law - epgp.inflibnet.ac.in

TRANSCRIPT

LAW

CORPORATE LAW Raising of capital by companies by issue of securities

Q1: E-TEXT Module ID 7: Raising of capital by companies by issue of securities

Module Overview:“Capital in many cases is the life-blood of a concern, and it is always a great misfortune where the development of a business is arrested or restricted by want of capital”i. The Module on ‘Raising of capital by companies by issue of securities’ introduces students to the methods in which a public company can raise public finance through shares and the procedure which has to be complied with for raising such funds for meeting its business requirements of funds. Besides this, it will also be discussed how a private can raise capital? Principles of issue of shares at par, at discount and at premiums will also be discussed. Acceptance of deposits by companies, procedure for share allotment, forfeiture of shares, and remedies available to shareholders against misrepresentations in offer documents will be discussed to provide full knowledge of the topic to students. Subject Name: Law Paper Name: Corporate Law Module ID: 7 Pre-requisites: Need of companies to raise finance for funding business activities Objectives:

Keywords:issue of shares,prospectus, initial public offer (IPO), further public offer (FPO), rights issue, acceptance of deposits by companies, share allotment, forfeiture of shares, Learning outcomes:

To know different methods available for a company for the purposes of raising funds To know what documents are required to be made by a company for raising capitalTo understand how and why a company issues shares at par, at discount or at premiumsTo understand the procedure of share allotment

Introduction: The company is the only medium of organizing business which is given the privilege of raising capital by public subscriptions either by way of shares or debenturesii. Therefore, a company has to take a decision whether it wants to raise capital through shares or wants to meet its need of funds through borrowings in the form of debentures or other debt securities. In view of corporate scams especially the ongoing Sahara case, it is very important to know about the company, its future prosperity, why it is raising money, where and how this money will be utilized and what is the financial viability of returns, what will be rights and liabilities as a shareholder or creditor of the company. This information is necessary for every investor who wants to invest money in companies for the purposes of making returns on his investment whether investment is in the form of shares or debentures. It has to be decided by a company whether to raise share capital or to borrow money after analyzing how much amount it requires, whether loan is easily available or share subscription is more feasible, interest rates, dividend rates, how much and what type of regulatory compliance is required etc. In this module, provisions of the Companies Act, 2013 for raising capital by issue of shares by both public and private companies with the prescribed procedure will be discussed. It is also necessary to know here that the Securities and Exchange Board of India Act, 1992 (SEBI) and Securities (Contracts) Regulation Act, 1956 (SCRA) also play an important role in raising of capital by companies in India. All public companies which want to raise capital through public offer have to list their securities under the provisions of SCRA and follow SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009 and SEBI (Issue and Listing of Debt Securities) Regulations, 2008. These regulations are made by Securities and Exchange Board of India which was established under the SEBI Act, 1992 for promoting the development and regulation of securities market in India as well as protecting interests of investors in securities. It regulates collective investment schemes, mutual funds; fraudulent and unfair trade practices in securities, insider trading, take- over of companies and conducts enquiries and audits of stock exchanges etc. It regulates the working of stock brokers, sub-brokers, share transfer agents, bankers to an issue, underwriters, portfolio managers, investment advisors etc. SEBI has power of investigation and give directions for matters relating to securities. Recently, Securities Laws (Amendment) Act, 2014 has given wide powers to SEBI.

Understanding the availability of different methods for companies for the purposes of raising capital through issue of securities and acceptance of deposits. Knowledge about share allotment, its procedure and types

Distinction in procedure for raising of capital by public and private companies Different documents to be prepared by companies for raising capital and liability of companies’ directors for giving misrepresentations in the documents

First of all, let us understand the meaning of ‘securities’. The term ‘securities’ is defined by s. 2(h) of the Securities (Contracts) Regulation Act, 1956. Same definition is adopted by the Companies Act, 2013 under s. 2(81). ‘Securities’ include: (i) shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate; (ia) derivative; (ib) units or any other instrument issued by any collective investment scheme to the investors in such schemes; (ic)security receipt as defined in clause (zg) of section 2 of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002; (id) units or any other such instrument issued to the investors under any mutual fund scheme; (ie) any certificate or instrument issued to investors by a special purpose distinct entity which possess any debt or receivable including a mortgage debt assigned to it. The certificate or instrument issued acknowledges beneficial interest of the investor in debt or receivable or mortgage debt. (ii) Government securities; (iia) such other instruments as may be declared by the Central Government to be securities; and (iii) rights or interest in securities [S. 2(h), Securities (Contracts) Regulation Act, 1956] Different methods available for a company for the purposes of raising funds

Public offer: When a public company issues securities to the public for subscription, it is known as public offer. Public offer may be initial public offer IPO) or further public offer (FPO). When an unlisted issuer issues securities to the public, it is known as initial public offer whereas when a listed issuer issues securities to the public, it is further pubic offer i.e. further issue of capital by a company. Public offer also includes offer for sale (OFS) by existing shareholders of the company. Public offer has to be through issue of a prospectus. Every public offer by a public company should be in dematerialized form in compliance with the Depositories Act, 1996. According to s. 23 of the Companies Act, 2013(CA, 2013), a public company may issue securities as under: i. issue of securities to public through prospectus; or ii. issue of securities through private placement; or iii. through a rights issue or a bonus issue after complying with the provisions of the Act. If a company is listed or wants to list its securities, it will have to comply with Securities and Exchange Board of India Act, 1992 with its Rules and Regulations. Private Placement:According to s. 23 of the CA, 2013, a private company may issue securities as under: i. private company may issue securities by way of rights issue or bonus issue; or ii. through private placement

Private placement means any offer of securities or invitation to subscribe to securities to a select group f persons by a company. S. 42, CA, 2013 deals with offer of securities on private placement which can be made through issue of private placement offer letter. Such an offer for securities or invitation to subscribe can be made to such persons not exceeding fifty in a financial year. This does not include offer to qualified institutional buyers and employees of the company receive securities under employees’ stock options.

Rights Issue: Rights issue means an offer of specified securities by a listed issuer to the shareholders of the issuer as on the record date fixed for the said purpose under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009. Every equity shareholder of a company has a right to be offered shares when the company goes for further issue of capital. Such right falls under pre-emptive rights of existing shareholders of any company having a share capital and is protected by s. 62 of the Companies Act, 2013. Issue of bonus shares: A bonus share is issued when a company capitalizes its profits by transferring an amount equal to the face value of the share from its reserves to the nominal capitaliii. Prospectus: A public company can issue securities to public through prospectus. According to s. 2(70), CA, 2013, ‘prospectus’ means any document described or issued as a prospectus and includes a red-herring prospectus, shelf prospectus or any notice, circular, advertisement or other document inviting offers from the public for the subscription or purchase of any securities of a body corporate. Every prospectus has to include the matters prescribed by s. 26, 2013. It is required to include information about capital structureof the company, main objects of public offer, terms of present issue, main objects and present business of the company and its location, schedule and implementation of the project, names, addresses of registered office of the company, its company secretary, Chief Financial Officer, auditors, legal advisors, underwriters, bankers, trustees etc., dates of opening and closing of issues, declaration about issue of allotment letters, refunds, statement of Board of directors for the separate bank account for depositing money collected for the issue and disclosure of money utilized or not utilized out of the previous issue, details about underwriting of the issue, consent of directors, auditors, bankers and experts’ to the issue, authority for the issue and resolution passed. Prospectus is also required to include particulars relating to management perception of risk factors specific for the project, gestation period, and extent of progress, deadline for the project, any litigation or legal action pending against the promoters of the company during the last five years. Details

i. private company may issue securities by way of rights issue or bonus issue; or ii. through private placement

of minimum subscription, premium payable, issue of shares otherwise than on cash, details of directors, their appointment, remuneration and interest in the company. The company also has to disclose about the sources of promoter’s contribution to the issue. The Prospectus has to set out reports for financial information namely, auditors’ report, reports on profits and losses of the company for each of the financial year preceding the year of issue of prospectus including reports of its subsidiaries, report of auditors’ on profit and losses of the business of the company for each of such five preceding years and assets and liabilities of its business on the last date to which accounts were made up. This date should not be more than 180 days before the issue of prospectus. Reports about the business or transaction to which proceeds of the issue will be applied should also be given irrespective of the fact whether proceeds will be directly or indirectly applied. At the end, a declaration about compliance of the Act and statement that nothing in prospectus is contrary to the provisions of the CA, 2013, SCRA, 1956 and SEBI Act, 1992 with its rules and regulations. The above stated requirements do not apply to the following: i. when the company makes an issue of prospectus or form of application to existing members or debenture holders of the company for shares or debentures irrespective of the right of applicant to renounce shares or not in favour of any other person under s. 63 (1) (a) (ii); or ii. when the company issues a prospectus or form of application relating to shares or debentures which are uniform in all respects to shares or debentures previously issued by the company and quoted or dealt in recognized stock exchange for the time being. A copy of the prospectus with signatures of all persons named as directors or proposed directors in the prospectus should be submitted with the Registrar before issue of it. It should be issued within ninety days of registration with the Registrar. Any variation in contracts or objects in prospectus are subject to approval of or authority given in the general meeting by the company by passing a special resolution.

Deemed prospectus: Any document containing offer for sale of securities by the company to the public is deemed to be prospectus for the purposes of the Act. All relevant sections

i. when the company makes an issue of prospectus or form of application to existing members or debenture holders of the company for shares or debentures irrespective of the right of applicant to renounce shares or not in favour of any other person under s. 63 (1) (a) (ii); orii. when the company issues a prospectus or form of application relating to shares or debentures which are uniform in all respects to shares or debentures previously issued by the company and quoted or dealt in recognized stock exchange for the time being.

relating to matters to be contained in prospectus, liability for misstatements or omissions in prospectus are applicable to deemed prospectus also. Shelf Prospectus: Shelf prospectus can be filled by classes of companies allowed by SEBI. Such companies may at the stage of first of offer of securities included in the prospectus file a shelf prospectus with the Registrar. Validity of shelf prospectus can be no more than one year. During this one year, company may give second or third offer of shares without there being any need to file again a prospectus. However, the company before every subsequent offer will have to file an information memorandum relating to financial position of the company, all changes that occurred during this time period etc. Red-herring prospectus: It means a prospectus which does not include full particulars of the quantum or price of securities included in the issue. It can be filed with the Registrar at least three days prior to the opening of the subscription list and the offer. It contains same obligations as a regular prospectus and all variations in it and a prospectus should be highlighted as variations in the prospectus. Abridged prospectus: it means a memorandum containing salient features of a prospectus as are specified by SEBI in this behalf. No application form for purchase of securities of the company can be issued unless it is accompanied by abridged prospectus.

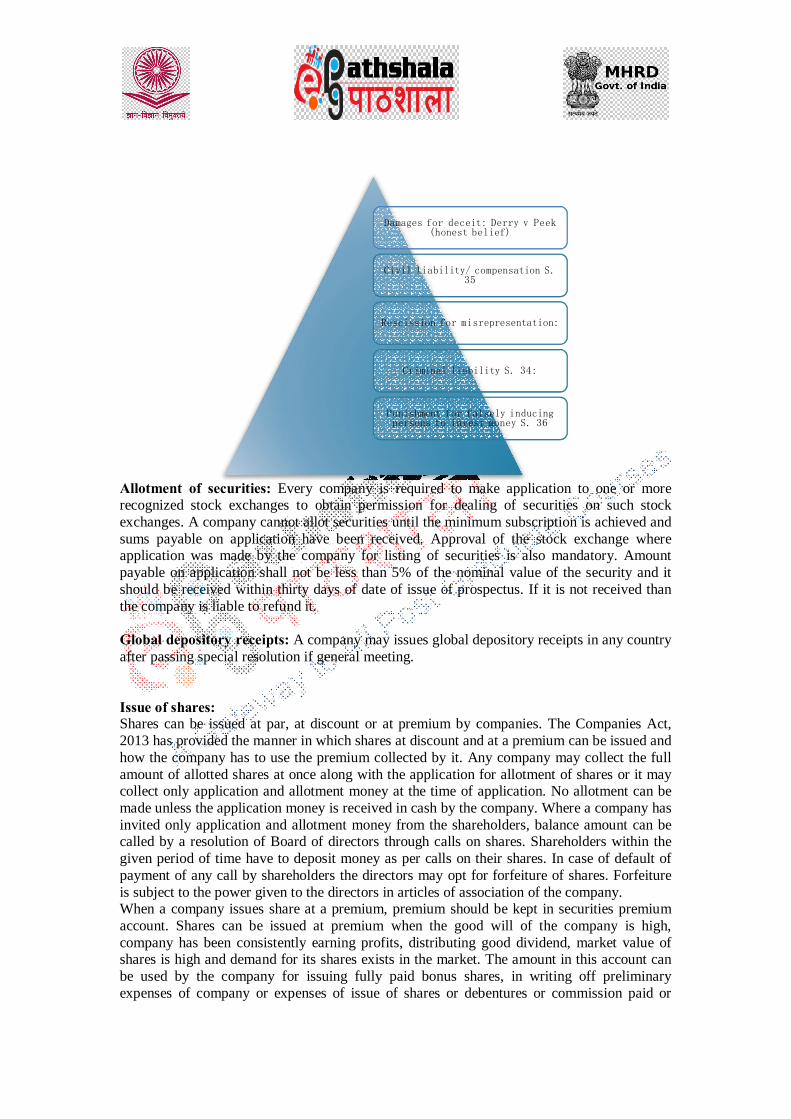

Liability for misstatements in prospectus: S. 34, CA, 2013 provides for criminal liability for untrue or misleading statements and for inclusion or omission of any matter which is likely to mislead. Every person authorizing issue of such prospectus is held liable under s. 447 for imprisonment for a term which shall be not less than six months but which may extend to ten years and shall also be liable to fine which should not be less than the amount involved up to three time that amount. Defences of immateriality of such statements or omission, reasonable belief about truthfulness of the statement and necessity of inclusion or omission are available. S. 35 provides for civil liability for misstatements. S. 36 provides for punishments for falsely inducing persons to invest money.

Different kinds of

prospectus:

Deemed ProspectusShelf Prospectus

Red-Herring Prospectus

Abridged Prospectus

Allotment of securities: Every company is required to make application to one or more recognized stock exchanges to obtain permission for dealing of securities on such stock exchanges. A company cannot allot securities until the minimum subscription is achieved and sums payable on application have been received. Approval of the stock exchange where application was made by the company for listing of securities is also mandatory. Amount payable on application shall not be less than 5% of the nominal value of the security and it should be received within thirty days of date of issue of prospectus. If it is not received than the company is liable to refund it. Global depository receipts: A company may issues global depository receipts in any country after passing special resolution if general meeting. Issue of shares: Shares can be issued at par, at discount or at premium by companies. The Companies Act, 2013 has provided the manner in which shares at discount and at a premium can be issued and how the company has to use the premium collected by it. Any company may collect the full amount of allotted shares at once along with the application for allotment of shares or it may collect only application and allotment money at the time of application. No allotment can be made unless the application money is received in cash by the company. Where a company has invited only application and allotment money from the shareholders, balance amount can be called by a resolution of Board of directors through calls on shares. Shareholders within the given period of time have to deposit money as per calls on their shares. In case of default of payment of any call by shareholders the directors may opt for forfeiture of shares. Forfeiture is subject to the power given to the directors in articles of association of the company. When a company issues share at a premium, premium should be kept in securities premium account. Shares can be issued at premium when the good will of the company is high, company has been consistently earning profits, distributing good dividend, market value of shares is high and demand for its shares exists in the market. The amount in this account can be used by the company for issuing fully paid bonus shares, in writing off preliminary expenses of company or expenses of issue of shares or debentures or commission paid or

Damages for deceit: Derry v Peek (honest belief)

Civil liability/ compensation S. 35

Rescission for misrepresentation:

Criminal liability S. 34:

Punishment for falsely inducing persons to invest money S. 36

discount allowed on them, in providing premium payable on redemption of references shares or debentures of the company or for the purchase of its own shares by the company. A company can issue shares at a discount only in accordance with s. 54, CA, 2013 for issuing sweat equity shares. A company may issue sweat shares of the class which are already issued. Holders of such shares are ranked paripassu with other equity shareholders of the company and they are subject to same rights, limitations, restrictions and provisions of the Act. Acceptance of deposits by companies: Under s. 73, CA, 2013, a company, not being a banking or non-banking financial company, may after passing a resolution in this behalf may accept deposits of money from its members. Acceptance of deposits by a company is subject to terms and conditions including provision of security and payment of interest etc. A circular giving statement on financial health of the company, credit rating, total numbers of existing depositors and the amount due on them has to be circulated by the company. The company should maintain a deposit repayment reserve account for the purposes of repayment and deposit not less than 15% of the amount of deposits maturing during a financial year and financial year next following in the account. Statistics about capital raised in 2013 in India: About fifty companies in different industries raised 27, 716 crores till Dec, 2013. Major industries were banking or financial institutions, cement and construction, engineering, entertainment, finance, information and technology and poweriv. Declaration of Bonus shares in 2013: About twelve companies offered bonus shares for the shareholders in 2013. Larsen and Toubro recommended one bonus share for two shares and Sun Pharma proposed one bonus share for each sharev. Offers Documents filed with SEBI in 2014: As of August, 2014, seven companies in the year had filed offer documents with SEBI. Under SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009, every issuer making desirous of making an IPO or Rights Issue of more than fifty lakhs or a FPO has to file a draft offer document with SEBI through its merchant banker. ShardaCropchem Ltd and Lavasa Corporation Ltd have filed draft offer document for IPO, IL&FS Engineering And Construction Company Limited, NCC Limited and Future Retail Ltd for rights issue whereas Adlabs Entertainment Limited and Monte Carlo Fashion Ltd have filed documents for fresh IPO with Offer for salevi. Summary: The module has dealt with the different methods of raising of funds by companies through issue of securities and acceptance of deposits. The difference between the methods adopted by a private company and a public company for raising finance has been briefed. Share allotment procedure, different types of prospectuses that can be issued by the companies depending upon their needs and liabilities of persons authorizing the issue of prospectus have also been added. End Notes: i Palmer’s Private Companies, forty second edition, 1961, p. 24 ii A. Singh, Company Law, fifteenth edition, 2007, p. 12, Eastern Book Company

iii Standard Chartered Bank v Custodian, (2000) 6 SCC 427 iv SEBI: Handbook of Statistics in Indian Securities Market, 2013, p. 19 http://www.sebi.gov.in/cms/sebi_data/attachdocs/1404362427338.pdf vNearly dozen companies announce bonus shares in one month by M Allirajan, TOI, June 20, 2013, http://timesofindia.indiatimes.com/business/india-business/Nearly-dozen-companies-announce-bonus-shares-in-one-month/articleshow/20672802.cms; accessed on Aug 7, 2014 vihttp://www.sebi.gov.in/sebiweb/home/list/3/14/8/0/Issues accessed on Aug 7, 2014