l-3: balance of payment crises - jvi · l-3: balance of payment crises irina bunda macroeconomic...

TRANSCRIPT

L-3: BALANCE OFPAYMENT CRISES

IRINA BUNDA

MACROECONOMIC POLICIES IN TIMES OF HIGHCAPITAL MOBILITY

VIENNA, MARCH 21–25, 2016

THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI) AND IS INTENDED FOR USE INJVI COURSES. ANY REUSE REQUIRES THE PERMISSION OF THE JVI.

OUTLINE

Currency/Balance of Payment Crises

IMF Advice on dealing with Capital Outflows

Cases of Recent BOP Crises and Adjustment

2

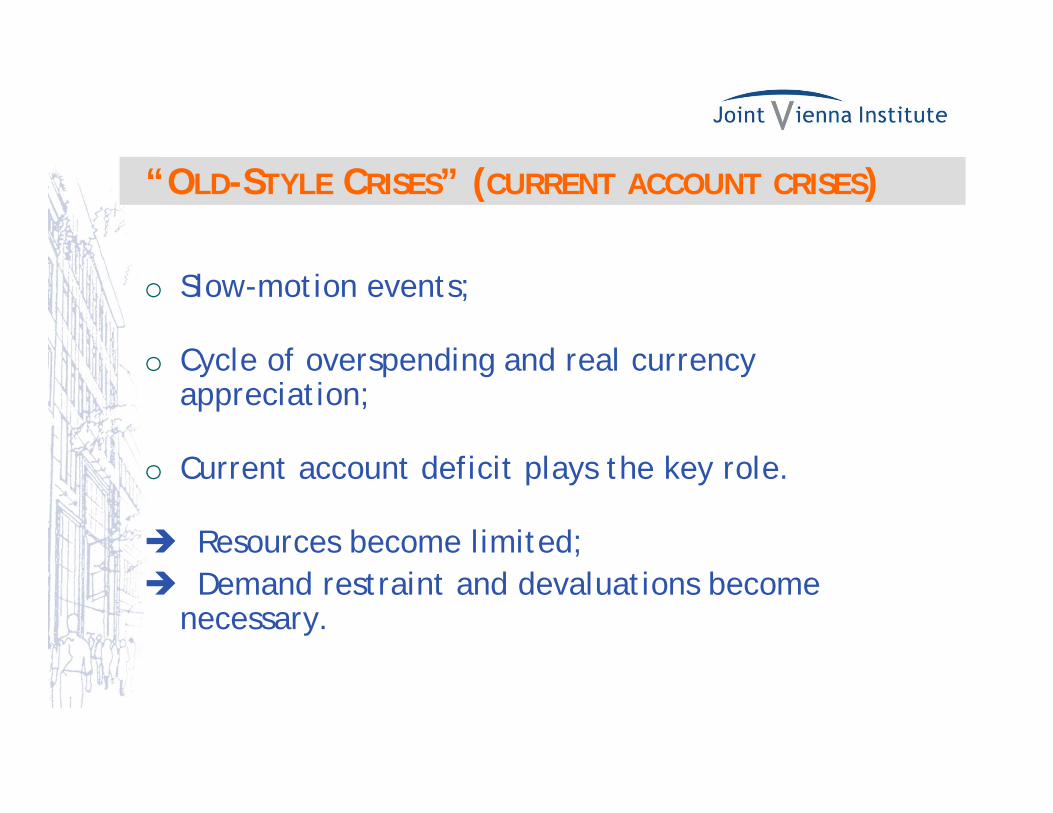

“OLD-STYLE CRISES” (CURRENT ACCOUNT CRISES)

o Slow-motion events;

o Cycle of overspending and real currency appreciation;

o Current account deficit plays the key role.

Resources become limited; Demand restraint and devaluations become

necessary.

“NEW-STYLE CRISES” (CAPITAL ACCOUNT CRISES)

o Fast-action crises,

o Doubts about o balance sheet strength of significant part of economy and o the exchange rate,

capital flow reversals.

Capital account plays the key role: Large capital inflows prior to the crisis; Substantial capital outflows during the crisis.

OLD-STYLE VS. NEW-STYLE CRISES

o Traditional analysis—examination of flow variables (such as current account, fiscal deficit);

o The balance sheet approach focuses on stock variables (types of debt, illiquid assets, etc.)

Important source of vulnerabilities: composition and size of liabilities and assets.

VULNERABILITIES AND TRIGGERS

For financial crises to occur there have to be:

o financial vulnerabilities

o trigger events

VULNERABILITIES AND TRIGGERS

o Financial markets can be quite forgiving of imprudent behavior and policies and balance sheet weaknesses;

o At other times, financial markets can react virulently and act preemptively.

o Underlying vulnerabilities can linger for years without triggering a crisis;

o Exact timing of crises difficult to predict.

o How financial market participants react is influenced by a wide range of factors.

VULNERABILITIES

Key factor:

o Composition and size of assets and liabilities of a country’s financial balance sheet.

Key balance sheet vulnerabilities:

o Maturity mismatches

o Currency mismatches

o Capital structure weaknesses

VULNERABILITIES VERSUS TRIGGERS

o Vulnerabilities are largely necessaryconditions for crises,

o but they are not necessarily sufficientconditions for crises.

o It usually takes a trigger event to make the vulnerabilities felt and ignite a crisis.

o At what level are vulnerabilities becoming problematic?

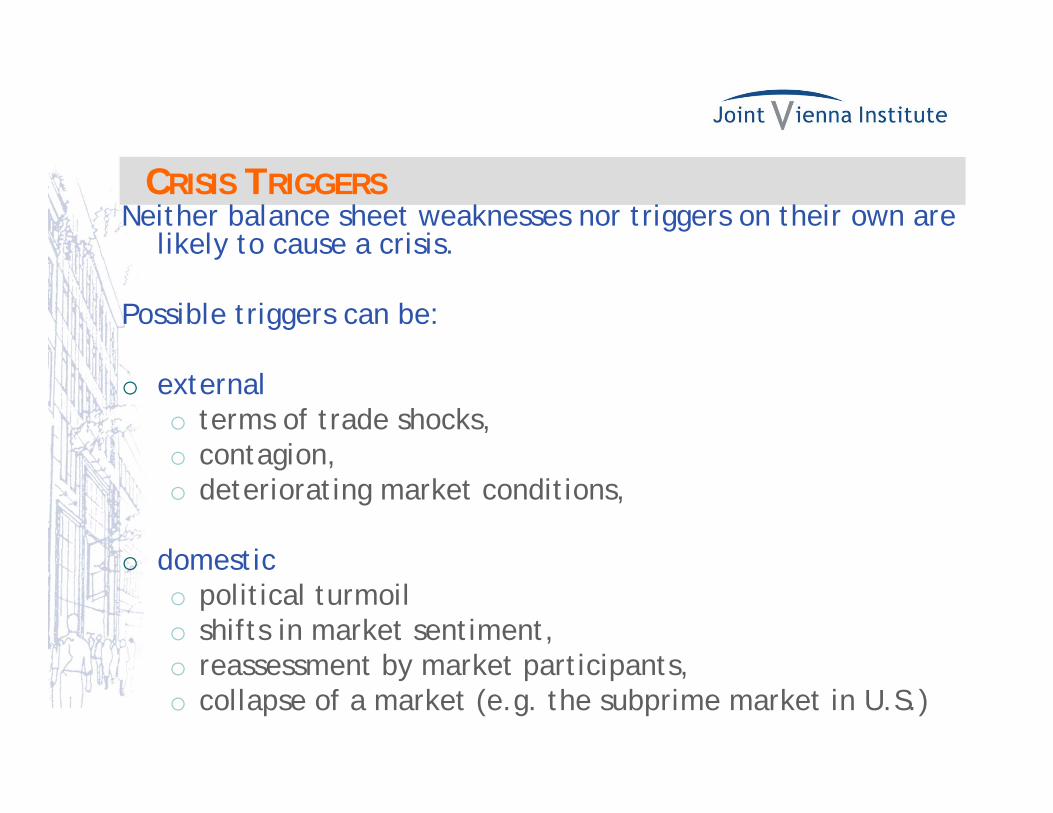

CRISIS TRIGGERSNeither balance sheet weaknesses nor triggers on their own are

likely to cause a crisis.

Possible triggers can be:

o externalo terms of trade shocks, o contagion, o deteriorating market conditions,

o domestico political turmoilo shifts in market sentiment,o reassessment by market participants,o collapse of a market (e.g. the subprime market in U.S.)

DEFINITION OF A CURRENCY/BOP CRISIS

11

o A currency crisis occurs when an attack on a country’s currency results in a sudden and rapid fall in the value of a currency (large devaluation or depreciation)

o Often triggers counter-measures:o Increase in interest rateso Run-down of reserves o Imposing capital controls

o A BOP crisis (or sudden stop) occurs when capital inflows reverse and/or international reserves drop sharply

CURRENCY/BOP CRISES

12

o Definitions of “currency crisis” and “BOP crisis” overlapping, and concepts often used interchangeably, but

o They do not necessarily occur together:o speculative attacks may fail to trigger

devaluations (e.g., successfully resisted by the central bank) & cause a BOP but not a currency crisis.

o Theoretical models explain joint currency and BOP crises

o Empirical studies usually define them as separate events

THEORIES OF CURRENCY/BOP CRISES

13

o A theoretical framework is important for:o identifying the causes of currency/BOP crises o providing a list of relevant variables that allows us

to develop an early warning systemo diagnosing a country’s vulnerabilityo devising appropriate economic policies

o Models: o First generation models: unsustainable fiscal policy

o Second generation models: self-fulfilling expectations (multiple equilibria)

o Third generation models: balance-sheet effects

FIRST GENERATION MODELS

14

o The collapse of a fixed exchange rate regime is caused by unsustainable fiscal policy in presence of high K mobility:o The government runs a persistent primary fiscal deficito Deficit is often financed by credit from the central banko At some point, a sudden, a sharp drop in international

reserves (speculative attack) occurs, and the fixed regime collapses

o Capital flows role is passive

o Without policy changes, collapse is inevitable (deterministic)

Causes of Currency/BOP crises:Ongoing fiscal deficits, rising debt levels, falling reserves

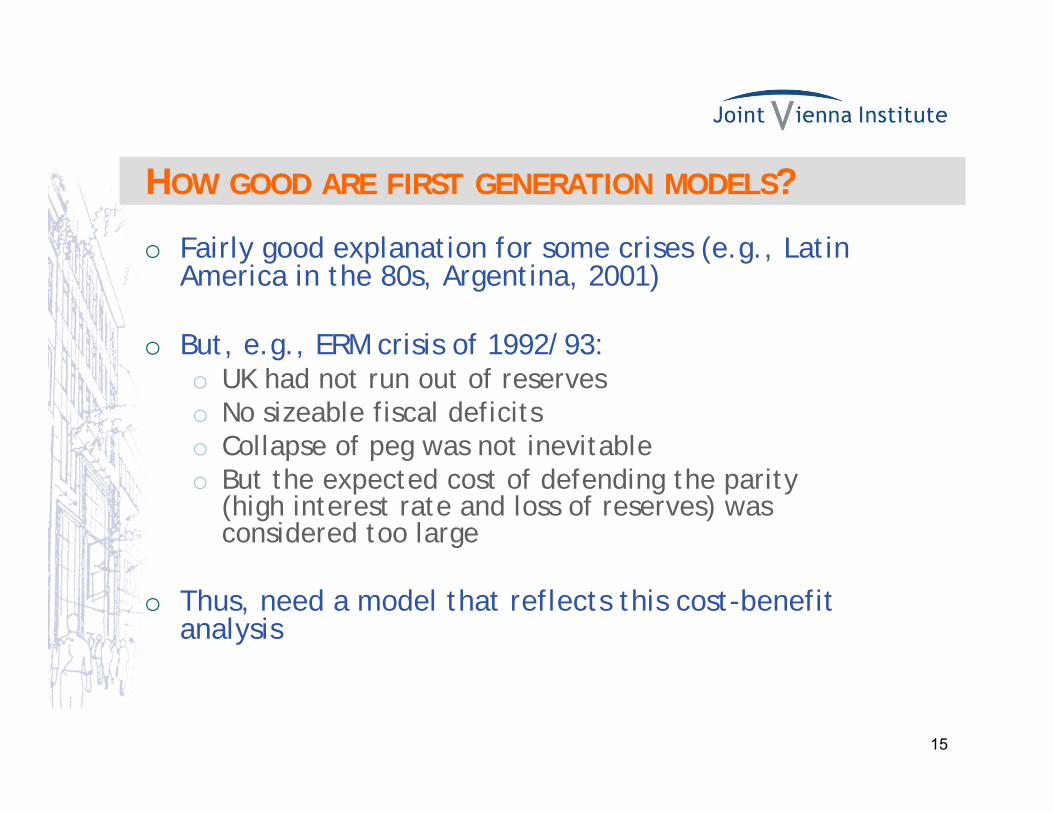

HOW GOOD ARE FIRST GENERATION MODELS?

15

o Fairly good explanation for some crises (e.g., Latin America in the 80s, Argentina, 2001)

o But, e.g., ERM crisis of 1992/93:o UK had not run out of reserveso No sizeable fiscal deficitso Collapse of peg was not inevitableo But the expected cost of defending the parity

(high interest rate and loss of reserves) was considered too large

o Thus, need a model that reflects this cost-benefit analysis

SECOND GENERATION MODELS

16

o Inspired, e.g., by the EMS 1992-93 crisiso References: Flood and Garber (1984) and Obstfeld (1986, 1994)

o Crises are expectations-driven and can occur even in the presence of sound fundamentals

o The government maximizes an explicit objective function comparing the (ex-ante) benefits and costs of a devaluation given multiple objectives, such aso Price stability, signaling markets to pursue a disciplined monetary

policy achieved through nominal anchor of a fixed exchange rate

o Limit debt service obligations, lower unemployment, inject liquidity into a troubled banking system achieved through monetary expansion (abandon fixed FX rate)

SECOND GENERATION MODELS, CONT’D

17

o Multiple equilibria: when agents expect a devaluation and higher inflation:

o Government needs to raise the policy rate, with negative impact on employment, activity, financial stability;

o no devaluation: cost in terms of output loss and unemployment

o Devaluation: cost in terms of reputation, inflation anchor, volatility

o Once the cost of maintaining the peg become higher than the costs of a devaluation --the government will devalue and validate agents’ expectations (crisis is self-fulfilling)

Causes of Currency/BOP crises:Private sector expectations and government trade-offs

SECOND GENERATION MODELS, END

18

o Government’s policy interacts with expectations

o The self-fulfilling crises do not imply that fundamentals do not matter (Bensaid and Jeanne, 1997). There is typically a range of strong fundamentals (where no attack takes place), intermediate (it depends), and weak fundamentals (crisis).

o But many currency crises are preceded by/coincide with financial sector problems o Kaminsky-Reinhart (1999): Banking crises often

precede currency/BOP criseso E.g., East Asia crisis 1997

THIRD GENERATION MODELS

19

o Stress the role of the financial sector and balance sheets in causing crises and propagating their effectso Inspired by Asian Crisis 1997-98o Moral-hazard-driven lending (Krugman, 1998)o Currency crises as the by-product of bank runs (Chang &

Velasco, 1998)o Currency and maturity mismatches (dollarized short-term

debts) in balance sheets, and the impacts of currency depreciation on balance sheets

Causes of Currency/BOP crises:Financial vulnerabilities, including in banking and

corporate sectors, and (implicit or explicit) government guarantees

THIRD GENERATION: Moral Hazard

20

Krugman (1998), Corsetti, Pesenti, Roubini (1998)o Weak financial institutions take too much risk

and have too large losses:o E.g., Connected lending

o Government guarantees and moral hazard driven lending provided a hidden subsidy to investment the anticipation of a bailout provides a strong incentive to take on more risk contingent liability for the government

THIRD GENERATION: Liquidity

21

o Bank runs: sudden shifts in confidenceo Banks hold long-term assets (loans) and short-term

liabilities (deposits).o This makes them vulnerable to liquidity risk: if each

depositor starts to worry that other depositors will withdraw their deposits, then a bank run could occur.

o Depositors may withdraw funds from banks and from the country currency depreciation pressures

o A country’s financial system is internationally illiquid if its potential short-term obligations in foreign currency exceed the amount of foreign currency it can have access to on short notice. investors may withdraw capital (and/or not rollover credit)

ANATOMY OF A BALANCE-SHEET CRISIS

22

Balance sheet mismatches: • Currency mismatch • Maturity mismatch• Capital structure mismatch

LINKS BETWEEN CURRENCY & BANKING CRISES

23

o Currency crises → Banking crises

o The central bank defends currency by increasing interest rates a slowdown in growth and deterioration of bank assets

o Currency devaluation leads to banking crisis if banks have large unhedged positions in foreign currency or if they have lent in foreign currency to corporations that produce non-tradable goods

LINKS BETWEEN CURRENCY & BANKING CRISES

24

o Banking crises → Currency crises

o If the central bank bails out financial institutions, its ability to defend the currency is eroded

o Bank runs lead to moving deposits abroad (capital flight), leading to a fall in reserves and currency crisis

LINKAGES ACROSS SECTORS

25

o Financial vulnerability can come from different sources given the inter-linkages across different sectors:

o Government → Financial Sector: Domestic financial institutions may be large holders of public debt

o Financial Sector → Government: Deposit insurance/bailout can imply a large fiscal contingent liability

BANKS-SOVEREIGN FEEDBACK LOOPS

SovereignDebt risk level:

Banks

Assets: Liabilities:Sovereigndebt

Loans to firms

Bank debtrisk

Equity risk

!

Real economyBailout probability 26

Source: World Economic Outlook (May 1998)

TWIN CRISES ARE COSTLY

27

o Has your country been faced with a twin (currency and banking) crisis recently? What was the sequence of events ? What was the real impact of the crisis ?

o Was the adjustment internal or external ?

o If not, is your country vulnerable to such a crisis ? Where do the main vulnerabilities stem from ?

o In the end, designate a group representative to summarize his/her country’s experience in front of the class.

BUZZ GROUP: ISSUES FOR DISCUSSION

29

Sudden Stops and Policy Responses

IMF Advice on dealing with Capital Outflows

Cases of Recent BOP crises and Adjustment

IMF POLICY FRAMEWORK FOR MANAGING CAPITALOUTFLOWS

o Outflows should primarily be managed using appropriate macro, structural, and financial sector policies.

o If large but no immediate threat of crisis: adjust macroeconomic and financial sector policieso Korea, Russia, and South Africa during 2009–11

o Use CFMs on inflows as a crisis prevention measure during inflow surges

o Take preemptive structural and macroprudentialmeasures to improve country’s resilience to crisis

30

IMF POLICY FRAMEWORK FOR MANAGING CAPITALOUTFLOWS, CONT’D

o Controls (CFM) on capital outflows can be considered in crisis or near crisis conditions to prevent the free fall of the exchange rate and the depletion of international reserves

o Argentina (2001–02), Iceland (2008), Ukraine (2008)

o CFM may be necessary when countries face domestic or external shocks that cannot be handled by macroeconomic adjustment or financial sector policies alone

o The effectiveness of CFMs on outflows can erode quickly

31

IMF POLICY FRAMEWORK FOR MANAGING CAPITALOUTFLOWS, CONT’D

o Outflow controls can be effective for longer periods if they are well designed and (re)enforced and part of a comprehensive macroeconomic policy adjustment package (see Iceland vs Argentina and Ukraine)

o CFMs on outflows adopted in a crisis should be temporary and lifted as soon as certain conditions are meto Macroeconomic stability (especially with respect to the

exchange rate and debt sustainability); o Confidence in domestic assets; o Access to international capital markets; o Financial system stability; and o Adequate reserves.

32

CAPITAL OUTFLOWS—UNDERLYING FACTORS ANDPOTENTIAL POLICY RESPONSES

If the source of the sudden-stop is

o External shock (e.g., t-o-t shock) o Let the exchange rate depreciate to its new

equilibrium level;o Defend the peg if the shock is temporary and reserves

sufficient.

o Inconsistent macroeconomic policieso Macroeconomic adjustment necessary; o Temporary CFMs on outflows could provide breathing

space for other policies to be implemented.

33

• Financial fragility (e.g., loss of confidence)• Step up prudential regulation and supervision,

improve deposit guarantee schemes, and provide liquidity support;

• Temporary CFMs on outflows can provide breathing space.

o Global conditions (e.g., increased risk aversion, tighter monetary conditions in advanced economies)o If significant outflows but seen as temporary:

adjust the macroeconomic policy mix (e.g., depreciation+ monetary tightening+ fiscal expansion).

34

CAPITAL OUTFLOWS—UNDERLYING FACTORS ANDPOTENTIAL POLICY RESPONSES, CONT’D

35

Sudden Stops and Policy Responses

IMF Advice on dealing with Capital Outflows

Cases of Recent BOP crises and Adjustment

COUNTRY CASES WITH SIGNIFICANT CAPITALOUTFLOWS AND POLICY RESPONSES

o Argentina 2001–02: o Corralito system to limit bank withdrawals;o Restrictions on transfers and loans in foreign currency;o External payments suspended;o Peso devalued by 40 percent (early 2002).

o Latvia, 2008-09; Iceland 2008;o Malaysia 1998 :

o Monetary tightening led to economic contraction; o Capital controls to isolate the offshore -onshore ringgit market;o Further measures: controls limiting offshore swap operations,

ban on short-selling, strict regulation on offshore operations, 12-month holding period for nonresidents to sell profits from Malaysian securities; approval requirement to invest abroad, etc.

36

o Russia 1998 o Capital controls (freezing the trading of short term treasury

bills, lengthening the maturity of domestic debt, practical restrictions on transfers abroad by nonresidents);

o Selective debt moratorium;o Stability achieved only when policies to tackle the underlying

causes were implemented: close fiscal imbalances, unification of the currency markets, bank restructuring.

o Russia, 2008o Turkey 2001:

o No capital controls;o Exchange rate allowed to float (50 percent depreciation); o Stabilization program backed by the IMF: prudent macro

policies, significant reforms in the financial sector and privatizations.

37

COUNTRY CASES WITH SIGNIFICANT CAPITALOUTFLOWS AND POLICY RESPONSES, CONT’D

o Ukraine 2008: o Regulatory measures and exchange controls to help

stem outflows and defend the exchange rate (e.g., restrictions on banking activities, ban on foreign exchange forward transactions, currency controls on foreign investments, etc.) with mixed results.

o Uruguay 2002: o No capital controls;o Peg abandoned (25 percent depreciation);o Five-day bank holiday, some banks were nationalized;o Re-profiling and swap of public debt.

38

COUNTRY CASES WITH SIGNIFICANT CAPITALOUTFLOWS AND POLICY RESPONSES

-39-

BUZZ GROUP: DEALING WITH CAPITAL OUTFLOWS

In small groups, discuss the following issue for about 15 minutes:

• Are capital controls on outflows the appropriate answer to a sudden stop in capital flows? If yes, under which circumstances ?

• Has your country experienced a sudden stop in capital flows in recent years? What were the main features of the adjustment ?

In the end designate a group representative who will report back on your group’s findings

CONCLUSION

o Manage capital outflows primarily with macroeconomic and financial sector policies.

o Use structural policies and macroprudential measures to increase the resilience of the financial, corporate, and household sectors to sudden stops; CFM to deal with surges in inflows;

o Can use CFMs on outflows: o In crisis or near crisis conditions; o To provide breathing space to fundamental policy adjustment

When deciding on CFMs:o Consider country-specific circumstances (e.g. administrative

capacity), preexisting degree of financial openness; o Should be temporary;o Bear in mind multilateral effects of CFMs on outflows.

40

o The best prevention is still to keep good macro fundamentals• Fiscal balance• Current account balance• Exchange rate alignment• Debt sustainability

o Countries should be particularly concerned about economic booms accompanied by• Rapid credit expansion• Loosening of lending standards• Large inflows of short term capital• Real exchange rate appreciations• Boom in asset prices (stock market, real estate)

POLICY IMPLICATIONS: PREVENTING FINANCIAL CRISES

-41-