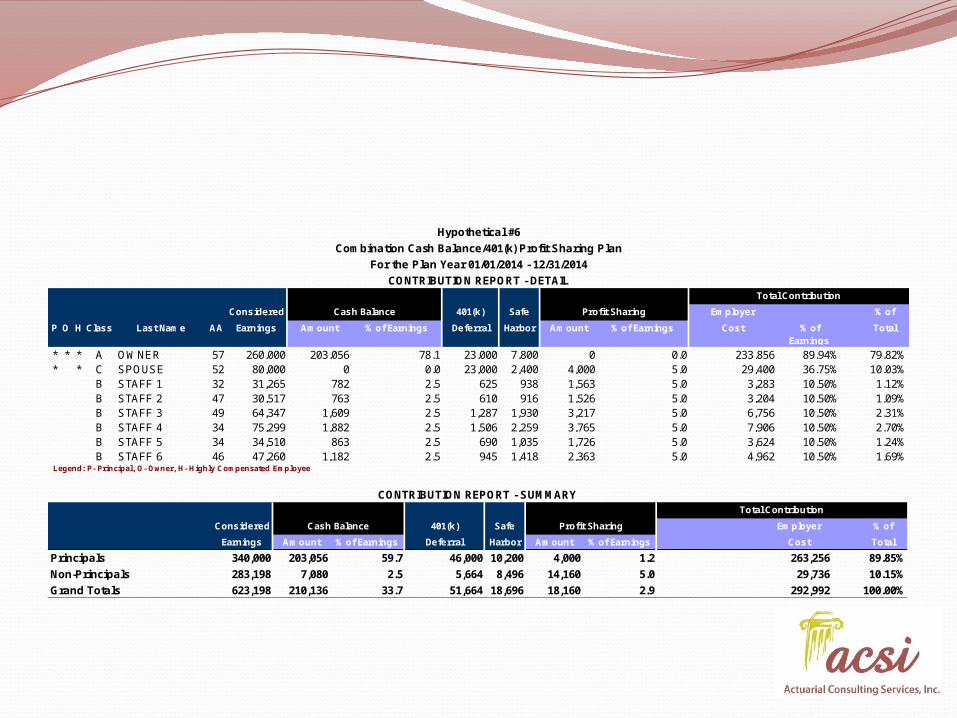

Hypothetical #6A One-Owner Business with 6 employees plus

the Owner and his spouse.The Owner maintains both a Cash Balance

DB Plan and a 401(k) New Comparability Profit Sharing Plan.

P O H Class

* * * A* * C B B B B B B

292,992 100.00%

Employer

Cost

233,85629,4003,2833,204

10.15%

Grand Totals 623,198 210,136 33.7 51,664 18,696 18,160 2.9

14,160 5.0 29,736Non-Principals 283,198 7,080 2.5 5,664 8,496

1.2 263,256 89.85%

Cost Total

Principals 340,000 203,056 59.7 46,000 10,200 4,000

% of

Earnings Amount % of Earnings Deferral Harbor Amount % of Earnings

Total Contribution

Considered Cash Balance 401(k) Safe Profit Sharing Employer

1.69% Legend: P- Principal, O- Owner, H- Highly Compensated Employee

CONTRIBUTION REPORT - SUMMARY

1,418 2,363 5.0 10.50%4,962

Last Name

OWNER SPOUSE STAFF 1 STAFF 2

46 47,260 1,182 2.5 945STAFF 6 5.034,510 863 2.5 690 1.24%3,624

STAFF 3 STAFF 4 STAFF 5

2.70%34

6,756

1,035 1,7262,259 3,765 5.0 10.50%

10.50%7,90634 75,299 1,882 2.5 1,506

5.01,930 3,217 10.50% 2.31%1.09%

49 64,347 1,609 2.5 1,287916 1,526 5.0 10.50%47 30,517 763 2.5 610

5.0 10.50% 1.12%10.03%52 80,000 0 0.0 23,000

32 31,265 782 2.5 625

79.82%

Total

1,5632,400 4,000 5.0 36.75%

938

57 260,000 203,056 78.1 23,000 7,800 0

Harbor Amount % of Earnings % of Earnings

0.0 89.94%

% of

AA Earnings Amount % of Earnings Deferral

Total Contribution

Considered Cash Balance 401(k) Safe Profit Sharing

Hypothetical #6

Combination Cash Balance/401(k) Profit Sharing Plan

For the Plan Year 01/01/2014 - 12/31/2014

CONTRIBUTION REPORT - DETAIL

Actuarial Consulting Services, Inc., 200 John James Audubon Parkway, Suite 100, Amherst, NY 14228, (716) 691-2181 ext. 103Mark E. Brand, Esq. ([email protected])